Unpacking the IFRS Implications of COVID-19 for Travel and Leisure Companies Listed on the JSE

Abstract

:1. Introduction

2. Literature Review

- The cash-to-cash sequence of the company, as well as their liquidity;

- The financial effect on variable costs;

- The implementation of a capital investment plan.

3. Methodology

3.1. Research Approach

3.2. Data Collection and Procedure

3.3. Sampling

4. Results and Discussion

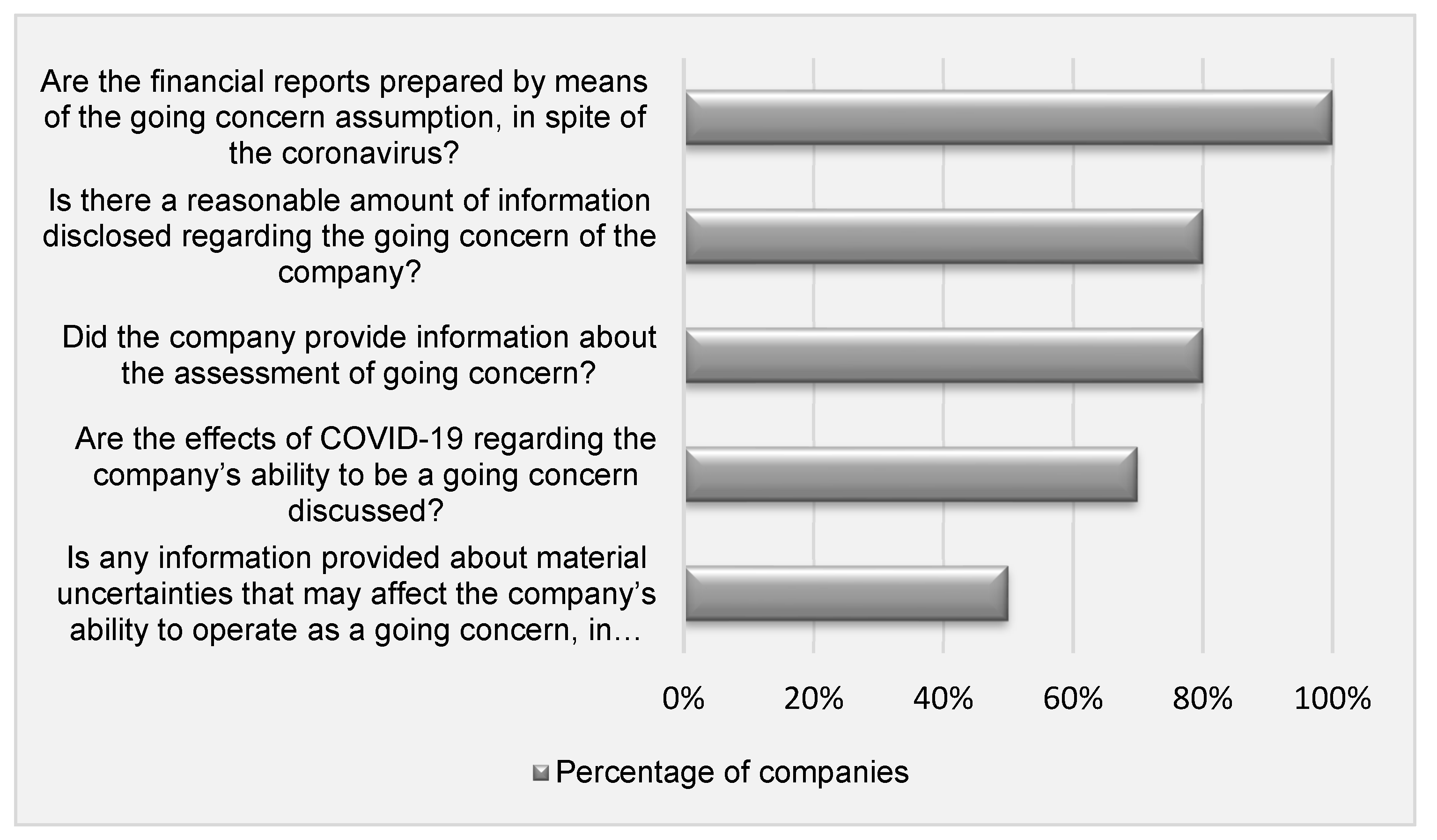

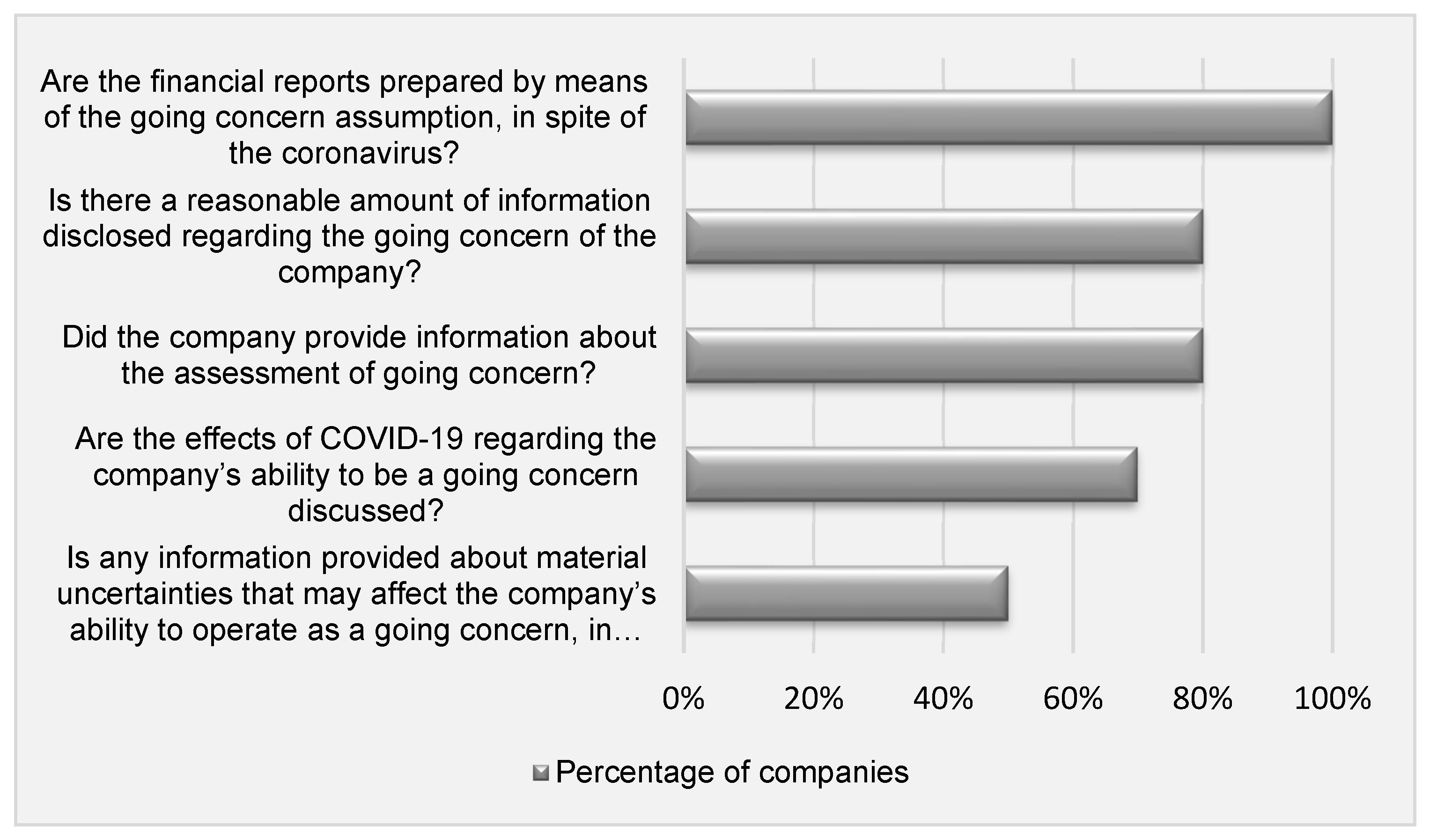

4.1. Going Concern

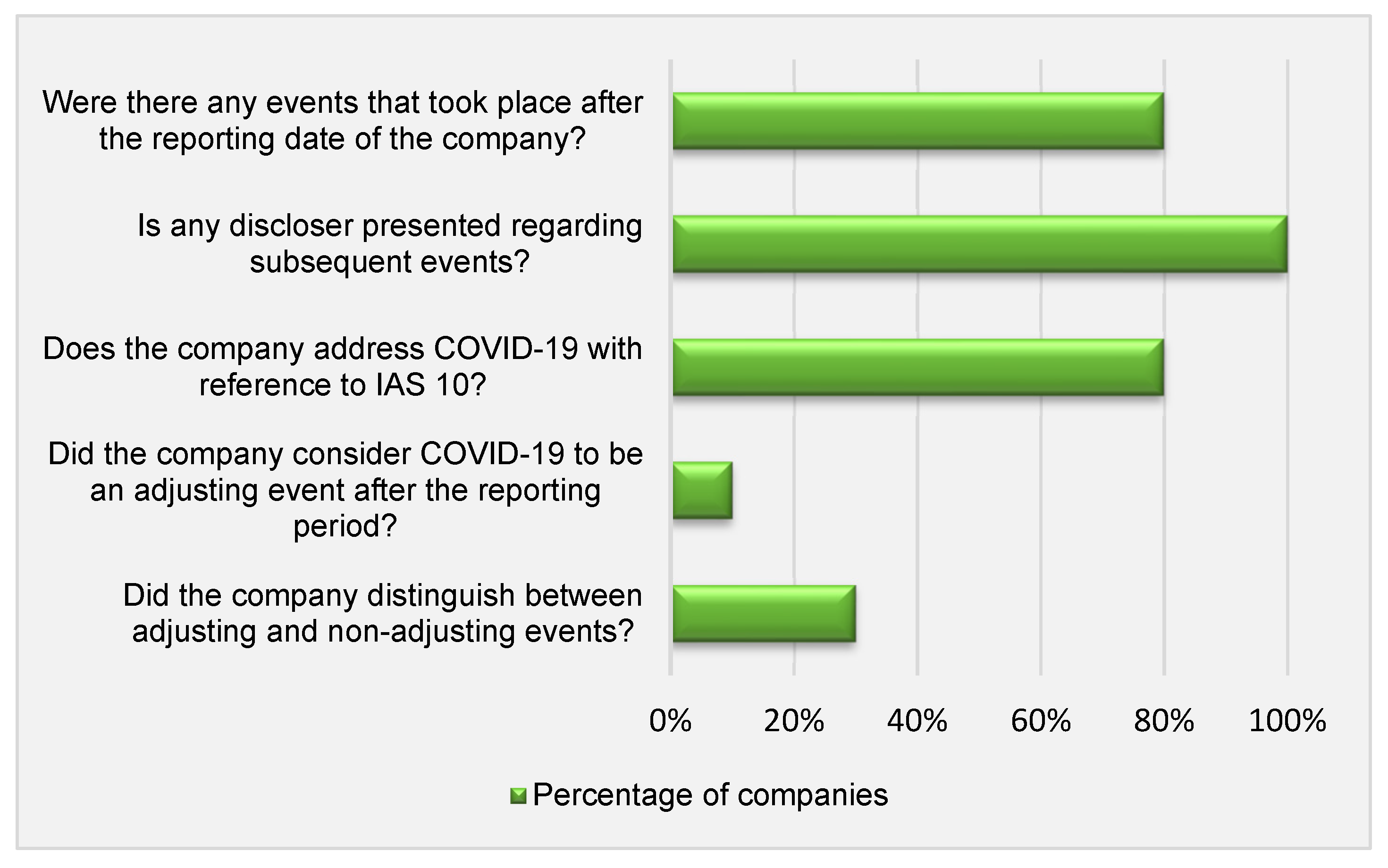

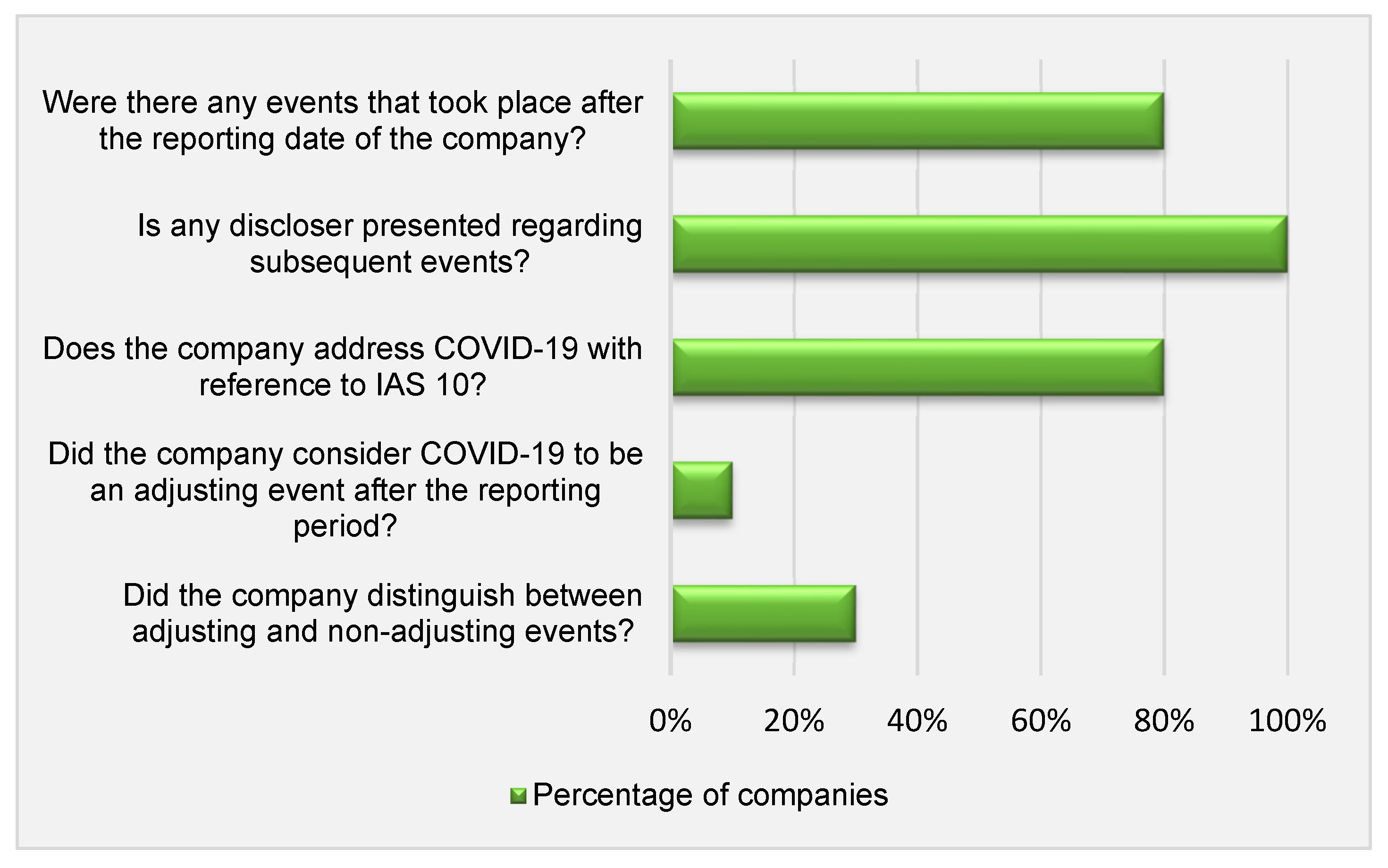

4.2. Events after the Reporting Period

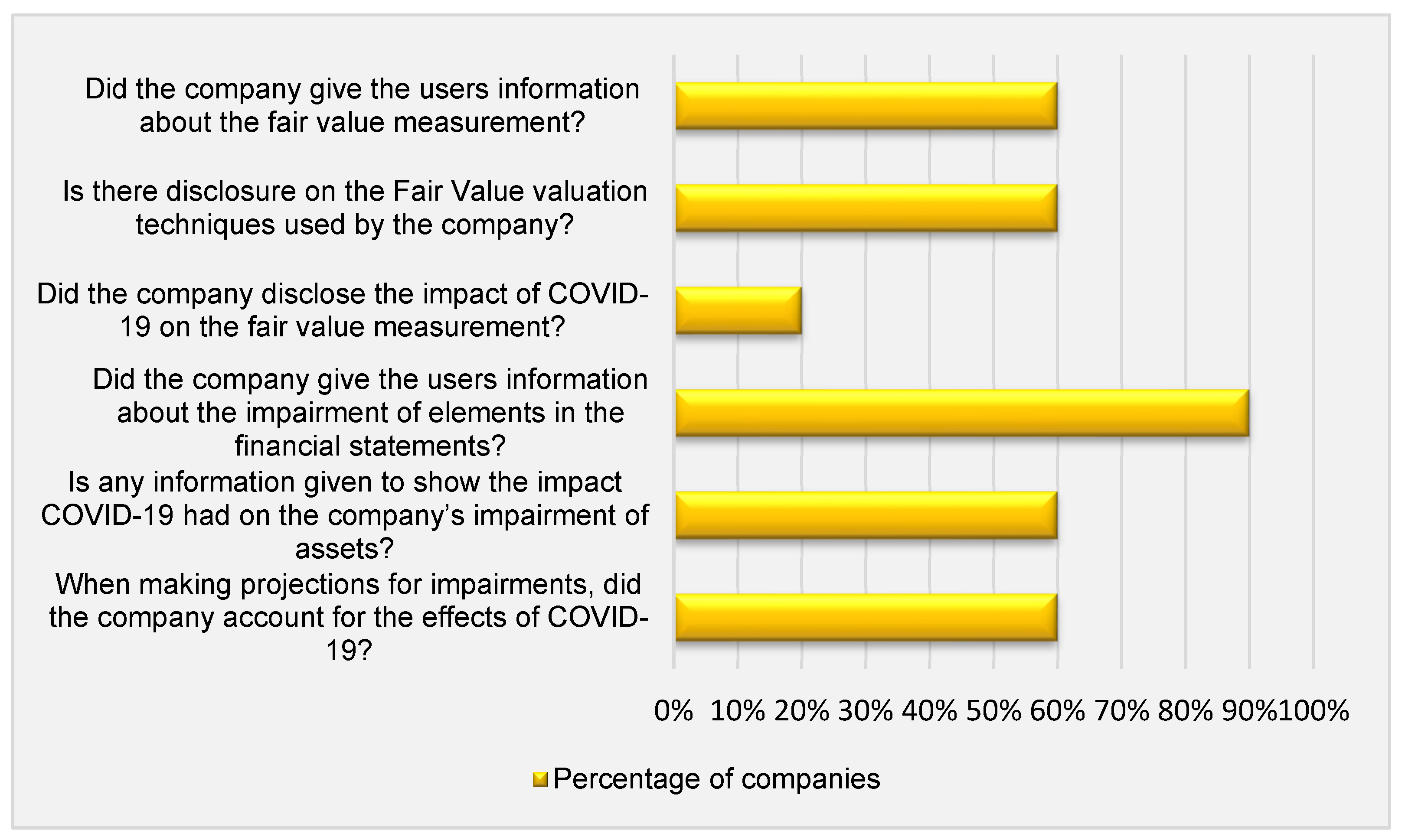

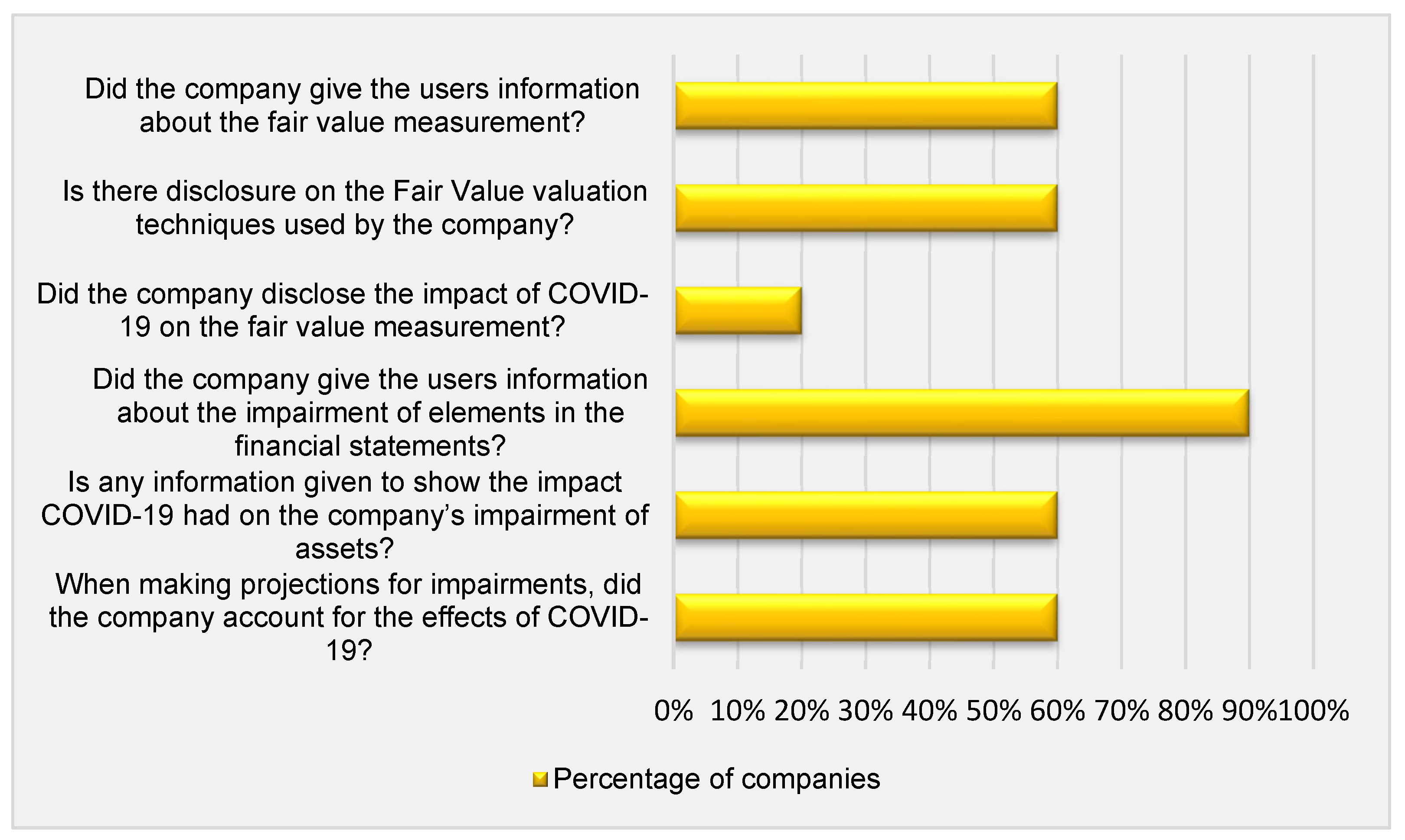

4.3. Fair Value Measurement and Impairment

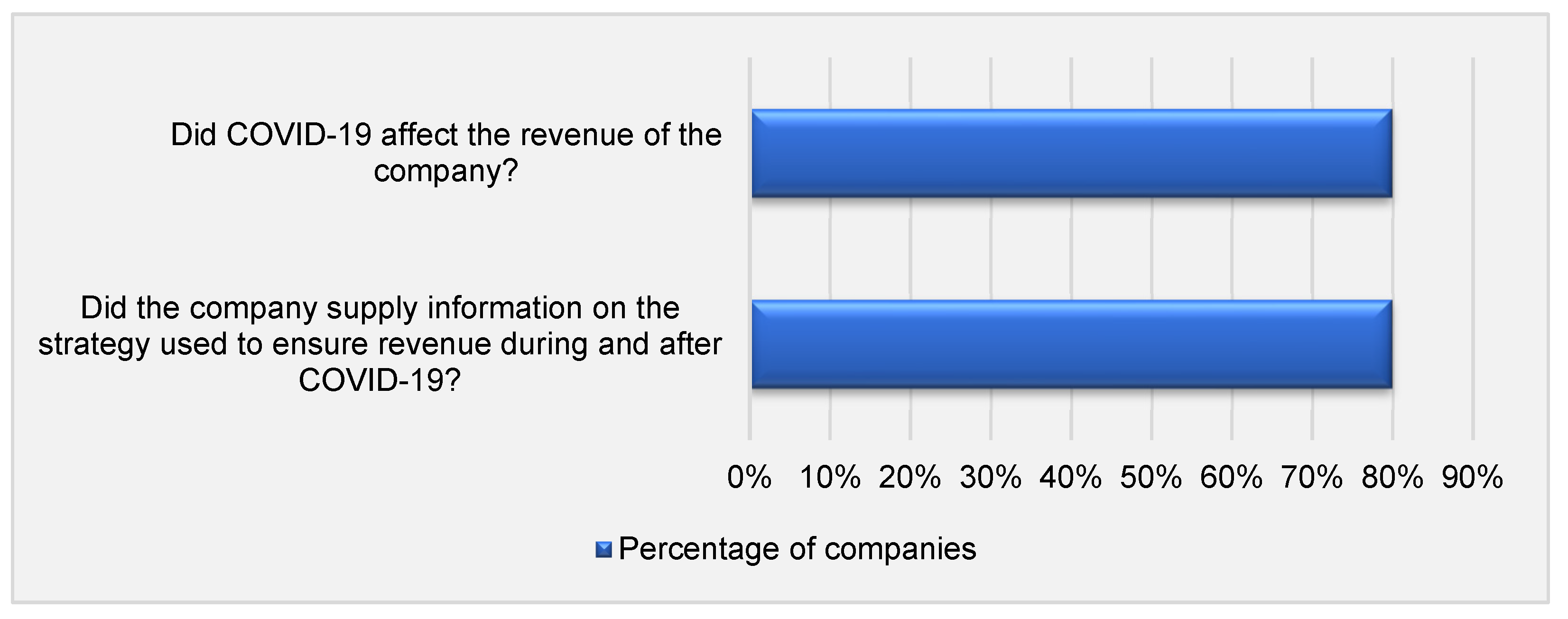

4.4. Revenue Recognition

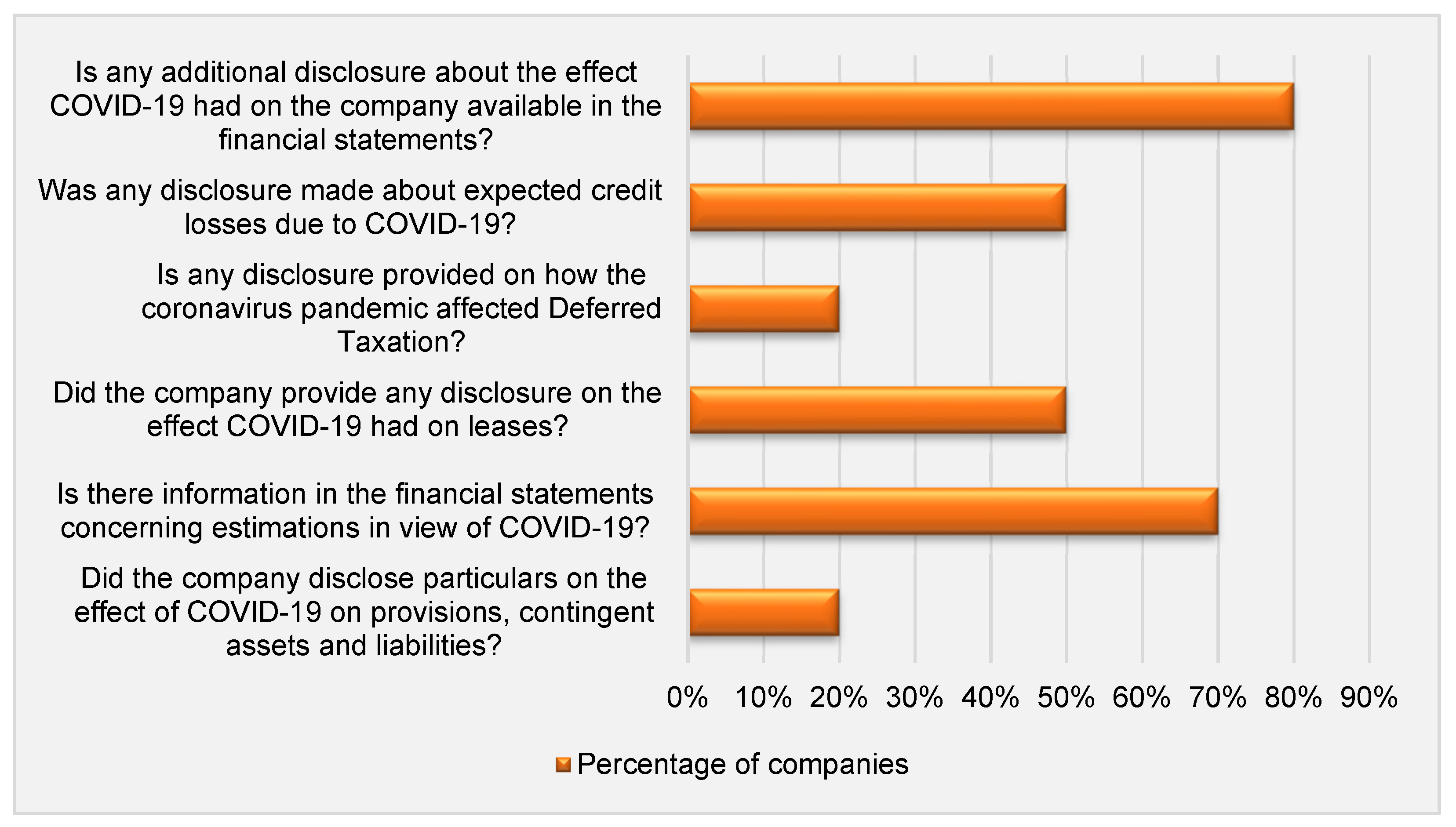

4.5. Other Financial Statement Disclosures

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company Name | About the Company | Address & Contact Details | Auditor | Total Assets | Interesting Facts |

|---|---|---|---|---|---|

| Arden Capital Limited | The Arden Capital company is a Mauritian diversified investment holding company and is listed on the JSE. This company invests in assets that are consumer-facing and cash-generative. Their aims include building a portfolio that will deliver capital growth, with the focus on Zimbabwe. | c/o Adansonia Management Services Limited Suite 1, Perrieri Office Suites, C2-302, Level 3, Office Block C, La Croisette, Grand Baie, 30517, Republic of Mauritius. Tel: +230 269 4166 Fax: +230 468 1267 Email: investorrelations@arden-capital.com Webpage: https://www.arden-capital.com/ (accessed on: 22 May 2021). | Independent Statutory Auditors: Deloitte Business Registration Number: P10019073, 7th–8th Floor, Standard Chartered Tower, 19–21 Bank Street, Cybercity, Ebène, Réduit 72201, Mauritius JSE Accredited Independent Auditors: Deloitte 5 Magwa Crescent, Waterfall City, 2090, Johannesburg, Gauteng, South Africa | On 30 June 2020 the company had a total of US$124,700,632 assets. The year before on 30 June 2019 the company had a total of US$122,998,117 assets. | Arden Capital Limited is formerly known as Brainwork Limited. The Arden Capital group structure includes Arden Capital (Private) Limited 100%; African Sun Limited 57.67%; Dawn properties Limited 66.81%; FML 100%. The board of Arden Capital Limited endorses the King IV principles as part of the company’s corporate governance and has four separate committees to assist with the corporate governance of the company. |

| City Lodge Hotel Group Limited | The City Lodge Hotel Group has a variety of hotels not only in South Africa but across the African continent. The hotels that form part of this group are dedicated to providing their guests with comfort at the level that suits each individual guest’s needs. The company’s vision is to be recognised as the preferred hotel group in sub-Sahara Africa. With values that include, caring for guests and the communities in which the company situated. | The Lodge” Bryanston Gate Office Park, Corner Homestead Avenue and Main Road, Bryanston. P.O. Box 97, Cramerview, 2060. Telephone: +27 11 557 2600 Fax: +27 11 557 2601 Email: info@clhg.com Reservations: 0800 11 37 90 Webpage: https://clhg.com/ (accessed on: 22 May 2021). | KPMG Crescent 85 Empire Road Parktown Johannesburg 2193 | For the year ended 30 June 2020 the City Lodge Hotel Group had total assets to the amount of R3,858,404,000. As for in the 2019 financial year the company had assets to the value of R3,025, 728,000. | For the year ending 30 June 2020 the City Lodge Hotel Group Limited had a revenue of R1,16bn. The dividend declared by the City Lodge Hotel Group Limited amounted to 153,0c per share for the 2020 financial year. |

| Comair Limited | Comair is an aviation and travel group founded in 1946 and has been operating in Southern Africa for over six decades. The company also has an internationally recognised safety record. Since 1996, the company has serviced local and regional routs under the British Airways livery. This forms part of the licence agreement the company has with British Airways. In 2001 Comair launched Kulula. This was the first low-cost airline for South Africa. Interestingly, the word “kulula” means easily in the Zulu Language. | Head Office Telephone Number: +27 (0) 11 921 0111 Physical Address: 1 Marignane Drive Bonaero Park South Africa 1619 Email: cr@comair.co.za Webpage: https://www.comair.co.za/ (accessed on: 22 May 2021). | BDO South Africa Incorporated Wanderers Office Park 52 Corlett Drive Illovo, 2196 | On 31 December 2019 Comair had a total of R8,698,226,000 assets. For the unaudited 6-month period on 31 December 2018 the company had total assets amounting to R6,616,108,000. | The Comair Limited brand includes two airline brands namely British Airways and Kulula.com. Across the two brands Comair Limited operates 26 Boeing 737 aircrafts. The company’s fleet furthermore comprises of 23x next-generation Boeing 737–800s, 3x Boeing 737–400, 10x next-generation Boeing 737–800s, 3x Boeing 737–400s, and lastly 13x next-generation Boeing 737–800s |

| Famous Brands Limited | Famous Brands Limited is Africa’s leading branded food service franchisor. Famous Brands dates back to the year 1960. During this time a family started a business with a limited supply chain and comprised of one brand, known as Steers. The company operates franchised, master license and company-owned restaurants. The three core pillars of the company include: Brands, Manufacturing and Logistics. Famous Brands portfolio consists of 24 restaurant brands including, Steers, Wimpy, Mugg & Bean, Debonairs Pizza and House of Coffees, to name a few. In South Africa, the rest of Africa, the Middle East and the United Kingdom, the company has a total of 2 898 restaurants. | Head Office Tel: +27 11 315 3000 Webpage: https://famousbrands.co.za/ (accessed on: 29 February 2020). Address: 478 James Crescent, Midrand, Gauteng Postal Address: P.O. Box 2884, Halfway House, 1685 | Deloitte & Touche Deloitte 5 Magwa Crescent Waterfall City Waterfall Docex 10 Johannesburg | This company had a total of R6,173,171,000 assets as at 29 February 2020. At the end of the 2019 financial year the company had a total of R4,959,933,000 assets. | Famous Brands has the vision to be the leading innovative food service and branding franchised business in South Africa as well as in other selected markets. The company’s core values include: Growth; Quality; Humility; Speed; Agility; Innovation; Integrity. The company was listed on the JSE in the year 1994. |

| Hosken Passenger Logistics and Rail Limited | Hosken Passenger Logistics and Rail Limited (HPL & R) is a company focused on investments in the mobility and logistics sector. Currently the company has a portfolio in the commuter bus and luxury coach segments. The company has over 157 years of expertise. HPL & R) has a number of investments. The company has a 100% investment in Golden Arrow Bus Services; 100% investment in Sibanye Bus Services; 33.33% investment in N2 Express; 76% investment in the company Eljosa Travel & Tours; lastly. the company has a 100% investment in Table Bay Rapid Transit. | 103 Bofors Circle Epping Industria 7460 P.O. Box 115 Cape Town 8000 Tel 021 507 8800 Fax 021 534 8818 Email info@hplr.co.za Webpage: https://www.hplr.co.za/ (accessed on: 22 May 2021). | BDO South Africa Incorporated. 6th Floor, 123 Hertzog Boulevard, Foreshore, Cape Town, 8001 (P.O. Box 3883, Cape Town, 8000) | As at 31 March 2020 the company had total assets to the value of R2,363,634,000. Furthermore, as at 31 March 2019 the company’s total assets amounted to R2,220,330,000. | For the 2020 financial year Golden Arrow’s fleet consumed 2.53 km/L of fuel. The Sibanye Bus Services employed 2534 staff members and travelled a total of 65 million km. Table Bay Rapid Transit travelled a total of 4.1 million km and employ 237 staff members. Lastly for the 2020 financial year ended on 31 March 2020 the Eljosa Travel & Tours company travelled a total of 2.8 million km. |

| LUXE Holdings Limited | The company has a dream to be the preferred premium watch and jewellery retailer in South Africa. They strive to deliver a memorable shopping experience to all customers and have a work environment that inspires the employees of the company to always give their best to the company and its customers. LUXE Holdings states that the company’s purpose is to put the customer at the centre of everything they do by delivering an affordable and premium luxury experience. | P.O. Box 784429 Sandton, 2146 Tel: +27(0) 11 669 5600 Email: info@luxeholdings.co.za Webpage: https://www.luxeholdings.co.za/ (accessed on: 22 May 2021). | BDO South Africa Incorporated Wanderers Office Park 52 Corlett Drive Illovo, 2196 | For the year ended 29 February 2020 LUXE Holdings had assets to the total of R468,160,000. As for the year before, on 29 February 2019 LUXE Holdings had a total of R258,514,000 assets. | LUXE Holdings offers a diversified portfolio that is focused on first time jewellery buyers. Arthur Kaplan, NWJ Jewellery and World’s Finest Watches are some of the brand included in the LUXE Holdings Limited company. The company includes the values of leadership, quality, diversity, passion, accountability, integrity, collaboration, innovation and service excellence as part of their vision for a better company. |

| Spur Corporation Limited | The Spur Corporation is primarily a franchisor. The company supports and manage franchised restaurant operations utilising their skills, support structures, experiences and more. | Registered office: 14 Edison Way, Century Gate Business Park, Century City, 7441 Telephone: 021-555-5100 E-mail: spur@spur.co.za Webpage: https://www.spurcorporation.com/ (accessed on: 22 May 2021). | KPMG Incorporated Registered Auditor The Halyard 4 Christiaan Barnard Street Cape Town City Centre 8000 | For the six months ended 31 December 2019 the company had total assets amounting to R869,707,000. In the 2018 financial year for the same period the company had assets of R1, 023,357,000 in total. | Spur Corporation Limited brands include: John Dory’s RocoMamas Casa Bella Spur Steak Ranches Panarottis The Hussar Grill And more The company open its first international Namibia Spur franchise in 1991. After this the company opened more international locations in Botswana, Mauritius and Zambia in the year 1995. It was only in 1996 that the first franchise locations were opened in both Swaziland and Australia. In the year 1997 Zimbabwe got their own franchise location, but it was only in 2016 that Spur opened its first location in New Zealand. |

| Sun International Limited | Sun International brand is known for gaming, hospitality and entertainment and is seen as a premium brand. The company has world class five star hotels, modern casinos and some of the world’s prime resorts. | Head Office Tel: +27 11 780 7000 Email: crobook@suninternational.com Webpage: https://www.suninternational.com/ (accessed on: 22 May 2021). Address: 6 Sandown Valley Crescent, Sandton Gauteng, South Africa | PricewaterhouseCoopers Incorporated 4 Lisbon Lane Waterfall City Jukskei View 2090 South Africa | As at 30 June 2020 Sun International had a total of R22,991,000 assets. At 30 June 2019 the company had a total of R24,635,000 assets. | Sun International has a verity of graduate programs, internships and bursaries available to passionate people trying to make it in the gaming, hospitality and entertainment industry. |

| Tsogo Sun Hotels Limited | Tsogo Sun Hotels is a prominent company in the southern African hospitality industry. The company has a standing heritage of 50 years for markets in South Africa, Africa, Seychelles and the Middle East. The company has over one hundred hotels across these different countries. | Palazzo Towers East, Montecasino Boulevard, Fourways, 2055 Private Bag X200, Bryanston, 2021 South Africa Tel: +27 11 461 9744 Webpage: https://www.tsogosun.com/ (accessed on: 22 May 2021). | PricewaterhouseCoopers Incorporated 4 Lisbon Lane, Jukskei View, 2090 Private Bag X36, Sunninghill, 2157 | For the year ending 31 March 2020 the company assets amounted to a total of R15,382,000. For the year ending 31 March 2019 the company assets amounted to a total of R14,586,000. | This company has a Citizenship program called Caring Across Communities. Through this program Tsogo Sun Hotels helps uplift and develop South African communities in need. The main focus of this program are on three areas, specifically community development, the natural environment and entrepreneurial developments. |

| Tsogo Sun Gaming Limited | The company has 13 Tsogo Sun Gaming casinos and 23 Galaxy Bingo sites in South Africa. Moreover, Tsogo Sun Gaming offer more than just authentic casino life and action. The company strives to have activities for the whole family. The company offers live shows, fun-filled events, local and international theatre productions, movies, wonderful dining and ten-pin bowling. The company has theme parks as well as bird parks that the whole family can enjoy. | Palazzo Towers East, Montecasino Boulevard, Fourways, 2055 Private Bag X200, Bryanston, 2021 South Africa Tel: +27 11 510 7700 Webpage: https://www.tsogosungaming.com/ (accessed on: 22 May 2021). | PricewaterhouseCoopers Incorporated 4 Lisbon Lane, Jukskei View, 2090 Private Bag X36, Sunninghill, 2157 | The company had a total of R19,003,000 in assets as at 31 March 2020. In the 2019 financial year the company had a total of R35,077,000 assets. | Names included in the group are as follows: Montecasion; Suncoast; Gold Reef City; Silverstar; Golden Horse; The Ridge; Emnotweni; Blackrock; Goldfields; Mykonos; The Caledon; Garden Route; Hemingways. For the 2020 financial year Tsogo Sun Gaming had an Income of R11.7 billion, which is a 1% increase from the previous year. The company however showed an adjusted earnings amount of R1.4 billion and an adjusted HEPS of 134.5 cents, both 14% lower than in the 2019 financial year. |

Appendix B

| Arden Capital Limited | City Lodge Hotel Group Limited | Comair Limited | Famous Brands Limited | Hosken Passenger Logistics and Rail Limited | LUXE Holdings Limited | Spur Corporation Limited | Sun International Limited | Tsogo Sun Hotels Limited | Tsogo Sun Gaming Limited | |

|---|---|---|---|---|---|---|---|---|---|---|

| Going concern (category 1) | ||||||||||

| Is there a reasonable amount of information disclosed regarding the going concern of the company? | Yes | Yes | No | Yes | Yes | Yes | No | Yes | Yes | Yes |

| Did the company provide information about the assessment of going concern? | Yes | Yes | No | Yes | Yes | Yes | No | Yes | Yes | Yes |

| Are the effects of COVID-19 regarding the company’s ability to be a going concern discussed? | Yes | Yes | No | Yes | Yes | Yes | No | No | Yes | Yes |

| Are the financial reports prepared by means of the going concern assumption, in spite of the coronavirus? | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Does the company provide information concerning any material uncertainties that may affect the company’s ability to operate as a going concern, in light of COVID-19? | No | No | No | Yes | Yes | Yes | No | No | Yes | Yes |

| Events after the reporting period (category 2) | ||||||||||

| Is any discloser presented regarding subsequent events? | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Did the company distinguish between adjusting and non-adjusting events? | No | No | No | Yes | No | No | No | No | Yes | Yes |

| Does the company address COVID-19 with reference to IAS 10? | Yes | Yes | No | Yes | Yes | Yes | No | Yes | Yes | Yes |

| Did the company consider COVID-19 to be an adjusting event after the reporting period? | No | No | No | No | No | No | No | No | No | Yes |

| Were there any events that took place after the reporting date, for the company? | Yes | Yes | No | Yes | No | Yes | Yes | Yes | Yes | Yes |

| Fair value measurement and impairment (category 3) | ||||||||||

| Did the company give the users information about the Fair Value measurement? | Yes | Yes | No | Yes | No | No | Yes | No | Yes | Yes |

| Is there disclosure on the Fair Value valuation techniques used by the company? | Yes | Yes | No | Yes | No | No | Yes | No | Yes | Yes |

| Did the company disclose the impact of COVID-19 on the Fair Value Measurement? | No | No | No | No | No | No | No | No | Yes | Yes |

| Did the company give the users information about the impairment of elements in the financial statements? | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes | Yes |

| Is any information given to show the impact COVID-19 had on the company’s impairment of assets? | Yes | Yes | No | Yes | No | No | No | Yes | Yes | Yes |

| When making projections for impairments, did the company account for the effects of COVID-19? | Yes | Yes | No | Yes | No | No | No | Yes | Yes | Yes |

| Revenue recognition (category 4) | ||||||||||

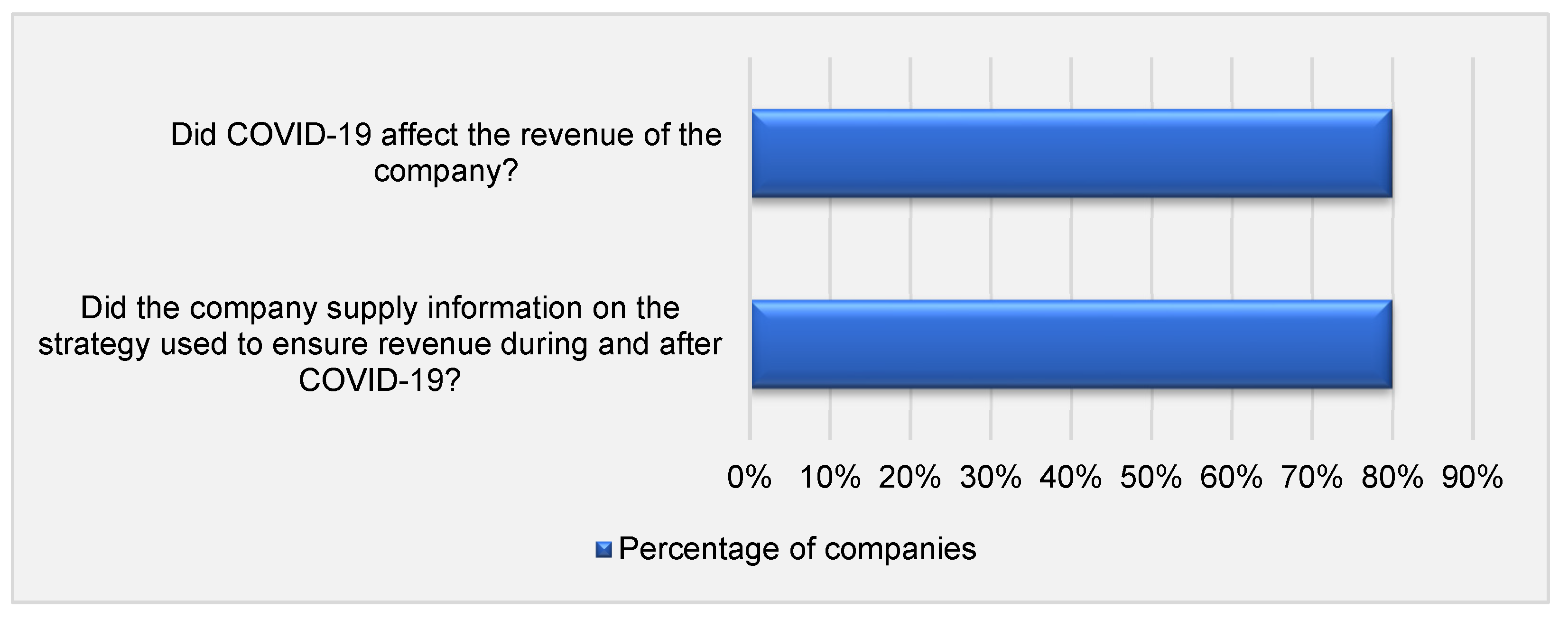

| Did the company supply information on the strategy used to ensure revenue during and after COVID-19? | Yes | Yes | No | Yes | Yes | Yes | No | Yes | Yes | Yes |

| Did COVID-19 affect the revenue of the company? | Yes | Yes | No | Yes | Yes | Yes | No | Yes | Yes | Yes |

| Other financial statement disclosure (category 5) | ||||||||||

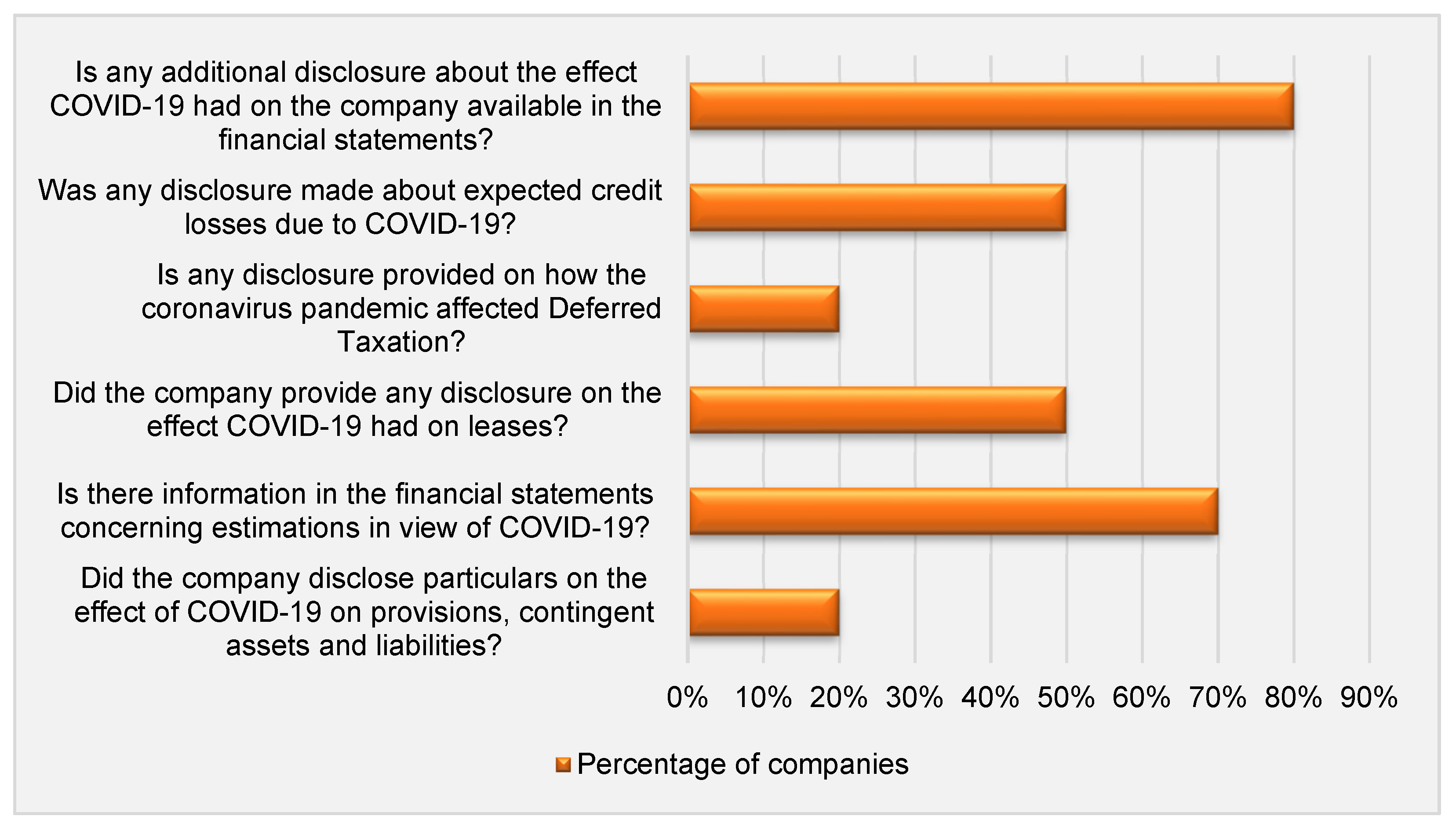

| Is any additional disclosure about the effect COVID-19 had on the company available in the financial statements? | Yes | Yes | No | Yes | Yes | Yes | No | Yes | Yes | Yes |

| Did the company provide any disclosure on the effect COVID-19 had on leases? | Yes | Yes | No | Yes | No | Yes | No | No | Yes | No |

| Is any disclosure provided on how the coronavirus pandemic affected Deferred Taxation? | No | Yes | No | Yes | No | No | No | No | No | No |

| Was any disclosure made about Expected Credit Losses (ECL) as a result of the coronavirus? | Yes | Yes | No | Yes | No | Yes | No | No | Yes | No |

| Is there information in the financial statements concerning estimations in view of COVID-19? | No | Yes | No | Yes | Yes | Yes | No | Yes | Yes | Yes |

| Did the company disclose particulars on the effect of COVID-19 on provisions, contingent assets and liabilities? | No | No | No | Yes | No | No | No | No | Yes | No |

| Cash-flow | + | − | + | + | + | + | + | + | + | + |

References

- World Health Organization (WHO). Novel Coronavirus (2019-nCoV) Situation Report—1. 2020. Available online: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200121-sitrep-1-2019-ncov.pdf?sfvrsn=20a99c10_4 (accessed on 15 July 2020).

- World Health Organization (WHO). Coronavirus Disease 2019 (COVID-19) Situation Report—51. 2020. Available online: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200311-sitrep-51-covid-19.pdf?sfvrsn=1ba62e57_10 (accessed on 15 July 2020).

- World Health Organization (WHO). Coronavirus Disease 2019 (COVID-19) Situation Report—60. 2020. Available online: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200320-sitrep-60-covid-19.pdf?sfvrsn=d2bb4f1f_2 (accessed on 15 July 2020).

- Lopatta, K.; Alexander, E.K.; Gastone, L.M.; Tammen, T. To Report or Not to Report about Coronavirus? The Role of Periodic Reporting in Explaining Capital Market Reactions during the Global. 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3567778 (accessed on 15 July 2020).

- Altig, D.; Baker, S.; Barrero, J.M.; Bloom, N.; Bunn, P.; Chen, S.; Mihaylov, E. Economic uncertainty before and during the COVID-19 pandemic. J. Public Econ. 2020, 191, 104274. [Google Scholar] [CrossRef]

- Barnoussi, A.E.; Howieson, B.; van Beest, F. Prudential application of IFRS 9: (Un)Fair reporting in Covid-19 crisis for banks worldwide?! Aust. Account. Rev. 2020, 30, 178–192. [Google Scholar] [CrossRef]

- Kanu, I.A. COVID-19 and the economy: An African perspective. J. Afr. Stud. Sustain. Dev. 2020, 3, 29–36. [Google Scholar]

- Alao, B.B.; Gbolagade, O.L. Coronavirus pandemic and business disruption: The consideration of accounting roles in business revival. Int. J. Acad. Multidiscip. Res. 2020, 4, 108–115. [Google Scholar]

- Taylor, M. Economic Impact of Covid-19 and the Policy Response by ACCA’s Chief Economist Michael Taylor. 2020. Available online: https://www.accaglobal.com/gb/en/news/2020/march/ACCA-Covid-19_Economy.html (accessed on 16 July 2020).

- Kapiki, S. The impact of economic crisis on tourism and hospitality: Results from a study in Greece. Cent. Eur. Rev. Econ. Financ. 2012, 2, 19–30. [Google Scholar]

- Gössling, S.; Scott, D.; Hall, C.M. Pandemics, tourism and global change: A rapid assessment of COVID-19. J. Sustain. Tour. 2020, 29, 1–20. [Google Scholar] [CrossRef]

- Albitar, K.; Gerged, A.M.; Kikhia, H.; Hussainey, K. Auditing in times of social distancing: The effect of COVID-19 on auditing quality. Int. J. Account. Inf. Manag. 2020, 29, 169–178. [Google Scholar] [CrossRef]

- Carmeli, A.; Schaubroeck, J. Organisational crisis-preparedness: The importance of learning from failures. Long Range Plan. 2008, 41, 177–196. [Google Scholar] [CrossRef]

- Fagerström, A.; Hartwig, F.; Cunningham, G. Accounting and auditing of sustainability: Sustainable Indicator Accounting (SIA). Sustainability 2017, 10, 45–52. [Google Scholar] [CrossRef]

- Geerts, M.; Dooms, M.; Stas, L. Determinants of sustainability reporting in the present institutional context: The case of port managing bodies. Sustainability 2021, 13, 3148. [Google Scholar] [CrossRef]

- Jung, S.; Nam, C.; Yang, D.; Kim, S. Does corporate sustainability performance increase corporate financial performance? Focusing on the information and communication technology industry in Korea. Sustain. Dev. 2017, 26, 243–254. [Google Scholar] [CrossRef]

- Kaczmarek, J. The mechanisms of creating value vs. financial security of going concern-sustainable management. Sustainability 2019, 11, 2278. [Google Scholar] [CrossRef] [Green Version]

- Aras, G.; Crowther, D. Evaluating sustainability: A need for standards. Issues Soc. Environ. Account. 2008, 2, 19–35. [Google Scholar] [CrossRef]

- Mishra, A.K. Organizational responses to crisis: The centrality of trust. In Trust in Organizations: Frontiers of Theory and Research; Kramer, R., Tyler, T., Eds.; Sage: Thousand Oaks, CA, USA, 1996; pp. 261–287. [Google Scholar]

- Marcus, A.A.; Goodman, R.S. Victims and shareholders: The dilemmas of presenting corporate policy during a crisis. Acad. Manag. J. 1991, 34, 281–305. [Google Scholar]

- McKinsey & Company. Leading in a Crisis: Five Practices That Help Most [Podcast]. 2020. Available online: https://www.mckinsey.com/about-us/covid-response-center/leadership-mindsets/podcasts/leading-in-a-crisis-five-practices-that-help-most (accessed on 4 October 2020).

- Baskan, T.D. Analyzing the going concern uncertainty during the period of covid-19 pandemic in terms of independent auditor’s reports. ISPEC Int. J. Soc. Sci. Humanit. 2020, 4, 28–42. [Google Scholar]

- Centers for Disease Control and Prevention (CDC). Severe Acute Respiratory Syndrome (SARS). 2017. Available online: https://www.cdc.gov/sars/ (accessed on 19 July 2020).

- Centers for Disease Control and Prevention (CDC). Influenza (Flu). 2010. Available online: https://www.cdc.gov/flu/pastseasons/0910season.htm (accessed on 19 July 2020).

- Adegun, O. The effects of Ebola virus on the economy of West Africa through the trade channel. IOSR J. Humanit. Soc. Sci. 2014, 19, 48–56. [Google Scholar] [CrossRef]

- Fan, E.X. SARS: Economic Impacts and Implications. 2003. Available online: https://www.adb.org/publications/sars-economic-impacts-and-implications (accessed on 16 July 2020).

- Verikios, G.; Sullivan, M.; Stojanovski, P.; Giesecke, J.A.; Woo, G. The Global Economic Effects of Pandemic Influenza: Centre of Policy Studies (CoPS). 2011. Available online: http://vuir.vu.edu.au/29271/1/g-224.pdf (accessed on 16 July 2020).

- Maphanga, P.M.; Henama, U.S. The tourism impact of ebola in Africa: Lessons on crisis management. Afr. J. Hosp. Tour. Leis. 2019, 8, e59. Available online: https://www.ajhtl.com/uploads/7/1/6/3/7163688/article_59_vol_8_3__2019.pdf (accessed on 16 July 2020).

- PricewaterhouseCoopers (PWC). Accounting Implications of the Effects of Coronavirus: PwC in Depth. 2020. Available online: https://inform.pwc.com/inform2/show?action=informContent&id=2051233603128854 (accessed on 15 November 2020).

- Arnold, C.; Gould, S. The Financial Reporting Implications of COVID-19. 2020. Available online: https://www.ifac.org/knowledge-gateway/supporting-international-standards/discussion/financial-reporting-implications-covid-19 (accessed on 14 August 2020).

- Kothari, S.; Lester, R. The role of accounting in the financial crisis: Lessons for the future. Account. Horiz. 2012, 26, 335–351. [Google Scholar] [CrossRef] [Green Version]

- Islam, A.I. Impact of Covid-19 pandemic on global output, employment and prices: An assessment. Trans. Corp. Rev. 2021, 13, 189–201. [Google Scholar]

- Sidley. SEC Issues New Disclosure Guidance and Extends Conditional Filing Relief Amid COVID-19 Pandemic. 2020. Available online: https://www.sidley.com/en/insights/newsupdates/2020/03/sec-issues-new-disclosure-guidance-and-extends-conditional-filing-relief-amid-covi19-pandemic (accessed on 19 July 2020).

- Arnold, C.; Gould, S. Summary of Covid-19 Financial Reporting Considerations. 2020. Available online: https://www.ifac.org/knowledge-gateway/supporting-international-standards/discussion/summary-covid-19-financial-reporting-considerations (accessed on 14 November 2020).

- Ernst & Young. COVID-19 Enterprise Resilience Checklist. 2020. Available online: https://www.ey.com/en_za/covid-19/financial-investor (accessed on 1 November 2020).

- Deller, D. How Covid-19 Will Affect Adjusting Events, Impairments and Financial Instruments. 2020. Available online: https://www.accaglobal.com/africa/en/member/discover/cpd-articles/corporate-reporting/adjusting-events.html (accessed on 31 October 2020).

- Ernst & Young. Applying IFRS-Accounting Considerations of the Coronavirus Outbreak. 2020. Available online: https://www.ey.com/en_gl/ifrs-technical-resources/applying-ifrs-accounting-considerations-of-the-coronavirus-outbreak (accessed on 14 November 2020).

- Association of Chartered Certified Accountants (ACCA). IFRS 16 Changes for Covid-19 Rent Holidays and Reductions. 2020. Available online: https://www.accaglobal.com/africa/en/cam/coronavirus/IFRS16-covid190.html (accessed on 31 October 2020).

- Rajah, F.; Human, M.; Groenewald, J.; Schleritzko, A.; Gouws, J.; Munakamwe, M. Impairment Testing During the Global Pandemic. 2020. Available online: https://www.pwc.co.za/en/assets/pdf/impairment-testing-during-global-pandemic-covid-19.pdf (accessed on 1 November 2020).

- Tokar, M.; Kumar, S. Applying IFRS Standards in 2020-Impact of Covid-19. 2020. Available online: https://cdn.ifrs.org/-/media/feature/news/2020/inbrief-covid19-oct2020.pdf?la=en (accessed on 30 October 2020).

- Johannesburg Stock Exchange (JSE). COVID-19: Extension of Financial Reporting. 2020. Available online: https://www.jse.co.za/content/JSEAnnouncementItems/JSE%20Letter%20FSCA%20Notification%2029%20May%202020.pdf (accessed on 15 July 2020).

- Umeano, O. After the Covid-19 War Has Been Won, Africa Needs to Rethink Its Road to Economic Development. 2020. Available online: https://www.accaglobal.com/africa/en/member/member/accounting-business/2020/05/in-focus/economic-development.html (accessed on 1 November 2020).

- Milne, M.J.; Adler, R.W. Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar] [CrossRef] [Green Version]

- Bowen, G.A. Document analysis as a qualitative research method. Qual. Res. J. 2009, 9, 27. [Google Scholar] [CrossRef] [Green Version]

- Marshall, C.; Rossman, G.B. Designing Qualitative Research, 4th ed.; Sage Publications: Thousand Oaks, CA, USA, 2006; Available online: https://search-ebscohost-com.nwulib.nwu.ac.za/login.aspx?direct=true&db=cat01185a&AN=nwu.b1439139&site=eds-live (accessed on 16 January 2021).

- Yoshino, N.; Taghizadeh-Hesary, F. Unlocking SME Finance in Asia: Role of Credit Rating and Credit Guarantee Schemes, 1st ed.; Routledge: New York, NY, USA, 2020. [Google Scholar]

- Abeysekera, I.; Guthrie, J. An empirical investigation of annual reporting trends of intellectual capital in Sri Lanka. Crit. Perspect. Account. 2005, 16, 151–163. [Google Scholar] [CrossRef] [Green Version]

- Vourvachis, P.; Woodward, T. Content analysis in social and environmental reporting research: Trends and challenges. J. Appl. Acc. Res. 2015, 16, 166–195. [Google Scholar] [CrossRef] [Green Version]

- Basit, T. Manual or electronic? The role of coding in qualitative data analysis. Educ. Res. 2003, 45, 143–154. [Google Scholar] [CrossRef]

- IRESS. JSE Listed Companies: Travel and Leisure Sector. 2020. Available online: https://expert.inetbfa.com/ (accessed on 12 February 2020).

- Kegalj, G. How Should Companies Assess COVID-19 Events after the Reporting Date. 2020. Available online: https://assets.kpmg/content/dam/kpmg/xx/pdf/2020/04/covid19-reporting-date.pdf (accessed on 15 November 2020).

- Binder Dijker Otte (BDO). Potential Effects of the Coronavirus Outbreak on 31 December 2019 Yearend Financial Reporting. 2020. Available online: https://global-www.bdo.global/getmedia/3dea529b-2521-43d2-b73f-ee8f3418eea4/IFRB-2020-02-Potential-effects-of-the-Coronavirus-Outbreak-31-12-2019-year-ends.aspx (accessed on 16 November 2020).

- O’Donovan, B. Are Customer Contracts still Enforceable? 2020. Available online: https://assets.kpmg/content/dam/kpmg/xx/pdf/2020/03/isg-covid-19-customer-contracts-enforceable.pdf (accessed on 15 November 2020).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

da Silva, D.; Schutte, D.; Surujlal, J. Unpacking the IFRS Implications of COVID-19 for Travel and Leisure Companies Listed on the JSE. Sustainability 2021, 13, 7942. https://doi.org/10.3390/su13147942

da Silva D, Schutte D, Surujlal J. Unpacking the IFRS Implications of COVID-19 for Travel and Leisure Companies Listed on the JSE. Sustainability. 2021; 13(14):7942. https://doi.org/10.3390/su13147942

Chicago/Turabian Styleda Silva, Diana, Danie Schutte, and Jhalukpreya Surujlal. 2021. "Unpacking the IFRS Implications of COVID-19 for Travel and Leisure Companies Listed on the JSE" Sustainability 13, no. 14: 7942. https://doi.org/10.3390/su13147942

APA Styleda Silva, D., Schutte, D., & Surujlal, J. (2021). Unpacking the IFRS Implications of COVID-19 for Travel and Leisure Companies Listed on the JSE. Sustainability, 13(14), 7942. https://doi.org/10.3390/su13147942