Gold and Bitcoin Optimal Portfolio Research and Analysis Based on Machine-Learning Methods

Abstract

1. Introduction

- Based on the historical pricing data of gold and bitcoin, to establish a price fluctuation prediction model for both;

- Establishment of a model for effective evaluation of the portfolio strategies;

- Based on the investment portfolio model of the financial industry, this paper studies the relationship between bitcoin and gold, puts forward investment suggestions for maximizing benefits and conducts a sensitivity analysis of the scheme to put forward reasonable suggestions for improvement.

2. Assumptions and Justifications

3. Notations

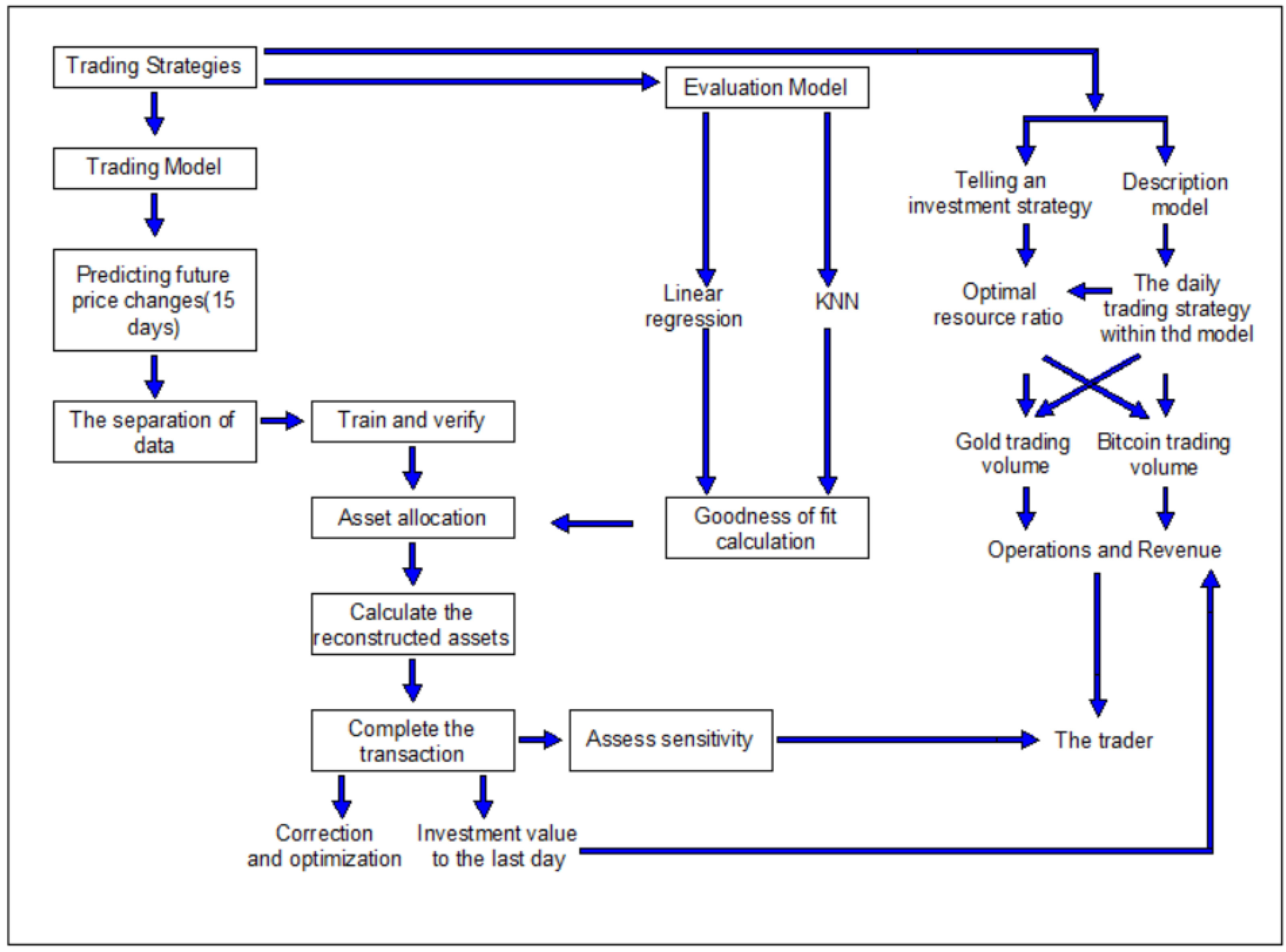

4. Model Preparation

5. Model I: Linear Regression Prediction Model

5.1. Data Preprocessing

5.2. Data Segmentation

5.3. Linear Regression Model (LRM)

5.3.1. Regression to the Problem

5.3.2. Linear Regression Model Description

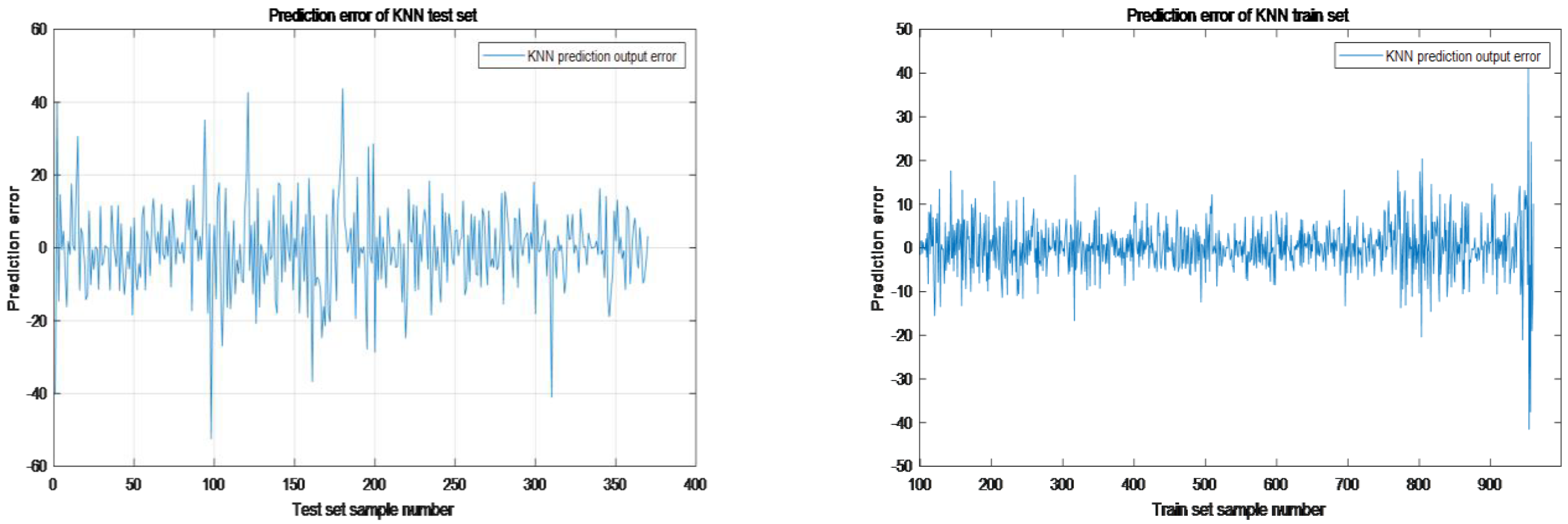

6. Model II: K-Nearest Neighbor Algorithm

6.1. KNN Algorithm Application

6.1.1. Selecting the Appropriate K-Value

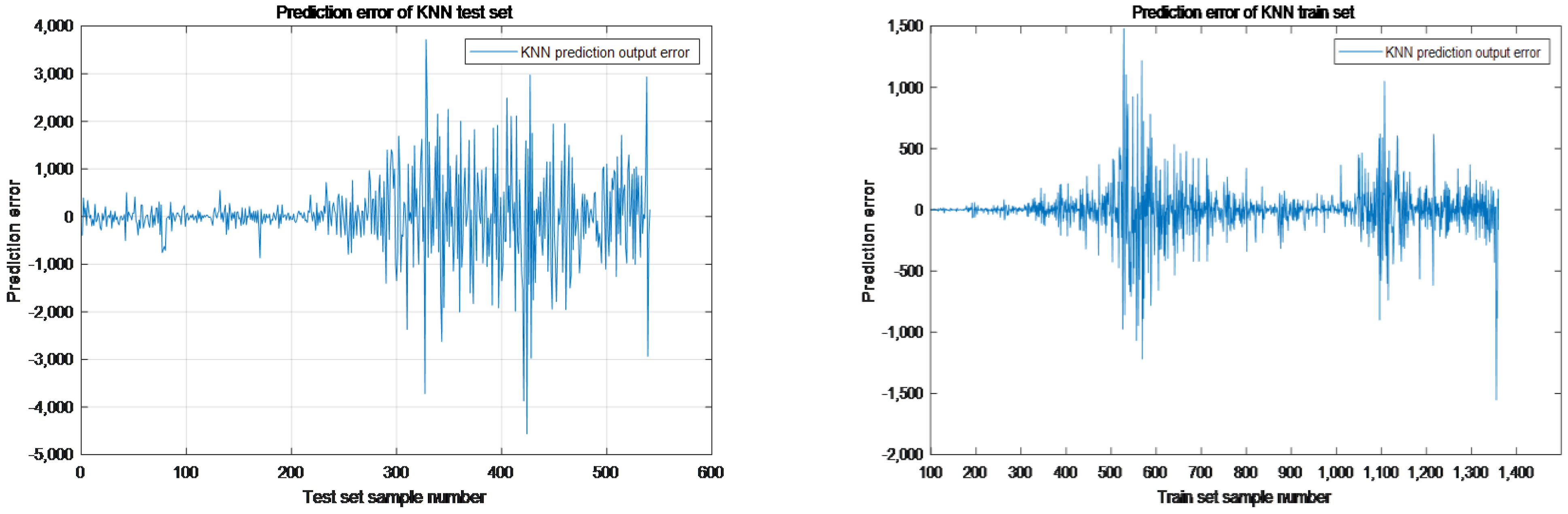

6.1.2. Obtaining the Results

6.2. Score Function to Determine Portfolio

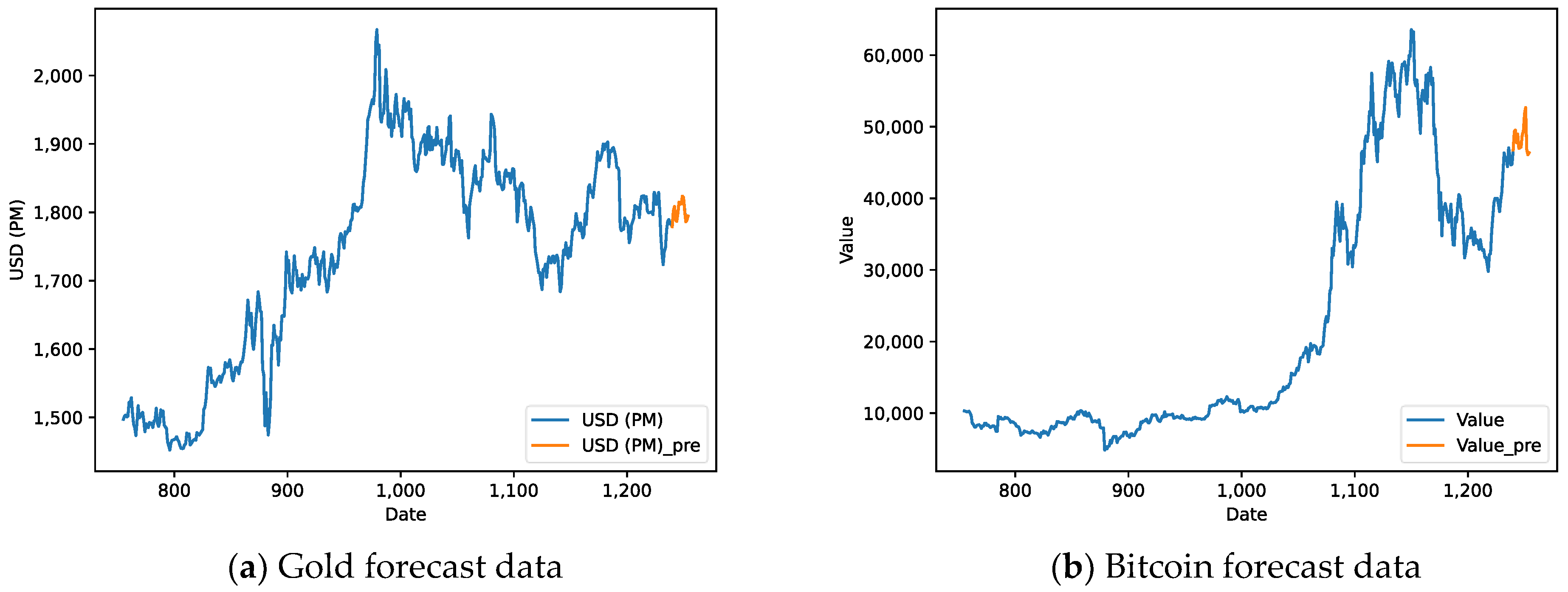

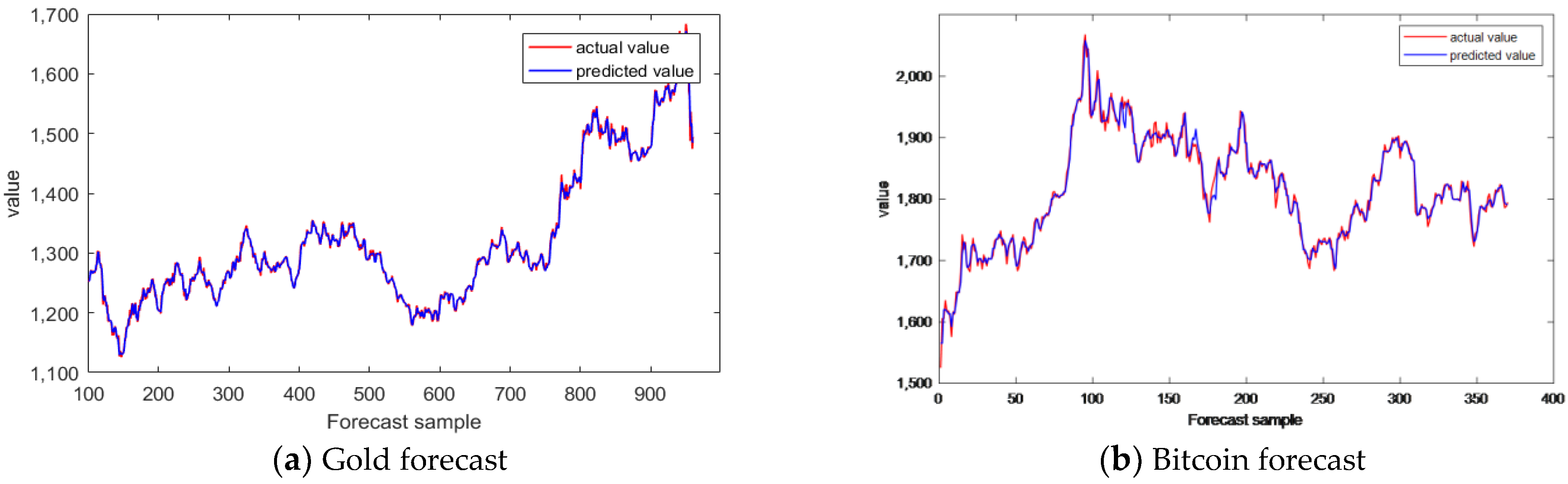

7. Results

7.1. Forecast Results

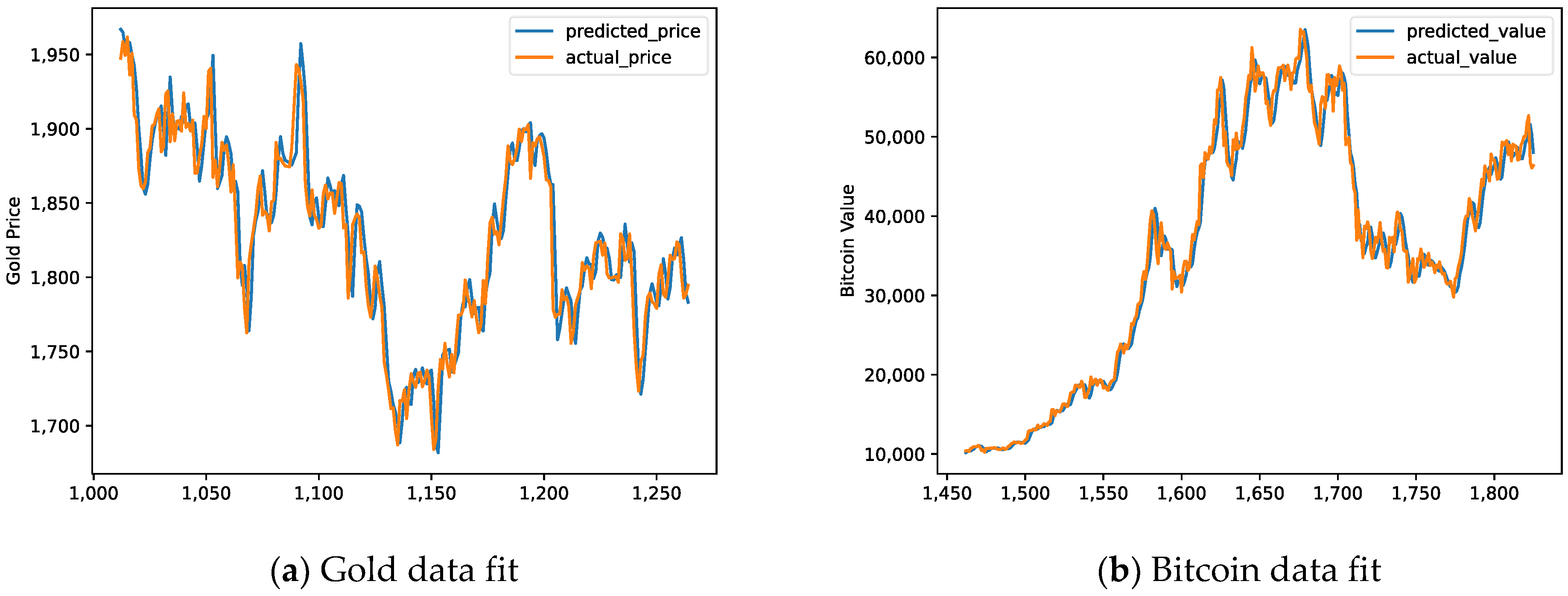

7.2. Test of Goodness of Fit

7.3. Price Change Weights Determine the Optimal Strategy

8. Discussion

9. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ciaian, P.; Rajcaniova, M.; Kancs, D.A. The economics of BitCoin price formation. Appl. Econ. 2016, 48, 1799–1815. [Google Scholar] [CrossRef]

- Munim, Z.H.; Shakil, M.H.; Alon, I. Next-day bitcoin price forecast. J. Risk Financ. Manag. 2019, 12, 103. [Google Scholar] [CrossRef]

- Hayes, A.S. Bitcoin price and its marginal cost of production: Support for a fundamental value. Appl. Econ. Lett. 2019, 26, 554–560. [Google Scholar] [CrossRef]

- Greaves, A.; Au, B. Using the bitcoin transaction graph to predict the price of bitcoin. No Data 2015, 8, 416–443. [Google Scholar]

- Velankar, S.; Valecha, S.; Maji, S. Bitcoin price prediction using machine learning. In Proceedings of the 2018 20th International Conference on Advanced Communication Technology (ICACT), Chuncheon, South Korea, 11–14 February 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 144–147. [Google Scholar]

- Chen, Z.; Li, C.; Sun, W. Bitcoin price prediction using machine learning: An approach to sample dimension engineering. J. Comput. Appl. Math. 2020, 365, 112395. [Google Scholar] [CrossRef]

- Atsalakis, G.S.; Atsalaki, I.G.; Pasiouras, F.; Zopounidis, C. Bitcoin price forecasting with neuro-fuzzy techniques. Eur. J. Oper. Res. 2019, 276, 770–780. [Google Scholar] [CrossRef]

- Lamothe-Fernández, P.; Alaminos, D.; Lamothe-López, P.; Fernández-Gámez, M.A. Deep learning methods for modeling bitcoin price. Mathematics 2020, 8, 1245. [Google Scholar] [CrossRef]

- Wu, C.H.; Lu, C.C.; Ma, Y.F.; Lu, R.S. A new forecasting framework for bitcoin price with LSTM. In Proceedings of the 2018 IEEE International Conference on Data Mining Workshops (ICDMW), Singapore, 17–20 November 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 168–175. [Google Scholar]

- Phaladisailoed, T.; Numnonda, T. Machine learning models comparison for bitcoin price prediction. In Proceedings of the 2018 10th International Conference on Information Technology and Electrical Engineering (ICITEE), Bali, Indonesia, 24–26 July 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 506–511. [Google Scholar]

- Sin, E.; Wang, L. Bitcoin price prediction using ensembles of neural networks. In Proceedings of the 2017 13th International Conference on Natural Computation, Fuzzy Systems and Knowledge Discovery (ICNC-FSKD), Guilin, China, 29–31 July 2017; IEEE: Piscataway, NJ, USA, 2017; pp. 666–671. [Google Scholar]

- Awoke, T.; Rout, M.; Mohanty, L.; Satapathy, S.C. Bitcoin Price Prediction and Analysis Using Deep Learning Models. In Communication Software and Networks; Springer: Singapore, 2021; pp. 631–640. [Google Scholar]

- Roy, S.; Nanjiba, S.; Chakrabarty, A. Bitcoin price forecasting using time series analysis. In Proceedings of the 2018 21st International Conference of Computer and Information Technology (ICCIT), Dhaka, Bangladesh, 22–24 December 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 1–5. [Google Scholar]

- Cretarola, A.; Figà-Talamanca, G.; Patacca, M. Market attention and Bitcoin price modeling: Theory, estimation and option pricing. Decis. Econ. Financ. 2020, 43, 187–228. [Google Scholar] [CrossRef]

- Nikou, M.; Mansourfar, G.; Bagherzadeh, J. Stock price prediction using DEEP learning algorithm and its comparison with machine learning algorithms. Intell. Syst. Account. Financ. Manag. 2019, 26, 164–174. [Google Scholar] [CrossRef]

- Lei, J.; Lin, Q. Analysis of gold and bitcoin price prediction based on LSTM model. Acad. J. Comput. Inf. Sci. 2022, 5, 95–100. [Google Scholar]

- Yu, J.; Shang, Y.; Li, X. Dependence and Risk Spillover among Hedging Assets: Evidence from Bitcoin, Gold, and USD. Discret. Dyn. Nat. Soc. 2021, 2021, 2010705. [Google Scholar] [CrossRef]

- Sun, Y.; Xie, S.; Li, N. Research on Gold and Bitcoin Price Prediction Model and Sensitivity Analysis. World Sci. Res. J. 2022, 8, 468–471. [Google Scholar]

- Zhou, Q.; Chen, Z.; Cai, Z.; Xia, Z. Prediction of the Best Portfolio for Bitcoin and Gold based on the ARIMA Model. Front. Bus. Econ. Manag. 2022, 4, 141–149. [Google Scholar] [CrossRef]

- Liu, F.; Peng, Y.; Chen, Z.; Shi, Y. Modeling of characteristics on artificial intelligence IQ test: A fuzzy cognitive map-based dynamic scenario analysis. Int. J. Comput. Commun. Control. 2020, 14, 653–669. [Google Scholar] [CrossRef]

- Klein, T.; Thu, H.P.; Walther, T. Bitcoin is not the New Gold—A comparison of volatility, correlation, and portfolio performance. Int. Rev. Financ. Anal. 2018, 59, 105–116. [Google Scholar] [CrossRef]

- Qiu, Q.; Maillart, L.; Prokopyev, O.; Cui, L. Optimal Condition-Based Mission Abort Decisions. IEEE Trans. Reliab. 2022. [Google Scholar] [CrossRef]

- Liu, X.; Masoud, N.; Zhu, Q.; Khojandi, A. A markov decision process framework to incorporate network-level data in motion planning for connected and automated vehicles. Transp. Res. Part C Emerg. Technol. 2022, 136, 103550. [Google Scholar] [CrossRef]

- Dyhrberg, A.H. Bitcoin, gold and the dollar–A GARCH volatility analysis. Financ. Res. Lett. 2016, 16, 85–92. [Google Scholar] [CrossRef]

- Ye, W.; Sun, L.; Miao, B. Dynamic Cointegration of Gold and Bitcoin based on Semi-parametric MIDAS fractional regression model. Syst. Sci. Math. 2020, 40, 1270–1285. [Google Scholar]

- Kang, Y.Z. Analysis on the trajectory characteristics and influencing factors of gold price fluctuation. Mod. Enterp. 2022, 9, 94–96. [Google Scholar]

- Zhang, D. Establishment, Evaluation and Improvement of Spot Gold Trading Strategy; Xinjiang University of Finance and Economics: Urumqi, China, 2015. [Google Scholar]

- Wang, Q.; Du, Z. Research on the difference between Bitcoin and gold hedging Function: Based on VAR-BEKK-GARCH model. Manag. Sci. 2022, 35, 134–146. [Google Scholar]

- Meng, T. Currency Trading Data in Network Characteristics Research; Beijing University of Posts and Telecommunications: Beijing, China, 2021. [Google Scholar]

- Available online: https://www.comap.com/contests (accessed on 1 October 2022).

- Available online: https://www.python.org/downloads/windows/ (accessed on 1 October 2022).

- Available online: https://ww2.mathworks.cn/products/matlab.html (accessed on 1 October 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Symbol | Description | Unit |

|---|---|---|

| PCT_change | Past price fluctuation | % |

| HL_PCT | Maximum price difference in the past | % |

| present_crash | Cash held after the transaction | $ |

| present_gold | Post-trade gold holdings | oz.t |

| Hold bitcoin after the transaction | BTC | |

| Change in the estimated price of gold (15 days later) | $/oz.t | |

| Change in the estimated price of bitcoin (after 15 days) | $/BTC | |

| The current price of gold | $ |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, J.; Rao, X.; Li, X.; Guan, S. Gold and Bitcoin Optimal Portfolio Research and Analysis Based on Machine-Learning Methods. Sustainability 2022, 14, 14659. https://doi.org/10.3390/su142114659

Li J, Rao X, Li X, Guan S. Gold and Bitcoin Optimal Portfolio Research and Analysis Based on Machine-Learning Methods. Sustainability. 2022; 14(21):14659. https://doi.org/10.3390/su142114659

Chicago/Turabian StyleLi, Jingjing, Xinge Rao, Xianyi Li, and Sihai Guan. 2022. "Gold and Bitcoin Optimal Portfolio Research and Analysis Based on Machine-Learning Methods" Sustainability 14, no. 21: 14659. https://doi.org/10.3390/su142114659

APA StyleLi, J., Rao, X., Li, X., & Guan, S. (2022). Gold and Bitcoin Optimal Portfolio Research and Analysis Based on Machine-Learning Methods. Sustainability, 14(21), 14659. https://doi.org/10.3390/su142114659