Enhanced Agriculture Insurance with Climate Forecast

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Literature Review

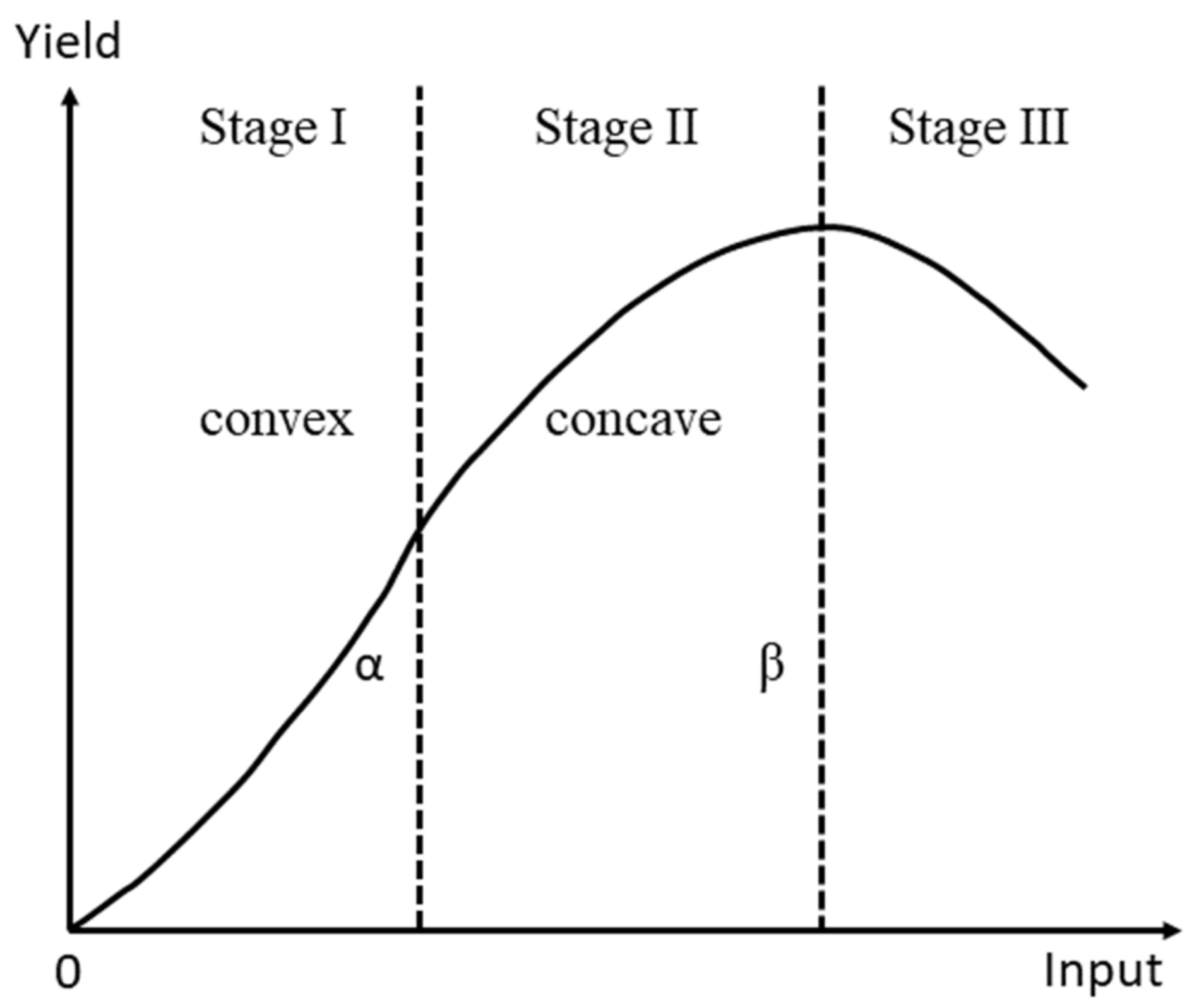

3. Preliminaries and the Base Model

3.1. Climate Forecasts

3.2. Agricultural Insurance

3.2.1. Voluntary Agricultural Insurance

3.2.2. Variance of Profit with Agricultural Insurance

3.2.3. Compulsory Agricultural Insurance

3.3. Government Bailouts and Tax

4. Agricultural Insurance and Policy after the Climate Forecast

5. Conclusions and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix B

Appendix C

Appendix D

References

- Cummins, J.D.; Mahul, O. Catastrophe Risk Financing in Developing Countries; The International Bank for Reconstruction and Development/The World Bank: Washington, DC, USA, 2009. [Google Scholar]

- Cornaggia, J. Does risk management matter? Evidence from the U.S. agricultural industry. J. Financ. Econ. 2013, 109, 419–440. [Google Scholar] [CrossRef]

- Carriquiry, M.A.; Osgood, D.E. Index Insurance, Probabilistic Climate Forecasts, and Production. J. Risk Insur. 2012, 79, 287–299. [Google Scholar] [CrossRef]

- Fawzy, S.; Osman, A.I.; Doran, J.; Rooney, D.W. Strategies for mitigation of climate change: A review. Environ. Chem. Lett. 2020, 18, 2069–2094. [Google Scholar] [CrossRef]

- McGlashan, N.R.; Workman, M.H.W.; Caldecott, B.; Shah, N. Negative Emissions Technologies; Briefing Paper n. 8; Grantham Institute for Climate Change, Imperial College of London: London, UK, 2012. [Google Scholar]

- Panepinto, D.; Riggio, V.A.; Zanetti, M. Analysis of the emergent climate change mitigation technologies. Int. J. Environ. Res. Public Health 2021, 18, 6767. [Google Scholar] [CrossRef] [PubMed]

- Teixeira, E.I.; de Ruiter, J.; Ausseil, A.-G.; Daigneault, A.; Johnstone, P.; Holmes, A.; Tait, A.; Ewert, F. Adapting Crop Rotations to Climate Change in Regional Impact Modelling Assessments. Sci. Total. Environ. 2018, 616–617, 785–795. [Google Scholar] [CrossRef] [PubMed]

- Swinton, S.M. Drought survival tactics of subsistence farmers in Niger. Hum. Ecol. 1988, 16, 123–144. [Google Scholar] [CrossRef]

- Wu, Y.-C. Reexamining the feasibility of diversification and transfer instruments on smoothing catastrophe risk. Insur. Math. Econ. 2015, 64, 54–66. [Google Scholar] [CrossRef]

- Goddard, L.; Mason, S.J.; Zebiak, S.E.; Ropelewski, C.F.; Basher, R.; Cane, M.A. Current Approaches to Seasonal-to-International Climate Predictions. Int. J. Climatol. 2001, 21, 1111–1152. [Google Scholar] [CrossRef]

- Ropelewski, C.; Halpert, M. Global and Regional Scale Precipitation Patterns Associated with the El Nino/Southern Oscillations. Mon. Clim. Rev. 1987, 115, 1606–1626. [Google Scholar] [CrossRef]

- Hansen, J.; Sato, L.M.; Nazarenko, R.; Ruedy, A.; Lacis, D.; Koch, I.; Tegen, T.; Hall, D.; Shindell, B.; Santer, P. Climate forcings in Goddard Institute for Space Studies SI2000 simulations. J. Geophys. Res. 2002, 107, 4347. [Google Scholar] [CrossRef]

- Rowhanji, P.; Lobell, D.; Lindermann, M.; Ramankutty, N. Climate variability and crop production in Tanzania. Agric. For. Meteorol. 2011, 151, 449–460. [Google Scholar] [CrossRef]

- Anton, J.; Kimura, S.; Lankoski, J.; Cattaneo, A. A Comparative Study of Risk Management in Agriculture under Climate Change. In OECD Food, Agriculture and Fisheries Papers; No. 58; OECD Publishing: Paris, France, 2012. [Google Scholar]

- Kuosmanen, T. Green productivity in agriculture: A critical synthesis. In Proceedings of the OECD Expert Workshop: Measuring Environmentally Adjusted Total Factor Productivity for Agriculture, Session 4, Paris, France, 14–15 December 2015. [Google Scholar]

- Debertin, D.L. Agricultural Production Economics, 2nd ed.; Createspace Independent Pub: Scotts Valley, CA, USA, 2012; pp. 26–29. [Google Scholar]

- Albersen, P.; Fischer, G.; Keyzer, M.A.; Sun, L. Estimation of Agricultural Production Relations in the LUC Model for China; IIASA Research Report; IIASA: Laxenburg, Austria, 2002. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, L.; Liu, Z.; Chen, J.-Y.; Wu, Y.-C.; Li, H. Enhanced Agriculture Insurance with Climate Forecast. Sustainability 2022, 14, 10617. https://doi.org/10.3390/su141710617

Li L, Liu Z, Chen J-Y, Wu Y-C, Li H. Enhanced Agriculture Insurance with Climate Forecast. Sustainability. 2022; 14(17):10617. https://doi.org/10.3390/su141710617

Chicago/Turabian StyleLi, Lanlan, Zhengqiao Liu, Jing-Yi Chen, Yang-Che Wu, and Hong Li. 2022. "Enhanced Agriculture Insurance with Climate Forecast" Sustainability 14, no. 17: 10617. https://doi.org/10.3390/su141710617

APA StyleLi, L., Liu, Z., Chen, J.-Y., Wu, Y.-C., & Li, H. (2022). Enhanced Agriculture Insurance with Climate Forecast. Sustainability, 14(17), 10617. https://doi.org/10.3390/su141710617