Circular Economy and Value Creation: Sustainable Finance with a Real Options Approach

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Theoretical Background

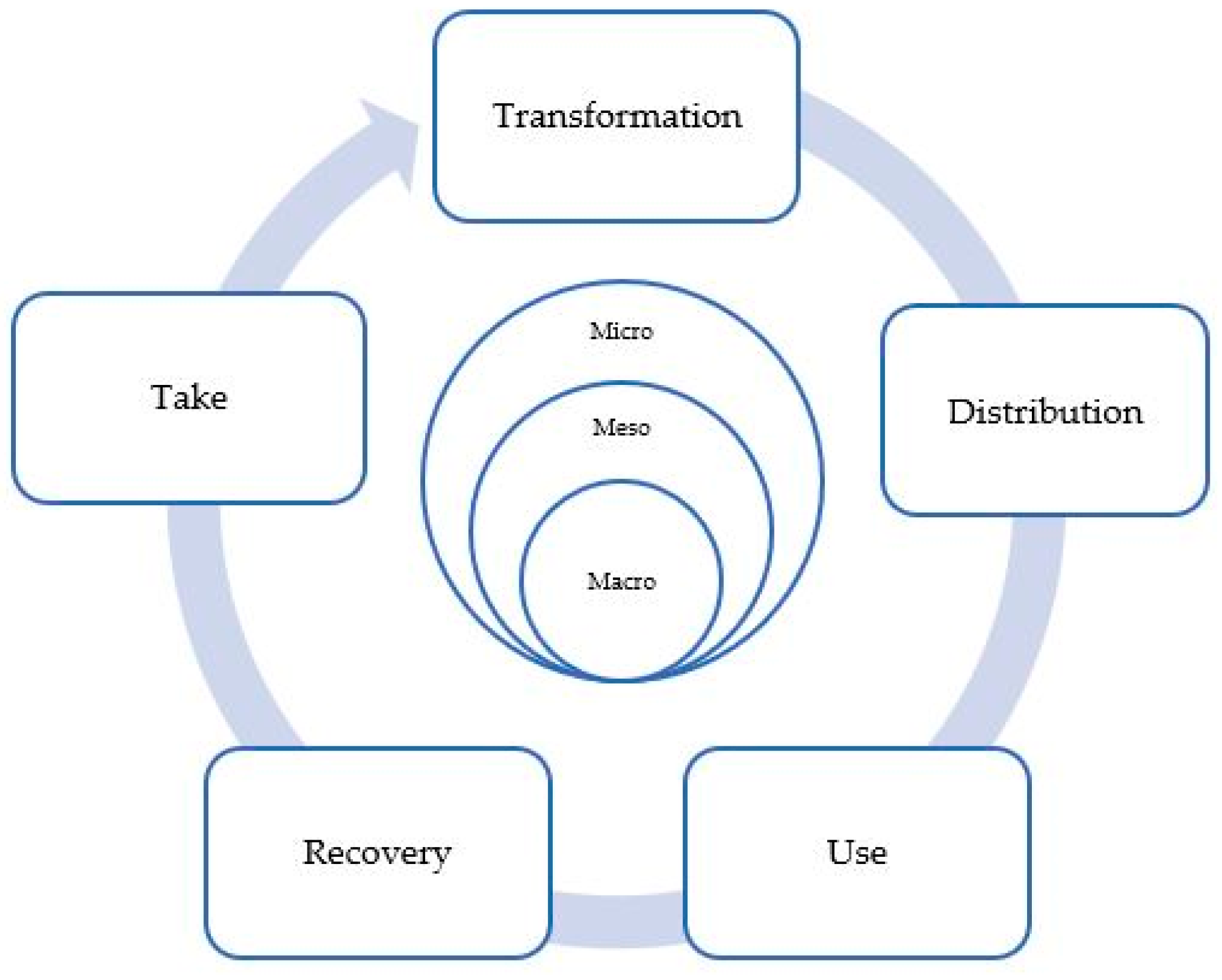

2.1. Circular Economy

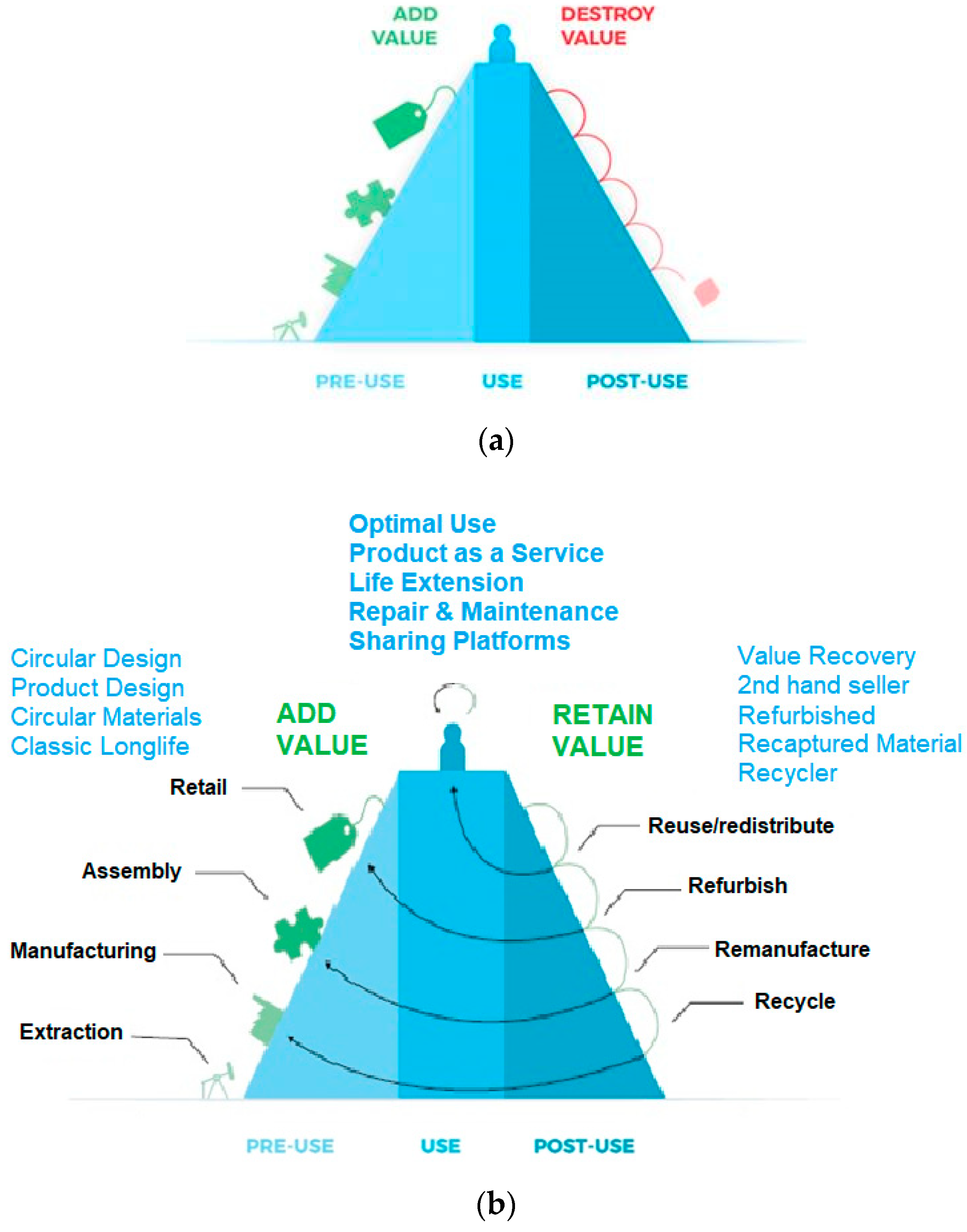

Value Hill Model and Circular Business Strategies

- Circular Design strategies are suitable for activities developed in the pre-use phase, where the company can design the product in order to allow or facilitate the use and circular post-use of the product; for example, designing a product that is easy to maintain and repair.

- Optimal Use strategies are appropriate for the use phase of the product. This category of strategies aims to optimize the use of the product through complementary services or products that allow the value of the initial product to be maintained.

- Value Recovery strategies are appropriate for the post-use phase of the product. These strategies seek to recover the value of products that have lost their usefulness.

- Network Organization strategies do not correspond to any particular phase as they aim to facilitate the functioning and coordination of the actors and the flows of resources in the value system and between the phases.

2.2. Sustainable Finance

2.2.1. Relevance of Sustainable Finance

2.2.2. Framework for Developing Non-Financial Information in the European Union

2.2.3. Sustainable Value Creation: A New Paradigm

3. Methodology

- Reuse: If the product continues to work but has no use for the current user, it is necessary to look for a new user or an alternative use for the product. The cycles of reuse involve minimum investment since the product is still in good condition (e.g., selling second-hand washing machines).

- Refurbish: This allows the product to reenter the market after minimal adjustments and aesthetic improvements (e.g., painting and changing the brakes on a used bicycle).

- Remanufacture: This involves rebuilding the product so that it has the same characteristics as a new product. Remanufacturing cycles involve a much greater investment (e.g., changing critical components of an engine so that it has the same benefits as a new one).

- Recycle: When the product can no longer be used, the components and raw materials can be recovered for the production of new products. Recycling cycles do not involve any investment because they act as a residual value (e.g., recovering metal and plastic from a mobile phone).

3.1. Circularity Value from the Classical NPV Method

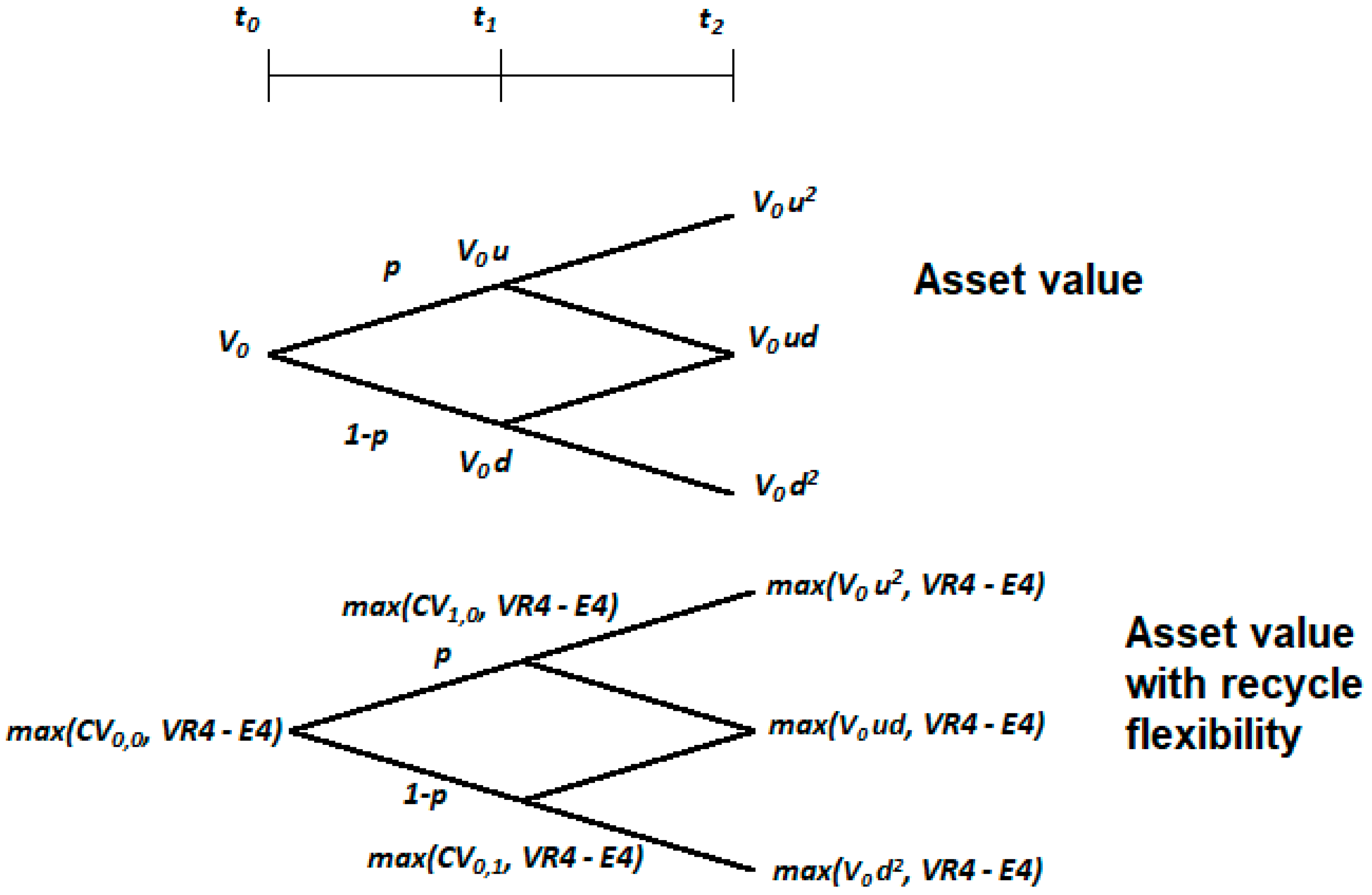

3.2. Circularity Value from Real Options Method

A Binomial Model

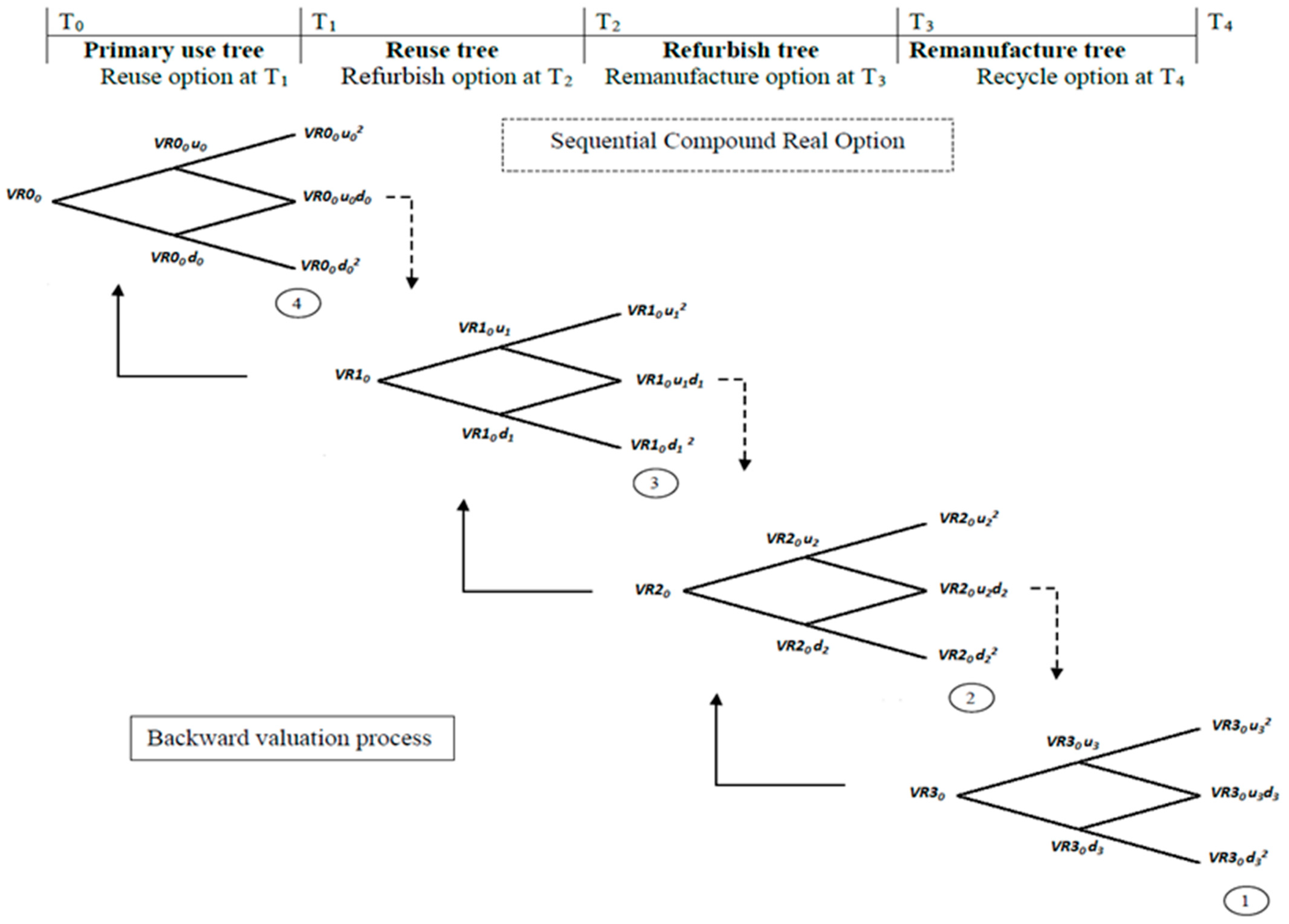

3.3. Sequential Compound Options

- Step 1. In the remanufacturing phase, a recycle option exists. The option value is computed as the difference between the remanufacture value with (VR3*) and without (VR3) flexibility. The valuation at the terminal date T4 (European style) is also distinguished from the valuation at a previous date t < T4 (American style). Figure 5 shows the scheme of sequential compound options by considering a binomial process of the value without flexibility for two periods. Specifically, we denote VR30 as the starting remanufacture value, as the up factor, as the down factor, as the volatility of the remanufactured asset value, as the depletion rate and as the risk-neutral probability of up. In this step, the flexibility onward comes from the recycle option, which, once added, produces a similar tree to the remanufacture value with flexibility. The recycle option is viewed as a single option as it corresponds to the final phase of the Value Hill. Next, we formulate the process to compute the European option value at the terminal date T4, followed by the backward recursive process to compute the American option value at a previous date where t < T4. Let τ4 = T4 − T3 be the lifetime of recycle option.

- European Style Recycling Option

- American Style Recycle Option

- Step 2. In the refurbishing phase, it is still possible to remanufacture the underlying real asset. Thus, a remanufacture option exists, the value of which is computed as the difference between the refurbish value with (VR2*) and without (VR2) flexibility. The valuation at the terminal date T3 (European style) is again distinguished from the valuation at a previous date where t < T3 (American style). As before, Figure 5 represents the binomial process of the value without flexibility for two periods, with VR20 being the starting refurbish value, the up factor, the down factor, the volatility of the refurbished asset value, the depletion rate, and the risk-neutral probability of up. By adding the value of the remanufacture option at each node of the refurbish tree, a new, extended refurbish tree may be drawn. The remanufacture option is a compound option, since it conveys the recycle option. Next, the process is formulated to compute the European option value at the terminal date T3, followed by the backward recursive process to compute the American option value at a previous date where t < T3. Let τ3 = T3 − T2 be the lifetime of remanufacture option.

- European Style Remanufacture Option

- American Style Remanufacture Option

- Step 3. In the reuse phase, an option exists in the next refurbishing phase. The option value is computed as the difference between the reuse value with (VR1*) and without (VR1) flexibility. We also distinguish the valuation at the terminal date T2 (European style) from the valuation at a previous date where t < T2 (American style). For brevity, Figure 5 depicts the binomial process of the reuse value without flexibility for only two periods, where VR10 is the starting reuse value, the up factor, the down factor, the volatility of the reused asset value, the depletion rate, and the risk-neutral probability of up. By adding the refurbish option value at each node of the reuse tree, a new extended reuse tree may be drawn. The refurbish option is also a compound option that conserves both the remanufacture and recycle options. Next, we formulate the process to compute the European option value at the terminal date T2, followed by the backward recursive process to compute the American option value at a previous date where t < T2. Let τ2 = T2 − T1 be the lifetime of refurbish option.

- European Style Refurbish Option

- American Style Refurbish Option

- Step 4. In the primary use phase, an option exists in the reuse phase. The option value is computed as the difference between the use value with (VR0*) and without (VR0) flexibility. The valuation at the terminal date T1 (European style) is also distinguished from the valuation at a previous date where t < T1 (American style). Figure 5 shows the binomial process of the primary use value without flexibility for two periods, where VR00 is the starting primary use value, the up factor, the down factor, the volatility of in-use asset value, the depletion rate, and the risk-neutral probability of up. By adding the option value at each node of the primary use tree, a new extended use tree is drawn. The reuse option is a compound option that keeps the options on refurbish, remanufacture and recycle. Next, we first formulate the process to compute the European option value at the terminal date T1, followed by the backward recursive process to compute the American option value at a previous date where t < T1. Let τ1 = T1 − T0 be the lifetime of reuse option.

- European Style Reuse Option

- American Style Reuse Option

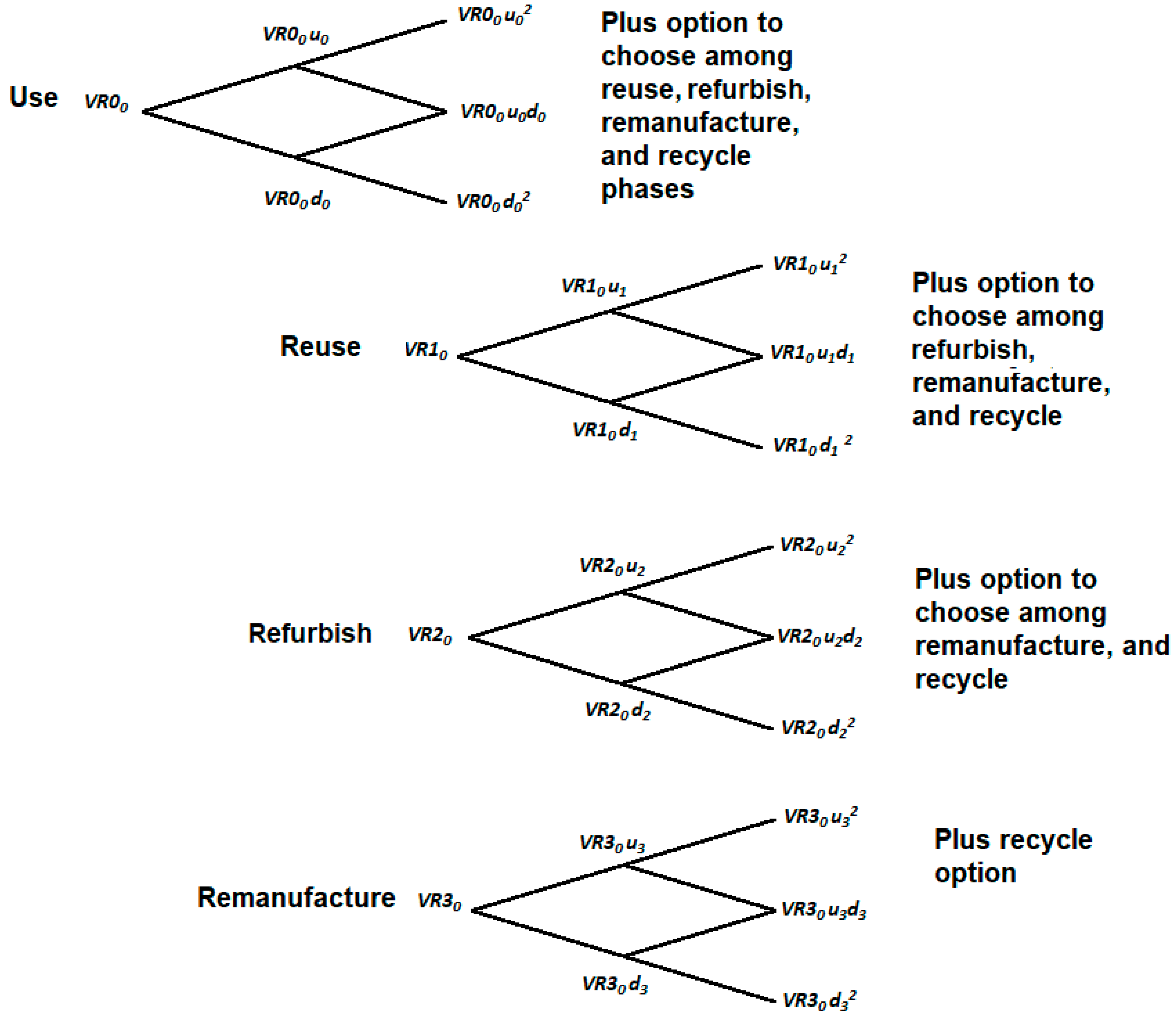

3.4. Options to Choose

- Step 1. In the remanufacturing phase, a recycle option exists (Choose Option 4). The option value is computed as the difference between the remanufacture value with (VR3*) and without (VR3) flexibility. The valuation at the terminal date T4 (European style) is also distinguished from the valuation at a previous date where t < T4 (American style). For clarity, Figure 6 shows the binomial process of the value without flexibility for two periods, with VR30 being the starting remanufacture value, the up factor, the down factor, the volatility of the remanufactured asset value, the depletion rate, and the risk-neutral probability of up. At this step, the flexibility onward comes from the recycle option, which, once added, produces a similar tree of the remanufacture value with flexibility. The recycle option is a single option as it corresponds to the final phase of the Value Hill. Next, we formulate the process to compute the European option value at the terminal date T4, followed by the backward recursive process to compute the American option value at a previous date where t < T4. Let τ4 = T4 − T3 be the lifetime of Option 4.

- European Style Choose Option 4

- American Style Choose Option 4

- Step 2. In the refurbishing phase, an option to choose between remanufacturing and recycling exists (Choose Option 3). The option value is computed as the difference between the refurbish value with (VR2*) and without (VR2) flexibility. The valuation at the terminal date T3 (European style) is also distinguished from the valuation at a previous date where t < T3 (American style). Figure 6 shows the binomial process of the value without flexibility for two periods, where VR20 is the starting refurbish value, the up factor, the down factor, the volatility of the refurbished asset value, the depletion rate, and the risk-neutral probability of up. In this phase of the Value Hill, the flexibility onward is due to the option to choose among the next two phases, remanufacturing and recycling. By adding the option value at each node of the refurbish tree, a new extended refurbish tree may be drawn. The Choose Option 3 is a compound option that corresponds to an intermediate phase of the Value Hill and keeps the recycle option. Next, we formulate the process to compute the European option value at the terminal date T3, followed by the backward recursive process to compute the American option value at a previous date where t < T3. Let τ3 = T3 − T2 be the lifetime of Option 3.

- European Style Choose Option 3

- American Style Choose Option 3

- Step 3. In the reuse phase, an option to choose between refurbish, remanufacture and recycle exists (Choose Option 2). The option value is computed as the difference between the reuse value with (VR1*) and without (VR1) flexibility. The valuation at the terminal date T2 (European style) is also distinguished from the valuation at a previous date where t < T2 (American style). Figure 6 shows the binomial process of the value without flexibility for two periods, where VR10 is the starting reuse value, the up factor, the down factor, the volatility of the reused asset value, the depletion rate, and the risk-neutral probability of up. In this phase of the Value Hill, the flexibility onward is due to the option to choose among the next three phases: refurbish, remanufacture and recycle. By adding the option value at each node of the reuse tree, a new extended reuse tree may be drawn. The Choose Option 2 is a compound option that involves both the remanufacture and recycle options. Next, we formulate the process to compute the European option value at the terminal date T2, followed by the backward recursive process to compute the American option value at a previous date where t < T2. Let τ2 = T2 − T1 be the lifetime of Option 2.

- European Style Choose Option 2

- American Style Choose Option 2

- Step 4. In the primary use phase, an option to choose between reuse, refurbish, remanufacture and recycle exists (Choose Option 1). The option value is computed as the difference between the use value with (VR0*) and without (VR0) flexibility. The valuation at the terminal date T1 (European style) is also distinguished from the valuation at a previous date where t < T1 (American style). Figure 6 shows the binomial process of the value without flexibility for two periods, where VR00 is the starting primary use value, the up factor, the down factor, the volatility of in-use asset value, the depletion rate, and the risk-neutral probability of up. In this phase of the Value Hill, the flexibility onward is due to the option to choose among the next four phases: reuse, refurbish, remanufacture and recycle. By adding the option value at each node of the primary use tree, a new extended use tree is drawn. The Choose Option 1 is a compound option that involves the refurbish, remanufacture and recycle options. Next, we formulate the process to compute the European option value at the terminal date T1, followed by the backward recursive process to compute the American option value at a previous date where t < T1. Let τ1 = T1 − T0 be the lifetime of Option 1.

- European Style Choose Option 1

- American Style Choose Option 1

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Sustainable Development Goals. Available online: https://www.un.org/sustainabledevelopment/sustainable-development-goals (accessed on 12 April 2021).

- The Paris Agreement. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed on 12 April 2021).

- United Nations Global Compact. Principles for Responsible Investment; An investor Initiative in Partnership with UNEP Finance Initiative and the UN Global Compact; UN Global Compact: New York, NY, USA, 2018; Available online: https://www.unglobalcompact.org/take-action/action/responsible-investment (accessed on 15 July 2021).

- European Commission. Closing the Loop—An EU Action Plan for the Circular Economy; Brussels, Belgium. 2015. Available online: https://www.eea.europa.eu/policy-documents/com-2015-0614-final (accessed on 15 July 2021).

- Van Putten, A.; MacMillan, I. Making Real Options Really Work. Harvard Bus. Rev. 2004, 82, 134–141. [Google Scholar]

- Finance Working Group. Money-Make the World Go Round. 2016. Available online: https://circulareconomy.europa.eu/platform/sites/default/files/knowledge_-_money_makes_the_world_go_round.pdf (accessed on 15 July 2021).

- Meadows, D.H.; Meadows, D.L.; Randers, J.; Behrens, W.W. The Limits to Growth; Potomac Associates Book-Universe Books: New York, NY, USA, 1972. [Google Scholar]

- Sauvé, S.; Bernard, S.; Sloan, P. Environmental sciences, sustainable development and circular economy: Alternative concepts for trans-disciplinary research. Environ. Dev. 2016, 17, 48–56. [Google Scholar] [CrossRef]

- Howard, T. Entropy: A New World View; Viking Press: New York, NY, USA, 1980. [Google Scholar]

- European Commission. Towards a Circular Economy: A Zero-Waste Programme for Europe; Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions; Brussels, Belgium. 2014. Available online: https://www.kowi.de/Portaldata/2/Resources/fp/2014-COM-circular-economy.pdf (accessed on 15 July 2021).

- CIRAIG (International Reference Centre for the Life Cycle of Products, Processes and Services). Circular Economy: A Critical Literature Review of Concepts; Polytechnique Montréal: Montreal, QC, Canada, 2015. [Google Scholar]

- Kirchherr, J.; Reike, D.; Hekkert, M. Conceptualizing the circular economy: An analysis of 114 definitions. Res. Conserv. Recycl. 2017, 127, 221–232. [Google Scholar] [CrossRef]

- Prieto-Sandoval, V.; Jaca, C.; Ormazabal, M. Towards a consensus on the circular economy. J. Clean. Prod. 2018, 179, 605–615. [Google Scholar] [CrossRef]

- Stahel, W.R. Circular economy. Nature 2016, 531, 435–438. [Google Scholar] [CrossRef] [PubMed]

- Yuan, Z.; Bi, J.; Moriguichi, Y.; Yuan, J. The circular economy: A new development strategy in China. J. Ind. Ecol. 2006, 10, 4–8. [Google Scholar] [CrossRef]

- Geng, Y.; Fu, J.; Sarkis, J.; Xue, B. Towards a national circular economy indicator system in China: An evaluation and critical analysis. J. Clean. Prod. 2012, 23, 216–224. [Google Scholar] [CrossRef]

- Ghisellini, P.; Cialani, C.; Ulgiati, S. A review on circular economy: The expected transition to a balanced interplay of environmental and economic systems. J. Clean. Prod. 2016, 114, 11–32. [Google Scholar] [CrossRef]

- Haas, W.; Krausmann, F.; Wiedenhofer, D.; Heinz, M. How circular is the global Economy? An assessment of material flows, waste production, and recycling in the European Union and the world in 2005. J. Ind. Ecol. 2015, 19, 765–777. [Google Scholar] [CrossRef]

- European Commission. The Circular Economy—An Investment with a Triple Win, Blogpost by European Commissioner for the Environment Carmenu Vella. 2016. Available online: http://ec.europa.eu/commission/2014-2019/vella/blog/circular-economy-investment-triple-win_en (accessed on 6 April 2021).

- Flynn, A.; Hacking, N. Setting standards for a circular economy: A challenge too far for neoliberal environmental governance? J. Clean. Prod. 2019, 212, 1256–1267. [Google Scholar] [CrossRef]

- Rizos, V.; Behrens, A.; Van der Gaast, W.; Hofman, E.; Ioannou, A.; Kafyeke, T.; Topi, C. Implementation of circular economy business models by small and medium-sized enterprises (SMEs): Barriers and enablers. Sustainability 2016, 8, 1212. [Google Scholar] [CrossRef]

- Zamfir, A.M.; Mocanu, C.; Grigorescu, A. Circular economy and decision models among European SMEs. Sustainability 2017, 9, 1507. [Google Scholar] [CrossRef]

- Demirel, P.; Danisman, G.O. Eco-innovation and firm growth in the circular economy: Evidence from European small-and medium-sized enterprises. Bus. Strateg. Environ. 2019, 28, 1608–1618. [Google Scholar] [CrossRef]

- Flynn, A.; Hacking, N.; Xie, L. Governance of the circular economy: A comparative examination of the use of standards by China and the United Kingdom. Environ. Innov. Soc. Transit. 2019, 33, 282–300. [Google Scholar] [CrossRef]

- Achterberg, E.; Hinfelaar, J.; Bocken, N. Master Circular Business Models with the Value Hill; White Paper; Circle Economy: Utrecht, The Netherlands, September 2016. [Google Scholar]

- Achterberg, E.; Hinfelaar, J.; Bocken, N. The Value Hill Business Model Tool: Identifying Gaps and Opportunities in a Circular Network. 2016. Available online: www.scienceandtheenergychallenge.nl (accessed on 15 July 2021).

- Cash, D. Sustainable finance ratings as the latest symptom of ‘rating addiction’. J. Sustain. Financ. Investig. 2018, 8, 242–258. [Google Scholar] [CrossRef]

- High-Level Expert Group on Sustainable finance. Financing a Sustainable European Economy—Final Report 2018. Available online: https://ec.europa.eu/info/sites/info/files/180131-sustainable-finance-final-report_en.pdf (accessed on 15 March 2021).

- Fullwiler, S. Sustainable Finance: Building a More General Theory of Finance; Working Paper 106; Binzagr Institute for Sustainable Prosperity. 2015. Available online: http://www.global-isp.org/wp-content/uploads/WP-106.pdf (accessed on 15 July 2021).

- Weber, O. Finance and Sustainability. In Sustainability Science: An Introduction; Heinrichs, H., Martens, P., Michelsen, G., Wiek, A., Eds.; Springer: New York, NY, USA, 2015; pp. 119–129. [Google Scholar]

- Ziolo, M.; Fidanoski, F.; Simeonovski, K.; Filipovski, V.; Jovanovska, K. Sustainable finance Role in Creating Conditions for Sustainable Economic Growth and Development. In Sustainable Economic Development Green Economy and Green Growth; World Sustainability Series; Leal, W., Pociovalisteanu, D., Quasem, A., Eds.; Springer: New York, NY, USA, 2017; pp. 187–211. [Google Scholar]

- European Parliament and Council. Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups. OJ L 330. 2014. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014L0095&from=FI (accessed on 10 April 2021).

- European Commission. TEG Report Proposal for an EU Green Bond Standard. Brussels: European Commission. 2019. Available online: https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/190618-sustainable-finance-teg-report-green-bond-standard_en.pdf (accessed on 5 April 2021).

- Cerrato, D.; Ferrando, T. The Financialization of Civil Society Activism: Sustainable finance, Non-Financial Disclosure and the Shrinking Space for Engagement. Acc. Econ. Law A Convivium. 2020, 10, 1–28. [Google Scholar] [CrossRef]

- Lagoarde-Segot, T. Sustainable finance. A critical realist perspective. Res. Int. Bus. Financ. 2019, 47, 1–9. [Google Scholar] [CrossRef]

- Dechezleprêtre, A.; Martin, R.; Bassi, S. Climate Change Policy, Innovation and Growth. In Handbook on Green Growth; Edward Elgar Publishing: Cheltenham, UK, 2019; Available online: http://www.lse.ac.uk/GranthamInstitute/wp-content/uploads/2016/01/Dechezlepretre-et-al-policy-brief-Jan-2016.pdf (accessed on 25 March 2021).

- Galeotti, M.; Salini, S.; Verdolini, E. Measuring Environmental Policy Stringency: Approaches, Validity, and Impact on Environmental Innovation and Energy Efficiency. Energy Policy 2020, 136, 111052. [Google Scholar] [CrossRef]

- Lovell, H.; MacKenzie, D. Accounting for carbon: The role of accounting professional organisations in governing climate change. Antipode 2011, 43, 706–752. [Google Scholar] [CrossRef]

- Villiers, C.; Mähönen, J. Accounting, auditing, and reporting: Supporting or obstructing the sustainable companies objective? In Company Law and Sustainability: Legal Barriers and Opportunities; Sjåfjell, B., Richardson, B., Eds.; Cambridge University Press: Cambridge, UK, 2015; pp. 175–225. [Google Scholar]

- Gelmini, L.; Bavagnoli, F.; Comoli, M.; Riva, P. Waiting for materiality in the context of integrated reporting. In Sustainability Disclosure: State of the Art and New Directions; Songini, L., Pistoni, S., Eds.; Emerald Group: Bingley, UK, 2015; pp. 135–162. [Google Scholar]

- Baumuller, J.; Schaffhauser-Linzatti, M. In search of materiality for nonfinancial information-reporting requirements of the directive 2014/95/EU, MM. Sustain. Manag. Forum 2019, 26, 101–111. [Google Scholar]

- Paranque, B. Enterprise beyond the Firm; Working Paper; KEDGE Business School: Talence, France, 2014. [Google Scholar]

- Schinckus, C. Positivism in finance and its implication for the diversification of finance research. Int. Rev. Financ. Anal. 2015, 40, 103–106. [Google Scholar] [CrossRef]

- Walter, C. The financial logos. The framing of financial decision making by mathematical modelling. Res. Int. Bus. Financ. 2016, 37, 597–604. [Google Scholar] [CrossRef]

- Alijani, S.; Karyotis, C. Sustainability: Finance, Economy, and Society; Emerald Group Publishing: Bingley, UK, 2016. [Google Scholar]

- Boussard, V. Finance at Work; Routledge: Abingdon, UK, 2016. [Google Scholar]

- Lawson, T. The Nature and State of Modern Economics. Economics as Social Theory; Routledge: Abingdon, UK, 2015. [Google Scholar]

- Zeidan, R. Obstacles to sustainable finance and the covid19 crisis. J. Sustain. Financ. Investig. 2020. [Google Scholar] [CrossRef]

- Fatemi, A.; Fooladi, I. Sustainable finance: A new paradigm. Glob. Financ. J. 2013, 24, 101–113. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.; Mishra, D. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Plumlee, M.; Brown, D.; Hayes, R.; Marshall, S. Voluntary Environmental Disclosure Quality and Firm Value: Further Evidence; Working Paper; University of Utah: Salt Lake City, UT, USA; Portland State University: Portland, OR, USA, 2010. [Google Scholar]

- Goss, A.; Roberts, G. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Hawn, O.; Loannou, I. Do Actions Speak Louder than Words? The Case of Corporate Social Responsibility (CSR); SSRN Working Paper Series; Academy of Management: Briarcliff Manor, NY, USA, 2012; p. 14137. [Google Scholar]

- Eccles, R.; Ioannou, I.; Serafeim, G. The Impact of a Corporate Culture of Sustainability on Corporate Behavior and Performance; National Bureau of Economic Research Working Paper Series No. 17950; Harvard Business School: Boston, MA, USA, 2012. [Google Scholar]

- Blázquez, F.C.; González, A.G.; Sánchez, C.S.; Rodríguez, V.D.; Salcedo, F.C. Waste valorization as an example of circular economy in extremadura (Spain). J. Clean. Prod. 2018, 181, 136–144. [Google Scholar] [CrossRef]

- Trigeorgis, L.; Reuer, J. Real options theory in strategic management. Strateg. Manag. J. 2017, 38, 42–63. [Google Scholar] [CrossRef]

- Myers, S.C. Determinants of corporate borrowing. J. Financ. Econ. 1977, 5, 147–175. [Google Scholar] [CrossRef]

- Myers, S.C. Finance Theory and Financial Strategy. Interfaces 1984, 14, 126–137. [Google Scholar] [CrossRef]

- Trigeorgis, L.; Mason, S.P. Valuing Managerial Flexibility. Midl. Corp. Financ. J. 1987, 5, 14–21. [Google Scholar]

- Trigeorgis, L. Real Options and Interactions with Financial Flexibility. Financ. Manag. 1993, 22, 202–224. [Google Scholar] [CrossRef]

- Savolainen, J. Real options in metal mining project valuation: Review of literature. Res. Policy 2016, 50, 49–65. [Google Scholar] [CrossRef]

- Marques, J.; Cunha, M.; Savić, D.; Giustolisi, O. Water network design using a multiobjective real options framework. J. Optim. 2017, 2017, 4373952. [Google Scholar] [CrossRef]

- Erfani, T.; Pachos, K.; Harou, J.J. Real-options water supply planning: Multistage scenario trees for adaptive and flexible capacity expansion under probabilistic climate change uncertainty. Water Resour. Res. 2018, 54, 5069–5087. [Google Scholar] [CrossRef]

- Pringles, R.; Olsina, F.; Garcés, F. Real option valuation of power transmission investments by stochastic simulation. Energy Econ. 2015, 47, 215–226. [Google Scholar] [CrossRef]

- D’Halluin, Y.; Forsyth, P.A.; Vetzal, K.R. Wireless network capacity management: A real options approach. Eur. J. Oper. Res. 2007, 176, 584–609. [Google Scholar] [CrossRef][Green Version]

- Cassimon, D.; De Backer, M.; Engelen, P.J.; Van Wouwe, M.; Yordanov, V. Incorporating technical risk in compound real option models to value a pharmaceutical R&D licensing opportunity. Res. Policy 2011, 40, 1200–1216. [Google Scholar]

- Fan, Y.; Zhu, L. A real options-based model and its application to China’s overseas oil investment decisions. Energy Econ. 2010, 32, 627–637. [Google Scholar] [CrossRef]

- Zhu, L.; Fan, Y. A real-options-based CCS investment evaluation model: Case study of China’s power generation sector. Appl. Energy 2011, 88, 4320–4333. [Google Scholar] [CrossRef]

- Zhang, M.M.; Zhou, P.; Zhou, D.Q. A real options model for renewable energy investment with application to solar photovoltaic power generation in China. Energy Econ. 2016, 59, 213–226. [Google Scholar] [CrossRef]

- Cox, J.C.; Ross, S.A.; Rubinstein, M. Option Pricing: A Simplified Approach. J. Financ. Econ. 1979, 7, 229–263. [Google Scholar] [CrossRef]

- Tufano, P. A Real-World Way to Manage Real Options. Harvard Bus. Rev. 2004, 82, 90–99. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rodrigo-González, A.; Grau-Grau, A.; Bel-Oms, I. Circular Economy and Value Creation: Sustainable Finance with a Real Options Approach. Sustainability 2021, 13, 7973. https://doi.org/10.3390/su13147973

Rodrigo-González A, Grau-Grau A, Bel-Oms I. Circular Economy and Value Creation: Sustainable Finance with a Real Options Approach. Sustainability. 2021; 13(14):7973. https://doi.org/10.3390/su13147973

Chicago/Turabian StyleRodrigo-González, Amalia, Alfredo Grau-Grau, and Inmaculada Bel-Oms. 2021. "Circular Economy and Value Creation: Sustainable Finance with a Real Options Approach" Sustainability 13, no. 14: 7973. https://doi.org/10.3390/su13147973

APA StyleRodrigo-González, A., Grau-Grau, A., & Bel-Oms, I. (2021). Circular Economy and Value Creation: Sustainable Finance with a Real Options Approach. Sustainability, 13(14), 7973. https://doi.org/10.3390/su13147973