Shareholder Option Valuation in Mezzanine Financing Applied to CO2 Reduction in Sustainable Infrastructure Projects: Application to a Tunnel Road in Medellin, Colombia

Abstract

:1. Introduction

2. Literature Review

2.1. Infrastructure Projects

2.2. Sustainability in Infrastructure Projects

2.3. ROA

2.4. Mezzanine Financing

3. Materials and Methods

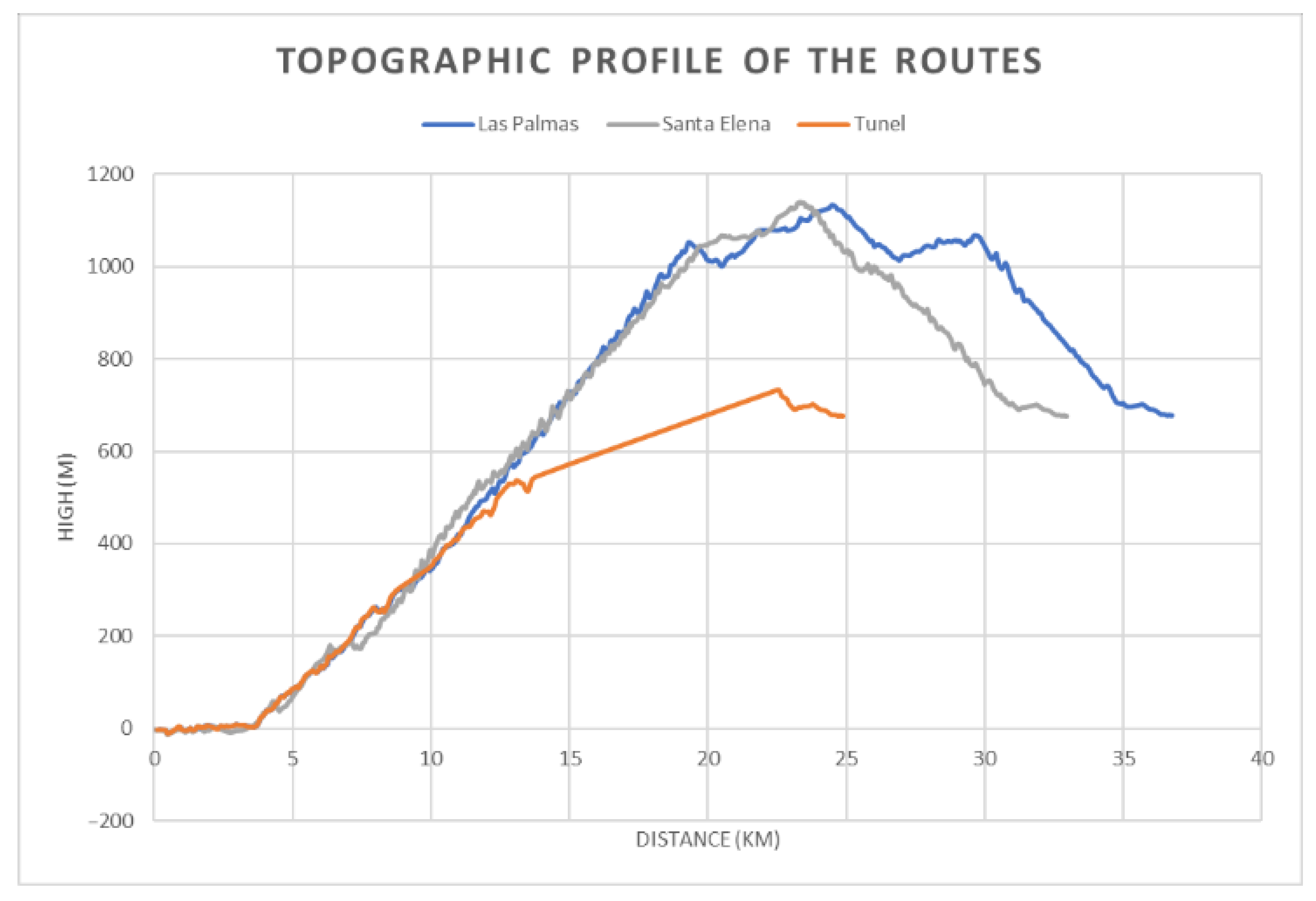

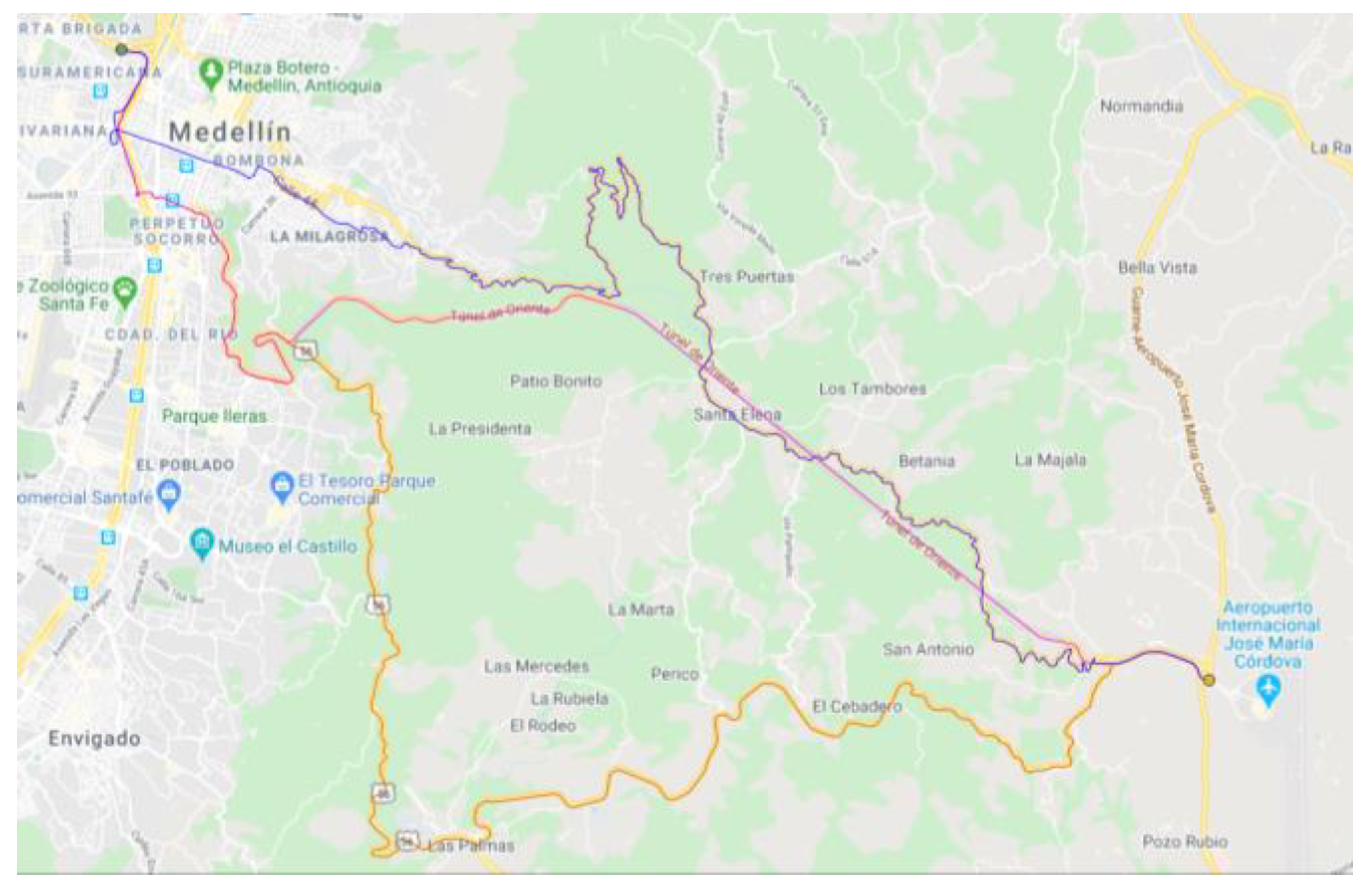

3.1. Alternative Routes Analyzed

- Santa Elena: it is a two-lane road that is the oldest road between the two points, since it was designed at the beginning of the 20th century; it has numerous curves.

- Las Palmas: it was constructed in the second half of the 20th century and is longer than Santa Elena, but it is designed for higher speed. Half of it is a four-lane road (two lanes in each direction), and the other half is a two-lane road with fewer curves than Santa Elena.

- Tunnel: This shares the initial path of Las Palmas, but instead of going up and down hill, it crosses the mountain with a tunnel, reducing the travel time. This is known as the Eastern Tunnel (in Spanish “Túnel de oriente”).

3.2. ROA

3.3. Methodology

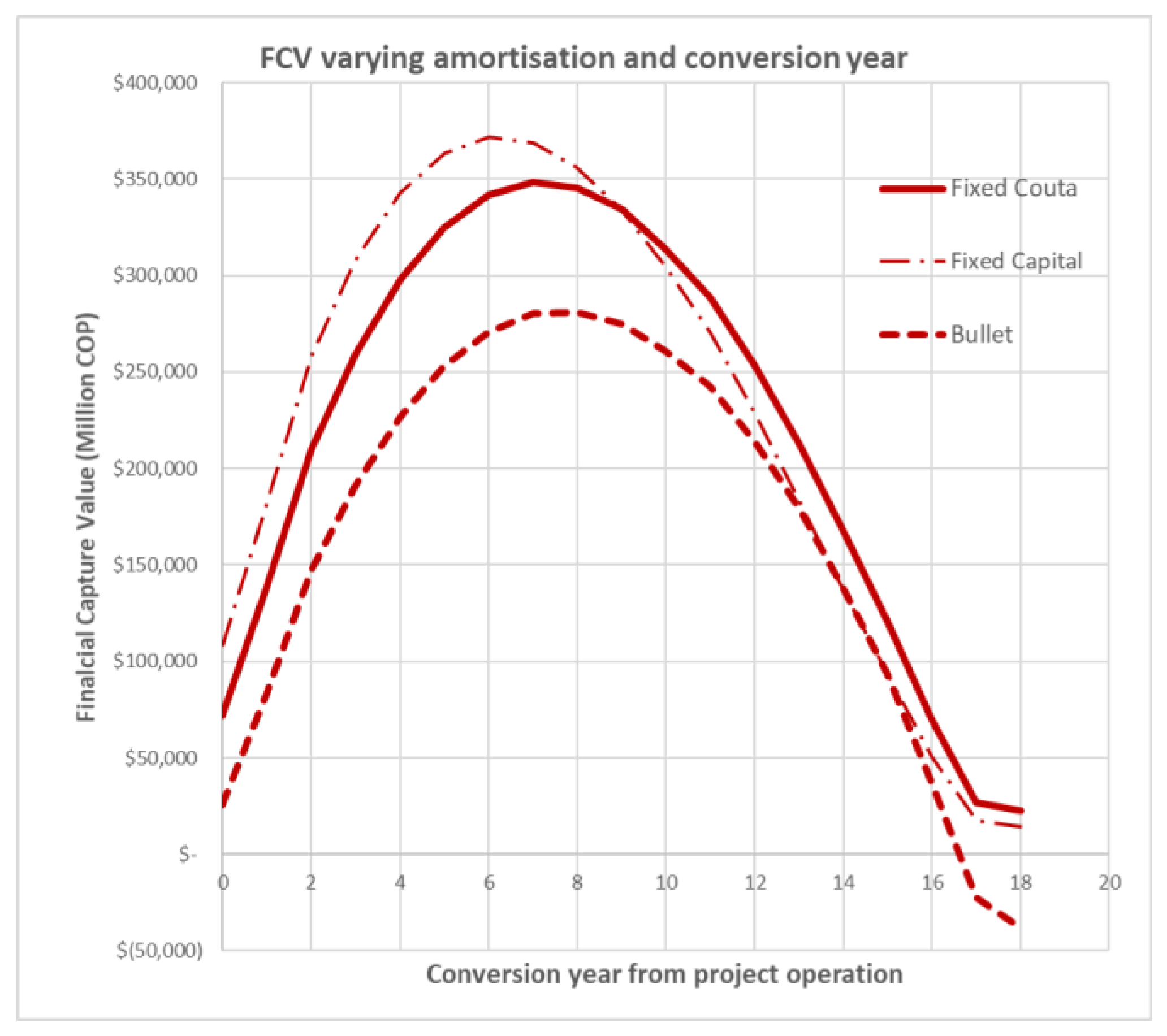

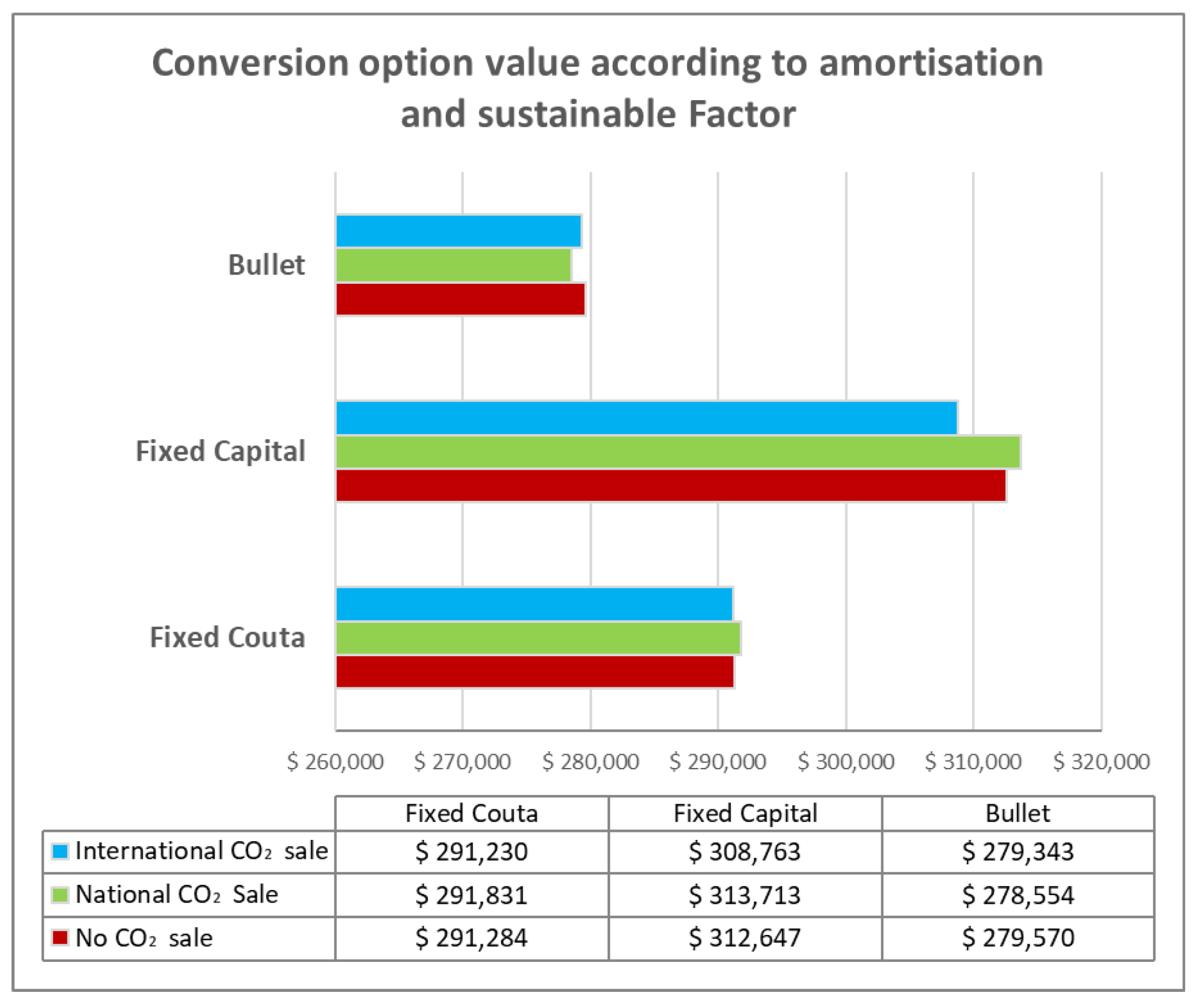

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Gonzalez-Ruiz, J.D.; Arboleda, A.; Botero, S.; Rojo, J. Investment valuation model for sustainable infrastructure systems: Mezzanine debt for water projects. Eng. Constr. Archit. Manag. 2019, 26, 850–884. [Google Scholar] [CrossRef]

- Kim, K.; Cho, H.; Yook, D. Financing for a sustainable PPP development: Valuation of the contractual rights under exercise conditions for an urban railway PPP Project in Korea. Sustainability 2019, 11, 1573. [Google Scholar] [CrossRef] [Green Version]

- Liu, J.; Yu, X.; Cheah, C.Y.J. Evaluation of restrictive competition in PPP projects using real option approach. Int. J. Proj. Manag. 2014, 32, 473–481. [Google Scholar] [CrossRef]

- Ford, D.N.; Lander, D.M.; Voyer, J.J. A real options approach to valuing strategic flexibility in uncertain construction projects. Constr. Manag. Econ. 2002, 20, 343–351. [Google Scholar] [CrossRef]

- Abdel Aziz, A.M. Successful delivery of public—Private partnerships for infrastructure development. J. Constr. Eng. Manag. 2007, 133, 918–931. [Google Scholar] [CrossRef]

- Garvin, M.J.; Cheah, C.Y.J. Valuation techniques for infrastructive investment decisions. Constr. Manag. Econ. 2004, 22, 373–383. [Google Scholar] [CrossRef]

- Zhang, X. Critical success factors for public–private partnerships in infrastructure development. J. Constr. Eng. Manag. 2005, 131, 3–14. [Google Scholar] [CrossRef]

- Menheere, S.; Pollalis, S.; Huijbregts, R. Case Studies on Build Operate Transfer; Delft University of Technology: Delft, The Netherlands, 1996. [Google Scholar]

- Xenidis, Y.; Angelides, D. The financial risks in build-operate-transfer projects. Constr. Manag. Econ. 2005, 23, 431–441. [Google Scholar] [CrossRef]

- De Marco, A.; Mangano, G.; Zou, X.Y. Factors influencing the equity share of build-operate-transfer projects. Built Environ. Proj. Asset Manag. 2012, 2, 70–85. [Google Scholar] [CrossRef] [Green Version]

- Finnerty, J. Project Financing: Asset-Based Financial Engineering; Wiley: Hoboken, NJ, USA, 2013. [Google Scholar]

- Bakatjan, S.; Arikan, M.; Tiong, R.L.K. Optimal capital structure model for BOT power projects in Turkey. J. Constr. Eng. Manag. 2003, 129, 89–97. [Google Scholar] [CrossRef]

- Zhang, X. Financial viability analysis and capital structure optimization in privatized public infrastructure projects. J. Constr. Eng. Manag. 2005, 131, 656–668. [Google Scholar] [CrossRef]

- Garvin, M.J. Enabling development of the transportation public–private partnership market in the United States. J. Constr. Eng. Manag. 2010, 136, 402–411. [Google Scholar] [CrossRef]

- Bybee, R.W. Planet earth in crisis: How should science educators respond? Am. Biol. Teach. 1991, 53, 146–153. [Google Scholar] [CrossRef]

- Spackman, M. Handling Non-Monetised Factors in Project, Programme and Policy Appraisal; Grantham Research Institute on Climate Change and Environment: London, UK, 2013; pp. 1–37. [Google Scholar]

- World Commission on Environment and Development. Our Common Future; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- Egler, H.; Frazao, R. Sustainable Infrastructure and Finance: How to Contribute to a Sustainable Future; 2016; p. 41. Available online: https://www.greengrowthknowledge.org/sites/default/files/downloads/resource//Sustainable_Infrastructure_and_Finance_UNEPInquiry.pdf (accessed on 5 May 2021).

- Bhattacharya, A.; Contreras, C.; Jeong, M.; Amin, A.-L.; Watkins, G.; Silva, M. Atributos y Marco Para la Infraestructura Sostenible; N° IDB-TN-01653; IDB Group: Washington, DC, USA, 2019. [Google Scholar]

- González-Ruíiz, J.D.; Botero-Botero, S.; Duque-Grisales, E. Financial eco-innovation as a mechanism for fostering the development of sustainable infrastructure systems. Sustainability 2018, 10, 4463. [Google Scholar] [CrossRef] [Green Version]

- Arvidsson, S. Challenges in Managing Sustainable Business Reporting, Taxation, Ethics and Governance; Springer International Publishing: Cham, Switzerland, 2018. [Google Scholar]

- Shaydurova, A.; Panova, S.; Fedosova, R.; Zlotnikova, G. Investment attractiveness of ‘Green’ financial instruments. J. Rev. Glob. Econ. 2018, 7, 710–715. [Google Scholar] [CrossRef] [Green Version]

- González-Ruiz, J.D.; Arboleda, C.A.; Botero, S. A Proposal for Green Financing as a Mechanism to Increase Private Participation in Sustainable Water Infrastructure Systems: The Colombian Case. Procedia Eng. 2016, 145, 180–187. [Google Scholar] [CrossRef] [Green Version]

- Radavoi, C.N.; Bian, Y. The Asian Infrastructure Investment Bank’s environmental and social policies: A critical discourse analysis. J. Int. Comp. Soc. Policy 2018, 34, 1–18. [Google Scholar] [CrossRef]

- Diaz-Sarachaga, J.M.; Jato-Espino, D.; Alsulami, B.; Castro-Fresno, D. Evaluation of existing sustainable infrastructure rating systems for their application in developing countries. Ecol. Indic. 2016, 71, 491–502. [Google Scholar] [CrossRef] [Green Version]

- Ugwu, O.O.; Haupt, T.C. Key performance indicators for infrastructure sustainability—A comparative study between Hong Kong and South Africa. J. Eng. Des. Technol. 2005, 3, 30–43. [Google Scholar] [CrossRef]

- Umer, A.; Hewage, K.; Haider, H.; Sadiq, R. Sustainability assessment of roadway projects under uncertainty using Green Proforma: An index-based approach. Int. J. Sustain. Built Environ. 2016, 5, 604–619. [Google Scholar] [CrossRef] [Green Version]

- Boschmann, E.E.; Kwan, M.-P. Toward socially sustainable urban transportation: Progress and potentials. Int. J. Sustain. Transp. 2008, 2, 138–157. [Google Scholar] [CrossRef]

- Clevenger, C.; Ozbek, M.; Simpson, S. Review of sustainability rating systems used for infrastructure projects. In Proceedings of the 49th ASC Annual International Conference, San Luis Obispo, CA, USA, 10–13 April 2013; pp. 10–13. [Google Scholar]

- Flores, R.F.; Montoliu, C.M.; Guedella Bustamante, E. Life cycle engineering for Roads (LCE4ROADS), the new sustainability certification system for roads from the LCE4ROADS FP7 project. Transp. Res. Procedia 2016, 14, 896–905. [Google Scholar] [CrossRef] [Green Version]

- Lim, S. Framework and Processes for Enhancing Sustainability Deliverables in Australian Road Infrastructure Projects. Doctoral dissertation, Queeland University of Technology, Brisbane City, Australia, 2009. Available online: https://eprints.qut.edu.au/32053/ (accessed on 15 January 2021).

- Griffiths, K. Project sustainability management in infrastructure projects. In Proceedings of the 2nd International Conference on Sustainability Engineering and Science, Auckland, New Zealand, 21–23 February 2007. [Google Scholar]

- Luehrman, T.A. What’s it worth? A general manager’s guide to valuation. Harv. Bus. Rev. 1997, 75, 132–142. [Google Scholar] [PubMed]

- Gijsen, F. Added Value of Different Approaches of Real Options in Transportation Infrastructure Projects Decision-Making; TU Delft: Delft, The Netherlands, 2016; pp. 1–10. [Google Scholar]

- Kim, Y.; Shin, K.; Ahn, J.; Lee, E.-B. Probabilistic cash flow-based optimal investment timing using two-color rainbow options valuation for economic sustainability appraisement. Sustainability 2017, 9, 1781. [Google Scholar] [CrossRef] [Green Version]

- Ashuri, B.; Kashani, H.; Molenaar, K.R.; Lee, S.; Lu, J. Risk-neutral pricing approach for evaluating BOT highway projects with government minimum revenue guarantee options. J. Constr. Eng. Manag. 2012, 138, 545–557. [Google Scholar] [CrossRef]

- Shi, J.; Duan, K.; Wen, S.; Zhang, R. Investment valuation model of public rental housing PPP project for private sector: A real option perspective. Sustainability 2019, 11, 1857. [Google Scholar] [CrossRef] [Green Version]

- Sazonov, S.; Ezangina, I.; Makarova, E.; Gorshkova, N.; Vaysbeyn, K. Alternative sources of business development: Mezzanine financing. Sci. Pap. Univ. Pardubice Ser. D Fac. Econ. Adm. 2016, 23, 143–155. [Google Scholar]

- Jain, S. Investing in credit series: Mezzanine debt. UBS Altern. Invest. 2012, 1–15. Available online: https://ssrn.com/abstract=2102859 (accessed on 15 January 2021).

- Silbernagel, C. Mezzanine Finance; Bond Capital: Vancouver, BC, Canada, 2012; p. 8. [Google Scholar]

- Svedik, J.; Tetrevova, L. Mezzanine financing instruments as alternative sources of financing industrial enterprises. In METAL 2014, Proceedings of the 23rd International Conference on Metallurgy and Materials, Brno, Czech Republic, 21–23 May 2014; University of Pardubice: Pardubice, Czech Republic, 2014; pp. 1908–1913. [Google Scholar]

- Hartmann-Wendels, T.; Keienburg, G.; Sievers, S. Adverse selection, investor experience and security choice in venture capital finance: Evidence from Germany. Eur. Financ. Manag. 2011, 17, 464–499. [Google Scholar] [CrossRef]

- Espen-Eckbo, B.; Thorburn, K. Corporate restructuring. Found. Trends Financ. 2012, 7, 159–288. [Google Scholar] [CrossRef]

- Milanesi, G. Teoria de Opciones: Modelos Específicos y Aplicaciones Para Valorar Estrategias, Activos Reales e Instrumentos Financieros; Editorial de la Universidad Nacional del Sur: Bahía Blanca, Argentina, 2013; p. 256. [Google Scholar]

- Lamothe, P.; Mendez, M. Opciones Reales: Métodos de Simulación y Valoración; Ecobook-Editorial del Economista: Madrid, Spain, 2013. [Google Scholar]

- Copeland, T.; Antikarov, V. Real Options: A Practitioner’s Guide; Texere: New York, NY, USA, 2001. [Google Scholar]

- Ruiz, J.; Navarro, J. Valoración y análisis de riesgo para concesiones viales en Colombia marco teórico y desarrollo. Undergraduate’s Thesis, Uniandes, Bogotá, Colombia, 2010. Available online: https://repositorio.uniandes.edu.co/handle/1992/14362 (accessed on 15 January 2021).

- Knoope, M.M.J.; Ramírez, A.; Faaij, A.P.C. The influence of uncertainty in the development of a CO2 infrastructure network. Appl. Energy 2015, 158, 332–347. [Google Scholar] [CrossRef]

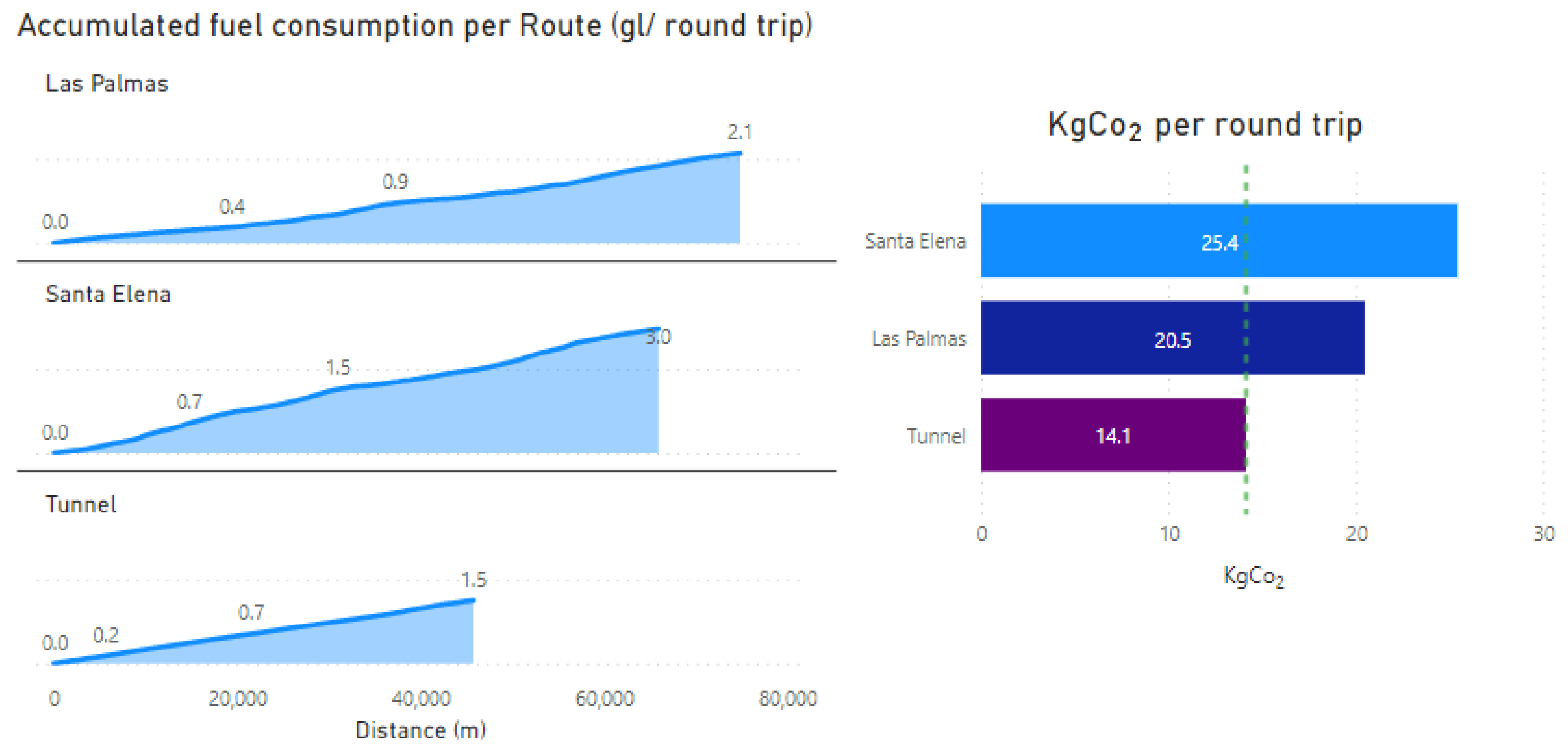

- Posada, J.; Sarmiento, I.; Correa, A. Consumo de Combustible en Camiones Según Peso del Vehículo y Otras Variables; Universidad Nacional de Colombia: Bogotá, Colombia, 2014. [Google Scholar]

- Climate Bonds Initiative. Low Carbon Land Transport and the Climate Bonds Standard (Version 1.0)—Background Paper to Elegibility Criteria. 2017. Available online: https://www.climatebonds.net/files/files/standards/Land%20transport/Land%20Transport%20Criteria%20Version%201%20Feb%202017.pdf (accessed on 10 July 2021).

- Aguilar, L. Modelo de Decisión de Ejercicio de Una Opción de Accionista en Proyectos de Infraestructura Sostenible Bajo un Esquema de Financiación Tipo Mezzanine. Master’s Thesis, Universidad Nacional de Colombia, Bogotá, Columbia, 2020. Available online: https://repositorio.unal.edu.co/handle/unal/78803 (accessed on 15 January 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

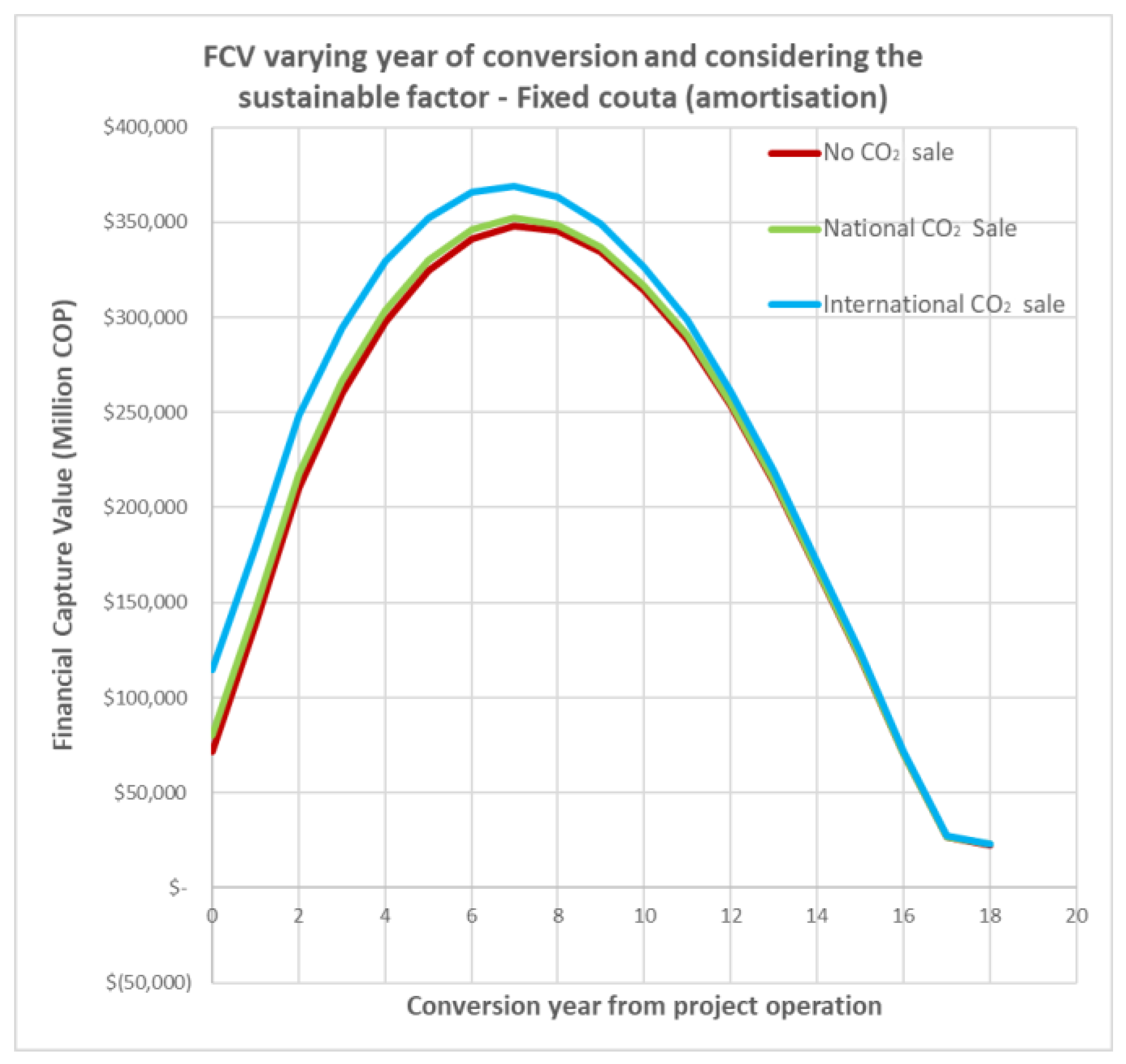

| CO2 Scenario | International Sale | National Sale | No Sale |

|---|---|---|---|

| FCV | $114,947 | $80,027 | $71,650 |

| Tax Rate | 25% | 33% |

|---|---|---|

| NPV FCF | $440,209 | $445,669 |

| FCV | $71,650 | $32,626 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aguilar, L.; González-Ruiz, J.D.; Botero, S. Shareholder Option Valuation in Mezzanine Financing Applied to CO2 Reduction in Sustainable Infrastructure Projects: Application to a Tunnel Road in Medellin, Colombia. Sustainability 2022, 14, 7199. https://doi.org/10.3390/su14127199

Aguilar L, González-Ruiz JD, Botero S. Shareholder Option Valuation in Mezzanine Financing Applied to CO2 Reduction in Sustainable Infrastructure Projects: Application to a Tunnel Road in Medellin, Colombia. Sustainability. 2022; 14(12):7199. https://doi.org/10.3390/su14127199

Chicago/Turabian StyleAguilar, Luis, Juan David González-Ruiz, and Sergio Botero. 2022. "Shareholder Option Valuation in Mezzanine Financing Applied to CO2 Reduction in Sustainable Infrastructure Projects: Application to a Tunnel Road in Medellin, Colombia" Sustainability 14, no. 12: 7199. https://doi.org/10.3390/su14127199

APA StyleAguilar, L., González-Ruiz, J. D., & Botero, S. (2022). Shareholder Option Valuation in Mezzanine Financing Applied to CO2 Reduction in Sustainable Infrastructure Projects: Application to a Tunnel Road in Medellin, Colombia. Sustainability, 14(12), 7199. https://doi.org/10.3390/su14127199