Demand Uncertainty, Cost Behavior, and the Asian Financial Crisis: Evidence from Korea

Abstract

1. Introduction

2. Hypothesis Development

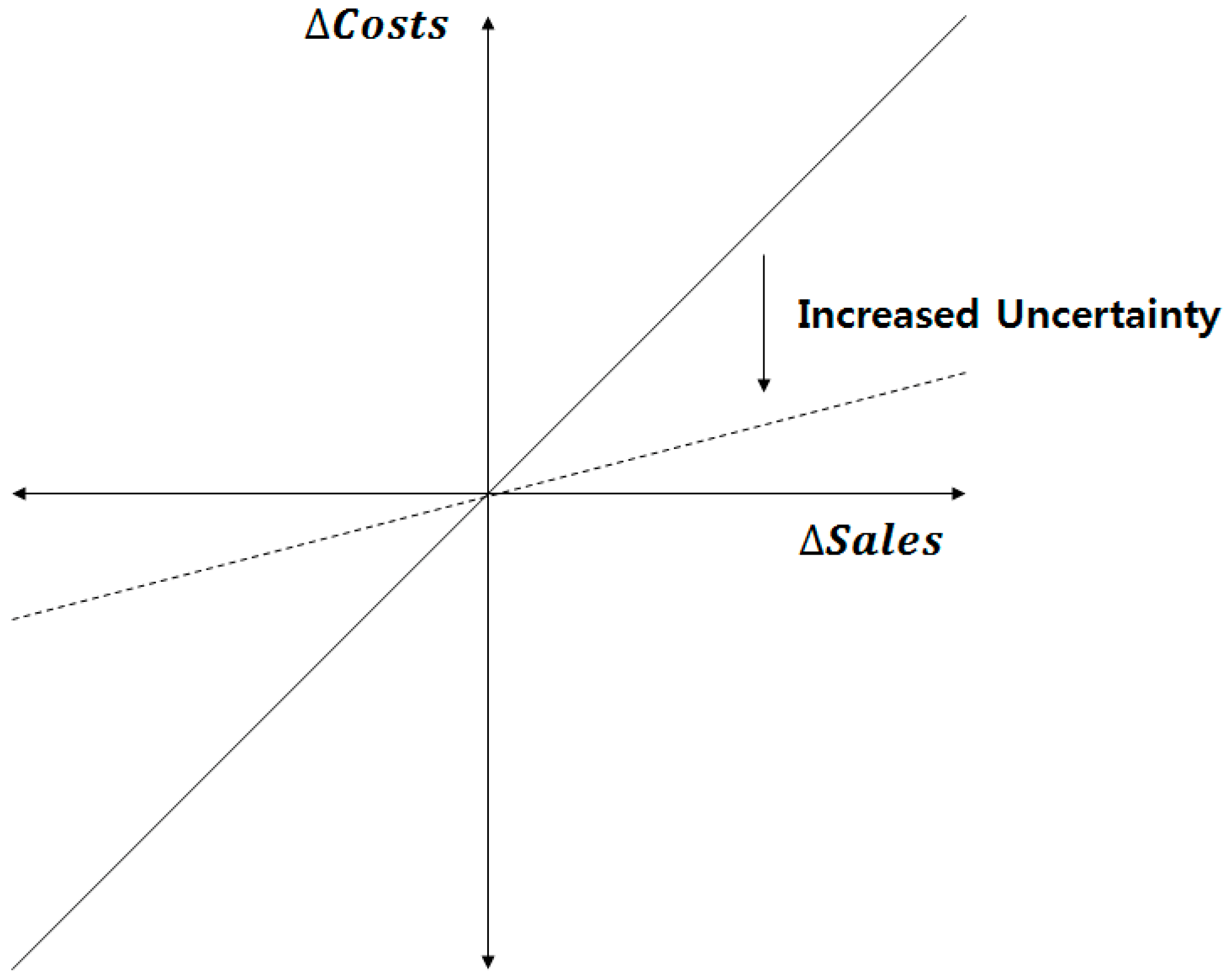

2.1. Demand Uncertainty and Cost Rigidity

2.2. The Impact of the Asian Financial Crisis on the Association between Demand Uncertainty and Cost Rigidity

3. Methods

3.1. Sample

3.2. Empirical Model

4. Empirical Results

4.1. Descriptive Statistics

4.2. Results of Testing Hypotheses

4.3. Additional Tests

5. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Anderson, M.C.; Banker, R.D.; Janakiraman, S.N. Are selling, general, and administrative costs “sticky”? J. Account. Res. 2003, 41, 47–63. [Google Scholar] [CrossRef]

- Noreen, E.; Soderstrom, N. Are overhead costs strictly proportional to activity?: Evidence from hospital departments. J. Account. Econ. 1994, 17, 255–278. [Google Scholar] [CrossRef]

- Noreen, E.; Soderstrom, N. The accuracy of proportional cost models: Evidence from hospital service departments. Rev. Account. Stud. 1997, 2, 89–114. [Google Scholar] [CrossRef]

- Weiss, D. Cost behavior and analysts’ earnings forecasts. Account. Rev. 2010, 85, 1441–1471. [Google Scholar] [CrossRef]

- Chen, C.X.; Lu, H.; Sougiannis, T. The agency problem, corporate governance, and the asymmetrical behavior of selling, general, and administrative costs. Contemp. Account. Res. 2012, 29, 252–282. [Google Scholar] [CrossRef]

- Dierynck, B.; Landsman, W.R.; Renders, A. Do managerial incentives drive cost behavior? Evidence about the role of the zero earnings benchmark for labor cost behavior in private Belgian firms. Account. Rev. 2012, 87, 1219–1246. [Google Scholar] [CrossRef]

- Kama, I.; Weiss, D. Do earnings targets and managerial incentives affect sticky costs? J. Account. Res. 2013, 51, 201–224. [Google Scholar] [CrossRef]

- Kallapur, S.; Eldenburg, L. Uncertainty, real options, and cost behavior: Evidence from Washington State Hospitals. J. Account. Res. 2005, 43, 735–752. [Google Scholar] [CrossRef]

- Holzhacker, M.; Krishnan, R.; Mahlendorf, M.D. Unraveling the black box of cost behavior: An empirical investigation of risk drivers, managerial resource procurement, and cost elasticity. Account. Rev. 2015, 90, 2305–2335. [Google Scholar] [CrossRef]

- Banker, R.D.; Byzalov, D.; Plehn-Dujowich, J.M. Demand uncertainty and cost behavior. Account. Rev. 2014, 89, 839–865. [Google Scholar] [CrossRef]

- Johnson, S.; Boone, P.; Breach, A.; Friedman, E. Corporate governance in the Asian financial crisis. J. Financ. Econ. 2000, 58, 141–186. [Google Scholar] [CrossRef]

- Lemmon, M.L.; Lins, K.V. Ownership structure, corporate governance, and firm value: Evidence from the East Asian financial crisis. J. Financ. 2003, 58, 1445–1468. [Google Scholar] [CrossRef]

- Mitton, T. A cross-firm analysis of the impact of corporate governance on the East Asian financial crisis. J. Financ. Econ. 2002, 64, 215–241. [Google Scholar] [CrossRef]

- Fan, J.P.; Wong, T.J. Corporate ownership structure and the informativeness of accounting earnings in East Asia. J. Account. Econ. 2002, 33, 401–425. [Google Scholar] [CrossRef]

- Choi, D.S.; Lee, J.W. The impact of uncertainty on growth opportunity and investment. Asian Rev. Financ. Res. 2001, 14, 23–57. [Google Scholar]

- Kim, B.K. The effects of uncertainty on investments. Korea Prod. Rev. 2005, 19, 147–172. [Google Scholar]

- Lee, H.Y. The impacts of uncertainty on investment: Empirical evidence from manufacturing firms in Korea. Korea Dev. Rev. 2005, 27, 91–121. [Google Scholar]

- Balakrishnan, R.; Sivaramakrishnan, K.; Sprinkle, G. Managerial Accounting; John Wiley & Sons: Hoboken, NJ, USA, 2008. [Google Scholar]

- Baek, J.S.; Kang, J.K.; Park, K.S. Corporate governance and firm value: Evidence from the Korean financial crisis. J. Financ. Econ. 2004, 71, 265–313. [Google Scholar] [CrossRef]

- Hahm, J.H. The post-crisis transformation of Korea’s financial system. Korean Econ. Rev. 2007, 55, 401–445. [Google Scholar]

- Park, S.S.; Lee, D.H. Recent changes in the announcement effect of seasoned equity offering in Korea. In Proceedings of the Korean Securities Association, Seoul, Korea, 4 December 2010. [Google Scholar]

- Kim, J.H.; Ko, Y.S. An empirical study on the earnings management and debt-equity ratio reduction after the crisis of foreign currency. Korea Account. J. 2006, 15, 119–144. [Google Scholar]

- Ha, G.; Yoon, S.; Choi, S. Critical factors for outsourcing partner selection of manufacturing firms: An AHP based analysis. Korea Bus. Educ. Res. 2011, 26, 489–515. [Google Scholar]

- Cho, J.; Keum, J. Dualism in job stability of the Korean labour market: The impact of the 1997 financial crisis. Pac. Econ. Rev. 2009, 14, 155–175. [Google Scholar] [CrossRef]

- Petersen, M.A. Estimating standard errors in finance panel data sets: Comparing approaches. Rev. Financ. Stud. 2009, 22, 435–480. [Google Scholar] [CrossRef]

- Fama, E.F.; MacBeth, J.D. Risk, return, and equilibrium: Empirical tests. J. Political Econ. 1973, 81, 607–636. [Google Scholar] [CrossRef]

- Calleja, K.; Steliaros, M.; Thomas, D.C. A note on cost stickiness: Some international comparisons. Manag. Account. Res. 2006, 17, 127–140. [Google Scholar] [CrossRef]

- Banker, R.D.; Byzalov, D.; Chen, L.T. Employment protection legislation, adjustment costs and cross-country differences in cost behavior. J. Account. Econ. 2013, 55, 111–127. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Panel A | ||||||

| Variables | N | Mean | Std | Median | p25 | p75 |

| Sales Revenue ($ mil.) | 14,357 | 11.03 | 42.09 | 1.90 | 0.82 | 5.56 |

| SG&A Costs ($ mil.) | 14,357 | 1.35 | 7.70 | 0.19 | 0.08 | 0.61 |

| SG&A/Sales (%) | 14,357 | 14.35 | 14.04 | 9.76 | 6.06 | 16.43 |

| Demand_Uncertainty | 14,357 | 0.17 | 0.06 | 0.16 | 0.12 | 0.21 |

| GDP_Growth (%) | 14,357 | 5.87 | 3.58 | 5.90 | 3.30 | 8.90 |

| Panel B | ||||||

| Pre-Crisis Period | Post-Crisis Period | |||||

| Variables | N | Mean | Median | N | Mean | Median |

| Sales Revenue ($ mil.) | 3677 | 8.07 | 1.76 | 8383 | 13.69 | 2.21 |

| SG&A Costs ($ mil.) | 3677 | 0.63 | 0.20 | 8383 | 1.90 | 0.24 |

| SG&A/Sales (%) | 3677 | 12.34 | 9.48 | 8383 | 15.76 | 10.10 |

| Demand_Uncertainty | 3677 | 0.13 | 0.12 | 8383 | 0.17 | 0.15 |

| GDP_Growth (%) | 3677 | 9.35 | 9.60 | 8383 | 4.45 | 3.90 |

| Full Sample | ||||||

|---|---|---|---|---|---|---|

| Dependent Var: log(SG&Ai,t/SG&Ai,t−1) | (1) | (2) | (3) | (4) | (5) | (6) |

| Clustering | Clustering | Clustering | Clustering | Fama and MacBeth | Fama and MacBeth | |

| Constant | 0.005 (0.32) | 0.006 (0.44) | −0.016 (−1.30) | −0.012 (−0.97) | 0.057 *** (2.82) | 0.057 *** (2.82) |

| β1: log(Salesi,t/Salesi,t−1) | 0.579 *** (23.05) | 0.751 *** (17.73) | 0.596 *** (13.10) | 0.683 *** (17.01) | 0.494 *** (3.95) | 0.663 *** (5.45) |

| β2: Demand_Uncertainty * log(Salesi,t/Salesi,t−1) | −1.024 *** (−4.92) | −0.529 *** (−6.51) | −1.026 *** (−5.76) | |||

| ∑γk Controls | ||||||

| GDP_Growth * log(Salesi,t/Salesi,t−1) | 0.005 * (1.96) | 0.005 * (1.83) | −0.001 (−0.37) | −0.001 (−0.29) | ||

| Industry dummies * log(Salesi,t/Salesi,t−1) | included | included | included | included | included | included |

| ∑γj Controls | ||||||

| GDP_Growth | 0.006 *** (13.70) | 0.006 *** | 0.007 *** | 0.006 *** | ||

| (13.26) | (11.44) | (10.70) | ||||

| Industry dummies | included | included | included | included | included | included |

| Observations | 14,357 | 14,357 | 10,647 | 10,647 | 14,357 | 14,357 |

| Adjusted R2 | 0.23 | 0.24 | 0.22 | 0.24 | 0.27 | 0.28 |

| Linear combination of β1 and ∑γk Control | 0.470 *** (26.30) | 0.677 *** (15.37) | 0.385 *** (14.57) | 0.528 *** (15.22) | 0.525 *** (7.48) | 0.719 *** (10.03) |

| Pre-Crisis | Post-Crisis | |||

|---|---|---|---|---|

| Dependent Var: log(SG&Ai,t/SG&Ai,t−1) | (1) | (2) | (3) | (4) |

| Constant | 0.029 * (1.71) | 0.034 ** (2.02) | 0.027 (1.47) | 0.028 (1.51) |

| β1: log(Salesi,t/Salesi,t−1) | 0.707 *** (8.23) | 0.988 *** (9.39) | 0.493 *** (12.25) | 0.674 *** (13.77) |

| β2: Demand_Uncertainty * log(Salesi,t/Salesi,t−1) | −1.637 *** (−4.86) | −0.894 *** (−5.03) | ||

| ∑γk Control | ||||

| γ1: GDP_Growth * log(Salesi,t/Salesi,t−1) | 0.003 (0.35) | 0.005 (0.61) | 0.012 ** (2.17) | 0.011 ** (1.97) |

| γ2: Industry dummies * log(Salesi,t/Salesi,t−1) | included | included | included | included |

| ∑γj Control | ||||

| GDP_Growth | 0.001 (1.38) | 0.001 (0.80) | 0.002 ** (2.43) | 0.002 ** (2.25) |

| Industry dummies | included | included | included | included |

| Observations | 3677 | 3677 | 8383 | 8383 |

| Adjusted R2 | 0.24 | 0.25 | 0.19 | 0.20 |

| Linear combination of β1 and ∑γkControl | 0.393 *** (14.68) | 0.649 *** (11.72) | 0.427 *** (24.26) | 0.624 *** (15.60) |

| Sig. of difference: Column (2) and (4) | Coef. | z | P > |z| | |

| [Pre_mean]β2 - [Post_mean]β2 = 0 | −0.743** | −2.19 | 0.028 | |

| Full Sample | Pre-Crisis | Post-Crisis | ||||

|---|---|---|---|---|---|---|

| Dependent Var: log(SG&Ai,t/SG&Ai,t−1) | (1) | (2) | (3) | (4) | (5) | (6) |

| Constant | −0.039 *** (−8.31) | −0.039 *** (−8.21) | −0.089 *** (−7.36) | −0.086 *** (−7.13) | −0.010 (−0.73) | −0.009 (−0.72) |

| β1: log(Salesi,t/Salesi,t−1) | 0.213 *** (2.92) | 0.276 *** (3.58) | 0.388 *** (4.35) | 0.538 *** (4.73) | 0.116 ** (2.17) | 0.184 *** (2.67) |

| β2: Demand_Uncertainty * log(Salesi,t/Salesi,t−1) | −0.397 *** (−2.74) | −1.230 *** (−2.77) | −0.295 * (−1.81) | |||

| ∑γk Control | ||||||

| γ1: GDP_Growth * log(Salesi,t/Salesi,t−1) | 0.002 (0.65) | 0.001 (0.42) | 0.032 *** (3.15) | 0.033 *** (3.24) | 0.006 (1.35) | 0.005 (1.23) |

| γ2: Industry dummies * log(Salesi,t/Salesi,t−1) | included | included | included | included | included | included |

| ∑γj Control | ||||||

| GDP_Growth | 0.002 *** (6.58) | 0.002 *** (6.28) | 0.002 * (1.66) | 0.002 (1.45) | −0.003 *** (−4.44) | −0.003 *** (−4.64) |

| Industry dummies | included | included | included | included | included | included |

| Observations | 12,363 | 12,363 | 2267 | 2267 | 7666 | 7666 |

| Adjusted R2 | 0.13 | 0.13 | 0.17 | 0.18 | 0.10 | 0.11 |

| Linear combination of β1 and ∑γkControl | 0.238 *** (16.46) | 0.325 *** (9.68) | 0.351 *** (15.50) | 0.553 *** (7.15) | 0.173 *** (10.68) | 0.244 *** (6.11) |

| Sig. of difference: Column (4) and (6) | Coef. | z | P > |z| | |||

| [Pre_mean]β2 - [Post_mean]β2 = 0 | −0.935 ** | −2.09 | 0.037 | |||

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kwon, D.-H. Demand Uncertainty, Cost Behavior, and the Asian Financial Crisis: Evidence from Korea. Sustainability 2019, 11, 2238. https://doi.org/10.3390/su11082238

Kwon D-H. Demand Uncertainty, Cost Behavior, and the Asian Financial Crisis: Evidence from Korea. Sustainability. 2019; 11(8):2238. https://doi.org/10.3390/su11082238

Chicago/Turabian StyleKwon, Dae-Hyun. 2019. "Demand Uncertainty, Cost Behavior, and the Asian Financial Crisis: Evidence from Korea" Sustainability 11, no. 8: 2238. https://doi.org/10.3390/su11082238

APA StyleKwon, D.-H. (2019). Demand Uncertainty, Cost Behavior, and the Asian Financial Crisis: Evidence from Korea. Sustainability, 11(8), 2238. https://doi.org/10.3390/su11082238