1. Introduction

Dynamic changes in economies caused by globalization have influenced the development of new approaches to the management and functioning of enterprises (e.g., process approach, reorganization of processes, outsourcing, new business models, supply chains) [

1]. The market, i.e., the environment, has become the point of reference for businesses. This means that companies focus on customer needs and integrate social and environmental issues into their operational and strategic functioning [

2,

3,

4,

5]. As companies have moved beyond their organizational framework, many business functions (business processes) have been outsourced. Thus, service activities have emerged, leading to the emergence of supply chains and value chains [

1,

3,

6,

7,

8].

Value is the key to the success of modern enterprises and supply chains, which ensures their long-term existence in the market, including a solid competitive position. The value can be obtained through effective management, which at present must consider balancing the economic, social, and environmental spheres, i.e., sustainable development [

2,

3]. Creating value and ensuring sustainability by companies in supply chains is a particular challenge during a pandemic such as COVID-19. Enterprises and their supply chains that want to survive on the market adopt sustainability as a central business requirement, reflected in their activity strategy [

2,

3,

9]. The value creation takes place in various spheres, including supply chain phases (e.g., research and development, purchasing, production, distribution (i.e., logistics, sales, and customer service), or marketing and human resources (HR)) and stages of business or product/service functioning (e.g., product launch, maturity, decline, as product withdrawal from the market). It is ultimately intended to deliver value to various stakeholders (customers, suppliers, and society), not just shareholders [

10]. Therefore, value management is closely related to sustainable management, which affects the sustainable development of a company and its supply chains [

3,

6,

11,

12].

Sustainable management includes two perspectives. The first one assumes that managing the standpoint of customers and other stakeholders is essential for the development of the sustainable supply chain. The second identifies potential links between sustainable practices and the various dimensions of development–economic, environmental, and social [

3,

13]. These areas should be adequately measured and communicated within and between organizations to manage and influence sustainability [

2,

5,

12,

14] effectively. The chosen research indicates that companies adopting sustainable practices have better financial performance than those that have not [

12,

13,

15]. However, to make a proper measurement in the organization, i.e., oriented towards value creation in connection with sustainability and communicating information in this respect (e.g., reporting), appropriate resources are needed. Within the framework of resources, particular importance should be attributed to human resources (employees) despite the progressing robotization and automation in the world [

13,

14,

16]. The role of employees in business has also changed, as they are increasingly business partners who participate in management and decision-making processes [

17,

18].

Proper management of human resources and their competences contribute to gaining a competitive advantage in the long term. This is confirmed by resource-based theory (RBV) [

19]. Shang et al. [

7] and Shi et al. [

20] stress the need to use RBV to understand the relationship between sustainability and organizational performance. Considering performance measurement and management issues in organizations and outside them, it seems appropriate to emphasize accountants’ role, especially from this perspective. Gray [

21] indicated that accountants have a major role in environmental issues, both through their traditional roles of recording and reporting financial details and their roles as business managers. It means that the changing management approach is transforming the roles of accountants and their perception in business. Since 1990, more and more studies have been encountered in the publications dedicated to verifying the essence of accountants on value measurement and sustainability [

8,

22,

23,

24]. Among the professions of accountants, controllers/management accountants play a special role [

13,

14,

17,

24,

25,

26,

27].

Sustainable development, and therefore sustainable management, especially in the COVID-19 pandemic, need high-quality information that is properly communicated. This issue is solved by reporting, thus accounting system [

14,

24,

28,

29,

30]. Because sustainability is focused on creating value in different business areas and for different recipients, controllers/management accountants can play a special role in this regard. Thus far, the role of management accountants has been smaller than that of financial accountants, particularly in Anglo-Saxon countries. However, the orientation of accounting towards an international perspective (International Financial Reporting Standards—IFRS), and therefore towards supply chain and value chain creation, has increased the role of controllers/management accountants in business practice [

8,

28,

31,

32,

33]. The controller is perceived as a specialist oriented towards supporting strategic management, thus characterized by ‘far-sighted’ business thinking and actively cooperating with managers in various business fields [

14,

34]. The special development of controllers against the background of globalization is visible in German-speaking countries. On the practical side, controlling is identified with management accounting, and controllers correspond to management accountants [

17,

30,

35,

36,

37,

38,

39].

Controlling as a separate department and as an internal information system only for management existed alongside financial accounting system focusing on creditor protection and based on the commercial law. This solution is called the dual ledger accounting approach [

31,

36,

38], and this dimension of accounting, supported by such organizations as ‘Internationaler Controller Verein’ (ICV) (German)/International Group of Controlling (IGC), is also distributed in German-language publications [

26,

27,

40]. However, the emphasis put on the internationalization of business and thus on science has led to specific changes in control and profession in the German-speaking countries [

41,

42].

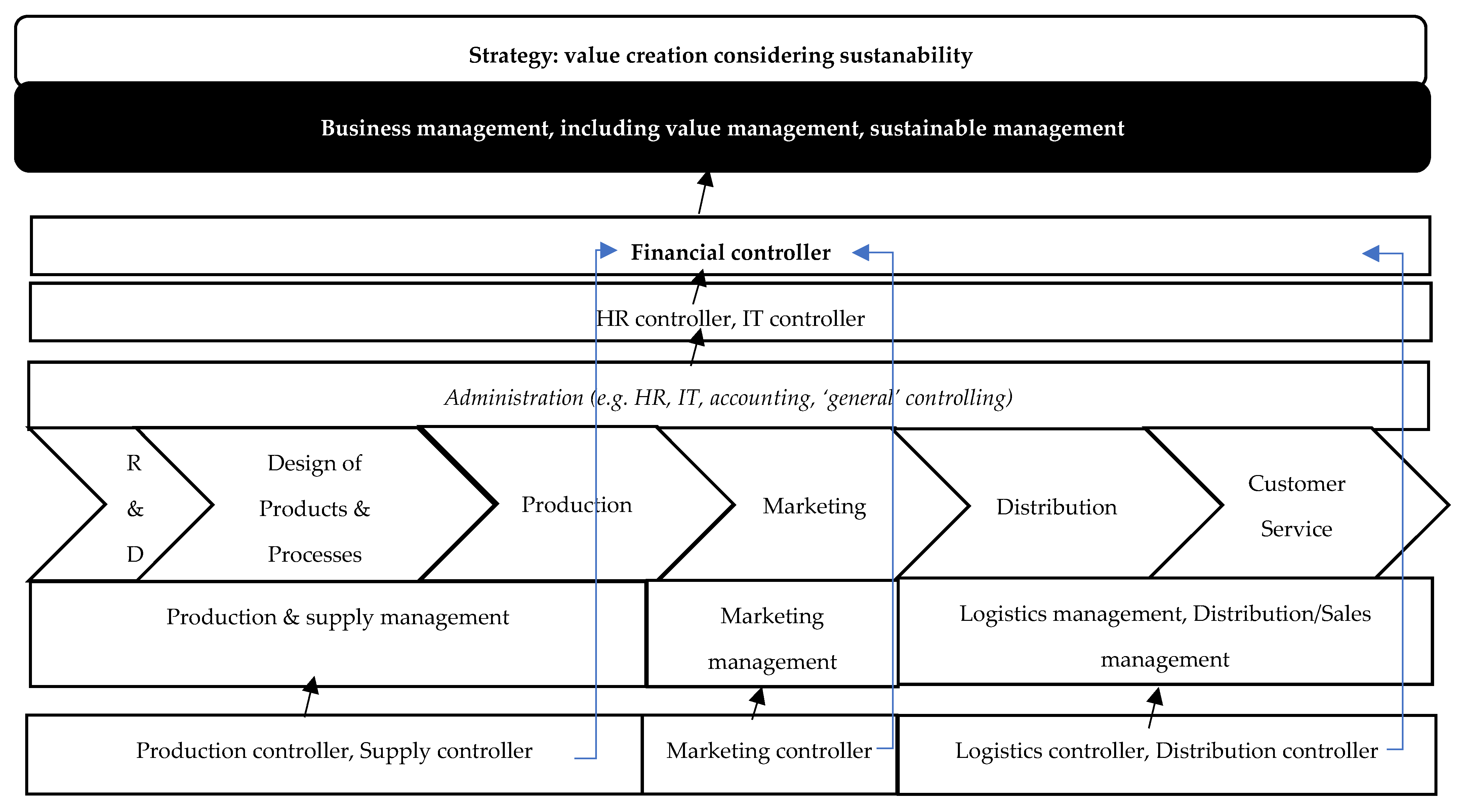

The complexity of enterprises, including the growing role of functions/processes around production (e.g., logistics, distribution, marketing, and sales) as links in the supply/value chain in increasing profitability and implementation of the concept of sustainable development, as well as the intensification of promotional activities of ICV/IGC, have contributed to another direction of changes in controlling and its profession, i.e., its diversification [

26,

27]. Hence, so-called functional controlling emerged, directed at business functions/processes such as supply, logistics, production, distribution, HR, IT, marketing, and finance [

43]. As a result, in German-speaking countries, on the labor market, there is a demand for a specialized controller in a given business function/process that creates the supply chain and thus value chain.

Considering the dual development of control, i.e., controllers in German-speaking countries, i.e., (1) the integration of financial accounting and controlling and (2) the decentralization of control, it is worth taking a closer look at this issue in terms of shaping new profiles of controllers-functional controllers in terms of competences and tasks for essential business functions/processes that affect the creation of the supply chain as the value chain and that participate in the implementation of the concept of sustainability.

The paper contributes in different ways to science and practice. Firstly, previous publications on the studied issues have mainly focused on showing the general importance and development of controllers from the conceptual point of view (professionals supporting the management process in organizations, which are especially links in the supply chain), or their location in specific economies (management accounting as controlling in Germany) and business models (controlling for the holistic supply chain management) [

5,

18,

31,

35,

39,

44,

45,

46,

47]. However, there is no publication on an international scale that presents a new perspective of the controller, i.e., functional controllers, regarding their competences and tasks.

Secondly, few articles link management accountants to IFRS in Anglo-Saxon countries, although such a discourse is popular in German-speaking countries [

27,

28,

31,

32,

48]. As a result, there is a lack of publications on shaping the specific dimension of the controller (functional controller) in German-speaking countries from the point of view of tasks and competences, at the same time considering the system changes in accounting and business (e.g., focusing on value creation, and hence building the supply chain as value chain, strategic management, and therefore on sustainability and sustainable management) [

24].

Third, many studies indicate that controllers should be more involved in creating sustainable development, i.e., actively participate in decision-making and strategy-making in this direction (concept of business partners) [

13,

17,

26,

27,

49]. This is due to various factors, including jurisdictional requirements that include demands for sustainability for organizations and their cooperation in the supply chains. On the other hand, it results from calls from global institutions or countries that organizations should be more aware of sustainability. The third rationale is social changes affecting positive public perception of sustainability [

2,

44]. It shows that global changes in the economic–political–social sphere affect companies (new approaches to management, i.e., value management, sustainable management) and thus impact organizational and inter-organizational structures and information systems, including controlling (e.g., the emergence of functional controlling). As a result, a need arises to employ new specialists with adequate competences to perform tasks supporting value creation and sustainability, who would be proactive in this process, not only within the organization but also outside of it. Such specialists may be functional controllers [

13,

14,

43,

49].

The article aims to present a profile of functional controllers created in German-speaking countries in the context of their competences and tasks for sustainable management and value chain creation. For the research, the following controllers were distinguished: supply controller, production controller, logistics controller, marketing controller, HR controller, financial controller, IT controller, and distribution controller. The choice of the above controllers is dictated by the growing importance of these functions/processes in modern business and the creation of the supply chain as a value chain, and their frequent presentation in publications in German-speaking countries [

34,

41]. Furthermore, these functions/processes have to participate in implementing the concept of sustainability, and therefore sustainable management, so there is a need for their measurement and the information derived from it. Thus, these tasks can be fulfilled by controllers specialized in these particular functions.

The identity of functional controllers is analyzed by the types of competences presented in the professional model of Cheetham and Chivers [

50] and task areas reflecting controlling functions in business practice [

26,

27]. Job advertisements [

51] from the German market (Web portals with job advertisements) posted at the end of April and June 2020 are the basis for identifying the competences and tasks of selected controllers. The job ads refer to the COVID-19 pandemic period.

Data were analyzed using descriptive statistics and advanced statistical approaches, i.e., the Student’s t-test with Cochran–Cox correction and the Wilcoxon–Mann–Whitney test. These collected data are intended to address the seven research questions (RQ). The answers to the last two RQs result from analysis and reflection based on publication and empirical research.

The article consists of three parts. The theoretical part refers to changes in accounting in the macro and micro perspectives, perception of controlling in the context of the Anglo-Saxon approach, understanding of occupational identification including the essence of competences, and characteristics of the controller’s profile. The following parts of the article present the research methodology and results. Finally, the article ends with a discussion and conclusions.

3. Materials and Methods

The study analyzed job advertisements for the position of a controller [

51]. These adverts focused on the following business functions/processes: production, finance, logistics, marketing, HR, IT, supply, and distribution. These functions/processes are essential for modern business, as their proper management improves performance, including profitability in the company and supply chain. They have separate departments or activity centers in business practice and are often subject to outsourcing [

43,

48]. Moreover, they are part of the value chain [

3]. The indicated functions/processes can be supported by functional controllers that influence cost reduction, life cycle minimization, and value maximization as perceived by the end customer. They break down barriers between departments, business units, and areas and promote better performance [

42].

The job advertisements under analysis come from Germany. This country has specific cultural conditions, which strongly influence the development of controlling and characterizes institutional support by the ICV/IGC. Furthermore, the activity of these organizations outlines and strengthens the identity of controllers, i.e., their specialization [

26,

27].

The job advertisements were downloaded at the end of April and beginning of June 2020, from the most significant and most popular job search websites in Germany: indeed.de, monster.de, stepstone.de, xing.com, and kimeta.de. The data collection period comprises the COVID-19 pandemic period, which has affected the labor market and the specific needs of employers.

To isolate target job advertisements related to the profiles of controllers, the following keywords in the German language were entered into the search engine of these websites: Produktionscontroller, Finanzcontroller, Marketing Controller, Logistikcontroller, IT Controller, HR or Personalcontroller, Beschaffungscontroller or Einkaufscontroller, and Vetriebscontroller.

First, the number of controller positions and the number of posts mentioned above were indicated. However, the number presented by the job websites was not synonymous with the actual job advertisements for the analyzed controllers. In most cases, there were other announcements related to a given function; e.g., in a distribution controller, there were job adverts for salesman, sales specialist, and sales manager.

A total number of 120 advertisements were isolated, 15 for each occupational profile. When finding a certain number of job advertisements in a particular search engine for a specific controller, another job search engine was added from the job as mentioned above search engines. The number of the sample is sufficient to analyze the professional identity of functional controllers because the ads are to some extent structured. Further searches for job advertisements looking for these occupations often showed repeated adverts.

Table 1 shows the number of job advertisements for studied functional controllers in each job search engine.

Researchers frequently apply a method of analyzing content based on job advertisements. There are many publications from various fields in which this technique was used to understand the overall conditions of the studied phenomenon and, on this basis, make assessments and carry out further in-depth research. It is worth noting that job advertisements reflect the needs of business, the labor market, and education [

51].

The analysis of collected research material focused on separating two data areas: (1) required competences and (2) tasks. The competences in the job advertisement were organized according to elements of occupational competence mix models of Cheetham and Chivers [

11]. At the same time, the required future tasks performed by controllers were ranked according to the range of tasks presented by ICV/IGC [

26,

27] and researchers [

68] and corresponding main ‘controlling’ functions in organizations. The following areas of controllers’ tasks were identified for analysis (1) forecasting, (2) controlling and monitoring, (3) planning and budgeting, (4) analyzing (performance measurement and deviation analysis), (5) reporting, (6) coordinating and optimizing, (7) participating in the management process and making decisions, and (8) defining new methods and tools. The first five relate primarily to supporting management’s operational and tactical perspective, while groups seven and eight respectively connect to the strategic perspective. The sixth group can be distinguished at any management level, i.e., operational, tactical, and strategic. However, this group has been assigned to the strategic context of management support for the study, as coordination or optimization requires a conceptual approach and time. In addition, in the context of competences, they have been further subdivided into soft and hard competencies considering the types of competencies from the model by Cheetham and Chivers [

50]. Thus, it was assumed that communication, self-development, creativity, and personal or behavioral and values/ethical competences illustrate soft competences. In contrast, analysis, problem-solving, knowledge/cognitive competence, and functional competences refer to hard competences [

44].

The article formulates the following research questions (RQs):

- RQ1.

Are there any significant differences in meta competences between functional controllers?

- RQ2.

Are there significant differences in core competencies between functional controllers?

- RQ3.

Are there any significant differences in the area of tasks between functional controllers?

- RQ4.

Are there significant differences in soft and hard competences between functional controllers?

- RQ5.

Are there significant differences in terms of operational and strategic tasks between functional controllers?

- RQ6.

Do the task areas indicate the role of business by the studied functional controllers?

- RQ7.

Can the tasks and competencies of functional controllers enhance the effectiveness of sustainable management?

The obtained data were analyzed using descriptive statistics and advanced statistical approaches, i.e., the Student’s t-test with Cochran-Cox correction and the Wilcoxon-Mann–Whitney test. These quantitative methods are intended to address the first five RQs. The answers to RQ6 and RQ7 result from the analysis and reflection based on literature and empirical research.

4. Results

The descriptive analysis of data for the Cheetham and Chivers model showed that for eight analyzed profiles of controllers, 853 indications in the job advertisements related to the core competences and 306 to meta competences. The meta competences were dominated by communication competences (118 indications) and analysis (104 indications). This is in line with the coordinating function of controlling. A controller has to communicate with data providers, modify it accordingly through various analyses, and ultimately provide information to relevant recipients. The least number of indications related to competences of problem-solving (12 indications). It may be because the problem-solving ability is assigned to communication and analytical thinking, or this competence is more emphasized in job advertisements for managerial positions than controllers. In terms of core competences, functional competences (353 indications) and knowledge/cognitive competences (296 indications) prevailed. Only one indication was assigned to the values/ethical competences. This seems logical because every controller should behave ethically and respect the values of organizations and other people. In functional competences, practically every employer required functional controllers to specialize in controlling within a given field of a study program.

On the other hand, in terms of IT controllers graduating from IT studies, mainly technical studies, was emphasized. All functional controllers were required to have 2–3 years of experience in controlling; additionally, expertise in a given function/process was an additional advantage. Each job advertisement requires knowledge of ERP systems, mainly SAP, and advanced Excel support. In the case of marketing controller and distribution controller, the need to know SQL was often indicated in job advertisements. Occasionally, or as an additional asset, the knowledge of VBA and Business Analyse and Intelligence Software was required in the analyzed occupational profiles. In terms of employee’s ability/cognitive competence, graduating from Business Administration studies was stressed in most controllers. In three to five job advertisements, graduating from Economics (e.g., supply controller, financial controller, HR controller, IT controller, distribution controller) and Engineering (in 12 job advertisements for logistics controller) was preferred. Moreover, in each job advertisement, English as a foreign language and general knowledge of Microsoft Office was required independently from the functional controller.

The combination of core and meta competences revealed a more significant advantage of hard competences (765 indications) than soft competences (394 inclusions) in the analyzed professional profiles. This correlation is correct, as functional controllers are foremost required to have special education and experience in controlling to effectively carry out controlling tasks, such as optimizing processes or implementing new tools in functional control.

In the context of tasks, in terms of all the studied controllers, the majority of required tasks were related to analysis (performance measurement and deviation analysis) (204 indications), coordination and optimization (199 indications), and reporting (109 indications). Forecasting (39 indications) was required the least in terms of tasks. Perhaps these tasks are already automated in companies, so the focus of controllers is shifted to more strategic activities. It is also reflected in the division into operational and strategic controlling tasks. Although operational tasks were more often indicated in the advertisements (495 indications-but there are more groups of tasks subordinated to this perspective in the study), there are also quite a few activities of strategic nature (368 indications). For example, among the second (strategic) area, 93 indications refer to tasks from the group referring to defining new methods and tools, and 73 indications refer to participation in the management process and decision making. It may mean that specialized departments of controlling or its information systems are created only in practice. Therefore, such expectations of employers exist on the market.

Frequent indication of strategic controlling tasks in the job advertisements shows a change in the perception of a controller in the organization. Functional controllers are not ‘counters’, but their function is closer to the so-called business partner (RQ6). The studied controllers actively participate in consulting, communication, management, and decision-making. The expressions used in the job advertisements confirm that, for example, ‘Advising specialist departments on purchasing and assortment related issues’ (supply controller), ‘Sparring partner for the Logistics Director and the Head of Purchasing in all commercial issues’ (supply controller), ‘Strategic and operational inventory management’ (supply controller), ‘Advising managers and colleagues on operational and strategic decisions’ (financial controller), ‘Internal commercial consultant and recognized business partner of the production managers’ (production controller), ‘Consulting for decision-makers and managers on business management issues (logistics controller), ‘active support and advice for professional and managerial staff, e.g., through (staff requirement) planning and scenario calculations’ (HR controller), ‘You participate in the decision making regarding budget planning with rational, data-based advice’ (marketing controller), and ‘Active support of the management/sales management in the use of sales control systems, sales analyses and measures to achieve sales targets in media sales’ (distribution controller). However, based on job advertisements, it is not easy to verify the active involvement of controllers in the management process. Still, their strategic position in the company is also confirmed by the tasks related to the creation of new processes or controlling tools, or the extension of existing tool solutions in specific functions/business processes. Examples of such formulations in job advertisements include: ‘Definition of controlling standards and processes’ (supply controller), ‘Further development of control-relevant information and KPI’s in production and logistics’ (production controller), ‘Support in establishment/further development of controlling instruments and harmonization of commercial processes to optimize performance management (production controller), ‘Development of “Digital Controlling” with a new reporting system’ (financial controller), ‘Establishment and further development of personnel controlling in the HR area’ (HR controller), ‘Development of a project-specific storage system according to the project procedure model’ (IT controller), ‘Establishment and further development of IT controlling processes’ (IT controller), ‘Definition of the relevant key sales figures’ (distribution controller), and ‘Definition and implementation of measures for the optimization of control and planning processes’ (distribution controller).

A unique role among functional controllers can be assigned to the financial controller. Before the appearance of other functional controllers, the position of a financial controller had been present in German practice for years, often equivalent to the role of a controller [

23]. The review of tasks in terms of this occupational profile showed that they are not only in the scope of supporting internal control in the company and management process but also relate to financial reporting. Examples of tasks required from the financial controller identified in the job advertisements include: ‘Preparation of internal and external reports’, ‘Preparation of variance analyses and comments’, ‘Cooperation in the implementation of the operating income statement is required’, ‘Being the contact for auditors’, ‘Responsibility for corporate planning, including preparation of the financial model’, ‘Preparation of relevant documents and financial figures for investors’, ‘Reporting of overhead costs and financial ratios’, ‘Analysis, evaluation and preparation of financial data’, ‘Participation in the preparation of monthly and annual financial statements according to German GAAP or IFRS’, ‘You will also evaluate financial effects of the MRSA mechanism and changes in the portfolio, carry out risk and structural analyses and prepare relevant key figures such as the coverage ratios’, ‘Preparation of monthly, quarterly and annual financial statements, including the calculation of provisions and accruals and the usual closing operations secure’, ‘Variance analyses and comment on monthly, quarterly and annual financial statements’, and ‘Liquidity planning’. The financial controller tasks in practice show that their scope exceeds operational business aspects, and there is a greater focus on financial accounting and corporate finance. This is partly related to the adaptation of IFRS to the accounting system in the organization. Still, it is also associated with the fact that this type of controller is responsible for measuring the whole business (thus value measuring) and the entire reporting, including financial but also non-financial reporting. This second type of reporting stems from the idea of sustainable development or Corporate Social Responsibility.

Based on the analysis of functional controllers’ tasks and competences, functional controllers can undoubtedly affect the efficiency of sustainable management and value creation in various spheres of business and the whole supply chain (RQ7).

Answers to RQs 1–5 related to the significance of differences between the studied job profiles of functional controllers in terms of competences and tasks can be obtained using an advanced statistical analysis (the Student’s t-test with Cochran–Cox correction Wilcoxon–Mann–Whitney test).

The conducted statistical analyses based on average tests in particular categories of competence/tasks and groups of competence/tasks categories allowed to identify statistically significantly different areas at the level of 0.05. Various statistical tests were considered depending on the way of decoding the occurrence of crucial features in the analyzed job advertisement ({0,1} vs. natural numbers = n).

On the basis of the Student’s t-test with Cochran-Cox correction, significant differences at the level of 0.05 were shown for meta competences respectively:

Communication: supply vs. logistics controller, marketing controller {0,1} (0.380, 0.380);

Creativity: supply vs. production controller (N) (0.036); production vs. marketing, IT, HR, distribution controller (N) (0.202, 0.036, 0.042, 0.020);

Analysis: supply vs. IT controller (N) (0.047), logistics vs. IT controller (N) (0.044).

In terms of core competences, significant differences at the same level were shown for:

Personal or behavioural competence: supply vs. marketing controller (N) (0.042), Production vs. distribution controller (N) (0.036), financial vs. distribution controller (N) (0.010), logistics vs. distribution controller (N) (0.038), marketing vs. distribution controller (N) (0.002).

In the context of tasks, significant differences were identified between the following profiles:

Controlling and monitoring: supply vs. production, logistics controller (N) (0.041, 0.029); production vs. financial, marketing controller (N) (0.022, 0.021); financial vs. logistics controller (N) (0.030); logistics vs. marketing, IT controller (N) (0.020, 0.044); logistics vs. marketing controller {0,1} (0.039);

Planning & budgeting: production vs. financial controller (N) (0.043), financial vs. logistics controller (N) (0.037);

Analyzing (performance measurement and deviation analysis): supply vs. financial controller (N) (0.029), production vs. financial, logistics, marketing controller (N) (0.003, 0.008, 0.007); financial vs. HR, distribution controller (N) (0.028, 0.002); logistics vs. distribution controller (N) (0.045); marketing vs. distribution controller (N) (0.004); HR vs. distribution controller (N) (0.045);

Reporting: supply vs. financial controller {0,1} (0.030) and (N) (0.004), production vs. financial controller {0,1} (0.030) and (N) (0.004), financial vs. logistics, marketing, HR, distribution controller (N) (0.004, 0.0002, 0.001, 0.0003), financial vs. logistics, marketing, distribution controller {0,1} (0.030, 0.043, 0.023);

Coordination and optimization: supply vs. marketing, IT controller {0,1} (0.043); supply vs. logistics, marketing, IT, distribution controller (N) (0.008, 0.0001, 0.001, 0.004); production vs. logistics, marketing, IT, distribution controller (N) (0.021, 0.0004, 0.005, 0.011); production vs. marketing, IT controller {0,1} (0.043, 0.043); financial vs. logistics, marketing, IT, distribution controller (N) (0.008, 0.0002, 0.002, 0.004); financial vs. marketing, IT, distribution controller {0,1} (0.023, 0.023, 0.049); logistics vs. marketing, HR controller (N) (0.048, 0.041); HR vs. IT, distribution controller (N) (0.001, 0.023);

Defining new methods and tools: supply vs. financial controller (N) (0.038);

Participation in the management process and decision making: production vs. financial, logistics controller (N) (0.032, 0.024).

In the context of other verified data, significant differences were shown in terms of soft competences between the supply vs. logistics controller {0,1} (0.027) and in terms of strategic tasks between financial vs. HR, IT controller {0,1} (0.024, 0.024); financial vs. marketing, HR, IT, distribution controller (N) (0.007, 0.037, 0.002, 0.016); logistics vs. HR, IT controller {0,1} (0.044, 0.044); logistics vs. IT controller (N) (0.037).

In contrast, statistical analysis based on the Wilcoxon–Mann–Whitney test for small samples without rank adjustment does not lead to discrimination in any subgroups/categories, so its results are not suitable for interpretation.

It is not possible to relate the analysis conclusions to the entire population based on the data collected from selected job advertisements for functional controllers. However, assuming randomness of placing offers on job websites and the lack of their positioning or sorting, it can be concluded that the differences between the study of functional controllers’ profiles are particularly evident in terms of tasks rather than competences, including meta-competences. Concerning meta competences out of five distinguished profiles of the functional controllers (280 interactions), the tests showed their relevance (3.21%) only in nine cases, all of which are related to three competencies: communication, analysis, and creativity (and thus 3/5 out of 280). In turn, concerning core competencies, there are five relevancies out of 224 tested relationship pairs. In the case of tasks, it can be stated that only forecasting was not significant in any of the discussed occupational profiles, and for 448 interactions, they were found to be important in 56 cases giving 12.5%. The level of adequacy of the description/discriminant of studied profiles considering tasks and competences is equal to 4.5. This result means 4.5 times ‘better’ differentiation of occupational profiles in tasks than in competences.

5. Discussion

The number of job advertisements posted for the position of controller in Germany in the analyzed job search engines proves that this profession is significant for the German business practice and very popular due to ICV/IGC activity [

26,

27]. On the other hand, the number of studies on functional controllers was not very high and depended on a particular type. Identification of job advertisements for production, HR, IT, and distribution controllers was the easiest, and titles of job adverts looking for marketing and supply controllers were the hardest. In contrast, the identification of job ads for logistics controllers was moderate. This is because production, HR, IT and distribution, and partly logistics are the most developed in modern business and are often outsourced. Moreover, they are essential areas of the supply chain. In other functions, many controlling tasks are performed by specialists from these departments and not by separate controllers.

In the context of competences for the analyzed functional controllers, core competences prevail over meta competences, i.e., hard over soft competences, although both categories of skills are of high importance. This is consistent with theories presented in this area [

66,

69,

70]. However, the highest number of hard competences occurred in terms of the supply controller and logistics controller, which may be related to the requirement of having technical and engineering knowledge and skills rather than knowledge and skills related to general business. Meta competences are dominated by those skills related to analysis and communication, which is in line with the role of controllers in business practice [

26,

27]. Concerning core competences, on the other hand, functional competences prevail. This is related to having specialist knowledge and skills; for example, in terms of the HR controller, the familiarity with human resources and experience in controlling or HR, and knowledge of SAP HR or HCM and SAP CO modules will be required. The fewest number indications in the job advertisements related to self-development and values/ethical competences. However, this is because employers assume that controllers will develop their knowledge and skills in their work and that their actions have to be ethical and create value inside and outside the organization.

Identifying groups of controlling tasks revealed that tasks linked to analysis prevail, especially those related to the performance measurement, financial and non-financial analysis, and deviation analysis. This is consistent with the dimension of competence in this area. Next, there are activities related to coordination and optimization. There are two approaches in this area: (1) coordination and optimization related to data and controlling tools and (2) these functions related to specific business activities (e.g., transport optimization). Most often, tasks in this area were assigned to logistics, marketing, IT, and distribution controllers.

A considerable number of indications concerned the definition of new methods and tools. Since these occupations under analysis are only just developing in German-speaking culture, there is a need to organize structures first. Then, within these structures, the tools of functional information systems of controlling should be established. Active participation in the management and decision-making process was also often indicated in the analyzed advertisements. This means that functional controllers can be called business partners [

18,

47,

54]. This notion is also proved by a significant number of controlling supporting strategic management of the organization. A substantial group of tasks of functional controllers is reporting [

55], which allows communicating information to stakeholders. Reporting is widely considered, including financial and non-financial aspects, i.e., social and environmental aspects. This means that the work of functional controllers impacts sustainable management because it supports managers in this process with the necessary information. In turn, planning and forecasting, although important categories of tasks, constitute a smaller portion of functional controllers’ work. Activities in this area are currently subject to automation and standardization or are outsourced [

16,

54].

The identity of the financial controller is worth emphasizing. The financial controller is a professional profile that has been featured in numerous job advertisements on the German market. The analysis of tasks of the financial controller indicated that, apart from typical controlling activities (budgeting, deviation analysis, forecasting), tasks include preparing financial reports and integrated reports (financial and non-financial reports); financial, non-financial, and liquidity analyses; and activities related to valuation in finance and business. This means that the financial controller is an essential support for financial accountants and CFOs in meeting international accounting standards and creating value. The analysis of competences and tasks of functional controllers shows that new occupational identities are being made among controllers in German-speaking countries. In integrating financial accounting and controlling, and therefore the impact of IFRS on accounting and value creation, the financial controller plays a unique role. In addition, its special role should be considered in the context of the impact on sustainability in the sphere of measuring not only financial but non-financial (social and environmental) issues and reporting this information. It can be pointed out that the financial controller integrates the work of other functional controllers. At the same time, from the point of view of value creation, including value chain building and taking into account the necessity to adapt the idea of sustainable development in all spheres of business, functional controllers are essential for fulfilling the objectives of value and sustainable management [

58].

To summarize, one could ask whether developing a new occupational identity in German-speaking countries is a ‘fashion’ or a necessity? The research findings indicated that the formation of functional controllers is not a fashion but a real need. This results from globalization processes related to international accounting regulations (IFRS) and sustainable development, including searching for a balance between economic, social, and environmental perspectives and reporting in these areas and value chain creation. Functional controllers with specialized knowledge and skills perform their tasks more efficiently than those without. Therefore, they can influence the value management process and sustainable management better than so-called ‘general’ controllers. Although there are differences between the functional controllers studied (concerning certain types of competences and tasks), each of them creates value for a specific function/process. As a result, an entire business and a supply chain, thanks to the competences of functional controllers and, in addition, considering sustainable development aspects into account in their tasks, influence the construction of a sustainable value chain (see

Figure 1).

6. Conclusions

Globalization strives for consistency and uniformity, which means that economies and companies are moving in one direction (sustainable development (Agenda 2030 and its goals), principles of international accounting regulations (IFRS)). However, in the process of centralization and standardization, there is a need to specialize certain areas to achieve the common direction goals more efficiently and quickly [

12,

46]. Such specialization can be seen in creating new occupational profiles in German-speaking countries in the context of controllers. Their specialized competences (core competences) and general competences (meta competences) enable them to accurately perform the tasks of measuring and reporting on a given function, which in the long run creates value for the entire business and thus the supply chain. In addition, functional controllers with detailed knowledge of their area can effectively support managers responsible for their management in implementing sustainability concepts. It is worth noting that the business’s complexity, or individual functions, results in specialists being responsible for them (managers), not having sufficient ‘capacity’ (e.g., time, own resources). The organization of activities and their simultaneous measurement and dispersion of data within the organization between different business units in the supply chain can result in wrong decisions. Additionally, sudden turns in economies (e.g., the situation with COVID-19 pandemics) require industry-specific knowledge to better deal with the resulting difficulties. Thus, a functional controller proves to be adequate support in such cases.

The paper contributes to science by developing the research on accounting in the context of occupational/professional profiles of functional controllers, and in addition, the reference of controllers to management accountants, taking into account the German and Anglo-Saxon conditions, also seems essential [

17,

25,

30,

40,

45,

48,

54]. Secondly, the study contributes to education as it pays more attention to creating study programs separate from controlling, but with appropriate emphasis on the design of courses with its comprehensive specialization (mainly in developing and emerging countries). In addition, the suggested trend signals that courses in functional controlling in business study programs (e.g., HR Management, Logistics, Supply Chain Management, apart from Accounting and Finance) should be added. Thirdly, it is an indication for complex business activities that appointing an additional specialist, i.e., a functional controller as an effective coordinator for significant production-related functions, would add value to the organization and supply chains. Fourthly, due to the influence of the German economy on the countries of Central and Eastern Europe (the spread of controlling in companies with German capital and the dynamic activity of ICV/IGC in recent years), it can be assumed that new controller profiles, i.e., functional controllers, will soon develop in the indicated geographical area. This should be a stimulus for universities to change their syllabuses to meet business expectations. Fifth, if companies and supply chains want to survive in the global marketplace and pursue global strategies, i.e., sustainable development in an efficient way and in a shorter time, the inclusion of functional controllers among the permanent workforce seems to be an appropriate action in pursuing this strategy [

5,

13,

14,

59].

The article has limitations. First of all, job advertisements are prepared according to a specific structure. Many types of competences or tasks are standardized, so they do not always reflect the particular character of the work of analyzed controllers. Moreover, the assignment of studied categories of job advertisements is partly subjective. Thirdly, the analysis of research issues refers primarily to large organizations, most often operating globally in supply chains, where there is a need to coordinate many functions simultaneously. In addition, in large organizations, the impact of IFRS and sustainability on controlling can be seen, and the links between financial controllers and other types of controllers can be observed.

The research presented in the article has a developmental character. Therefore, it would be worthwhile to survey functional controllers to verify the nature of the competences and tasks needed and developed in their work, particularly in the context of sustainability and value chain creation. For example, a study may investigate the implementation of a case study in a company that employs several functional controllers simultaneously. Thus the actual relationships between them and their strength can be shown. It would also be worthwhile to verify the essential need (e.g., survey research) among enterprises (managers, owners) to employ functional controllers in countries other than Germany. In turn, the results of this study lead to the following recommendations for further statistical analyses: (1) carrying out tests with corrections for bonded ranks, continuity, and large samples; (2) carrying out multidimensional cluster or discriminatory analyses; and (3) carrying out analysis of market trends over time, assuming a larger sample size and automatic data acquisition for the study.

{kind=link}