Digital Transformation in Banking: A Managerial Perspective on Barriers to Change

Abstract

1. Introduction

2. Literature Review

3. Methodology

3.1. Data

3.1.1. Interview Process

3.1.2. Data Preparation

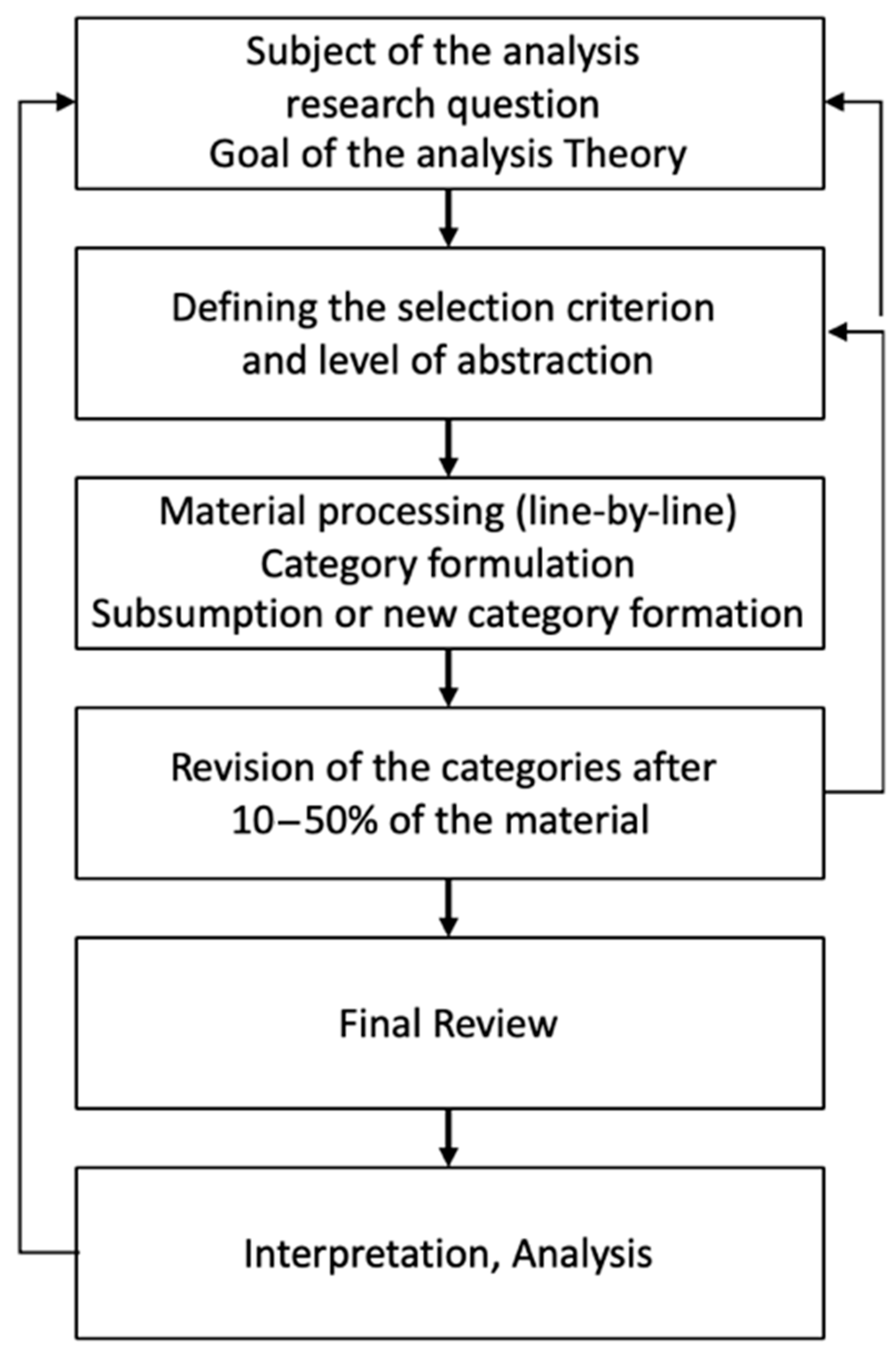

3.2. Analysis Procedure

3.3. Structure of the Interview Guideline

3.4. Conducting the Survey

4. Qualitative Evaluation

4.1. Consistency of Coding

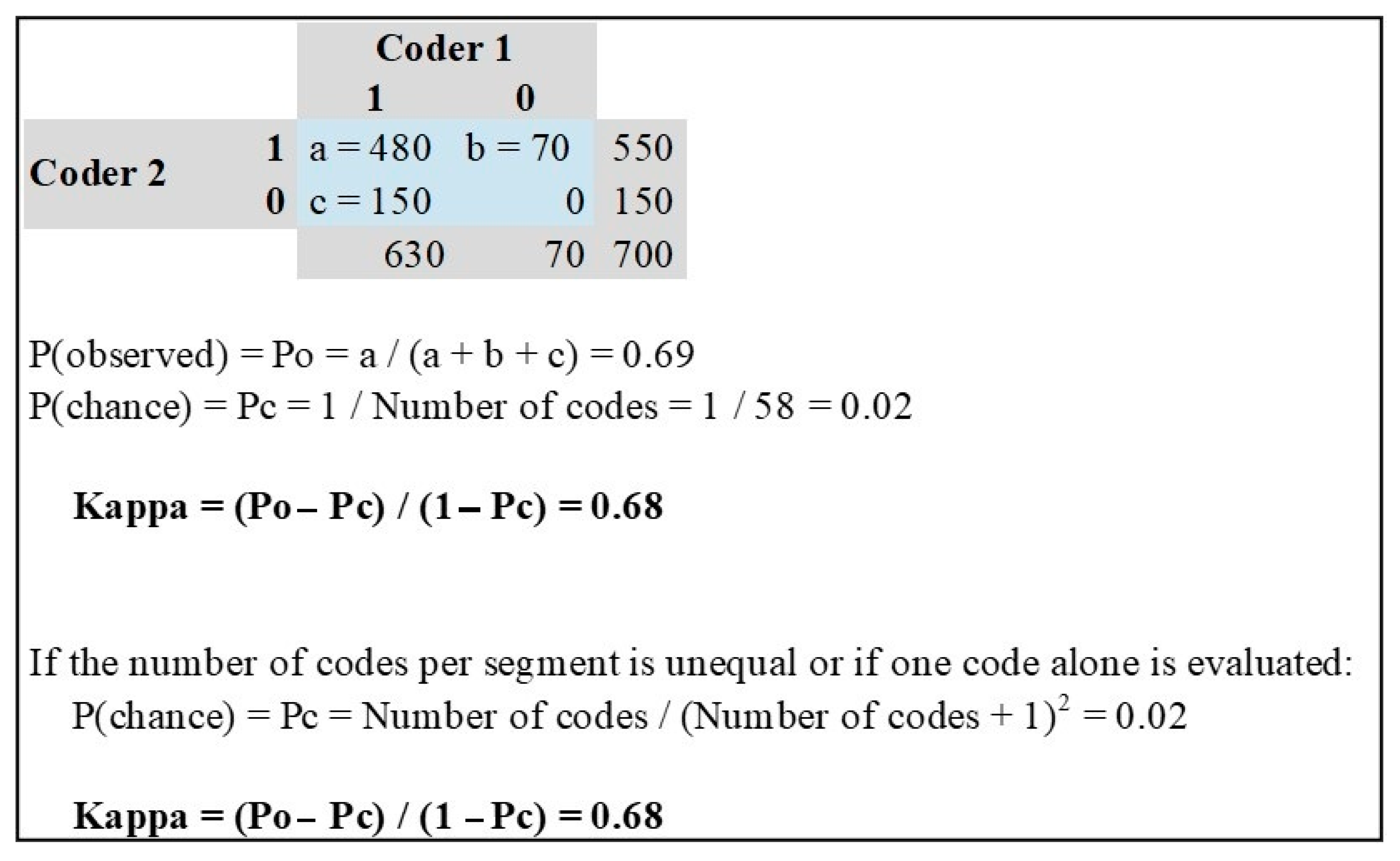

- A qualitative path by means of the joint checking of codings, called consensual coding, and

- a quantitative path by calculating percentage agreement and, under certain circumstances, a suitable coefficient [65].

4.2. Consensus Coding

4.3. Calculation of Inter-Rater Reliability

5. Results

5.1. Contributions to Theory

5.2. Contributions to Practice

What concrete measures have you/has your bank taken in the past to keep pace with digital competition and the changing pace of digitalisation?(Interview Question 10)

6. Conclusions and Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Main Category | Sub-Code | Code Description | Number of Sub-Codes |

| Benefits | No public funding | No public funding is known or available for the (further) development of banking technologies. It is assumed that banks have the necessary financial resources to implement digital transformation themselves and, therefore, do not need support. | 27 |

| Customer | Customer | Customers have concerns and reject digitalisation in general. | 1 |

| Acceptance | Customer acceptance and trust in the application/technology varies from person to person and is an essential factor that has to be created and considered. | 18 | |

| State of the art | More and more is expected from and offered to the customer. However, customers are not always able to use the technology to its full extent. | 6 | |

| Age structure | Based on their different ages, customers have different knowledge and expectations towards digital technology and possibilities to use it. | 13 | |

| Usage behaviour | The customer’s behaviour is changing in the sense that he/she is evolving from an analogue to a digital customer. Services, especially digital ones, should be available at all times, but old services should be retained as well. | 12 | |

| Expectations | Customer expectations are very diverse. On the one hand, some expect the permanent availability of technology and, at the same time, the possibility to continue to use personal consultants. On the other hand, others do not expect multi-channel offers. Both, however, are characterized by the expectation of security. | 28 | |

| Knowledge | Today’s customers are often well informed, but this knowledge as a whole is very heterogeneous, though increasing. | 3 | |

| Non-existing knowledge | Customers are not informed about the existing possibilities and are not familiar with banking and technology issues. | 5 | |

| Existing knowledge | The customers have knowledge and are well informed. Knowledge is acquired online. For certain topics, no consultants will be needed in the future. | 2 | |

| Customer proximity | Digitalisation and the resulting consequences of branch closures lead to a minimization of personal customer contact. | 12 | |

| Switching behaviour | Digitalisation leads to a reduction in customer retention and loyalty. Customers become more open-minded for new things and “everything from one single source” is less important than before. | 9 | |

| Employee | Employee | Employees will be needed less in the future. However, digital transformation is not possible without a minimum number of employees, who, in turn, can only be maintained with appropriate compensation (war for talents). Existential worries, fears, and inhibitions arise, which are individually pronounced for each employee. | 14 |

| Flexibility | Employees are often overwhelmed by digitalisation and reach their limits. In the future, they need to be flexible and fast enough to adapt to and deal with new developments. | 9 | |

| Acceptance | Employees do not show acceptance at the beginning of a change and often reject the new at first. Employees have to be involved in the change process and learn how to deal with digitalisation and corresponding innovations. It is fundamental that employees should use software and hardware themselves. | 20 | |

| Qualification | Relevant qualifications for employees are not sufficiently available, and this turns out to be a disadvantage for the implementation of complex digital topics and the general digital change in banks. Qualifications will have to be adapted in the future. | 16 | |

| Availability | There are not enough people on the market to fill open IT vacancies for a decent salary and, ultimately, to work on digital issues and enable digital transformation. | 15 | |

| Friendliness | Employee friendliness could be improved. | 1 | |

| Age structure | The age structure in banks will change in the future. Increasingly obsolete employees will lead to the need for digitalisation. It is assumed that the majority of predominantly older employees will slow down or even prevent change. Young people, on the other hand, will not, as they have grown up with digital media and processes. | 10 | |

| Transparency | Digitalisation leads to increased employee and process transparency, which, in turn, is feared by employees. | 3 | |

| Knowledge and Product | Product and Bank complexity | The banking world and its range of products and services is becoming increasingly complex. Here, the complexity of the offer determines whether analogue or digital consulting services are used. Customers often obtain information online and then contact their bank offline. Complex topics can currently only be digitally modelled to a limited extent. However, numerous simple processes are also still offered exclusively in analogue form. | 9 |

| Human uncertainty factor | Man-made mistakes lead to widespread effects in a centrally organized (IT) infrastructure. Digitalisation can increase transparency and minimise error, but it can also promote them and create uncertainty. | 2 | |

| Experts (internal) | Experts on digital issues are (still) available internally to a certain extent and are fundamental for digital transformation in banking. Decentralised digitalisation will require more qualified personnel in the future. | 19 | |

| Experts (external) | External (digital) experts/consultants are available to banks in large numbers. Universities also support banks. Both are available to banks for digitalisation projects if required. External consultants usually charge high costs. | 23 | |

| Market | Market situation | Investments in digitalisation require capital. The current market situation poses challenges for banks: Only lower earnings are being generated due to the interest rate policy. | 8 |

| Market uncertainty | The results of the digitalisation process cannot be measured yet. Future market developments and uncertain success are determined by the customer. Banks are concerned about the right corporate positioning, as there are few sustainable approaches. | 11 | |

| Market power | The current market situation poses challenges for banks. With their increased market power, they can block competitors and thus defend their position. | 2 | |

| Market/competitive pressure | The increased competitive pressure due to technical and market-driven developments will increase in the future, not only between FinTechs and banks, but also between banks themselves. | 22 | |

| Participation | Employee involvement | Employees are actively involved in digitalisation issues by management and are encouraged to develop and implement their own ideas. The management creates the appropriate space for this. In the end, they can (better) identify themselves with the transformation and become a part of it. It is fundamental that employees should apply the technology themselves. | 18 |

| Customer integration | Customers are seen as partners. They are actively involved in development and in ongoing processes. By involving them at an early stage, their needs can be taken into account and they can actively participate in shaping the process. | 15 | |

| Strategy/Management | FinTechs (partners/(non-)competitors) | FinTechs can be both partners and competitors. | 5 |

| FinTech (partners) | FinTechs have become much more like partnership-based companies (partners) that want to advance their own ideas through cooperation and are looking for banks to support them in this. | 8 | |

| FinTech (non-competitors) | Banks will continue to exist in the future and will be increasingly digitalised through constant development. FinTechs should be seen as a complementary approach and not as a competitor that poses a threat to banks. | 10 | |

| FinTech (competitors) | Competition is increasing in the financial industry and FinTechs are now seen as competitors, forcing banks to react and bring their own digital solutions to the market. | 22 | |

| Banks want to cooperate | Banks seek proximity to external FinTechs or try to become active themselves in the FinTech sector with their own developments. These young companies very often offer innovative solutions: Accordingly, banks would like to cooperate with them in order to develop themselves further. | 23 | |

| Banks will not/cannot cooperate | Banks are unwilling or unable to cooperate with FinTechs for organisational or interface reasons. The dominant positioning of banks is intended to make market access more difficult for FinTechs. | 6 | |

| Dependence on providers | Banks and FinTechs need customers and their data. There is a risk of dependence on external providers and loss of control over their own business. Only in exceptional cases is cooperation favoured. | 5 | |

| Reaction to market development | Banks are reacting to market and competitive situations and are trying to keep up with the latest developments in analogue and digital services. They rely on systematic development, which is implemented with the help of internal innovation management. This approach is embedded in their strategy. | 26 | |

| Complex corporate structure and multiple interests | In a large and differentiated corporate structure, banks have to meet multiple and often complex customer needs of different age groups. Expectations of permanent analogue and simultaneous digital accessibility increase the complexity of today’s banking business. | 16 | |

| (Re)structuring | Banks will have to restructure themselves in the future and rethink both new and traditional approaches. This requires change processes that are appropriate to the bank’s size. Restructuring leads to obstacles/resistance among employees and customers, which are very much shaped by individual humanity. | 19 | |

| Reputation worries | Banks are concerned about negative reputational consequences if the cooperation with or participation in FinTechs fails. | 2 | |

| Risk aversion | Managers avoid the risks associated with new issues such as digitalisation. | 1 | |

| Organizational dependency | Banks often organise themselves in a central association structure and can thus position themselves more strongly as a group. However, this leads to dependencies on central services and technologies and limits decision-making options. The individuality of each bank is lost, as organisations dictate the corporate guidelines. | 27 | |

| Reaction speed | Due to the historically evolved and centralised organisational structures of banks within a banking group, the speed of reaction of an institution depends strongly on centralised developments. Banks are therefore slower in digitalisation compared to FinTechs. | 23 | |

| Digitalisation strategy | Digitalisation is an essential part of the current strategy of financial institutions. One is aware that the future of the financial markets will be strongly influenced by digital topics. The basic prerequisite for sustainable development in the future must be created today. | 28 | |

| Transparency | Digitalisation leads to transparent markets and products. Offers and banks can be compared by the customer, allowing them to choose the most suitable solution. | 4 | |

| Corporate culture/tradition | Banks are shaped by the historical corporate culture and tradition that has been established over many decades. This is precisely what determines the processes and the orientation of banks. Young customers, in particular, are questioning this. Management must rethink and a change in leadership from old to young is required. | 17 | |

| Management perception | The management sees the importance of the topic of digitalisation and takes the need for further development and its influence. In their opinion, digitalisation will contribute to process optimization and automation in the future. It is assumed that banks are on the right track, but only a small part of what is possible has been implemented to date. | 33 | |

| Resources not available | Resources are not available for digital in-house and further development of products and approaches. | 13 | |

| Resources limited | Resources for digital developments are limited. | 4 | |

| Resources available | Resources are available for further digital development or are mobilized if the company positions itself digitally accordingly. | 16 | |

| Resource allocation | Resources must be allocated within established structures in such a way that they finance existing and new approaches adequately and that institutions do not fall behind. Misallocation can slow down important developments such as digitalisation. | 19 | |

| Costs | Digitalisation and the infrastructure required for it is associated with high costs, which a bank has to finance independently. Investment decisions are closely monitored, as they are ultimately borne by the bank’s customers. Potentials such as cost savings in a corporate structure can be achieved through digitalisation. The costs can be seen as an obstacle. | 18 | |

| Decision-making process | The decision-making process is time-consuming. Many internal and external interests have to be taken into account. Additionally, decisions are influenced by umbrella organisations. The boards of directors of banks still make their decisions largely independently, but the basis is increasingly integrated to create greater acceptance for change. | 16 | |

| Disruption | Banks face technological developments and the associated risk of disruption in an increasingly fast and competitive market. They have to adapt to technologies and, at the same time, to the pace of digitalisation, without losing their own identity, in order to survive and remain competitive. | 15 | |

| Technology and Regulation | Useability | Usability is essential for customers in digital applications. Customers must be taken into account—for certain customer groups, usability is not a given. | 3 |

| Technical effort | The technical and cost-related expenditures for banks for the new and further development and adaptation of solutions are very high. This makes digitalisation more difficult, which ultimately becomes an obstacle. | 13 | |

| Regulatory obstacles | Regulatory requirements must be met by banks by law. This confronts them, from an internal and external perspective of further development, with major obstacles that slow down digitalisation. | 21 | |

| Data protection/security and integrity | Banks and FinTechs are becoming more and more networked, and customers are becoming more and more transparent, particularly through free access and exchange of data. In this context, data are subject to special protection requirements, which poses a challenge for both banks and FinTechs. This is slowing down digitalisation. Banks are subjectively more strongly monitored and are more in public focus than FinTechs. | 18 | |

| Implementation difficulties | The implementation of new processes and technologies in banks, taking into account legal requirements and the growing IT infrastructure, causes implementation problems of digital approaches and slows down or even completely inhibits digitalisation in banking. | 13 | |

| Public infrastructure | The public infrastructure does not meet the requirements for comprehensive digitalisation of banks. | 6 | |

| Outdated IT infrastructure | The demands on banking IT are increasing together with the speed of technology cycles and the associated technological developments. Banks will never be able to keep up with the latest developments. Legacy IT infrastructures place limits on digitalisation in banks. | 7 | |

| State of the art/integration (today) | Centrally provided technology and corresponding interfaces are not sufficiently developed to allow technical approaches to be integrated into banks without problems and to enable holistic digitalisation. | 11 |

References

- Türkmen, E.; Soyer, A. The Effects of Digital Transformation on Organizations. In Handbook of Research on Strategic Fit and Design in Business Ecosystems: Advances in E-Business Research; IGI Global: Hershey, PA, USA, 2020; pp. 259–288. [Google Scholar] [CrossRef]

- Hess, T.; Matt, C.; Benlian, A.; Wiesböck, F. Options for Formulating a Digital Transformation Strategy. MIS Q. Exec. 2016, 15, 123–139. [Google Scholar]

- Ivančić, L.; Stjepic, A.-M.; Vugec, D.S. Mastering digital transformation through business process management: Investigating alignments, goals, orchestration, and roles. J. Entrep. Manag. Innov. 2020, 16, 41–73. [Google Scholar] [CrossRef]

- Ismail, M.H.; Khater, M.; Zaki, M. Digital Business Transformation and Strategy: What Do We Know So Far? Working Paper University of Cambridge; University of Cambridge: Cambridge, UK, 2018. [Google Scholar]

- Westerman, G.; Bonnet, D.; McAfee, A. The Nine Elements of Digital Transformation. MIT Sloan Manag. Rev. 2014, 55, 1–6. [Google Scholar]

- Aydalot, P.; Keeble, D. High Technology Industry and Innovative Environments, 1st ed.; Routledge: London, UK, 2018. [Google Scholar]

- Cohen, B.; Amorós, J.E.; Lundy, L. The generative potential of emerging technology to support startups and new ecosystems. Bus. Horiz. 2017, 60. [Google Scholar] [CrossRef]

- Li, L.; Su, F.; Zhang, W.; Mao, J.-Y. Digital transformation by SME entrepreneurs: A capability perspective. Inf. Syst. J. 2017, 28, 1–29. [Google Scholar] [CrossRef]

- Deutsche Bundesbank. Zahlungsverhalten in Deutschland—Eine empirische Studie über die Auswahl und Verwendung von Zahlungsinstrumenten in der Bundesrepublik Deutschland. 2009. Available online: https://www.bundesbank.de/resource/blob/599956/4d15527da87c104926f9ad8c5a53707a/mL/zahlungsverhalten-in-deutschland-2009-data.pdf (accessed on 10 September 2019).

- Deutsche Bundesbank. Zahlungsverhalten in Deutschland 2011—Eine empirische Studie über die Verwendung von Bargeld und unbaren Zahlungsinstrumenten. 2012. Available online: https://www.bundesbank.de/resource/blob/663302/8b1c7f5a6407b21aac71dd41cef8bbd2/mL/zahlungsverhalten-in-deutschland-2011-data.pdf (accessed on 10 September 2019).

- Deutsche Bundesbank. Zahlungsverhalten in Deutschland 2014—Dritte Studie über die Verwendung von Bargeldund unbaren Zahlungsinstrumenten. 2015. Available online: https://www.bundesbank.de/resource/blob/599406/8deaa2563cb837cb33d2d38edef6c4d6/mL/zahlungsverhalten-in-deutschland-2014-data.pdf (accessed on 10 September 2019).

- Deutsche Bundesbank. Zahlungsverhalten in Deutschland 2017—Vierte Studie über die Verwendung von Bargeld und unbaren Zahlungsinstrumenten. 2018. Available online: https://www.bundesbank.de/resource/blob/634056/8e22ddcd69de76ff40078b31119704db/mL/zahlungsverhalten-in-deutschland-2017-data.pdf (accessed on 10 September 2019).

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Chen, M.A.; Wu, Q.; Yang, B. How Valuable Is FinTech Innovation? Rev. Financ. Stud. 2019, 32, 2062–2106. [Google Scholar] [CrossRef]

- Gomber, P.; Kaufmann, R.J.; Parker, C.; Weber, B.W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2017, 35, 220–265. [Google Scholar] [CrossRef]

- Schepinin, V.; Bataev, A. Digitalization of financial Sphere: Challenger banks efficiency estimation. In Proceedings of the International Scientific Conference “Digital Transformation on Manufacturing, Infrastructure and Service”, Saint-Petersburg, Russia, 21–22 November 2019. [Google Scholar]

- Breidbach, C.F.; Keating, B.W.; Lim, C. Fintech: Research Directions to Explore the Digital Transformation of Financial Service Systems. J. Serv. Theory Pract. 2020, 30, 79–102. [Google Scholar] [CrossRef]

- Krasonikolakis, I.; Tsarbopoulos, M.; Eng, T.-Y. Are incumbent banks bygones in the face of digital transformation. J. Gen. Manag. 2020, 46, 60–69. [Google Scholar] [CrossRef]

- Fernández-Portillo, A.; Hernández-Mogollón, R.; Sánchez-Escobedo, M.C.; Coca Pérez, J.L. Does the Performance of the Company Improve with the Digitalization and the Innovation? In Economy, Business and Uncertainty: New Ideas for a Euro-Mediterranean Industrial Policy. AEDEM 2017. Studies in Systems, Decision and Control; Gil-Lafuente, J., Marino, D., Morabito, F.C., Eds.; Springer: Cham, Switzerland, 2019; pp. 276–291. [Google Scholar] [CrossRef]

- Groberg, M.; Vetter, H.-M.; Flatten, T.C. A measurement instrument for digitization: Scale development and impact on new product performance. In Academy of Management Proceedings 2016; Academy of Management: Briarcliff Manor, NY, USA, 2016. [Google Scholar] [CrossRef]

- Kelchevskaya, N.R.; Shirinkina, E.V.; Strih, N.I. Estimation of interrelation of components of human capital and level of digitalization of industrial enterprises by method of modeling of structural equations. In Proceedings of the 1st International Scientific Conference “Modern Management Trends and the Digital Economy: From Regional Development to Global Economic Growth” (MTDE 2019); Atlantis Press: Cambridge, MA, USA, 2019. [Google Scholar]

- Niemand, T.; Rigtering, J.P.C.; Kallmüzer, A.; Kraus, S.; Maalaoui, A. Digitalization in the financial industry: A contingency approach of entrepreneurial orientation and strategic vision on digitalization. Eur. Manag. J. 2020. [Google Scholar] [CrossRef]

- Dorfleitner, G.; Hornuf, L.; Schmitt, M.; Weber, M. FinTech in Germany; Springer International Publishing: Cham, Switzerland, 2017. [Google Scholar]

- Crunchbase. N26. 2019. Available online: https://www.crunchbase.com/organization/n26#section-twitter (accessed on 4 May 2019).

- Dorfleitner, G.; Hornuf, L. Fintech-Markt in Deutschland; Bundesministerium der Finanzen: Berlin, Germany, 2016. [Google Scholar]

- Christensen, C.M.; Bower, J.L. Customer Power, Strategic Investment, and the Failure of Leading Firms. Strateg. Manag. J. 1996, 17, 197–218. [Google Scholar] [CrossRef]

- Christensen, C.M.; Raynor, M.E.; Rory, M. What Is Disruptive Innovation? Harvard Business Review. December 2015, pp. 44–53. Available online: https://hbr.org/2015/12/what-is-disruptive-innovation (accessed on 12 February 2021).

- Diener, F.; Špaček, M. The Role of “Digitalization” in German Sustainability Bank Reporting. Int. J. Financ. Stud. 2020, 8, 16. [Google Scholar] [CrossRef]

- Braun, A. Deutsche Bank voll “Digital”. 2016. Available online: http://boerse.ard.de/aktien/deutsche-bank-voll-digital100.html (accessed on 17 November 2018).

- Mohan, D. How banks and FinTech startups are partnering for faster innovation. J. Digit. Bank. 2015, 1, 12–21. [Google Scholar]

- Matt, C.; Hess, T.; Benlian, A. Digital Transformation Strategies. Bus. Inf. Syst. Eng. 2015, 57, 339–343. [Google Scholar] [CrossRef]

- Terrar, D. What is Digital Transformation? 2015. Available online: http://www.theagileelephant.com/what-is-digital-transformation/ (accessed on 12 May 2020).

- Valdez-de-Leon, O. A Digital Maturity Model for Telecommunications Service Providers. Technol. Innov. Manag. Rev. 2016, 6, 19–32. [Google Scholar] [CrossRef]

- Gartner. Gartner IT Glossary—Digitization. 2020. Available online: https://www.gartner.com/en/information-technology/glossary/digitization (accessed on 11 May 2020).

- Francis, B.; Hasan, I.; Küllü, A.M.; Mingming, Z. Should banks diversify or focus? Know thyself: The role of abilities. Econ. Syst. 2018, 42, 106–118. [Google Scholar] [CrossRef]

- Hensmans, M. How digital fantasy work induces organizational ideal reversal? Long-term conditioning and enactment of digital transformation fantasies at a large alternative bank (1963–2019). Organization 2020. [Google Scholar] [CrossRef]

- Lotriet, R.A.; Dltshego, K.K. An assessment of perceptions concerning digital transformation at a South African commercial bank—A case of Anthropocene denial for the economy. Tydskrif vir Geesteswetenskappe 2020, 60, 687–707. [Google Scholar] [CrossRef]

- Von Solms, J. Integrating Regulatory Technology (RegTech) into the digital transformation of a bank Treasury. J. Bank. Regul. 2020. [Google Scholar] [CrossRef]

- Bican, P.M.; Brem, A. Digital Business Model, Digital Transformation, Digital Entrepreneurship: Is There A Sustainable “Digital”. Sustainability 2020, 12, 5239. [Google Scholar] [CrossRef]

- Fekete, A.; Rhyner, J. Sustainable Digital Transformation of Disaster Risk-Integrating New Types of Digital Social Vulnerability and Interdependencies with Critical Infrastructure. Sustainability 2020, 12, 9324. [Google Scholar] [CrossRef]

- Forcadell, F.J.; Aracil, E.; Ubeda, F. Using reputation for corporate sustainability to tackle banks digitalization challenges. Bus. Strategy Environ. 2020, 29, 2181–2193. [Google Scholar] [CrossRef]

- El Hilali, W.; El Manouar, A.; Janati Idrissi, M.A. Reaching sustainability during a digital transformation: A PLS approach. Int. J. Innov. Sci. 2020, 12, 52–79. [Google Scholar] [CrossRef]

- Ordieres-Meré, J.; Prieto Remón, T.; Rubio, J. Digitalization: An Opportunity for Contributing to Sustainability FROM Knowledge Creation. Sustainability 2020, 12, 1460. [Google Scholar] [CrossRef]

- Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An Explanation through Business Model Scalability and Market Valuation. Sustainability 2020, 12, 10316. [Google Scholar] [CrossRef]

- Verhagen, T. Catalysing FinTech for Sustainability. Lessons from Multi-Sector Innovation. A Report of the BEI’s Fintech Taskforce. Preprint. Available online: https://www.researchgate.net/publication/328345987_Catalysing_Fintech_for_Sustainability_Lessons_from_multi-sector_innovation_A_report_of_the_BEI’s_Fintech_Taskforce/comments (accessed on 23 January 2021).

- Aguayo, F.Z.; Ślusarczyk, B. Risks of Banking Services’ Digitalization: The Practice of Diversification and Sustainable Development Goals. Sustainability 2020, 12, 4040. [Google Scholar] [CrossRef]

- Moudud-Ul-Huq, S.; Ashraf, B.N.; Gupta, A.D.; Zheng, C. Does bank diversification heterogeneously affect performance and risk-taking in ASEAN emerging economies. Res. Int. Bus. Financ. 2018, 46, 342–362. [Google Scholar] [CrossRef]

- Shin, Y.J.; Choi, Y. Feasibility of the Fintech Industry as an Innovation Platform for Sustainable Economic Growth in Korea. Sustainability 2019, 11, 5351. [Google Scholar] [CrossRef]

- Mărăcine, V.; Voican, O.; Scarlat, E. The Digital Transformation and Disruption in Business Models of the Banks under the Impact of FinTech and BigTech. In Proceedings of the International Conference on Business Excellence; Walter de Gruyter GmbH: Berlin, Germany, 2020; pp. 294–305. [Google Scholar] [CrossRef]

- Hough, J.; Chan, K.-Y. Factors influencing the acceptance of digital banking: An empirical study in South Africa based on the enhanced Technology Acceptance Model. In Proceedings of the 27th Annual Conference of the International Association for Management of Technology (IAMOT 2018), Birmingham, UK, 22–26 April 2018. [Google Scholar]

- Sadigov, S.; Vasilyeva, T.; Rubanov, P. FinTech in Economic Growth: Cross-country Analysis. In Economic and Social Development: Book of Proceedings, Proceedings of the 55th International Scientific Conference on Economic and Social Development, Baku, Azerbaijan, 17–18 June 2020; Ismayilov, A., Aliyev, K., Benazic, M., Eds.; ProQuest: Ann Arbor, MI, USA, 2020; pp. 729–739. [Google Scholar]

- Chan, E.S.W. Barriers to EMS in the hotel industry. Int. J. Hosp. Manag. 2008, 28, 187–196. [Google Scholar] [CrossRef]

- Chan, E.S.W. Implementing Environmental Management Systems in Small- and Medium-Sized Hotels: Obstacles. J. Hosp. Tour. Res. 2011, 35, 3–23. [Google Scholar] [CrossRef]

- Vikneswaran, N.; Anantharajah, S. A green makeover for our hotels? Q. DOE Update Environ. Dev. Sustain. 2012, 2, 10–12. [Google Scholar]

- Kamalulariffin, N.S.; Nabiha, S.; Khalid, A.; Wahid, N.A. The barriers to the adoption of environmental management practices in the hotel industry: A study of Malaysian hotels. Bus. Strategy Ser. 2013, 14, 106–117. [Google Scholar] [CrossRef]

- Yusof, Z.B.; Jamaludin, M. Barriers of Malaysian Green Hotels and Resorts. In Procedia—Social and Behavioral Sciences, Proceedings of the AMER International Conference on Quality of Life, AicQoL2014KotaKinabalu, The Pacific Sutera Hotel, Sutera Harbour, Kota Kinabalu, Sabah, Malaysia, 4–5 January 2014; Elsevier: Amsterdam, The Netherlands, 2014; pp. 501–509. [Google Scholar]

- Chan, E.S.W.; Okumus, F.; Chan, W. What hinders hotels’ adoption of environmental technologies: A quantitative study. Int. J. Hosp. Manag. 2020. to be published. [Google Scholar] [CrossRef]

- Chan, E.S.W.; Okumus, F.; Chan, W. Barriers to Environmental Technology Adoption in Hotels. J. Hosp. Tour. Res. 2015, 42, 1–25. [Google Scholar] [CrossRef]

- Deutsche Bundesbank. Bankenstatistik Januar 2015. Available online: https://www.bundesbank.de/resource/blob/693922/a24868217d3ad9478b920930e2226987/mL/2015-01-bankenstatistik-data.pdf (accessed on 9 April 2019).

- Deutsche Bundesbank. Bankenstatistik Januar 2016. Available online: https://www.bundesbank.de/resource/blob/693932/28e421937f44e7c19fee43daf9266b0b/mL/2016-01-bankenstatistik-data.pdf (accessed on 9 April 2019).

- Deutsche Bundesbank. Bankenstatistik Januar 2018. Available online: https://www.bundesbank.de/resource/blob/693982/7b3c771cecbc6b44934c408310bbb35f/mL/2018-01-bankenstatistik-data.pdf (accessed on 9 April 2019).

- Deutsche Bundesbank. Bankenstatistik Januar 2019. Available online: https://www.bundesbank.de/resource/blob/773438/048ad3c478cd071493582c25ca847a8a/mL/2019-01-bankenstatistik-data.pdf (accessed on 9 April 2019).

- Deutsche Bundesbank. Bankenstatistik Januar 2020. Available online: https://www.bundesbank.de/resource/blob/822138/b3d37fcb3c2a65a40ea3ada27a0988d4/mL/2020-01-bankenstatistik-data.pdf (accessed on 9 January 2019).

- Diener, F. Empirical Evidence of a Changing Operating Cost Structure and Its Impact on Banks’ Operating Profit: The Case of Germany. J. Risk Financ. Manag. 2020, 13, 247. [Google Scholar] [CrossRef]

- Kuckartz, U. Qualitative Inhaltsanalyse. Methoden, Praxis, Computerunterstützung, 3rd ed.; Beltz Juventa: Weinheim, Germany, 2016. [Google Scholar]

- Dresing, T.; Pehl, T. Praxisbuch Interview, Transkription & Analyse, 6th ed.; Dr. Dresing und Pehl: Marburg, Germany, 2015. [Google Scholar]

- Helfferich, C. Die Qualität Qualitativer Daten: Manual für die Durchführung Qualitativer Interviews, 5th ed.; Springer VS: New York, NY, USA, 2020. [Google Scholar]

- Mayring, P. Qualitative Inhaltsanalyse: Grundlagen und Techniken, 12th ed.; Beltz: Weinheim, Germany, 2015. [Google Scholar]

- Döring, N.; Bortz, J. Forschungsmethoden und Evaluation in den Sozial- und Humanwissenschaften, 5th ed.; Springer: Berlin/Heidelberg, Germany, 2016. [Google Scholar]

- Gläser, J.; Laudel, G. Experteninterviews und Qualitative Inhaltsanalyse als Instrumente Rekonstruierender Untersuchungen, 4th ed.; VS Verlag für Sozialwissenschaften: Wiesbaden, Germany, 2010. [Google Scholar]

- Bogner, A. Interviews mit Experten: Eine praxisorientierte Einführung, 2014 ed.; Springer VS: New York, NY, USA, 2014. [Google Scholar]

- Glaser, B.G.; Strauss, A.L. The Discovery of Grounded Theory: Strategies for Qualitative Research; Aldine Transaction: Piscataway, NJ, USA, 1967. [Google Scholar]

- Morse, J.M. Designing funded qualitative research. In Handbook of Qualitative Research; Denzin, N.K., Lincoln, Y.S., Eds.; Sage Publications: Thousand Oaks, CA, USA, 1994; pp. 220–235. [Google Scholar]

- Creswell, J.W. Qualitative Inquiry & Research Design, 3rd ed.; Sage Publications: Thousand Oaks, CA, USA, 2012. [Google Scholar]

- Mayring, P. Einführung in die Qualitative Sozialforschung, 6th ed.; Beltz: Weinheim, Germany, 2016. [Google Scholar]

- Mayring, P. Einführung in Die Qualitative Sozialforschung. Eine Anleitung zu Qualitativem Denken, 5th ed.; Beltz: Weinheim, Germany, 2002. [Google Scholar]

- Brislin, R.W. Translation and content analysis of oral and written materials. In Handbook of Cross-cultural Psychology; Triandis, H.C., Berry, J.W., Eds.; Allyn and Bacon: Boston, MA, USA, 1980; pp. 389–444. [Google Scholar]

- Allmark, P.; Boote, J.; Chambers, E.; Clarke, A.; McDonnell, A.; Thompson, A.; Tod, A.M. Ethical Issues in the Use of In-Depth Interviews: Literature Review and Discussion. Res. Ethics 2009, 5, 48–54. [Google Scholar] [CrossRef]

- Guest, G.; MacQueen, K.M.; Namey, E.E. Applied Thematic Analysis; SAGE Publications: Thousand Oaks, CA, USA, 2012. [Google Scholar]

- Hopf, C.; Schmidt, C. Zum Verhältnis von Innerfamilialen Sozialen Erfahrungen, Persönlichkeitsentwicklung und Politischen Orientierungen: Dokumentation und Erörterung des Methodischen Vorgehens in Einer Studie zu Diesem Thema. Available online: https://nbn-resolving.org/urn:nbn:de:0168-ssoar-456148 (accessed on 24 August 2020).

- Fleiss, J.; Levin, B.; Paik, M.C. Statistical Methods for Rates and Proportions, 3rd ed.; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Hallgran, K. Computing Inter-Rater Reliability for Observational Data: An Overview and Tutorial. Tutor. Quant. Methods Psychol. 2012, 8, 23–24. [Google Scholar] [CrossRef] [PubMed]

- Rädiker, S.; Kuckartz, U. Analyse qualitativer Daten mit MAXQDA; Springer VS: Wiesbaden, Germany, 2018. [Google Scholar]

- Bajpai, S.; Bajpai, R.; Chaturvedi, H.K. Evaluation of Inter-Rater Agreement and Inter-Rater Reliability for Observational Data: An Overview of Concepts and Methods. J. Indian Acad. Appl. Psychol. 2015, 41, 20–27. [Google Scholar]

- Carletta, J. Assessing agreement on classification statistics: The kappa statistic. ACL Anthol. 1996, 22, 249–254. [Google Scholar]

- Gewt, K.L. Kappa Statistic is not Satisfactory for Assessing the Extent of Agreement Between Raters. Stat. Methods Inter Rater Reliab. Assess. 2002, 1, 1–6. [Google Scholar]

- Ishak, N.M.; Bakar, A.Y.A. Qualitative Data Management and Analysis using NVivo: An Approach used to Examine Leadership Qualities among Student Leaders. Educ. Res. J. 2012, 2, 94–103. [Google Scholar]

- Landis, J.R.; Koch, G.G. The measurement of observer agreement for categorical data. Biometrics 1997, 33, 159–174. [Google Scholar] [CrossRef]

- Brennan, R.L.; Prediger, D.J. Coefficient kappa: Some uses, misuses, and alternatives. Educational and Psychological Measurement. Educ. Psychol. Meas. 1981, 41, 687–699. [Google Scholar] [CrossRef]

- Diener, F.; Špaček, M. The Awareness of Digitisation in Strategic Sustainability Reporting in Banking. In Innovation Management, Entrepreneurship and Sustainability 2019 (IMES 2019), Proceedings of the 7th International Conference, Prague, Czech Republic, 30–31 May 2019; Dvouletý, O., Lukeš, M., Mísař, J., Eds.; Prague University of Economics and Business: Prague, Czech Republic, 2019; pp. 137–150. [Google Scholar]

{kind=link}

{kind=link}

| Revenue 2008 | Revenue 2011 | Revenue 2014 | Revenue 2017 | CAGR 3 | |||||

|---|---|---|---|---|---|---|---|---|---|

| € | % | € | % | € | % | € | % | ||

| cash | 405,486 | 57.89% | 317,137 | 53.10% | 267,249 | 53.18% | 297,901 | 47.58% | −2.16% |

| debit card | 178,829 | 25.53% | 169,093 | 28.31% | 147,592 | 29.37% | 212,576 | 33.95% | 3.22% |

| credit card | 25,538 | 3.65% | 44,369 | 7.43% | 19,582 | 3.90% | 27,578 | 4.40% | 2.12% |

| contactless payment | - | - | 318 | 0.05% | 386 | 0.08% | 7103 | 1.13% | 66.50% 1 |

| other cards | 5127 | 0.73% | 815 | 0.14% | 486 | 0.10% | 676 | 0.11% | −19.16% |

| bank transfer | 62,199 | 8.88% | 49,181 | 8.23% | 26,405 | 5.25% | 34,749 | 5.55% | −5.09% |

| direct debit | 13,024 | 1.86% | 4268 | 0.71% | 14,881 | 2.96% | 15,181 | 2.42% | 2.99% |

| online payment | 1939 | 0.28% | 10,115 | 1.69% | 13,986 | 2.78% | 23,258 | 3.71% | 33.45% |

| mobile payment | - | - | - | - | 77 | 0.02% | 124 | 0.02% | 8.63% 2 |

| other techniques | 8297 | 1.18% | 1984 | 0.33% | 11,900 | 2.37% | 6955 | 1.11% | −0.71% |

| ∑ | 700,439 | 100% | 597,280 | 100% | 502,544 | 100% | 626,102 | 100% | |

| Interview | Duration | Bank Experience | Gender | Validity | |

|---|---|---|---|---|---|

| (mm:ss) | (In Years) | ||||

| 1. | 27:57 | 20 | M | 🗸 | |

| 2. | 31:25 | 5 | M | 🗸 | |

| 3. | 24:15 | 42 | M | 🗸 | |

| 4. | 38:57 | 9 | M | 🗸 | |

| 5. | 23:02 | 17 | M | 🗸 | |

| 6. | 23:48 | 33 | M | 🗸 | |

| 7. | 13:12 | 25 | M | 🗴 | |

| 8. | 39:39 | 32 | M | 🗸 | |

| 9. | 29:04 | 7 | M | 🗸 | |

| 10. | 25:24 | 20 | M | 🗸 | |

| 11. | 28:05 | 17 | M | 🗸 | |

| 12. | 34:19 | 8 | M | 🗸 | |

| 13. | 27:03 | 27 | M | 🗸 | |

| 14. | 34:46 | 34 | M | 🗸 | |

| 15. | 27:13 | 11 | M | 🗸 | |

| 16. | 66:58 | 22 | M | 🗸 | |

| 17. | 46:48 | 19 | M | 🗸 | |

| 18. | 25:57 | 28 | M | 🗸 | |

| 19. | 34:48 | 12 | M | 🗸 | |

| 20. | 31:49 | 26 | M | 🗸 | |

| 21. | 35:18 | 30 | M | 🗸 | |

| 22. | 38:02 | 17 | M | 🗸 | |

| 23. | 35:59 | 28 | M | 🗸 | |

| 24. | 22:54 | 23 | M | 🗸 | |

| 25. | 52:55 | 20 | M | 🗸 | |

| 26. | 46:59 | 10 | M | 🗸 | |

| 27./28. * | 54:05 | 44/11 | M | 🗸 | |

| 29. | 37:31 | 25 | M | 🗴 | |

| 30. | 28:43 | 30 | M | 🗸 | |

| 31. | 33:31 | 20 | M | 🗸 | |

| 32. | 35:14 | 27 | M | 🗸 | Duration (hh:mm:ss) |

| 33. | 37:02 | 20 | M | 🗸 | ∑ (total) 18:43:56 |

| 34. | 31:14 | 25 | M | 🗸 | ∑ (valid) 17:53:13 |

| Evaluation question | What obstacles do banks face when implementing digital banking approaches according to the respondents? |

| Category definition | Subjective as well as objective assessments and perceptions of decision-makers and experts on the topic of digitalisation and the associated implementation barriers. All related issues affecting the industry and the specific situations of individual institutions in the banking sector. |

| Abstraction level | Concrete content on the subject of digitalisation for people, departments, companies, customers, and the market. |

| Coding unit | Clear and meaningful elements in the context of digitalisation in banking and general financial services. |

| Context unit | The whole interview with a person—verbatim transcription. |

| Analysis unit | All valid research material from the 32 interviews. |

| File | Match | Non-Match | Percentage | Kappa (RK) |

|---|---|---|---|---|

| Interview 4 | 57 | 6 | 90.48 | 0.90 |

| Interview 13 | 56 | 7 | 88.89 | 0.89 |

| Interview 20 | 53 | 10 | 84.13 | 0.84 |

| Interview 24 | 54 | 9 | 85.71 | 0.86 |

| Interviews 27 and 28 | 46 | 17 | 73.02 | 0.73 |

| Interview 31 | 54 | 9 | 85.71 | 0.86 |

| <Total> | 320 | 58 | 84.66 |

| Main Category | Number of Sub-Categories |

|---|---|

| Benefits | 1 |

| Customer | 11 |

| Employee | 8 |

| Knowledge and Product | 4 |

| Market | 4 |

| Participation | 2 |

| Strategy and Management | 25 |

| Technology and Regulation | 8 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Diener, F.; Špaček, M. Digital Transformation in Banking: A Managerial Perspective on Barriers to Change. Sustainability 2021, 13, 2032. https://doi.org/10.3390/su13042032

Diener F, Špaček M. Digital Transformation in Banking: A Managerial Perspective on Barriers to Change. Sustainability. 2021; 13(4):2032. https://doi.org/10.3390/su13042032

Chicago/Turabian StyleDiener, Florian, and Miroslav Špaček. 2021. "Digital Transformation in Banking: A Managerial Perspective on Barriers to Change" Sustainability 13, no. 4: 2032. https://doi.org/10.3390/su13042032

APA StyleDiener, F., & Špaček, M. (2021). Digital Transformation in Banking: A Managerial Perspective on Barriers to Change. Sustainability, 13(4), 2032. https://doi.org/10.3390/su13042032