1. Introduction

An efficient system of control is often considered to be one of the guarantors of the efficiency of the management activities that have been undertaken within the scope of each implemented function of an organization, including the function of marketing. Control indicates the areas of marketing with varying degrees of utilization, efficiency, and effectiveness, thereby determining the need for resource allocation, combining various activities and changes in the scope and intensity of activities, and in this way becoming one of the crucial factors determining the level of efficiency of marketing management. This instills an interest in this issue, both in theoretical as well as pragmatic terms. The two approaches are inherently intertwined since, on the one hand, the theory provides a foundation for practical solutions: the methods, techniques, and tools of control. On the other hand, a theory is a generalization of solutions stemming from management practice. Attempts to describe control by way of models constituting the theoretical basis for the implementation solutions seem to be an important element of the theoretical considerations.

The opening of national markets and globalization, involving the movement of production factories to low-cost areas, have influenced corporate strategies on ways to reach and hold global competitiveness. In this approach, new forms of competition have been established as new competitors arise. This has led to a rapid increase in participation of all companies in all global activities, with high involvement. In times of economic crisis, companies begin to evaluate their performance and effectiveness through internal audits. Using unsuitable or wrong metrics seems like a big mistake from the point of view of companies. Companies focus on the comparison of results obtained in previous periods from a point of view that emphasizes the fundamentality of using metrics. As an effect, a comparison of values from different periods arises, for which the various conditions of their achievement are identified. Companies have to monitor their processes and activities no matter the results. These processes and activities must implement individual aspects of marketing activities.

The purpose of the present discussion is to highlight marketing control concepts that have been described in the literature as a relative part of an evaluation of marketing effectiveness. This discussion can be understood to concern marketing control model solutions, reflecting the depth of previous considerations and the implementation control. The research interests of the authors in marketing strategic control prompted them to undertake more extensive investigations focused on theoretical as well as practical aspects of marketing strategic control to describe it.

The purpose of this study was to analyze the relevance of marketing and business activities in connection to performance evaluation in three areas: market, customer, and financial performance. Following the defined purpose of the study, we hypothesized that relationships exist between various observable factors, namely market indicators, financial indicators, and customers’ value indicators. The empirical evidence of the paper came from quantitative, firm-level data gathered through an email questionnaire, which yielded 708 qualified responses from companies in the Czech Republic. The analysis employed factor analysis to identify the key marketing indicators supporting corporate strategy marketing in specific areas. Furthermore, Pearson’s chi-square test was used to identify possible dependencies between observed factors.

This article is divided into separate parts as follows: The first part provides an introduction to the theoretical framework developed in connection to the control of marketing activities. The second part includes the methodology and provides details on data collection and analytical methods. The third part presents the findings of the analyses, and the final section summarizes the conclusions of the study.

2. Theoretical Background

2.1. Control as a Key Function of the Measurement Process

The control as management function should be interpreted in various ways due to the need for descriptions on the general, technical, organizational, and legal levels, where an actual condition is compared to the assumed benchmark or norm, testing the reasons for possible deviations. Control understood in this way has another practical dimension, and it realizes another scope of functions in the management process. The terms that are often assumed to be the equivalents of control (e.g., assessment, verification, evaluation, inspection, vetting, revision), should be perceived as their specific forms, which are embedded in the historical context related to the stages of development of the organization’s environment that necessitated taking the appropriate controlling actions in certain circumstances [

1,

2].

The control of marketing activities focuses on fulfilling requirements on marketing effectiveness. The differences in the perception of control are attributable to its various interpretations within the evolving concepts of management. For obvious reasons, its most expressive place was to be found in the scientific organization of work, where it was regarded to be an inalienable function of management. Highlighting the role of control is apparent in the concept of the organized work cycle, where the action is perceived to be the consequence of thinking. It is considered to be the final element whose role boils down to comparing the result with the previous assumptions, drawing the appropriate conclusions, and making the corrections in the successive stages of the cycle [

3].

The control process is a means and not an end, thus pointing to the necessity of rationalizing the selection of controlling activities and the adequacy of resources in order to reach a sufficient and ultimately the highest possible level of precision, continuity, effectiveness (incurring only the indispensable costs), sufficiency, and promptness of the resultant information [

4].

The need for control of marketing activities was perceived and stressed by the representatives’ view due to the managerial functions and their implementation [

5]. The importance of control has grown in line with the dissemination of Weber’s concept of a bureaucratic organization. In this approach, an organization required the whole system of control to oversee its members, which led to a continuous increase in control. The control process is usually defined as a kind of operating activity in a company environment within subsequent interpretations of corporate internal rules about coordination, task implementations, and influence of individual behavior [

6,

7,

8,

9,

10].

From the systemic (cybernetic) perspective, control is perceived to be comprehensive both at the level of the entire organization (system) and at the level of individual subsystems. The essence of control is seen in analyzing the causes of disordered phenomena in order to avoid them in the future. Ultimately, the image of control as a cybernetic system of regulation has been formed. That system is to lead to the assumed normative solution by monitoring information on the progress and the results of operation, measuring the condition of objects and their determining factors, comparing the current condition of objects with their planned state, interpreting and discriminating between disturbing factors, and taking proper corrective or preventive measures [

11].

The strategic control approach has been derived from the systemic approach, which boils down to the control of the selected elements—the key points, which are granted the status of the strategic elements. Those elements can stimulate or inhibit the operation of the whole organization, affecting its efficiency and effectiveness, and the ability to identify them is one of the crucial skills of good management [

12].

2.2. Control in Marketing Management

The first distinctive consideration on the role of marketing control appeared in the period of marketing formalization. In his analysis of the situation of an organization, in line with the premises of the historical school of management (analysis of the past), Hypps [

13], who followed the historical theory of management (analysis of the past), discussed reaching competitive advantage due to this particular method. This might have been the first attempt to point out the principles and procedures for control (signposts) within the area of marketing. Then, he addressed the system of marketing control, whose goal he described as streamlining the plans, defining problems, correcting errors, measuring results, and studying trends and changes [

14]. In his opinion, control should focus on the assessment of variables that exert a major impact on the execution of three groups of goals related to the market position of a company, organization of marketing, and the result of marketing activity. Hence, he attempted to define the scope of marketing control which would reflect the problems and operation of an organization itself, without reference to the situation of its environment.

The marketing approach professed in the latter half of the past century (the time for paradigm constitution) at first considered marketing to be a business activity, and then it urged the producers to carry on marketing activities, suggesting extending those activities beyond purely commercial dimension. Marketing was perceived to be the basic function of management, which organizes and leads business activity, converting buying propensity of customers into demand, moving goods and services to the end-users, and assuring generation of profit and reaching other goals for companies. Hence, the basic idea to express the new marketing approach was to shift marketing activity to the beginning of the business cycle. By this token, marketing was given a character that integrates the production cycle and sales [

15]. In most cases, control understood in feedback terms embraced monitoring of a marketing program with the use of an appropriately chosen marketing mix [

16,

17]. Irrespective of the applied approach to control, it was assigned a servant role concerning planning, which required defining the degree of goal satisfaction, and/or laying a foundation for planning decisions [

18,

19]. Such approaches that helped to integrate the two functions of management (planning and control) with the managerial function brought about the development of marketing controlling as a separate area of strategic and operational controlling, referring to the implementation of strategic and short-term marketing plans [

20,

21].

The new marketing concepts that emerged in the latter half of the 20th century were the consequence of transformations observed within the business environment (new economy), the theory of economics (new economics), methods of management, and the character and role of market subjects, as well as the re-evaluation of tangible and intangible resources, business models, and the role of marketing within their structures. They led to a new interpretation of control as a process providing knowledge about efficiency, effectiveness, and the efficiency of marketing and allowing adapting to changing conditions or seeking improvement of operations in the future [

22]. A reference to the final aspects of productivity and the outcomes was considered as a key principle of control. The description of the control aimed at securing the achievement of the desired goal distinguishes formal control, i.e., top-down control mechanisms affecting the behavior of the marketing staff (control in the aspect of power) from informal control, i.e., bottom-up control mechanisms initiated directly by the marketing staff (control in the aspect of behavior). In an optimal solution, they should create a combination of mechanisms ensuring, on the one hand, the behavior of the marketing staff in support of the organization’s goals (formal control), and on the other, achieving high morale and coherence of the staff’s values and beliefs (informal control).

The formulated definitions of control explicitly expressed its essence in terms of power, e.g., superiors controlling the behavior of subordinates (personnel) to reach the set goals [

23]. The level of management proper for taking marketing control, the self-contained business units (SBUs) was also signaled, and it was control specified as a set of elements ensuring the personnel fulfills its obligations leading to the implementation of the adopted corporate strategy [

24].

Currently, marketing is understood as a certain marketing operation of a company within the market. In the narrow meaning, it stands for the set of goals and instruments to affect the market. In the broader sense, it expresses a new concept of operation that takes into account the perception of the constituting elements such as the entities entering into mutual relationships, the models of implemented business, and the role of the marketing function with the orientation on market subjects [

25,

26]. The outline of the scope of marketing control for the selected marketing concepts is presented in

Table 1 below.

As the last stage of the management process, control is the apex of all considerations, decisions, and management activities. Its importance in the management process in general, and in marketing in particular, has decisively grown over the past decades. Control per se is considered to be a complex process, in terms of the wide range of issues it deals with and its position bridging the successive cycles of operation. It concludes one cycle of the management process, and at the same time, it becomes the foundation (a point of reference) for the next management cycle. Marketing control should be multidimensional; it should refer to those elements of operation that are the driving force for reaching success on the market. It is a prerequisite for the review and correction of the current plans, goals, and marketing strategies and the formulation of new ones. The basic forms of control focus on the efficiency of allocation of marketing operations and their effectiveness.

Marketing management perceived as a series of processes of decision-making, executive, and control character, being an integral part of an organization’s functioning, is realized at both strategic and operating levels. It includes a full range of typical management functions (starting from the analysis; proceeding through planning, organization, motivation, and implementation; and ending with control, which is a prerequisite of that process because of planning). It includes all the decisions and actions involved in the selection and/or creation and then rational market exploitation as the basic source of revenue of a company [

27]. A complex process requires the greater active participation of all relevant subjects as a core part of the whole strategy [

28].

2.3. Marketing Operational Control

From a general point of view, marketing control should be divided into operational and strategic categories. Most often, operational control is understood to be the valuation of the obtained results relative to the formulated goals (a cybernetic approach, feedback, ex post control) [

29,

30,

31]. Less frequently, it is considered to be the assessment of implementation (current, on-going control) [

29] or the assessment of the changing environment allowing correcting the planned volumes (pre-emptive control) [

32].

The assessment of the marketing environment poised to modify the implemented plans may be regarded to be a bridge between operational and strategic control. Once we treat that assessment as a part of the diagnostic function meant to streamline the currently implemented plans and marketing programs, then it has an operational function. Still, once we look at it from the forecasting perspective, it has a rather strategic value. The scope of operational control is directly attributable to the goals, strategies, standard of operation, and a set of control values that should be specified by marketing plans [

3,

33]. It is recommended to conduct control of sales, marketing expenditure, the impact of marketing expenditure on total sales, and customer satisfaction within the basic controlling measures.

Marketing control efficiency pertains to the assessment of relations between the basic control values—the results and expenditure considered in various cross-sections. Most frequently, controlling values showing the results are turnover, sales, and financial results, while the values showing expenditure include functional costs such as sales, promotion, distribution, packaging, branding, and relation building. Control should consider a few types of costs, i.e., the direct costs (directly related to particular elements of the cross-sections), determinable overheads (i.e., the costs that can be determined with the known parameters related to the conducted marketing activity), and undetermined overheads (those attributable to particular components in an arbitrary, subjective, or abstract manner) [

34]. Control results help a company to supervise corporate performance and effectiveness in the marketing area on the way to achieve corporate goals [

14].

Effectiveness of marketing activities is defined as the return on financial sources spent on realized marketing activities. To verify the return rate, many possible methods have been invented. Companies must prioritize the measurement of marketing effectiveness through marketing metrics. Marketing metrics help to create a measurement system for the quantification of possible trends, dynamics, or characteristics of individual marketing activities. Strictness and objectivity must be necessarily observed to be able to compare monitoring at various times and various places [

35]. Measurement of the performance of marketing activities represents a corporate process, which provides performance feedback about marketing results. Corporate performance is becoming an important part of the corporate budget procedure, performance substitutes, and promotion [

36,

37]. Measurement of the effectiveness of marketing activities strongly depends on and is strongly influenced by a group of factors. These factors are considered as requirements for the successful implementation of marketing plans at different corporate levels. Target factors are marketing strategy, marketing creativity, a realization of marketing activities, marketing infrastructure, and external factors [

38,

39].

It is worth noting that marketing operational control is mostly based on the external data that are generated due to the information provided by the company. That is quite convenient, if the information is continually recorded, aggregated, appropriately processed, and made available [

40,

41,

42]. The final marketing operational control should help managers to make the on-going assessments of marketing operations effectiveness along various cross-sections and profitability of such activity, which ultimately facilitates the assessment of marketing function effectiveness [

43,

44].

The logic of such conduct seems to reflect the process of a classic control activity. Its implementation should be facilitated by the character of data (internal, secondary), which is a prerequisite for making the assessment. Nonetheless, as pointed out by numerous researchers dealing with sales management, the assessment may be difficult to make due to the acquisition of aggregate data for the whole organization, and not just the cross-sections desired for the marketing assessment. This is particularly true when the categories of incurred expenditures are considered. Problems also emerge with the use of data provided by the accounting and financial sections, since they are not always available in their original form (as they are processed, aggregated, or purged) and with the delays in access to the indispensable data. Many flaws and impediments are currently minimized due to more and more efficient computer solutions. However, as shown by the process of setting up an integrated system, fully useful for all organizational units, that would be functional and user-friendly (available to users who are not fully conversant with technology), this is a very difficult task that is costly (as in most cases it needs individual solutions) and not always rational [

3].

2.4. Marketing Strategic Control

Strategic control embracing all the adopted provisions (directions, forecasts, adopted policies for marketing operations) that is the basis for an update or elaboration of a new marketing strategy for a company [

45] should follow the systematic operational marketing control. The description of the marketing control structure at a strategic level includes the following [

34,

46,

47]:

An assessment of marketing accuracy;

An assessment of marketing excellence;

A marketing audit;

A review of the ethical and social responsibility of the company.

Marketing control has been tasked with the assessment of meeting the implementation of five elements of the marketing concept: philosophy of operation, organizational integration, relevance of information, strategic orientation, and efficiency of operation. Marketing control can only produce a very superficial assessment of the correctness of marketing concept implementation in an organization, answering the question of whether an entity demonstrates key and prerequisite characteristics that would qualify its stance as a marketing orientation. When the evaluation of the correctness of the marketing concept is not positive, this should strongly suggest implementing other strategic control tools, such as the marketing audit procedure. The evaluation of marketing excellence is one step further in the strategic evaluation of marketing correctness. With this control tool, companies can gradually employ the concept of marketing by applying the comparative analysis (e.g., benchmarking technique). A major issue of this seems to be finding the benchmark for comparisons, in line with the solutions proposed by benchmarking [

48,

49].

The marketing audit is another step in the strategic control, which is understood to be a comprehensive, systematic, independent, regular, and professional study of the marketing environment and the goals, strategies, and operations of an entity (a company, SBU, an institution) and is conducted to identify the correctness of strategic marketing decision implementation.

The need for social responsibility control includes the three areas: legal (respecting the law), ethical (integrity respecting the rights of the stakeholders), behavioral (conscious, voluntary responsibility in contacts with the company stakeholders). It draws attention to the fact that the changes taking place in a socio-economic, cultural, and natural environment in the contemporary world impose significant limitations on marketing activity that cannot be ignored for the good of the company and its all stakeholders (individual and collective) [

34].

The literature presents other forms of marketing control structure, in which the subject of control, and not the level of controlling activity, has become the distinguishing criterion [

50]. One proposal lists six levels of control and marketing evaluation [

51]:

A comprehensive marketing plan and marketing strategy (Does it exist, and is it implemented? If the answer is affirmative, is it implemented well? Has the implemented strategy been effective in changing market conditions?);

Profit centers and SBUs (Have the centers for generating financial benefits been identified? Have the strategic recommendations been adapted to the situation of SBUs?)

Marketing programs engaged in the implementation of the marketing strategy (How are properly prepared programs consistent with the general strategy of the company? How efficient and effective is the marketing mix for each program? (In case every program is perceived to be self-contained, then the marketing mix for each program should be audited in terms of costs and effectiveness.));

Marketing tactics prerequisite for the implementation of programs within some operations or marketing functions (tools);

Personnel responsible for the development and implementation of programs and tactics (control of (1) the standards related to precise values such as the volume of sales or the share in profit; (2) “soft” provisions including such factors as personality, character, initiative, righteousness, and organizational skills; and (3) task norms that are directly connected with short-term issues of the implemented projects);

Market surrounding (competitive) subjects, including the recipients of the offer, suppliers, subcontractors, and middlemen (their “usefulness”, efficiency, effectiveness, flexibility, communication skills, etc.).

The assumption of marketing control made from the angle of value marketing establishes that the ultimate test of investment in marketing is whether it delivers value to the shareholders. Such an approach brought about a three-level model of marketing efficiency measurement. The first level refers to marketing strategy, and it discusses its role in generating shareholder value; i.e., it shows how marketing decisions (understood as the decisions on the selection of the target market and its service) raised or lowered that value [

52,

53].

Such a strategic approach to the assessment of marketing efficiency involves a provision stating that marketing permeates all economic activity of a company. In this way, it becomes a way of management rather than a separate function [

54]. The second (tactical) level combines marketing activity with the results. It is also assumed that it is not feasible to separate the impact of investment in marketing from the obtained results. Hence, any attempts to evaluate the profitability of such investment are not substantiated or proper from the methodological perspective. That is because the results of expenditure (outlays, costs) incurred on marketing may accumulate with other types of investment and/or may be deferred in time.

The third operational level refers to concrete marketing activities such as promotion, branding, and distribution. At this stage, an assessment is made of the impact of the expenditure incurred on the concrete elements of marketing activity (marketing mix) on sales and, in a fuller perspective, on the market share and share price. All these levels contribute to full, precise control of the activity on the market and constitute an important premise of the marketing audit control process.

2.5. The Conceptual Approach to Strategic Marketing Control

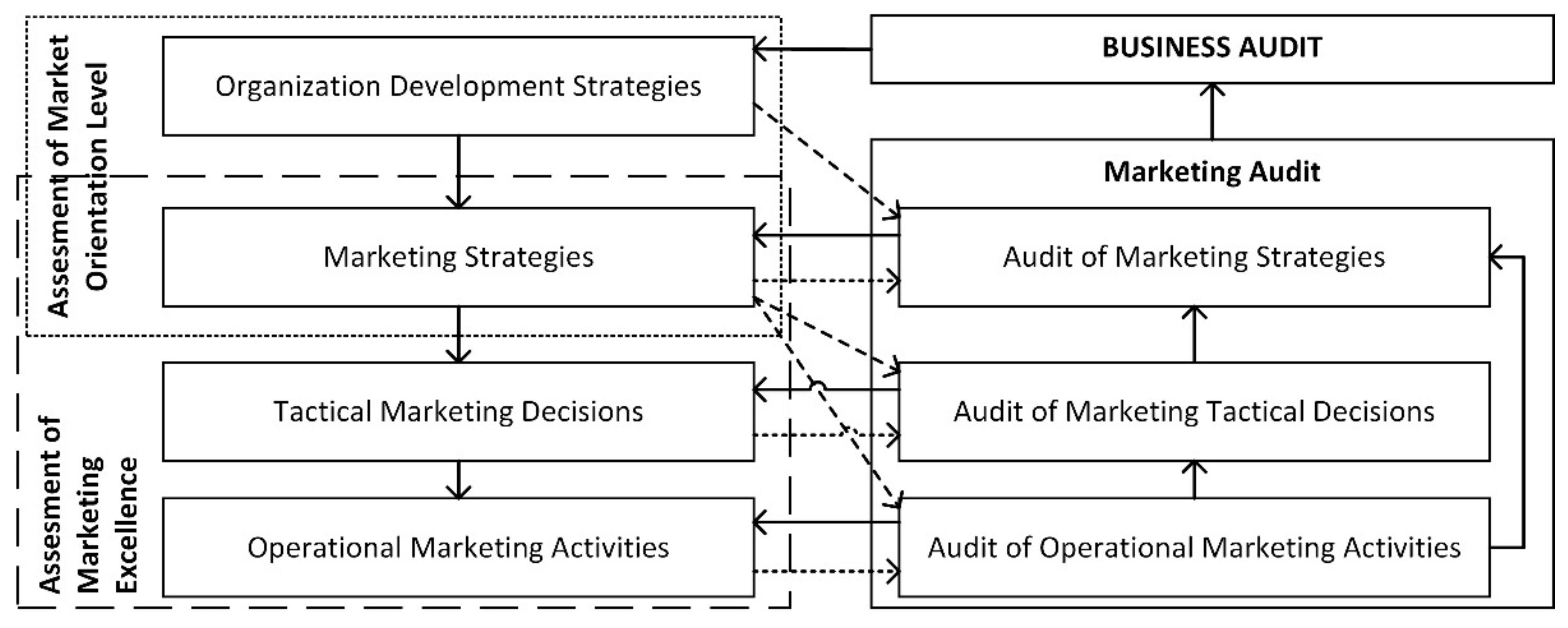

By referring to the foregoing concept of the description of marketing control, which is a distinctive level of strategic control, we may present a concept of its model reflecting its logically complex character (see

Figure 1).

Our point of departure, i.e., the first level of control, should be a look at the level of marketing orientation of a company, once it has been adopted to be a concept of market impact appropriate for a given company. Such control should not be poised to identify the market orientation of a company, but to answer the following question: what is the degree of implementation of its principles? In the case of another orientation of a company, the objective of control seems unjustified. This does not preclude marketing activity assessment at the subsequent levels of control. Then, it seems reasonable to proceed with the control at the second and third levels. Naturally, it is a prerequisite to adopt the appropriate points of reference for the relative comparison (i.e., such objects where marketing has become one of many functions implemented in a company, and it is not one dominant feature) as well as proper assessment criteria.

By the same token, a consideration of whether marketing orientation was rightly selected to become a concept for the development of a company is equally futile. That issue is assessed at a higher level of company management. Making such a decision should be analyzed within a wider context of prerequisites that go far beyond marketing considerations. Having said that, it does not seem right to “put the blame” for such an assessment on the area of marketing. In turn, the marketing orientation of a company demands pointing out the directions for operation employing a marketing strategy, one way or another. It is a prerequisite and proper point of reference for the research and the decisions made at the subsequent levels of strategic control.

Satisfactory assessment of marketing orientation should be the stepping-stone for the transition to the second level of strategic control, i.e., the assessment of marketing excellence. Its goal is a relative assessment of the marketing organizations’ activity—their scope and results. The relative character of the assessment allows determining specific problems of an organization, the objective conditions for the functioning of the whole market (a sector, industry, or strategic group), assuming that a comparison is made concerning the entities functioning within the competitive surroundings of an organization, and not just the theoretical model constructs. In particular, the unsatisfactory results of the relative assessment of the implementation of various marketing elements should prompt transition to the level of more thorough control, i.e., marketing. That level of control should be substantiated by the assessments of the mismatch of activities to the marketing concept diagnosed at the earlier level of strategic control and/or relative imperfection of those activities. If this is not the case, the legitimacy of the audit control may be put in doubt.

3. Materials and Methods

According to the specification of Ambler [

55], Muchiri et al. [

56], and Hornungová [

57], it is necessary to focus on three main areas that provide a relevant competitive advantage for the company, especially in the role of the seller. The choice of marketing activities is an entire part of the marketing management process in the company, and these activities must be connected to required corporate performance. Specification of these activities is compound and theoretically significant, and it is usually influenced by several managerial approaches. Description of individual activities is under the possibility of classification activities. In general, aspects of time (time aspect is done at three levels, namely strategic, tactical, and operative), product life cycle, market character, or product specification are applied. Requirements of the stakeholders for the company and its long-term profitability are in close connection to the choice of marketing activities and sequential realization.

The main objective of the paper is to define key factors in individual areas (market area, area of customer’s value, financial area), connected to business activities, and show their interconnection. To support the main objective, the partial aim of the paper was defined. The partial aim is the definition of possible relationships between observed factors. According to the partial objective of the paper, the hypothesis was stated: “there exists dependence between the realization of individual business activities and their performance”. All data were processed by the employment of the statistical program IBM SPSS Statistics 25 under the application of the following statistical tests:

3.1. Variable Definition

Marketing metrics are determined to identify the effectiveness of marketing activities in the company. Various types, depending on the field of activity of the company, can be considered as key marketing metrics. The reason is the very high complexity of certain metrics. The most suitable way to guarantee quality measurement of fields, which the company considers as key, is the use of metrics portfolio in harmony with the needs of a particular company [

58]. Marketing metrics should be classified from many points of view. Concerning the involvement of metrics in various groups, the passing of individual metrics is obvious.

The most common classification is by financial description—into nonfinancial metrics and financial metrics. These groups are based on traditional performance monitoring, comparing results of past periods. In general, financial metrics are used as traditional indicators and specific applications are used as modern indicators. However, when only the visualization of the past was made, results lacked elements of warning in case of unfavorable development. The use of a certain warning system, providing timely information about possible development by potential success or failure, has been described [

59]. Individual variables, which we used for evaluation of all three areas (market, customer, financial), are as follows:

Market area: xM1—market share; xM2—SBU market share; xM3—relative market share; xM4—category development index; xM5—market penetration; xM6—brand penetration; xM7—purchase reasons; xM8—loyalty; xM9—customer satisfaction; xM10—product cannibalization level; xM11—number of customers; xM12—monitoring in wide audience.

Area of customer’s value: xC1—profit per customer; xC2—customer’s lifetime value; xC3—average costs of acquisition; xC4—average costs for keeping customer; xC5—cost for 1000 asked; xC6—costs per click; xC7—costs per order.

Financial area: xF1—price elasticity; xF2—profit %; xF3—variable and fixed costs; xF4—marketing expenses; xF5—break-even point; xF6—net profit; xF7—return on sale (ROS); xF8—earnings before interest, taxes, depreciation, and amortization (EBITDA); xF9—economic value added (EVA); xF10—return on marketing investment (ROMI); xF11—return on investment (ROI).

For the research, a questionnaire survey was employed. This survey was focused on a corporate area of realization of their business and marketing activities and their connection to the area of corporate effectiveness and usage of business models. According to the number of all possible answers to the questions included, the length of the questionnaire was 23 pages and it included over 300 variables.

3.2. Sample Description

The basic population is defined as technology companies that operate in the Czech Republic. Respondents to the questionnaire survey were managers of the surveyed companies, who were responsible for marketing activities. Companies were selected randomly from the statistical register of economic activities. For the research, we sent the survey to 2627 companies. In total, 708 forms were returned with valid answers (i.e., completely and correctly filled), for a return rate of 26.95%.

3.3. Methods

We applied exploratory factor analysis to define key composite indicators on the way of controlling marketing activities. As the compute method in factor analysis, varimax rotation was used. The applicability of factor analysis was verified by two relevant tests. The first test was the Kaiser–Meier–Olkin (KMO) test. The KMO coefficient has values in interval 〈0; 1〉 and is defined as the rate of correlation coefficient and the sum of squares of correlations within the partial coefficient. The second test was Bartlett’s sphericity test, which evaluates the null hypothesis within the identity matrix [

60,

61].

In the requirement of evaluation factors, relevant formulas have to be defined through a calculation of factor loadings of variables at the input. The values of factor loadings were taken from the component matrix and were changed in value proportion with a sum equal to 1. New loading values exemplified the weight of the variable in the factor. In processing, there were uninvolved variables, which change a defined factor, but only such a single variable item. Of the 30 variables, six items had a lower loading value under 0.5 and were thus excluded (see

Table 2).

Definition of factor formula is based on following relations:

where w

i is defined as the calculated weight of the variable (its loading value), x

i is an abbreviation of variable as input to factor analysis, and i is a total number of variables at the input.

As the score for verification of factor analysis application, Cronbach’s alpha indicator was applied. This indicator is a coefficient of consistency and reliability of items in a factor (according to verification of dimensionality as part of exploratory factor analysis). The value of Cronbach’s alpha refers to the intercorrelation among the items [

62,

63].

This indicator refers to the relevant reliability of factor analysis with a close connection to the correlation coefficient. This score has the interval 〈0; 1〉, where a value close to 0 refers to a situation without a correlation of the variable to others. If the value is close to 1, there is a strong correlation of the variable to others. In a situation where the value is under 0.5, the internal consistency signifies a bad level. In the case of a value level close to 0.7, the defining factor should be considered acceptable and very significant. Values close to 1.0 are excellent. Applications of Cronbach’s alpha include the confirmation of measuring a latent construct of a factor [

64,

65].

3.4. Data Collection

The paper builds on survey data collected in the Czech Republic, which is considered a rapidly growing economy. This survey was realized from November 2019 to July 2020. The research for the paper was realized in the precrisis period before the COVID-19 pandemic based on quantitative data through an email questionnaire. The sample population comprised companies operating in the Czech Republic. Operation in the Czech Republic was the only key parameter for choice across the industries. Companies were selected randomly from the statistical register of economic activities. For the research, we sent the survey to 2627 companies. In total, 708 forms were returned with valid answers (i.e., completely and correctly filled), for a return rate of 26.95%. The respondents in the questionnaire were managers of the companies, who were responsible for marketing and business activities. In the questionnaire, respondents answered questions regarding their level of business and marketing activities in their company in connection to the knowledge of marketing-related topics; a dichotomous scale score (variable with Yes/No answer) was applied. All respondents were competent and reliable according to their organizational decision-making process and their organizational level [

66].

4. Results

Marketing management and its activities must be divided into three groups (as shown in

Section 3), which were put into the reduction process due to the application of factor analysis. The base for the employment of factor analysis is the correlation matrix of an individual number of items, which support the effectiveness of marketing activities in the company. For the analyses of the market indicators, 12 items were included. In connection with the customer’s value, we used seven variables. Finally, to define financial factors, 11 items were chosen. Therefore, there three different correlation matrixes of the total of 30 items were examined, leading to the evaluation of the effectiveness of marketing activities. Logically, from the application of factor analyses, it is rational to expect a situation in which input variables are reduced to a better set of variables according to possible dimensions. The factor analyses were in exploratory form with the application of varimax rotation, which leads to a reduction in the count of variables for a relevant explanation of marketing activities. The evaluation process in the exploratory factor analysis requires defining several important criteria, interpreting the relevance of application factor analysis. The total variance explained (value must be equal or higher than 0.50), the factor loading (value must be equal or higher than 0.50), and the internal consistency of the obtained factor due to Cronbach’s alpha score were applied [

60,

61].

The result of the Kaiser–Meyer–Olkin (KMO) index of sampling adequacy was above the recommended cut-off point of 0.50. The significance of factor analysis was declared by the Bartlett’s test value of 0.000, which confirms adequate usage. The values obtained for individual areas are as follows:

Market area: KMO = 0.796; Bartlett’s test = 0.000;

Area of customer’s value: KMO = 0.699; Bartlett’s test = 0.000;

Financial area: KMO = 0.843; Bartlett’s test = 0.000.

All of these KMO values corroborate the possibility to apply factor analysis on chosen indicators, which is followed by verification of values in Bartlett’s test. The application of Cronbach’s alpha score allowed us to confirm the relevance of extracted factors, representing individual input variables. According to all defined areas, individual factors and their Cronbach’s alpha scores were stated [

63,

64]. Individual factors include basic variables, which are used to evaluate marketing activities and support marketing management at the strategic level.

4.1. Factors in the Market Area

Results of factor analysis in the market area give three factors, from which two of them have acceptable values of Cronbach’s alpha only. Cronbach’s alpha is 0.641 (acceptable) for factor 1 and 0.546 (acceptable) factor 2. The last factor has Cronbach’s alpha value of 0.441, which is under the minimal acceptable value (under 0.500); therefore, it is not accepted. Final values for calculating acceptable factors need the transformation of individual coefficients. These coefficients express the significance of the used elements (see

Table 3). Their total sum must be 1.

Formulas for individual acceptable factors are based on values in the component matrix. They are expressed as follows:

These formulas can be defined for each company that looks after the measurement of marketing activities. All factors reflect requirements on effectiveness in the market area by the application of relevant indicators.

4.2. Factors of Customer’s Value

Results of factor analysis in the area of customer’s value provide two factors, of which one has an acceptable value of Cronbach’s alpha. Cronbach’s alpha for factor 1 is 0.553 (acceptable). The second factor (factor 2) has Cronbach’s alpha value of 0.491, which is under minimal acceptable value (under 0.500); therefore, it is not accepted. Final values for calculating acceptable factors need the transformation of individual coefficients. These coefficients express the significance of the used elements (see

Table 4). Their total sum must be 1.

The formula for the individual acceptable factor is based on values in the component matrix. The factor is expressed as follows:

These formulas can be defined for each company that looks after the measurement of marketing activities. All factors reflect requirements on effectiveness in the context of the delivery of customer’s value by the application of relevant indicators.

4.3. Factors in Financial Area

Results of factor analysis in the financial area give two factors, which have acceptable values of Cronbach’s alpha. Cronbach’s alpha is 0.776 (acceptable) for factor 1 and 0.577 (acceptable) for factor 2. Final values for calculating acceptable factors need the transformation of individual coefficients. These coefficients express the significance of the used elements (see

Table 5). Their total sum must be 1.

Formulas for individual acceptable factors are based on values in the component matrix. The factors are expressed as follows:

These formulas can be defined for each company that looks after the measurement of marketing activities. All factors reflect requirements on effectiveness in the financial area by application of relevant indicators. For all obtained factors, individual formulas were defined, providing exact value in a specific area. These factors should be considered as basic requirements to achieve defined corporate objectives. By stated factors, companies could develop the progress of their business activities to meet the requirements of long-term sustainability. For defined factors, descriptive statistics were calculated; individual values are shown in

Table 6.

All factors obtained by the application of factor analysis can be defined by any company that wants to evaluate its business activities by using a relevant tool. By obtained factors’ values, all companies can compare their results with their old data in a long-term process of improvement. The importance of such business activities should be considered a crucial area in a company on the way to being more sustainable and achieving defined corporate strategy objectives.

There could be a problem in the definition of a factor with higher importance. Besides, there is a question as to whether a connection exists between individual factors. Therefore, we used the Pearson chi-square test to evaluate possible dependencies between two variables. Application of the Pearson chi-square test requires pivot tables as the estimation. Obtained results of the dependence of individual variable categories are presented in

Table 7. By processing of data in case of reliability, almost all significance values for possible relationships were found to be under the limit of 0.05 [

67]. Only one relationship did not reach significance under limitation—that between F

M1 and F

F2, which provides a 0.207 significance level.

5. Discussion

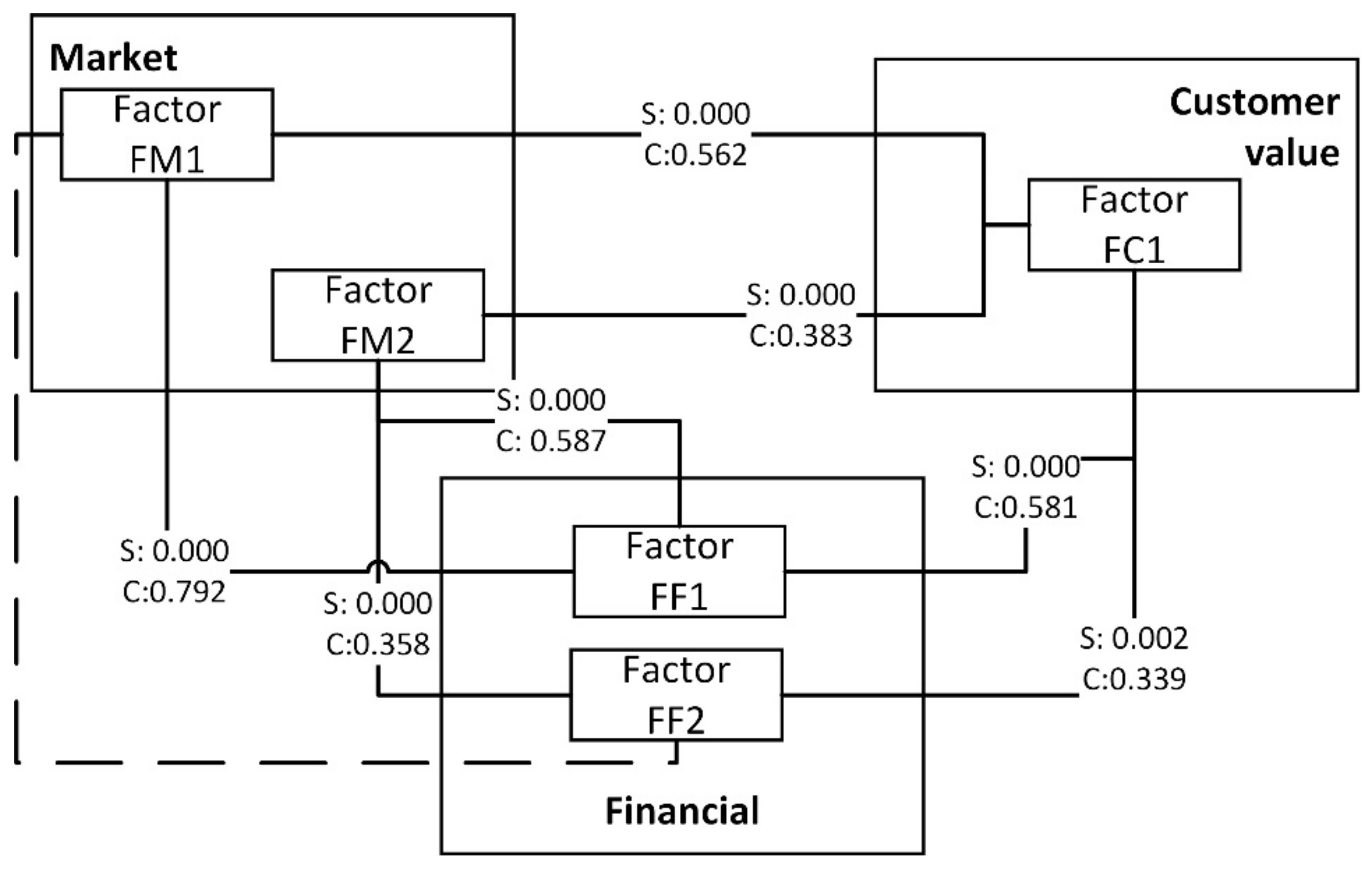

The results bring us to the conclusion that an alternative hypothesis should be applied—there are dependencies between all observed factors, except FM1 and FC1. Subsequently, the degree of such dependence was examined. To that end, the intensity of dependence employing the contingency coefficient was defined for all relationships. For each relationship and observed dependence, the defined contingency coefficient was defined as the intensity of two variables. The intensity of dependence is in the interval 〈0; 1〉. In the case of a higher absolute value, the intensity of dependence is greater. Levels of the intensity of dependence between observed factors are defined as follows:

Values within the interval (0; 0.25〉 have an intensity of dependence that is low and weak, and they do not need to be under continued monitoring (none);

Values within the interval (0.25; 0.5〉 reach rather low dependence between two variables and become more interesting for monitoring (FM2 and FC1 = 0.383; FM2 and FF2 = 0.358; FC1 and FF2 = 0.339);

Values within the interval (0.5; 0.75〉 show strong dependences and represent important fields for observation (FM1 and FC1 = 0.562; FM2 and FF1 = 0.587; FC1 and FF1 = 0.581);

Values within the interval (0.75; 1.0〉 show strong dependences and should be regarded as crucial (FM1 and FF1 = 0.792).

All connections observed between individual factors are shown in

Figure 2. The scheme in

Figure 2 includes determining connections between individual obtained factors. These connections represent dependencies between two factors and their intensity due to contingency coefficients. The lowest power of the dependence is for the FF2 and FC1 factor pair. The highest dependence value is between factor FM1 and factor FF1. The connection between market and customer is described by the dependence value the for FM1 and FC1 factor pair.

The important part of the evaluation process is continuous control of marketing activities’ relevance. Such control should be followed by a correction of identified imperfections with subsequent repetition of the whole cycle. For the control, it is important to accomplish the following objectives:

Appointing a person responsible for control;

Continuously monitoring and evaluating realized marketing activities;

Registering carried-out controls;

Innovating for continuous improvement of the effectiveness of marketing activities.

Our results of factor analysis relate to the conclusions of Tuan [

38]. He mentions the necessity of defining corporate strategy profitably concerning the internal organization of the company, relevant information sources in connection to adequate marketing activities, and marketing effectiveness. To achieve marketing effectiveness, five factors must be applied, namely relevant marketing strategy, setup of marketing creativity, suitable execution of marketing activities, adequate marketing infrastructure, and exogenous factors. Moreover, marketing effectiveness is defined as an efficient application of marketing strategy to relevant marketing activities directed towards meeting customers and building a strong brand.

Similar areas are defined by Zhang and Watson [

2] as key parts for a definition of the marketing ecosystem. The marketing ecosystem represents an open system, which consists of various perspectives of business activities, which are connected to diverse stakeholders’ requirements. The purpose of the marketing ecosystem is supported by many strengths that are developed from the corporate strategy with connection to the marketing area and corroborate market awareness to reach greater effectiveness.

Our results are in agreement with those of Mintz et al. [

68], who present the significance of all groups affecting the performance of marketing activities—market, customer, and financial areas. These areas of effectiveness with relevant impact on marketing mix suggest possible implications on the mindset of customers and managers. It is important to apply combination metrics to get a complex view of application marketing activities. By adequate realization of marketing activities and application of relevant measuring metrics, the company could reach a sustainable marketing system with correct relationships with all stakeholders, not only between subjects in the market but also with employees, owners, and so on [

69].

Management of corporate performance can be defined as a system that uses information for the introduction of optimal changes in organizational structure, systems, and processes to reach an optimal accord between performance objectives and resource allocation, report to top management about corporate strategy changes, or share observed results for individual partial objectives. This system would be able to monitor and control the strategy implementation process [

70]. Measurement of corporate performance is dependent on the requirements of stakeholders, who usually want to maximize their profit. Nevertheless, such maximization is also dependent on the actual corporate health, achievement of defined objectives, and global economic situation in the target market [

71].

Without any stakeholder interest, it is important to have a designed benchmark that is used to determine effectiveness and evaluate results. Achievement of efficiency and effectiveness of the company is based on appropriate levels of corporate strategy. This relationship is influenced by the external corporate environment and organizational structure of the company, among other factors. The external environment includes three basic elements [

72]:

Dynamic of innovative processes;

Difficulties in production and marketing techniques;

Level of competitiveness.

6. Conclusions

Strategic indications and decisions and tactical as well as operational activity can be evaluated only with a formulation of their theoretical basis. Control, the results of which would be nothing but the result of the taken action, without reference to the binding or planned strategic decisions, could be perceived as tactical control at best, and most often as operational control (irrespective of their significance or the complexity of time horizon, they are considered to be the symptoms of a strategic character). This is because a proper assessment of those decisions and actions depends on the internal situation of a company (the resources, market position, and competitive advantage) and the situation in its environment (both near and distant). That is why the assessment of relationships between the strategic decisions made, their resultant actions, and their determinants in endo- and exogenous areas is the key to proper control. The sense and the form of these relationships are dependent on the subject of control, and the control of the match of marketing strategy to the current macro- and microenvironment of a company is a special case. One way or another, a marketing strategy should be an integral element of reference for each marketing strategic control. It should be asserted that the results of marketing control do not pertain to the assessment of absolute states of the studied marketing areas, but the relationships between these states and the defined goals and directions of the development of strategic marketing in a company, taking into account the internal and external conditions of the company functioning.

Control is apparent in every statement that advocates striving to reach the goal (customer satisfaction, profit, developing the range of products, etc.) or taking concrete steps (creating customers, markets, launching new products, shaping the price, distribution, assortment, and promotional policy). Each of the above requires determining the ultimate result of the procedure. Such reasoning limits a wider interest in the specified control stage. At the same time, the managerial approach to marketing designates new areas for its control, inter alia the ability to integrate various business functions under the umbrella of marketing, the ability to shape demand and transform it into purchasing acts, and the ability to generate the desired market and economic results.

The main objective of the paper was to define key factors in individual areas (market area, area of customer’s value, financial area) connected to business activities and show their interconnection. To support the main objective, the partial aim of the paper was defined. The partial aim was the definition of possible relationships between observed factors. According to the partial objective of the paper, a hypothesis was stated: “there exists dependence between the realization of individual business activities and their performance”. The purpose of the paper was to analyze the relevance of marketing and business activities in connection to the performance evaluation in three areas: market, customer, and financial. There is a problem with the definition of the measuring indicator set. From a general point of view, there is no universal set of indicators, not only in the financial area but also in all relevant areas in a company [

73,

74]. If the company makes a correct choice of relevant metrics for measuring marketing activities, their realization moves to the minds of managers, leading to long-term sustainability, and the company transforms its environment according to the concept of Society 5.0 [

36,

75].

Proved empirical research due to the application of factor analysis reduced individual activities. According to the results of the research, we can mention five new factors, which include key indicators in chosen areas. We identified two factors in the market area, one factor in the customer’s value area, and two factors in the financial area. Individual variable indicators are as follows:

All obtained factors were evaluated by Pearson’s chi-square test for independence. From eight relations of observed factors, seven connections were verified, all reaching significance values within 5% of the limit of error. One connection was over the 5% significance value. The intensities of all dependencies were in the range from 0.339 to 0.792.

A primary limitation of this paper is the focus on companies operating in the Czech Republic. The next specific barrier is due to the application of the dichotomic variable (Yes/No answer) in the questionnaire survey, which could lead to misinterpretation at a certain level. Improved results could be reached in case of elimination of such barriers. The best way to identify the index of the factor is the use of a particular value of the metrics. However, such value would be obtained mainly from accounting sheets employing financial metrics. On the contrary, nonfinancial metrics do not contain any specific value. The kind of limitation could depend on the specificity of the measuring habits in the company. The best results can be obtained by a company inputting correct results of financial indicators. There could be a problem with the values because each industry should have specific values. In the case of the usage of nonfinancial indicators, there is the problem of indicators having no general scale for measuring. This is because many nonfinancial indicators are connected to the corporate environment and particularity of industry.

Based on factor analyses of both financial and nonfinancial metrics groups, key metrics were found; these metrics must be used by companies in almost all cases of the effectiveness verification process. According to Horák et al. [

76], financial and nonfinancial indicators play important roles in the explanation of corporate health and support a company’s possibilities of reaching relevant performance levels. The health of a company is given not only by its financial results but also by nonfinancial results in connection to the environment [

77].

If a company requires monitoring of marketing activities’ effectiveness, it is necessary to define these activities in the right way. This way is linked with stakeholder’s knowledge (their wishes and needs) and awareness of corporate goals. These key activities in the marketing area are under regular and periodical effectiveness measuring. All areas in the company, in connection to marketing activities, are focused mainly on customer value creation. If a company could understand their needs, then it may fulfill these needs in a better way. To observe individual activities, a company must (1) use market research to determine customer’s requirements and the requirements of the rest of the stakeholders and (2) maintain relationships with individual stakeholder groups.

We defined descriptive statistics for observed factors, which represent value in individual records. It is possible to consider these values as characteristics of relations within factors. This determination is made by the answer scale in the questionnaire (see

Table 6).

It should be appropriate to use the same answer scale as was used in the survey for index modification. For comparison of individual results within descriptive statistics, these answers must be put as variables into index formulas due to the comparison of corporate results and factor descriptive statistics showing the reached effectiveness level of realized activities. If the factor value is higher than the mean, the company has effective marketing activities. If an index is lower than the mean, the company realizes marketing activities in a noneffective way and must improve these activities. In the evaluation process and comparison of the results, it is necessary to achieve the following objectives:

Defining responsible person for effectiveness evaluation;

Preparing evaluation report;

Giving evaluation reports to responsible persons.

An important part of the evaluation process is continuous control of marketing activities’ relevance. All defects observed during control must be corrected. Then, it is important to apply the whole control process. In the evaluation process and comparison of the results, it is necessary to achieve the following objectives:

Defining responsible person for control;

Continuous monitoring and scoring of realized marketing activities;

Obtaining evidence of control;

Developing innovations for continuous effectiveness of marketing activities.

{kind=link}

{kind=link}