The Customer Orientation Service of Spanish Brokers in the Insurance Industry: The Advisory Service of the Insurance Distribution Channel Bancassurance

Abstract

1. Introduction

2. Literature Review

2.1. Insurance Broker

2.2. Bancassurance Distribution Channel

3. Hypotheses to be Tested and Research Design

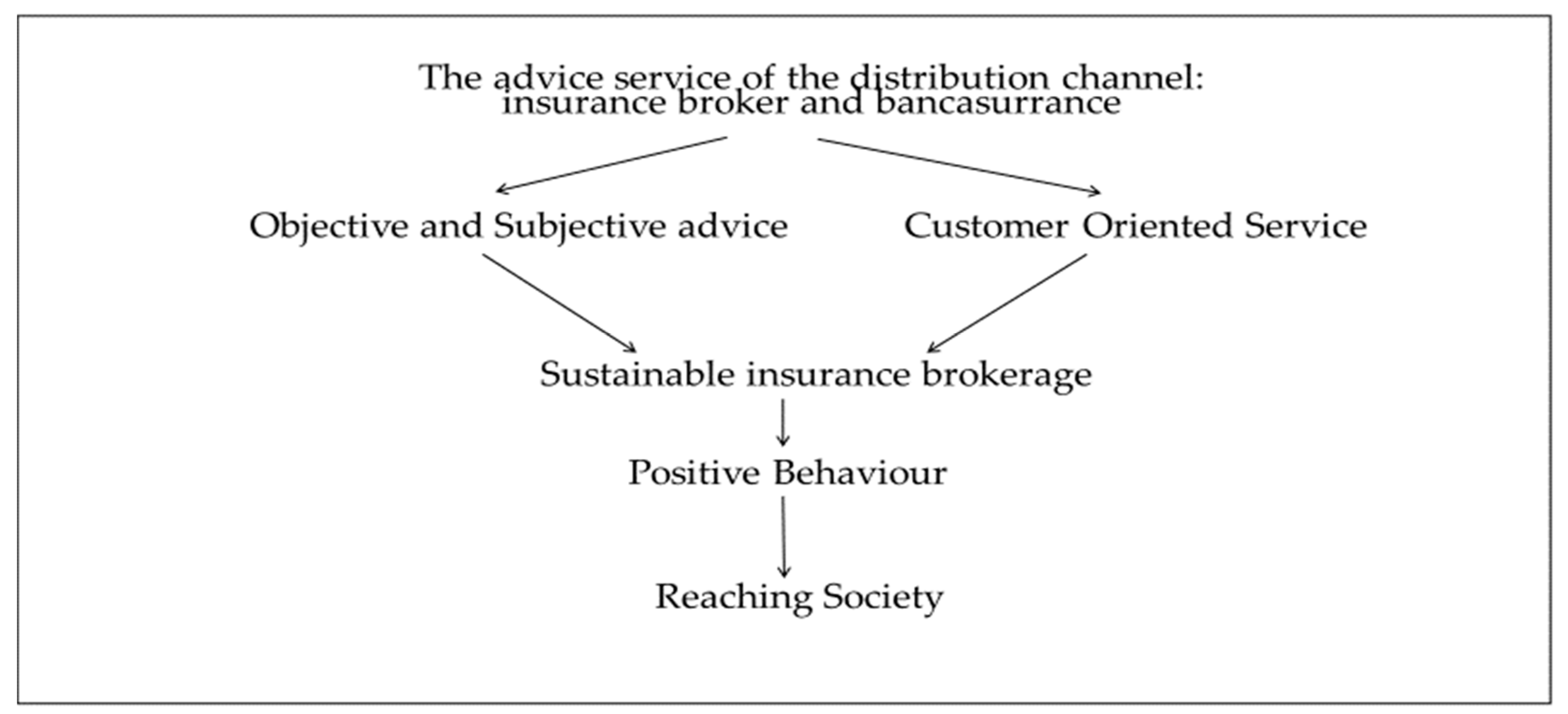

- The advisory service of the distribution channel: insurance broker and bancassurance evaluates customer perception of the advisory service provided by the broker and banks’ services.

- Objective and subjective advice: describes the form of the selection of risks and the information provided by the intermediary.

- Customer-oriented Service: evaluates the extent of customers’ positive perception of the benefits of insurance coverage and the value of insurance services.

- Sustainable insurance brokerage: measures sustainable services that satisfy customers’ needs.

- Positive behaviour: evaluates the client’s perception of the payment of insurance premiums within the established deadlines to the insurance companies.

- Reaching society associates: a positive behaviour towards the customer with its benefits for society.

4. Sample and Methodology

4.1. Data and Sample Selection

4.2. Descriptive Characteristics of the Sample

4.3. Estimation of Accounting Ratios to Measure Operating Performance of the Insurance Brokers

4.4. Panel Data Regression Analysis Estimates of the Customer-Oriented Responsibility Ratio for the Full Sample

5. Results

5.1. Univariant Analysis Results

5.2. Multivariant Analysis Results

6. Discussion, Implications and Limitations

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| Euribor: | European Interbank Offered Rate |

| SABI: | Iberian Balance Analysis System |

| EC: | European Parliament and of the Council |

| H: | Hypotheses |

| GDP: | Gross Domestic Product |

| ROA: | Return on assets |

| ROE: | Return on equity |

| ROS: | Return on sales |

| SALEFF: | Sales efficiency |

| INEFF: | Income efficiency |

| EMPL: | Total employment |

| TDTA: | Total debt to total assets |

| CACL: | Current assets to current liabilities |

| EBIT: | Earnings Before Interest and Taxes |

| GDP: | Gross Domestic Product |

References

- Marano, P. Navigating InsurTech: The digital intermediaries of insurance products and customer protection in the EU. Maastricht J. Eur. Comp. Law 2019, 26, 294–315. [Google Scholar] [CrossRef]

- Euribor-Rates. EU. Available online: http://es.euribor-rates.eu/tipos-de-interes-Euribor-por-ano.asp (accessed on 25 March 2019).

- Pani, L.K.; Swain, S. Bancassurance and Indian banks. Int. J. Res. Dev. A Manag. Rev. 2013, 2, 11–19. [Google Scholar]

- Alavudeen, R.; KD, S.R. Growing Role of Bancassurance in Banking Sector. Bonfring Int. J. Ind. Eng. Manag. Sci. 2015, 5, 10–16. [Google Scholar] [CrossRef]

- Jan, A.; Baber, H. Bancassurance-Growth Guaranteed In India. Econ. Financ. Lett. 2014, 1, 104–113. [Google Scholar] [CrossRef][Green Version]

- Yıldırım, İ. Insurance Distribution Channels in Turkey: Effectiveness of Bancassurance. Int. J. Trends Econ. Manag. Technol. 2014, 3, 7–10. [Google Scholar]

- Boadi, E.K.; Antwi, S.; Lartey, V.C. Determinants of profitability of insurance firms in Ghana. Int. J. Bus. Soc. Res. 2013, 3, 43–50. [Google Scholar]

- Kabajeh, M.A.M.; Al Nuaimat, S.M.A.; Dahmash, F.N. The relationship between the ROA, ROE and ROI ratios with Jordanian insurance public companies market share prices. Int. J. Hum. Soc. Sci. 2012, 2, 115–120. [Google Scholar]

- Anuonye, N.B. Effect of intellectual capital on return on assets of insurance firms in Nigeria. Glob. J. Manag. Bus. Res. 2016, 16, 2249–4588. [Google Scholar]

- Greene, W.H.; Segal, D. Profitability and efficiency in the US life insurance industry. J. Product. Anal. 2004, 21, 229–247. [Google Scholar] [CrossRef]

- Malik, H. Determinants of insurance companies’ profitability: An analysis of insurance sector of Pakistan. Acad. Res. Int. 2011, 1, 315. [Google Scholar]

- Chen, M.S.; Chang, P.L. Distribution channel strategy and efficiency performance of the life insurance industry in Taiwan. J. Financ. Serv. Mark. 2010, 15, 62–75. [Google Scholar] [CrossRef]

- Pointer, L.V.; Khoi, P.D. Predictors of Return on Assets and Return on Equity for Banking and Insurance Companies on Vietnam Stock Exchange. Entrep. Bus. Econ. Rev. 2019, 7, 185–198. [Google Scholar] [CrossRef]

- Barber, B.M.; Lyon, J.D. Detecting abnormal operating performance: The empirical power and specification of test statistics. J. Financ. Econ. 1996, 41, 359–399. [Google Scholar] [CrossRef]

- Boubakri, N.; Cosset, J.C. The financial and operating performance of newly privatized firms: Evidence from developing countries. J. Financ. 1998, 53, 1081–1110. [Google Scholar] [CrossRef]

- Alonso, R. La nueva Regulación de los mediadores de seguros. ICADE Rev. Cuatrimest. Fac. Derecho Cienc. Económicas Empresariales 2007, 71, 35–57. [Google Scholar]

- Latorre, M.A. Shedding the light on insurance brokers’ remuneration: The role of the fees. Opción 2015, 31, 654–676. [Google Scholar]

- Latorre, M.A.; Farinos, J.E. Ethical behaviour and operating performance of insurance broker firms. J. Int. Bus. Econ. 2015, 3, 44–51. [Google Scholar] [CrossRef]

- Eckardt, M. Agent and broker intermediaries in insurance markets-An empirical analysis of market outcomes. Thünen Ser. Appl. Econ. Theory 2002, 4, 1–32. [Google Scholar] [CrossRef]

- Eckardt, M. Insurance Intermediation: An Economic Analysis of the Information Services Market; Springer: Heilderber, Germany, 2007. [Google Scholar]

- Kim, Y.; Mo, J. Pricing of Digital Video Supply Chain: Free versus Paid Service on the Direct Distribution Channel. Sustainability 2019, 11, 46. [Google Scholar] [CrossRef]

- Traub, W. Markfunktion und Dienstleistung des Versicherungsmaklers. In Zeitschriftfür die Gesamte Versicherungswirtschaft; Springer-Verlag GmbH: Berlin, Germany, 1994; pp. 369–397. [Google Scholar]

- Rose, F. The economics, concept, and design of information intermediaries. Inf. Age Econ. 1999, 163–207. [Google Scholar]

- Cummins, J.; Doherty, N. The economics of insurance intermediaries. J. Risk Insur. 2006, 73, 359–396. [Google Scholar] [CrossRef]

- Doman, A.; Duchen, T.; Martin, M. Brokers vs. insurers. Mckinsey Q. 1999, 3, 26–35. [Google Scholar]

- Tseng, L.M.; Kang, Y.M. The influences of sales compensations, management stringency and ethical evaluations on product recommendations made by insurance brokers. J. Financ. Regul. Compliance 2014, 22, 26–42. [Google Scholar] [CrossRef]

- Nguyen, H.T.; Nguyen, H.; Nguyen, N.D.; Phan, A.C. Determinants of customer satisfaction and loyalty in Vietnamese life-insurance setting. Sustainability 2018, 10, 1151. [Google Scholar] [CrossRef]

- Owusu-Sekyere, F.; Kotey, R.A. Profitability of insurance brokerage firms in Ghana. Acad. J. Econ. Stud. 2019, 5, 179–192. [Google Scholar]

- Law 26/2006 of July 17, Insurance Mediation and Private Reinsurance. Available online: www.dgsfp.mineco.es (accessed on 14 March 2020).

- Morgan, G.; Sturdy, A.; Daniel, J.P.; Knights, D. Bancassurance in Britain and France: Innovating strategies in the financial services. Geneva Pap. Risk Insur. Issues Pract. 1994, 19, 178–195. [Google Scholar] [CrossRef][Green Version]

- Benoist, G. Banc assurance: The new challenges. Geneva Pap. Risk Insur. Issues Pract. 2002, 27, 295–303. [Google Scholar] [CrossRef]

- Teunissen, M. Bancassurance: Tapping into the banking strength. Geneva Pap. Risk Insur. Issues Pract. 2008, 33, 408–417. [Google Scholar] [CrossRef][Green Version]

- Gonulal, S.O.; Goulder, N.; Lester, R.R. Bancassurance—A Valuable Tool for Developing Insurance in Emerging Markets; Working Paper: 6196; World Bank Policy Research; The World Bank: Washington, DC, USA, 2012. [Google Scholar]

- Chen, T.J. Marketing channel, corporate reputation, and profitability of life insurers: Evidence of bancassurance in Taiwan. Geneva Pap. Risk Insur. Issues Pract. 2019, 44, 679–701. [Google Scholar] [CrossRef]

- Arguedas, S.B. Banca-seguros: Nueva alternativa de intermediación en la región centroamericana con sus implicaciones legales. Rev. Ibero-Latinoam. Seguros 2008, 17, 23–41. [Google Scholar]

- Belz, F.M.; Peattie, K. Sustainability Marketing: A Global Perspective, 2nd ed.; Wiley & Sons Ltd.: Chichester, UK, 2012. [Google Scholar]

- Brady, M.; Knight, G.; Cronin, J.; Tomas, G.; Hult, G.; Keillor, B. Removing the contextual lens: A multinational, multi-setting comparison of service evaluation models. J. Retail. 2005, 81, 215–230. [Google Scholar] [CrossRef]

- Park, E.; Lee, S.; Kwon, S.J.; delPobil, A.P. Determinants of Behavioral Intentions to use South Korean Airline Services: Effects of Service Quality and Corporate Social Responsibility. Sustainability 2015, 7, 12106–12121. [Google Scholar] [CrossRef]

- Game, A.M.; Gregoriou, A. Do brokers act in the best interests of their clients? New evidence from electronic trading systems. Bus. Ethics Eur. Rev. 2016, 25, 185–197. [Google Scholar] [CrossRef]

- Ronald, D. The Etichs of Reward Sytems in the Financial Services Industry. Bus. Soc. Rev. 2002, 104, 34–41. [Google Scholar]

- Kurland, N.B. Sales agents and clients: Ethics, incentives, and a modified theory of planned behavior. Hum. Rel. 1996, 49, 51–74. [Google Scholar] [CrossRef]

- Kaptein, M. The appearance standard: Criteria and remedies for when a mere appearance of unethical behaviour is morally unacceptable. Bus. Ethics Eur. Rev. 2019, 28, 99–111. [Google Scholar] [CrossRef]

- Boatright, J.R. Ethics in Finance; John Wiley & Sons: West Sussex, UK, 2013. [Google Scholar]

- European Parliament and the Council. Directive 2002/92/EC on Insurance Mediation. Brussels (Belgium). 2002. Available online: www.ec.europa.eu (accessed on 14 March 2020).

- Latorre, M.A. La problemática de la gestión de cobro en una correduría de seguros. In Ebook Contenidos Innovadores Dentro de las Ciencias Naturales; Aplicadas y de la Salud. Libro digital; McGraw-Hill Interamericana de España S.: Madrid, España, 2015; Chapter 6; pp. 75–86. [Google Scholar]

- Ennew, C.T.; Reed, G.V.; Binks, M.R. Importance-performance analysis and the measurement of service quality. Eur. J. Mark. 1993, 27, 59–70. [Google Scholar] [CrossRef]

- Zeithaml, V.A.; Berry, L.L.; Parasuraman, A. The behavioral consequences of service quality. J. Mark. 1996, 60, 31–46. [Google Scholar] [CrossRef]

- Heskett, J.L.; Jones, T.O.; Loveman, G.W.; Sasser, W.E.; Schlesinger, L.A. Putting the service profit chain to work. Harv. Bus. Rev. 1994, 72, 105–111. [Google Scholar]

- Zikmund, W.G.; Babin, B.J.; Carr, J.C.; Griffin, M. Business Research Methods, 8th ed.; South Western Cengage Learning: Mason, OI, USA, 2010. [Google Scholar]

- Asogwa, J.O.; Onyekwelu, U.L. Relationship between Fundamental Accounting Ratios and Firms’market Valuation in Brewery Firms in Nigeria. Adv. J. Manag. Account. Financ. 2019, 4, 7. [Google Scholar]

- David, A. Freedman. In Statistical Models: Theory and Practice; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Simon, L.J. Size, Strength and Profit. In Proceedings of the Casualty Actuarial Society Casualty Actuarial Society, Arlington, Texas, 22–23 May 1962; pp. 41–48. [Google Scholar]

- Lee, H.H.; Lee, C.Y. An analysis of reinsurance and firm performance: Evidence from the Taiwan property-liability insurance industry. Geneva Pap. Risk Insur. Issues Pract. 2012, 37, 467–484. [Google Scholar] [CrossRef]

- Liebenberg, A.P.; Sommer, D.W. Effects of corporate diversification: Evidence from the property–liability insurance industry. J. Risk Insur. 2008, 75, 893–919. [Google Scholar] [CrossRef]

- Sandhu, H.S.; Neetu, B. Customers’ Perception towards Service Quality of Life Insurance Corporation of India: A Factor Analytics Approach. Int. J. Bus. Soc. Sci. 2011, 2, 219–231. [Google Scholar]

- Gera, R. Modelling the service antecedents of favourable and unfavourable behaviour intentions in life insurance services in the India: An SEM study. Int. J. Qual. Serv. Sci. 2011, 3, 225–242. [Google Scholar] [CrossRef]

- Anagol, S.; Cole, S.; Sarkar, S. Understanding the advice of commissions-motivated agents: Evidence from the Indian life insurance market. Rev. Econ. Stat. 2017, 99, 1–15. [Google Scholar] [CrossRef]

- Inderst, R.; Ottaviani, M. Competition through commissions and kickbacks. Am. Econ. Rev. 2012, 102, 780–809. [Google Scholar] [CrossRef]

- Gabaix, X.; Laibson, D. Shrouded attributes, consumer myopia, and information suppression in competitive markets. Q. J. Econ. 2006, 121, 505–540. [Google Scholar] [CrossRef]

- Bolton, P.; Freixas, X.; Shapiro, J. Conflicts of interest, information provision, and competition in the financial services industry. J. Financ. Econ. 2007, 85, 297–330. [Google Scholar] [CrossRef]

- Hoechle, D.; Ruenzi, S.; Schaub, N.; Schmid, M. Financial advice and bank profits. Rev. Financ. Stud. 2018, 31, 4447–4492. [Google Scholar] [CrossRef]

- Ahmad, G.N.; Prasetyo, R.P. Profitability Analysis of Non-life Insurance: Case in Indonesia Stock Exchange. KnE Soc. Sci. 2018, 2018, 335–350. [Google Scholar] [CrossRef]

- Egbunike, C.F.; Okerekeoti, C.U. Macroeconomic factors, firm characteristics and financial performance. Asian J. Account. Res. 2018, 3, 142–168. [Google Scholar] [CrossRef]

- Burca, A.M.; Batrinca, G. The determinants of financial performance in the Romanian insurance market. Int. J. Acad. Res. Account. Financ. Manag. Sci. 2014, 4, 299–308. [Google Scholar] [CrossRef]

- Baltagi, B. Econometric Analysis of Panel Data, 3rd ed.; John Wiley & Sons: West Sussex, UK, 2008. [Google Scholar]

- Alipour, M.; Ghanbari, M.; Jamshidinavid, B.; Taherabadi, A. Does board independence moderate the relationship between environmental disclosure quality and performance? Evidence from static and dynamic panel data. Corp. Gov. Int. J. Bus. Soc. 2019, 19, 580–610. [Google Scholar] [CrossRef]

- Charumathi, B. On the determinants of profitability of Indian life insurers—An empirical study. In Proceedings of the World Congress on Engineering, London, UK, 4–6 July 2012; Volume 1, pp. 4–6. [Google Scholar]

- Mehari, D.; Aemiro, T. Firm Specific Factors that Determine Insurance Companies’ Performance in Ethiopia. Eur. Sci. J. 2013, 9. [Google Scholar] [CrossRef]

- Tukur, G.; Balkisu, A.A. Corporate board diversity and financial performance of insurance companies in Nigeria: An application of panel data approach. Asian Econ. Financ. Rewiew 2014, 4, 257–277. [Google Scholar]

- Batool, A.; Sahi, C.A. Determinants of Financial Performance of Insurance Companies of USA and UK during Global Financial Crisis (2007–2016). Int. J. Account. Res. 2019, 7, 194. [Google Scholar] [CrossRef]

- Kobayashi, M. Comparison of efficiencies of several estimators for linear regressions with autocorrelated errors. J. Am. Stat. Assoc. 1985, 80, 951–953. [Google Scholar] [CrossRef]

- King, M.L.; Giles, D.E. (Eds.) Specification Analysis in the Linear Model, 1st ed.; Routledge: London, UK, 2018. [Google Scholar]

- Gujarati, D. Basic Econometrics; McGraw-Hill: New York, NY, USA, 1995. [Google Scholar]

- Dumm, R.E.; Hoyt, R.E. Insurance distribution channels: Markets in transition. J. Insur. Regul. 2003, 22, 27–48. [Google Scholar]

- Beloucif, A.; Donaldson, B.; Kazanci, U. Insurance broker–client relationships: An assessment of quality and duration. J. Financ. Serv. Mark. 2004, 8, 327–342. [Google Scholar] [CrossRef]

- Trigo-Gamarra, L. Reasons for the coexistence of different distribution channels: An empirical test for the German insurance market. Geneva Pap. Risk Insur. Issues Pract. 2008, 33, 389–407. [Google Scholar] [CrossRef]

- Lymperopoulos, C.; Chaniotakis, I.E.; Soureli, M. The importance of service quality in bank selection for mortgage loans. Manag. Serv. Qual. 2006, 16, 365–379. [Google Scholar] [CrossRef]

- Hoschka, T.C. Bancassurance in Europe; Springer: London, UK, 2016. [Google Scholar]

- Das, S.K. Social and innovative banking strategies for sustainable banking in India. Int. J. Econ. Financ. Manag. 2013, 2, 91183817. [Google Scholar]

- Kamath, K.V.; Kohli, S.S.; Shenoy, P.S.; Kumar, R.; Nayak, R.M.; Kuppuswamy, P.T.; Ravichandran, N. Indian banking sector: Challenges and opportunities. Vikalpa 2003, 28, 83–100. [Google Scholar] [CrossRef]

- Fayed, A.M.; Dubey, S. An empirical study of impact of EVA momentum on the shareholders’ value creation as compared to traditional financial performance measures-with special reference to the UAE. Int. J. Econ. Financ. 2016, 8, 23–38. [Google Scholar] [CrossRef]

- Anderson, D.R.; Anderson, K.E. Sustainability risk management. Risk Manag. Insur. Rev. 2009, 12, 25. [Google Scholar] [CrossRef]

- King, G.; Smallman, C.; Van Weegen, M. Management strategy in UK insurance broking. Manag. Decis. 1997, 35, 58–67. [Google Scholar] [CrossRef]

- Froestad, J.; Gjuvsland, K.; Herbstein, T.; Shearing, C. Insurance as a regulatory mechanism towards sustainable companies. In Proceedings of the Towards Sustainable Companies Conference UiO, Oslo, Norway, 29–30 August 2011. [Google Scholar]

- Nebo, G.N.; Okolo, V.O. Effects of the strategies for customer satisfaction on the performance of insurance firms in Enugu Metropolis. J. Bus. Manag. 2016, 18, 78–90. [Google Scholar]

- Fernández, E.; Iglesias-Antelo, S.; López-López, V.; Rodríguez-Rey, M.; Fernandez-Jardon, C.M. Firm and industry effects on small, medium-sized and large firms’ performance. BRQ Bus. Res. Q. 2019, 22, 25–35. [Google Scholar] [CrossRef]

{kind=link}

| Insurance Mediators Spanish Markets | 2013 | 2017 | Difference | % |

|---|---|---|---|---|

| Insurance Brokers | 3038 | 3272 | 234 | 7.70% |

| Insurance Agents | 86,042 | 76,044 | −9998 | −11.62% |

| Bancassurance operators | 53 | 49 | −4 | −8.16% |

| Total Insurance Mediators | 89,133 | 79,365 | −9768 | −12.08% |

| Observations | |

|---|---|

| Initial Sample | 500 |

| Companies whose information on financial income and sales is not available in the Sabi database | (103) |

| Final Sample | 397 |

| Year | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| Panel A: Full Sample | |||||

| Sample size | 397 | 397 | 397 | 397 | 397 |

| No. of employees | 20.34 | 20.96 | 21.3 | 23.01 | 25.27 |

| Total assets (thousand €) | 1704.89 | 1801.75 | 1872.17 | 2024.31 | 2091.39 |

| Sales (thousand €) | 1372.42 | 1552.49 | 1703.07 | 1885.49 | 2035.51 |

| Financial income (thousand €) | 30.54 | 27.06 | 20.34 | 20.31 | 45.67 |

| Customer-oriented responsibility ratio (%) | 2.23 | 1.74 | 1.19 | 1.08 | 2.24 |

| Panel B: Low customer-oriented responsibility ratio | |||||

| Sample size | 119 | 119 | 119 | 119 | 119 |

| No. of employees | 9.33 | 11.83 | 12.82 | 13.34 | 15.47 |

| Total assets (thousand €) | 300.80 | 348.43 | 409.78 | 457.10 | 520.26 |

| Sales (thousand €) | 210.27 | 307.49 | 412.37 | 462.61 | 506.80 |

| Financial income (thousand €) | 10.31 | 5.44 | 0.46 | 0.23 | 00.00 |

| Customer-oriented responsibility ratio (%) | 4.90 | 1.77 | 0.11 | 0.05 | 0.00 |

| Panel C: High customer-oriented responsibility ratio | |||||

| Sample size | 119 | 119 | 119 | 119 | 119 |

| No. of employees | 20.57 | 20.75 | 21.25 | 21.55 | 22.14 |

| Total assets (thousand €) | 700.25 | 713.18 | 694.95 | 764.36 | 844.60 |

| Sales (thousand €) | 415.13 | 372.13 | 363.65 | 372.13 | 415.13 |

| Financial income (thousand €) | 14.60 | 17.82 | 16.09 | 17.89 | 44.18 |

| Customer-oriented responsibility ratio (%) | 3.94 | 4.81 | 4.42 | 5.12 | 10.64 |

| Proxies | Measurement | Characteristics |

|---|---|---|

| Return on assets (ROA) | = EBIT/Average total assets | Profitability |

| Return on equity (ROE) | = EBIT /Average total equity | Profitability |

| Return on sales (ROS) | = EBIT/Sales | Profitability |

| Sales efficiency (SALEFF) | = Real sales/Total employment | Operating efficiency |

| Size (SIZE) | = Total Assets | Size |

| Income efficiency (INEFF) | = EBIT/ Total employment | Employment |

| Total employment (EMPL) | = Total number of employees | Employment |

| Total debt to total assets (TDTA) | = Total debt/Total assets | Leverage |

| Current assets to current liabilities (CACL) | = Current assets/current liabilities | Liquidity |

| 2013 | 2014 | 2015 | 2016 | 2017 | |

|---|---|---|---|---|---|

| Panel A: | Low customer-oriented responsibility ratio group | ||||

| ROA | 0.01 | 0.01 | 0.01 | 0.01 | 0.00 |

| ROE | 0.01 | 0.03 | 0.04 | 0.04 | 0.04 |

| ROS | 0.11 | 0.11 | 0.12 | 0.12 | 0.15 |

| SALEFF | 79.65 | 80.39 | 95.24 | 90.92 | 102.60 |

| INEFF | 9.91 | 9.23 | 10.96 | 13.68 | 14.51 |

| EMPL | 4.00 | 5.00 | 6.00 | 5.00 | 6.00 |

| TDTA | 0.04 | 0.54 | 0.60 | 0.44 | 0.57 |

| CACL | 1.25 | 1.28 | 1.48 | 1.50 | 1.59 |

| Panel B: | High customer-oriented responsibility ratio group | ||||

| ROA | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 |

| ROE | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 |

| ROS | 0.18 | 0.17 | 0.17 | 0.22 | 0.19 |

| SALEFF | 100.97 | 101.13 | 110.13 | 111.49 | 108.53 |

| INEFF | 16.96 | 17.90 | 16.72 | 18.14 | 19.18 |

| EMPL | 7.00 | 6.50 | 7.00 | 6.00 | 7.00 |

| TDTA | 0.02 | 0.27 | 0.25 | 0.21 | 0.21 |

| CACL | 2.46 | 2.57 | 3.13 | 3.30 | 3.61 |

| Panel C: | (High–Low) customer-oriented responsibility ratio groups | ||||

| ROA | a 0.01 | b 0.01 | 0.01 | 0.01 | 0.02 |

| ROE | b 0.02 | 0.00 | −0.01 | −0.01 | c −0.01 |

| ROS | b 0.07 | a 0.06 | 0.05 | b 0.10 | 0.04 |

| SALEFF | c 21.32 | b 20.74 | 14.89 | 20.57 | 5.93 |

| INEFF | c 7.05 | a 8.67 | b 5.76 | 4.46 | c 4.67 |

| EMPL | a 3.00 | c 1.50 | 1.00 | 1.00 | 1.00 |

| TDTA | b −0.02 | a −0.27 | a −0.35 | a −0.23 | a −0.36 |

| CACL | a 1.21 | a 1.29 | a 1.65 | a 1.80 | a 2.02 |

| Insurance % | Bancassurance Premium | Broker Premium | Bancassurance Commissions | Broker Commissions | Broker Fees | Broker Com.+ Fees | Difference Commissions |

|---|---|---|---|---|---|---|---|

| Health | 1.07 | 3.07 | 28.95 | 8.97 | 0.03 | 9.00 | −19.95 |

| Car | 18.65 | 27.36 | 10.81 | 11.93 | 2.06 | 14.00 | 3.19 b |

| Accident | 5.13 | 4.09 | 25.31 | 17.21 | 1.07 | 18.28 | −7.03 |

| Transport | 0,11 | 4.44 | 16.46 | 12.06 | 0.36 | 12.42 | −4.04 |

| Travel | 0.18 | 1.18 | 16.82 | 21.71 | 0.04 | 21.75 | 4.93 b |

| Multi-risk Home | 41.86 | 5.23 | 21.19 | 24.16 | 0.15 | 24.32 | 3.13 b |

| Multi-risk Shops | 2.87 | 2.21 | 22.88 | 18.30 | 4.89 | 23.19 | 0.31 |

| Multi-risk Industrial | 2.55 | 6.60 | 19.41 | 13.81 | 0.78 | 14.59 | −4.82 b |

| General Liability | 2.32 | 11.95 | 18.40 | 13.43 | 0.46 | 13.90 | −4.50 |

| Insurance % | Bancassurance Premium | Broker Premium | Bancassurance Commissions | Broker Commissions | Broker Fees | Broker Com.+ Fees | Difference Commissions |

|---|---|---|---|---|---|---|---|

| Health | 1.53 | 1.51 | 36.69 | 15.35 | 0.04 | 15.39 | −21.30 |

| Car | 16.06 | 31.76 | 12.61 | 12.09 | 1.51 | 13.60 | 0.99 b |

| Accident | 5.16 | 3.67 | 25.91 | 17.66 | 0.19 | 17.85 | −8.06 |

| Transport | 0.15 | 6.06 | 13.71 | 12.23 | 0.18 | 12.41 | −1.30 |

| Travel | 0.38 | 1.93 | 19.92 | 24.57 | 0.03 | 24.60 | 4.68 b |

| Multi-risk Home | 18.06 | 3.61 | 21.35 | 25.97 | 0.17 | 26.14 | 4.79 b |

| Multi-risk Shops | 3.03 | 1.83 | 24.95 | 18.33 | 0.12 | 18.46 | −6.49 |

| Multi-risk ndustrial | 2.54 | 5.35 | 19.03 | 13.13 | 0.38 | 13.51 | −5.52 b |

| General Liability | 2.61 | 10.43 | 18.86 | 13.96 | 0.62 | 14.58 | −4.28 |

| Variables | Firm-year Obs. | Mean | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|

| ROA | 1956 | 0.0256769 | 0.0898855 | −3.148431 | 0.5112977 |

| ROE | 1962 | 0.0750231 | 0.3713187 | −5.335539 | 8.688471 |

| ROS | 1899 | 0.1898202 | 1.941489 | −34.19343 | 64.20772 |

| LEV | 1927 | 0.3839274 | 0.351499 | 0 | 4.508143 |

| LIQ | 1933 | 2.016168 | 3.447185 | 0 | 14.859.5 |

| SIZE | 1924 | 7.599825 | 1.122057 | 0.0927706 | 12.21656 |

| SALES | 1894 | 6.872502 | 1.556864 | 0.6174857 | 12.03256 |

| CUS | 1894 | 0.5406291 | 10.61705 | 0 | 41.46062 |

| Variable | Lev | Liq | Size | Sales | Cus |

|---|---|---|---|---|---|

| Lev | 1 | ||||

| Liq | −0.0566 | 1 | |||

| Size | 0.1069 | 0.0543 | 1 | ||

| Sales | 0.2149 | −0.0939 | 0.6676 | 1 | |

| Cus | −0.0472 | 0.8926 | 0.0872 | −0.1304 | 1 |

| ROA | ROE | ROS | ||||

|---|---|---|---|---|---|---|

| Independent Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

| Size | 0.0092 a | −0.0069 | 0.3393 b | |||

| Sales | 0.0165 a | 0.0260 | −0.2671 a | |||

| Leverage | 0.0006 | −0.0001 | 0.1287 | 0.1207 a | 0.2610 | 0.4157 b |

| Customer | −0.0000 | 0.0000 | −0.0000 | 0.0000 | 0.0056 | 0.0054 |

| Constant | −0.0422 b | −0.0853 a | 0.0806 | −0.1483 | −2.4989 b | 1.8632 a |

| Adjusted R-squared | 2.13 | 9.99 | 0.01 | 1.78 | 0.02 | 0.01 |

| ROA | ROE | ROS | ||||

|---|---|---|---|---|---|---|

| Independent Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

| Size | 0.0083 a | 0.0042 | 0.1158 b | |||

| Sales | 0.0131a | 0.0219 c | −0.0677 c | |||

| Leverage | −0.0042 | −0.0077 c | 0.1171 a | 0.1057 a | 0.1505 | 0.2373 |

| Customer | −0.0000 | 0.0000 | −0.0001 | 0.0001 | −0.0043 | −0.0043 |

| Constant | −0.0330 c | −0.0582 a | 0.0010 | −0.1131b | −0.7476 c | 0.5648 b |

| Adjusted R-squared | 2.89 | 11.31 | 1.03 | 1.77 | 0.01 | 0.03 |

| ROA | ROE | ROS | ||||

|---|---|---|---|---|---|---|

| Independent Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

| Size | 0.0094 a | 0.0084 | 0.1428 | |||

| Sales | 0.0131 a | 0.0252 a | −0.0366 | |||

| Leverage | −0.0116 a | −0.0169 a | 0.0948 c | 0.0848 c | 0.3739 c | 0.4243 |

| Customer | −0.0001 b | 0.0000 | −0.0001 | 0.0001 | −0.0020 | 0.0018 |

| Constant | −0.0386 b | −0.0551 a | −0.0206 | −0.1263 b | −1.0353 | 0.2848 |

| Adjusted R-squared | 4.17 | 11.42 | 0.77 | 1.35 | 0.36 | 0.24 |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Latorre Guillem, M.A. The Customer Orientation Service of Spanish Brokers in the Insurance Industry: The Advisory Service of the Insurance Distribution Channel Bancassurance. Sustainability 2020, 12, 2970. https://doi.org/10.3390/su12072970

Latorre Guillem MA. The Customer Orientation Service of Spanish Brokers in the Insurance Industry: The Advisory Service of the Insurance Distribution Channel Bancassurance. Sustainability. 2020; 12(7):2970. https://doi.org/10.3390/su12072970

Chicago/Turabian StyleLatorre Guillem, Miguel Angel. 2020. "The Customer Orientation Service of Spanish Brokers in the Insurance Industry: The Advisory Service of the Insurance Distribution Channel Bancassurance" Sustainability 12, no. 7: 2970. https://doi.org/10.3390/su12072970

APA StyleLatorre Guillem, M. A. (2020). The Customer Orientation Service of Spanish Brokers in the Insurance Industry: The Advisory Service of the Insurance Distribution Channel Bancassurance. Sustainability, 12(7), 2970. https://doi.org/10.3390/su12072970