Spatial Considerations for Implementing Two Direct-to-Consumer Food Models in Two States

and

and

Abstract

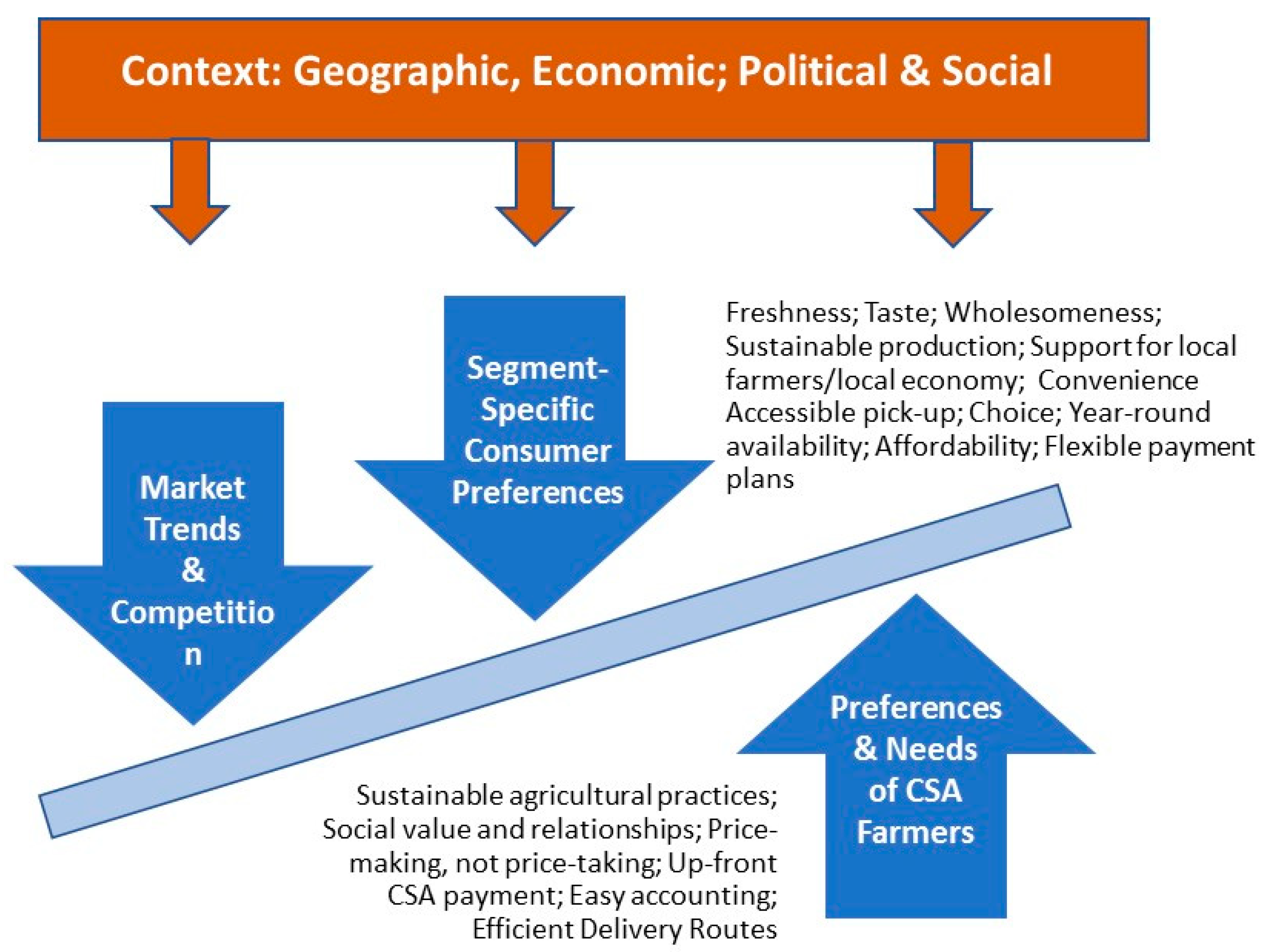

1. Introduction

1.1. Study Purpose

1.2. Design and Setting

2. Materials and Methods

2.1. Analysis of Quantitative and Geospatial Data

2.2. Analysis of Qualitative Data

3. Results

3.1. Quantitative Findings

3.1.1. Community Demographics

3.1.2. Transportation Environment

3.1.3. Geospatial Results

3.1.4. Context Summary

3.2. Qualitative Findings

3.2.1. Farm Fresh Food Boxes (F3B)

“CSAs in general are kind of a little tapped out, in this locality at least, you know? Everyone who is ‘right’ to sign up for a CSA probably has already done so.”—(WA1/4)

“…people are being pushed into these eastern countries all up and down western Washington in search of affordability. But if they’re driving down valley every day, they can also shop at Fred Meyer and Costco and Walmart and, you know…and the food co-op.”—WA10/18

“… has a different feel to it…They sell beer and they have cigarettes, but the cigarettes are tucked behind the counter… You go in there and there are aisles of cereal boxes, and there are cold cases where you can get milk, and eggs, you know? And kinda like that place where it’s like, “Oh, yeah, we’re out of eggs.” And you run down to the corner and grab some, you know, to finish baking Christmas cookies…”—WA1/4

“…general stores and mom and pop stores, you know, they’ve been around…and the family that owns them is well known. And, you know, so if they’re committed and talking it up and giving time to it, it’s almost like people think, “Oh, this is worthwhile, because, you know, the Johnsons are into it.”—VT4/0.2

“We targeted stores [for F3B implementation] that are sort of people’s drive-by stores. Like, they drive by, they stop, they make their purchase, they go. So, there’s a little bit in terms of the efficiency, like they don’t have to go specifically drive somewhere else to make the purchase”—(VT4/0.2)

“You know, we haven’t had a ton of success in terms of volume, so I was trying to figure out, like, you know, is it the price? Is it the … wrong products for the customer that’s there? You know, is it the convenience that isn’t there? Like--what is it that’s not working?”—VT4/0.2

“I think it’s going to come down to just, like, marketing and how to really demonstrate what it is and how, like, what a great value it is and why they should do it. You know, it’s not enough just to sort of, like, put a picture on a poster…”—VT2/6

“Wherever the store is conveniently located-- that should be a good fit. But really it always has a lot to do with store personnel. You know, the store manager, or store personnel, they’ve gotta be excited about it, or it’s just gonna be, like, you know, a sack of potatoes in the back room for them.”—VT4/0.6

3.2.2. Farm Fresh Foods for Healthy Kids (F3HK)

“Frequently [before the study] the driver would show up to a drop site and couldn’t wait around for the EBT customer to come and physically swipe the card, so we would leave the box and then not receive payment for that week. And so, this helped a lot, having a central location with a window of time where people could come.”—WA26/1

“… as a whole of being comparable [with farmers’ markets] —the ability to accept EBT and have that central location! I mean all over the place, farmers markets …you can switch out things in your box, you can talk to somebody from the farm—that’s what people really want. For future people wanting to join, [accepting EBT is] definitely a huge deal to them and I think in the future that’s going to increase our profits a lot, too.”—(WA26/1)

“…given the fact that people are paying with cash sometimes, we’re a lot better set up to record and give change and that sort of thing at the farm stand…Also, people have lots more flexibility on when they come”—WA10/1

“It’s a lot of extra time…if they want to pay weekly. In order to make sure that we’re there when they’ll be there, because we don’t generally hang out for the whole pickup time…so we’re talking about shifting our schedules or the pickup time”—VT0/0.5

“I think that the CSA model is pretty unfamiliar for people and if they don’t quite know what they’re getting into, there were a lot of missed shares. We’d drop a share off and the CSA member thought she was at a different place or kept switching, didn’t really realize the commitment to a site or to a time”—(VT 0/0.5)

“But at the end of the day, like I said before, I can’t scoff at some other entity coming and handing me 9 CSA members. That’s a huge benefit to the farm.”—VT12/2

“I would say, as much as anything, it was probably just learning about the potential of how it might work… But I guess because I knew that it was a new program and trying to get things rolling, I was willing to hang in there with it”—WA 17/1

3.2.3. Qualitative Interview Summary

4. Discussion

4.1. Suitability/Accessibility of the Pickup Location

4.2. Effect of Neighboring Food Venues

4.3. Potential Farmer Burden Related to Pickup Distance

4.4. Summary of Findings

4.5. Study Limitations

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Farm Fresh Food Boxes | Farm Fresh Foods for Healthy Kids | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Farm | Farm to Retail (mi) | Retail to Supermarket (mi) | Retail to Farmers’ Market (mi) | RUCA Code | Farm | Farm to Pickup (mi) | Pickup to Supermarket (mi) | Pickup to Farmers’ Market (mi) | RUCA Code |

| VT2/6 | 2.1 | 6 | 17.5 | 5.0 | VT0/0.5 | 0 | 0.5 | 16.7 | |

| VT4/0.2 | 4.2 | 0.2 | 0.0 | 1.0 | VT12/2 | 0 and 11.9 | 1.6 | 11.1 | |

| VT4/0.6 | 4.2 | 0.6 | 38.0 | 10.6 | VT0/2 | 0 | 1.7 | 0.8 | |

| ----- | ----- | ----- | ----- | ----- | VT14/8 | 14 | 8.4 | 2.8 | |

| Average | 3.5 | 2.3 | 19.0 | ----- | Average | 5.18 | 3.05 | 6.3 | ----- |

| WA1/4 | 0.9 | 4.1 | 4.2 | 2.0 | WA10/1 | 10.3 | 1.4 | 1.3 | 2.0 |

| WA6/6 | 5.6 | 5.7 | 19.4 | 2.0 | WA26/1 | 26.5 | 1.1 | 0.8 | 2.0 |

| WA10/18 | 9.9 | 18.3 | 5.7 | 2.1 | WA17/1 | 16.9 | 0.9 | 4.5 | 2.1 |

| Average | 5.5 | 9.4 | 9.8 | ----- | Average | 17.9 | 1.1 | 2.2 | ----- |

| Representative Quotes from Farmer Interviews: Key Findings by State | ||||

|---|---|---|---|---|

| F3B Vermont | F3B Washington | F3HK Vermont | F3HK Washington | |

| DTC model’s profitability & other benefits | VT4/0.6: “It’s another venue to sell our produce … I was hoping to reach some other type of customers and citizens that, for whatever reason, didn’t have access to what we were growing…You know, it did help sort of draining out some of the surplus, which is what I wanted it to do.” | WA1/4: “[F3B] stood out to me as something that was good and had potential. “ WA2: “… it made us continue to think about the ways in which we can reach people and market better.” | VT0/0.5: “It hasn’t [made money]. Just with the two [CO-CSA] people, there wasn’t that big of a difference. It was really nice to get half of the cost up front” VT12/2: “…it was economically a net benefit despite the challenges and frustrations… It’s hard for me to… scoff at 9 x $360. That’s income for the farm.” | WA10/1: “If I thought that it had made a huge positive [financial]… impact, I would know… Now in the feel-good impact—it’s there.” WA26/1: “I would say it increased it because … we picked up more money. The cost of doing the deliveries and stuff … it was still a gain to do it.” |

| DTC model’s impact on increasing customer base | VT2/6: “Calling it a food box instead of the CSA… making it accessible in locations that are not sort of your typical CSA locations—I appreciate that effort to just make it, make CSA, a little bit more of an accessible concept and locations.” | WA6/6 “…people who hear about us through the [F3B] marketing and then who buy the boxes and get hooked on the food and the experience…if we can continue to grow the program and get more boxes, that supports us financially…to be able to build a successful financial business” | VT12/2: “And also it was going to be a huge benefit for our farm to have 10 to 20 new CSA members. In our experience, usually when people become CSA members, we have a really high retention rate. | WA26/1: “I think what really worked well was helping things to be more accessible so that people could use their EBT benefits” WA17/1: “We do all our shares in [County B] in the [major city] area and we’re interested in trying to shift some of our market to [County A].” |

| Farmer’s awareness of food access barriers | VT2/6: “…perceptions that, you know, buying organic food is more expensive…lack of time and… resources to cook [fresh produce] …we definitely see there’s sort of, like, a big skill gap in folks VT 4: Farmer: I would say maybe transportation, convenience, and maybe money, financial reasons. | WA10/18: “…the barriers, I think, are education and money… most of my clientele from my CSA has really been associated even with the national parks… a more educated community… They’ve had college degrees and they share about their food. And it’s a long drive to get to good food. | ||

| Effect of geographic isolation/food deserts | VT4/0.2: “[if] the closest store that sells any produce within, you know, 30 min or 45 min, or something, and all they have is the… iceberg lettuce, and the pink pale tomatoes, you know, then those people might be psyched [about] fresh veggies” | WA10/18: “there’s two small convenience stores and gas stations in the last town of our valley…that becomes a dead-end in the winter…in the mountains, the pass is closed. And the only people that go up there are skiers in the winter and snowmobilers.” | ||

| Competition from conventional and other DTC venues | VT4/0.2: “…our food is going to be more expensive than at Costco or Walmart, I think the local… agricultural products in general are really available now in almost all retail settings, you know, stores, restaurants, a lot of CSAs, a lot of farm stands, a lot of farmer’s markets.” | WA6/6: “[the pickup] it’s in a really small, little town … demographically, [it] is mostly older people who have their own gardens or just people passing through who aren’t necessarily thinking about getting vegetables from a farm that they don’t know about.” | WA26/1:”…being comparable, the ability to accept EBT and have that central location… farmers markets that offer that kind of model where… you can switch out things in your box, you can talk to somebody from the farm, that’s what people really want… in the future, [offering similar features] that’s going to increase our profits” | |

| DTC Model and farmer burden | VT4/0.2: “It [staffing and resource expenditures] didn’t change it much. I mean, you know, in terms of pack-out and distribution, we’re already all set up for that, and it was such a low volume…It was not like we had to shift our pack-out timing or anything because we have so much to do.” | WA1/4: “The proximity of the location was definitely a life saver just because, you know, it was not something that I was able to, going back to habit, create really effective ones that I could ingrain into my schedule.” | VT0/0.5: if they want to pay weekly–in order to make sure that we’re there when they’ll be there … we’re talking about shifting our schedules or the pickup time or I- don’t-know-what, so it’s easier for somebody to be there. | WA10/1:” Basically, people brought checks or they brought cash and that presented a bit of an issue because we don’t generally carry change for the pickup site” WA17/1:… if we are going to be doing CSA delivery, that we could tie in with nonsubsidized people at the same time… basically it allowed me …to make it worthwhile to deliver to some people in [town A] |

| Pricing Accom-modations | VT4/0.6: “…we kind of subsidize the pricing of what we’re putting in the box to reach a certain price point…We gave away a lot of produce at a really good price… I was pricing the produce in the box … almost below wholesale prices.” | WA10/18: “…you know, my CSA is pretty cheap because my clientele is not high-income… I certainly review other people’s CSA [prices] … I see I’m always on the low end of the spectrum. | WA26/1:”… people are pretty much buying things at cost anyway by joining a CSA. It’s really hard for a farmer to make that cost even lower and offer a discount sometimes, but a pretty minimal discount, because so much of that price is just going directly into [paying operating expenses for] the farm. “ | |

| Pickup location--suitability | VT4/0.2: “[at convenience stores], you go grab something quick, you grab your lunch quick, or you get that gallon of milk that you forgot, or maybe they have ice cream on sale…But you’re not going out to go grocery shopping when you stop there typically. | WA1/4: “I would be the happiest person in the world if 7-11s were selling fresh food. But I don’t think those are the spot where you’re gonna be able to snag people, unless you are doing, like, heavily promoted, subsidized options, you know?” | VT0/0.5: “…we’d love to have [pickup] it at the farm but because of neighbors, we can’t have that much traffic on the road… But we’re building a house and a new barn sort of up the road, so we could have a different access road and not be sharing the road with the summer camp.” | WA26/1: “I am curious about why people dropped out of the program, particularly residents at [apartment complex that also served as pickup site] who it seemed like a very accessible thing. Did they give you [researches] reasons why they were dropping out, or did they just stop coming?” |

| Suggestions & planned changes | VT4/0.2: “…that maybe it’s a smaller price point, a smaller package, and something that they can display where people can see the product and grab and go. You know, you market it as more of like a quick meal prep. Or a quick lunch addition. Or, you know, here’s your salad for the week or something.” VT4: [At] the farmers market, there’s “crop-cash” that people on [EBT] cards get…[this could be] tied in where they could use it on, you know, the farm box and stuff like that. | WA1/4: “…try to expand the venues at which this can be offered. So don’t confine it necessarily to stores, if you will. I think the community centers, and health clubs” WA10/18: “I don’t really understand how far social media reaches into impoverished communities. That’s one question. … for example, how many of them have smartphones and are on Facebook? … you know--how do you outreach into rural communities?” | VT0/0.5 “…instead of putting everybody’s share in a single box, we have 8 boxes out and one would have kale and one would have tomatoes and it would say take one bunch of kale and a pound of tomatoes.” VT12/2: “… as long as …it’s not against the research policies or if I’m not collecting food stamps in advance from someone, I think I’m going to tell them that’s how we’re going to do it [monthly rather than weekly installments]” | WA26/1:”Well, we were talking about having the dropsite at the [nonprofit CBO]. I think that could change things and might make it more accessible to people–a window of time and then also give them choice with their box if they need to switch things out.” WA17/1: “I would like to make a couple of changes but the main one being I’d like to discuss the possibility of having the pickup site be at our fruit stand. “ |

| Question | Quantitative Findings | Qualitative Findings | Comments |

|---|---|---|---|

| How suitable/accessible was the pickup location? | --Both DTC models in VT & WA had low walkability, high car dependence, lack of public transportation in pickup areas. --VT pickup locations were in more rural areas for both models | --F3B farmers in both states recognized geographic isolation, lack of public transportation and car-dependence as potential issues for customers 1 --F3B farmers spoke more about the suitability of setting than suitability of location. --2 WA F3HK farmers specifically said they selected pickup sites with customer convenience in mind | --Although RUCA codes designations showed VT to have more rural locations, there were pockets of more isolated and rural areas within WA for both DTC models. |

| Did farmers feel other nearby food venues enhanced or detracted from implementation? | --Both DTC models VT & WA had few farmers markets within two miles of pickup sites. --WA F3B locations had the longest average pickup to SM distance --WA F3HK locations had the shortest pickup to SM distance --VT F3B and F3HK pickup sites had pickup to SM distances that fell in between these extremes | --VT F3B farmers said local produce was common in conventional stores and nearby DTC venues --WA F3B farmers said food pantries and gardens were additional sources of local food --a WA farmer thought geographic isolation combined with few local stores, might provide a niche for F3B --Accepting EBT put F3HK on more equal footing with nutrition incentives at FM, according to a WA farmer --F3HK in WA and VT did not mention other local food venues in interviews | --All VT F3HK farms, and one WA F3HK farm, pickup either on-farm or at existing CSA drop sites --VT & WA F3B farmers were equally likely to mention the effect other local food venues, despite differences in pickup to SM distances |

| How did actual farm to pickup distances correspond with farmer’s perceived delivery time burden? | WA farmers implementing F3HK had the longest average farm-to-pickup site driving distance | --F3HK farms in both states reported deliveries constituted no burden, but said extra staff time was required to handle payment transactions and maintain records --WA F3B farmers said proximity to the retailer made for easy delivery but noted interacting with retailers took extra time. | --All VT F3HK farms, and one WA F3HK farm, had pickups either on-farm or at existing CSA drop sites --Only F3HK farmers were asked specifically about burden related to deliveries |

References

- Tropp, D. Why Local Food Matters: The Rising Importance of Locally-Grown Food in the US Food System; No. 160752; United States Department of Agriculture: Washington, DC, USA, 2013.

- US Department of Agriculture. 1992 Census of Agriculture; US Department of Agriculture: Washington, DC, USA, 1994.

- US Department of Agriculture. 2007 Census of Agriculture; US Department of Agriculture: Washington, DC, USA, 2009.

- US Department of Agriculture. 2012 Census of Agriculture; US Department of Agriculture: Washington, DC, USA, 2014.

- Sitaker, M.; Kolodinsky, J.; Pitts, S.J.; Seguin, R. Do entrepreneurial food systems innovations impact rural economies and health? Evidence and gaps. Am. J. Entrep. 2014, 7, 3–16. [Google Scholar]

- Kloppenburg, J.; Hendrickson, J.; Stevenson, G.W. Coming in to the foodshed. Agric. Hum. Values 1996, 13, 33–42. [Google Scholar] [CrossRef]

- Key, N.; Roberts, M.J. Nonpecuniary Benefits to Farming: Implications for Supply Response to Decoupled Payments. Am. J. Agric. Econ. 2009, 91, 1–18. [Google Scholar] [CrossRef]

- Brown, C.; Miller, S. The impacts of local markets: A review of research on farmers markets and community supported agriculture (CSA). Am. J. Agric. Econ. 2008, 90, 1298–1302. [Google Scholar] [CrossRef]

- Guthman, J.; Morris, A.W.; Allen, P. Squaring farm security and food security in two types of alternative food institutions. Rural Soc. 2006, 71, 662–684. [Google Scholar] [CrossRef]

- Feenstra, G. Local Food Systems and Sustainable Communities. Am. J. Altern. Agric. 1997, 12, 28–36. [Google Scholar] [CrossRef]

- Morgan, T.K.; Alipoe, D. Factors affecting the number and type of small-farm direct marketing outlets in Mississippi. J. Food Distrib. Res. 2001, 32, 125–132. [Google Scholar]

- King, R.; Hand, M.S.; DiGiacomo, G.; Clancy, K.; Gomez, M.I.; Hardesty, S.D.; Lev, L.; McLaughlin, E.W. Comparing the Structure, Size, and Performance of Local and Mainstream Food Supply Chains; ERS-99; U.S. Department of Agriculture, Economic Research Service: Washington, DC, USA, 2010.

- Cone, C.A.; Myhre, A. Community-supported agriculture: A sustainable alternative to industrial agriculture? Hum. Organ. 2000, 59, 187–197. [Google Scholar] [CrossRef]

- Jarosz, L. The city in the country: Growing alternative food networks in Metropolitan areas. J. Rural. Stud. 2008, 24, 231–244. [Google Scholar] [CrossRef]

- Galt, R.E. The moral economy is a double-edged sword: Explaining farmers’ earnings and self-exploitation in community-supported agriculture. Econ. Geogr. 2013, 89, 341–365. [Google Scholar] [CrossRef]

- McKee, E. It’s the Amazon World: Small-Scale Farmers on an Entrepreneurial Treadmill. Cult. Agric. Food Environ. 2018, 40, 65–69. [Google Scholar] [CrossRef]

- Guptill, A.; Wilkins, J.L. Buying into the food system: Trends in food retailing in the US and implications for local foods. Agric. Hum. Values 2002, 19, 39–51. [Google Scholar] [CrossRef]

- Morgan, E.; Severs, M.; Hanson, K.; McGuirt, J.; Becot, F.; Wang, W.; Kolodinsky, J.; Sitaker, M.; Jilcott Pitts, S.; Ammerman, A.; et al. Gaining and Maintaining a Competitive Edge: Evidence from CSA Members and Farmers on Local Food Marketing Strategies. Sustainability 2018, 10, 2177. [Google Scholar] [CrossRef]

- Feldmann, C.; Hamm, U. Consumers’ perceptions and preferences for local food: A review. Food Qual. Prefer. 2014, 40, 152–164. [Google Scholar] [CrossRef]

- Pole, A.; Kumar, A. Segmenting CSA members by motivation: Anything but two peas in a pod. Br. Food J. 2015, 117, 1488–1505. [Google Scholar] [CrossRef]

- Bean, M.; Sharp, J.S. Profiling alternative food system supporters: The personal and social basis of local and organic food support. Renew. Agric. Food Syst. 2011, 26, 243–254. [Google Scholar] [CrossRef]

- Ostrom, M.R. Community supported agriculture as an agent of change: Is it working. In Remaking the North American Food System; Hinrichs, C., Lyson, T., Eds.; University of Nebraska Press: Lincoln, NE, USA, 2007; pp. 99–120. [Google Scholar]

- McGuirt, J.T.; Pitts, S.B.J.; Hanson, K.L.; DeMarco, M.; Seguin, R.A.; Kolodinsky, J.; Ammerman, A.S. A modified choice experiment to examine willingness to participate in a Community Supported Agriculture (CSA) program among low-income parents. Renew. Agric. Food Syst. 2018, 1–18. [Google Scholar] [CrossRef]

- Perez, J.; Allen, P.; Brown, M. Community Supported Agriculture on the Central Coast: The CSA Member Experience; Center for Agroecology and Sustainable Food Systems, University of California: Santa Cruz, CA, USA, 2003. [Google Scholar]

- Mittal, A.; Krejci, C.C.; Craven, T.J. Logistics Best Practices for Regional Food Systems: A Review. Sustainability 2018, 10, 168. [Google Scholar] [CrossRef]

- Lohr, L.; Diamond, A.; Dicken, C.; Marquardt, D. Mapping Competition Zones for Vendors and Customers in U.S. Farmers Markets; US Department of Agriculture: Washington, DC, USA, 2011.

- Woods, T.; Ernst, T.; Tropp, D. Community Supported Agriculture–New Models for Changing Markets; U.S. Department of Agriculture: Washington, DC, USA, 2017.

- Rossi, J.J.; Woods, T.A.; Allen, J.E. Impacts of a Community Supported Agriculture (CSA) Voucher Program on Food Lifestyle Behaviors: Evidence from an Employer-Sponsored Pilot Program. Sustainability 2017, 9, 1543. [Google Scholar] [CrossRef]

- Wholesome Wave. How to Start a CSA Nutrition Incentive Program. Available online: https://www.wholesomewave.org/sites/default/files/network/resources/files/How-to-Start-a-CSA-Incentive-Program-Toolkit.pdf (accessed on 22 February 2019).

- Kolodinsky, J.M. Community Supported Agriculture. In The Sage Encyclopedia of Food Issues; Albala, K., Ed.; Sage: Los Angeles, CA, USA, 2015; pp. 204–209. ISBN 978-1-4522-4301-6. [Google Scholar]

- LeRoux, M.N.; Schmit, T.M.; Roth, M.; Streeter, D.H. Evaluating marketing channel options for small-scale fruit and vegetable producers. Renew. Agric. Food Syst. 2010, 25, 16–23. [Google Scholar] [CrossRef]

- Park, T.; Mishra, A.K.; Wozniak, S.J. Do farm operators benefit from direct to consumer marketing strategies? Agric. Econ. 2014, 45, 213–224. [Google Scholar] [CrossRef]

- Smith, D.; Greco, L.; Van Soelen Kim, J.; Sitaker, M.; Kolodinsky, J. Farm Fresh Food Box: An Innovative Business Model for Rural Communities. In Rural Connections; University of Vermont: Burlington, VT, USA, 2018; pp. 25–28. [Google Scholar]

- Haynes-Maslow, L.; Osborne, I.; Jilcott Pitts, S.; Sitaker, M.; Byker Shanks, C.; Leone, L.; Maldonado, A.; McGuirt, J.; Andress, L.; Bailey-Davis, L.; et al. Rural Corner Store Owners’ Perceptions of Stocking Healthier Foods in Response to Proposed Changes to the United States’ Supplemental Nutrition Assistance Program Retailer Rule. Food Policy 2018, 81, 58–66. [Google Scholar] [CrossRef]

- Bauman, A.; Mcfadden, D.T.; Jablonski, B.B.R. The Financial Performance Implications of Differential Marketing Strategies: Exploring Farms that Pursue Local Markets as a Core Competitive Advantage. Agric. Resour. Econ. Rev. 2018, 47, 1–28. [Google Scholar] [CrossRef]

- Seguin, R.A.; Ammerman, A.S.; Hanson, K.L.; Kolodinsky, J.; Pitts, S.B.J.; Sitaker, M. Farm Fresh Foods for Healthy Kids: Innovative Cost-Offset Community Supported Agriculture Intervention to Prevent Childhood Obesity and Strengthen Local Agricultural Economies. J. Nutr. Educ. Behav. 2017, 49, S120. [Google Scholar] [CrossRef][Green Version]

- Kolodinsky, J.M.; Sitaker, M.; Morgan, E.H.; Connor, L.M.; Hanson, K.L.; Becot, F.; Pitts, S.B.; Ammerman, A.S.; Seguin, R.A. Can CSA Cost-Offset Programs Improve Diet Quality for Limited Resource Families? Choices 2017, 32, 1–10. [Google Scholar]

- Andreatta, S.; Wickliffe, W. Managing farmer and consumer expectations: A study of a North Carolina farmers market. Hum. Org. 2002, 61, 167–176. [Google Scholar] [CrossRef]

- Hoffman, J.A.; Agrawal, T.; Wirth, C.; Watts, C.; Adeduntan, G.; Myles, L.; Castaneda-Sceppa, C. Farm to family: Increasing access to affordable fruits and vegetables among urban head start families. J. Hunger. Environ. Nutr. 2012, 7, 165–177. [Google Scholar] [CrossRef]

- Blake, M.K.; Mellor, J.; Crane, L. Buying Local Food: Shopping Practices, Place, and Consumption Networks in Defining Food as “Local”. Ann. Assoc. Am. Geog. 2010, 100, 409–426. [Google Scholar] [CrossRef]

- McGuirt, J.T.; Pitts SB, J.; Ward, R.; Crawford, T.W.; Keyserling, T.C.; Ammerman, A.S. Examining the influence of price and accessibility on willingness to shop at farmers’ markets among low-income eastern North Carolina women. J. Nutr. Educ. Behav. 2014, 46, 26–33. [Google Scholar] [CrossRef]

- United States Census Bureau. 2012–2016 American Community Survey 5-Year Estimates [Data File]. 2016. Available online: http://www.huduser.org/Datasets/IL/IL08/in_fy2008.pdf (accessed on 26 February 2019).

- Walkscore. Available online: http://www.walkscore.com (accessed on 26 February 2019).

- Carr, L.J.; Dunsiger, S.I.; Marcus, B.H. Walk score as a global estimate of neighborhood walkability. Am. J. Prev. Med. 2010, 39, 460–463. [Google Scholar] [CrossRef]

- Duncan, D.T.; Aldstadt, J.; Whalen, J.; Melly, S.J. Validation of Walk Scores and Transit Scores for estimating neighborhood walkability and transit availability: A small-area analysis. Geo J. 2013, 78, 407–416. [Google Scholar] [CrossRef]

- Hirsch, J.A.; Moore, K.A.; Evenson, K.R.; Rodriguez, D.A.; Roux AV, D. Walk Score® and Transit Score® and walking in the multi-ethnic study of atherosclerosis. Am. J. Prev. Med. 2013, 45, 158–166. [Google Scholar] [CrossRef]

- Ref USA. 2018. Available online: http://resource.referenceusa.com/ (accessed on 26 February 2019).

- National Organic Farmers Association-Vermont (NOFA-VT). Available online: https://nofavt.org/ (accessed on 26 February 2019).

- Washington State Farmers Market Association. Available online: http://wafarmersmarkets.org/ (accessed on 26 February 2019).

- Google Maps Application Programming Interface (API). Available online: https://developers.google.com/maps/documentation/javascript/reference/geocoder#Geocoder.geocode (accessed on 26 February 2019).

- BatchGeo. Available online: https://batchgeo.com/ (accessed on 26 February 2019).

- ARC GIS. Proximity Analysis [Commonly Used Tools]. Available online: http://desktop.arcgis.com/en/arcmap/10.3/analyze/commonly-used-tools/proximity-analysis.htm (accessed on 26 February 2019).

- Zepeda, L.; Deal, D. Organic and local food consumer behaviour: Alphabet Theory. Int. J. Consum. Stud. 2009, 33, 697–705. [Google Scholar] [CrossRef]

- Sirieix, L.; Delanchy, M.; Remaud, H.; Zepeda, L.; Gurviez, P. Consumers’ perceptions of individual and combined sustainable food labels: A UK pilot investigation. Int. J. Consum. Stud. 2013, 37, 143–151. [Google Scholar] [CrossRef]

- Pinchot, A. The Economics of Local Food Systems: A Literature Review of the Production, Distribution, and Consumption of Local Food; University of Minnesota, Extension Center for Community Vitality: Duluth, MN, USA, 2014; Available online: https://conservancy.umn.edu/bitstream/handle/11299/171637/2014-Economics-of-Local-Food-Systems.pdf?sequence=1 (accessed on 26 March 2019).

- Paul, M. Farmer Perspectives on Livelihoods Within Community Supported Agriculture. Economics Department Working Paper Series, Paper 212. 2016. Available online: http://scholarworks.umass.edu/econ_workingpaper/212 (accessed on 26 March 2019).

- White, M.J.; Pitts, S.B.J.; McGuirt, J.T.; Hanson, K.L.; Morgan, E.H.; Kolodinsky, J.; Seguin, R.A. The perceived influence of cost-offset community-supported agriculture on food access among low-income families. Publ. Health Nutr. 2018, 21, 2866–2874. [Google Scholar] [CrossRef]

- Izumi, B.T.; Higgins, C.E.; Baron, A.; Ness, S.J.; Allan, B.; Barth, E.T.; Smith, T.M.; Pranian, K.; Frank, B. Feasibility of using a community-supported agriculture program to improve fruit and vegetable inventories and consumption in an underresourced urban community. Prev. Chronic Dis. 2013, 10, E136. [Google Scholar]

- Bailey, J. Regional Food Systems in Nebraska: The Views of Consumers, Producers and Institutions; Center for Rural Affairs: Lyons, NE, USA, 2013; Available online: http://files.cfra.org/pdf/ne-food-systems-report.pdf (accessed on 26 March 2019).

- Van Berkum, S.; Dengerink, J.; Ruben, R. The Food Systems Approach: Sustainable Solutions for a Sufficient Supply of Healthy Food; No. 2018-064; Wageningen Economic Research: Den Haag, The Netherlands, 2018; Available online: https://knowledge4food.net/wp-content/uploads/2018/10/180630_foodsystems-approach.pdf (accessed on 28 March 2019).

- Global Harvest Initiative. GAP Report: Measuring Global Agricultural Productivity. 2015. Available online: https://www.globalharvestinitiative.org/GAP/2016_GAP_Report.pdf (accessed on 28 March 2019).

- Pilgeram, R. The only thing that isn’t sustainable…is the farmer: Social sustainability and the politics of class among Pacific Northwest farmers engaged in sustainable farming. Rural Soc. 2011, 76, 375–393. [Google Scholar] [CrossRef]

- McGuirt, J.T.; Sitaker, M.; Jilcott Pitts, S.; Ammerman, A.; Kolodinsky, J.; Seguin, R. A mixed-methods examination of the geospatial and sociodemographic context of a direct-to-consumer food system innovation. J. Agric. Food Syst. Commum. Dev. under review.

| Farm Fresh Food Box | Farm Fresh Foods for Healthy Kids | |||

|---|---|---|---|---|

| Demographic Characteristics | Vermont | Washington | Vermont | Washington |

| Population Range | 1057–2321 | 461–952 | 690–2309 | 755–1860 |

| Mean [Standard deviation (SD)] | 1750 (641) | 740 (252) | 1376 (745) | 1307 (553) |

| Median Age Range | 38–47.4 | 37.5–50.7 | 29–54 | 26–38 |

| Average (SD) | 42.5 (4.7) | 45.8 (7.2) | 38 (9.6) | 31 (6) |

| Median HH Income Range | $50,662–$93,281 | $24,830–$100,735 | $20,284–$66,938 | $35,083–$52,708 |

| Average (SD) | $69,949 ($21,595) | $66,438 ($38,477) | $45,972 ($18,374) | $42,313 ($9228) |

| % H.S. Graduates Range | 10.0–20.0 | 12.0–22.0 | 9.0–23.0 | 6.0–27.0 |

| Average (SD) | 14 (5.3) | 16 (5.3) | 16.4 (5.7) | 15.7 (10.6) |

| % Minority population Range | 3.0–6.0 | 5.0–26.0 | 0.0–51.0 | 9.0–27.0 |

| Average (SD) | 5.0 (1.7) | 12.7 (11.6) | 14.6 (20.7) | 18.0 (9.0) |

| % Living in Poverty Range | 2.7–5.4 | 0.0–12.0 | 2.7–51.8 | 15.7–25.6 |

| Average (SD) | 4.2 (1.4) | 4.8 (6.3) | 19.3 (18.9) | 25.0 (10.0) |

| % HH receiving SNAP Range | 3.0–25.0 | 3–40.0 | 5.0–56.0 | 14.0–43.0 |

| Average (SD) | 12.3 (11.4) | 14.3 (22.3) | 25.6 (21.1) | 31.0 (15.1) |

| Transportation Environment | Vermont | Washington | Vermont | Washington |

| Walk Score Range | 24–44 | 12–20 | 4–66 | 21–69 |

| Average (SD) | 34.3 (10.0) | 17.0 (4) | 27 (24.5) | 44 (24.1) |

| Transit Score Range | 0 | 0 | 0–39 | 0–27 |

| Average (SD) | 0 | 0 | 8 (17.4) | 9 (15.6) |

| % Drive to work Range | 47.1–89.6 | 70.6–93.3 | 47.1–89.6 | 75.4–95.7 |

| Average (SD) | 88.0 (5.2) | 83.6 (11.7) | 75.0 (18.7) | 83.5 (10.8) |

| Geospatial Characteristics | Vermont | Washington | Vermont | Washington |

| Farm-to-pickup (mi) | 2.1–4.2 | 0.9–9.9 | 0–14.0 | 10.3–26.5 |

| Average (SD) | 3.5 (1.2) | 5.5 (4.5) | 5.2 (7.1) | 17.9 (8.15) |

| # SM within a 2 mi radius | 0–2 | 0–3 | 0–5 | 4–7 |

| Average (SD) | 0.7 (1.2) | 1.0 (1.7) | 1.6 (2.1) | 5.0 (1.7) |

| Pickup to Supermarket | 0.2–6 | 4.1–18.3 | 0.5–8.4 | 0.9–1.4 |

| Average (SD) | 2.3 (3.2) | 9.4 (7.8) | 2.8 (3.2) | 1.1 (0.3) |

| # FM within a 2 mi radius | 0–1 | 0 | 0–5 | 0–2 |

| Average (SD) | 0.3 (0.6) | 0 | 1.2 (2.2) | 1.0 (1.0) |

| Pickup to FM (miles) | 0–38 | 4.2–19.4 | 0.3–16.7 | 0.8–4.5 |

| Average (SD) | 18.5 (19) | 9.8 (8.4) | 6.3 (7.2) | 2.2 (2.0) |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sitaker, M.; McGuirt, J.T.; Wang, W.; Kolodinsky, J.; Seguin, R.A. Spatial Considerations for Implementing Two Direct-to-Consumer Food Models in Two States. Sustainability 2019, 11, 2081. https://doi.org/10.3390/su11072081

Sitaker M, McGuirt JT, Wang W, Kolodinsky J, Seguin RA. Spatial Considerations for Implementing Two Direct-to-Consumer Food Models in Two States. Sustainability. 2019; 11(7):2081. https://doi.org/10.3390/su11072081

Chicago/Turabian StyleSitaker, Marilyn, Jared T. McGuirt, Weiwei Wang, Jane Kolodinsky, and Rebecca A. Seguin. 2019. "Spatial Considerations for Implementing Two Direct-to-Consumer Food Models in Two States" Sustainability 11, no. 7: 2081. https://doi.org/10.3390/su11072081

APA StyleSitaker, M., McGuirt, J. T., Wang, W., Kolodinsky, J., & Seguin, R. A. (2019). Spatial Considerations for Implementing Two Direct-to-Consumer Food Models in Two States. Sustainability, 11(7), 2081. https://doi.org/10.3390/su11072081