A Study of the Relationship between Corporate Culture and Corporate Sustainable Performance: Evidence from Chinese SMEs

Abstract

1. Introduction

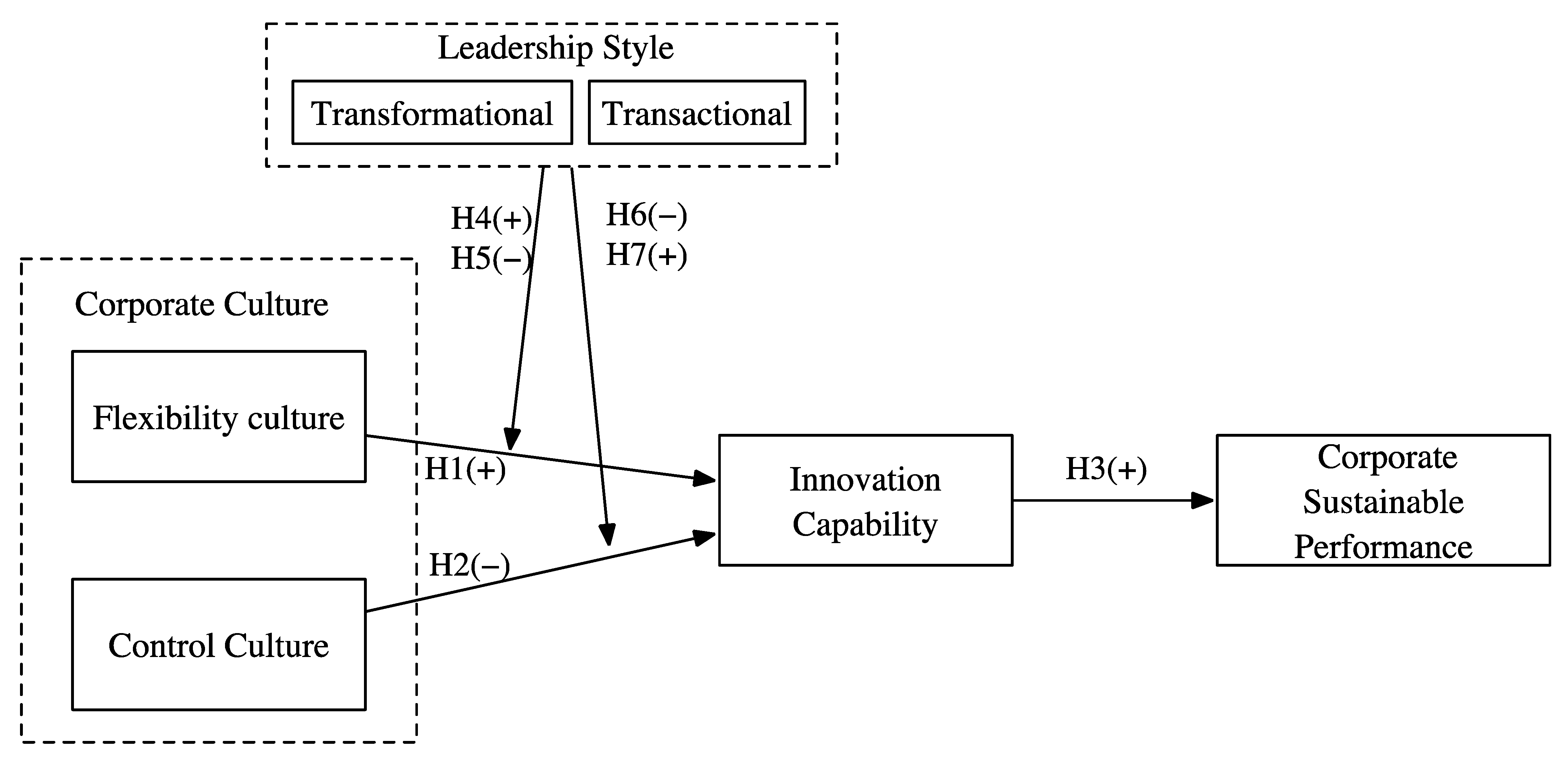

2. Theoretical Background and Research Hypothesis

2.1. Resource-Based View

2.2. Corporate Sustainable Performance

2.3. Corporate Culture

2.4. Leadership Style

2.5. Corporate Culture and Innovation Capability

2.6. Corporate Innovation Capability and Sustainable Performance

2.7. Moderating Effects of Leadership Style

2.7.1. The Moderating effect of Transformational Leadership

2.7.2. The Moderating Effect of Transactional Leadership

3. Method

3.1. Sample and Procedure

3.2. Measures

{kind=link}

{kind=link}

| Construct | Item | Factor Loadings | Sources |

|---|---|---|---|

| Flexibility culture | Cronbach’s α = 0.814; CR = 0.8776; AVE = 0.6456; Respondent: managers | ||

| FC_1: Sense of loyalty and corporate culture bring all employees together | 0.841 | [37,38] | |

| FC_2: The company challenges status quo and has a preference for risk-taking | 0.627 | ||

| FC_3: The company always prioritizes quality products and services | 0.896 | ||

| FC_4: The company invites new ideas for business growth from employees | 0.824 | ||

| Control culture | Cronbach’s α = 0.879; CR = 0.9176; AVE = 0.7361; Respondent: managers | ||

| CC_1: Regulation and system hold all staff together | 0.893 | ||

| CC_2: The company emphasizes durability and stability | 0.890 | ||

| CC_3: The company takes the production-oriented approach | 0.820 | ||

| CC_4: The company values work achievements | 0.826 | ||

| Transformational leadership | Cronbach’s α = 0.871; CR = 0.8995; AVE = 0.5288; Respondent: employees | ||

| TFL_1: He/she advises employees to approach tasks from new perspectives | 0.728 | [94] | |

| TFL_2: He/she encourages employees to analyze problems with different views | 0.740 | ||

| TFL_3: He/she encourages employees to solve problems with different approaches | 0.727 | ||

| TFL_4: He/she is always optimistic about the future | 0.641 | ||

| TFL_5: He/she sets a clear vision and motivates employees to work hard | 0.767 | ||

| TFL_6: His/her behavior is respected and recognized by employees | 0.768 | ||

| TFL_7: He/she believes that employees have their own needs, abilities, and ambitions | 0.746 | ||

| TFL_8: He/she helps bring employee strengths into play | 0.692 | [94] | |

| Transactional leadership | Cronbach’s α = 0.875; CR = 0.9099; AVE = 0.6699; Respondent: employees | ||

| TAL_1: He/she sets clear rewards for employees who hit targets | 0.748 | ||

| TAL_2: He/she rewards and helps employees so to motivate them to work harder | 0.763 | ||

| TAL_3: He/she focuses on inconformity and exception errors | 0.879 | ||

| TAL_4: He/she devotes much energy to handling deviations, complaints, and mistakes | 0.857 | ||

| TAL_5: He/she is concerned with employee mistakes and is aware of problem and mistake details | 0.837 | ||

| Innovation Capability | Cronbach’s α = 0.873; CR = 0.9143; AVE = 0.7276; Respondent: managers | ||

| IC_1: Our company often comes up with new ways to solve legacy issues | 0.818 | [100,101] | |

| IC_2: Our company is very creative in operations | 0.890 | ||

| IC_3: Our company often seek for new approaches | 0.886 | ||

| IC_4: Many of our new products or services are on offer | 0.815 | ||

| Corporate Sustainable performance | Cronbach’s α = 0.815; CR = 0.9548; AVE = 0.6385; Respondent: managers; 1 for “much worse” and 5 for “much better” | ||

| SP_1: Return on investment | 0.784 | [96,97,98,99] | |

| SP_2: Earnings growth | 0.844 | ||

| SP_3: Sales growth | 0.819 | ||

| SP_4: Market share. | 0.768 | ||

| SP_5: Comply with environmental regulations | 0.832 | ||

| SP_6: Limit environmental impacts beyond compliance | 0.832 | ||

| SP_7: Prevent and mitigate environmental crises | 0.832 | ||

| SP_8: Educate employees and the public about the environment | 0.760 | ||

| SP_9: Customer satisfaction | 0.691 | ||

| SP_10: Employee satisfaction | 0.833 | ||

| SP_11: Community recognition | 0.806 | ||

| SP_12: Investor recognition. | 0.774 |

4. Results

4.1. Reliability and Validity Testing

4.2. Common Method Bias

4.3. Hypothesis Testing

5. Discussions and Conclusions

5.1. Findings

5.2. Theoretical Implications

5.3. Management Implications

5.4. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- De Sousa Jabbour, A.B.L.; Ndubisi, N.O.; Seles, B.M.R.P. Sustainable development in Asian manufacturing SMEs: Progress and directions. Int. J. Prod. Econ. 2020, 225, 107567. [Google Scholar] [CrossRef]

- Zhang, Y.; Yu, Y.; Chen, Z. Artificial Intelligence, SME Financing and Bank Digitalization. China Ind. Econ. 2021, 12, 69–87. [Google Scholar] [CrossRef]

- Das, M.; Rangarajan, K.; Dutta, G. Corporate sustainability in SMEs: An Asian perspective. J. Asia Bus. Stud. 2020, 14, 109–138. [Google Scholar] [CrossRef]

- Huang, Y.; Baruah, B.; Ward, T. How do High-Tech Software SMEs in China Manage Risks and Survive in Today’s Complex Environment? In Proceedings of the 16th European Conference on Innovation and Entrepreneurship, ECIE 2021, Lisbon, Portugal, 16–17 September 2021; pp. 1144–1152. [Google Scholar]

- Dai, R.; Feng, H.; Hu, J.; Jin, Q.; Li, H.; Wang, R.; Wang, R.; Xu, L.; Zhang, X. The impact of COVID-19 on small and medium-sized enterprises (SMEs): Evidence from two-wave phone surveys in China. China Econ. Rev. 2021, 67, 101607. [Google Scholar] [CrossRef]

- Moore, S.B.; Manring, S.L. Strategy development in small and medium sized enterprises for sustainability and increased value creation. J. Clean. Prod. 2009, 17, 276–282. [Google Scholar] [CrossRef]

- Winston, A. What 1000 CEOs Really Think about Climate Change and Inequality; Harvard Business Review: Brighton, MA, USA, 2019. [Google Scholar]

- Neubaum, D.O.; Zahra, S.A. Institutional Ownership and Corporate Social Performance: The Moderating Effects of Investment Horizon, Activism, and Coordination. J. Manag. 2006, 32, 108–131. [Google Scholar] [CrossRef]

- Montiel, I.; Delgado-Ceballos, J. Defining and Measuring Corporate Sustainability. Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Niesten, E.; Jolink, A.; de Sousa Jabbour, A.B.L.; Chappin, M.; Lozano, R. Sustainable collaboration: The impact of governance and institutions on sustainable performance. J. Clean. Prod. 2017, 155, 1–6. [Google Scholar] [CrossRef]

- Di Vaio, A.; Varriale, L. Blockchain technology in supply chain management for sustainable performance: Evidence from the airport industry. Int. J. Inf. Manag. 2020, 52, 102014. [Google Scholar] [CrossRef]

- Yusliza, M.Y.; Yong, J.Y.; Tanveer, M.I.; Ramayah, T.; Faezah, J.N.; Muhammad, Z. A structural model of the impact of green intellectual capital on sustainable performance. J. Clean. Prod. 2020, 249, 119334. [Google Scholar] [CrossRef]

- Mousa, S.K.; Othman, M. The impact of green human resource management practices on sustainable performance in healthcare organisations: A conceptual framework. J. Clean. Prod. 2020, 243, 118595. [Google Scholar] [CrossRef]

- Jilani, M.M.A.K.; Fan, L.; Islam, M.T.; Uddin, M. The influence of knowledge sharing on sustainable performance: A moderated mediation study. Sustainability 2020, 12, 908. [Google Scholar] [CrossRef]

- Rathore, H.; Jakhar, S.K.; Bhattacharya, A.; Madhumitha, E. Examining the mediating role of innovative capabilities in the interplay between lean processes and sustainable performance. Int. J. Prod. Econ. 2020, 219, 497–508. [Google Scholar] [CrossRef]

- Eccles, R.G.; Perkins, K.M.; Serafeim, G. How to become a sustainable company. MIT Sloan Manag. Rev. 2012, 53, 43–50. [Google Scholar]

- Lozano, R. Are Companies Planning their Organisational Changes for Corporate Sustainability? An Analysis of Three Case Studies on Resistance to Change and their Strategies to Overcome it. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 275–295. [Google Scholar] [CrossRef]

- Galpin, T.; Whitttington, J.L.; Bell, G. Is your sustainability strategy sustainable? Creating a culture of sustainability. Corp. Gov. 2015, 15, 1–17. [Google Scholar] [CrossRef]

- Linnenluecke, M.K.; Griffiths, A. Corporate sustainability and organizational culture. J. World Bus. 2010, 45, 357–366. [Google Scholar] [CrossRef]

- Baumgartner, R.J. Managing Corporate Sustainability and CSR: A Conceptual Framework Combining Values, Strategies and Instruments Contributing to Sustainable Development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Islam, M.S.; Tseng, M.-L.; Karia, N. Assessment of corporate culture in sustainability performance using a hierarchical framework and interdependence relations. J. Clean. Prod. 2019, 217, 676–690. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Quinn, R.E.; Rohrbaugh, J. A Spatial Model of Effectiveness Criteria: Towards a Competing Values Approach to Organizational Analysis. Manag. Sci. 1983, 29, 363–377. [Google Scholar] [CrossRef]

- Burns, J.M. Leadership; Harper & Row: New York, NY, USA, 1978. [Google Scholar]

- Wernerfelt, B. A resource-based view of the firm. Strateg. Manag. J. 1984, 5, 171–180. [Google Scholar] [CrossRef]

- Fiol, C.M. Managing culture as a competitive resource: An identity-based view of sustainable competitive advantage. J. Manag. 1991, 17, 191–211. [Google Scholar] [CrossRef]

- Klein, A. Corporate culture: Its value as a resource for competitive advantage. J. Bus. Strategy 2011, 32, 21–28. [Google Scholar] [CrossRef]

- Kayworth, T.; Leidner, D. Organizational Culture as a Knowledge Resource. In Handbook on Knowledge Management 1. International Handbooks on Information Systems; Holsapple, C.W., Ed.; Springer: Berlin/Heidelberg, Germany, 2004; Volume 1. [Google Scholar] [CrossRef]

- Hart, S.L. A Natural-Resource-Based View of the Firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Brundtland, G.H. Our common future—Call for action. Environ. Conserv. 1987, 14, 291–294. [Google Scholar] [CrossRef]

- Buyukozkan, G.; Karabulut, Y. Sustainability performance evaluation: Literature review and future directions. J. Environ. Manag. 2018, 217, 253–267. [Google Scholar] [CrossRef]

- Lourenço, I.C.; Branco, M.C.; Curto, J.D.; Eugénio, T. How Does the Market Value Corporate Sustainability Performance? J. Bus. Ethics 2011, 108, 417–428. [Google Scholar] [CrossRef]

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The determinants of corporate sustainability performance. Account. Financ. 2010, 50, 31–51. [Google Scholar] [CrossRef]

- Sharma, S.; Henriques, I. Stakeholder influences on sustainability practices in the Canadian forest products industry. Strateg. Manag. J. 2005, 26, 159–180. [Google Scholar] [CrossRef]

- Schein, E.H. Coming to a new awareness of organizational culture. MIT Sloan Manag. Rev. 1984, 25, 3–16. [Google Scholar]

- Yu, T.; Wu, N. A review of study on the competing values framework. Int. J. Bus. Manag. 2009, 4, 37–42. [Google Scholar] [CrossRef]

- Deshpandé, R.; Farley, J.U.; Webster Jr, F.E. Corporate culture, customer orientation, and innovativeness in Japanese firms: A quadrad analysis. J. Mark. 1993, 57, 23–37. [Google Scholar] [CrossRef]

- Liu, H.; Ke, W.; Wei, K.K.; Gu, J.; Chen, H. The role of institutional pressures and organizational culture in the firm’s intention to adopt internet-enabled supply chain management systems. J. Oper. Manag. 2010, 28, 372–384. [Google Scholar] [CrossRef]

- Sethuraman, K.; Suresh, J. Effective Leadership Styles. Int. Bus. Res. 2014, 7, 165. [Google Scholar] [CrossRef]

- Bass, B.M. Leadership and Performance beyond Expectations; Collier Macmillan: New York, NY, USA, 1985. [Google Scholar]

- Burns, J.S. Defining leadership: Can we see the forest for the trees? J. Leadersh. Stud. 1996, 3, 148–157. [Google Scholar] [CrossRef]

- Judge, T.A.; Piccolo, R.F. Transformational and transactional leadership: A meta-analytic test of their relative validity. J. Appl. Psychol. 2004, 89, 755–768. [Google Scholar] [CrossRef]

- Eagly, A.H.; Johannesen-Schmidt, M.C.; van Engen, M.L. Transformational, transactional, and laissez-faire leadership styles: A meta-analysis comparing women and men. Psychol. Bull. 2003, 129, 569–591. [Google Scholar] [CrossRef]

- Bono, J.E.; Judge, T.A. Personality and transformational and transactional leadership: A meta-analysis. J. Appl. Psychol. 2004, 89, 901–910. [Google Scholar] [CrossRef]

- Pieterse, A.N.; van Knippenberg, D.; Schippers, M.; Stam, D. Transformational and transactional leadership and innovative behavior: The moderating role of psychological empowerment. J. Organ. Behav. 2009, 31, 609–623. [Google Scholar] [CrossRef]

- MacKenzie, S.B.; Podsakoff, P.M.; Rich, G.A. Transformational and transactional leadership and salesperson performance. J. Acad. Mark. Sci. 2001, 29, 115–134. [Google Scholar] [CrossRef]

- Jensen, U.T.; Andersen, L.B.; Bro, L.L.; Bøllingtoft, A.; Eriksen, T.L.M.; Holten, A.-L.; Jacobsen, C.B.; Ladenburg, J.; Nielsen, P.A.; Salomonsen, H.H.; et al. Conceptualizing and Measuring Transformational and Transactional Leadership. Adm. Soc. 2016, 51, 3–33. [Google Scholar] [CrossRef]

- Avolio, B.J.; Waldman, D.A.; Yammarino, F.J. Leading in the 1990s: The Four I′s of Transformational Leadership. J. Eur. Ind. Train. 1991, 15, 16–19. [Google Scholar] [CrossRef]

- Eliyana, A.; Ma’arif, S.; Muzakki. Job satisfaction and organizational commitment effect in the transformational leadership towards employee performance. Eur. Res. Manag. Bus. Econ. 2019, 25, 144–150. [Google Scholar] [CrossRef]

- Bass, B.M.; Avolio, B.J.; Jung, D.I.; Berson, Y. Predicting unit performance by assessing transformational and transactional leadership. J. Appl. Psychol. 2003, 88, 207–218. [Google Scholar] [CrossRef]

- Zhang, T.; Wang, X.; Zhuang, G. Building channel power: The role of IT resources and information management capability. J. Bus. Ind. Mark. 2017, 32, 1217–1227. [Google Scholar] [CrossRef]

- Saunila, M. Innovation capability in SMEs: A systematic review of the literature. J. Innov. Knowl. 2020, 5, 260–265. [Google Scholar] [CrossRef]

- Lam, L.; Nguyen, P.; Le, N.; Tran, K. The Relation among Organizational Culture, Knowledge Management, and Innovation Capability: Its Implication for Open Innovation. JOItmC 2021, 7, 66. [Google Scholar] [CrossRef]

- Mendoza-Silva, A. Innovation capability: A systematic literature review. Eur. J. Innov. Manag. 2020, 24, 707–734. [Google Scholar] [CrossRef]

- Weber, B.; Heidenreich, S. When and with whom to cooperate? Investigating effects of cooperation stage and type on innovation capabilities and success. Long Range Plan. 2018, 51, 334–350. [Google Scholar] [CrossRef]

- Pascual-Fernández, P.; Santos-Vijande, M.L.; López-Sánchez, J.Á.; Molina, A. Key drivers of innovation capability in hotels: Implications on performance. Int. J. Hosp. Manag. 2021, 94, 102825. [Google Scholar] [CrossRef]

- Çakar, N.D.; Ertürk, A. Comparing Innovation Capability of Small and Medium-Sized Enterprises: Examining the Effects of Organizational Culture and Empowerment. J. Small Bus. Manag. 2010, 48, 325–359. [Google Scholar] [CrossRef]

- Yang, Z.; Nguyen, V.T.; Le, P.B. Knowledge sharing serves as a mediator between collaborative culture and innovation capability: An empirical research. J. Bus. Ind. Mark. 2018, 33, 958–969. [Google Scholar] [CrossRef]

- Chang, W.-J.; Liao, S.-H.; Wu, T.-T. Relationships among organizational culture, knowledge sharing, and innovation capability: A case of the automobile industry in Taiwan. Knowl. Manag. Res. Pract. 2017, 15, 471–490. [Google Scholar] [CrossRef]

- Naranjo Valencia, J.C.; Sanz Valle, R.; Jiménez Jiménez, D. Organizational culture as determinant of product innovation. Eur. J. Innov. Manag. 2010, 13, 466–480. [Google Scholar] [CrossRef]

- Lemon, M.; Sahota, P.S. Organizational culture as a knowledge repository for increased innovative capacity. Technovation 2004, 24, 483–498. [Google Scholar] [CrossRef]

- Martins, E.C.; Terblanche, F. Building organisational culture that stimulates creativity and innovation. Eur. J. Innov. Manag. 2003, 6, 64–74. [Google Scholar] [CrossRef]

- Arad, S.; Hanson, M.A.; Schneider, R.J. A framework for the study of relationships between organizational characteristics and organizational innovation. J. Creat. Behav. 1997, 31, 42–58. [Google Scholar] [CrossRef]

- Hartmann, A.; Dulaimi, M. The role of organizational culture in motivating innovative behaviour in construction firms. Constr. Innov. 2006, 6, 159–172. [Google Scholar] [CrossRef]

- Osipova, E.; Eriksson, P.E. Balancing control and flexibility in joint risk management: Lessons learned from two construction projects. Int. J. Proj. Manag. 2013, 31, 391–399. [Google Scholar] [CrossRef]

- Pierce, J.L.; Delbecq, A.L. Organization Structure, Individual Attitudes and Innovation. Acad. Manag. Rev. 1977, 2, 27–37. [Google Scholar] [CrossRef]

- Olssen, M. Understanding the mechanisms of neoliberal control: Lifelong learning, flexibility and knowledge capitalism. Int. J. Lifelong Educ. 2006, 25, 213–230. [Google Scholar] [CrossRef]

- Schultz, J.R. Creating a culture of empowerment fosters the flexibility to change. Glob. Bus. Organ. Excell. 2014, 34, 41–50. [Google Scholar] [CrossRef]

- Child, J. Predicting and understanding organization structure. Adm. Sci. Q. 1973, 18, 168–185. [Google Scholar] [CrossRef]

- Aghion, P.; Tirole, J. The management of innovation. Q. J. Econ. 1994, 109, 1185–1209. [Google Scholar] [CrossRef]

- FitzRoy, F.R.; Kraft, K. Innovation, rent-sharing and the organization of labour in the federal republic of Germany. Small Bus. Econ. 1990, 2, 95–103. [Google Scholar] [CrossRef]

- Dobni, C.B. Measuring innovation culture in organizations. Eur. J. Innov. Manag. 2008, 11, 539–559. [Google Scholar] [CrossRef]

- Richard, O.C.; Barnett, T.; Dwyer, S.; Chadwick, K. Cultural Diversity in Management, Firm Performance, and the Moderating Role of Entrepreneurial Orientation Dimensions. Acad. Manag. 2004, 47, 255–266. [Google Scholar] [CrossRef][Green Version]

- Schwarz, G.M.; Huber, G.P. Challenging Organizational Change Research. Br. J. Manag. 2008, 19, S1–S6. [Google Scholar] [CrossRef]

- Rajapathirana, R.P.J.; Hui, Y. Relationship between innovation capability, innovation type, and firm performance. J. Innov. Knowl. 2018, 3, 44–55. [Google Scholar] [CrossRef]

- AlNuaimi, B.K.; Khan, M. Public-sector green procurement in the United Arab Emirates: Innovation capability and commitment to change. J. Clean. Prod. 2019, 233, 482–489. [Google Scholar] [CrossRef]

- Chofreh, A.G.; Goni, F.A.; Shaharoun, A.M.; Ismail, S.; Klemeš, J.J. Sustainable enterprise resource planning: Imperatives and research directions. J. Clean. Prod. 2014, 71, 139–147. [Google Scholar] [CrossRef]

- Boadu, F.; Xie, Y.; Du, Y.; Dwomo-Fokuo, E. Management innovation and firm innovation performance: A moderated moderation effects of absorptive capacity and environmental dynamism. Total Qual. Manag. Bus. Excell. 2021; in press. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between corporate social responsibility and competitive advantage. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Kim, D.-Y.; Kumar, V.; Kumar, U. Relationship between quality management practices and innovation. J. Oper. Manag. 2012, 30, 295–315. [Google Scholar] [CrossRef]

- Ehie, I.C.; Olibe, K. The effect of R&D investment on firm value: An examination of US manufacturing and service industries. Int. J. Prod. Econ. 2010, 128, 127–135. [Google Scholar] [CrossRef]

- Pace, L.A. How do tourism firms innovate for sustainable energy consumption? A capabilities perspective on the adoption of energy efficiency in tourism accommodation establishments. J. Clean. Prod. 2016, 111, 409–420. [Google Scholar] [CrossRef]

- Cancino, C.A.; La Paz, A.I.; Ramaprasad, A.; Syn, T. Technological innovation for sustainable growth: An ontological perspective. J. Clean. Prod. 2018, 179, 31–41. [Google Scholar] [CrossRef]

- Di Vaio, A.; Varriale, L. Management Innovation for Environmental Sustainability in Seaports: Managerial Accounting Instruments and Training for Competitive Green Ports beyond the Regulations. Sustainability 2018, 10, 783. [Google Scholar] [CrossRef]

- Zhang, Y.; Khan, U.; Lee, S.; Salik, M. The Influence of Management Innovation and Technological Innovation on Organization Performance. A Mediating Role of Sustainability. Sustainability 2019, 11, 495. [Google Scholar] [CrossRef]

- Fan, Y.-J.; Liu, S.-F.; Luh, D.-B.; Teng, P.-S. Corporate Sustainability: Impact Factors on Organizational Innovation in the Industrial Area. Sustainability 2021, 13, 1979. [Google Scholar] [CrossRef]

- Bass, B.M.; Waldman, D.A.; Avolio, B.J.; Bebb, M. Transformational leadership and the falling dominoes effect. Organ. Stud. 1987, 12, 73–87. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; García-Morales, V.J.; Cordón-Pozo, E. Leadership and organizational learning’s role on innovation and performance: Lessons from Spain. Ind. Mark. Manag. 2007, 36, 349–359. [Google Scholar] [CrossRef]

- Feldman, J.M.; Lynch, J.G. Self-generated validity and other effects of measurement on belief, attitude, intention, and behaviour. J. Appl. Psychol. 1988, 73, 421–435. [Google Scholar] [CrossRef]

- Loken, B.; John, D.R. Diluting brand beliefs: When do brand extensions have a negative impact? J. Mark. 1993, 57, 71–84. [Google Scholar] [CrossRef]

- Lane, V.; Jacobson, R. The reciprocal impact of brand leveraging: Feedback effects from brand extension evaluation to brand evalution. Mark. Lett. 1997, 8, 261–271. [Google Scholar] [CrossRef]

- Herr, P.M.; Kardes, F.R.; Kim, J. Effects of word-of-mouth and product-attribute information on persuasion: An accessibility-diagnosticity perspective. J. Consum. Res. 1991, 17, 454–462. [Google Scholar] [CrossRef]

- Brislin, R.W. Translation and Content Analysis of Oral and Written Material. In Handbook of Cross-Cultural Psychology: Methodology; Triandis, H.C., Berry, J.W., Eds.; Allyn and Bacon: Boston, MA, USA, 1980; Volume 2, pp. 389–444. [Google Scholar]

- Bass, B.M.; Avolio, B.J. MLQ: Multifactor Leadership Questionnaire for Research: Permission Set; Mind Garden: Redwood City, CA, USA, 1995. [Google Scholar]

- Krajnc, D.; Glavič, P. A model for integrated assessment of sustainable development. Resour. Conserv. Recycl. 2005, 43, 189–208. [Google Scholar] [CrossRef]

- Judge, W.Q.; Douglas, T.J. Performance implications of incorporating natural environmental issues into the strategic planning process: An empirical assessment. J. Manag. Stud. 1998, 35, 241–262. [Google Scholar] [CrossRef]

- Kalchschmidt, M.; Golini, R.; Gualandris, J.; Stefan Schaltegger, P.R.B.D. Do supply management and global sourcing matter for firm sustainability performance? Supply Chain. Manag. 2014, 19, 258–274. [Google Scholar] [CrossRef]

- Eikelenboom, M.; de Jong, G. The impact of dynamic capabilities on the sustainability performance of SMEs. J. Clean. Prod. 2019, 235, 1360–1370. [Google Scholar] [CrossRef]

- Wijethilake, C. Proactive sustainability strategy and corporate sustainability performance: The mediating effect of sustainability control systems. J. Environ. Manag. 2017, 196, 569–582. [Google Scholar] [CrossRef] [PubMed]

- Hurt, H.T.; Joseph, K.; Cook, C.D. Scales for the measurement of innovativeness. Hum. Commun. Res. 1977, 4, 58–65. [Google Scholar] [CrossRef]

- Calantone, R.J.; Cavusgil, S.T.; Zhao, Y. Learning orientation, firm innovation capability, and firm performance. Ind. Mark. Manag. 2002, 31, 515–524. [Google Scholar] [CrossRef]

- Sharma, S.; Aragón-Correa, J.A.; Rueda-Manzanares, A. The contingent influence of organizational capabilities on proactive environmental strategy in the service sector: An analysis of North American and European ski resorts. Can. J. Adm. Sci. 2007, 24, 268–283. [Google Scholar] [CrossRef]

- Darnall, N.; Edwards, D. Predicting the cost of environmental management system adoption: The role of capabilities, resources and ownership structure. Strateg. Manag. J. 2006, 27, 301–320. [Google Scholar] [CrossRef]

- Autio, E.; Sapienza, H.J.; Almeida, J.G. Effects of age at entry, knowledge intensity, and imitability on international growth. Acad. Manag. J. 2000, 43, 909–924. [Google Scholar] [CrossRef]

- John, G.; Reve, T. The Reliability and Validity of Key Informant Data from Dyadic Relationships in Marketing Channels. J. Mark. Res. 1982, 19, 517–524. [Google Scholar] [CrossRef]

- Anderson, J.C.; Gerbing, D.W. Structural equation modeling in practice: A review and recommended two-step approach. Psychol. Bull. 1988, 103, 411–423. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Pearson Education: Upper Saddle River, NJ, USA, 2014. [Google Scholar]

- Fornell, C.; Larcker, D.F. Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2005, 43, 115–135. [Google Scholar] [CrossRef]

- Lindell, M.K.; Whitney, D.J. Accounting for common method variance in cross-sectional research designs. J. Appl. Psychol. 2001, 86, 114–121. [Google Scholar] [CrossRef] [PubMed]

- Podsakoff, P.M.; Organ, D.W. Self-reports in organizational research: Problems and prospects. J. Manag. 1986, 12, 531–544. [Google Scholar] [CrossRef]

- Fuller, C.M.; Simmering, M.J.; Atinc, G.; Atinc, Y.; Babin, B.J. Common methods variance detection in business research. J. Bus. Res. 2016, 69, 3192–3198. [Google Scholar] [CrossRef]

- Gefen, D.; Straub, D.; Boudreau, M.C. Structural equation modeling and regression: Guidelines for research practice. Commun. Assoc. Inf. Syst. 2000, 4, 7. [Google Scholar] [CrossRef]

- Cohen, J.; Cohen, P.; West, S.G.; Aiken, L.S. Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences; Lawrence Erlbaum: Mahwah, NJ, USA, 2003. [Google Scholar]

- Chen, C.H. The mediating effect of corporate culture on the relationship between business model innovation and corporate social respon-sibility: A perspective from small-and medium-sized enterprises. Asia Pac. Manag. 2022; in press. [Google Scholar] [CrossRef]

- Shafi, M. Sustainable development of micro firms: Examining the effects of cooperation on handicraft firm’s performance through innovation capability. Int. J. Emerg. Mark. 2020, 16, 1634–1653. [Google Scholar] [CrossRef]

- Tran, Q.H. Organisational culture, leadership behaviour and job satisfaction in the Vietnam context. Int. J. Organ. Anal. 2020, 29, 136–154. [Google Scholar] [CrossRef]

- Mansouri, A.A.A.; Singh, S.K.; Khan, M. Role of organisational culture, leadership and organisational citizenship be-haviour on knowledge management. Int. J. Knowl. Manag. Stud. 2018, 9, 129–143. [Google Scholar] [CrossRef]

- Faul, F.; Erdfelder, E.; Lang, A.G.; Buchner, A. G*Power 3: A flexible statistical power analysis program for the social, behavioral, and biomedical sciences. Behav. Res. Methods 2007, 39, 175–191. [Google Scholar] [CrossRef]

- Preacher, K.J.; Curran, P.J.; Bauer, D.J. Computational tools for probing interactions in multiple linear regression, multilevel modeling, and latent curve analysis. J. Educ. Behav. Stat. 2006, 31, 437–448. [Google Scholar] [CrossRef]

- Preacher, K.J.; Hayes, A.F. SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behav. Res. Methods Instrum. Comput. 2004, 36, 717–731. [Google Scholar] [CrossRef] [PubMed]

| Items | Categories | % | Items | Categories | % |

|---|---|---|---|---|---|

| Profile of Organizations: | Profile of Respondents: | ||||

| Ownership | State-owned | 17.2% | Gender | Male | 67.74% |

| Private | 76.9% | Female | 32.26% | ||

| Joint ventures | 2.7% | Position | Senior managers | 18.82% | |

| Foreign-funded | 3.2% | Managers | 31.18% | ||

| Employees | 50 and below | 16.7% | Employees | 50% | |

| 51 to 100 | 24.2% | Education | High school and below | 4.84% | |

| 101 to 200 | 40.3% | Three-year college | 20.97% | ||

| 201 to 300 | 14% | Bachelor | 54.57% | ||

| 300 and above | 4.8% | Master and above | 19.62% | ||

| Firm age | Below 1 year | 6.5% | Age | Below 30 years old | 30.1% |

| 1–3 years | 11.8% | 30–40 years old | 32.25% | ||

| 3–5 years | 38.7% | 41–50 years old | 23.94% | ||

| 5–10 years | 40.9% | Above 50 years old | 13.7% | ||

| Above 10 years | 2.2% | ||||

| Industry | Retailing and wholesale | 12.37% | |||

| Foods and beverage | 9.68% | ||||

| Software and Services | 19.89% | ||||

| Textile | 6.45% | ||||

| Transportation and logistics | 6.99% | ||||

| Manufacturing/engineering | 24.19% | ||||

| Environmental | 9.13% | ||||

| Others | 11.29% | ||||

| Geographic location | Chengdu | 18.82% | |||

| Shanghai | 8.6% | ||||

| Xi’an | 9.68% | ||||

| Beijing | 7.53% | ||||

| Guiyang | 11.29% | ||||

| Guangzhou | 10.75% | ||||

| Qingdao | 10.22% | ||||

| Shenyang | 12.9% | ||||

| Lanzhou | 10.22% | ||||

| Variable | Mean | S.D. | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|---|

| 1. Flexibility Culture | 3.579 | 0.9579 | 0.8034 | −0.511 *** | 0.425 *** | 0.150 * | −0.113 |

| 2. Control Culture | 2.448 | 1.1129 | −0.518 *** | 0.8579 | −0.545 *** | −0.183 ** | 0.311 *** |

| 3. Innovation Capability | 3.235 | 0.8029 | 0.440 *** | −0.552 *** | 0.8529 | 0.373 *** | −0.670 *** |

| 4. Sustainable Performance | 3.041 | 0.7186 | 0.164 * | −0.192 ** | 0.382 *** | 0.7991 | −0.088 |

| 5. Transactional Leader | 2.959 | 1.1760 | −0.138 | 0.332 *** | −0.678 *** | −0.102 | 0.8185 |

| 6. Transformational Leader (MV) | 3.209 | 0.9844 | 0.178 * | −0.104 | 0.155 * | 0.099 | −0.158 * |

| Construct | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| 1. Flexibility Culture | |||||

| 2. Control Culture | 0.613 | ||||

| 3. Innovation Capability | 0.514 | 0.628 | |||

| 4. Sustainable Performance | 0.206 | 0.222 | 0.439 | ||

| 5. Transformational Leader | 0.222 | 0.127 | 0.176 | 0.158 | |

| 6. Transactional Leader | 0.166 | 0.366 | 0.772 | 0.148 | 0.254 |

| Variable | Innovation Capability | SP | |||

|---|---|---|---|---|---|

| Model1 | Model 2 | Model 3 | Model 4 | ||

| Controlled Variable | |||||

| Firm Size | 0.074 | 0.045 | 0.001 | 0.022 | |

| Ownership | −0.177 ** | −0.134 * | 0.041 | −0.046 | |

| Firm age | 0.123 * | 0.154 ** | −0.081 | −0.042 | |

| Industry | 0.085 | 0.052 | 0.031 | 0.141* | |

| Main Effect | |||||

| FC | H1 | 0.186 ** | 0.306 *** | 0.234 *** | |

| CC | H2 | −0.477 *** | −0.414 *** | −0.185 ** | |

| IC | H3 | 0.367 *** | |||

| Moderating Effect | |||||

| TFL | 0.060 | ||||

| TAL | −0.582 *** | ||||

| TFL × FC | H4 | 0.473 *** | |||

| TFL × CC | H5 | 0.245 *** | |||

| TAL × FC | H6 | 0.063 | |||

| TAL × CC | H7 | −0.113 * | |||

| R2 | 0.392 | 0.536 | 0.653 | 0.167 | |

| Adjusted R2 | 0.371 | 0.513 | 0.635 | 0.144 | |

| F value | 19.209 *** | 22.625 *** | 36.780 *** | 7.207 *** | |

| Power (1-β err prob) | 1 | 1 | 1 | 0.99 | |

| Model | Indirect Effect | BootSE | 95% Confidence Interval | Direct Effect | BootSE | 95% Confidence Interval | ||

|---|---|---|---|---|---|---|---|---|

| BootLLCI | BootULCI | BootLLCI | BootULCI | |||||

| FC-IC-SP | 0.1562 | 0.0416 | 0.0811 | 0.2453 | −0.0053 | 0.0759 | −0.1551 | 0.1445 |

| CC-IC-SP | −0.2154 | 0.0480 | −0.3112 | −0.1215 | 0.0254 | 0.0844 | −0.1411 | 0.1918 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, S.; Huang, L. A Study of the Relationship between Corporate Culture and Corporate Sustainable Performance: Evidence from Chinese SMEs. Sustainability 2022, 14, 7527. https://doi.org/10.3390/su14137527

Wang S, Huang L. A Study of the Relationship between Corporate Culture and Corporate Sustainable Performance: Evidence from Chinese SMEs. Sustainability. 2022; 14(13):7527. https://doi.org/10.3390/su14137527

Chicago/Turabian StyleWang, Siyuan, and Linglan Huang. 2022. "A Study of the Relationship between Corporate Culture and Corporate Sustainable Performance: Evidence from Chinese SMEs" Sustainability 14, no. 13: 7527. https://doi.org/10.3390/su14137527

APA StyleWang, S., & Huang, L. (2022). A Study of the Relationship between Corporate Culture and Corporate Sustainable Performance: Evidence from Chinese SMEs. Sustainability, 14(13), 7527. https://doi.org/10.3390/su14137527