1. Introduction: The Unfolding Carbon-Based Crisis and the Rise of ‘Stranded Assets’: Pre-Cursors to Sustainable Transformations in the Energy/Agri-Food Nexus?

The 2007–2008 financial crisis and its continuing effects strengthen the need to critically explore the pathways of transformation towards sustainability and sustainable development. At the same time, as Marsden [

1] argues, the signature crisis, which in fact was a ‘combined retrenchment of the food, fuel, finance and fiscal crisis’, also questioned the ability of the sustainability concept to address it, let alone resolve it. Since then, the concept has been contested in theory, as well as appropriated in practice. Therefore, today we are at what seems to be the crossroads of these debates. First, we see alternative and transformational theoretical “roads”, namely eco-economic and bioeconomy approaches, and the practical “roads” between eco and bio-economies. However, after a decade of capital and state crisis, this crossroads is ever more contested, connected, intertwined and path-dependent, thus potentially giving way to both transformational change on the one hand, although with serious carbon-based ‘lock in’ tendencies on the other. In this paper, we explore this crossroads and a possible ‘tragedy of the horizons’ [

2], as it offers an opportunity to re-conceptualise, strengthen and re-ground our understanding of potential transformation, especially in the critical nexus of energy and agri-food arena.

In 1992, the International Conference of Parties on Climate Change took place, marking the recognition that global natures are being affected and need to be protected, for human and non-human species survival, rather than being continually exploited. However, this would involve a step back from practices that have arguably benefited humans for the last two centuries in doing so, requiring Heads of States to implement changes. Since then, there has been significant progress in technology, adoption of new practices, reductions of pollution, but there is still a long way to go to achieve a transition to a post-carbon emission world, despite the urgency. This progress has been stalled due to many factors, but in this paper, we want to emphasise the economic Janus-faced interest in climate change negotiations. To put it in simple terms, cutting emissions, the closing down of coal power plants, and switching to renewables leads to losses of short-term profits without which an investment in green energy might be challenging. The most developed or fastest growing countries still owe their financial progress (as well as regress) to polluting industries and the wealth generated through market forces.

Despite a growing understanding and agreement on anthropocentric causes of global climate change and resource depletion, the tensions between the progress towards a low or zero-carbon world versus the business-as-usual economic development model have been evident in a lack of firm agreement in climate negotiations between Heads of States. Only in December 2015, during the 21st Conference of Parties (known as COP21), was an agreement reached between many of the top national polluters signaling that “business as usual” cannot continue. COP21 is a significant step regarding bringing forth a more precise, long-term signal and direction to Heads of States spelt out in 5 provisions: five year plans and reporting; adaptation; loss and damage; finance; transparency; and capacity building. On 22 of April, 2016, 175 parties (174 countries and the European Union) signed the Paris Agreement. The agreement entered into force on 4 November 2016, thirty days after the date on which at least 55 Parties to the Convention, accounting in total for at least an estimated 55 % of the total global greenhouse gas emissions, signed it [

3].

While the Paris Agreement is being actioned, the emerging literature [

4,

5,

6] highlights the concept of ‘stranded assets’—a possible effect of regime shift from oil to renewables. Stranded assets emerge as a result of new technologies being implemented which then cause a devaluation of existing carbon-based assets which were once dominant. The regime shift toward a post-Paris 2015 “world” might mean that owners and traders of hydrocarbon assets (conventional and unconventional oil, gas, and coal) begin to devalue or experience a devaluation of their assets. ‘Stranding’ of assets is predicted to be acute, because of circulation of hydrocarbon assets in the world economy, which when at risk impacts upon rural and urban places, political decisions, government spending and all productive industries depending on oil, such as the food sector and especially meat production. However, not only is the concept being contested [

7], it is almost invisible in the current sustainability research and literature. We aim to highlight the potency of this concept in material terms (risks and impacts) and in strengthening multidisciplinary research and furthering critical thinking about sustainability.

Research Methods and Design.

This paper outlines post-Paris 2015-18 events and focuses on the concept of stranded assets and the emerging contested dynamics in the agri-food-energy nexus. Considering the fast-changing nature of the post-Paris 2015 “world”, we draw our arguments from systematic reviews of academic, trade literature and news media conducted between 2015 and 2018.The evidence and events described in this paper come from the trade publications and major news outlets with a focus on changes with regard to energy as a result of COP21. Considering that the paper is only attempting to “make sense of” the fast-changing world of finance and politics, we have deliberately resisted using pre-defined frames of analysis. Instead, we aimed to paint the picture. However, as the news was unfolding over the years, we noted the complex co-evolutionary shifts in the policy of both countries and companies.

The paper pursues the following structure, which traces and explores this process of competitive co-evolution. First, and arising from our systematic reviews of literatures, trade and media reports in the field, we assemble a schematised conceptual model which explores the juxtapositioning of these trends and contestations (

Section 2). This raises new questions concerning what the potential for new options and spatial re-configurations will be emerging as we move through this highly contested period of transformation. Second, we examine the particular rise in carbonised ‘stranded assets’ as potential push factors for transformations and, indeed, reducing the ‘lock in’ and ‘spatial fixing’ tendencies in carbonised systems of agri-food and energy production. Third,

Section 4 and

Section 5 lead into an analysis of the dialectics between carbonised and post-carbonised geo-politics and political ecologies. This demands, it is argued, that more needs to be done to shift investments into renewables (

Section 6), and that the global financial sector is a critical bellwether in this regard. Finally, in conclusion (

Section 7) we critically consider and posit the possibilities for a more distributed agri-food/energy nexus in this contested landscape, suggesting that this nexus approach coupled with a critical political-ecological perspective is of significant value in further charting and indeed mobilising the transformations in the enery/agri-food/energy nexus, and in generating the institutional capacities for this to become far more embedded.

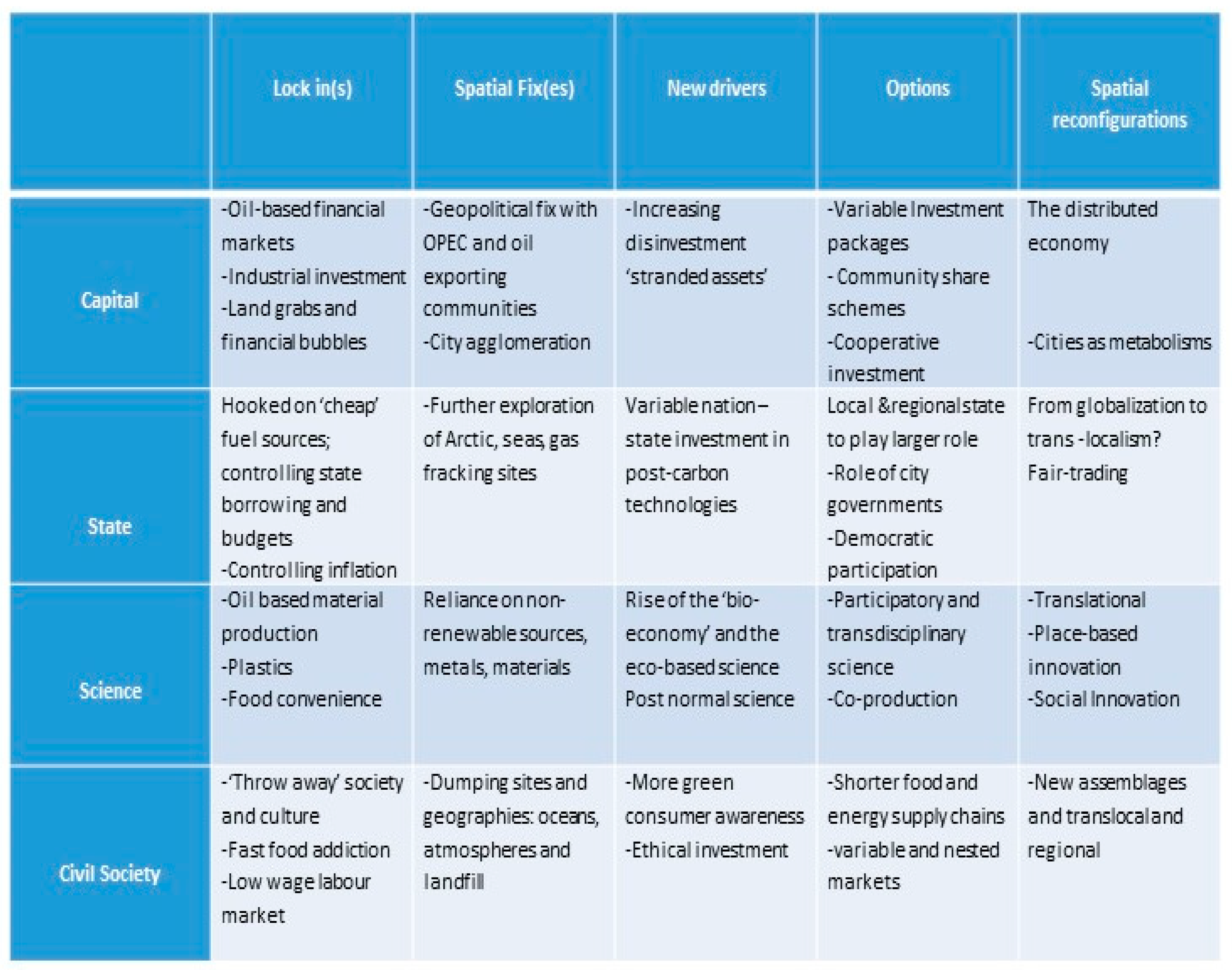

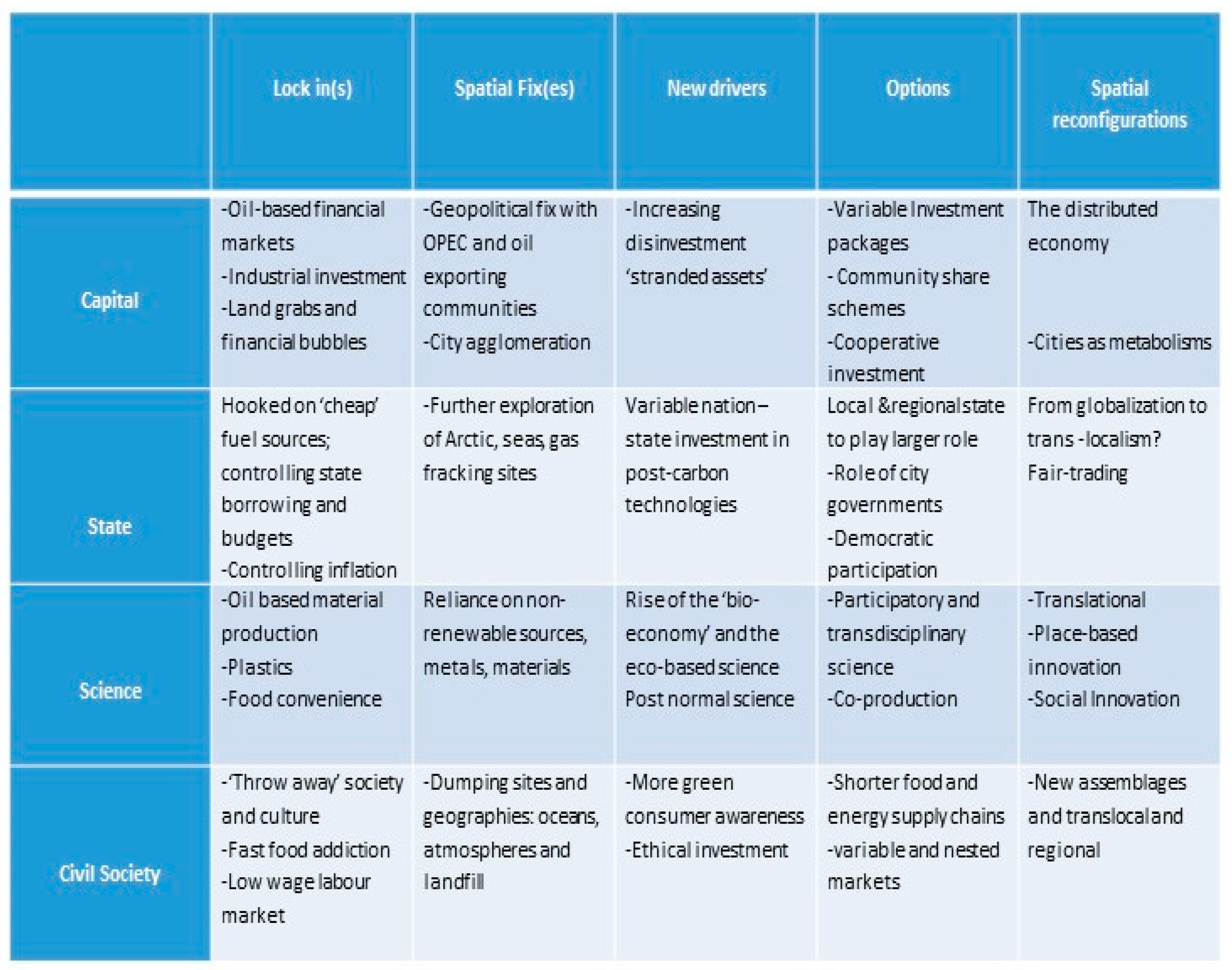

2. A Conceptual Model: The Dialectical Relationships between Carbon-Based ‘Lock-In’ and New Drivers and Spatial Re-Configurations

Some of the major changes which we will delineate in this discussion are identified in summary form in

Box 1. This attempts to summarise some of the current key dynamics regarding the agri-food/energy nexus. The dynamics presented in

Box 1 add to the persistent and new uncertain-by-nature challenges within agri-food sectors across the globe, as set out by Thompson et al. [

8] over 10 years ago.

This extends Marsden’s earlier arguments on the importance of the four pillars of sustainability: ‘place, reflexivity, distributed eco-economy and re-financialisation’ [

1,

9]. We argue that transformations towards sustainability in the energy/agri-food nexus need to be critically considered in the post-2007/8 political economic/ecological context of financial, fiscal, food and fuel crises that are both more profound and more volatile. This is currently leading both to the re-enforcement of existing conventional carbon regimes, as well as to significant and potentially transformative reactions to them. In the midst of these different relations is a dynamic of financialisation, growing vulnerability and common questions for more autonomous alternatives involving taking control of financing and developing localised and distributed systems of food and energy provision. As we shall see, this process of competitive co-evolution—that between carbonised and non-carbonised practices—is nowhere more explicitly expressed than in the energy/agri-food nexus.

Box 1. Key nexus dynamics in energy and agri-food. Source: developed by the authors.

Pressures on the dominant carbon—based regime.

Intergovernmental pressure to reduce CO2 emissions/SDGs.

More difficulty in sourcing carbon assets and the financing thereof.

Overall financialisation of energy and food systems creating ‘lock-in effects’.

More financial volatility and short-termism in investment.

Rising household costs and costs of production for small suppliers.

More intensive searches for ‘spatial fixes’ [

9] in the form of ‘land-grabs’.

Rise of renewable energy and food systems provision.

Attraction of new investments (despite gov’t actions in many cases).

Centralisation versus distributed debates about provision, control and democracy.

The rise of the bio-economy and further growth in stranded carbon-based assets and investments.

Agri-food system transformations follow energy transformations historically.

Following this, our conceptual model (see

Figure 1) postulates the juxtaposition between the ‘lock-in’ (and spatial effects) associated with the continuing carbon-based model of development explored in this paper and the emerging post-carbon developments. The argument is that both of these conditions are currently continuing at the same time; and that this co-evolution is becoming a macro-dialectic necessary for further conceptualisation and critical empirical interrogation. One implication of such an approach is that for real transformations to occur in the energy/agri-food nexus, we need to assess how shifts occur both in the established lock-in effects and in the rise of post-carbon alternatives. That is, across and within the boxes identified in

Figure 1. We are witnessing changes in the political ecologies of capital, state, science and civil society arena (i.e., on the vertical axis of our

Figure 1), which are challenging existing spatial and temporal fixes and configurations of conventional and carbonised systems of resource exploitation and production (i.e., the dynamic components on the horizontal axis). In particular, we document below how increasing investments are being made in energy renewables and that we are also witnessing the rise in ‘stranded assets’ in carbon-based financial markets.

As McCarthy [

10] argues, ‘a transition to profoundly different geographies of energy production, transmission and consumption could afford powerful political possibilities’. Recent work has suggested that energy production is, in various ways, becoming more spatially extensive, dispersed and visible, and hence more contested and overtly politicised [

11,

12]. Key issues here are likely to include ‘structures of ownership and control, the degree of centralisation, and the extent to which the focus on abstract “energy” as opposed to the use values derived from energy use. In short, a thorough overall of the energy system could and should provide multiple openings for re-thinking, rather than merely reproducing, our political-economic system’ [

10].

Clearly, these shifts have wider both direct and indirect implications for the energy-agri-food nexus [

1]. Frantal and Martinat argue that [

13]:

‘Renewable energy sources are regarded as spatially dispersed and difficult to collect, thereby requiring substantial land resources in comparison with conventional energy resources. Moreover, they are mostly undertaken in rural areas hitherto unaffected by large-scale industrial development. The problem of balancing the advantages and disadvantages, both real and perceived, of projects (taking into account such diverse considerations as, on the one hand, global climate issues, the energy strategies of national governments, regional development policies, and local community benefits, while also on the other hand stressing the significance of nature and landscape protection, calling for a restoration of productive farming, and the preservation of local cultural identity) often provokes political and social conflicts arising from differing values and conceptions of land-use’.

One spectre might be new spatial fixes of concentrated investment involving large-scale geographies of renewable energy production, distribution and consumption, involving powerful new rounds of investment in, and claims on rural areas for production and provision, on scales well beyond existing rounds of speculative ‘land grabs’. ‘In a capitalist world, those claims and their impacts would likely to fall disproportionately on rural areas, where land values are lowest and existing users often have less power and fewer formal land rights’ [

10]. In this context, rural land and indeed its multi-functional biospheric resources could become a new battlefield for contested control, as new capital and state interests attempt to appropriate and capture the rights to control these renewable resources. This could lead to the accelerated further appropriation and enclosure of biospheric and global resource ‘commons’.

This is McCarthy’s main question: will the rise of post-carbonised energy systems lead to a renewed and more intensified ‘spatial fixing’ process in neo-liberalised but monopoly capitalism? We wish to complement this concern here by additionally addressing the alternate question. Does the rise of post-carbonism in the energy/agri-food nexus provide opportunities for the co-evolution of alternative, more distributed and post-capitalist forms of sustainable production and consumption to take hold? It is important, we can argue, not to see these two questions as starkly and mutually opposing or in binary terms. Rather, they are both at the centre of a revised and critical political ecology of sustainability [

14,

15].

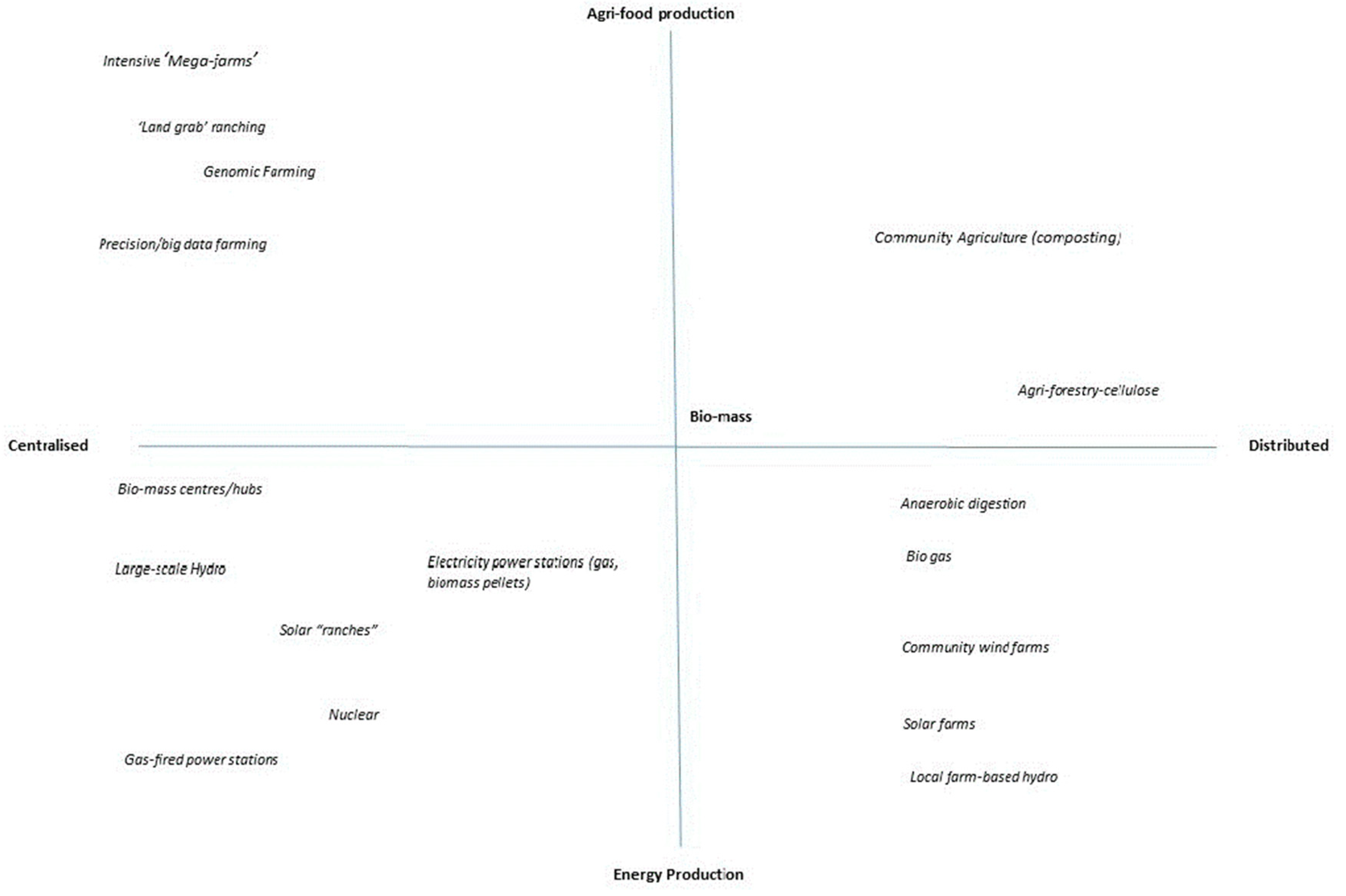

It may be, as we at least begin to outline in this paper, with an examination of both models, that both tendencies are in display over different time and space vectors. In

Figure 2, we attempted to conceptualise the emerging landscape of energy and food. In particular, we wanted to draw attention to where within this landscape, characterised by distributed and centralised systems of governance, some of the examples of food and energy production fall into. As we see and summarise in

Figure 1 and

Figure 2 then, both the tendencies to continue to spatially fix both carbonised and renewable concentrated capital and production continues, at the same time and through different spatial and temporal logics, alternative and more distributed transformations are also indeed occurring.

A major question thus becomes: what will be the potential for new options and spatial configurations emerging as we move through this highly contested period of transformation? Will it lead to new rounds of centralised capitalist ‘lock-in’ and spatial fixes (see

Figure 1), for instance, appropriating even more global frontiers (like rural and ocean spaces)? Or will the political and social implications of the process of transformation itself lead to civic and state-based interventions which push for more decentred and distributed power and spatial reconfigurations?

In the agri-food sector and the agri-food/energy nexus, we are seeing, we argue here, the beginnings and emergence of new power and spatial configurations, both in and through the rise of micro and community energy schemes, and alternative food networks and assemblages (see

Figure 2). In the UK (2018), it is estimated that over a third of all farmers are, in addition to foods, also producing some form of renewable energy in the form of solar, bio-gas, wind turbines and local hydro capture [

16,

17]. This is not ‘business-as-usual- capitalism’, and it challenges both the ‘lock-in’ tendencies and spatial fixes associated with carbon-based agglomerative capitalism. Instead, it creates new nested markets and re-localised production niches using distinctive and more distributed organising principles. This is a new dynamic in post-carbon capitalism, and it is, as we shall explore in the rest of this paper, affecting the energy/agri nexus. Clearly, at a generalised level, there are a series of ‘push’ and ‘pull’ factors at work, and these will be explored in the following sections.

3. The Rise of Stranded Assets: Financial Push Factors towards Transitions and Reducing ‘Lock-In’ Effects

As new technologies emerge, and new companies outcompete incumbents, a relentless process of ‘creative destruction’ results in stranded assets [

4]. To strand assets in financial terms means to prematurely write off, devalue or convert them to liabilities. Assets can become stranded due to many factors, from environmental protest and policy, through to social to regulatory change. However, due to a connection of assets to a broader system (or a network) assets are not left out, abandoned or cancelled out completely.

The concept of stranded assets is a contested one, as it assumes that sooner or later, hydrocarbon assets will become ‘stranded’ because of pressure from civic society (divestment), physical (un)availability of conventional and unconventional hydrocarbons, the emergence of alternative technologies, and new state policy causing economic shifts (disinvestment). This means that they will be prematurely written off or unwanted in financial terms, therefore affecting the economy, which still rests on the performance of hydrocarbons in stock exchanges. A poor performance, as history shows [

18], means that investments, i.e., injection and circulation of capital (in whichever form) will be held up, thus further impacting a financial system built on an assumption of continuous growth and predictability of assets.

Currently, the most prominent rejection (or at least denial) of this concept comes from the established oil and energy industry (and investors), who still argue that while societies support sustainable pathways, they also need to exploit carbonised energy, which at the moment will not be entirely replaced by renewables. The oil industry assumes that overall energy demands will not subside anytime soon, thus investing can continue irrespective of policies. The industry also recognises that governments, being reliant on oil tax revenues, might change or delay policy instruments such as heavy taxing of the oil industry and tax breaks for renewables [

7]. Thus, even though high-profile financiers, for example, Mark Carney of Bank of England, are warning that stranded assets are becoming a reality [

2], the concept is continually denied and resisted. Indeed, there should be no denial on our part that oil holds a strong bearing on the world economies. We also, do not deny that a rising and wealthier global population will need more energy. To accept that refined oil is a source of energy and income, does not mean rejecting the stranded assets concept. Instead, we need to accept that sustainable futures will have to reconcile the existence of oil and its impact, especially on political decisions. Thus, stranded assets need to be seen in the context of:

- a)

The highs and peaks of hydrocarbons as a traded commodity;

- b)

The (un)availability of conventional and unconventional hydrocarbons;

- c)

The physical impact of climate change—floods, droughts, fires, etc.;

- d)

Societal pressures and political instabilities.

The stranded assets concept extends beyond oil, as the process of prematurely writing assets off be it financial or physical, is not bound to one industry. Industrialised carbonism has interconnected industrial sectors, not least the agri-food and energy sectors. It thus needs to be emphasised that agricultural and agri-food assets and processes, being linked to the oil industry and classed as a high GHG emitter, can be equally vulnerable to stranding by the points mentioned above. Even though agriculture is not targeted in formal COP21 negotiations, the parties to the Paris accord agreed to ‘recognise the fundamental priority of safeguarding food security and ending hunger, and the particular vulnerabilities of food production systems to the adverse impacts of climate change’ [

19]. Article 2 of the accord writes:

‘This Agreement, in enhancing the implementation of the Convention, including its objective, aims to strengthen the global response to the threat of climate change, in the context of sustainable development and efforts to eradicate poverty, including by increasing the ability to adapt to the adverse impacts of climate change and foster climate resilience and low greenhouse gas emissions development, in a manner that does not threaten food production’.

Article 2 has been criticised for not giving specific measures or attention to the agri-food sector. Nevertheless, the meat industry, as the

Global Meats reports suggests, is threatened by the above accord [

20], arguing that it cannot be treated like hydrocarbon industries. However, the multiplex stranding process in the agri-food sector can occur irrespective of direct policy pressures. As a result of climate change, climate change negotiations and instability of hydrocarbons the paradigm will thus shift for the agri-food system too. The agri-food system will experience its direct pressures from the environment as well as a local and global society. Exposure to assets that will become directly or indirectly “stressed” will be highest where the value of such assets is high (e.g., environmental pressure and vulnerability) and the vulnerability to drivers (physical or economic) is also high [

5].

Stranding of assets under a direct or indirect paradigm shift is, therefore, a concept that cannot be disregarded, as it is closely related and linked to more than one sector, concern and place. In addition, in the agri-food sector, these re-financialised processes are beginning to act as essential drivers for paradigm change towards more post-carbon agri-food/energy practices (among those we witness around agro-ecological practices: the rise of place-based and more distributed markets, and consumer as well as producer–led solidarity economies).

4. Climate Change Negotiations, Paris, 2015—A Paradigm Shifter.

The Conference of Parties (henceforth COP) started in 1995 with the aim of beginning implementation of the United Nations Framework Convention on Climate Change (also known as the “Rio Conventions”). Since then, various efforts have been made to achieve reduction of unsustainable practices at local, national and international levels. Consecutive COPs addressed carbon emissions through a series of protocols and agreements, with the latest being the “Paris Agreement”.

Although it is deemed too weak to achieve the pledges, it marked an era of global action. Until now, parties of the conference, i.e., member states, have been in disagreement over which states and in what ways they are to mitigate emissions and adapt to climate change. Considering that the wealth of states has been resting on hydrocarbon industries, the reluctance to scale down the profits these industries create is evident in the lack of firm and legal action, let alone reductions of carbon emissions. The Paris agreement, as the former President of the United States, Barack Obama, noted, ‘is a turning point’ [

21], because at last many nations recognised that action needs to be taken. Many pledges have been made, for example, to keep global temperatures “well below” 2.0 °C (3.6 °F) above pre-industrial times and “endeavour to limit” them even more, to 1.5 °C; to limit the amount of greenhouse gases emitted by human activity to the same levels that trees, soil and oceans can absorb naturally, beginning at some point between 2050 and 2100; to review each country’s contribution to cutting emissions every five years, so they can scale up to the challenge; and for rich countries to help poorer nations by providing “climate finance” to adapt to climate change and switch to renewable energy [

22].

However, the essential notion of the agreement—emissions targets—remains voluntary. Emissions targets are spelled out in Intended National Determined Contributions (INDCs), which have been disclosed [

3], but they are not legally binding. In 2015, Carbon Action Tracker [

23] calculated that the pledged targets, even if achieved, would curb warming at only 2.7 degrees Celsius, not at 2.0 degrees Celsius (as promised in the agreement). As of 2018, Carbon Action Tracker writes [

24] ‘little to no progress has been detected globally on climate action either, with the total global effect of currently implemented policies in countries expected to lead to warming of 3.3°C by 2100, which is still above the Paris Agreement commitment level, the emission targets are still far too low, voluntary and non-binding. Only a strong regulatory framework and clear signals to investors can help to curb global warming and contribute to achieving sustainable development goals such as a reduction of poverty and inequality, responsible consumption and production, and affordable and clean energy, to name but a few. However, as we show in the next section, the signals from the policy makers are mixed.

5. Carbon Liquid ‘Lock-In’ (Despite the Risks).

Oil, as Labban [

25] puts it, is both a material and fictitious entity that flows underground and seeps through the ground. It is extracted and refined, runs through car engines and many of our everyday products [

18] but is also a financialised traded stock on market exchanges. Whether oil is at its peak, in demand or high supply, it is still traded and therefore impacts severely on the world hydrocarbon economy. Investors will be making decisions based on oil performance as a fictitious entity that is influenced by the society-environment-geopolitics-economy nexus. In practice, it is manifested in an acknowledgement of big oil producers and big investors of climate change, but without a shift in practices. BP [

26] and Exxon, in their 2016 outlooks [

27], stated that oil would be in demand and that performance of these companies will remain intact. Big investment banks also acknowledge climate change and social pressures, but as long as the oil is traded on the markets and banks are having connections to oil, the logic of investment or disinvestment will be governed by market forces. For example, oil prices in 2016 were at their lowest due to a slowdown in China’s growth. Low prices are bad for oil-dependent economies—especially the Organization of Petroleum Exporting Countries (OPEC). With low prices and low return, investors are cautious and waiting for political movement. However, political campaigns are tied to economic performance on markets, so who is to give a signal?

During the COP21, Bill Gates, a founder of Microsoft, a leading investor and trend-setter/opinion-maker, created a coalition of smart investors to ‘develop effective and creative mechanisms to analyse potential investments coming out of the research pipeline, create investment vehicles to facilitate those investments, and expand the community of investors [

28]. Meanwhile, Warren Buffet also a leading opinion-maker, philanthropist and investor, in his position paper, wrote:

‘As a citizen, you may understandably find climate change keeping you up nights. As a homeowner in a low-lying area, you may wish to consider moving. However, when you are thinking only as a shareholder of a major insurer, climate change should not be on your list of worries’ [

29].

Unlike coal or gas, oil has contributed to the fastest economic growth, and while coal mining is being decommissioned, oil and its derivatives still rattle around world markets hour by hour. Since the 1900s, when oil replaced kerosene as a source of light and was found to be useful for energy production, the world has never looked the same [

16]. The geography of oil was not only limited to the young North American nation—the USA—but also to countries whose destinies changed depending how much crude oil was left. Soon it was realised that the USA, Canada, the Middle East, Russia, Venezuela, Nigeria, and Peru, but also stateless oceans, hold vast reserves of extractable crude oil (hereafter conventional oil). So the fight over the rights to those reserves took place, with War World One being one the first drastic effects.

Today, the Middle East, and in particular, the Kingdom of Saudi Arabia, is the largest “owner“ of (as yet) undepleted oil reserves. Due to the abundance of oil in the countries mentioned above, economic development was built solely and exclusively on oil as an exportable (in barrels) and tradable (on stock markets) entity. For example, the USA’s economic power was built on its oil, which reached its peak in around the 1970s. The UK’s economic power was built on its exclusive access to Middle Eastern oil, which was cut by rising independence among Arab nations. South American (SA) states supplied the USA, but the contracts ceased to return benefits to SA. Each time one’s access to oil changed, power relations shifted, and with it the price of oil and the collapse of stock markets. To alleviate this, states whose economies rest on private oil giants (Exxon, Shell, BP) are now also seeking alternatives in unconventional oil—tar sands, shale gas, fracking, offshore oil, and other pockets of inaccessible oil.

Hydrocarbon economies are therefore economies that rely on conventional or unconventional oil as a source of their income. So while there is a need to cut emissions and move to renewable energy, there is a contradiction between two necessities: the first being for a shift away from carbon, and the second being related to and dependent on access to a 100-year-old source of income. The most interesting post-Paris 2015 examples of this tension are presented below.

On the 18th of December 2015, a few days after showing support for the COP21, the former President of the United States (Barack Obama) ended 40 years of U.S. crude oil export limits by signing off on a repeal passed by Congress [

30] in exchange for a

$1.1 trillion spending measure [

31]. As a result, tax breaks for renewable projects were secured, but at the same time, a repeal allowed “big oil” to remain in operations. In other words, the USA’s global pledge and support of Climate Change negotiations had to be re-negotiated at home, where the oil lobby remains strong. It was a trade-off between two paradigms—environmental and carbon-economic. However, in this case, the USA’s environmental paradigm (here tax breaks for renewables) was dictated by those who were in power to approve spending measures under economic conditions, i.e., that crude oil export limits will end. In March 2016, another supporter of the COP21, India’s Prime Minister, announced a new oil and energy policy which allows for an increase in domestic production [

32]. In April 2016, the Kingdom of Saudi Arabia (KSA) announced ‘it will sell off hundreds of billions of dollars’ worth of American assets held by the Kingdom if Congress passes a bill that would allow the Saudi government to be held responsible in American courts for any role in Sept. 11, 2001, attacks” [

33]. KSA also announced to add millions of barrels of oil at any time thus causing further oversupply, and consequently further decrease of oil prices which would not affect KSA but impact on world economy and environment as well as roll out a comprehensive national plan for the post-oil era [

34]. Lastly, in June 2017, a newly elected president of the United States withdrew from the Paris Agreement, thus reversing the pledges the United States previously made [

35].

In Europe, similarly, trade-offs have been made. For example, having made pledges at COP21, Europe ended decades of sanctions on Iranian oil exports in exchange for the end of Iran’s nuclear (military) programme [

36]. While the end of nuclear power programme is significant, geopolitically speaking, it shows that oil has gained leverage in highly politicised negotiations for global and regional (Middle East) peace. While Iran benefits from new oil exports and tensions in the region will be stabilised, global environmental pledges were sacrificed.

In the UK, the government has also made U-turns. In April 2016, the government has backed out from £1 billion worth of funding for carbon capture storage (CCS) companies [

37]. CCS is vital in reaching climate change targets while allowing to provide energy and keeping companies in business. Without the investment into renewables and total disinvestment in hydrocarbons, stranded assets will be realised sooner sending markets to disarray, thus further jeopardising a sustainable (financial and environmental) future. In June 2016 on the other hand, the UK’s Secretary of State for Energy and Climate Change announced a new, ambitious carbon budget (not yet made into a statutory instrument) [

24], reducing carbon emissions by 57% by 2030 with respect to 1990 levels [

38]. However, only a month later, the UK’s new Prime Minister (Mrs Theresa May, Conservative) abolished the Department of Energy and Climate Change by merging its mandate with the Department for Business, Energy and Industrial Strategy [

39]. Environmentalists and fellow politicians highly criticised the PM’s decision. Only two months later, and despite criticism regarding costs to the taxpayer (which might reach up to £35 billion) and calls to opting for renewable energy [

40], the UK’s PM gave the green light to the re-development of a nuclear power plant. Hinkley Point C is planned for completion in 2025, and it is said that it will provide 7 percent of Britain’s total electricity needs [

39]. Later in 2017, the British Government announced a Clean Growth strategy for decarbonising all sectors of the UK by focusing on investment in research and innovation, smart system plans, district heat, building regulations, electric cars, and carbon capture storage [

41].

6. The Rise of Renewables as a Necessity and Conditions for Change

We have already painted a very volatile picture; that is, political leaders supporting COP21 while compromising their stance due to their political and economic reliance on financialised hydrocarbons. To reverse this trend, firstly, a clear signal to investors needs to be sent, one that goes in hand with the decision-making of investors. In other words, investors first need to be assured that renewables are not too risky and unprofitable. A study conducted for Bloomberg’s energy finance report [

42] showed dollar investment globally growing in 2015 to nearly six times its 2004 total, and a new record of one-third of a trillion dollars, despite influences that might have been expected to restrain it. The study reports that ‘clean energy investment surged in China, Africa, the US, Latin America and India in 2015, driving the world total to its highest ever figure, of

$328.9 bn, up 4% from 2014′s revised

$315.9 bn, and exceeding the previous record, set in 2011, by 3%’ [

42].

Market analysts on the other hand warn that investing in oil might be tricky, but bets will be continued on the rise of oil, which oil producers believe in and promise to deliver until politicians introduce measures against it. However, as of 2016, no such measures had been introduced; rather, the opposite was true. Governments, along with oil giants, as mentioned in the previous sections, squeezed and explored the last drops of conventional and unconventional oil (which is not at peak, but rather in abundance). Others, however, warn that the shale-shale boom (unconventional oil) in the USA was founded on junk debt, similar to previous economic crises, thus warning of a new financial catastrophe. One example that Bloomberg used is the following:

“Energy XXI owes

$150 million to banks including Royal Bank of Scotland Group Plc, UBS Group AG and BNP Paribas SA, among others. S and Ridge has fully drawn its credit line with banks including Barclays Plc, Royal Bank of Canada and Morgan Stanley, according to data compiled by Bloomberg. The banks declined to comment.” [

43].

With this in mind, we can further emphasise that COP21 might not be the only reason for stranded assets, but rather, the nature of the increasingly volatile and financialised market itself, due to its mechanisms and undisclosed operations, leads to a limbo, and thus to potential financial disaster. Lloyds of London Insurance, the world’s oldest insurance market, has become the latest financial firm to announce plans to stop investing in coal companies [

44]. Other insurance firms, such as Aviva, Allianz, Axa, Legal and General, Scor and Zurich followed suit. Unfriend Coal [

45] reports that in the past two years about £20bn has been divested. This is starting to make good business sense for insurers, faced with hurricanes, wildfires and flooding and yawning gaps between the insurance cost of disasters and the actual amounts insured. The gap, currently standing at over

$100 billion, a (quadrupling since the 1980s), formed a major point of discussion at the 2018 Davos meeting. Inga Beale, chief executive of Lloyds, recently said: ‘It goes beyond climate change. The broader issue is how we clean up the planet’.

Although wholesale disinvestment has not yet occurred, many investors, banks and companies are now pledging a move toward 100% renewables and disinvestment in hydrocarbons. Some of the latest pledges have been made by the large banks and trading firms—Morgan Stanley, Citigroup, Well Fargo & Co [

46]. Regarding energy consumption and purchasing of “cleantech”, telecommunications are leading the way in the pledge to rely on renewables. Analysis by Bloomberg New Energy Finance [

47] indicates that

$8 trillion—two-thirds of the total spent on new power generation capacity between now and 2040—will be invested in renewable energy technologies. In May 2016, Shell—an oil producer —also announced investments in green technology through its new division. McCallister reports that Shell ‘with

$1.7bn of capital investment currently attached to it, and annual capital expenditure of

$200m, New Energies, will be run alongside the Integrated Gas division under executive board member Maarten Wetselaar’ [

48]. Although there is a long way to go, the demand is growing in both consumption and investment in “cleantech”.

Risks will need to be redefined and understood so that they can be accounted for. Christina Figueres mentioned that soon investors would need new types of policies and risk managers, which will come under scrutiny and be audited [

49]. We can argue that climate regime change might come to resemble the more sectoral changes in animal welfare. The pig, poultry and slaughtering industry are now subject to EU animal welfare directives and regulations, and are audited and accounted for. Retailers, here, could be compared to investors (as they purchase from producers), and further demand and audit these industries. Consumers end up purchasing the products they demanded. Animal producers are then forced to comply if they wish to stay in market operation. Poorer performing producers, due to low animal welfare performance, are “weeded out”. The shift to higher animal welfare requires a change in producers’ culture and attitude, but EU- and state-driven legislation can enable and prompt this shift to occur. However, the realisation that higher animal welfare means staying in business and on top of the game equally helps, too. State intervention, then, in carbon- and especially oil-based economies could be central for guiding and re-enforcing shifts to post-carbon economies in energy/agri-food.

This takes us to the final point, which concerns a willingness to think beyond short-term financialised returns, short-termism in business, and siding with ‘business as usual’ practices, which are indeed less and less predictable. Financial cycles have shorter spans than environmental cycles. Short-termism goes against long-term goals, but what is crucial is also the culture of quick returns. It is perhaps a choice of whether to persist with a business that is characterised by ‘mature provinces in decline and fiercely contested, prices volatile, ingenuity strained, exploration pushed to the ends of the earth at spiralling cost and risk, and unforeseen competitors are inexorably taking away demand’ [

50]. The question is ‘should hydrocarbon companies ignore, deny, resist, diversify, hedge, finance, transform, or decline?’ To which he answers, ‘That strategic choice is stark, tough, and increasingly urgent’ [

50]. In other words, business-as-usual and short-termism will cease to give a return on investment.

Scholars working in stranded assets have argued that financial behaviours and tools need to be adjusted [

51], while the UNEP Inquiry [

52] calls for a sustainable financial world, which is an important starting point and worth studying further. The question that needs to be asked is whether investing in and consuming clean technology would be enough to bring a better future for the world, or whether the financial world itself would also have to be changed so that the cleantech investment stays clean. Considering the points raised in this paper, we support the findings of stranded assets teams that suggest that without a change in the financial world [

52] and a reconceptualization of the role of oil, the sustainable progress might also be equally stranded. Changes in financial investment behaviours thus need to accompany the directional changes now being witnessed in post-carbon technologies. With this in mind, we propose a reconceptualization of the issue at stake in line with Marsden’s [

1,

8] four pillars of sustainability.

7. Conclusions: Exploring the Fragmented and Contested Energy/Agri-Food Nexus

It is now generally recognised that in the power sector, at least, a major and profound transformation is taking place towards renewable sources despite the conventional ‘lock in’ tendencies also outlined in this paper. Jacobson and Delucchi [

53,

54] have suggested that it is now technically possible to generate almost all of the world’s current (12.5 Terawatts) energy needs and deal with the future growing demands (17TW) by 2030. If this transition continues—and it is our conclusion, despite countervailing tendencies, that it will—it is likely to create the needs and conditions for both radical re-investment in centralised new production and distribution systems, concentrated solar power plants (such as those now being developed in China), geothermal plants, solar photovoltaic plants, tidal turbines and other wind and wave devices. A key question, following McCarthy [

10], becomes the degree to which these tendencies lead to further concentrated or distributed systems of production and provision (as outlined in

Figure 2).

We should recognise that renewable energy sources and production practices—not unlike food production—are typically more distributed, both in their energy capture and in their material production than fossil fuel and nuclear sources. In terms of capturing and using renewable energy, it is spread over more space and time, and does not necessarily lend itself to agglomeration or concentrated systems of delivery. In short, it requires a different scalar and geographical ‘fix’, and thus also provides significant opportunities for more distributed and decentralised systems to be developed, especially on or alongside rural and agricultural, and of course marine, resources (see

Figure 2 for examples). As a result, not unparalleled in pre-industrialised peasant agricultures and practices, the very natural capture and fixing of renewable energy and multifunctional agricultures gives opportunities for place-based communities and small businesses to enter and build new markets and production systems.

In Germany, for instance [

55], by 2013, and because of the national Energiewende policy of developing renewable and phasing out nuclear and carbon energy sources, nearly half of the new installed capacity for renewables is already operated by civil society at local and community levels. As Kropp [

55] argues ‘renewable energies entail a significant re-composition of the socio-eco-technical links between landscapes, energy and society, accompanied by fierce debates on energy policy’.

Major questions and opportunities thus surround how the opportunities for municipalities and civil society organisations (especially energy cooperatives) can compete with, or indeed develop alongside, the more capital-intensive and centralised infrastructures and renewable energy companies.

Marx indeed noted that, as Kropp [

55] quotes: ‘the hand mill gives you society with the feudal lord, the steam-mill society with the industrial capitalist [

56]. One might therefore now ask what types of new oligarchies or panarchies the renewable revolution will encourage? McCarthy [

10] tends to suggest [

3], that these transformations will provide just another timely ‘spatial fix’ for the next phase of neo-liberalised and crisis-ridden capitalism, and that the current write-downs in carbon-based investments are indeed the most recent manifestations of the crisis and contradictory nature of historical capitalist development. For these scholars, then, the spectre of the energy and agri-food transition can leave industrial and financial capitalism largely intact, but now without its reliance upon its traditional carbonised resources and markets. A sort of post-carbonised corporate capitalism built upon new concentrated technologies and spatialities of capture, enclosure and production.

We argue here (see

Figure 1;

Figure 2) that both the contested energy and the attendant agri-food transformations which are now ongoing will also provide opportunities for a wider vector of (post-capitalist) eco-economic development; some of which will create the conditions for more distributed and indeed socially and spatially emancipating development. The very material nature of both renewable energy and agri-food production now relies at least partly upon distributed sourcing over space, time and nature (not least, air, water and soils). It thus requires harnessing the bio-sphere in new ways, and it places rural land and producers with new local and community opportunities. With potentially more capital moving into these post-carbon fields (quite literally), as Ritchie and Dowlatabadi [

57] go on to conclude:

‘The (divestment) movement is not about purely financial logic—it does, in our view, have the potential to change social norms around the perceived acceptability of where financial capital is located and the impacts associated with its returns. This could produce signals that change the wider institutional landscape for investing in a low-carbon future. Divestment can establish a broader dialogue on investing in sustainable energy, and a holistic view of energy transition, while urging financial portfolios to reflect this. Reducing demand for fossil fuel energy and re-organising production processes in many sectors will require forward-looking investments, not just changing our mode of energy production. Reducing liquid fuel demand in transportation will be of prime importance. The development of energy-efficient housing and sustainable food will also be needed.’

Our nexus approach developed here necessarily leads to questions as to how the agri-food sector will emerge and develop within the context of these post-carbon energy transitions. We can expect an increasing (but uneven) demand upon rural land-as we indeed witnessed with the first wave of bio-fuels (2007-8), for use for renewable energy sources. The role of a reflexive and facilitative multi-level state, as Kropp [

55] identifies in Bavaria, will be critical in both stimulating and shaping these transitions to what she calls a ‘third modernity’.

Similarly, agricultural production itself will need to become far-less ‘carbonised’ and centralised. This can act as a stimulus for the growth of agro-ecological and organic food production and revised ‘nested markets’, which provide increasing supplies of quality foods to urban consumers. This is already leading to more re-localised food supply chains and assemblages in many parts of the world.

There is then a spectre of a co-evolutionary transformation of both energy and agri-food as part- and-parcel of the contested post carbon-transition. This will of course be highly uneven both over time and space, and create its own particular uneven geographies. In addition, not least will competitively co-evolve with more centralised, oligopolistic and corporate trajectories, which we also begin to outline here. As we have documented here, the nexus transformations we are thus now witnessing, we need to recognise, are not leading to the total demise or indeed passivity of industrial or financial capitalism. However, they are both set to radically transform its former reliance upon extractive and emitting technologies and practices, as well as potentially ‘shrink’ its spatial and level of corporate control. This, follows the logic developed by scholars such as Harvey [

58] and Moore [

59], that it is not realistic to assume constant annual growth rates (of approximately 3%) in capitalist economies any longer, as new frontiers of traditional resource-intensive appropriation are dwindling due to both resource depletion and indeed political and civic society opposition, not least by the growing divestment movements.

Thus, in this new political-ecological context, at the very least, environmental scholars and activists need to be exploring the potentialities for post-capitalist and certainly post-neo-liberal models of nexus development—such as community share schemes, agri-food solidarity and translocal movements, agro-ecological cooperatives, and shorter and more equitable profit-sharing schemes. These include and embody radically different spatialities, which are far removed from the spatial fix and lock-in tendencies of the past (see

Figure 1 and

Figure 2). We are only at the foothills of understanding these new nexus spatialities; and still less in articulating them such that both state authorities can see them and as well as civil society stakeholders. The current ecological crisis (climate change and resource depletion) has coincided with a strong bout of crisis ridden capitalist neo-liberalism. The rise of post carbonism does not need necessarily to follow the same pathway.

This is the opportunity that the timely but uncertain confluence of both the ‘shrinkage’ of carbonised capitalism, on the one hand, and the rise of the post-carbon transition on the other brings to the energy/agri-food nexus. It also necessitates a re-politicisation of natural resource governance- a renewed and engaged political ecology—in ways that re-connect civil society and local communities to the active and collective re-definition of their access, material production and use of natural and renewable assets. This provides an urgent research agenda framing the intermediaries and contestations between carbonised and post-carbon strategies with regard to unfolding the agri-food/energy nexus. Most importantly, the research agenda should consider the territorial (human and animal) and very much day-to-day inequalities, risks and uncertainties resulting from the battles within the agri-food-energy nexus.

{kind=link}

{kind=link}