1. Introduction

Businesses around the globe are becoming more socially responsible due to pressures from different stakeholders, such as consumers, competitors and governments [

1]. The concept of corporate social responsibility (CSR) has been around for decades, but its boundaries are still evolving even in 2021 [

2]. The prior literature has largely addressed the impact of CSR activities on the financial output of an organization [

3,

4]. This is quite a recent in the literature, that contemporary researchers have begun to explore the relationship between CSR activities and environment management [

5]. Hence, recent researchers have shown greater concern and want to address the widespread issue of environmental dilapidation through CSR initiatives [

6]. Industries around the globe are key players adding fuel to the risk of environmental degradation. Traditionally, it was thought that the prime concern of enterprises is to make profit, but in recent years, this traditional model has been replaced with a business philosophy of earning the profits not at the expense of society [

7]. Stakeholders in the current digital age are more knowledgeable due to the advancement in digital technology; hence, they are interested in learning about the socially responsible behavior of businesses in order to be assured that businesses are contributing positively to preserve the environment [

8]. In response to such emerging changes, developed countries such as the USA and countries from the European Union (EU) have already raised their environmental standards, due to which businesses in developed countries have significantly changed their behaviors toward the environment [

9]. However, the real problem lies in the developing countries of the world, where environmental standards are far behind as compared to developed nations. To further aggravate the situation, most of the developing economies are emitting a significant amount of pollution, which is a serious threat for planet Earth [

10].

Pakistan, being a developing nation, is experiencing the serious challenge of changing climatic conditions, due to which the country is facing several problems, including heavy floods, droughts, extreme temperatures and a poor air quality index [

11]. The country needs to take serious measures at every level to efficiently deal with the current environmental issues. This is the time for the country to rethink its environmental management and take initiatives to preserve the environment at all levels, including the individual (employee) level and group (organizational) level. CSR, in this context, may be a good strategy to reduce the environmental footprint of enterprises. Studies have shown that well-planned CSR initiatives can improve the environmental performance of an organization [

12,

13]. However, what has been missing in the prior literature is the potential role of CSR at the individual level (employees) in reducing the environmental footprint of enterprises. We define microlevel CSR (micro-CSR) in line with the definition of Rupp and Mallory [

14], who contended that micro-CSR is concerned with the CSR experience at the individual level. We further argue that there is a growing concern among contemporary scholars to realize the importance of individual psychological feelings toward CSR activities undertaken by a specific organization to shape their orientation towards nature [

15,

16]. Although Rupp and Mallory [

14] mentioned extending micro-CSR to any individual level inside or outside of an organization, we focused on a narrower aspect by considering an employee’s intervention toward environmental improvement at workplace. Unfortunately, in Pakistan, individuals’ thinking toward the relationship of self and nature is poor due to the lack of knowledge and understanding of the fact that every individual is important in the efforts to preserve the nature. Further, individuals are less concerned about the widespread issue of climate change in the country because of their poor knowledge and passive behavior toward the environment. The findings of the present study may be the dawn of a new horizon in which individuals at workplaces are expected to rethink their relationship with nature, and therefore a better sustainable future of the country can be hoped for.

We further argue that employees spend a significant amount of time at their workplaces, and so they may be key players in reducing the environmental footprint of an organization if they, at the individual level, show responsible behaviors to preserve the environment—for example, not consuming unnecessary electricity, not wasting organizational resources, etcetera. Further, out of the 200 million population of Pakistan, the labor force constitutes more than 72 million [

17], which is a huge number, thus neglecting its role in promoting environmental sustainability is unwise. Hence, the objective of the present study is to examine the relationship between micro-CSR activities and environmental performance, with the mediating role of employees’ proenvironmental behavior.

The proposed model of the present study was tested in the banking sector of Pakistan. This sector was chosen because in Pakistan, the current state of CSR initiatives from the business community is poor and the banking sector is one the leading sectors of the country, which contributes significantly to CSR activities [

18]. Further, the banking sector is not considered to be a pollution-emitting sector, and perhaps this is the reason that banks in Pakistan invest significantly in CSR activities, but the majority of such activities include community services such as supporting different community-building activities, including investing in education and donations in the name of charity [

19]. Unlikedeveloped nations, investing CSR funds in promoting environmental sustainability is not the priority of many developing nations [

20]. The findings of the present study will bring it to the focus of policymakers that environmental sustainability may be achieved only when all sectors of the community (manufacturing, service and others) assume their responsibility to preserve the environment.

The study at hands adds to the existing literature in many ways; for example, the prior studies in the existing literature underexplored the relationship of CSR initiatives at the individual level, which is of utmost importance for environmental sustainability. Moreover, this is a pioneering study in the context of a developing country, which aims to highlight the importance of employees at the individual level to preserve the environment. Lastly, the present study is important in addition to recent literature as it brings to the surface this mistaken belief of those in the service sector that this sector is not a pollution-emitting sector, and hence they might not be worried about their contribution towards environmental sustainability. The findings of this study will be helpful to change this behavior of the service sector towards the environment.

2. Literature and Hypotheses

The reason for businesses to participate in CSR activities is to achieve sustainability by improving competitiveness and the environment [

21]. According to Carroll [

22], CSR is the economic, legal, social and philanthropic engagement of a business in which organizations maximize their wealth by responding to the community and environment positively. Likewise, in his book “

Social Responsibilities of the Businessman,” Bowen and Johnson [

23] indicated that business has an impact on society, so the goal of businesses should be in line with social goals and values. Environmental performance can be improved when adopting a CSR plan leads to such interventions like, lower emissions, waste management systems and low energy consumption, playing an important role in eliminating the negative impact of business processes on the environment [

24]. Currently, researchers and policymakers are more concerned with CSR as consumers are looking for environmentally friendly goods and services. During the last decade, CSR has been recognized as one of the most important competitive business strategies [

2]. Furthermore, there are numerous studies on CSR, but there is no clear definition of it, as there is no universal consensus on CSR activities. To be successful, firms must live up to public expectations. Internally targeted organizations have a longer lifespan, and businesses that care more for their consumers are more likely to succeed in the modern competitive world. The CSR is the company’s commitment to adhere to these plans, make decisions and adhere to standards of conduct that are of value to the general public [

25]. Several scholars have identified the impact of CSR on a firm’s performance, noting that it improves with CSR activities [

3,

26]. Shabbir and Wisdom [

27] reported that CSR has significant meanings in a successful organizational life. Scholars have recently considered the relationship between CSR and environmental performance and found that CSR substantially improves environmental performance [

24,

28]. For certain companies, CSR is an approach to increase social power. “The notion of Green environment” is receiving a lot of attention from all stakeholders throughout the world, and consumers are pulled to support those organizations which are socially responsible. Organizations can utilize their CSR programs to expand their social capital and pull in consumers who back green activities [

4]. In the same vein, for organizations, handling the environment well is critical and this is reflected in their CSR programs. It is not exclusively a socially dependable practice; it is also an acceptable business norm according to various stakeholders [

29].

CSR initiatives of an organization are key touchpoints to shape the behavior of employees towards nature, because when workers see that their organization is concerned with environment management and is making real efforts to reduce environmental hazards, they feel positively for their organization [

12]. In line with the theory of norm reciprocity, it is expected that employees will reciprocate positively with their organization due to its engagement in CSR activities [

30]. Hence, we expect that microlevel CSR activities are intended to induce the environmental performance of an organization, so in light of the above literature and discussion, the following hypothesis is proposed:

Hypothesis 1. Microlevel CSR activities are associated with organizational environmental performance.

Organizations have begun to understand the relationship between environmental protection and sustainability and its effectiveness [

31]. Although the topic of CSR has been around for decades, in recent times, there has been a lot of pressure on businesses from stakeholders to act socially [

29]. As a result, CSR policies and procedures are and will be influential at the organizational level (macro-CSR) and at the individual level (micro-CSR). It is notable that the theoretical discussion supports the positive impact of CSR on employee behavior, especially to shape their environment-related behavior [

32,

33]. For example, CSR activities involve social responsibility [

34], and as a result, can lead to employees being engaged in positive behaviors towards the environment and community. In addition, CSR practices can provide a high level of care for employees and their needs [

35]. Therefore, based on the theory of social exchange [

36] and the norm of reciprocity [

37], in which people feel compelled to benefit from other people, we expect employees to reciprocate to the organizations, by building confidence in this positive behavior with their organizations. Goyal et al. [

38] noted that values related to the need of sustainability affect the perception and behavior of employees in the welfare system; that is, employees know and share such values, which motivate them to demonstrate proenvironmental behavior. Similarly, there is a general argument that an organization that supports the environment and sustainable activities can permeate an organization’s climate [

39]. Because employees’ attitudes toward CSR policies and practices define an organization’s “standards of accountability, responsibility, and ethics” [

40], we argue that CSR creates value for employees and consequently contributes to their task-related proenvironmental behavior. In addition, Farid et al. [

33] stated that employees’ perceptions of environmental management activities influence their negotiation for environmental behavior, which in turn attempts to enhance the environmental performance of an organization. Likewise, there have been different researchers in the contemporary literature who acknowledge that the environmental footprint of an organization can be significantly reduced through the responsible behavior of employees; for instance, the studies of Tolppanen and Kang [

41] and Koiwanit and Filimonau [

42] are some of the recent examples in the contemporary literature. We, in this regard, argue that employees spend a lot of time at their workplaces, and if their orientation towards environmental management is improved, then a significant improvement in the overall environmental performance of an organization is expected. CSR at the microlevel is an agent of change that develops positive emotions on the part of employees to promote sustainability, because when an organization communicates its CSR initiative with its employees, they feel elevated and want to respond to the organization in positive way. Hence, they are encouraged to rethink their relationship with nature with a larger perspective by recognizing their importance as an individual to a better and sustainable environment. Along these lines, we propose:

Hypothesis 2. Employees’ proenvironmental behavior positively influences organizational environmental performance.

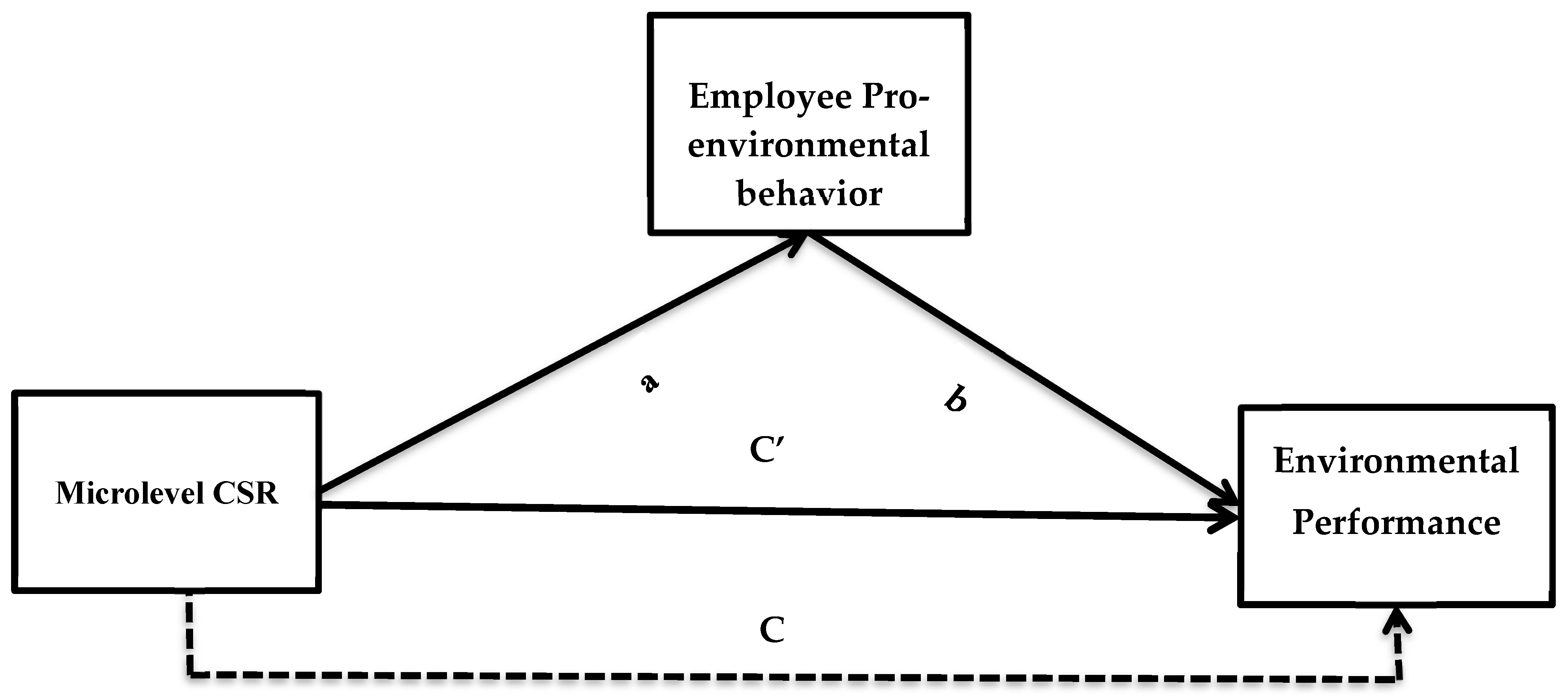

Hypothesis 3. Employees’ proenvironmental behavior mediates the relationship between micro-level CSR and environmental performance.

Based on above literature and discussion the following proposed research model has been framed (see

Figure 1).

4. Results

In the data analysis phase, first of all, we tested the factor loadings of all items in SPSS software through factor analysis in order to determine if there was some issue of factor loading for survey items; for example, cross-loading of an item onto more than one factor or weak loadings. For this purpose, we rotated all items through the varimax rotation from principal component factor analysis in SPSS. The initial extraction of items showed good factor loadings for all items, and all items were well loaded onto their respective factors, which mean there was no issue of factor loading. Next, we also checked the reliability values of our all three variables through assessing Cronbach alpha values (

α). The results revealed that all variables met the criteria of reliability analysis, as all values were above the threshold level of 0.7 (

Table 2).

The above two tests confirmed that the data was quite appropriate for analysis at further levels, so we conducted confirmatory factor analysis (CFA) using AMOS software in order to determine if the data fit our theoretical model. The results of CFA are presented in

Table 3, in which we have reported model fit indices, correlation results, average variance extracted (AVE), composite reliability (CR) and discriminant validity results. According to the results of

Table 3, the model fit values for both the absolute fit indices (

χ2, RMSEA, GFI) and comparative fit indices (IFI, CFI) produced adequate results to establish that our theoretical model fits to the data well. Further, we also tested correlation values in comparison to the square root of AVE values for all variables to establish the discriminant validity of our instrument; the rule of thumb is that if the square root value of the AVE for a variable is larger than the correlation values, then it is established that the items of one variable discriminate from the items of other variables. In this connection (see

Table 3), the value of correlation amongst CSR and proenvironmental behavior (PRB) was 0.218

** and CSR and environmental performance (EPF) was 0.236

**, whereas the value of the square root of the AVE for CSR is 0.768, which is larger than the correlational values, thus establishing that the criteria of discriminant validity is fulfilled. Further, the values of the correlations among different variables are within moderate ranges (the highest was 0.236

**), which raise our confidence to establish that the issue of multicollinearity is not a potential threat in the dataset of the present study. Moreover, the standard deviation (SD) results confirmed that there was less variability in our data, because all the values of SD were less than 1.

Finally, in

Table 3, we also presented the results of convergent validity, which can be observed through the AVE values for each variable; if the value of AVE is more than 0.5, then the criteria of convergent validity is established.

In order to test the hypotheses of the present study, we used a structural equation modeling (SEM) technique in AMOS using the maximum likelihood method, which is a covariance-based SEM approach. In doing so, we ran the structural model twice; the first time, we only tested the direct results without any interventions of a mediator. The results of our direct model produced significant outputs, as shown in

Table 4 (H1;

β = 0.211

**, S.E = 0.034, LLCI = 0.239, ULCI = 0.559,

p < 0.05 and H2;

β = 0.238

**, LLCI = 0.196, ULCI = 0.368,

p < 0.05), establishing that our Hypotheses 1 and 2 are accepted. Thus, it was statistically proven that H1 and H2 are accepted. Further, the results of direct model analysis confirmed that CSR positively predicts employee proenvironmental behavior and environmental performance, but the impact of CSR on environmental performance is more influential on environmental performance as compared to employee proenvironmental behavior, as per the results of the direct effect model (the upper span of

Table 4). Finally, we ran the structural model again with the inclusion of employee proenvironmental behavior as a mediator. For this purpose, we used the bootstrapping option in AMOS by using a large bootstrap sample of 2000. The results are reported in the lower span of

Table 4, which prove that environmental behavior mediates between micro-CSR and environmental performance (the beta was reduced from 0.238 to 0.116 but remained significant). As per the guidelines of Baron and Kenny [

50], if the beta value between the direct relationship of the independent variable and dependent variable is reduced after the inclusion of a mediator in the model, but remains significant, it means there is a partial mediation effect between the relationship of independent variable and dependent variable through the mediator. So, employees’ proenvironmental behavior is a partial mediator between CSR and environmental performance. Hence, we establish that micro-CSR activities directly and indirectly, via environmental behavior, influence the environmental performance of an organization. These results establish that H3 is true and accepted (H3;

β = 0.116

**, S.E = 0.0192, LLCI = 0.098, ULCI = 0.136,

p < 0.05). Thus, H3 of the present study is accepted. Hence, all three hypotheses (H1, H2 and H3) of the present study are accepted in the light of the empirical results.

5. Discussion

Over the last two decades, the topic of CSR has become increasingly interesting to researchers and experts. However, most of these studies have addressed CSR activities at the institutional level. Reasonably, scholars have called for more research on the basics of micro-CSR; in particular, CSR at the individual level. In addition, Hameed et al. [

51] noted that employees’ perceptions of their employer’s CSR practices may have a more direct and effective influence on those employees’ reactions who have a consideration for the environment The objective of this article was to examine the impact of micro-CSR activities on organizational environmental performance with the mediating effect of employees’ proenvironmental behavior in accordance with the environment. To achieve this and to respond to the lack of existing research in the area, the current study tested the proposed model in the banking sector of Pakistan and revealed that micro-CSR is positively related with the environmental performance of a bank and that employee proenvironmental behavior mediates this relationship.

Notwithstanding the link between CSR and environmental performance, the existing literature does not have sufficient evidence, and especially in the context of developing countries, the literature is scant. Our results have contributed to the available literature by showing that employees perceiving their organization to be actively involved in CSR activities pertinent to environment has a positive impact on their environmental behavior. Therefore, organizations implementing socially responsible policies create an environment that is adapted to the relevant values and personal level and consequently creates proenvironmental behaviors; these findings are also in line with previous studies [

39,

52,

53,

54]. Firms can use CSR initiatives to increase environmental performance, as CSR places emphasis on social and environmental issues. However, the relationship between CSR and environmental performance has not been studied in detail. Hence, this study examines the relationship between CSR and environmental performance.

When employees of an organization see that their organization is showing a serious concern towards preserving nature, it urges them to promote this motive of the organization on their part too; hence, employees are self-motivated to show proenvironmental behavior for a sustainable future. Further, the results of the present study also revealed that the microlevel CSR activities of an organization are important touchpoints to shape the view of self and nature in the context of employees’ workplace behavior. Because the CSR activities of an organization moralize the employees to rethink their view towards self and nature, they are motivated to actuate such actions at the individual level, through which they can contribute to reducing the level of environmental dilapidation. Hence, sustainability may be regarded as a “new normal” to change the behavior of oneself towards nature. Well-planned CSR activities play a significant role in improving the environmental consciousness of employees. Improving environmental performance remains an important issue for many organizations due to sustainability pressures from consumers and communities. Our results further establish that the employees of an organization are key players in improving environmental sustainability through their prosocial behavior. Hence, if the employees at each level, irrelevant to a specific industry, are dedicated to preserving the environment, then it follows that the widespread issue of environmental degradation can be encountered in a meaningful way.

Although much attention has been paid to the adoption of new technologies, product development and product performance, awareness of the role of each employee in reducing the environmental footprint of the organization is growing. We are not the first to propose that employees are imperative in preserving the environment and that their proenvironmental behavior is shaped by microlevel CSR activities of an organization; indeed, numerous scholars in the recent literature have reported the same findings [

55,

56,

57,

58].

5.1. Implications

The results of the present study have some important implications for theory and practice; to begin with, the findings of our study enrich the extant literature of CSR in the context of microfoundations to improve environmental performance, as the majority of prior studies have addressed this issue through establishing CSR and environment management relationship at the macrolevel. Likewise, the study at hand also adds to the existing literature in the context of a developing country such as Pakistan, where the issue of climate change is very serious and calls for emergency measures at each level. Lastly, the theoretical importance of the present study is significant as it adds to existing literature by introducing employee proenvironmental behavior as a mediator between the relationship of microlevel CSR and environmental performance.

Our results provide interesting implications for practice as well. Preliminary results of the present study suggest an important role of CSR in improving environmental performance. In particular, employees’ perceptions of the organization’s socially responsible image have a significant impact on employees’ active involvement in environmental protection activities. Therefore, if organizations want to promote environmental ethics at the individual level, they can benefit from the use of CSR activities. However, given that the current results focused on employee perspectives, it is important to keep in mind that organizations need to liaise with their employees to make them realize that the organization is effectively involved in environmental protection activities. Hence, in this way, organizations can improve the view of their employees toward the environment. Unfortunately, in Pakistan, such an orientation towards the environment is essentially non-existent, which is alarming for a country that is already facing extreme climate change conditions. It is very important for policymakers to use the interventions of the present study to involve the workforce in improving environment sustainability for a better and sustainable future. Policymakers can strengthen the CSR plans by addressing environmental responsibility at a higher level. To address this, the implementation and monitoring of the principle of CSR disclosure can be further strengthened.

Although CSR spending of organizations have increased over the years and there are significant efforts made by developed nations to invest CSR funds into environmental activities, the matter is different for developing nations, as they are spending CSR funds on social activities, as concern for the environment is not their prime objective. This is a serious concern for developing nations regarding environmental management. Our research suggests that the firms should be encouraged to invest in improving the environment as part of their social responsibility. One possible solution to change the current scenario may be suitable interventions (in terms of clear policymaking) from the government of Pakistan in order to make businesses realize that climate change is a burning issue at present and that organizations should take every possible step to reduce environmental hazards resulting from their business activities.

In addition, there should be platforms that raise awareness of various environmental issues and ways to help reduce environmental degradation. Corporate executives can use the findings of the present study as a benchmark to evaluate their CSR strategies. Firms can invest in and improve the environment in the framework of CSR. Moreover, they can make an effort to include environmental reporting in their annual reports, business liability reports and/or CSR reports.

5.2. Recommendations

Training and education should focus on the formation of knowledge about the environment, not on changing the attitude of employees to the environment. In addition, it may be more effective to focus on both the group and individual level. While training may involve additional cost, it will generate better results in long run that will offset this additional cost. Similarly, monetary and nonmonetary rewards for the organization should be inclusive and focused on environmental issues, which will motivate more employees than the already encouraged minority. Environmental responsibility should be integrated into core management philosophy so that employees understand that it is important for their organization and management. The biggest sustainability task that managers should be responsible for is taking into account the environmental concerns at the group level and at the individual level. This information should not be the result of the organizational level as a whole, but should be directed to each group, and if possible, to individuals. Personal focus may be on key roles such as managers, team leaders and staff as well as key operations.

6. Conclusions

To conclude, there is no way for modern businesses to negate the importance of sustainability because it has been emerging as an important concern for everyone. Especially in the context of developing nations, this issue is of utmost importance as most developing nations are facing extreme climate change conditions due to their poor environmental management strategies. Pakistan, being a developing nation, is without exclusion to this challenge of climate change, as the country has been a victim of extreme climatic conditions during the last two decades and it is expected that if serious measures are not taken, then this situation of extreme climatic conditions will prevail in the future too. In this connection, the country can help itself from the experience of the West, such as the EU and other developed countries where some extraordinary efforts have been taken at every level to preserve nature. Further, the management of organizations is encouraged to work with employees in relation to personal and environmental factors to reduce the pace of environmental degradation in the country. Due to the growing concern for social responsibility, especially the responsibility for the environment, it is important to realize the human impact on the company’s environmental performance. Because people spend a significant amount of their time at work, it is important for them to understand that their behavior can significantly contribute towards the company’s impact on the environment. It is clear to us that the potential for successful environmental change arises when organizations integrate sustainability or CSR processes into key business functions, such as human resource management and organizational management. In a nutshell, this is the time to purposefully address the issue of environmental sustainability by engaging the employees of an organization proactively, because this is one of the viable strategies through which a better and sustainable future can be achieved.

Limitations and Future Research Directions

The current research needs to address some limitations. First, although the use of time-lagged data decreases the probability of common method bias, it does not prevent some of the causal extrapolations, so in order to improve the causality, future researchers should use longitudinal data. Second, the data used in the present study was collected from Pakistan, a country where the concept of CSR is still at an introductory stage, and especially the effect of CSR to mitigate the impact of climate change, so generalizing the results to other countries may be risky as the phenomenon of CSR is perceived differently in different cultures; future research conducted in other developing nations may improve our understanding of this relationship. Lastly, additional mediators may be introduced; for instance, an ethical climate can influence employee attitudes (e.g., accountability, ethical outcomes and commitments) towards proenvironmental behavior. Therefore, future research should address these constructs as potential mediators in the relationship between CSR and environmental performance.

,

,

{kind=link}