1. Introduction

Accounting has become essential to the disclosure of information and establishment of fiscal transparency, ensuring clarity and reliability [

1]. However, at present, the development of highly competitive and developed markets has led to a constant process of innovation, causing unforeseen changes in both social, political and demographic areas [

2]. The main challenges an accountant faces are globalization, new technologies, increased competencies, changing government regulations, tax reforms, and Industry 4.0 and the 2030 Agenda [

3].

Universities must focus their efforts on educational innovation; it is necessary for traditional learning changes to promote social responsibility in students for a sustainable industry according to the 2030 agenda. This can be achieved by innovating practices in the classroom by making use of technologies, through project-based learning, which differs from traditional passive learning [

4].

Accounting must continue to evolve, and accountants must adapt to a new technological era, wherein the use of cloud technology, Big Data, block chain, and artificial intelligence all support Industry 4.0 [

5]. Here, machines have greater control in the decision-making aspects of production and maintenance, thus improving the performance, degree of automation, data visibility, and the capacity for decision making [

6,

7]. This forces accountants to develop new skills to face increasing challenges, in order to avoid being replaced by other professions, such as data scientists and technical experts [

8].

Technology continues to contribute to the constant growth in economic and financial areas, leading to greater effectiveness and efficiency in processes [

9,

10]. Similarly, the internet in the 21st century has led to the financial progression of companies, expanding their markets to all parts of the world and exchanging financial information [

11], as well as adapting traditional industries to a new digital economy and prompting accountants to master information and communications technology (ICT) and become experts in the relevant rules, regulations, and procedures [

12].

The International Auditing and Assurance Standards (IAASB) have also supported the collection of data in electronic formats, with some guidelines on how electronic information should be handled. Similarly, enterprise resource planning (ERP), or business intelligence (BI), has made accounting information available in real time, freeing accountants from routine scheduling tasks by creating new capabilities, such as the analysis and interpretation of data [

13,

14]. These are tools that help accountants to carry out various activities, facilitating better communication with departments and making their work much more efficient and effective. This has changed the role of accountants from transaction processors to company advisors [

15].

At the same time, the environment has played an important role in society and, since 1990, certain parties have been seeking to promote sustainable development [

16], which refers to the ability to satisfy the present needs without harming future generations by including environmental accounting in the economics, reporting structure and legal requirements [

17] of companies, with this integration being considered essential [

18]. However, this has presented challenges for accountants, such as in keeping accounting records of the results of environmental actions [

19].

Similarly, corporate social responsibility practices encourage positive changes in companies according to each country’s legislation. Companies must take its capital, work relations and training into account in order to implement those practices; these practices will enable companies to differ from others in the industrial sector and provide them with a positive perspective that will attract investment [

20].

Our current society demands entities that assume socio-environmental responsibilities and that can generate reports on environmental impacts to satisfy stakeholders [

21]. For this reason, the Global Compact and Global Reporting Initiative (GRI) guidelines were created to prepare reports on sustainability in a regular and standardized way, aiding compliance with socio-environmental indicators. Thus, accountants must consider their impact on the environment, whether negative or positive, and must address their results in respective financial documents [

22,

23].

In this sense, higher education institutions (HEIs) play a fundamental role in helping new accounting professionals to integrate themselves into this new technological and sustainable era [

24,

25], allowing them to innovate and adapt to the conditions and demands of Industry 4.0 and the 2030 Agenda [

26]. Similarly, teachers must help students to approach social and environmental problems, since accountants must display an advanced ecological, environmental, civic, and ethical profile [

27].

University education should help future accountants to develop skills that allow them to make decisions and form judgments, taking social responsibility, respect for diversity, and the construction of citizenship into account [

28]. They must also understand that, regarding accountants’ professional training, it is not only important to provide the tools needed to investigate, but they must also create interest in research [

29], new technologies, and the practice and execution of environmental regulations, providing them with sufficient capacity to propose initiatives that help solve environmental and social problems [

30].

Against this background, this article proposes a model that helps accounting students to acquire and improve their professional skills so as to better adapt to an Industry 4.0 and Agenda 2030 context. The model was provided to accounting students from Universidad Politécnica Salesiana in Cuenca, Ecuador in order to determine its effectiveness. The Delphi method was used to determine the competencies that accounting students should have and the best methods to acquire them.

The objective of this model is to enrich the debate around the methodology of learning professional competences in the accounting field, serving as a basis for the improvement or development of educational models that adapt to this new industrial era and the 2030 Agenda, so that new accounting graduates can help companies formulate sustainable development goals that will help them to disseminate their operating results beyond financial results. This will enable them to show that they have acquired sustainable practices with internal and external effects, since companies that have sustainable development goals are more attractive [

31].

In addition, it will prompt universities not to use just one approach when teaching, but to employ a combination of various teaching tools, such as group work, video conferencing, internships, accounting and financial software, and project-based learning. In this regard, this study aimed to improve the current teaching methods used in accounting undergraduate programs by presenting a model that uses a combination of existing methods, which is much more beneficial than when said methods are used individually. This research began in 2016 and ended in 2019 after an analysis of the students’ final grades, which helped to determine the effectiveness of the model in one university.

3. Methodology

This study involves an analysis of the existing research on accountant competencies and the efforts of universities to reduce the gap between the acquisition of knowledge and the incorporation of that knowledge into hands-on practice in companies involved in this new industrial era. Field research was also carried out to collect information and develop recommendations for how higher education could help improve accounting students’ competencies. Several methods were analyzed throughout this research to determine the most effective methods for student education, as well as the relationships between them. This enabled us to present a model to guide the teaching–learning process at universities. The model corresponded to the complexity of each year of study, the pace at which students developed knowledge, and the appropriate use of each method in each year of study. To conclude this research, we conducted an experimental trial, wherein the model was applied to undergraduate accounting students at Universidad Politécnica Salesiana’s branch campus in Cuenca, Ecuador. Below, in

Table 2, a summary of the research participants is presented.

3.1. Objectives

The study objective is to analyze the use of different educational methods and arrange them into a new model of higher education that will enable the development of competitive professional competencies, so that accounting and auditing graduates have better job opportunities in the new industrial era.

3.2. The Aim of the Research Is to Answer the Following Questions

Can new competencies be developed in accounting students so they can adapt to the goals of the 2030 agenda and be more competitive in this new industrial era?

Is it possible to develop a new model of educational methods in higher education to develop skills in accounting students for a 4.0 Industry and the 2030 Agenda?

3.3. Hypothesis Development

The development of a hybrid model of interrelated educational methods, applied progressively throughout the university career, allows for accounting and auditing students to develop competencies that help them develop their professional profile according to the needs of the companies of the new industrial era, which also relate to the context of the 2030 agenda.

3.4. Competencies Suggested by the International Federation of Accountants (IFAC)

In the present research, we considered the five professional competencies suggested by the IFAC [

45]:

Intellectual;

Technical and functional—concerning complex matters related to accounting;

Organizational and business management—demanded by the new global context;

Interpersonal and communication—essential in organizations;

Personal—related to the behavior of each individual.

These five competencies were subdivided to obtain a total of 34 competencies, as shown in

Table 3. Each classification refers to a different dimension of the individual’s personality, ranging from personal aspects to professional ones. These 34 competencies were analyzed and classified according to their level of importance during the first phase of the Delphi method. This level of importance refers to a rating based on a Likert Scale.

3.5. Participants

Our field research was based on the working with people (WWP) model, which is appropriate because it meant that the people who were directly involved in the research could actively and openly contribute and participate in the different activities that were planned by the researchers. The working with people methodology was chosen because, for a project seeking to influence the behavior of a group of people, it is important for them to learn the important aspects and areas where they want to improve from their own experience, and the WWP allows for these uncontrolled aspects to be worked with directly [

46]. Accounting experts, professors, and students took part in the research.

3.5.1. Delphi Method

The Delphi method was used to survey a panel of experts and a panel of professors and students, who were asked to evaluate the methods. This method was selected because it is a flexible tool to collect opinions from a diverse group of experts on a certain topic. It is a way of analyzing the opinions of experts with different perspectives and is widely used in doctoral or master’s degree research due to its flexibility [

47]. It is designed to gather sufficient information for decision-making. The participants do not know each other, and their responses are anonymous, which helps to obtain reliable results.

A total of 35% (16) of the experts who took part in the Delphi survey were women, and 65% (30) were men. They were between 27 and 71 years old. A total of 63% (29) of the experts had a master’s degree and 29% (13) had a Ph.D. degree or were about to complete one. The experts had broad experience in accounting and auditing, and they had management positions or were professors in university faculties. A total of 50% (23) of the experts worked only as professors, while the other 50% (23) worked both as professors and in companies.

The Delphi survey was applied in three languages (English, Spanish, and Portuguese) to 46 experts from 26 universities (

Table 4) in Australia, Bolivia, Brazil, Ecuador, El Salvador, Romania, Spain, USA, Mexico, New Zealand, the United Kingdom, and South Africa. This provided a global perspective on the competencies that accounting students must develop at university.

To contact experts, a database of universities was used. The data collection was conducted virtually. An email was sent to 950 teachers from around the world. The 46 experts selected were those who showed a willingness and enthusiasm to develop a model that helps accounting students to develop relevant skills to the new industrial era and the 2030 Agenda.

The process used in this study, according to the Delphi method, was as follows:

Prepare a database with information pertaining to accounting experts from each continent to obtain a global perspective based on their experience and the reality of the educational system in their country;

Prepare a questionnaire to collect expert opinions on the development of the 34 competencies and have it completed by the experts to obtain primary information according to their professional experience (

Appendix A);

Manage the information through factor analysis to obtain a synthesis of the results after the first phase;

Arrange the second questionnaire, the objective of which is to ask experts about the importance of each of the 17 educational methods, and their relevance to different competencies (

Appendix B);

Arrange the educational methods chosen by the experts such that they can later be applied to students.

The questionnaires were based on the recommendations provided by Stott and Ramil [

48], working at the Centro de Innovación en Tecnología para el Desarrollo Humano at Universidad Politécnica de Madrid:

Know who your study is aimed at;

Focus on the information you wish to obtain;

In the questionnaire, explain how the information will be used;

Write different types of questions to avoid a repetitive questionnaire;

Request information that allows you to determine the respondents’ profiles;

Write clear questions that encourage honest answers;

The questions must be in accordance with each other.

3.5.2. Panel with the Professors

To determine the functionality of the methods selected by the experts, a panel was held with a group of 23 professors heavily involved in the accounting undergraduate program at Universidad Politécnica Salesiana’s branch campus in Cuenca and this panel was guided by a questionnaire (

Appendix C). They were full-time professors, heads of academic areas, and professors in charge of internships and community engagement. The professors on the panel had about 10 years of teaching experience on average. In total, 91% of them had a master’s degree and the remaining 9% had a doctorate.

The aim of this panel was to address the hypothesis, which stated that the use of new educational methods will help to develop professional competencies in accounting students that are relevant to the new industrial era and the 2030 Agenda. Finally, the professors were asked to evaluate the competencies and methods.

3.5.3. Participation of the Students

To support the findings obtained using the Delphi method regarding the experts’ opinions on the best methods to develop competencies, as well as the professors’ views, accounting students from the three branch campuses of the Universidad Politécnica Salesiana in Quito, Guayaquil, and Cuenca in Ecuador were asked to respond to a questionnaire (

Appendix D). The student population consisted of 1268 students and the sample size was 320 students.

Determining Sample Size

The formula is used for samples of finite populations [

49], and the usual levels of confidence and error are used, which are 95% and 5%, respectively:

According to the formula, 295 students were obtained, but given the opportunity, 320 surveys were carried out, for which the degree of confidence remains 95% and the error was reduced to 4.74%.

The students were in different years of study. In total, 29% were men and 70% were women, while the remaining 1% did not specify their gender; 31% were first-year students, 28% second-year students, 18% third-year students, and 24% were senior students.

The information collected from the students was significant as, when combined with the WWP methodology, it enabled each student to become personally involved with the research and contribute more [

50].

Through the questionnaire, the students were asked about the methods to determine in which of them they had participated. Then, this information was used to create a hybrid model of methods based on their needs. To complement the analysis, students were also asked about the year of study in which they thought each method should be applied.

3.6. Educational Methods Applied at the Universidad Politécnica Salesiana

We analyzed the 17 educational methods used at the three branch campuses at the Universidad Politécnica Salesiana at the time this research started, during the second phase of proceedings, with the panel of experts. These methods were suggested by professors during the Academic Council meeting of the accounting and auditing undergraduate program before the start of academic period #51, in 2017, according to the guidelines of the university’s statute, whereby Article 5 states that the university must guarantee the students’ acquisition of competencies, a statement that was approved by the Ecuadorian Higher Education Council. The 17 methods were:

Students teaching accounting subjects in high schools;

Working in an accounting and tax advisory office, where students help people in the community and small-scale entrepreneurs;

Creating accounting spreadsheets;

Making financial statements in real companies;

Teaching reinforcement courses on accounting;

Learning through video conferencing;

Group work in the classroom;

Use of accounting commercial software in the classroom;

Professional internships in real companies;

Offering advice about entrepreneurship, sustainability accounting, taxation, and basic finance to people in rural communities;

Management consulting in real companies;

Individual or group tutorials;

Business simulation in the classroom;

Study of real fraud cases;

Meetings with alumni to discuss their experiences;

Learning through research and academic articles;

Project-based learning (PBL).

Each method was rated from 1 to 5 on a Likert Scale, with 1 being the most important and 5 being the least important. To reduce the methods to those that enhanced student competencies the most, factor analysis was applied.

4. Results and Discussion

The results of the quantitative and qualitative analysis of the participation of the experts, professors, and students are presented below.

4.1. Delphi Method with the Experts

Regarding the methods applied in universities, we focused on the use of methodologies that encouraged hands-on practice versus traditional theoretical methodologies. This analysis was performed using questionnaires that were answered by experts, professors, and students. Question 11 from the questionnaire asked experts about the use of traditional methods versus modern ones, wherein 89% agreed that universities must use methods that prioritize the use of hands-on activities to improve the development of competencies.

The experts explicitly pointed out that the use of more practical methods would complement the students’ education, allowing them to acquire the skills needed for their professional career, as well as generating self-confidence. They explained that if the universities devised activities or projects connected to real companies, students would acquire direct experience in the professional field. They added that the contextualization of concepts would help students to assimilate knowledge and stop them from being passive learners.

For the second stage of the Delphi method, that of working with the experts, a factorial analysis was used, which allowed for a reduction in the number of educational methods and working in the second stage of the Delphi method only with those that have the greatest interrelation. To carry out this analysis, the SPSS program was used to perform the corresponding tests, such as the chi-square values that present precise information for the validation of the analysis and after these, the results of the factorial analysis were obtained in the same software.

The chi square value seeks to determine the independence of one variable against another. The null hypothesis is that the methods are not related to each other and an alternative hypothesis is that, if they are related, the accepted significance level is 0.05, as indicated in

Table 5. If a significance lower than this value is obtained, the alternative hypothesis is considered valid, determining that the methods are interrelated and that they depend on each other.

The correlation index used was Spearman, which is generally used in factor analysis. Since this was a weak value, the correlations between the methods were high and it was possible to continue the analysis. The Kaiser–Meyer–Olkin (KMO) and Bartlett tests were performed, guided by the analysis parameters, where 0.7 < KMO was considered acceptable, confirming the validity of the analysis (

Table 5). The rotated component matrix, shown in

Table 6, demonstrates how the variables were related. For the analysis, the extraction method used was analysis of principal components and the rotation method was Varimax with Kaiser normalization

According to Martin et al., the methods are grouped according to the component in which they have the highest score, which is why they are grouped in this way [

49].

Since the coefficients of this matrix were organized by size, each component was correlated to one variable of each of the other components, resulting in three components or groups of methods (variables). At this stage of analysis, the educational models were divided into two groups. The experts who took part in the Delphi method were consulted to determine the most relevant methods in each group, and then asked to come to an agreement on the most important ones, which would then be used to develop the hybrid model.

The third component contained only one variable with no relation to any other; therefore, this method (accounting classes in high schools taught by university students) was not considered. Following these results, only 16 methods were considered for the rest of the investigation. The two groups of methods that were used in the hybrid model are presented in

Table 7, according to their importance to the development of competencies.

4.2. Panel with Professors from the Universidad Politécnica Salesiana

The panel encouraged professors to interact and determine the effects of the 17 methods on the development of student competencies. Regarding the methods applied in universities (question 4), 100% of professors believed that the use of projects in the classroom is the most effective method for the development of competencies. Therefore, this method should be applied throughout accounting undergraduate programs.

4.3. Questionnaire Given to Students

Students’ participation also included a Likert Scale rating for the educational method, regarding whether they consider the method to have influenced the development of their professional skills.

Table 8 shows the results obtained.

The results in the evaluation of the methods show that the opinion of the students confirms that the methods are highly effective in developing classroom skills. In total, 100% of students agreed that their learning would be better if their professors used hands-on practice methods more than theoretical ones. A significant number of students used several methods: 73% of the students participated in classroom activities, 68% in the research and study of academic articles, 48% in business simulations, 65% in creating accounting spreadsheets, and 64% in project-based learning. There were 10 methods in which only 11–35% of the students participated, namely the completion of financial statements of real companies; using accounting software in the classroom; undertaking internships in real companies; the study of fraud cases; the transfer of experiences of former students; learning via video conferences; undertaking courses to strengthen knowledge in accounting; running an accounting and tax advisory office; running management consultation with real companies; offering consultancy on entrepreneurship, accounting, and taxation and basic finance to rural communities.

Both experts and students provided information on when the methods should be implemented. The results are satisfying because they coincide with those of similar studies focusing on the benefits of using hands-on practice methods in the teaching and learning process, such as a study published in Argentina concerning Harvard University’s claim that one of the most effective study methods is solving new problems, which supposedly means that new challenges are raised in each situation and the simple repetition of theory is avoided [

51].

All the research techniques applied with experts, students and professors showed that the model was effective.

5. Creation of a Hybrid Model of Methods Based on the Results Obtained from the Delphi Method and the Questionnaires Applied to Students

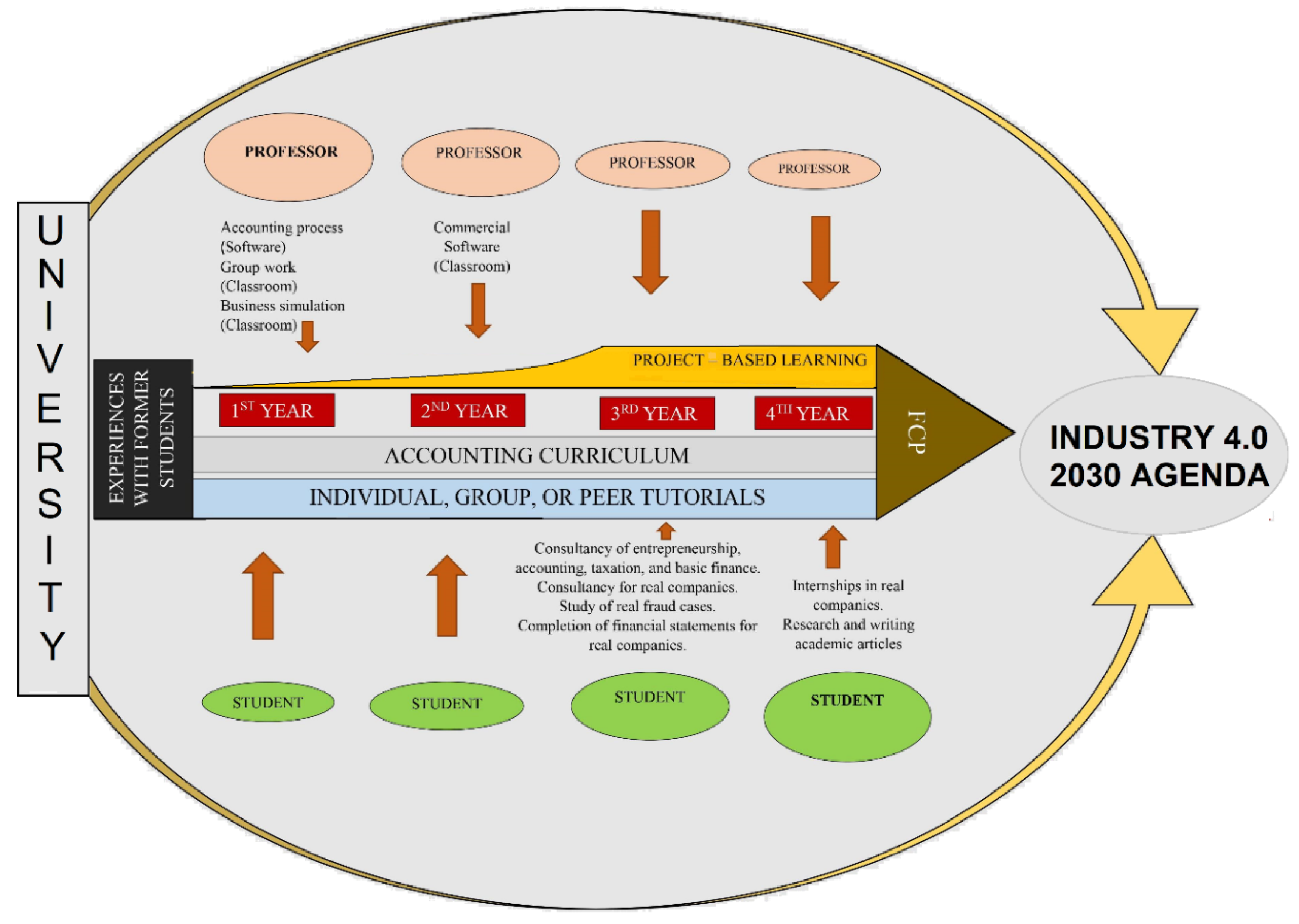

The hybrid model was created based on the results obtained via the Delphi method and students’ opinions regarding the different educational methods used in their undergraduate accounting program. Accounting programs generally take four or five years to complete. In Ecuador, where the hybrid model was applied, completing an accounting undergraduate program takes four and a half years, as well as a final graduation project. The hybrid model presents the year of study in which each method should be used; a four-year curriculum was used as the reference.

According to the results derived from the Delphi method, as well as the students’ responses and the professors’ opinions, project-based learning can be used during the entire undergraduate program in all years of study, but should be used carefully during the first year because students’ knowledge is limited. In the third year of study, it is possible to use teaching methods that incorporate knowledge and information from all the subjects being taught that year; this will enable the development of (1) negotiation skills, (2) organization skills, and (3) leadership and motivation, as well as helping with (4) the creation of project objectives, (5) the improvement of students’ fulfillment of deadlines and stages when working on projects, and (6) development of an orientation toward working on projects.

The experts agreed that tutoring should be given from the beginning to the end of the undergraduate program (four or five years, depending on the country the university is in).

When using the hybrid model of methods, professors must know that their guidance will be very important during the first year, because of the students’ limited level of knowledge. The degree of guidance will progressively decrease as the students move on, and will become almost unnecessary in their senior year, since their knowledge will have reached almost professional levels.

The research carried out by Moncada [

14] at the Universidad Técnica Particular de Loja supports the hybrid model presented in this research; it supports the idea that the involvement of students in hands-on practice activities is not only favorable for their education, but also ensures a more accurate evaluation of their academic progress, which allows universities to adjust the design of academic methods according to students’ needs.

According to the hybrid model, the methods that should be applied in the different years of study are listed below:

In the first year, to develop their ability to debate, predict needs, create projects, close contracts, develop financial skills, teamwork skills, and creativity, and become result-oriented, the methods include the use of accounting software, the undertaking of group work in the classroom, the transfer of experiences with former students, engagement in learning through research and academic articles, partaking in business simulations in the classroom, learning through video conferences and reinforcement courses, and the completion of accounting processes in spreadsheets (Excel).

Second-year students should use accounting software in the classroom and take part in the completion of financial statements in real companies; undertake management consultation in real companies; offer consultancy on entrepreneurship, accounting, taxation, and basic finance to rural communities. This will help them develop business communication skills.

Third-year students must become more involved with the completion of financial statements in real companies; undertake internships in real companies, the study of real fraud cases, and reinforcement courses; run offices offering sustainability accounting and taxation advice to the community and small companies; undertake management consulting in real companies; offer consultancy on entrepreneurship, accounting, taxation, and basic finance to rural communities to develop various competencies (reliability, human resources management, moving from theory to practice, managing stress and work pressure, identifying risks and opportunities, efficient portfolio management, ethical work practice, knowledge of laws, report preparation, the appreciation of values, and the integration of processes).

Fourth-year students must take part in the completion of financial statements in real companies, internships in real companies, the study of real fraud cases, sustainability accounting report generation, video conferences, and learning through research and academic articles related to Industry 4.0 and the 2030 Agenda. These five methods will help develop competencies such as commitment to work and an orientation toward programs.

To put the hybrid model into action, a bidirectional application strategy, as shown in

Figure 1, is required to reduce the degree of professorial guidance while increasing students’ autonomy until they complete their Final Graduation Project (FGP).

The bidirectional strategy allows for professors and students to contribute to the process of educating professionals, complemented by other quality processes [

52].

7. Conclusions

The experts who took part in the Delphi method agreed with other research [

4] that stated that universities should consistently apply more hands-on teaching methods to develop specific competencies in accounting students. Therefore, they supported the use of the hybrid model of methods. By applying the model, the accounting students were able to develop the competencies required by the job market [

25], thus precluding the need for employers to invest in additional training.

Students and professors agree that, at the university, less than 35% of students take part in hands-on practice activities, and 89% of professors agree that traditional teaching methods should be replaced [

27]. The results reflect the recommendations of experts, the favorable responses of students, and the better grades achieved in final exams and graduation projects. This model allowed for students to connect with the real world and gain a more up-to-date view of sustainability accounting [

53], Industry 4.0, the 2030 Agenda, and the future of accounting [

25].

Other studies [

54] have shown that higher education must contribute to sustainable development; therefore, the educational methods model presented in this research enables students to develop the professional skills that are needed in the context of the 2030 Agenda.

The hybrid model combines the best educational methods that can be used in accounting undergraduate programs to ensure that graduates are able to contribute to the sustainability of the new 4.0 industry and meet the needs of companies [

55].

The research states that the time spent presenting concepts in class should not exceed the time spent presenting practical case studies that simulate real situations that accounting professionals will encounter [

3]. The hybrid model of methods is a teaching approach that incorporates the active participation of professors and students into the development of competencies by the undergraduate program.

The model also contributes to the evolution of the educational system by encouraging a union between knowledge and practice [

4], and by integrating basic and specific competencies [

45]. This study suggests a flexible model, using methods in accordance with the specific context of each academic level throughout the program. This method will also enable students to properly use and disseminate their knowledge when developing competencies. The model opens the door to a debate regarding the learning methodologies used in the development of professional competences in the accounting field, serving as a basis for the improvement or development of educational models that are adapted to this new industrial era and the 2030 Agenda [

56].

This study was limited by a certain resistance to change [

57], which may have come from professors with a traditional teaching approach who are not willing to modernize their classes and adapt their mindset to the new industrial era and the 2030 Agenda.

The analysis of accountants’ competencies relates to other potential future research topics, such as (1) the significance of professional skills acquired at university when overcoming difficulties in accounting jobs in the new industrial era; (2) how to focus on the competencies accountants must have, according to the needs of different industries; (3) the analysis of the role of accountants in Industry 4.0 and the 2030 Agenda.

{kind=link}