Interest Rate Marketization, Financing Constraints and R&D Investments: Evidence from China

Abstract

:1. Introduction

2. Literature Review and Research Hypothesis

2.1. Financing Constraints and R&D Investment

2.2. Interest Rate Marketization and Financial Constraints

2.3. Ownership Structure

3. Research Design

3.1. Variable Definitions

3.1.1. Dependent Variable—Enterprise R&D Investment

3.1.2. Independent Variable—Cash Flow and Sale

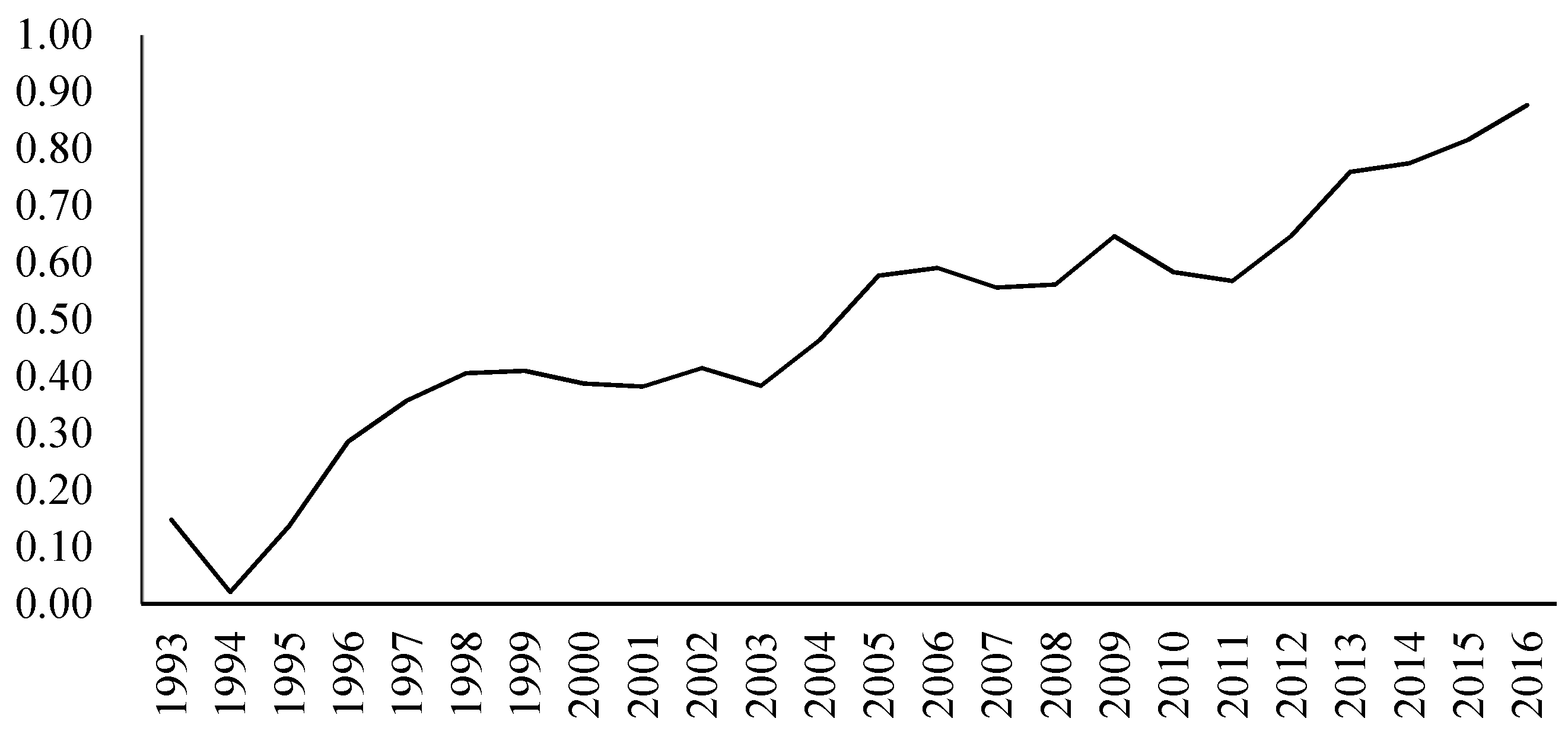

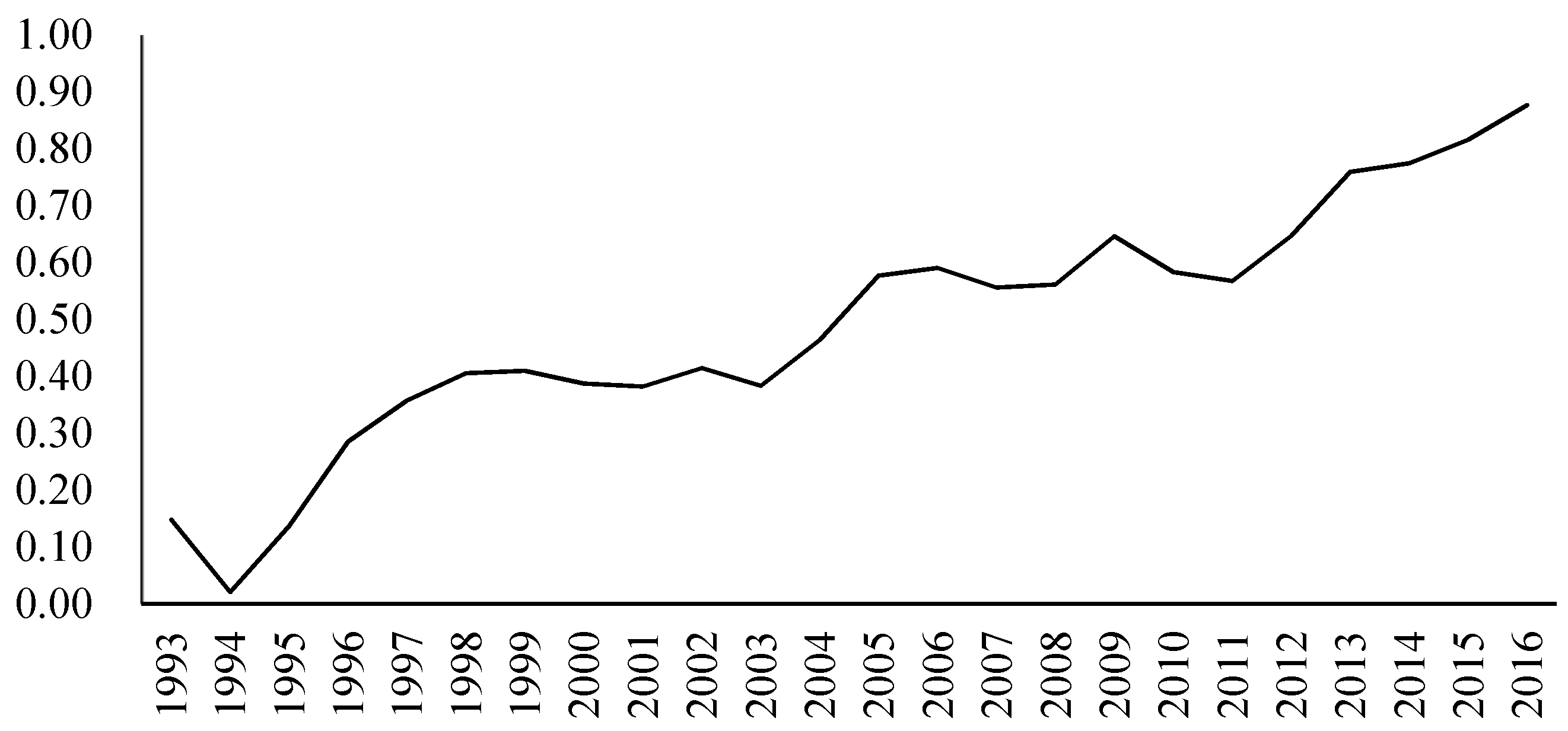

3.1.3. Moderating Variable—Interest Rate Marketization and Soe

3.2. Sample and Data

3.3. Model Establishment

4. Empirical Results

4.1. Descriptive Statistics

4.2. Correlation Analysis

4.3. Regression Result

4.3.1. Regression Results Analysis

4.3.2. Robustness Test

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- McKinnon, R.I. Money and Capital in Economic Development; Brookings Institution Press: Washington, DC, USA, 1973. [Google Scholar]

- Martinez, L.; Tornell, A.; Westermann, F. Globalization, growth and financial crises-Lessons from Mexico and the developing world. Trimest. Econ. 2004, 71, 251–351. [Google Scholar]

- Carlson, J.; Havmöller, R.; Herreros, A.; Platonov, P.; Johansson, R.; Olsson, B. Liberalization, corporate governance and the performance of privatized firms in developing countries. J. Corp. Financ. 2005, 11, 767–790. [Google Scholar]

- Yang, G.; Liu, H. Financial development, interest rate liberalization, and macroeconomic volatility. Emerg. Mark. Financ. Tr. 2016, 52, 1–11. [Google Scholar] [CrossRef]

- Love, I. Financial development and financing constraints: International evidence from the structural investment model. Rev. Financ. Stud. 2003, 16, 765–791. [Google Scholar] [CrossRef]

- Love, I.; Zicchino, L. Financial development and dynamic investment behavior: Evidence from panel VAR. Q. Rev. Eco. Financ. 2006, 46, 190–210. [Google Scholar] [CrossRef]

- Korosteleva, J.; Mickiewicz, T. Start-up financing in the age of globalization. Emerg. Mark. Financ. Tr. 2011, 47, 23–49. [Google Scholar] [CrossRef]

- Habibullah, M.S.; Smith, P.; Azman-Saini, W. Testing liquidity constraints in ten selected Asian countries: An error-correction approach. Appl. Econ. 2006, 38, 2535–2543. [Google Scholar] [CrossRef]

- Guermazi, A. Financial liberalization, credit constraints and collateral: The case of manufacturing industry in Tunisia. Procedia. Econ. Financ. 2014, 13, 82–100. [Google Scholar] [CrossRef]

- Wang, H.J. A stochastic frontier analysis of financing constraints on investment: The case of financial liberalization in Taiwan. J. Bus. Econ. Stat. 2003, 21, 406–419. [Google Scholar] [CrossRef]

- Galindo, A.; Schiantarelli, F.; Weiss, A. Does financial liberalization improve the allocation of investment? micro-evidence from developing countries. J. Dev. Econ. 2007, 83, 562–587. [Google Scholar] [CrossRef]

- Tseng, T.Y. Will both direct financial development and indirect financial development mitigate investment sensitivity to cash flow? The experience of Taiwan. Emerg. Mark. Financ. Tr. 2012, 48, 139–152. [Google Scholar] [CrossRef]

- Iacoviello, M.; Minetti, R. Financial liberalization and the sensitivity of house prices to monetary policy: theory and evidence. Manch. Sch. 2003, 71, 20–34. [Google Scholar] [CrossRef]

- Perotti, E.C. Finance and inequality: Channels and evidence. J. Comp. Econ. 2007, 35, 748–773. [Google Scholar]

- Kabango, G.P.; Paloni, A. Financial liberalization and the industrial response: Concentration and entry in malawi. World. Dev. 2011, 39, 1771–1783. [Google Scholar] [CrossRef]

- Alvarezcuadrado, F.; Japaridze, I. Trickle-down consumption, financial deregulation, inequality, and indebtedness. J. Econ. Behav. Organ. 2016, 5, 163–180. [Google Scholar]

- Kaminsky, G.L.; Schmukler, S.L. Short-run pain, long-run gain: Financial liberalization and stock market cycles. Rev. Financ. 2007, 12, 253–292. [Google Scholar] [CrossRef]

- Giné, X.; Townsend, R.M. Evaluation of financial liberalization: A general equilibrium model with constrained occupation choice. J. Dev. Econ. 2004, 74, 269–307. [Google Scholar] [CrossRef]

- Kikuchi, T.; Vachadze, G. Financial liberalization: Poverty trap or chaos. J. Math. Econ. 2015, 59, 1–9. [Google Scholar] [CrossRef]

- Ferraris, L.; Minetti, R. Foreign banks and the dual effect of financial liberalization. J. Money. Credit. Bank. 2013, 45, 1301–1333. [Google Scholar] [CrossRef]

- Arcand, J.; Berkes, E.; Panizza, U. Too much finance? J. Econ. Growth. 2015, 20, 105–148. [Google Scholar] [CrossRef]

- Tori, D.; Onaran, O. Financialisation, financial development, and investment: Evidence from European non-financial corporations. Soc. Econ. Rev. 2018, 1–43. [Google Scholar]

- Chan, K.S.; Dang, V.Q.T.; Yan, I.K.M. Financial reform and financing constraints: Some evidence from listed Chinese firms. China. Econ. Rev. 2012, 23, 482–497. [Google Scholar] [CrossRef]

- Schumpeter, J.A. The Theory of Economic Development: An Inquiry into Profits, Capital, Credit, Interest, and the Business Cycle; Transaction Publishers: Piscataway, NJ, USA, 1912. [Google Scholar]

- Szopik-Depczyńska, K. Effects of Innovation Activity in Industrial Enterprises in Eastern Poland. Oeconomia Copernicana 2015, 6, 53–65. [Google Scholar]

- Szopik-Depczyńska, K.; Kędzierska-Szczepaniak, A.; Szczepaniak, K.; Cheba, K.; Gajda, W.; Ioppolo, G. Innovation in sustainable development: An investigation of the EU context using 2030 Agenda indicators. Land Use Policy 2018, 79, 251–262. [Google Scholar]

- Ioppolo, G.; Szopik-Depczyńska, K.; Stajniak, M.; Konecka, S. Supply chain and innovation activity in transport related enterprises in Eastern Poland. Log. Forum 2016, 12, 227–236. [Google Scholar]

- Cimoli, M.; Dosi, G. Technological paradigms, patterns of learning and development: An introductory roadmap. J. Evol. Econ. 1995, 5, 243–268. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H. The cost of capital, corporation finance and the theory of investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Greenwald, B.; Stiglitz, J.E.; Weiss, A. Informational imperfections in the capital market and Macroeconomic Fluctuations. Am. Econ. Rev. 1984, 74, 194–199. [Google Scholar]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef]

- Holmstrom, B. Agency costs and innovation. J. Econ. Behav. Org. 1989, 12, 305–327. [Google Scholar] [CrossRef]

- Cincera, M. Financing Constraints, Fixed Capital and R&D Investment Decisions of Belgian Firms; National Bank of Belgium: Brussels, Belgium, 2002. [Google Scholar]

- Arrow, K.J. Economic welfare and the allocation of resources for invention. In Readings in Industrial Economics; Palgrave: London, UK, 1972; pp. 219–236. [Google Scholar]

- Himmelberg, C.P.; Petersen, B.C. R&D and internal finance: A panel study of small firms in high-tech industries. Rev. Econ. Stat. 1994, 76, 38–51. [Google Scholar]

- Schneider, C.; Veugelers, R. On young highly innovative companies: Why they matter and how (not) to policy support them. Ind. Corp. Change. 2010, 19, 969–1007. [Google Scholar] [CrossRef]

- Hall, B.H. Investment and Research and Development at the Firm Level: Does the Source of Financing Matter? National Bureau of Economic Research: Cambridge, MA, USA, 1992. [Google Scholar]

- Görg, H.; Strobl, E.A.; Bougheas, S. Is R&D financially constrained? Theory and evidence from Irish manufacturing. Rev. Ind. Org. 2003, 22, 159–174. [Google Scholar]

- Yang, E.; Ma, G.; Chu, J. The impact of financial constraints on firm R&D investments: Empirical evidence from China. Int. J. Technol. Manag. 2014, 65, 172–188. [Google Scholar]

- Bond, S.; Harhoff, D.; Van Reenen, J. Investment, R & D and Financial Constraints in Britain and Germany (No. W99/05); Institute for Fiscal Studies: London, UK, 1999. [Google Scholar]

- Czarnitzki, D. Research and development in small and medium-sized enterprises: The role of financial constraints and public funding. Scot. J. Polit. Econ. 2010, 53, 335–357. [Google Scholar] [CrossRef]

- Silva, F.; Carreira, C. Do financial constraints threat the innovation process? Evidence from Portuguese firms. Econ. Innov. New Technol. 2012, 21, 701–736. [Google Scholar] [CrossRef]

- Czarnitzki, D.; Hottenrott, H. R&D investment and financing constraints of small and medium-sized firms. Small Bus. Econ. 2011, 36, 65–83. [Google Scholar]

- Brown, J.R.; Martinsson, G.; Petersen, B.C. Do financing constraints matter for R&D? Eur. Econ. Rev. 2012, 56, 1512–1529. [Google Scholar]

- Li, D. Financial constraints, R&D investment, and stock returns. Rev. Financ. Stud. 2011, 24, 2974–3007. [Google Scholar]

- Lin, Z.J.; Liu, S.; Sun, F. The impact of financing constraints and agency costs on corporate R&D investment: Evidence from China. Int. Rev. Financ. 2017, 17, 3–42. [Google Scholar]

- Shaw, E. Financial Deepening in Economic Development; Oxford University Press: Oxford, UK, 1973. [Google Scholar]

- Li, H.; Meng, L.; Wang, Q.; Zhou, L.A. Political connections, financing and firm performance: Evidence from Chinese private firms. J. Dev. Econ. 2008, 87, 283–299. [Google Scholar] [CrossRef]

- Luo, D.; Liming, Z. Private Control, Political Relationship and Financing Constrain of Private Listed Enterprises. J. Financ. Res. 2008, 12, 164–176. (In Chinese) [Google Scholar]

- Tao, X. Research on the Financing Difficulties of Private Enterprises in China’s Gradual Reform. Stat. Decis. 2012, 15, 173–176. (In Chinese) [Google Scholar]

- Zhang, J. Financial Difficulties and Financing Sequences of Private Economy. Econ. Research. J. 2000, 4, 3–10. (In Chinese) [Google Scholar]

- Xu, C.; Xiuli, G. Research on the financing and financial support of Chinese private enterprise. J. Financ. Res. 2004, 9, 86–91. (In Chinese) [Google Scholar]

- Yin, M.; Zhoujie, W.; Dan, L. A New Framework for Interpreting the Mystery of SME Loan Difficulties. J. Financ. Res. 2008, 5, 99–106. (In Chinese) [Google Scholar]

- Qian, Y.; Xu, C. Innovation and bureaucracy under soft and hard budget constraints. Rev. Econ. Study. 1998, 65, 151–164. [Google Scholar] [CrossRef]

- Huang, H.; Xu, C. Soft budget constraint and the optimal choices of research and development projects financing. J. Comp. Econ. 1998, 26, 62–79. [Google Scholar] [CrossRef]

- Cull, R.; Xu, L.C. Institutions, ownership, and finance: The determinants of profit reinvestment among Chinese firms. J. Financ. Econ. 2005, 77, 117–146. [Google Scholar] [CrossRef]

- Chen, S.; Sun, Z.; Tang, S.; Wu, D. Government intervention and investment efficiency: Evidence from China. J. Corp. Financ. 2011, 17, 259–271. [Google Scholar] [CrossRef]

- Aghion, P.; Van Reenen, J.; Zingales, L. Innovation and institutional ownership. Am. Econ. Rev. 2013, 103, 277–304. [Google Scholar] [CrossRef]

- Obstfeld, M. Risk-taking, global diversification, and growth. Am. Econ. Rev. 1994, 84, 1310–1329. [Google Scholar]

- Harris, J.R.; Schiantarelli, F.; Siregar, M.G. The effect of financial liberalization on the capital structure and investment decisions of Indonesian manufacturing establishments. World bank Econ. Rev. 1994, 8, 17–47. [Google Scholar] [CrossRef]

- Gelos, R.G.; Werner, A.M. Financial liberalization, credit constraints, and collateral: Investment in the Mexican manufacturing sector. J. Dev. Econ. 2002, 67, 1–27. [Google Scholar] [CrossRef]

- Koo, J.; Shin, S. Financial liberalization and corporate investments: Evidence from Korean firm data. Asian Econ. 2004, 18, 277–292. [Google Scholar] [CrossRef]

- Laeven, L. Does financial liberalization reduce financing constraints? Financ. Manag. 2003, 32, 5–34. [Google Scholar] [CrossRef]

- Zhang, J.; Zhe, L.; Wenping, Z. Financing Constraints, Financing Channels and Corporate R&D investment. J. World Econ. 2012, 10, 66–90. (In Chinese) [Google Scholar]

- Li, Z.; Xiangang, X.; Xuhui, Y. The financial development, the debt financing constraint and pyramidal structure. Manag. World 2008, 1, 123–135. (In Chinese) [Google Scholar]

- Fazzari, S.M.; Hubbard, R.G.; Petersen, B.C. Financing Constraints and Corporate Investment. Brook. Pap. Econ. Act. 1988, 19, 141–206. [Google Scholar] [CrossRef]

- Carpenter, R.E.; Guariglia, A. Cash flow, investment, and investment opportunities: New tests using UK panel data. J. Bank. Financ. 2008, 32, 1894–1906. [Google Scholar] [CrossRef]

- Cleary, S. The Relationship between Firm Investment and Financial Status. J. Financ. 1999, 54, 673–692. [Google Scholar] [CrossRef]

- Lamont, O.; Polk, C.; Saá-Requejo, J. Financial Constraints and Stock Returns. Rev. Financ. Stud. 2001, 14, 529–554. [Google Scholar] [CrossRef]

- Whited, T.M.; Wu, G. Financial Constraints Risk. Rev. Financ. Stud. 2006, 19, 531–559. [Google Scholar] [CrossRef]

- Hadlock, C.J.; Pierce, J.R. New Evidence on Measuring Financial Constraints: Moving Beyond the KZ Index. Rev. Financ. Stud. 2010, 23, 1909–1940. [Google Scholar] [CrossRef]

- Gilchrist, S.; Himmelberg, C.P. Evidence on the role of cash flow for investment. J. Monetary. Econ. 1995, 36, 541–572. [Google Scholar] [CrossRef]

- Almeida, H.; Campello, M.; Weisbach, M.S. The Cash Flow Sensitivity of Cash. J. Financ. 2004, 59, 1777–1804. [Google Scholar] [CrossRef]

- Sasidharan, S.; Lukose, P.J.; Komera, S. Financing constraints and investments in R&D: Evidence from Indian manufacturing firms. Quart. Rev. Econ. Financ. 2015, 55, 28–39. [Google Scholar]

- Bond, S.R.; Meghir, C. Dynamic Investment models and the Firm’s financial policy. Rev. Econ. Stud. 1994, 61, 197–222. [Google Scholar] [CrossRef]

- Tao, X.; Mingjue, C. Measure and reform implications of china’s interest rate liberalization. J. Zhongnan Univ. Econ. Law 2013, 3, 74–79. (In Chinese) [Google Scholar]

- Wang, S.; Jiangang, P. The studies on the measurement and performance of china’s interest rate liberalization: Empirical analysis based on the bank credit channel. J. Financ. Econ. 2014, 6, 75–84. (In Chinese) [Google Scholar]

- Zhang, Y.; Qingmei, X. Statistical Measurement of China’s Interest Rate Marketization Process. Stat. Decis. 2016, 11, 154–157. (In Chinese) [Google Scholar]

- Kuh, E.; Meyer, J.R. Correlation and regression estimates when the data are ratios. J. Econ. Soc. 1955, 23, 400–416. [Google Scholar] [CrossRef]

- Tobin, J. A general equilibrium approach to monetary theory. J. Money. Credit. Bank. 1969, 1, 15–29. [Google Scholar] [CrossRef]

- Hubbard, R.G. Capital Market Imperfections and Investment. J. Econ. Lit. 1998, 36, 193–225. [Google Scholar]

- Kaplan, S.N.; Zingales, L. Do investment-cash flow sensitivities provide useful measures of financing constraints? Quart. J. Econ. 1997, 112, 169–215. [Google Scholar] [CrossRef]

- Gomes, J.F. Financing investment. Am. Econ. Rev. 2001, 91, 1263–1285. [Google Scholar] [CrossRef]

- Abel, A. Empirical investment equations: An integrative framework. Carn. Roch. Conf. Series 1980, 12, 39–91. [Google Scholar]

- Fazzari, S.M.; Hubbard, R.G.; Petersen, B.C. Investment, financing decisions, and tax policy. Am. Econ. Rev. 1988, 78, 200–205. [Google Scholar]

- Hubbard, G.; Kashyap, A. Internal Net Worth and the Investment Process: An Application to US Agriculture. J. Polit. Econ. 1992, 100, 506–534. [Google Scholar] [CrossRef]

- Solow, R.M. A contribution to the theory of economic growth. Quart. J. Econ. 1956, 70, 65–94. [Google Scholar] [CrossRef]

- Romer, P.M. Increasing returns and long-run growth. J. Polit. Econ. 1986, 94, 1002–1037. [Google Scholar] [CrossRef]

- Nadiri, M.I. Innovations and Technological Spillovers 1993. (No. w4423); National Bureau of Economic Research: Cambridge, MA, USA, 1993. [Google Scholar]

- Engelbrecht, H.J. International R&D spillovers amongst OECD economies. Appl. Econ. Lett. 1997, 4, 315–319. [Google Scholar]

- Hong, Y. On the strategy of innovation-driven economic development. Economist 2013, 1, 5–11. [Google Scholar]

- Li, Y.; Xiaojing, Z. The new normal: The logic and perspective of economic development. Econ. Res. J. 2015, 5, 4–19. [Google Scholar]

{kind=link}

| Primary Index | Secondary Index | Three-Level Index | Four-Level Index | Assignment or Calculation Description | |||

|---|---|---|---|---|---|---|---|

| Name | Weight | Name | Weight | Name | Weight | ||

| Interest rate Marketization (Im) | Rate determination ways (Im1) | 0.3333 | Deposit and loan rate (Im11) | 0.6340 | RMB loan (Im111) | 0.4375 | 0 complete suppression 0–0.25 very weak marketization 0.25–0.50 weak marketization 0.50 semi-marketization 0.50–0.75 strong marketization 1 full marketization |

| RMB deposit (Im112) | 0.4375 | ||||||

| Foreign currency loan (Im113) | 0.0625 | ||||||

| Foreign currency deposit (Im114) | 0.0625 | ||||||

| Money market interest rate (Im12) | 0.1747 | Interbank borrowing (Im121) | 0.7500 | ||||

| Discounted bills (Im122) | 0.2500 | ||||||

| Bond market interest rate (Im13) | 0.1074 | Bond issuance rate (Im131) | 0.6000 | ||||

| Bond repo rate (Im132) | 0.2000 | ||||||

| Current coupon transaction rate (Im133) | 0.2000 | ||||||

| Wealth product yield (Im14) | 0.0839 | Banking (Im141) | 0.5370 | ||||

| Monetary fund (Im142) | 0.2047 | ||||||

| Trust product (Im143) | 0.2583 | ||||||

| Rate fluctuation restriction (Im2) | 0.3333 | Deposit interest rate floating index (Im21) | 0.5000 | Deposit up-floating limit (Dup) | - | Construct Euler exponential function | |

| Deposit down-floating limit (Ddown) | |||||||

| Loan interest rate floating index (Im22) | 0.5000 | Loan up-floating limit (Lup) | - | Construct Euler exponential function | |||

| Loan down-floating limit (Ldown) | |||||||

| Real rate level (Im3) | 0.3333 | RMB one-year deposit benchmark rate (BR) | - | - | - | Use (BR-IR) to obtain the real interest rate, and then use the fuzzy comprehensive evaluation method to construct the membership function and calculate the value between 0 and 1 as the real interest rate index | |

| Inflation rate (IR) | - | - | - | ||||

| Variable Type | Symbols | Name | Definition |

|---|---|---|---|

| Dependent variable | Rd | R&D investment | R&D investment/total beginning assets |

| Independent variable | Cf | Cash flow | Net operating cash flow/total beginning assets |

| Sale | Revenue | Revenue/total beginning assets | |

| Moderating variable | Im | Interest rate marketization | Construct interest rate marketization index |

| Soe | ownership Dummy variable | Non-state-owned, 1; otherwise 0 |

| Variables | Samples | Mean | Median | Std. Dev | Min | Max | C·V |

|---|---|---|---|---|---|---|---|

| Rd (%) | 6172 | 2.890 | 2.277 | 2.596 | 0.000 | 38.46 | 89% |

| Cf (%) | 6172 | 4.823 | 4.597 | 10.750 | −322.400 | 103.000 | 223% |

| Im (%) | 6172 | 72.350 | 75.92 | 10.740 | 55.590 | 87.660 | 15% |

| Sale (%) | 6172 | 75.030 | 62.75 | 58.630 | 3.607 | 2206.000 | 78% |

| Soe | 6172 | 0.693 | 1.000 | 0.461 | 0.000 | 1.000 | 67% |

| Rd | Rdt−1 | Rd2t−1 | Cft−1 | Imt | Salet−1 | Own | |

|---|---|---|---|---|---|---|---|

| Rd | 1 | ||||||

| Rdt−1 | 0.736 *** | 1 | |||||

| Rd2t−1 | 0.497 *** | 0.832 *** | 1 | ||||

| Cft−1 | 0.211 *** | 0.089 *** | 0.056 *** | 1 | |||

| Imt | −0.141 *** | −0.202 *** | −0.139 *** | −0.001 | 1 | ||

| Salet−1 | 0.209 *** | 0.048 *** | 0.002 | 0.023 | −0.193 *** | 1 | |

| Own | 0.254 *** | 0.249 *** | 0.129 *** | 0.017 | −0.098 *** | −0.029 | 1 |

| Total Sample | ||||

|---|---|---|---|---|

| Variables | Model 1 | Model 2 | Model 3 | Model 4 |

| Constant | 0.173 | 0.552 | 0.231 | 1.855 *** |

| (1.43) | (0.84) | (0.33) | (2.63) | |

| Rdi,t−1 | 0.828 *** | 0.828 *** | 0.831 *** | 0.832 *** |

| (26.69) | (26.69) | (26.73) | (26.19) | |

| Rd2i,t−1 | −0.016 *** | −0.016 *** | −0.016 *** | −0.016 *** |

| (−7.25) | (−7.25) | (−7.26) | (−7.20) | |

| Salet−1 | 0.004 ** | 0.004 ** | 0.004 ** | 0.004 ** |

| (2.07) | (2.07) | (1.99) | (1.98) | |

| Cft−1 | 0.020 *** | 0.020 *** | 0.090 ** | −0.023 |

| (3.06) | (3.06) | (2.53) | (−0.67) | |

| Imt | −0.004 | −0.000 | −0.021 ** | |

| (−0.56) | (−0.00) | (−2.52) | ||

| Soe | −2.297 *** | |||

| (−5.58) | ||||

| Cft−1 × Imt | −0.001 * | 0.000 | ||

| (−1.83) | (0.76) | |||

| Cft−1 × Soe | 0.125 ** | |||

| (2.38) | ||||

| Imt × Soe | 0.029 *** | |||

| (5.38) | ||||

| Cft−1 × Soe × Imt | −0.001 * | |||

| (−1.95) | ||||

| Year | control | control | control | control |

| Industry | control | control | control | control |

| Observations | 5124 | 5124 | 5124 | 5124 |

| Adjusted R-squared | 0.628 | 0.628 | 0.630 | 0.632 |

| Total Sample | ||||

|---|---|---|---|---|

| Variables | Model 1 | Model 2 | Model 3 | Model 4 |

| Constant | −0.051 | 1.004 *** | −0.334 | −0.470 |

| (−0.91) | (2.69) | (−0.82) | (−0.66) | |

| Rdi,t−1 | 0.979 *** | 0.979 *** | 0.980 *** | 0.975 *** |

| (52.89) | (52.89) | (53.41) | (52.73) | |

| Rd2i,t−1 | −0.015 *** | −0.015 *** | −0.015 *** | −0.015 *** |

| (−12.49) | (−12.49) | (−12.58) | (−12.37) | |

| Salet−1 | 0.002 *** | 0.002 *** | 0.002 *** | 0.002 *** |

| (6.00) | (6.00) | (5.43) | (5.69) | |

| Cft−1 | 0.012 *** | 0.012 *** | 0.300 *** | 0.093 |

| (6.30) | (6.30) | (8.18) | (1.02) | |

| Imt | −0.012 *** | 0.005 | 0.006 | |

| (−2.66) | (0.93) | (0.69) | ||

| Soe | 0.472 | |||

| (0.57) | ||||

| Cft−1 × Imt | −0.004 *** | −0.001 | ||

| (−7.87) | (−0.97) | |||

| Cft−1 × Soe | 0.271 *** | |||

| (2.68) | ||||

| Imt × Soe | −0.005 | |||

| (−0.51) | ||||

| Cft−1 × Soe × Imt | −0.003 ** | |||

| (−2.57) | ||||

| Year | control | control | control | control |

| Industry | control | control | control | control |

| Observations | 3597 | 3597 | 3597 | 3597 |

| Adjusted R-squared | 0.735 | 0.735 | 0.739 | 0.740 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhao, X.; Wang, Z.; Deng, M. Interest Rate Marketization, Financing Constraints and R&D Investments: Evidence from China. Sustainability 2019, 11, 2311. https://doi.org/10.3390/su11082311

Zhao X, Wang Z, Deng M. Interest Rate Marketization, Financing Constraints and R&D Investments: Evidence from China. Sustainability. 2019; 11(8):2311. https://doi.org/10.3390/su11082311

Chicago/Turabian StyleZhao, Xinxin, Zongjun Wang, and Min Deng. 2019. "Interest Rate Marketization, Financing Constraints and R&D Investments: Evidence from China" Sustainability 11, no. 8: 2311. https://doi.org/10.3390/su11082311

APA StyleZhao, X., Wang, Z., & Deng, M. (2019). Interest Rate Marketization, Financing Constraints and R&D Investments: Evidence from China. Sustainability, 11(8), 2311. https://doi.org/10.3390/su11082311