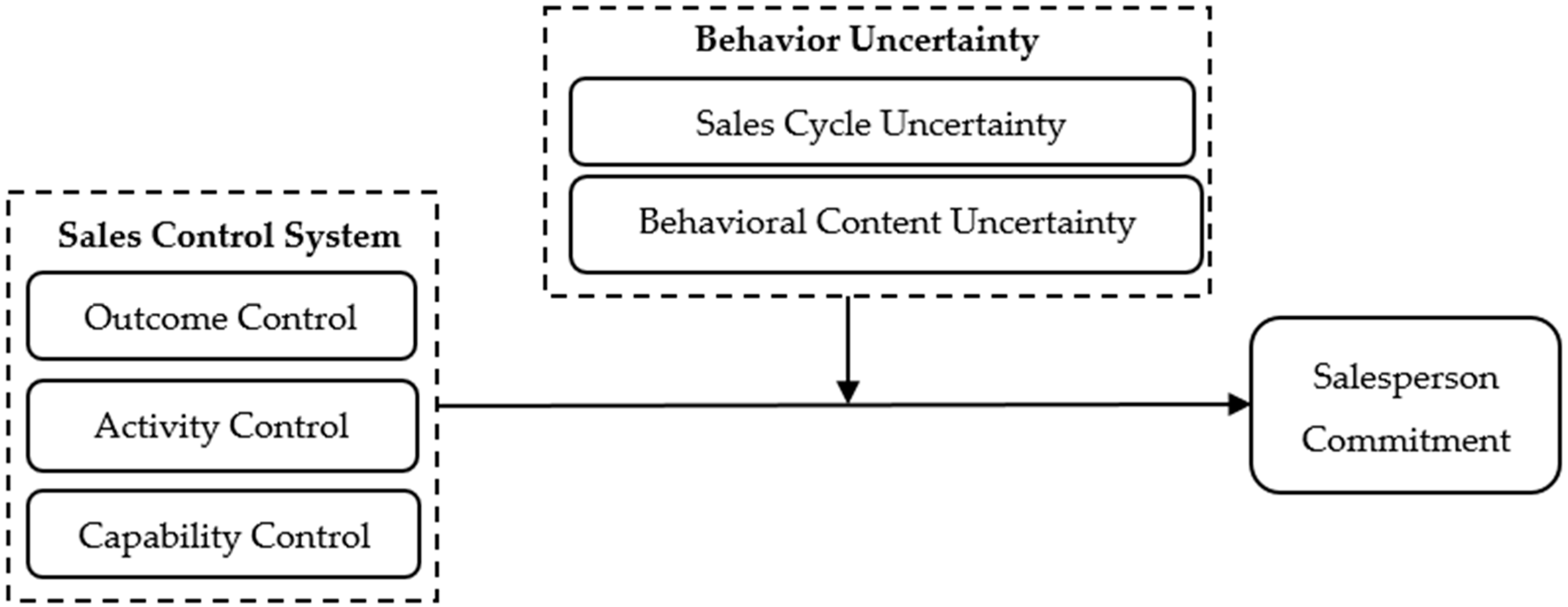

Sales Control Systems and Salesperson Commitment: The Moderating Role of Behavior Uncertainty

Abstract

1. Introduction

2. Conceptual Background

2.1. Sales Control Systems

2.2. Salesperson Commitment

2.3. Behavior Uncertainty

3. Research Hypotheses

3.1. Main Effect of Outcome Control

3.2. Main Effect of Activity Control

3.3. Main Effect of Capability Control

3.4. Contextual Effect of Behavioral Uncertainty—Sales Cycle Uncertainty

3.5. Contextual Effect of Behavioral Uncertainty—Behavioral Content Uncertainty

4. Empirical Analysis

4.1. Sample and Data Collection

4.2. Measurement

4.3. Results

4.3.1. Reliability and Validity Test

4.3.2. Common Method Variance

4.3.3. Hypotheses Test

Main Effects

Moderating Effects of Sales Cycle Uncertainty

5. Discussion and Conclusions

5.1. Main Findings

5.2. Theoretical Contributions

5.3. Managerial Contributions

5.4. Limitations and Future Research

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variables | α | AVE | CR | Factor Loading |

|---|---|---|---|---|

| Outcome Control | ||||

| 1. Specific goals and profit goals are established for my job. | 0.80 | 0.58 | 0.80 | 0.82 |

| 2. My pay increases would suffer if sales volume or market share targets are not met. | 0.73 | |||

| 3. I would get bonuses if I exceed my sales volume or market share targets. | 0.73 | |||

| Activity Control | 0.88 | 0.71 | 0.88 | |

| 1. My manager monitors how I perform the required job activities. | 0.83 | |||

| 2. I would be recognized by my supervisor if s/he were pleased with how well I perform sales activities. | 0.85 | |||

| 3. I would be put on probation if my manager is unhappy with how I perform specified sales activities. | 0.85 | |||

| Capability Control | 0.80 | 0.58 | 0.80 | |

| 1. My manager provides guidance on ways to improve my selling skills and knowledge. | 0.78 | |||

| 2. My manager assists by suggesting why using a particular sales approach may be useful. | 0.79 | |||

| 3. I would be commended if I improved my selling skills. | 0.71 | |||

| Sale Cycle Uncertainty | 0.80 | 0.57 | 0.80 | |

| 1. My sale cycle can be constrained to a specified time period (r). | 0.80 | |||

| 2. The time period for me to complete a sale order is quite uncertain. | 0.70 | |||

| 3. It’s hard for me to complete a sale order within a desired time period. | 0.76 | |||

| Behavioral content Uncertainty | 0.84 | 0.63 | 0.84 | |

| 1. It’s difficult for our manager to evaluate if this salesperson follows the recommended procedures in our firm. | 0.82 | |||

| 2. Our manager evaluates salesperson’s contribution to the organization in a highly subjective process. | 0.78 | |||

| 3. It is difficult for our manager to evaluate whether individual salesperson is doing a good job. | 0.78 | |||

| Salesperson Commitment | 0.82 | 0.60 | 0.82 | |

| 1. I feel a strong sense of belonging to my organization. | 0.80 | |||

| 2. I feel personally attached to my sales organization. | 0.74 | |||

| 3. I would be happy to work at my organization until I retire. | 0.79 | |||

| Overall Model Fit (χ2/df = 1.43, p < 0.001; CFI = 0.97; IFI = 0.97; TLI = 0.96; RMSEA = 0.045) | ||||

References

- Yeo, C.; Hur, C.; Ji, S. The customer orientation of salesperson for performance in Korean market case: A relationship between customer orientation and adaptive selling. Sustainability 2019, 11, 6115. [Google Scholar] [CrossRef]

- Mayberry, R.; Boles, J.S.; Donthu, N. An escalation of commitment perspective on allocation-of-effort decisions in professional selling. J. Acad. Mark. Sci. 2018, 46, 879–894. [Google Scholar] [CrossRef]

- Valenzuela, L.; Torres, E.; Hidalgo, P.; Farías, P. Salesperson CLV orientation’s effect on performance. J. Bus. Res. 2014, 67, 550–557. [Google Scholar] [CrossRef]

- Castro-González, S.; Bande, B.; Fernández-Ferrín, P. Responsible leadership and salespeople’s creativity: The mediating effects of CSR perceptions. Sustainability 2019, 11, 2053. [Google Scholar] [CrossRef]

- Hartmann, N.N.; Rutherford, B.N.; Hamwi, G.A.; Friend, S.B. The effects of mentoring on salesperson commitment. J. Bus. Res. 2013, 66, 2294–2300. [Google Scholar] [CrossRef]

- Angle, H.L.; Perry, J.L. An empirical assessment of organizational commitment and organizational effectiveness. Adm. Sci. Q. 1981, 26, 1–14. [Google Scholar] [CrossRef]

- Grego-Planer, D. The relationship between organizational commitment and organizational citizenship behaviors in the public and private sectors. Sustainability 2019, 11, 6395. [Google Scholar] [CrossRef]

- Wombacher, J.; Felfe, J. The interplay of team and organizational commitment in motivating employees’ interteam conflict handling. Acad. Manag. J. 2017, 60, 1554–1581. [Google Scholar] [CrossRef]

- Evans, K.R.; Landry, T.D.; Li, P.C.; Zou, S. How sales controls affect job-related outcomes: The role of organizational sales-related psychological climate perceptions. J. Acad. Mark. Sci. 2007, 35, 445–459. [Google Scholar] [CrossRef]

- Cravens, D.W.; Lassk, F.G.; Low, G.S.; Marshall, G.W.; Moncrief, W.C. Formal and informal management control combinations in sales organizations: The impact on salesperson consequences. J. Bus. Res. 2004, 57, 241–248. [Google Scholar] [CrossRef]

- Pettijohn, C.; Pettijohn, L.S.; Taylor, A.J.; Keillor, B.D. Are performance appraisals a bureaucratic exercise or can they be used to enhance sales-force satisfaction and commitment? Psychol. Mark. 2001, 18, 337–364. [Google Scholar] [CrossRef]

- Crosno, J.L.; Brown, J.R. A meta-analytic review of the effects of organizational control in marketing exchange relationships. J. Acad. Mark. Sci. 2015, 43, 297–314. [Google Scholar] [CrossRef]

- Kim, S.K.; Tiwana, A. Chicken or egg? Sequential complementarity among salesforce control mechanisms. J. Acad. Mark. Sci. 2016, 44, 316–333. [Google Scholar] [CrossRef]

- Purohit, B. Salesperson performance: Role of perceived overqualification and organization type. Mark. Intell. Plan. 2018, 36, 79–92. [Google Scholar] [CrossRef]

- Jaworski, B.J. Toward a theory of marketing control: Environmental context, control types, and consequences. J. Mark. 1988, 52, 23–39. [Google Scholar] [CrossRef]

- Bonner, J.M. The influence of formal controls on customer interactivity in new product development. Ind. Mark. Manag. 2005, 34, 63–69. [Google Scholar] [CrossRef]

- Kim, S.K.; Jung, Y.S. Regaining control of salesforce. Ind. Mark. Manag. 2018, 73, 84–98. [Google Scholar] [CrossRef]

- Hwan Choi, N.; Dixon, A.L.; Jung, J.M. Dysfunctional behavior among sales representatives: The effect of supervisory trust, participation, and information controls. J. Pers. Sell. Sales Manag. 2004, 24, 181–198. [Google Scholar]

- Lusch, R.F.; Jaworski, B.J. Management controls, role stress, and retail store manager performance. J. Retail. 1991, 67, 397. [Google Scholar]

- Malek, S.L.; Sarin, S.; Jaworski, B.J. Sales management control systems: Review, synthesis, and directions for future exploration. J. Pers. Sell. Sales Manag. 2018, 38, 30–55. [Google Scholar] [CrossRef]

- Challagalla, G.N.; Shervani, T.A. Dimensions and types of supervisory control: Effects on salesperson performance and satisfaction. J. Mark. 1996, 60, 89–105. [Google Scholar] [CrossRef]

- Rindfleisch, A.; Heide, J.B. Transaction cost analysis: Past, present, and future applications. J. Mark. 1997, 61, 30–54. [Google Scholar] [CrossRef]

- Cogin, J.A.; Williamson, I.O. Standardize or customize: The interactive effects of HRM and environment uncertainty on MNC subsidiary performance. Hum. Resour. Manag. 2014, 53, 701–721. [Google Scholar] [CrossRef]

- Verano-Tacoronte, D.; Melián-González, S. Human resources control systems and performance: The role of uncertainty and risk propensity. Int. J. Manpower. 2008, 29, 161–187. [Google Scholar] [CrossRef]

- Challagalla, G.; Shervani, T.; Huber, G. Supervisory orientations and salesperson work outcomes: The moderating effect of salesperson location. J. Pers. Sell. Sales Manag. 2000, 20, 161–171. [Google Scholar]

- Anderson, E. The salesperson as outside agent or employee: A transaction cost analysis. Mark. Sci. 2008, 27, 70–84. [Google Scholar] [CrossRef]

- Williamson, O.; Williamson, O.; Ghani, T.; Ghani, T. Transaction cost economics and its uses in marketing. J. Acad. Mark. Sci. 2012, 40, 74–85. [Google Scholar] [CrossRef]

- Plenborg, T. The operating cycle and the information content of earnings and cash flow. Scand. J. Manag. 1998, 14, 273–287. [Google Scholar] [CrossRef]

- Anderson, E.; Oliver, R.L. Perspectives on behavior-based versus outcome-based salesforce control systems. J. Mark. 1987, 51, 76–88. [Google Scholar] [CrossRef]

- Agarwal, S.; Ramaswami, S.N. Marketing controls and employee responses: The moderating role of task characteristics. J. Acad. Mark. Sci. 1993, 21, 293–306. [Google Scholar] [CrossRef]

- de Oliveira Santini, F.; Vieira, V.A.; Ladeira, W.J.; Sampaio, C.H. Behaviour-based and outcome-based control systems: A meta-analytic Study. Can. J. Adm. Sci. 2019, 36, 149–162. [Google Scholar] [CrossRef]

- Lewis, M.W.; Welsh, M.A.; Dehler, G.E.; Green, S.G. Product development tensions: Exploring contrasting styles of project management. Acad. Manag. J. 2002, 45, 546–564. [Google Scholar]

- Mowday, R.T.; Steers, R.M.; Porter, L.W. The measure of organizational commitment. J. Vocat. Behav. 1979, 14, 224–247. [Google Scholar] [CrossRef]

- Allen, N.J.; Meyer, J.P. The measurement and antecedents of affective, continuance and normative commitment to the organization. J. Occup. Organ. Psychol. 1990, 63, 1–18. [Google Scholar] [CrossRef]

- Meyer, J.P.; Alien, N.J. A three-component conceptualization of organizational commitment. Hum. Resour. Manag. Rev. 1991, 1, 61–89. [Google Scholar] [CrossRef]

- Boles, J.; Madupalli, R.; Rutherford, B.; Wood, J.A. The relationship of facets of salesperson job satisfaction with affective organizational commitment. J. Bus. Ind. Mark. 2007, 22, 311–321. [Google Scholar] [CrossRef]

- Whitener, E.M. Do “high commitment” human resource practices affect employee commitment? A cross-level analysis using hierarchical linear modeling. J. Manag. 2001, 27, 515–535. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A.; Rayton, B. The contribution of corporate social responsibility to organizational commitment. Int. J. Hum. Resour. Manag. 2007, 18, 1701–1719. [Google Scholar] [CrossRef]

- Seifert, M.; Brockner, J.; Bianchi, E.C.; Moon, H. How workplace fairness affects employee commitment. MIT Sloan Manag. Rev. 2016, 57, 14–17. [Google Scholar]

- Noordewier, T.G.; John, G.; Nevin, J.R. Performance outcomes of purchasing arrangements in industrial buyer-vendor relationships. J. Mark. 1990, 54, 80–93. [Google Scholar] [CrossRef]

- Macher, J.T.; Richman, B.D. Transaction cost economics: An assessment of empirical research in the social sciences. Bus. Politics 2008, 10, 1–63. [Google Scholar] [CrossRef]

- Stump, R.L.; Heide, J.B. Controlling supplier opportunism in industrial relationships. J. Mark. Res. 1996, 33, 431–441. [Google Scholar] [CrossRef]

- Chandler, G.N.; McKelvie, A.; Davidsson, P. Asset specificity and behavioral uncertainty as moderators of the sales growth—Employment growth relationship in emerging ventures. J. Bus. Ventur. 2009, 24, 373–387. [Google Scholar] [CrossRef]

- John, G.; Weitz, B.A. Salesforce compensation: An empirical investigation of factors related to use of salary versus incentive compensation. J. Mark. Res. 1989, 26, 1–14. [Google Scholar] [CrossRef]

- John, G.; Weitz, B.A. Forward integration into distribution: An empirical test of transaction cost analysis. J. Law Econ. Organ. 1988, 4, 337–355. [Google Scholar]

- Eisenhardt, K.M. Agency theory: An assessment and review. Acad. Manag. Rev. 1989, 14, 57–74. [Google Scholar] [CrossRef]

- Niesten, E.; Jolink, A. Incentives, opportunism and behavioral uncertainty in electricity industries. J. Bus. Res. 2012, 65, 1031–1039. [Google Scholar] [CrossRef]

- Latham, G.P.; Locke, E.A. Employee motivation. In Handbook of Organizational Behavior; Sage Publications: Newbury Park, CA, USA, 2008. [Google Scholar]

- Joshi, A.W.; Randall, S. The indirect effects of organizational controls on salesperson performance and customer orientation. J. Bus. Res. 2001, 54, 1–9. [Google Scholar] [CrossRef]

- Fang, E.; Evans, K.R.; Landry, T.D. Control systems’ effect on attributional processes and sales outcomes: A cybernetic information-processing perspective. J. Acad. Mark. Sci. 2005, 33, 553–574. [Google Scholar] [CrossRef]

- Wang, G.; Dou, W.; Zhou, N. The interactive effects of sales force controls on salespeople behaviors and customer outcomes. J. Pers. Sell. Sales Manag. 2012, 32, 225–243. [Google Scholar] [CrossRef]

- Miao, C.F.; Evans, K.R. The interactive effects of sales control systems on salesperson performance: A job demands–resources perspective. J. Acad. Mark. Sci. 2013, 41, 73–90. [Google Scholar] [CrossRef]

- Latham, G.P.; Locke, E.A. Self-regulation through goal setting. Organ. Behav. Hum. Des Decis. Proc. 1991, 50, 212–247. [Google Scholar] [CrossRef]

- Avlonitis, G.J.; Panagopoulos, N.G. Exploring the influence of sales management practices on the industrial salesperson: A multi-source hierarchical linear modeling approach. J. Bus. Res. 2007, 60, 765–775. [Google Scholar] [CrossRef]

- Liu, S.; Wang, L. User liaisons’ perspective on behavior and outcome control in IT projects: Role of IT experience, behavior observability, and outcome measurability. Manag. Decis. 2014, 52, 1148–1173. [Google Scholar] [CrossRef]

- Loi, R.; Hang-Yue, N.; Foley, S. Linking employees’ justice perceptions to organizational commitment and intention to leave: The mediating role of perceived organizational support. J. Occup. Organ. Psychol. 2006, 79, 101–120. [Google Scholar] [CrossRef]

- Bennett, R. Guanxi and salesforce management practices in China. Asia. Pac. Bus. Rev. 1999, 5, 73–93. [Google Scholar] [CrossRef]

- Brislin, R.W. Translation and content analysis of oral and written materials. Methodology 1980, 2, 389–444. [Google Scholar]

- Jaworski, B.J.; MacInnis, D.J. Marketing jobs and management controls: Toward a framework. J. Mark. Res. 1989, 26, 406–419. [Google Scholar] [CrossRef]

- Churchill, G.A. A paradigm for developing better measures of marketing constructs. J. Mark. Res. 1979, 16, 64–73. [Google Scholar] [CrossRef]

- Meyer, J.P.; Allen, N.J. Commitment in the Workplace; Sage Publications: Thousand Oaks, CA, USA, 1997. [Google Scholar]

- Im, S.; Chung, Y.W.; Yang, J.Y. Employees’ participation in corporate social responsibility and organizational outcomes: The moderating role of person-CSR fit. Sustainability 2017, 9, 28. [Google Scholar] [CrossRef]

- Netemeyer, R.G.; Brashear-Alejandro, T.; Boles, J.S. A cross-national model of job-related outcomes of work role and family role variables: A retail sales context. J. Acad. Mark. Sci. 2004, 32, 49–60. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 885, 10–37. [Google Scholar] [CrossRef] [PubMed]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; Black, W.C. Multivariate Data Analysis with Readings; Macmillan: New York, NY, USA, 1992. [Google Scholar]

- Aiken, L.S.; West, S.G.; Reno, R.R. Multiple Regression: Testing and Interpreting Interactions; Sage Publications: Newbury Park, CA, USA, 1991. [Google Scholar]

- Miao, C.F.; Evans, K.R. Motivating industrial salesforce with sales control systems: An interactive perspective. J. Bus. Res. 2014, 67, 1233–1242. [Google Scholar] [CrossRef]

- Hofstede, G.; Eckhardt, G. Culture’s Consequences: Comparing Values, Behaviors, Institutions and Organisations across Nations: Book Review; Sage Publications: Newbury Park, CA, USA, 2002. [Google Scholar]

- Rigopoulou, I.; Theodosiou, M.; Katsikea, E.; Perdikis, N. Information control, role perceptions, and work outcomes of boundary-spanning frontline managers. J. Bus. Res. 2012, 65, 626–633. [Google Scholar] [CrossRef]

- McGrath, J.E. Dilemmatics: The study of research choicesand dilemmas. In Judgment calls in research; Martin, J., McGrath, J.E., Kulka, R.A., Eds.; Sage Publications: Newbury Park, CA, USA, 1982. [Google Scholar]

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 Outcome Control (OC) | 0.76 | |||||||||

| 2 Activity Control (AC) | –0.34** | 0.77 | ||||||||

| 3 Capability Control (CC) | 0.19** | –0.26** | 0.75 | |||||||

| 4 Sales Cycle Uncertainty (SCU) | –0.08 | 0.03 | 0.22** | 0.75 | ||||||

| 5 Behavioral Content Uncertainty (BCU) | –0.09 | 0.06 | –0.01 | –0.02 | 0.79 | |||||

| 6 Salesperson Commitment | 0.34** | –0.38** | 0.33** | 0.01 | –0.06 | 0.78 | ||||

| 7 Gender | –0.12† | 0 | –0.01 | –0.02 | –0.04 | –0.20** | -- | |||

| 8 Age | 0.09 | 0.01 | 0.08 | –0.11 | –0.02 | 0.12† | –0.05 | -- | ||

| 9 Education | 0.03 | 0.06 | –0.03 | 0.07 | 0.05 | –0.19** | 0.03 | –0.06 | -- | |

| 10 Working Experience | –0.05 | 0.14† | –0.04 | –0.07 | 0.01 | 0.06 | 0.04 | 0.21** | –0.01 | -- |

| Mean | 3.25 | 3.02 | 3.32 | 3.22 | 3.55 | 3.49 | 0.42 | 2.55 | 2.45 | 2.61 |

| Std. deviation | 0.80 | 1.07 | 0.77 | 1.02 | 0.93 | 0.91 | 0.49 | 1.11 | 0.95 | 0.96 |

| Variables | Dependent Variable: Salesperson Commitment | ||

|---|---|---|---|

| Model 1 | Model 2 | Model 3 | |

| Control Effects | |||

| Gender | –0.19** | –0.17** | –0.12* |

| Age | 0.09 | 0.05 | 0.09 |

| Education | –0.18** | –0.17** | –0.13* |

| Working Experience | 0.04 | 0.10† | 0.06 |

| Simple Effects | |||

| OC | 0.20** | 0.14* | |

| AC | –0.26** | –0.14* | |

| CC | 0.22** | 0.16** | |

| Moderating Effects | |||

| SCU | 0.04 | ||

| OC x SCU | –0.12* | ||

| AC x SCU | 0.14* | ||

| CC x SCU | 0.17** | ||

| BCU | 0.05 | ||

| OC x BCU | 0.20** | ||

| AC x BCU | –0.17** | ||

| CC x BCU | 0.13* | ||

| Adjusted R2 | 0.07 | 0.29 | 0.44 |

| ΔR2 | 0.22 | 0.15 | |

| F | 4.74** | 13.04** | 11.95** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, M.; Peng, L.; Zhuang, G. Sales Control Systems and Salesperson Commitment: The Moderating Role of Behavior Uncertainty. Sustainability 2020, 12, 2589. https://doi.org/10.3390/su12072589

Li M, Peng L, Zhuang G. Sales Control Systems and Salesperson Commitment: The Moderating Role of Behavior Uncertainty. Sustainability. 2020; 12(7):2589. https://doi.org/10.3390/su12072589

Chicago/Turabian StyleLi, Miao, Luluo Peng, and Guijun Zhuang. 2020. "Sales Control Systems and Salesperson Commitment: The Moderating Role of Behavior Uncertainty" Sustainability 12, no. 7: 2589. https://doi.org/10.3390/su12072589

APA StyleLi, M., Peng, L., & Zhuang, G. (2020). Sales Control Systems and Salesperson Commitment: The Moderating Role of Behavior Uncertainty. Sustainability, 12(7), 2589. https://doi.org/10.3390/su12072589