1. Introduction

Between climate change and the ongoing SARS-CoV-2 (COVID) pandemic, systemic risk and financial stability have become critical metrics for global economies [

1,

2,

3]. Resilience and sustainability have each offered a path forward for post-COVID economic recovery and a post-Glasgow global financial order. Yet, the relationships between these two concepts are largely unexplored in economic policy and investment strategies. Without investments in a form of deterministic resilience, acute disruptions can quickly spiral into a ‘crisis of crises,’ including cascading disturbances that undermine nested critical functions in societies and economies. Worse, such disruptive catalysts may generate or exacerbate feedback loops that amplify long-term social, economic, and environmental vulnerabilities [

4]. As highlighted in Glasgow at the 2021 United Nations Climate Change Conference (hereinafter, COP26), global economies run the risk of maladaptive trajectories shaped by these shocks and stresses, which may be further exacerbated by the institutional lock-in of fossil fuel intensive economies [

5].

In light of emerging systemic risks and global demands for more resolute investments in resilience and sustainability, this perspective article takes the position that policymakers must begin to draw greater conceptual, empirical, and practical linkages between sustainability and resilience. This article provides a simplified framework for understanding the positively reinforcing, negatively conflicting and neutral relationships between different types of resilience and sustainability. On the upside, these linkages are centered on the propositions, (i) that various resilience processes may drive sustainable outcomes, and/or (ii) that an allocation of sustainable resources may reinforce resilience processes, as well as the transformative adaptation of markets (herein, the “Reinforcement Proposition”). Yet, on the downside, this framework also acknowledges the propositions (i) that certain resilience processes may perpetuate stability features that may thwart or delay an economic transition toward sustainability, and/or (ii) that certain sustainability outcomes associated with reorganized economic structures and relationships may undermine resources for resilience (herein, the “Conflict Proposition”).

There is a great diversity of different types of resilience that may be relevant in evaluating the underlying propositions. This article focused on a form deterministic resilience known as ‘engineering’ resilience (hereinafter, “Deterministic Engineering Resilience” or “DER”) that speaks to the reversionary capacity of designed systems, including economic policy systems, to revert to a pre-perturbation level of system performance [

6]. By extension, DER may—depending on the scale—provide a measure of economic stability [

7]. As will be discussed, this article also expands the conceptual dimensions of resilience to include another relevant form of resilience specific to economic systems that is non-deterministic, dynamically transformative, and beyond the capacity of policymakers to manage or steer (hereinafter, “Evolutionary Economics Resilience” or “EER”).

Here, sustainability is defined within the context of broad measures of social and environmental sustainability associated with, “[a]chieving higher and more equally distributed well-being levels within ecological limits” [

8]. While both concepts are used to describe systems at various scales, these scales may not always align or otherwise provide a measure of parity useful for exploring any possible convergence [

9]. However, with some measure of scalar alignment, the analysis of resilience processes may be complementary to various sustainability analyses [

10] that seek to broaden the parameters for the systemic analysis of risks and opportunities [

11,

12]. As highlighted in this article, new research inquires and methods are needed to integrate modes of analysis that expand the horizon of resilience performance and sustainable outcomes.

This article argues that post-COVID economic recovery investments in sustainable pathways defined in a post-Glasgow global financial order demand broader intelligence on shifting trade-offs, emerging values, and on how markets adapt and foster resilience against a range of stressors that exceed the structural constraints of socioeconomic systems. A sustainable economic transition driven by the principles of ESG [

13] is often framed naively in an overly simplified form as a series of linear and modular challenges akin to a series of fixed trade-offs within a vague triple-bottom-line approach [

14]. The convergence of DER, EER, and sustainability offers the prospects of a more dynamic understanding of transitional economies and systemic risks.

2. Negotiating the Relationship between Resilience and Sustainability

Across various fields, the relationship between resilience and sustainability may be organized around three primary perspectives: (i) resilience as a component of sustainability; (ii) sustainability as a component of resilience; or (iii) resilience and sustainability as independent concepts by virtue of their separate distinct objectives [

9]. Scholars in the broad interdisciplinary academy of risk science generally view DER and sustainability as distinct conceptual domains, wherein DER speaks to acute ‘threats’ that are managed through broad system responses and sustainability is framed as operating within the context of chronic stresses (e.g., resource constraints) that are shaped by external processes [

15]. This orientation has been further supported from a socioecological perspective, where some have argued that other types of resilience are primarily concerned with processes and system dynamics and sustainability is centered on normative outcomes [

16].

In ecological economics, this acknowledgement of a conceptual independence is further reinforced by the positioning of DER and some other types of resilience as being descriptive and sustainability as being positivist and normative [

17]. Yet, despite distinct objectives, ecological economists have opened the door for positive and neutral relationships to the extent that resilience may or may not—depending on the system—be “necessary and sufficient for sustainability” [

17]. Some have argued that any such integration or positive relationship by and between the concepts are found when there are shared common objectives [

18].

This is where conceptualizations of DER, as a designed processes that deterministically manages to achieve a single-state in engineering and risk management (i.e., engineering resilience) [

19], differ from conceptualizations of socioecological resilience across multiple potential future states that may be beyond the capacity to manage, control, or influence (i.e., socioecological resilience) [

16]. In the context of a broad range of potential risks and uncertainties, from the perspective of risk science, some have argued that DER—when applied to complex social systems (e.g., economic systems)—could have multiple performance measures (e.g., ESG) that together define a comprehensive desired state comparable to the single-state elasticities of a closed engineered system [

9,

20]. This opens the door for the common objectives between DER and sustainability wherein multiple performance criteria for DER may be contextually relatable to the normative outcomes of sustainability. For instance, two measures of DER may be the continued capacity in the face of droughts to provide water to crops and maintain crop yields. Sustainability outcomes associated with lower-energy irrigation and the utilization of drought tolerant plant species may represent a time-dependent co-alignment of process and objective [

21]. This is a classic co-benefits relationship.

DER is well positioned within economic geography and regional science scholarship that has sought to define and measure the resilience of economies in order to identify tunable economic policy measures that speak to common resilience processes that share “regularities across time and space” [

22]. Some have gone as far as to develop computable general equilibrium (CGE) models that estimate the post-facto reduction in economic losses from specific DER investments and policies [

23,

24]. From a contrasting macro-economic perspective, it has been argued that there are other forms of resilience beyond DER, and that the resilience of an economy may be understood to be “a nonequilibrium property of networked production systems” that may be evaluated through linear response theory-based models that evaluate the proportional flux in fixed capital stocks from an external force (e.g., economic crisis) [

25]. Such a perspective would allow for policy simulations that may be parametrized to a range of external perturbations associated with climate change, global change, and other known mechanisms of financial instability and systemic risk.

Yet, others have observed these lines of scholarship—that focus on resistance and recovery from macro-economic crises—are somewhat shortsighted, as they may be disregarding the structural reorganization of economies in such a way that suggests the potential for resilience processes to drive transformative adaptation [

26]. Indeed, resilience in economics includes theoretical and methodological dimensions of both deterministic stationarity akin to DER and dynamic non-linearity drawn in partial relation to socioecological resilience (e.g., EER) [

27]. While this article did not attempt to resolve or synthesize this diverse range of resilience scholarship, it may be reasonable to argue that both stationary (i.e., DER) and dynamic (i.e., EER) resilience processes may be happening at local and macro scales simultaneously—albeit unevenly—within and across economies. In addition, policies and investments in DER may have some endogenous and deterministic agency effect in driving or shaping both DER and EER processes and, as was argued, sustainability outcomes consistent with the Reinforcement Proposition [

28].

The key theoretical dimension is the extent to which resilience processes, including DER processes, in economies may yield sustainable outcomes and/or the extent to which sustainable outcomes support the resourcing and capacity necessary for resilience processes. Zhang, et al. raised this question by opining the following,

The sustainable improvement of economic output …refers to the extent to which the value added converges at the end of post-disaster recovery compared to its pre-disaster level. If the value added increases sustainably, it indicates that the economic system will benefit from the reconstruction process and produce better products and services. Furthermore, advanced productivity and stronger industrial linkages can better resist, absorb and recover from the shock of future disasters [emphasis added] [

27].

Zhang, et al. made an important theoretical contribution relating to value added as a collateral outcome of resilience processes driving recovery that may arise incidental to a “secondary shock” [

27]. Here, primary and secondary shocks drive the reorganization of capital and networked production systems that may provide a pathway for the introduction of alternative value regimes that allow for novel forms of economic value associated with social and environmental sustainability (e.g., ESG aligned values). By extension, the value added in the economic reorganization stimulated by DER (and possibly EER) processes—perhaps partially motivated by shared outcomes—may not only offset the costs of current resilience processes, but also provide the basis for the sustainable allocation of future resources to support resilience performance. This argument is at the heart of the Reinforcement Proposition in that resilience may drive shifts towards sustainability and sustainability may reciprocally support future resilience processes.

An additional potential theoretical benefit from resilience stimulated capital reorganization may also be a parallel and non-deterministic form of “evolutionary [economic] resilience” (EER) in the reconfiguration of relationships within the industrial structures that drive transformative adaptation [

29]. For instance, fossil fuel intensive firms who are unable to keep up with economics transitions and transformations (referenced as “Sunset Firms”) may file for bankruptcy and reemerge to build on technical and scientific labor expertise, advanced manufacturing capacities, and supply-chain connections—all processes supported by DER—to scale up low-to-no-carbon technologies and products in their adaptation to achieve sustainable outcomes (i.e., shift to “Sunrise Firms” that are ascendant in their market position). These same Sunset Firms may also be subject to non-linear processes of EER, which are entirely independent of DER processes, that dictate that such firms are broken-up in bankruptcy and their asset and intellectual property is redistributed in the economy in a way that drives asset revaluation and new industrial structures that accelerate a transformation to a sustainable economy. Both outcomes reinforce the second part of the Reinforcement Proposition that DER and EER processes may drive sustainable market transformations.

However, processes driving time- and space-dependent adaptation for some (i.e., Sunrise Firms) may also lead to time- and space-dependent maladaptation outcomes for others. As economic geographers suggest, where there is the possibility of adaptation at one scale, there may also be the prospects of maladaptation to the extent that forms of economic hysteresis may persist in the face of such capital reorganization and industrial reconfiguration [

30]. For instance, Sunset Firm labor markets that are increasingly less rigid due to DER or EER driven reorganization may feel the lagging negative effects of both post-crisis recessionary downsizing and shifts in capital investment associated with a net-zero energy transition [

31,

32]. DER driven processes may also operate to perpetuate Sunset Firms or institutional lock-in of non-sustainable markets through a narrow range of performance measures that not aligned with sustainable outcomes or co-benefits motivations. This outcome is the basis for the first part of the Conflict Proposition. In addition, DER or EER-driven or -facilitated transformations to new structures of sustainable economy may be so resource intensive and market risk intensive (e.g., highly volatile new sustainable markets based on untested technologies) that DER investments may be undervalued and under-resourced. Firms may simply question the value of maintaining stability through DER processes of a market that is so dynamic and unstable. The market may shift to a new technology or value-set prior to a fully amortized return on investment for any given DER investment. This outcome forms the logical basis for the second part of the Conflict Proposition insofar as resilience stimulated shifts toward sustainability may draw resources away from resilience. In either case, policymakers and private sector firms need to appreciate the dynamics associated with an affirmation of both the Reinforcement and Conflict Propositions.

3. The Convergence of Resilience and Sustainability in Emerging Policies

In summary, DER processes subject to multiple performance measures and sustainability defined outcomes may co-align through common objectives. This is in acknowledgment that any such relationship may also be either negatively conflicting or neutral. Risk science and economic geography have extended a deterministic form of resilience (DER) to recognize the potential for agent effects in shaping risk management and macroeconomic processes, while also opening the door among some scholars for the potential for EER that shares many common elements with socioecological resilience. DER processes may yield value added in the reorganization of capital allocations and structures necessary to support novel values in sustainability, which may, in turn, reinforce and resource resilience processes. In addition, EER may lead to adaptive and maladaptive transformations that are incidental to the post-crisis reorganization of capital investments and/or the reconfiguration of industrial structures. In this context, transformation may support the agility of economies to finds new forms of capital investment and economic structure that allows for participation in a new sustainable economy. However, sustainable economies, which may be unstable in early development phases, may be resource constrained to support DER. In the immediate context of post-COVID and post-Glasgow macro-economic policies with dual demands for resilience and sustainability, respectively, it is worth reflecting on the emergent policies and behaviors that offer some insight for the potential—whether by design and/or through evolutionary processes—to integrate objectives.

3.1. Dual Mandates in Post-Crisis Policies

Addressing linkages between sustainable economic outcomes, resilience processes, and stable economic growth necessary to drive such forces requires policy action based on a realistic theory of the role of the economy in relation to emerging risks and future crises. In 2019, the Organisation for Economic Co-operation and Development (OECD) created its New Approaches to Economic Challenges (NAEC) initiative to learn from and apply lessons based on prior financial and social crises. The NAEC warned that “a new crisis could emerge suddenly, from many different sources, and with potentially harmful effects” [

33]. This initiative argued that the lessons from the various financial crises, including the Global Financial Crisis (GFC), must inform a more radical approach to safeguarding social and environmental welfare. In this sense, the designed policy outcomes associated with DER processes were conceptualized to extend beyond financial stability to include new metrics for resilience performance that are co-aligned with the social and environmental welfare metrics (i.e., outcomes) that define sustainability and contemporary sustainable investment.

Policy subsystems are often driven by a stable cohort of legacy politicians, regulators, and interest groups that operate under the assumption that incremental policy making is driven by “dynamics [that] are endogenous to the subsystems” [

34]. Yet, agent-based financial market modeling demonstrates a great deal of exogeneity in not only the creation of financial crises, but also the market and regulatory responses thereafter [

35]. As was previously outlined, endogenous DER processes may exist in parallel with EER processes that may be shaped by both exogenous (e.g., external shocks) and endogenous (e.g., agent effects and industrial structure) phenomena. That is to say that both types of resilience may be validly considered when designing policy.

Despite a popular faith in agent-based self-correction, coordination failures among heterogeneous agents under conditions of strategic complementarity often destabilize economies despite trend-following behaviors [

36]. That destabilization may create new added value that links resilience and sustainability, or—depending on the scale and unit of analysis—it may also reinforce rigidity in industrial structures that limit the capacity of economies to adapt consistent with the Conflict Proposition. The economy is a complex adaptive system, with fundamental interdependencies among its parts with the potential for non-linear outcomes that often escape equilibrium conditions [

37]. Policymakers must recognize the limits of deterministic DER, with a recognition that instability and escape conditions may also germinate the transformations necessary to achieve sustainability. This creates a wicked policy dynamic wherein policymakers must seek short-term stability through DER in some parts of the economy and prepare for and possibly even accelerate the creative destruction of other parts of the economy to advance sustainable long-term outcomes—some of which may even be driven or shaped by EER [

38].

After the GFC, economists and policymakers broadened analytical frameworks to better assess the nexus between economic growth, inequality [

39], and environmental sustainability [

40]. Yet, post-GFC economic systems still largely utilized an approach based on managing trade-offs between competing objectives based on the value-construction of the pre-GFC and pre-climate economic order. With or without a “green stimulus,” post-COVID central bank-stimulated economies and liquidity measures run the same risk of relying on pre-crises assumptions [

41] and valuations that are undiscounted to physical and transition risks of climate change [

42]. This raises the prospects that deterministic resilience policies that blindly seek financial stability through DER may operate to reinforce an old (e.g., non-sustainable fossil fuel) economy that is broadly maladaptive over the long-term, particularly in the context of climate-driven revaluation trends driving emerging conflicts that pit the liberal world order of the vested old economy against unknown multilateral forces of the future [

43].

3.2. Practical Linkages in Physical and Transition Climate Risks

Emerging policy regimes associated with a net-zero global economic transition offer the most cogent connections for the practical linkages between DER and sustainability. At COP26 in Glasgow, the proceedings accelerated a series of emerging trends that have placed the global financial economy at the forefront of climate action. In 2009, at COP15 in Copenhagen in the middle of the GFC, countries committed to funneling

$100 billion (USD) a year in climate finance. It was a promise never kept, despite the increasing price tag for adaptation and the energy transition that runs well into the dozens of trillions of dollars [

44]. In recent years, policymakers realized the limits of bilateral and multilateral climate finance and came to terms with the recognition that countries were going to have to work together, through multilateral groups such as The Network of Central Banks and Supervisors for Greening the Financial System (NGFS), to rewrite the rules of the global financial order to advance a sustainable transition to a net-zero global economy.

At present, the most important policy tool for countries relates to public and private sector participation in measuring and disclosing of both emissions and physical and transitions climate risks. This has been accelerated by guidance and processes advanced by the Task Force on Climate-Related Financial Disclosures (TCFD), which is now the globally recognized defining standard [

45]. As countries have sought to catalyze private sector and country-specific flows of sustainable capital, they have been challenged to find common working definitions of sustainable performance and resilience (i.e., outcomes), among other foundational concepts. TCFD compliance is driving a race to standardize resilience processes and sustainability outcomes, as well as a race for climate services technologies that facilitate the resulting flow of information in market economies [

46].

Launched during COP26, one major contribution to this analytical gap was the release of the Global Resilience Index Initiative (GRII) by a consortium of NGOs and private sector financial services firms led by Oxford University [

47]. GRII was among a growing group of climate services providers vying to define the universe of data ontology for standardizing risk, resilience, sustainability assessment, and, ultimately, climate disclosure processes themselves. A closer review of these competing models often highlights common metrics and indicators for hazard exposure and vulnerability that are often identical to common sustainability indicators (e.g., water scarcity). More fundamentally, a lack of sustainability is often viewed as a vulnerability, which is often incorrectly oriented as an absolute inverse dimension to positivist resilience [

48].

These rapid policy and measurement advances offer insight into the practical convergence of DER and sustainability. In rhetorical terms, policy statements in climate finance often include undefined phrases like ‘resilient sustainability’ and ‘sustainable resilience.’ It is not clear whether stakeholders are attempting to reference two concepts caught up in the same workflow (e.g., disclosure, underwriting) or whether they view these concepts as fundamentally connected. This lack of disciplined determinism runs the risk of investments and policies in DER and other forms of resilience that do not adequately appreciate the capacity of resilience to undermine sustainability, consistent with the Conflict Proposition. A lack of awareness of a potential conflict may undermine the alignment of performance measures and the recognition of valuable co-benefits.

Despite the lack of analytical discipline in framing DER and different types of resilience, there is one area of climate finance where sustainability and resilience are viewed as deeply interconnected. This relates to the managed connections between physical and transition risks. DER is most closely aligned with the management of physical risks, whereas sustainability is viewed as a non-exclusive means to manage transition risks, particularly over the long-term. As TCFD assessment and disclosure processes mature with the more sophisticated use of scenario analysis, sustainability pathways are often used as the state variables for parametrizing dependency and systemic risks [

49].

One common emergent scenario includes the manifestation of “Green Swan” events, which are associated with a relatively rapid net-zero transition that is so disruptive that physical risks are amplified by an under-resourcing of resilience investments consistent with the Conflict Proposition [

50]. Conversely, physical impacts may cause financial stress for “Sunset” and “Sunrise” firms and industries that are seeking to manage transition risks [

51]. Additional TCFD scenarios are defined by an orderly transition to a sustainable global economy that yields additional value that both justifies and supports DER investments consistent with the Reinforcement Proposition. In these orderly scenarios, transitional change is not as disruptive as transformational change and this relative stability allows for a more clear alignment of sustainable outcomes and DER processes.

In a post-COVID and post-Glasgow global economy, many countries have adopted green growth policies as part of an effort to stimulate the economy by exploiting new markets for ESG-principled goods and services [

52]. These activities have focused on disclosure and asset revaluation through the use of market-based instruments, financial accounting, and the removal of fossil fuel subsidies in a manner that would enable an economy to reorganize in a way that balances economic growth demands and environmental sustainability [

53]. As TCFD processes mature, the interactions between resilience, sustainability, and, ultimately, adaptation are going to force the recognition of new pathways for systemic risk. In this context, policymakers will need to advance DER with full recognition of the potential for EER processes that may drive adaptations towards sustainability for some and maladaptive (e.g., Green Swan) market failure for others.

4. A Framework for Coupled Deterministic Resilience and Sustainability Policies

For policymakers to be more effective at balancing short-term financial stability through DER and long-term macroeconomic sustainability, which or may not be advanced through DER and/or EER, policymakers need a practical framework that serves as a heuristic for greater complementarity in policymaking. For instance, the identification of co-benefits may stimulate productive alignment. The general assumption among many policymakers is that robust investments in green stimulus require a measure of resilience to insulate such investments from future shocks and stresses [

2]. The standard policy is to ‘harden’ system components against a known risk or vulnerability.

Given that systemic interconnections have become blurred and often impossible to decouple, it is vital to sponsor action to increase both DER performance of designed systems and the long-term adaptive capacity of markets and firms to achieve sustainable benchmarks in the future [

1]. This dual-mandate approach recognizes that there may be non-linear trade-offs between resilience, sustainability, and, ultimately, economic growth that weight in favor of sustainable outcomes consistent with the parameters of a net-zero transition and an broader transformative adaptation necessary to supplant maladaptive elements (e.g., fossil fuel intensive industries) of the existing liberal world order broadly understood to be unsustainable [

11].

Emerging lessons from TCFD participation suggest that the ongoing irreversible financial damages [

53] are increasingly shaping the convergence of physical and transition risks that are imposing financial path dependencies on firms [

54]. DER interventions are not free, as they impose both real and opportunity costs. In normative terms, DER investments must yield additional value (or, in the language of Zhang, et al. ‘value added’) to off-set DER costs and to provide additional capital for the adjustment costs of achieving sustainable outcomes.

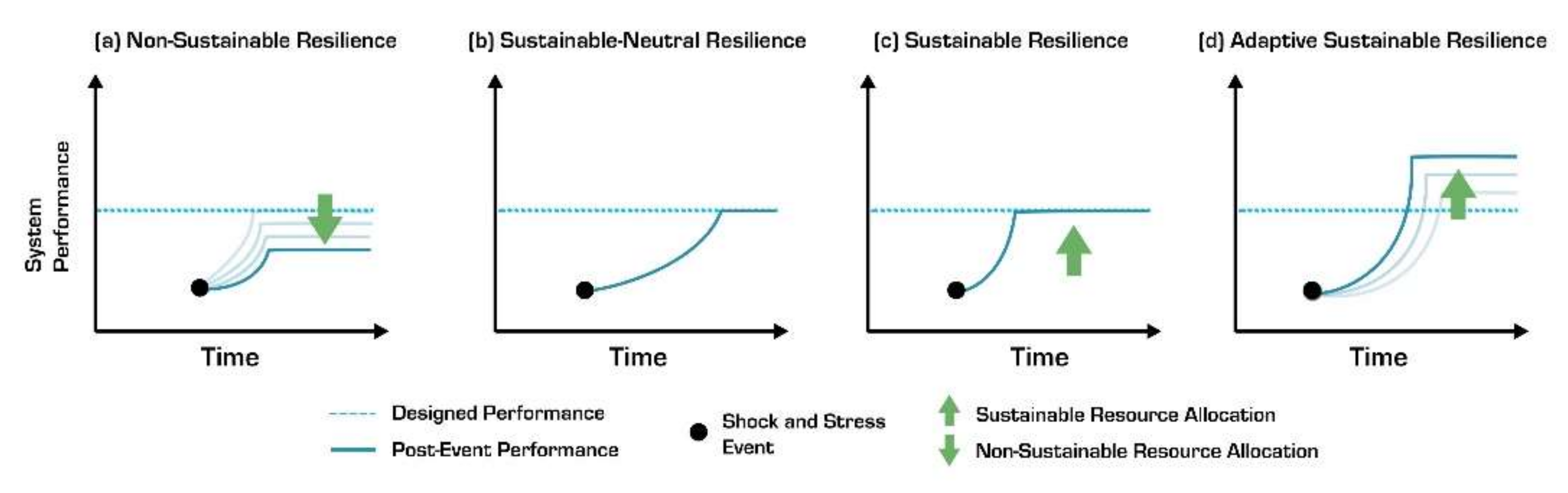

Figure 1 sets the landscape for the framework by denoting a measure of designed performance that is akin to the features of financial stability. Post-event performance assumes some measure of an immediate post-event degradation in capital stocks, output performance, and/or financial stability. As per

Figure 1a, resilience investments that are dependent on unsustainable resources or do not yield additional value to achieve sustainability outcomes may either have neutral or maladaptive outcomes overtime. Consistent with the Conflict Proposition, if DER is not a value-add-yielding process, then it may be stabilizing an economic agent, industrial sector, or structure that is inhibited or delayed from the reorganization and restructuring necessary for achieving adaptive sustainable outcomes.

DER in its theoretical state returns to a pre-perturbation state, as highlighted in

Figure 1b, and the multiple criteria for evaluating this elastic function may be relationally neutral to sustainability. However, this neutral outcome is more or less entirely theoretical because it assumes a measure of stationarity in the economic system that is independent of environmental and other systemic risk criteria that may be driving economic fluctuations and structural relationships. It should be noted that the Reinforcement Proposition and the Conflict Proposition are not universally valid as a binary objective outcomes. This recognizes the capacity, in some cases, for neutral or non-relationships to arise by and between resilience and sustainability.

Figure 1c is also a largely theoretical, if not idealized, state because it assumes a measure of equilibria between DER costs and resilience-stimulated value add that may reciprocally drive sustainably defined resource allocations that support DER processes. Hence, in

Figure 1c, with greater allocations of sustainable capital comes a greater capacity for DER performance. If DER performance criteria, and sustainability outcomes are aligned (e.g., ESG metrics and/or indicators), then maladaptive outcomes relating to systemic risks associated with global change and/or a net-zero transition (i.e., Green Swans) may be sufficiently managed. Although

Figure 1c represents a theoretical state, it is a useful frame for policymakers because they can seek to find some optimization between the costs of DER policies, the value add from DER driving sustainability, and even some measure of collateral costs associated with EER.

The predicate state of many economies and assets, particularly those dependent on fossil fuels, may not warrant a return to a pre-perturbation unsustainable state, as per

Figure 1b. As such, there is a normative conceptual alignment between resilience and sustainability wherein an allocation of sustainable resources supports a level of resilience performance that is superior to its pre-perturbation state—this is the frontier of adaptation, as represented in

Figure 1d and outlined in the Reinforcement Proposition. Sustainable resource allocation may arise from several different processes, including being (i) endogenously derived from value add of DER, (ii) exogenously derived from EER operating parallel to or independent of DER processes, and/or (iii) exogenously derived or allocated by sources entirely independent of any resilience processes.

This framework provides policymakers with a simplified heuristic to evaluate the intended and unintended costs and benefits of DER policies and investments. The framework allows for a recognition of a wide variety of performance metrics associated with the design of DER processes and the extent to which these metrics may be aligned with sustainability outcomes consistent with the Reinforcement Proposition. As such, these wider performance criteria should be evaluated to understand the extent to which resilience processes are stimulating added value that is capable of driving sustainable investments and resource allocations. Pursuant to the Conflict Proposition, it also opens the door for policymakers to evaluate the extent to which agency effects and EER may be driving adaptive or maladaptive reorganization and restructuring processes. Understanding these dynamics are arguable key for policies that efficiently, effectively, and fairly guide the distribution of resources.

5. Conclusions and Implications for Policy

This framework provides a more pragmatic understanding of what resilience policies and investments may really yield—good and bad. It imposes an obligation to conceptualize what policymakers might be able to control in terms of DER and what they might not be able to control with EER processes. Resilience processes may drive both financial stability and sustainable transitions and transformations. However, resilience processes might also be maladaptive to the extent that they reinforce Sunset Firms and industries, fossil fuel intensive economies, and other economic structures that perpetuate systemic risk.

There are currently a number of efforts underway to promote a ‘green’ recovery from COVID and to accelerate a transition to a net-zero global economy. As outlined with the Reinforcement and Conflict Propositions, these policies and investments must reflect on the potential for positively reinforcing, negatively conflicting, and neutral relationships between resilience and sustainability. The shift toward resilience processes that both support sustainable investments and are supported by sustainable investments would allow policymakers to coordinate policies across different branches within national economies by forcing recognition of a broader range of cross-cutting ESG principles (i.e., sustainable outcomes) and indicators of systemic risk (i.e., multiple resilience performance criteria).

Shared recognition may stimulate institutional coordination and consensus building that is useful for steering away from the worst impulses of unsustainable growth and the unintended distributional impacts of sustainable growth. To achieve a greater analytical understanding of the relationship between different types of resilience and sustainability, there are a number of key research areas that should be advanced. This includes the development of the next generation of lifecycle models for material assets that evaluate both emissions and environmental impacts with and without various DER and adaptation processes. These advanced lifecycle models, among other climate services-centered advancements, will help support more refined scenario analysis that sheds light on emerging relationships between physical and transition risks. Ultimately, the greatest scholarly challenge is to support economic policymakers in the development of clear definitions, standards, metrics, and indicators that set the boundaries for resilience processes and sustainable outcomes [

55].

In planning for post-COVID recovery in the short-term, systems methods offer insight into the behavior of complex systems that may improve the assessment of the consequences of DER and sustainable policy interventions [

2]. This includes thinking through tipping points, positive feedback loops, and cascading failures. COVID should not blind policymakers to the opportunities for investing in a future where economies seek not only sustainability, but also the opportunity to balance financial stability in the short-term with inevitable economic transformations in the long-term. Today, there is an opportunity to weave a new socioeconomic fabric to replace the one that has frayed under the weight of its own lack of principled recognition of social and environmental welfare. To weave this fabric, policymakers must draw closer connections between the processes, outcomes, and values of sustainability and resilience.

{kind=link}