Social Responsibility, Communication and Financial Data of Hospitals: A Structural Modelling Approach in a Sustainability Scope

Abstract

1. Introduction

2. Literature Review and Conceptual Model

2.1. Stakeholders and Dynamic Capabilities Theories

2.2. Theoretical Framework

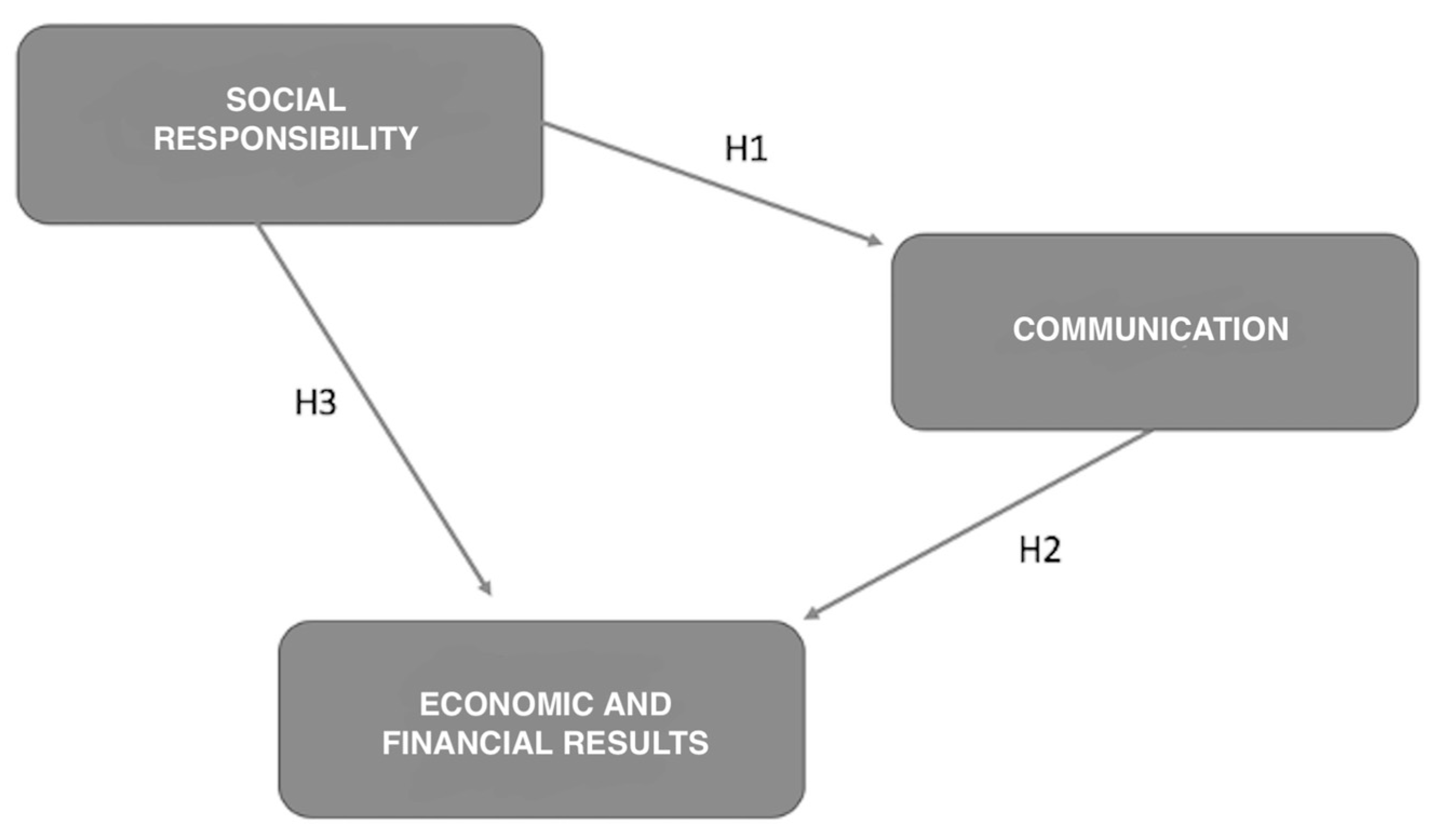

3. Development and Justification of Hypothesis

3.1. The Effect of Social Responsibility on Business Communication

3.2. The Effect of Business Communication on Economic and Financial Results

3.3. The Effect of Social Responsibility on Economic and Financial Results

4. Materials and Methods

4.1. Structural Equations Models

4.2. Population and Sample Selection

4.3. Creation and Measurement of Variables

5. Results

5.1. Global Model Fit Assessment

5.2. Measurement Model Evaluation

5.3. Structural Model Evaluation

5.4. Simple Mediation Analysis

6. Discussion

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Hossain, M.S.; Yahya, S.B.; Rahman, S.; Sobhani, F.A.; Rahman, R. Corporate Social Responsibility in Healthcare: A case of Islamic Banks (IBs) in Bangladesh. Bangladesh J. Med. Sci. 2019, 18, 567–573. [Google Scholar] [CrossRef]

- Desai, P.S.; Chandawarkar, M.R. Aligning CSR activities of health care sector to developmental needs of India. J. Pharm. Sci. Res. 2016, 8, 1008. [Google Scholar]

- Institute for Health Development and Integration. Sanidad Privada, Aportando Valor. Análisis de Situación; IDIS: Madrid, Spain, 2018. [Google Scholar]

- Martín, J.J. El sistema nacional de salud español ante la gran recesión. Cuad. Relac. Labor. 2016, 34, 315–334. [Google Scholar]

- Martínez, A.; Smith, K.; Llop-Gironés, A.; Vergara, M.; Benach, J. La mercantilización de la sanidad: El caso de Catalunya. Cuad. Relac. Labor. 2016, 34, 335–355. [Google Scholar]

- San-Jose, L.; Retolaza, J.L.; Bernal, R. Índice de valor social añadido: Una propuesta para analizar la eficiencia hospitalaria. Gac. Sanit. 2019, in press. [Google Scholar] [CrossRef] [PubMed]

- Sánchez, J.P.; Yañez-Araque, B.; Moreno-García, J. Moderating effect of firm size on the influence of corporate social responsibility in the economic performance of micro-small-and medium-sized enterprises. Technol. Forecast. Soc. Chang. 2020, 151, 119774. [Google Scholar] [CrossRef]

- Jamali, D.; Hallal, M.; Abdallah, H. Corporate governance and corporate social responsibility: Evidence from the healthcare sector. Corp. Gov. 2010, 10, 590–602. [Google Scholar] [CrossRef]

- Limbu, Y.B.; Long, P.; Manveer, M. Corporate social responsibility and hospital brand advocacy. Int. J. Pharm. Healthc. Mark. 2019, 14, 159–174. [Google Scholar] [CrossRef]

- Lubis, A.N. Corporate social responsibility in health sector: A case study in the government hospitals in Medan, Indonesia. Bus. Theor. Pract. 2018, 19, 25–36. [Google Scholar] [CrossRef]

- Takahashi, T.; Ellen, M.; Brown, A. Corporate social responsibility and hospitals: US theory, Japanese experiences, and lessons for other countries. Healthc. Manag. For. 2013, 26, 176–183. [Google Scholar] [CrossRef]

- Hansen, S.D.; Dunford, B.B.; Boss, A.D.; Boss, R.W.; Angermeier, I. Corporate social responsibility and the benefits of employee trust: A cross-disciplinary perspective. J. Bus. Ethics 2011, 102, 29–45. [Google Scholar] [CrossRef]

- Navarro, I.M.; Mira, J.J.; Lorenzo, S. Desarrollo y validación de un cuestionario para medir la reputación de los hospitales. Gac. Sanit. 2012, 26, 444–449. [Google Scholar] [CrossRef] [PubMed]

- Eiras, C.E.; Rubio, V.O. Incentivos financieros en la mejora de la calidad asistencial. Informe SESPAS 2012. Gac. Sanit. 2012, 26, 102–106. [Google Scholar] [CrossRef] [PubMed]

- Retolaza, J.L.; San-Jose, L.; Ruíz-Roqueñi, M. Social Accounting for Sustainability: Monetizing the Social Value; Springer: Cham, Switzerland, 2016. [Google Scholar]

- Freeman, R.E. A Stakeholder Theory of the Modern Corporation; Pincus, L.B., Ed.; Perspectives in Business, Ethics; McGraw-Hill: Singapore, 1998; pp. 171–181. [Google Scholar]

- Kiessling, T.; Isaksson, L.; Yasar, B. Market orientation and CSR: Performance implications. J. Bus. Ethics 2016, 137, 269–284. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J. Consecuencias de las prácticas de sostenibilidad en el coste de capital y en la reputación corporativa. Span. Account. Rev. 2014, 17, 153–162. [Google Scholar] [CrossRef][Green Version]

- Asher, C.; Mahoney, J.M.; Mahoney, J.T. Towards a property rights foundation for a stakeholder theory of the firm. J. Manag. Gov. 2005, 9, 5–32. [Google Scholar] [CrossRef]

- Fassin, Y.; de Colle, S.; Freeman, R.E. Intra-stakeholder alliances in plant-closing decisions: A stakeholder theory approach. Bus. Ethics Eur. Rev. 2016, 26, 97–111. [Google Scholar] [CrossRef]

- Walsh, J. Taking stock of stakeholder management. Acad. Manag. Rev. 2005, 30, 426–452. [Google Scholar] [CrossRef]

- Freeman, R.; Philips, R. Stakeholder theory: A libertarian defense. Bus. Ethics Q. 2002, 12, 331–349. [Google Scholar] [CrossRef]

- Martínez-Martínez, D.; Herrera Madueño, J.; Larrán Jorge, M.; Lechuga Sancho, M.P. The strategic nature of corporate social responsibility in SMEs: A multiple mediator analysis. Ind. Manag. Data Syst. 2017, 117, 2–31. [Google Scholar] [CrossRef]

- Richter, U.H.; Dow, K.E. Stakeholder theory: A deliberative perspective. Bus. Ethics Eur. Rev. 2017, 26, 428–442. [Google Scholar] [CrossRef]

- Rauf, F.; Voinea, C.L.; Azam, H.B.; Fratostiteanu, C. Moderating effect of polítical embeddedness on the relationship between resources base and quality of CSR diclosure in China. Sustainability 2020, 12, 3323. [Google Scholar] [CrossRef]

- Fernandez-Feijoo, B.; Romero, S.; Ruiz, S. Effect of stakeholders’ pressure on transparency of sustainability reports within the GRI framework. J. Bus. Ethics 2014, 122, 53–63. [Google Scholar] [CrossRef]

- Chiarini, A.; Opoku, A.; Vagnoni, E. Public healthcare practices and criteria for a sustainable procurement: A comparative study between UK and Italy. J. Clean. Prod. 2017, 162, 391–399. [Google Scholar] [CrossRef]

- Gonçalves, T.; Gaio, C.; Costa, E. Committed vs oportunistic corporate and social responsibility reporting. J. Bus. Res. 2020, in press. [Google Scholar]

- Pérez, A. Corporate reputation and CSR reporting to stakeholders: Gaps in the literature and future lines of research. Corp. Commun. Int. J. 2015, 20, 11–29. [Google Scholar] [CrossRef]

- Goergen, M.; Chahine, S.; Wood, G.; Brewster, C. Public listing, context and CSR: The effects of legal origin. J. Comp. Int. Manag. 2016, 19, 47–73. [Google Scholar]

- Becchetti, L.; Ciciretti, R.; Hasan, I.; Kobeissi, N. Corporate social responsibility and sharaholder’s value. J. Bus. Res. 2012, 65, 1628–1635. [Google Scholar] [CrossRef]

- Roca, L.C.; Searcy, C. An analysis of indicators disclosed in corporate sustainability reports. J. Clean. Prod 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Kachouie, R.; Mavondo, F.; Sands, S. Dynamic marketing capabilities view on creating market change. Eur. J. Mark. 2018, 52, 1007–1036. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef]

- Sarkar, S.; Coelho, D.M.; Maroco, J. Strategic orientations, dynamic capabilities, and firm performance: An analysis for knowledge intensive business services. J. Knowl. Econ. 2016, 7, 1000–1020. [Google Scholar] [CrossRef]

- Bitencourt, C.C.; Santini, F.D.; Ladeira, W.; Santos, A.C.; Teixeira, E.K. The extended dynamic capabilities model: A meta-analysis. Eur. Manag. J. 2020, 38, 108–120. [Google Scholar] [CrossRef]

- Galbreath, J. Building corporate social responsibility into strategy. Eur. Bus. Rev. 2009, 21, 109–127. [Google Scholar] [CrossRef]

- Ramachandran, V. Strategic corporate social responsibility: A ‘dynamic capabilities’ perspective. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 285–293. [Google Scholar] [CrossRef]

- Bernal-Conesa, J.A.; De Nieves-Nieto, C.; Briones-Penalver, A.J. CSR and technology companies: A study on its implementation, integration and effects on the competitiveness of companies. Int. Cap. 2016, 12, 1529–1590. [Google Scholar] [CrossRef]

- Sánchez, B.G.; Sampedro, E.L.; Conde, J.G. La evaluación del rendimiento en los hospitales públicos españoles: Una primera aproximación. Rev. Iberoam. Contab. Gestión 2009, 14, 1–11. [Google Scholar]

- Bem, A.; Predkiewicz, K.; Predkiewicz, P.; Ucieklak-Jez, P. Determinants of Hospital’s Financial Liquidity. Proc. Econ. Financ. 2014, 12, 27–36. [Google Scholar] [CrossRef]

- Benton, W. A Profitability Evaluation of America’s Best Hospitals, 2000–2008. Decis. Sci. 2013, 44, 1139–1153. [Google Scholar] [CrossRef]

- Retolaza, J.L.; San-Jose, L.; Ruiz-Roqueñi, M. Monetarizing the social value: Theory and evidence. CIRIEC 2015, 83, 43–62. [Google Scholar]

- Calvo, M.A. Herramientas para la participación ciudadana virtual y su desarrollo en las webs del Sistema Sanitario Público de Andalucía. Rev. Española Doc. Científica 2016, 39, 1–17. [Google Scholar] [CrossRef][Green Version]

- Moreira, R.; Faria, P.; Alexandre, I.; Alturas, B. Qualidade dos sítios Web da Administraçao Pública Portuguesa. Rev. Ibérica Sist. Tecnol. Inf. 2016, 20, 78–98. [Google Scholar]

- Cerci, U.O. Social media use of hospitals in terms of communication and public relations. Turkish Online J. Des. Art Commun. 2017, 7, 192–202. [Google Scholar] [CrossRef]

- Manzano, J.A.; Simó, L.A.; Pérez, R.C. La responsabilidad social como creadora de valor de marca: El efecto moderador de la atribución de objetivos. Rev. Dir. Econ. Empresa 2013, 22, 21–28. [Google Scholar]

- Calvo, M.A. Calidad y características de los sitios web de los hospitales españoles de gran tamaño. Rev. Española Doc. Científica 2014, 37, e032. [Google Scholar] [CrossRef]

- García Lacalle, J.; Pina, V.; Royo, S. The unpromising quality and evolution of Spanish public hospital web sites. Online Inf. Rev. 2011, 35, 86–112. [Google Scholar] [CrossRef]

- AECA. Información Integrada: El Cuadro Integrado de Indicadores (CII-FESG) y su Taxonomía XBRL.; Asociación Española de Contabilidad y Administración de Empresas: Madrid, Spain, 2018. [Google Scholar]

- Nevado-Gil, M.T.; Gallardo-Vázquez, D. Información sobre Responsabilidad Social contenida en las páginas webs de los ayuntamientos. Estudio en la región del Alentejo. Rev. Española Doc. Científica 2016, 39, e150. [Google Scholar] [CrossRef]

- Russo, F. What is the CSR’s Focus in Healthcare? J. Bus. Ethics 2016, 134, 323–334. [Google Scholar] [CrossRef]

- Hinze, A.K.; Sump, F. Corporate social responsibility and financial analysts: A review of the literature. Sustain. Account. Manag. Policy J. 2019, 10, 183–207. [Google Scholar] [CrossRef]

- De Villiers, C.; Marques, A. Corporate social responsibility country-level predispositions, and the consequences of choosing a level of disclosures. Account. Bus. Res. 2016, 46, 167–195. [Google Scholar] [CrossRef]

- Servera-Francés, D.; Piqueras-Tomás, L. The effects of corporate social responsibility on consumer loyalty through consumer perceived value. Econ. Res. 2019, 32, 66–84. [Google Scholar]

- García, J.L.S.; Sanz, J.M.D. Climate change, ethics and sustainability: An innovative approach. J. Innov. Knowl. 2018, 3, 70–75. [Google Scholar] [CrossRef]

- Sapena, J.; Almenar, V.; Apetrei, A.; Escrivá, M.; Gil, M. Some reflections on poverty eradication, true development and sustainability within CST. J. Innov. Knowl. 2018, 3, 90–92. [Google Scholar] [CrossRef]

- Khalaf, A.M.; Alsharqi, O.Z.; Al-Borie, H.M.; Ashoor, M.M.; Al-Orige, A.S. Corporate Social Responsibility and Brand Image: An Empirical Investigation of Private Sector Hospitals in Saudi Arabia. Int. Bus. Res. 2016, 9, 91. [Google Scholar]

- Jarousse, L.A. Environmental sustainability programs for hospitals. Trustee 2012, 65, 22. [Google Scholar]

- Weisz, U.; Haas, W.; Pelikan, J.M.; Schmied, H. Sustainable hospitals: A socio-ecological approach. GAIA Ecol. Perspect. Sci. Soc. 2011, 20, 191–198. [Google Scholar] [CrossRef]

- Gillet-Monjarret, C. Assurance reports included in the CSR reports of French firms: A longitudinal study. Sustain. Account. Manag. Policy J. 2018, 9, 570–594. [Google Scholar] [CrossRef]

- Rivera-Arrubla, Y.A.; Zorio-Grima, A.; García-Benau, M.A. El concepto de informe integrado como innovación en reporting corporativo. J. Innov. Knowl. 2016, 1, 144–155. [Google Scholar] [CrossRef]

- Vitolla, F.; Raimo, N.; Rubino, M. Appreciations, criticisms, determinants, and effects of integrated reporting: A systematic literature review. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 518–528. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Martínez-Ferrero, J.; Garcia-Benau, M.A. Integrated reporting: The mediating role of the board of directors and investor protection on managerial discretion in munificent environments. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 29–45. [Google Scholar] [CrossRef]

- Leela, V. Corporate social responsibility in hospitals: Need for transparent CSR initiatives for internal and external stakeholders. Int. J. Bus. Ethics Dev. Econ. 2014, 3, 1–11. [Google Scholar]

- Conesa, J.A.; De Nieves, C.; Briones, A.J. Aplicación de un modelo de ecuaciones estructurales para analizar los sistemas de gestión en la integración de la RSC y su influencia en la estrategia y el performance de las empresas tecnológicas. Rev. Met. Cuant. Econ. Emp. 2016, 21, 77–102. [Google Scholar]

- Bradley, O.J.; Botchway, G.O. Communicating corporate social responsibility (CSR) in the coffee industry: An examination of indicators disclosed. Sustain. Account. Manag. Policy J. 2018, 9, 139–164. [Google Scholar] [CrossRef]

- Langstaff, K.; Brzozowski, V. Managing environmental sustainability in a healthcare setting. Healthc. Manag. For. 2017, 30, 84–88. [Google Scholar] [CrossRef] [PubMed]

- Gómez, L.M.; Chalmeta, R. Corporate Responsibility in US corporate websites: A pilot study. Public Relat. Rev. 2011, 3, 93–95. [Google Scholar] [CrossRef]

- Tang, L.; Li, H. Corporate social responsibility communication of Chinese and global corporations in China. Public Relat. Rev. 2009, 35, 199–212. [Google Scholar] [CrossRef]

- Bai, X.; Chang, J. Corporate social responsibility and firm performance: The mediating role of marketing competence and the moderating role of market environment. Asia Pac. J. Manag. 2015, 32, 505–530. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. An overview of sustainability assessment methodologies. Ecol. Indic. 2011, 15, 281–289. [Google Scholar] [CrossRef]

- Gómez, L.M. Me gusta o te sigo: Análisis de la comunicación de prácticas de Responsabilidad Social Corporativa a través de los medios sociales. Corresp. Análisis 2013, 3, 89–109. [Google Scholar] [CrossRef]

- Morales, F.; Jarne, J. E-gobierno corporativo: Evidencia en Chile sobre la divulgación de información en internet. Capic Rev. 2009, 7, 45–62. [Google Scholar]

- Marston, C. Financial reporting on the Internet by leading Japanese companies. Corp. Commun. 2003, 8, 23–34. [Google Scholar] [CrossRef]

- Lee, M. Financial Analysis of National University Hospitals in Korea. Osong Public Health Res. Perspect. 2015, 6, 310–317. [Google Scholar] [CrossRef] [PubMed]

- Akmese, H.; Cetin, H.; Akmese, K. Corporate social responsibility reporting: A comparative analysis of tourism and finance sectors of G8 countries. Proc. Econ. Fin. 2016, 39, 737–745. [Google Scholar] [CrossRef][Green Version]

- Du, S.; Bhattacharya, C.B.; Sen, S. Maximizing business returns to corporate social responsibility (CSR): The role of CSR communication. Int. J. Manag. Rev. 2010, 12, 8–19. [Google Scholar] [CrossRef]

- Cohen, J.R.; Holder-Webb, L.L.; Nath, L.; Wood, D. Corporate reporting of nonfinancial leading indicators of economic performance and sustainability. Account. Horiz. 2012, 26, 65–90. [Google Scholar] [CrossRef]

- Morros, J. The integrated reporting: A presentation of the current state of art and aspects of integrated reporting that need further development. Int. Cap. 2016, 12, 336–356. [Google Scholar] [CrossRef]

- Lock, I.; Seele, P. The credibility of CSR (corporate social responsibility) reports in Europe. Evidence from a quantitative content analysis in 11 countries. J. Clean. Prod. 2016, 122, 186–200. [Google Scholar] [CrossRef]

- Akisik, O.; Gal, G. The impact of corporate social responsibility and internal controls on stakeholders’ view of the firm and financial performance. Sustain. Account. Manag. Policy J. 2017, 8, 246–280. [Google Scholar] [CrossRef]

- Wang, D.H.; Chen, P.H.; Yu, T.H.; Hsiao, C.Y. The effects of corporate social responsibility on brand equity and firm performance. J. Bus. Res. 2015, 68, 2232–2236. [Google Scholar] [CrossRef]

- Lo, S.F. Performance evaluation for sustainable business: A profitability and marketability framework. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 311–319. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar] [CrossRef]

- Tang, Z.; Hull, C.E.; Rothenberg, S. How corporate social responsibility engagement strategy moderates the CSR-financial performance relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Chen, L.; Feldmann, A.; Tang, O. The relationship between disclosures of corporate social performance and financial performance: Evidences from GRI reports in manufacturing industry. Int. J. Prod. Econ. 2015, 170, 445–456. [Google Scholar] [CrossRef]

- Braam, G.J.; De Weerd, L.U.; Hauck, M.; Huijbregts, M.A. Determinants of corporate environmental reporting: The importance of environmental performance and assurance. J. Clean. Prod. 2016, 129, 724–734. [Google Scholar] [CrossRef]

- Mion, G.; Loza Adaui, C.R. Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies. Sustainability 2019, 11, 4612. [Google Scholar] [CrossRef]

- Fernández-Guadaño, J.; Sarria-Pedroza, J.H. Impact of corporate social responsibility on value creation from a stakeholder perspective. Sustainability 2018, 10, 2062. [Google Scholar] [CrossRef]

- Loprevite, S.; Ricca, B.; Rupo, D. Performance sustainability and integrated reporting: Empirical evidence from mandatory and voluntary adoption contexts. Sustainability 2018, 10, 1351. [Google Scholar] [CrossRef]

- Sierra-Garcia, L.; Garcia-Benau, M.A.; Bollas-Araya, H.M. Empirical analysis of non-financial reporting by Spanish companies. Admin. Sci. 2018, 8, 29. [Google Scholar] [CrossRef]

- Gallego-Álvarez, I.; Lozano, M.B.; Rodríguez-Rosa, M. Analysis of Social Sustainability Information in a Global Context According to the New Global Reporting Initiative 400 Social Standards. Sustainability 2019, 11, 7073. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. In Managing Sustainable Bbusiness; Springer: Dordrecht, The Netherlands, 2019; pp. 323–346. [Google Scholar]

- Ringle, C.M.; Wende, S.; Will, A. Smart PLS 3.0 (beta). EEUU. 2005. Available online: http://www.smartpls.de (accessed on 1 May 2019).

- Roldán, J.L.; Sánchez-Franco, M.J. Variance-Based Structural Equation Modeling: Guidelines for using Partial Least Squares in Information Systems Research. In Research Methodologies, Innovations and Philosophies in Software Systems Engineering and Information Systems, Information Science Reference; Mora, M., Gelman, O., Steenkamp, A., Raisinghani, M.S., Eds.; IGI Global: Hershey, NY, USA, 2012; pp. 193–221. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences; Hillsdale: Erlbaum, NJ, USA, 1988. [Google Scholar]

- Barroso, M.J. Procesos de Asociación Entre Empresas y ONGD. Un Modelo de eExito Desde la Perspectiva del Marketing de Relaciones; Universidad de Extremadura: Badajoz, Spain, 2015. [Google Scholar]

- Sánchez, D.; Subiela, B.J. La comunicación de la responsabilidad social corporativa en las organizaciones españolas con mejor reputación. Sphera Public 2016, 2, 39–53. [Google Scholar]

- Creixans-Tenas, J. Las Empresas Hospitalarias Españolas en el Contexto Europeo: Análisis de Los Estados Financieros, Comunicación y Responsabilidad Social; Universitat de Vic-UCC: Barcelona, Spain, 2018. [Google Scholar]

- Benitez, M.; Faba-Perez, C. Presence of social networks in the health sector: A case-study on the best positioned hospitals in the world. Ibersid 2016, 10, 21–30. [Google Scholar]

- Costa-Sanchez, C.; Túnez-Lopez, M.; Videla-Rodriguez, J.J. Spanish hospitals in the social web. The management of Facebook and Twitter by Hospital Sant Joan de Deu (Barcelona). Rev. Lat. Comun. Soc. 2016, 71, 1108–1130. [Google Scholar]

- Gutiérrez-Ponce, H.; Creixans-Tenas, J.; Arimany-Serrat, N. Características de las páginas web de los hospitales de la Comunidad de Madrid: Relación entre la calidad web y la responsabilidad social corporativa. Rev. Española Doc. Científica 2018, 41, e194. [Google Scholar] [CrossRef]

- Rodríguez, A.; Calle, C.; Zöller, B.; Pons, A.; Benavente, Y.; Durán, N. Responsabilidad social corporativa en los hospitales catalanes: ¿qué nos dicen sus webs? Rev. Comun. Salud 2017, 7, 13–28. [Google Scholar] [CrossRef]

- McGain, F.; Naylor, C. Environmental sustainability in hospitals—A systematic review and research agenda. J. Health Serv. Res. Policy 2014, 19, 245–252. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using PLS path modelling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Henseler, J. Partial Least Squares Path Modeling: Quo Vadis? Qual. Quant. 2018, 52, 1–8. [Google Scholar] [CrossRef]

- Henseler, J.; Dijkstra, T.; Sarstedt, M.; Ringle, C.; Diamantopoulos, A.; Straub, D.; Ketchen, D.J.; Hair, J.; Hult, G.; Calantone, R.J. Common beliefs and reality about PLS: Comments on Rönkkö and Evermann. Organ. Res. Methods 2013, 17, 182–209. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. Testing measurement invariance of composites using partial least squares. Int. Mark. Rev. 2016, 33, 405–431. [Google Scholar] [CrossRef]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a silver bullet. J. Mark. Theory Pract. 2011, 19, 139–152. [Google Scholar] [CrossRef]

- Chin, W.W.; Dibbern, J. An introduction to a permutation-based procedure for multi-group PLS analysis: Results of tests of differences on simulated data and a cross cultural analysis of the sourcing of information system services between Germany and the USA. In Handbook of Partial Least Squares: Concepts, Methods and Applications in Marketing and Related Fields; Esposito, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer: Berlin, Germany, 2010; pp. 171–193. [Google Scholar]

- Vadenberg, R.J.; Lance, C.E. A review and synthesis of the measurement in variance literature: Suggestions, practices, and recommendations for organizational research. Organ. Res. Methods 2000, 3, 4–70. [Google Scholar] [CrossRef]

- Edgington, T.M.; Bentler, P.M. Contemporary Reporting Practices Regarding Covariance-Based SEM with a Lens on EQS. In Research Methodologies, Innovations and Philosophies in Software Systems Engineering and Information Systems; Mora, M., Gelman, O., Steenkamp, A.L., Raisinghani, M., Eds.; Information Science Reference: Hershey, PA, USA, 2012; pp. 166–192. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modelling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Wright, R.T.; Campbell, D.E.; Thatcher, J.B.; Roberts, N. Operationalizing multidimensional constructs in structural equation modeling: Recommendations for IS research. Commun. Assoc. Inf. Syst. 2012, 30, 367–412. [Google Scholar] [CrossRef]

- Hair, J.F.; Risher, J.; Sarstedt, M.; Ringle, C. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modelling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Chin, W.W. How to write up and report PLS analyses. In Handbook of Partial Least Squares: Concepts, Methods and Applications; Esposito, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer: Berlin, Germany, 2010; pp. 655–690. [Google Scholar]

- Falk, R.; Miller, N. A Primer for Soft Modeling; University of Akron Press: Akron, OH, USA, 1992. [Google Scholar]

- Leal-Rodríguez, A.L.; Ariza-Montes, J.A.; Roldán, J.L.; Leal-Millán, A.G. Absorptive capacity, innovation and cultural barriers: A conditional mediation model. J. Bus. Res. 2014, 67, 763–768. [Google Scholar] [CrossRef]

- Preacher, K.J.; Hayes, A.F. Asymptotic and resampling strategies for assessing and comparing indirect effets in multiple mediator models. Behav. Res. Methods 2008, 40, 879–891. [Google Scholar] [CrossRef]

- Roldán, J.L.; Cepeda, G. Seminario Modelos de Ecuaciones Estructurales Basados en la Varianza: Partial Least Squares (PLS) Para Investigadores en Ciencias Sociales, 3rd ed.; Universidad de Sevilla: Sevilla, Spain, 2016. [Google Scholar]

- Williams, J.; MacKinnon, D. Resampling and distribution of the product methods for testing indirect effects in complex models. Struct. Equ. Model. J. 2008, 15, 23–51. [Google Scholar] [CrossRef]

- Nitzl, C.; Roldan, J.L.; Cepeda, G. Mediation analyses in Partial Least Squares path modeling: Helping researchers discuss more sophisticated models. Ind. Manag. Data Syst. 2016, 116, 1849–1864. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; SAGE: New York, NY, USA, 2017. [Google Scholar]

{kind=link}

| Database | SABI |

|---|---|

| Period | 2018 |

| Status | Active companies |

| National activity code | 8610–Hospital activities |

| Type of company | Mercantile companies |

| Business dimension | Large and medium enterprises |

| Typology of annual accounts | Unconsolidated accounts |

| Availability annual accounts | 2018 financial year available |

| Geographic location | Spain |

| Final sample | 122 companies |

| CONSTRUCT | INDICATOR | DESCRIPTION | SOURCE | AUTHORS |

|---|---|---|---|---|

| Social Responsibility (SR) | SR1 | N° of quality accreditations and certifications | Corporate website | [66,99] |

| SR2 | Number of awards received | Corporate website | [66,99] | |

| SR3 | Social responsibility disclosure index | Corporate website | [100] | |

| SR4 | Number of general sustainability aspects | Corporate website | Table 3 | |

| SR5 | Number of social aspects | Corporate website | Table 3 | |

| SR6 | Number of environmental aspects | Corporate website | Table 3 | |

| Communication (C) | C1 | Number of social networks | Corporate website | [101,102] |

| C2 | Web quality | Corporate website | [103] | |

| C3 | Average of monthly visitors on the website | Similar web | [101] | |

| C4 | Number of incoming links in Google search | Google Search | [102] | |

| C5 | Number of incoming links in Yahoo search | Yahoo Search | [102] | |

| C6 | Nº of items in the press in which it appears | MyNews Database | [101] | |

| Economic and financial results (EFR) | EFR1 | Operating income | SABI database | [50,54] |

| EFR2 | Return on assets (ROA) | SABI database | [101] | |

| EFR3 | Return on equity (ROE) | SABI database | [101] | |

| EFR4 | Solvency | SABI database | [76] | |

| EFR5 | Indebtedness | SABI database | [50] | |

| EFR6 | Personnel productivity | SABI database | [50] | |

| EFR7 | Cash flows from operating activities | SABI database | [76] | |

| EFR8 | Cash flows from investment activities | SABI database | [76] |

| SR4: Number of general sustainability aspects | ||

| 1 | It has a director, department or head of SR | [50,104] |

| 2 | SR policy available | |

| 3 | Strategic plan available | |

| 4 | A quality management system is available | |

| 5 | Sustainability reports are compiled | |

| 6 | Sustainability reports have external validation | |

| 7 | It has adopted the United Nations Global Compact | |

| 8 | The identity, mission, vision and values of the hospital are defined | |

| 9 | There is an exclusive section dedicated to sustainability or SR | |

| 10 | Economic, environmental and social aspects are separated | |

| SR5: Number of social aspects | ||

| 1 | Code of ethics available | [50,104] |

| 2 | Equality plan is available | |

| 3 | Concerns about the reconciliation between work and family life | |

| 4 | It cares about diversity management | |

| 5 | Solidarity projects are available | |

| 6 | Corporate volunteer programs are carried out | |

| 7 | Training for employees | |

| 8 | Media are asked to express doubts or suggestions | |

| 9 | Information on medical knowledge is disclosed | |

| 10 | Job creation is encouraged | |

| SR6: Number of environmental aspects | ||

| 1 | Environmental policy is available | [50,104,105] |

| 2 | It participates in activities related to protection of the natural environment | |

| 3 | Energy saving is considered to achieve higher levels of efficiency | |

| 4 | Water saving is considered to achieve higher levels of efficiency | |

| 5 | The reduction of emissions of gases and waste is considered | |

| 6 | The introduction of alternative energy sources is positively valued | |

| 7 | There is a concern to minimize the environmental impact | |

| 8 | Consumables and products with low environmental impact are used | |

| 9 | The use of recyclable containers and packaging is valued | |

| 10 | Data related to environmental improvement are specified | |

| Construct Indicators | Loadings (λ) | Cronbach’s Alpha | Composite Reliability | AVE |

|---|---|---|---|---|

| Social Responsibility | 0.889 | 0.935 | 0.704 | |

| SR1 | 0.742 | |||

| SR3 | 0.767 | |||

| SR4 | 0.851 | |||

| SR5 | 0.925 | |||

| SR6 | 0.964 | |||

| Communication | 0.847 | 0.804 | 0.523 | |

| C1 | 0.766 | |||

| C2 | 0.798 | |||

| C3 | 0.713 | |||

| C4 | 0.742 | |||

| Economic Financial | 0.876 | 0.932 | 0.643 | |

| Results | ||||

| EFR1 | 0.934 | |||

| EFR2 | 0.887 | |||

| EFR4 | 0.932 | |||

| EFR5 | 0.717 | |||

| EFR8 | 0.806 |

| Fornell-Larcker Criterion | HTMT | |||||

|---|---|---|---|---|---|---|

| Constructs | SR | C | EFR | SR | C | EFR |

| SR | 0.723 | |||||

| C | 0.462 | 0.821 | 0.486 | |||

| EFR | 0.632 | 0.415 | 0.833 | 0.588 | 0.432 | |

| Hypotheses | Path Coefficients (β) | T-statistic (Bootstrap) | Explained Variance (%) | Relationship Validation |

|---|---|---|---|---|

| H1: SR → C | 0.201 | 4.437 *** | 7.85% | Validated |

| H2: C → EFR | 0.453 | 7.684 *** | 21.22% | Validated |

| H3: SR → EFR | 0.288 | 3.722 *** | 14.95% | Validated |

| Direct Effects | Coefficient | Bootstrap 90% CI | ||

|---|---|---|---|---|

| Percentile | ||||

| H1: c’ | 0.259sig | 0.022 | 0.474 | |

| a | 0.509sig | 0.365 | 0.670 | |

| b | 0.324sig | 0.217 | 0.459 | |

| Indirect Effect | Point Estimate | Percentile | VAF | |

| H2: a * b | 0.214sig | 0.018 | 0.396 | 0.306 (30.6%) |

| Total Indirect Effect | 0.538sig | |||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Creixans-Tenas, J.; Gallardo-Vázquez, D.; Arimany-Serrat, N. Social Responsibility, Communication and Financial Data of Hospitals: A Structural Modelling Approach in a Sustainability Scope. Sustainability 2020, 12, 4857. https://doi.org/10.3390/su12124857

Creixans-Tenas J, Gallardo-Vázquez D, Arimany-Serrat N. Social Responsibility, Communication and Financial Data of Hospitals: A Structural Modelling Approach in a Sustainability Scope. Sustainability. 2020; 12(12):4857. https://doi.org/10.3390/su12124857

Chicago/Turabian StyleCreixans-Tenas, Judit, Dolores Gallardo-Vázquez, and Núria Arimany-Serrat. 2020. "Social Responsibility, Communication and Financial Data of Hospitals: A Structural Modelling Approach in a Sustainability Scope" Sustainability 12, no. 12: 4857. https://doi.org/10.3390/su12124857

APA StyleCreixans-Tenas, J., Gallardo-Vázquez, D., & Arimany-Serrat, N. (2020). Social Responsibility, Communication and Financial Data of Hospitals: A Structural Modelling Approach in a Sustainability Scope. Sustainability, 12(12), 4857. https://doi.org/10.3390/su12124857