Abstract

Companies play a role in society that clearly goes beyond mere economic interest. Their contribution to social development and to the sustainability of the territory where they are located seems unquestionable. However, after the great financial scandals of companies such as ENRON, WorldCom or AHOLD, interest groups require accurate and transparent financial information. The development of more demanding financial reporting standards seems, however, not to have been up to scratch, since accounting fraud continues to be detected all over the world. The search, therefore, for possible causes that may induce companies to act unethically was the main motivation behind this research. To do this, a review of the literature in high-impact journals that has dealt with accounting fraud, covering the main lines of research, was carried out. The findings of the literature review highlight the importance of responsible corporate governance and good accounting practices, as well as the importance of certain psychological characteristics of managers and employees as enhancers of the lack of ethics. It is clear that the social cost of accounting fraud should be minimized, and governments should develop specific policies that combine responsible corporate governance in companies with the sustainability of their environment.

1. Introduction

In an increasingly commercialized world, the drive of companies directs social development and determines the evolution of sustainability in society and the environment. From this perspective, adequate business management marked by clearly rooted ethical standards conditions the development of a more balanced society in an environment that adequately combines economic development and sustainable business behavior, which constitutes Corporate Social Responsibility [1].

According to Joss [2], ethics condition the sense of responsibility, and this, in turn, has a particular importance in relation to sustainability. In fact, ethical and moral judgments allow us to direct the difficult choices between economic, social and environmental priorities, so that there is no conflict between profitability objectives and social objectives.

In recent years, and before the accounting scandals of major companies worldwide, there has been an increase in the demand for business information. This demand has focused on both ethical and social issues, as well as environmental aspects, highlighting the clear convergence of these areas, seemingly disparate, and yet strongly linked to a sense of responsibility [3]. Corporate social responsibility has thus become a strategic requirement for competing [4]. According to Kim, Park and Wier [5], there is evidence of a positive relationship between sustainable business practices and the quality of the accounting result. Similarly, the work of Kolk [6] reflects the awareness of the link between corporate governance and broadly defined sustainability.

On the contrary, a lack of ethics encompasses a lack of responsibility, which generates the fraudulent action of certain managers. The consequences of managerial malpractice by managers are harmful to companies, causing them to lose value, reputation and image [7]. In addition, a negative relationship has been found between the sustainable practices put in place by companies and fraudulent behavior [8]. Following this approach, and as fraud is a very serious global, social and economic problem [9], the present document reviews the latest research related to accounting fraud, shedding light on the factors that induce managers to act unethically and other aspects on which the studies have focused.

Focusing on purely quantitative aspects, the latest report of the ACFE (Association of Certified Fraud Examiners) for the year 2018 states that organizations lose 5% of their annual income because of fraud. This amount, translated into Gross World Product figures, equals 4 trillion dollars [10]. Although, as indicated by this organization, it is unlikely that we can ever calculate the real cost of fraud on a global scale, what is clear is that this expense provides no commercial or social benefit whatsoever.

According to Salleh and Othman [11], among the activities regarded as being fraudulent are the theft of money, omission of information, misuse of company assets, fraudulent acquisitions, misstatements of financial statements (accounting fraud), corruption, conspiracy, money laundering and bribery. Within these fraudulent activities, accounting fraud is of considerable importance, representing 22% of the economic crimes that occur worldwide [12]. This is one of the reasons behind the demand for greater transparency in corporate behavior. An example of this is the requirement for the rendering of accounts to corporate governance and the preparation of a sustainability report, including social and financial aspects [6].

According to the ACFE, fraud can be classified into three main blocks: fraud in financial statements, embezzlement or misappropriation of assets, and corruption, with fraud in the financial statements generating the highest costs, although it is less common than the misappropriation of assets [13]. Examples of these costs are the loss of value for shareholders, creditors, customers and suppliers, or economic damages to employees and governments [14]. According to Sadaf et al. [15], greater control by governments of corruption and political stability could reduce the number of fraud cases. Because of the great costs involved, it would be essential to mitigate the enormous costs of corporate fraud in companies and society in general [16].

The Enron case, which has been one of the most resounding accounting frauds of all time worldwide, showed the need to take regulatory measures in order to avoid this type of case reoccurring in the future. Thus, for example, the Sarbanes-Oxley Act was created in 2002 in the USA and, in the European Union, Directive 2006/43/EC of the European Parliament and the Council came into being in 2006. However, despite this greater governmental concern, there is evidence that companies continue to commit accounting fraud [17], with cases being detected all over the world [18], having a cyclical behavior [19].

Given all this, it is not surprising that there has also been greater interest, from the academic world and governments, to clarify the causes that give rise to accounting fraud. In fact, it has been noted through the present work that the study of accounting fraud has increased widely in recent years [20]. However, there are few reviews of the literature covering this field. Van Akkeren and Buckby [21] analyzed through a qualitative study the perceptions of forensic accountants to determine if the conceptual framework collected in the literature on the subject of fraud, included the causes that can lead to fraudulent behavior by individuals and groups [22]; Botes and Saadeh address the changes that have taken place in the concept of forensic accounting; review misconduct in financial reports from the perspectives of law, accounting and finance [23]; review the concept of “reporting irregularities” in accounting [24]; the skills that the forensic accounting professions should possess to carry out their work successfully [25]; applications of data mining in accounting, indicating the strengths and weaknesses of the same [26]; the application and use of Big Data in auditing [27]; discuss the “Fraud Triangle” [28] and [29]. Ref. [30], who start with a review of the literature on accounting and auditing fraud conducted by Hogan et al. [31], complete it with a discussion of disciplines including ethics, psychology and criminology, misperceptions of fraud and fraudsters [32], and a review of the literature on the detection of financial fraud using data mining methods [33].

Although all the documents indicated in the previous paragraph are reviews of the literature based on accounting fraud, the analysis undertaken in each of them covers very specific areas.

This article differs from other research summaries of accounting fraud (e.g., [30,31]), as it reviews and updates the literature in a single document, as well as embracing the different topics on which research into accounting fraud has focused.

Based on a review of 156 articles published in the main academic journals dealing with accounting fraud for the period 2000–2018, the following objectives were extracted for the present research: (a) the chronological trend of accounting fraud; (b) the type of research conducted and; (c) the main topics investigated.

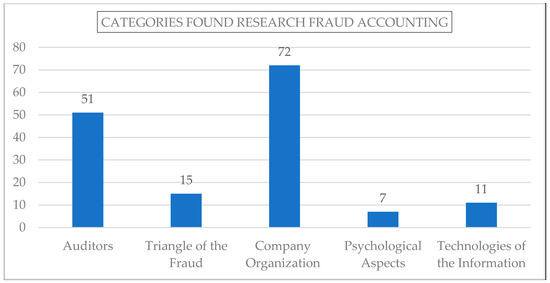

Furthermore, from the review, it can be inferred that the areas dealt with by the different authors can be grouped into five major categories. The first category consists of research that analyzes the aspects related to company organization (corporate governance, incentives, rotation of managers, collusion, reporting irregularities, investors) and represents 45% of the total. The second focuses on articles that deal with the role of the auditor, representing 32%. The third group is that which investigates the subject of the Fraud Triangle, covering 10% of the total. The fourth focuses on the use of information technologies for the detection and prevention of fraud (7%), and the last on the topic of the psychological aspects of fraudsters, representing 5% of the total number of articles. These last two categories are the most current trends.

The review allows us to provide a series of contributions to the literature on accounting fraud:

First, the focus on the figure of the auditor as the main person responsible for the detection of accounting fraud has not diminished. There has been greater interest in using artificial intelligence that allows the analysis of large amounts of data and facilitates the detection of accounting fraud.

Second, the Fraud Triangle and its three elements (pressure, opportunity and rationalization) are still used in the investigation of accounting fraud. It is important to analyze the three elements separately in the investigations and combine them with issues related to ethics, values, morals and criminology in order to improve effectiveness in the detection of accounting fraud.

Third, company organization is a very broad field in terms of its relationship with accounting fraud; it is also the area that constitutes the greatest number of articles published in journals. Corporate governance is the most studied topic for which proposals have been made, such as promoting the independence of the board of directors, its size and the separation of the role of the CEO and the chairman from the board to reduce the likelihood of fraud.

Fourth, the psychological aspect of fraudsters is a relatively recent line of research in which personality traits, especially of CEOs are taken into consideration. Narcissism is the most studied aspect in this field.

Fifth, the use of information technology to improve the early detection of accounting fraud in companies has increased in recent years. Applications of artificial intelligence and data mining have emerged, especially in recent years, to help auditors do their job better.

This literature review aims to help researchers better understand cutting-edge research trends in this area and can be used as a starting point for future research. Also, it allows the identification of personality traits that induce fraud, as well as knowing the most innovative detection technologies. Finally, it will allow the identification of types of manager or circumstances with a lack of ethics, and consequently, with tendencies towards fraudulent behavior.

The article has been organized as follows. The first section offers an overview of the research in accounting fraud during the years 2000–2018. The objectives and methodology of the research are specified in the second section. In the third, the results of the analysis are presented. Finally, the conclusions and lines of future research are provided.

2. Accounting Fraud: A General Vision

Accounting fraud is a problem that negatively affects the users of accounting information, among which are shareholders, creditors, senior managers and society in general [34]. Even other companies in the same sector experience the negative reaction of the market once the fraud has been detected [35].

There are several definitions of accounting fraud that have been proposed by different organizations. Among them is that established by the SAS (Statement on Auditing Standards) No. 99 (page 1721), according to which it is “an intentional act carried out by one or more persons in the management of the company, its employees or third parties, which results in a misstatement in the financial or accounting statements that are subject to an audit” [36].

On the other hand, the International Auditing Standard NIA 240 (p. 159) [37] defines it as “an intentional act carried out by one or more persons in the management team, those responsible for the government of the entity, employees or third parties, which involves the use of deception in order to gain an unfair or illegal advantage”. According to this norm, relevant errors are considered to be due to both fraudulent financial information and misappropriation of assets. The first involves misleading and intentionally reporting the company’s financial statements, for example, manipulating or falsifying accounting records, or erroneously applying generally accepted accounting principles (GAAP) [38]. On the other hand, asset misappropriation involves the theft or unauthorized use of company assets [39], or causing an entity to pay for goods or services that have not been received (SAS No. 99, p. 4) [36].

As mentioned in the introduction, the lines of investigation in accounting fraud have been divided into five categories. For students of accounting fraud, the role of the auditor has been regarded as one of the main elements in the process, despite the fact that detecting fraud is particularly difficult due to companies’ efforts to hide it [40,41]; therefore, trust in the auditing profession has suffered serious setbacks in recent years [42]. Despite this, internal auditors are more easily able to detect misappropriation of assets, while for external auditors, fraud in the financial statements is easier to track [43]. However, the auditing role continues to represent a greater guarantee against accounting fraud, especially when there is such little research work related to dissuasive measures, despite the enormous costs involved in this type of fraud [44]. Their adequate academic training and experience in detecting fraud [45] and due exercise of an appropriate professional skepticism [46] are elements that must be taken into account for optimum performance in their work.

On the other hand, the Fraud Triangle and its three interactive elements (pressure, opportunity and rationalization) are common to all frauds [47,48], and those related to accounting are not an exception. Despite its importance, different authors do not agree on which of its three elements is most important. For some [28,49], the emphasis is on the opportunity. Others, however, claim that the Fraud Triangle should not be seen as a sufficiently reliable model for anti-fraud professionals, since fraud is a multifaceted model [50]. What the authors do seem to agree on is the need to break it down into its three elements for assessing the risk of fraud [44]. Trompeter et al. conducted a comprehensive review of this construct in accounting and non-accounting research, complementing it with other fields such as criminology, ethics, psychology and sociology [29].

The relationship between accounting fraud and organizational aspects of the company has also been widely studied. Accounting, auditing and financial information and corporate governance are related (e.g., [51,52]). The influence of incentives in the performance of managers (e.g., [53]), the relationship between corporate governance and sustainability [54], the rotation of managers in fraudulent companies (e.g., [55,56,57]), professional connections between managers (e.g., [58,59]), collusion (e.g., [60]), the role of employees in detecting fraud (e.g., [34]), the use of internal and external telephone lines (e.g., [61,62]), the integration of ethics with finance and accounting (e.g., [63]), and investors and the use of the company financial information to detect fraud (e.g., [17,64,65]).

On the other hand, the investigation of the psychological factors related to fraud is a recent study trend. According to Ramamoorti and Olsen [66], understanding them could shed light on the understanding of the behavior of fraudsters. Thus, the narcissism of the CEO has been studied as a psychological trait that correlates positively with fraud [67,68,69].

Finally, the use of information technologies is a trend that seems to be breaking through in the study of accounting fraud. New technologies seem to favor fraud, but also provide more sophisticated detection techniques [70]. Data analysis (e.g., [71]), support vector machines (e.g., [72]), blockchain [73] and data mining (e.g., [26,74,75]) are some of the techniques used. In this same line, corporate governance should also use a systematic approach to investigate fraud in a company. This means using appropriate software to detect unusual activities [52].

3. Methodology of the Review

Our work is based on a review of the literature or meta-analysis of articles published in high-impact journals during the period between 2000 and 2018 with an accounting- and/or auditing-related topic in order to identify interesting new research. The search was done through the Web of Science, reviewing articles with the word “fraud” in the title during the indicated years. The initial search generated 6989 results for the year 2000; however, refining the results with the filters “Business Economics” (Research area) and “Article” (Type of document), the result was reduced to 2888 articles. We focus on the findings related to accounting fraud in these documents. Since the literature in this field is voluminous, we went through a painstaking selection process about the specific articles and themes, which finally lead us to selecting 156 articles. This methodology has also been used by several other authors who have also undertaken literature reviews for their research (Carcello, Hermanson, and Ye, 2011 [76]; Lee and Xiao, 2018 [77]; Schnatterly, Gangloff, and Tuschke, 2018 [78]).

To analyze how the 156 articles analyzed were distributed among the five categories, all the articles were first reviewed and then divided, according to the main theme, into five subject areas (Auditors, Fraud Triangle, Corporate Governance, Psychological Aspects, Information Technology). For each area, a specific computation was made of the total number of articles found and finally the tables below were drawn up based on the authors, year of publication and the main conclusions of each article.

4. Analysis of Investigation in Accounting Fraud

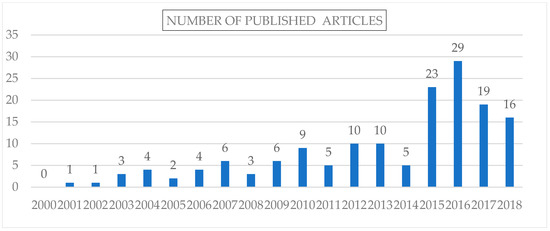

Chronologically speaking, the investigation into the issue of accounting fraud experienced an exponential growth during the analyzed period, increasing from one article in the year 2001 to 16 articles in the year 2018 (Figure 1).

Figure 1.

Number of articles published per year.

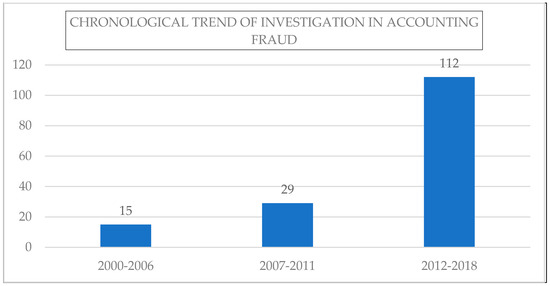

Therefore, there is clearly growing interest in the subject of accounting fraud, especially between the years 2012 and 2018, in which the number of articles published almost tripled with respect to that of previous years (Figure 2).

Figure 2.

Trend in the publication of articles on accounting fraud (2000–2018). Source: The authors’ own elaboration.

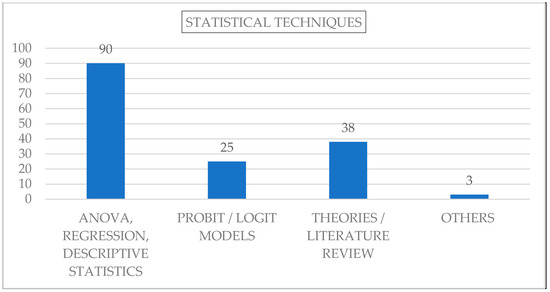

4.1. Statistical Techniques Used in the Investigation of Accounting Fraud

The articles included in the review used a wide variety of statistical techniques (Figure 3), most notably the ANOVA analysis (e.g., [68,79,80]), descriptive statistics (e.g., [81,82]) and regression (e.g., [83,84]). These three techniques, along with the use of logit/probit models (e.g., [85,86]), account for almost 80% of the articles reviewed. The rest are mostly theoretical works (e.g., [87,88,89]). The section “others” includes two articles that use structural equations ([90,91,92]) and one that, instead of using ANOVA, used Contrast of Weighting (Buckless and Ravenscroft, 1990) ([93]).

Figure 3.

Techniques used in articles. Source: The authors’ own elaboration.

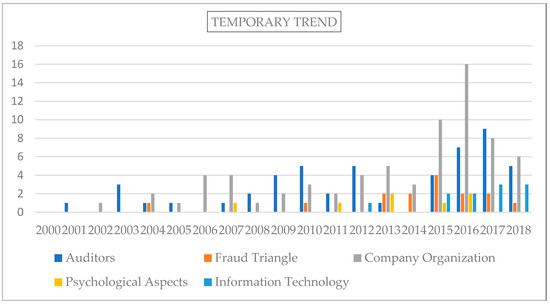

4.2. Topics, Temporary Trends and Main Findings Studied in Accounting Fraud

As mentioned above, if the 156 articles are classified by the main topic on which the research focused, we find that they can be grouped into five categories (see Figure 4):

Figure 4.

Classification of articles in 5 categories. Source: The authors’ own elaboration.

The temporary trend in the evolution of accounting fraud as a subject area has clearly been on the rise. Nevertheless, as the figure (Figure 5) indicates, the period 2012–2018 clearly accounts for the majority of the articles. The area that had most coverage was “Company Organization”. The next most studied subject was “Auditors”, with articles appearing throughout almost the whole analyzed period. As for the third subject, that is, the “Fraud Triangle”, the articles center fundamentally on the period 2013–2018. The articles on the topic of “Information Technology” appear from the year 2012 and reach a high between 2015 and 2018. The subject of “Psychological Aspects” appears in 2007, but it should be highlighted that this area is the least covered.

Figure 5.

Temporary trend of accounting fraud issues. (Source: The authors’ own elaboration.)

The following sections provide five tables with a chronological list of the articles included in our review, detailing the research topic, the author, the year of publication and the main conclusion. Along with each table, a brief review of the main issues that the literature gathers in each of the five categories can be found.

4.2.1. Auditors

For auditors, detecting fraud can be a difficult job, mainly because it is an act that is intended to be hidden and, although fraud prediction models are available, they are not totally reliable [33,83]. To assist the auditor in carrying out his/her work, he/she is required to conduct “brainstorming” tasks as a means to develop robust ideas of a potential client fraud [84,85,86,87]. The current audit standards indicate this (SAS No. 99), although they do not clarify which specific form of the brainstorming process must be used [94]. What is specified is that “the members of the auditing team should use the brainstorming tool to find out how and where they believe that the entity’s financial statements could be susceptible to errors due to fraud and how the administration could commit and conceal fraudulent financial information” (AICPA 2002, 10). This may explain the different amount of brainstorming processes that have been used in the articles reviewed [89,90,91].

Fraud does not favor the auditing profession [43], and organizations such as ACFE express their concern about the lack of success auditors have in detecting fraud. Auditors can only succeed if the factors that contribute to fraud are eliminated or help them to be more effective in detecting fraud [87].

Therefore, auditors require tools that can help them in the performance of their work, such as the possibility of consulting with fraud specialists, or having lists of standard risk factors for fraud [93,94]. In fact, auditors seem to be more motivated to use the work of the specialists, out of respect for the authority they perceive [95]. On the other hand, some researchers point out that the use of checklists by auditors makes them less critical in their study of financial statements [96].

Hamilton proposes that auditors use the client’s perspective, that is, take into account the circumstances that the client was facing when preparing the financial statements, especially if there are indications of intentional misstatements [97].

According to Bazrafshan [98], the most important risk components in companies for auditors are those related to the misappropriation of assets. Although fraud due to asset misappropriation has received very little attention in research, some authors [36,94] clarify that external auditors investigate fraud by focusing on financial statements, while internal auditors cover a greater variety of frauds, including asset misappropriation. This type of fraud is not negligible, and it is estimated that 6 percent of the income of US companies in 2002 was lost through the same [99].

This situation highlights the need to establish adequate internal control systems as measures to prevent fraudulent financial information [100,101]. These control systems include internal audits, the introduction of responsibilities for employees in the accounting area, or the use of control measures based on information technologies [102].

According to the ACFE (2010), 80% of the companies that have been victims of fraud have modified their internal controls and taken measures accordingly; among such measures are performing surprise audits, increasing the division of tasks among employees, or establishing a code of conduct.

On the other hand, it is more likely that studies that evaluate the importance of having as part of the corporate management an internal audit function detect fraud and self-report the misappropriation of assets [82]. The relationship between corporate governance and the areas of accounting and auditing has increased in recent years. The importance of the CEO and CFO (Chief Financial Officer) [76] being jointly supervised by the board and the company’s auditing committee is highlighted. It is very positive that strong corporate governance is complemented by a strong auditing board in order to decrease the likelihood of fraud. On the other hand, other authors state that outsourcing the auditing function is better than internal auditing for detecting this type of fraud [95,96].

Furthermore, it has been noted that part of the literature focuses on the role of the auditors regarding the motivation they have in detecting fraud taking into account the threats of legal action against them. Along these lines, the research of Reffett [92] and Eutsler, Nickell and Robb [86], using the Theory of Counterfactual Reasoning, concludes that auditors can be penalized and have legal action taken against them for not detecting fraud, even though they have investigated it. This is because those who evaluate their work (Congress and the United States Securities and Exchange Commission (hereinafter SEC)) could draw the conclusion that the auditors have been negligent in their investigation and could have done things differently (Counterfactual Reasoning).

Table 1 offers a summary of the main contributions found in the articles reviewed based on the auditors.

Table 1.

Category: Auditors. (Main conclusions drawn on the figure of the auditor in the articles reviewed).

4.2.2. The Fraud Triangle

The term “Fraud Triangle” was coined long after Cressey’s work; it was Joseph Wells, founder of the ACFE, who popularized it [28], replacing the notion of an unshared problem, indicated by Cressey, with that of pressure [131]. The use of the same in the field of forensic accounting and in the examination of fraud has increased significantly [132].

According to Haefele and Stiegeler [133], the commission of “white collar” crimes, especially accounting fraud, usually follows the same pattern, which researchers have called the Fraud Triangle. The investigation into the risk of fraud has used the Fraud Triangle and the interaction of its three components as elements common to all frauds. These elements are: (1) incentives or perceived motivation, (2) the perceived opportunity and (3) the attitude or character that allows a person to rationalize the act of fraud [134].

Thus, the Fraud Triangle is presented as a credible methodology that allows fraud specialists to speak with authority and intervene, in a certain way, in organizational fraud [28]. Of the three elements indicated, some authors have conducted studies in which the opportunity is considered a universal precondition for acts defined as fraudulent [20,41].

Although it is highlighted in the investigations carried out that the three elements, indicated above, are important and necessary in the study of fraud, the decomposition of the same into fraud risk assessments increases the sensitivity of auditors to detecting the same [99,135].

The study of accounting fraud, using the Fraud Triangle tool, has been enriched and combined with contributions from other disciplines, such as ethics, morals and values [123,126], criminology, psychology and sociology [21,130], or combined with other frameworks such as the Crime Triangle (Mui and Mailley) [136].

However, according to [50], the Fraud Triangle should not be seen as a sufficiently reliable model for anti-fraud professionals, since fraud is a multifaceted phenomenon with contextual factors that may not always fit into a particular framework.

Table 2 offers a summary of the main contributions found in the articles reviewed with the topic “Fraud Triangle”.

Table 2.

Category: the Fraud Triangle (Main conclusions drawn on the topic of the Fraud Triangle in the articles reviewed).

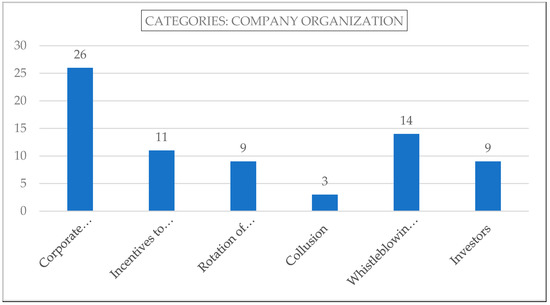

4.2.3. Company Organization

Most of the articles analyzed were concentrated in this group, representing 47% of the total articles. Due to the heterogeneity of the perspectives addressed in this area, it was considered necessary to structure the articles reviewed in six categories (Figure 6):

Figure 6.

Subcategories of the subject “Company Organization”. (Source: The authors’ own elaboration).

Corporate Governance/Board of Directors

The fraud committed by a company’s top management can be considered a subset of the so-called “white collar crimes”, among which are embezzlement, insider trading, intentional distortion in the financial statements and corruption. The consequences affect shareholders, employees and the community through a decrease in the share price, as well as the loss of confidence in the company and in its top management [144]. It even has side effects for other companies that belong to the same industry, such as an increase in the fees of auditing companies and greater scrutiny by auditors on financial information processes [145].

There is no doubt that the pressure to maintain good financial results can tempt managers to commit accounting fraud, even though these results do not correspond with reality [146]. Managers of companies are more prone to accounting fraud when the stock price has remained sustained for a period of up to five years [147].

The characteristics of the board of directors and the corporate governance of the company are correlated with the occurrence of fraud [85]. In this sense, one of the first research papers in which corporate governance was related to fraud was presented by Beasley [148]. This shows that the presence of independent directors, or those external to the company, significantly reduces the likelihood of fraud. As the percentage of independent directors on the board increases, the double role between CEO (Chief Executive Officer) and BOD (Board of Directors) should be separated. This would reduce the agency costs, because such power and influence would not fall on one person. Sharma finds that if this double function is not separated, then the probability of fraud increases [149], and companies will remain internally weak [150].

However, Halbouni et al. [44] state that, in the United Arab Emirates, corporate governance has a moderate role in preventing and stopping fraud. In addition, these same authors conclude that CEOs and boards of directors must adequately establish the tone and ethical climate (tone at the top) to generate an environment of integrity and ethics in the company. The establishment of codes of ethics by senior management and the board of directors is essential as an integral part of Corporate Social Responsibility [151]. Financial statements must be prepared ethically, since compliance with accounting standards does not necessarily guarantee ethical reports in all contexts [152]. Along these lines, Carcello, Hermanson, and Ye [76] propose the establishment of ethical measures monitored by the CRO (Chief Risk Officer), CCO (Chief Compliance Officer), CEthO (Chief Ethics Officers), duly informing the audit committee. Contrary to the above Tan, Chapple and Walsh [153] indicate that the role of corporate governance in reducing fraud is only significant for companies that have a culture of fraud.

On the other hand, some research highlights the importance of the improvements that occur in companies after the discovery of fraud [30,114]. Thus, companies that significantly reduced the percentage of internal executive directors and increased the percentage of external directors in their meetings saw their reputation improve in the market. Farber [73] ensures that the perceptions that investors have about improvements in the corporate governance of the company after fraud can generate an increase in the price of shares [84].

Another line of research is that followed by Cumming, Leung and Rui [154]. They examine how the gender diversity of the board of directors has an effect on the likelihood that the company will commit fraud. Their study establishes three interesting conclusions: (1) gender diversity in the board of directors acts as a significant moderator for the frequency of fraud; (2) the response of the stock market to fraud, in the case of a board with diverse gender, is much less pronounced; and (3) women are more effective in industries dominated by men at reducing the frequency and severity of fraud. Therefore, increasing the representation of women in boardrooms can help reduce fraud [155].

With regards demographic characteristics such as professional experience, age and academic background of the CEO, it has been concluded that younger CEOs with less academic background and experience are more likely to rationalize accounting fraud and see their acts as ethical and justified [38]. If the demographic characteristics of the CEO are added to unbalanced corporate strategies, there is more likelihood of committing fraud, as this type of strategy harms the financial strength of the company, making fraud the easy way to obtain additional resources [156].

On the other hand, the ownership structure of the company (dispersed/concentrated) also influences the type of fraud that occurs. In this way, corporate governance, designed to protect the interests of shareholders, cannot work in the same way in both types of companies [157].

Finally, it has also been shown that the frequency with which corporate governance meetings take place can help owners, auditors and the general public to identify fraud in companies early on [11].

At this point, it is important to clarify two important aspects related to the size of companies and endogeneity in corporate governance investigations.

Most of the articles analyzed related to this subcategory do not make reference to the importance of the size of the company in their empirical investigations. Thus, the measurement of the size of the company should be taken into account as a key variable or control by researchers in corporate finance [158]. In this sense, the work of Dang, Li and Yang focuses on the study of the importance of the size of the company in 20 areas of corporate finance. To do this, they analyze three measures of size: total assets, total sales and equity market value, since they are the proxies of companies most used in corporate finance. Using these three measures, they conclude that large companies tend to have more external directors, larger boards and more duality of the CEO (separation between CEO and chairman of the board (COB)); thus, this work is to be considered by researchers in corporate finance who need to measure the impact of the size of the company. We recommend researchers in corporate finance consult the article indicated, since it provides a guide for choosing the size of the company in their empirical studies.

On the other hand, research on corporate governance is plagued by the problem of endogeneity, which can bias the claims that researchers make about the hypotheses raised in their studies. Much of the research assumes that the corporate governance variables are exogenous and yet the characteristics of the company can also affect the characteristics of the board of directors, at this point they become related with the phenomenon that is being studied [76]. This endogeneity occurs when an independent variable correlates with the error term in a regression model of ordinary least squares. To address this problem, Li [159] proposes different econometric models to analyze the relationship between the power of the CEO and the subsequent performance of the company, observing a negative relationship between said variables. Furthermore, Semadeni, Withers and Trevis [160] propose instrumental variables techniques to alleviate this problem; whereas Garcia-Castro, Ariño and Canela [161] study how endogeneity problems affect the positive relationship found between the company’s social performance and financial performance. If endogeneity is taken into account, this relationship becomes non-significant or even negative [162]. Finally, Wintoki, Linck and Netter [162] find no relationship between the current structure of the board and the current performance of the board, which is inconsistent with previous work.

It is clear that the challenge for researchers is to develop appropriate variables to investigate corporate governance avoiding the problem of endogeneity.

Incentives to Management

The relationship between executive incentives and fraud has been widely studied, and among the conclusions drawn is that whereby performance-based compensation can induce managers to misreport their performance and influence their own salary. In this way, there is a clear relationship between CEO compensation and accounting fraud [80,81,82,83,84,85,86,87,88,89,90,91,92,93,94,95,96,97,98,99,100], with it being more common in private companies [83]. Therefore, the opportunity offered by the asymmetry of information is sufficient for CEOs to present fraudulent financial reports [163].

In keeping with previous work, Johnson, Ryan and Tian, [53] analyze corporate fraud as an undesired result and one associated with managerial incentives. The framework they use for their analysis is Becker’s Economic Theory (1968) of the crime framework. According to these authors, the agents commit a crime because the reward they expect outweighs the punishment in the event that they were discovered. Thus, in the work of Sen [88], it is concluded that there is a clear de-compensation between the profits that derive from the fraud and the penalties imposed. Contrary to this idea, Erickson, Hanlon and Maydew [164] find no consistent evidence that executive incentives are associated with fraud.

Finally, it should be mentioned that in recent years, and as a deterrent, companies have tried to mitigate the dysfunctional effects of the use of incentives using reintegration clauses in cases of fraud, which seems to have had an effect on the behavior of executives, by discouraging or penalizing them [165].

Rotation of Directors/Connections of Managers

The relationship between fraud in companies and the rotation of their managers is an obvious and contrasted fact [19,47,120]. Thus, in the work of Persons [57], which was carried out on 224 fraudulent companies judicially sued in the United States, it was highlighted that, in general, there is a greater turnover of executives in said companies, with their compensation being less.

How the professional connection of managers and directors in companies reduces accounting fraud, while non-professional connectivity increases the propensity to fraud has also been studied [59].

As previously mentioned, although the presence of external directors on the board reduces the likelihood of fraud, it seems that the complaints for this reason have significant reputational consequences for these directors, and also have a negative effect on the management positions that they hold in other companies [166]. This loss of reputation is suffered not only by the directors but also by the companies themselves, leading to investors also “punishing” them for their damaged reputation [127,128].

Despite the reputational damage that fraud can cause, a series of mechanisms have been established to prevent fraud in financial statements. Thus, for example, the Sarbanes-Oxley Act (SOX) establishes regulations that suppose an increase in the internal control of evaluations by auditors and also an increase in the severity of sanctions against the management of inaccurate financial information. Thus, Ugrin and Odom [167] indicate that the potential threat of time in jail may deter fraud in financial statements, although its effectiveness is influenced by social, environmental and demographic factors. According to McEnroe [168], it seems that executives do not perceive that SOX is an effective deterrent, and they assert that labor market forces and social discredit are more effective than the possibility of going to jail.

Trying to alleviate the situation derived from fraud and its consequences in the management of the company, Marcel and Cowen [169] propose two mechanisms to redirect the post-fraud business volume of the company. One involves repairing the legitimacy of the organization to avoid the withdrawal of resources and the other, increasing the individual effort of the directors to safeguard their own reputations and mitigate their professional devaluation

Collusion

Fraud in financial statements is characterized, among other aspects, by the fact that it can be hidden through collusion between management, employees or third parties. Management can also ignore or instruct others to overlook effective controls of this type of fraud [36].

Collective fraud (collusion) has hardly been studied. Proof of this is that of the 156 articles analyzed, only 3 deal with this area [49,131,132].

Free and Murphy [60] explain that fraud has a social rather than an individual nature, and that this aspect is key to understanding its etiology and some of its distinctive features. Aspects such as loyalty, trust and distrust can consolidate a group and provide reasons to co-commit and rationalize fraudulent behavior. Albrecht et al. [48] analyze how senior management can influence other individuals into committing fraud in financial statements through five types of power—reward, coercive, expert, legitimate and reference—having detected the use of all of them in the research carried out.

Khanna, Kim and Lu [58] show how the previous relationships between CEOs and directors or senior executives of a company, either through previously established personal links or by influencing the latter in the decision of their appointment, are associated with a greater probability of fraud. This is more difficult to detect and is carried out over a longer period of time.

Whistleblowing and Media

In 50% of the cases, employees are the most common means for detecting fraud. Sources external to the company, such as customers and vendors, accounted for 34%, and the rest came from the review of the company management and internal audits [13]. Thus, according to the ACFE survey (2010), reporting irregularities is the simplest method of detecting fraud. Gao and Brink have reviewed existing literature on this concept [24]. Furthermore, Wilde [170] provides evidence of how companies with mechanisms for reporting irregularities available to employees reduce the performance of incorrect financial reports and fiscal aggression. Along the same lines, Johansson and Carey [171] have also analyzed the same for small businesses drawing similar conclusions.

Among the mechanisms that employees can use to report irregularities in the company is the implementation of a hotline [62]. However, although employees are often aware of the existence of such mechanisms, they do not use them [134,139]. Thus, 82% of those who reported the fraudulent behavior of their company were dismissed or resigned under duress, and thus, many affirmed that if they had to do it again they would not [34].

On the other hand, some authors have studied the acts employees are most willing to report [137,143]. They found that employees are more likely to report acts involving the appropriation of assets than the existence of fraudulent financial information. It seems that employees perceive that the appropriation of assets supposes a personal benefit for the one who commits it. On the contrary, fraudulent financial information is observed as something that benefits the organization, to protect its employees and shareholders.

Accounting fraud has attracted public attention, and the press seems to play an important role in its dissemination, among other aspects, due to the pressure that it exerts on management [172]. Miller [173] states that business press investigates particularly technical information in order to subsequently prepare reports. He highlights the role as the same as that of a “watchdog” providing a better analysis than the non-business press, whose main purpose is only to retransmit the fraud.

Investors

Large accounting scandals have been detected throughout the world [174], with investors being one of the most affected parties, as well as being those for whom it is most difficult to detect the fraud. For this reason, the SEC is interested in training investors to be familiar with warning signs (red flags) that could help protect them from fraudulent financial information. Among these signals, investors focus, fundamentally, on SEC investigations, the existence of pending litigation or high turnover in the management of the company [65]. In addition to these signals, investors use the information provided by business analysts, as they act as intermediaries between the information provided by management and themselves [17]. On the other hand Wu, Johan and Rui [175] point out that groups of shareholders with a large number of shares in their possession (institutional investors) can reduce the incidence of fraud through their supervision and influence on the management of the company, which will also benefit small investors. Additionally, they contribute that if, in addition, the managers of the companies have political connections, the legal actions to which the company would be exposed for fraud would be diminished.

Finally, regulators and auditors should remain alert to periods of economic boom, since, in this case, the probability that a company will commit fraud is greater. This is because the mechanisms of internal surveillance of companies are relaxed [78,141].

Table 3 offers a summary of the main contributions found in the articles reviewed with the topic “Company Organization”.

Table 3.

Category: Company Organization (Main conclusions drawn on the theme of organization company in the articles reviewed).

4.2.4. Psychological Aspects

Fraudulent behavior also depends on the psychological factors of those who commit it [66]. The study of the managers´ psychological factors of the companies and their relationship with the fraudulent behavior is a current trend that has gained more strength. Dacin and Murphi [198] identify three ways to become involved in fraud, namely: lack of awareness, rationalization and reasoning. The personality traits of the CEO, such as the lack of moral values and narcissism, are important aspects related to the commission of fraud [156]. Specifically, the narcissism of managers seems to be a potentially important risk factor for fraud [60,144,145], and thus auditors should be aware of narcissistic behavior when making their evaluations. In other research, the psychological characteristics of the CEO are combined with traditional tools in the investigation of accounting fraud, such as the Fraud Triangle (e.g., [199]).

Table 4 offers a summary of the main contributions found in the articles reviewed with the topic “Psychological Aspects”.

Table 4.

Category: Psychological Aspects (Main conclusions drawn on the subject of the psychological aspects of fraudsters in the articles reviewed).

4.2.5. Information Technology

This section comprises research that analyzes the use of information technology to detect accounting fraud. Since 2012, a significant increase in the use of these technologies has been observed, as, when investigating large amounts of data, they can be used proactively to identify patterns that suggest fraudulent activity in companies [201]. Another of the methodologies used is the analysis of texts, exploring the language used in the discussion and analysis of annual and quarterly reports in the company. In this case, words and terms are searched that may indicate deception, litigation, uncertainty or negative feelings [202]. In the article by Dbouk and Zaarour, supervised machine learning is proposed for detecting the manipulation of profits [203]. On the other hand, Amani and Fadlalla and West and Bhattacharya review the applications of data mining for accounting. Amani and Fadlalla reveal that the detection of fraud is one of the areas of accounting that has most benefited from this technique, while the latter focus on techniques based on computational intelligence [18,66].

Table 5 offers a summary of the main contributions found in the articles reviewed with the topic “Information technology”.

Table 5.

Category: Information Technology (Main conclusions drawn on the use of information technologies in the detection / prevention of fraud in the articles reviewed).

5. Conclusions and Future Research

This article contributes to the literature on accounting fraud through a review and analysis of 156 articles published in high-impact journals during the period 2000–2018. Thus, the importance of accounting fraud in the current socioeconomic context, the research methodology used in its analysis, the different approaches to it, and the main conclusions of the articles have been analyzed.

To carry out the analysis of the topic of accounting fraud, the articles have been divided into five large groups: Auditors, Fraud Triangle, Company Organization, Psychological Aspects and Information Technology.

After examining the articles, we cannot conclude that any of the categories have lost their strength or importance over the 18 years reviewed. This conclusion is drawn after studying the years in which the articles and the specific topics have been published. On the other hand, it was observed that there are two aspects that seem to be gaining more followers in the last six years. These are: (1) those related to the use of information technology to help auditors better identify the patterns of fraudulent behavior in the company; and (2) the importance that is being given to the psychological aspects of fraud.

The present study leaves the door open for many lines of future research, aimed at a better understanding of the phenomenon of accounting fraud.

As far as the organizational aspects of the company are concerned, which is the topic on which the largest group of articles was found (72 articles), it would be necessary to study three aspects in depth. The first aspect would be to expand the investigation of collective fraud (collusion), since only three of the articles reviewed dealt with this specifically and, according to the ACFE (2018), fraud losses increase significantly when more than one fraudster is involved. Second, it is necessary to delve into the reasons that would induce employees to reveal fraud or to report irregularities (14 articles). Further study of the influence of monetary rewards for whistleblowers is a debate that continues to be open, as well as the confidence and protection that should be provided to the complainants, both in the design of the collection process and the analysis of the same. Thirdly, future research can address the relationship between a company’s auditing committee and the management of the company (26 articles), especially the importance of the role of the chairman of the auditing committee both from the perspective of his relationship with the auditing committee and with the company’s management [76]. The issue of developing ethical codes to guide the responsible behavior of the organization is another of the proposed future lines of research ([63,90]).

For the “auditors” category, which is second in the number of articles analyzed (51 articles), future research can study the effect of Artificial Intelligence and its various technologies (data mining, text analysis, etc.) on their daily work [26]. We also propose expanding the study of the auditor’s responsibility in the evaluation of the financial statements, since this influences the same [104].

The category of the Fraud Triangle is the third in importance, since it includes 15 articles. Expanding the study of the triangle to include areas such as criminology, ethics, morals and values would provide a broader view of accounting fraud ([48,116]).

Finally, the information technology (11 articles) and psychological categories (7 articles) are the least numerous. However, future investigations may be aimed firstly towards the detection and classification of erroneous financial statements with the intention of fraud using Big Data techniques, which have until now been underutilized in this field [27]. Regarding the psychological aspects, it would be worth expanding the studies on the influence of narcissism in the involvement of accounting fraud, adding other aspects such as psychopathy or Machiavellianism to create profiles of fraudsters that help the identification of these individuals in companies [200].

Author Contributions

Conceptualization, M.R.M. and A.J.S.M.; methodology, M.R.M. and A.J.S.M.; Investigation: M.R.M.; resources, M.R.M., A.J.S.M. and F.B.S.; writing, M.R.M., A.J.S.M., F.B.S.; writing—review and editing, M.R.M., A.J.S.M., F.B.S.; supervision, A.J.S.M. and F.B.S.

Funding

This study was funded by State Research Agency—Spanish Ministry of Science, Innovation and Universities—project I+D DER2014-57128-P y “Transparencia Institucional, Participacion Ciudadana y Lucha Contra la Corrupcion: Analisis, Evaluacion y Propuestas”.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Heal, G. Corporate Social Responsibility: An economic and financial framework. Geneva Pap. Risk Insur. Pract. 2005, 30, 387–409. [Google Scholar] [CrossRef]

- Joss, S. Accountable governance, accountable sustainability? A case study of accountability in the governance for sustainability. Environ. Policy Gov. 2010, 20, 408–421. [Google Scholar] [CrossRef]

- Rossouw, G.J. Business ethics and corporate governance: A global survey. Bus. Soc. 2005, 44, 32–39. [Google Scholar] [CrossRef]

- Garrigues Walker, A.; Trullenque, F. Responsabilidad social corporativa: ¿papel mojado o necesidad estratégica? Harv. Deusto Bus. Rev. 2008, 164, 18–36. [Google Scholar]

- Kim, Y.; Park, M.S.; Wier, B. Is earnings quality associated with corporate social responsibility? Account. Rev. 2012, 87, 761–796. [Google Scholar] [CrossRef]

- Kolk, A. Sustainability, Accountability and Corporate Governance: Exploring Multinationals’ Reporting Practices. Bus. Strateg. Environ. 2008, 15, 1–15. [Google Scholar] [CrossRef]

- Fombrun, C.J.; Gardberg, N.A.; Barnett, M.L. Opportunity Platforms and Safety Nets: Corporate Citizenship and Reputational Risk. Bus. Soc. Rev. 2002, 105, 85–106. [Google Scholar] [CrossRef]

- Martinez-Ferrero, J.; Prado-Lorenzo, J.M.; Fernandez-Fernandez, J.M. Responsabilidad social corporativa vs. responsabilidad contable. Rev. Contab. 2013, 16, 32–45. [Google Scholar] [CrossRef]

- Karpoff, J.M.; Koester, A.; Lee, D.S.; Martin, G.S. A critical analysis of databases used in financial misconduct research. Ssrn Electron. J. 2012, 15–18. [Google Scholar] [CrossRef]

- ACFE. 2018 Report to the Nations; Association of Certified Fraud Examiners: Austin, TX, USA, 2018. [Google Scholar]

- Salleh, S.M.; Othman, R. Board of Director’s Attributes as Deterrence to Corporate Fraud. Procedia Econ. Financ. 2016, 35, 82–91. [Google Scholar] [CrossRef]

- PwC. Economic Crime: A Threat to Business Globally; PwC: London, UK, 2014; pp. 1–57. [Google Scholar]

- ACFE. 2014 Report To the Nations; Association of Certified Fraud Examiners: Austin, TX, USA, 2014; p. 31. [Google Scholar]

- Velikonja, U. the Cost of Securities Fraud. William Mary Law Rev. 2013, 54, 1887–1957. [Google Scholar]

- Sadaf, R.; Oláh, J.; Popp, J.; Máté, D. An investigation of the influence of theworldwide governance and competitiveness on accounting fraud cases: A cross-country perspective. Sustainability 2018, 10, 588. [Google Scholar] [CrossRef]

- Helge, L.; Müller, M.A.; Vergauwe, S. Tournament incentives and corporate fraud. J. Corp. Financ. 2015, 34, 251–267. [Google Scholar]

- Young, S.M.; Peng, E.Y. An Analysis of Accounting Frauds and the Timing of Analyst Coverage Decisions and Recommendation Revisions: Evidence from the US. J. Bus. Financ. Account. 2013, 40, 399–437. [Google Scholar] [CrossRef]

- Stolowy, H. Creative Accounting, Fraud and International Accounting Scandals. TAR 2012, 87, 1087–1098. [Google Scholar] [CrossRef]

- Gong, J.; Mcafee, R.P.; Williams, M. Fraud cycles. J. Inst. Theor. Econ. Jite 2016, 172, 544–572. [Google Scholar] [CrossRef]

- Aghghaleh, S.F.; Mohamed, Z.M.; Rahmat, M.M. Detecting Financial Statement Frauds in Malaysia: Comparing the Abilities of Beneish and Dechow Models. Asian J. Account. Gov. 2016, 7, 57–65. [Google Scholar] [CrossRef]

- Van Akkeren, J.; Buckby, S. Perceptions on the Causes of Individual and Fraudulent Co-offending: Views of Forensic Accountants. J. Bus. Ethics 2017, 146, 383–404. [Google Scholar] [CrossRef]

- Botes, V.; Saadeh, A. Exploring Evidence to develop a nomenclature for forensic accounting. Pac. Account. Rev. 2018, 30, 135–154. [Google Scholar] [CrossRef]

- Amiram, D.; Bozanic, Z.; Cox, J.D.; Dupont, Q.; Karpoff, J.M.; Sloan, R.G. Financial Reporting Fraud and Other Forms of Misconduct: A Multidisciplinary Review of the Literature. Rev. Account. Stud. 2018, 23, 732–783. [Google Scholar] [CrossRef]

- Gao, L.; Brink, A.G. Whistleblowing studies in accounting research: A review of experimental studies on the determinants of whistleblowing. J. Account. Lit. 2017, 38, 1–13. [Google Scholar] [CrossRef]

- Tiwari, R.K.; Debnath, J. forensic accounting: A blend of Knowledge. J. Financ. Regul. Compliance 2017, 25, 73–85. [Google Scholar] [CrossRef]

- Amani, F.A.; Fadlalla, A.M. Data mining applications in accounting: A review of the literature and organizing framework. Int. J. Account. Inf. Syst. 2017, 24, 32–58. [Google Scholar] [CrossRef]

- Gepp, A.; Linnenluecke, M.K.; O’Neill, T.J.; Smith, T. Big data techniques in auditing research and practice: Current trends and future opportunities. J. Account. Lit. 2018, 40, 102–115. [Google Scholar] [CrossRef]

- Morales, J.; Gendron, Y.; Guénin-Paracini, H. The construction of the risky individual and vigilant organization: A genealogy of the fraud triangle. Account. Organ. Soc. 2014, 39, 170–194. [Google Scholar] [CrossRef]

- Trompeter, G.M.; Carpenter, T.D.; Jones, K.L.; Riley, R.A. Insights for research and practice: What we learn about fraud from other disciplines. Account. Horiz. 2014, 28, 769–804. [Google Scholar] [CrossRef]

- Trompeter, G.M.; Carpenter, T.D.; Desai, N.; Jones, K.L.; Riley, R.A. A Synthesis of Fraud-Related Research. Audit. A J. Pract. Theory 2013, 32, 287–321. [Google Scholar] [CrossRef]

- Hogan, C.E.; Rezaee, Z.; Riley, R.A.; Velury, U. Financial statement fraud: Insights from the academic literature. Audit. A J. Pract. Theory 2008, 27, 231–252. [Google Scholar] [CrossRef]

- Brody, R.G.; Melendy, S.R.; Perri, F.S. Commentary from the American accounting association’s 2011 annual meeting panel on emerging issues in fraud research. Account. Horiz. 2012, 26, 513–531. [Google Scholar] [CrossRef]

- West, J.; Bhattacharya, M. Intelligent financial fraud detection: A comprehensive review. Comput. Secur. 2016, 57, 47–66. [Google Scholar] [CrossRef]

- Dyck, A.; Morse, A.; Zingales, L. Who blows the Whistle on Corporate Fraud? J. Financ. 2010, 65, 2213–2253. [Google Scholar] [CrossRef]

- Goldman, E.; Peyer, U.; Stefanescu, I. Financial Misrepresentation and its impact on rivals. Financ. Manag. 2012, 41, 915–945. [Google Scholar] [CrossRef]

- PCAOB. AU Section 316 Consideration of Fraud in a Financial Statement Audit; PCAOB: Washington, DC, USA, 2002; pp. 167–218. [Google Scholar]

- IFAC. NIA 240. Responsabilidades del auditor en la auditoría de estados financieros con respecto al fraude; IFAC: Geneva, Switzerland, 2013; pp. 1–39. [Google Scholar]

- Troy, C.; Smith, K.G.; Domino, M.A. CEO demographics and accounting fraud: Who is more likely to rationalize illegal acts? Strateg. Organ. 2011, 9, 259–282. [Google Scholar] [CrossRef]

- Kaplan, S.E.; Pope, K.R.; Samuels, J.A. An Examination of the Effect of Inquiry and Auditor Type on Reporting Intentions for Fraud. Audit. A J. Pract. Theory 2011, 30, 29–49. [Google Scholar] [CrossRef]

- Nieschwietz, R.J.; Schultz, J.J., Jr.; Zimbelman, M.F. Empirical research on external auditors’ detection of financial statement fraud. J. Account. Lit. 2000, 19, 190–246. [Google Scholar]

- Knapp, C.A.; Knapp, M.C. The efects of experience and explicit fraud risk assessment in detecting fraud with analytical procedures. Account. Organ. Soc. 2001, 26, 25–37. [Google Scholar] [CrossRef]

- Wuerges, A. Auditors’ responsibility for fraud detection: New wine in old bottles? Available online: www.scribd.com/doc/63671899/Auditors-Responsibility-for-Fraud-Detection (accessed on 3 November 2012).

- Imoniana, J.O.; de Feitas, E.C.; Jacob Perera, L.C. Assessment of internal control systems to curb corporate fraud—Evidence from Brazil. Afr. J. Account. Audit. Financ. 2016, 5, 1–24. [Google Scholar] [CrossRef]

- Davis, J.S.; Pesch, H.L. Fraud dynamics and controls in organizations. Account. Organ. Soc. 2013, 38, 469–483. [Google Scholar] [CrossRef]

- Hamdan, S.L.; Jaffar, N.; Ab Razak, R. The Effect of Competency on Internal Auditors’ Contribution to Detect Fraud in Malaysia. In Proceedings of the 29th IBIMA Conference, Vienna, Austria, 3–4 May 2017. [Google Scholar]

- Mubako, G.; O’Donnell, E. Effect of fraud risk assessments on auditor skepticism: Unintended consequences on evidence evaluation. Int. J. Audit. 2018, 22, 55–64. [Google Scholar] [CrossRef]

- Machado, M.R.R.; Gartner, I.R. The Cressey hypothesis (1953) and an investigation into the occurrence of corporate fraud: An empirical analysis conducted in Brazilian banking institutions. Rev. Contab. Finanç. 2017, 29, 60–81. [Google Scholar] [CrossRef]

- Albrecht, C.; Holland, D.; Malagueño, R.; Dolan, S.; Tzafrir, S. The Role of Power in Financial Statement Fraud Schemes. J. Bus. Ethics 2015, 131, 803–813. [Google Scholar] [CrossRef]

- Schuchter, A.; Levi, M. Beyond the fraud triangle: Swiss and Austrian elite fraudsters. Account. Forum 2015, 39, 176–187. [Google Scholar] [CrossRef]

- Lokanan, M.E. Challenges to the fraud triangle: Questions on its usefulness. Account. Forum 2015, 39, 201–224. [Google Scholar] [CrossRef]

- Soltani, B. The Anatomy of Corporate Fraud: A Comparative Analysis of High Profile American and European Corporate Scandals. J. Bus. Ethics 2014, 120, 251–274. [Google Scholar] [CrossRef]

- Halbouni, S.S.; Obeid, N.; Garbou, A. Corporate governance and information technology in fraud prevention and detection: Evidence from the UAE. Manag. Audit. J. 2016, 31, 589–628. [Google Scholar] [CrossRef]

- Johnson, S.A.; Ryan, H.E.; Tian, Y.S. Managerial Incentives and Corporate Fraud: The Sources of Incentives Matter. Rev. Financ. 2009, 13, 115–145. [Google Scholar] [CrossRef]

- UNEP/SustainAbility. Risk & Opportunity: Best Practice in Non-Financial Reporting; SustainAbility: London, UK, 2004; p. 56. [Google Scholar]

- Agrawal, A.; Cooper, T. Corporate Governance Consequences of Accounting Scandals: Evidence from Top Management, CFO and Auditor Turnover. Q. J. Financ. 2017, 7, UNSP 1650014. [Google Scholar] [CrossRef]

- Beneish, M.D.; Marshall, C.D.; Yang, J. Explaining CEO retention in misreporting firms. J. Financ. Econ. 2017, 123, 512–535. [Google Scholar] [CrossRef]

- Persons, O.S. The Effects of Fraud and Lawsuit Revelation on U.S. Executive Turnover and Compensation. J. Bus. Ethics 2006, 64, 405–419. [Google Scholar] [CrossRef]

- Khanna, V.; Kim, E.H.; Lu, Y. CEO Connectedness and Corporate Fraud. J. Financ. 2015, 70, 1203–1252. [Google Scholar] [CrossRef]

- Yu, X. Securities Fraud and Corporate Finance: Recent Developments. Manag. Decis. Econ. 2013, 34, 439–450. [Google Scholar] [CrossRef]

- Free, C.; Murphy, P.R. The ties that bind: The decision to co-offend in fraud. Contemp. Account. Res. 2015, 32, 18–54. [Google Scholar] [CrossRef]

- Stone, T.H.; Jawahar, I.M.; Kisamore, J.L. Using the theory of planned behavior and cheating justifications to predict academic misconduct. Career Dev. Int. 2009, 14, 221–241. [Google Scholar] [CrossRef]

- Lee, G.; Fargher, N. Companies’ Use of Whistle-Blowing to Detect Fraud: An Examination of Corporate Whistle-Blowing Policies. J. Bus. Ethics 2013, 114, 283–295. [Google Scholar] [CrossRef]

- Melé, D.; Rosanas, J.M.; Fontrodona, J. Ethics in Finance and Accounting: Editorial Introduction. J. Bus. Ethics 2017, 140, 609–613. [Google Scholar] [CrossRef]

- Wang, T.Y.; Winton, A.; Yu, X. Corporate fraud and business conditions: Evidence from IPOs. J. Financ. 2010, 65, 2255–2292. [Google Scholar] [CrossRef]

- Brazel, J.F.; Jones, K.L.; Thayer, J.; Warne, R.C. Understanding investor perceptions of financial statement fraud and their use of red flags: Evidence from the field. Rev. Account. Stud. 2015, 20, 1373–1406. [Google Scholar] [CrossRef]

- Ramamoorti, S.; Olsen, W.P. Fraud the Human Factor. Financ. Exec. 2007, 53–55. [Google Scholar] [CrossRef]

- O’Reilly, C.A.; Doerr, B.; Chatman, J.A. “See You in Court”: How CEO narcissism increases firms’ vulnerability to lawsuits. Leadersh. Q. 2018, 29, 365–378. [Google Scholar] [CrossRef]

- Johnson, E.N.; Kuhn, J.R.; Apostolou, B.A.; Hassell, J.M. Auditor Perceptions of Client Narcissism as a Fraud Attitude Risk Factor. Audit. A J. Pract. Theory 2013, 32, 203–219. [Google Scholar] [CrossRef]

- Rijsenbilt, A.; Commandeur, H. Narcissus Enters the Courtroom: CEO Narcissism and Fraud. J. Bus. Ethics 2013, 117, 413–429. [Google Scholar] [CrossRef]

- Coderre, D.; Royal Canadian Mounted Police. Continuous Auditing: Implications for Assurance, Monitoring, and Risk Assessment. Glob. Technol. Audit Guid. 2005, 3, 1–33. [Google Scholar]

- Perols, J.L.; Bowen, R.M.; Zimmermann, C.; Samba, B. Finding needles in a haystack: Using data analytics to improve fraud prediction. Account. Rev. 2017, 92, 221–245. [Google Scholar] [CrossRef]

- Wei, Y.; Chen, J.; Wirth, C. Detecting fraud in Chinese listed company balance sheets. Pac. Account. Rev. 2017, 29, 356–379. [Google Scholar] [CrossRef]

- Wang, Y.; Kogan, A. Designing confidentiality-preserving Blockchain-based transaction processing systems. Int. J. Account. Inf. Syst. 2018, 30, 1–18. [Google Scholar] [CrossRef]

- West, J.; Bhattacharya, M. An Investigation on Experimental Issues in Financial Fraud Mining. Procedia Comput. Sci. 2016, 80, 1734–1744. [Google Scholar] [CrossRef]

- Dutta, I.; Dutta, S.; Raahemi, B. Detecting financial restatements using data mining techniques. Expert Syst. Appl. 2017, 90, 374–393. [Google Scholar] [CrossRef]

- Carcello, J.V.; Hermanson, D.R.; Ye, Z. Corporate Governance Research in Accounting and Auditing: Insights, Practice Implications, and Future Research Directions. Audit. A J. Pract. Theory 2011, 30, 1–31. [Google Scholar] [CrossRef]

- Lee, G.; Xiao, X. Whistleblowing on accounting-related misconduct: A synthesis of the literature. J. Account. Lit. 2018, 41, 22–46. [Google Scholar] [CrossRef]

- Schnatterly, K.; Gangloff, K.A.; Tuschke, A. CEO Wrongdoing: A Review of Pressure, Opportunity, and Rationalization. J. Manag. 2018, 44, 2405–2432. [Google Scholar] [CrossRef]

- Trotman, K.T.; Wright, W.F. Triangulation of audit evidence in fraud risk assessments. Account. Organ. Soc. 2012, 37, 41–53. [Google Scholar] [CrossRef]

- Boritz, J.E.; Kochetova-Kozloski, N.; Robinson, L. Are fraud specialists relatively more effective than auditors at modifying audit programs in the presence of fraud risk? Account. Rev. 2015, 90, 881–915. [Google Scholar] [CrossRef]

- Asare, S.K.; Wright, A.M. The Effectiveness of Alternative Risk Assessment and Program Planning Tools in a Fraud Setting. Contemp. Account. Res. 2004, 21, 325–352. [Google Scholar] [CrossRef]

- Coram, P.; Ferguson, C.; Moroney, R. Internal audit, alternative internal audit structures and the level of misappropriation of assets fraud. Account. Financ. 2008, 48, 543–559. [Google Scholar] [CrossRef]

- Hass, L.H.; Tarsalewska, M.; Zhan, F. Equity Incentives and Corporate Fraud in China. J. Bus. Ethics 2016, 138, 723–742. [Google Scholar] [CrossRef]

- Farber, D.B. Restoring Trust after Fraud:Does Corporate Governance Matter? Account. Rev. 2005, 80, 539–561. [Google Scholar] [CrossRef]

- Uzun, H.; Szewczyk, S.H.; Varma, R. Board Composition and Corporate Fraud. Financ. Anal. J. 2004, 60, 33–43. [Google Scholar] [CrossRef]

- Eutsler, J.; Nickell, E.B.; Robb, S.W.G. Fraud risk awareness and the likelihood of audit enforcement action. Account. Horiz. 2016, 30, 379–392. [Google Scholar] [CrossRef]

- Albrecht, W.S.; Albrecht, C.; Albrecht, C.C. Current Trends in Fraud and its Detection. Inf. Secur. J. A Glob. Perspect. 2008, 17, 2–12. [Google Scholar] [CrossRef]

- Sen, P.K. Ownership Incentives and Management Fraud. J. Bus. Financ. Account. 2007, 34, 1123–1140. [Google Scholar] [CrossRef]

- Povel, P.; Singh, R.; Winton, A. Booms, Busts, and Fraud. Rev. Financ. Stud. 2007, 20, 1219–1254. [Google Scholar] [CrossRef]

- Domino, M.A.; Wingreen, S.C.; Blanton, J.E. Social Cognitive Theory: The Antecedents and Effects of Ethical Climate Fit on Organizational Attitudes of Corporate Accounting Professionals—A Reflection of Client Narcissism and Fraud Attitude Risk. J. Bus. Ethics 2015, 131, 453–467. [Google Scholar] [CrossRef]

- Popoola, O.M.J.; Ahmad, A.C.; Samsudin, R.S. An Examination of Task Performance Fraud Risk Assessment on Forensic Accountant Knowledge and Mindset in Nigerian Public Sector. Int. J. Bus. Manag. 2013, 9, 1–16. [Google Scholar] [CrossRef]

- Reffett, A.B. Can Identifying and Investigating Fraud Risks Increase Auditors’ Liability? Account. Rev. 2010, 85, 2145–2167. [Google Scholar] [CrossRef]

- Hoffman, V.B.; Zimbelman, M.F. Do Strategic Reasoning Brainstorming Help Auditors Change Their Standard Audit Procedures in Response to Fraud Risk? Account. Rev. 2009, 84, 811–837. [Google Scholar] [CrossRef]

- Simon, C.A. Individual Auditors’ Identification of Relevant Fraud Schemes. Audit. A J. Pract. Theory 2012, 31, 1–16. [Google Scholar] [CrossRef]

- Mock, T.J.; Turner, J.L. Auditor Identification of Fraud Risk Factors and their Impact on Audit Programs. Int. J. Audit. 2005, 9, 59–77. [Google Scholar] [CrossRef]

- Shelton, S.W.; Ray Whittington, O.; Landsittel, D. Auditing firms’ fraud risk assessment practices. Account. Horiz. 2001, 15, 19–33. [Google Scholar] [CrossRef]

- Griffith, E.E. When do auditors use specialists’ work to improve problem representations of and judgments about complex estimates? Account. Rev. 2018, 93, 177–202. [Google Scholar] [CrossRef]

- Bazrafshan, S. Exploring expectation gap among independent auditors’ points of view and university students about importance of fraud risk components. Iran. J. Manag. Stud. 2016, 9, 305–331. [Google Scholar]

- Holtfreter, K. Fraud in US organisations: An examination of control mechanisms. J. Financ. Crime 2004, 12, 88–95. [Google Scholar] [CrossRef]

- Carpenter, T.D.; Reimers, J.L.; Fretwell, P.Z. Internal Auditors’ Fraud Judgments: The Benefits of Brainstorming in Groups. Audit. A J. Pract. Theory 2011, 30, 211–224. [Google Scholar] [CrossRef]

- Chen, W.; Khalifa, A.S.; Trotman, K.T. Facilitating Brainstorming: Impact of Task Representation on Auditors’ Identification of Potential Frauds. Audit. A J. Pract. Theory 2015, 34, 1–22. [Google Scholar] [CrossRef]

- Horvat, T.; Lipicnik, M. Internal Audits of Frauds in Accounting Statements of a Construction Company. Strateg. Manag. 2016, 21, 29–36. [Google Scholar]

- Patterson, E.; Wright, D. Evidence of Fraud, Audit Risk and Audit Liability Regimes. Rev. Account. Stud. 2003, 8, 105–131. [Google Scholar] [CrossRef]

- Patterson, E.; Noel, J. Audit Strategies and Multiple Fraud Opportunities of Misreporting and Defalcation. Contemp. Account. Res. 2003, 20, 519–549. [Google Scholar] [CrossRef]

- Glover, S.M.; Prawitt, D.F.; Schultz, J.J.; Zimbelman, M.F. A Test of Changes in Auditors’ Fraud-Related Planning Judgments since the Issuance of SAS No. 82. Audit: A J. Pract. Theory 2003, 22, 237–251. [Google Scholar] [CrossRef]

- Firth, M.; Mo, P.L.; Wong, R.M. Financial Statements Fraud and Auditor Sanctions: An Analysis of Enforcement Actions in China. J. Bus. Ethics 2005, 62, 367–381. [Google Scholar] [CrossRef]

- Carpenter, T.D. Audit Team Brainstorming, Fraud Risk and Fraud Risk Identification, Assessment: Of SAS No. 99 Implications. Account. Rev. 2007, 82, 1119–1140. [Google Scholar] [CrossRef]

- Kerler, W.A.; Killough, L.N.; Iii, W.A.K. The Effects of Satisfaction with a Client’s Management During a Prior Audit Engagement, Trust, and Moral Reasoning on Auditors’ Perceived Risk of Management Fraud. J. Bus. Ethics 2008, 85, 109–136. [Google Scholar] [CrossRef]

- Brazel, J.F.; Jones, K.L.; Zimbelman, M.F. Using Nonfinancial Measures to Assess Fraud Risk. J. Account. Res. 2009, 47, 1135–1166. [Google Scholar] [CrossRef]

- Trotman, K.T.; Simnett, R.; Khalfia, A. Impact of the Type of Audit Team Discussions on Auditors’ Generation of Material Frauds. Contemp. Account. Res. 2009, 26, 1115–1142. [Google Scholar] [CrossRef]

- Hammersley, J.S.; Bamber, E.M.; Carpenter, T.D. The Influence of Documentation Specificity and Priming on Auditors’ Fraud Risk Assessments and Evidence Evaluation Decisions. Account. Rev. 2010, 85, 547–571. [Google Scholar] [CrossRef]

- Hunton, J.E.; Gold, A. A Field Experiment Comparing the Outcomes of Three Fraud Brainstorming Procedures: Nominal Group, Round Robin, and Open Discussion (Retracted). Account. Rev. 2010, 85, 911–935. [Google Scholar] [CrossRef]

- Brazel, J.F.; Carpenter, T.D.; Jenkins, J.G. Auditors’ Use of Brainstorming in the Consideration of Fraud: Reports from the Field. Account. Rev. 2010, 85, 1273–1301. [Google Scholar] [CrossRef]

- Norman, C.S.; Rose, A.M.; Rose, J.M. Internal Audit reporting lines, fraud risk decomposition, and assessments of fraud risk. Account. Organ. Soc. 2010, 35, 546–557. [Google Scholar] [CrossRef]

- Hammersley, J.S.; Johnstone, K.M.; Kadous, K. How Do Audit Seniors Respond to Heightened Fraud Risk? Audit. J. Pract. Theory 2011, 30, 81–101. [Google Scholar] [CrossRef]

- Gold, A.; Knechel, W.R.; Wallage, P. The Effect of the Strictness of Consultation Requirements on Fraud Consultation. Account. Rev. 2012, 87, 925–949. [Google Scholar] [CrossRef]

- Smith, A.L.; Murthy, U.S.; Engle, T.J. Why computer-mediated communication improves the effectiveness of fraud brainstorming. Int. J. Account. Inf. Syst. 2012, 13, 334–356. [Google Scholar] [CrossRef]

- Gullkvist, B.; Jokipii, A. Perceived importance of red flags across fraud types. Crit. Perspect. Account. 2013, 24, 44–61. [Google Scholar] [CrossRef]

- Markelevich, A.; Rosner, R.L. Auditor Fees and Fraud Firms. Contemp. Account. Res. 2013, 30, 1590–1625. [Google Scholar] [CrossRef]

- Popoola, O.M.J.; Che-Ahmad, A.B.; Samsudin, R.S. An empirical investigation of fraud risk assessment and knowledge requirement on fraud related problem representation in Nigeria. Account. Res. J. 2015, 28, 78–97. [Google Scholar] [CrossRef]

- Lisic, L.L.; Silveri, S.D.; Song, Y.; Wang, K. Accounting fraud, auditing, and the role of government sanctions in China. J. Bus. Res. 2015, 68, 1186–1195. [Google Scholar] [CrossRef]

- Hamilton, E.L. Evaluating the intentionality of identified misstatements: How perspective can help auditors in distinguishing errors from fraud. Audit. A J. Pract. Theory 2016, 35, 57–78. [Google Scholar] [CrossRef]

- Zager, K.; Malis, S.S.; Novak, A. Accountants’ views regarding the effectiveness of fraud prevention controls. In Proceedings of the 5th International Scientific Symposium Economy Of Eastern Croatia - Vision And Growth Colección: Medunarodni Znanstveni Simpozij Gospodarstvo Istocne Hrvatske-Jucer Danas Sutra, Osijek, Hrvatska, 2–4 June 2016; pp. 849–857. [Google Scholar]

- Okat, D. Deterring fraud by looking away. Rand J. Econ. 2016, 47, 734–747. [Google Scholar] [CrossRef]

- Reid, C.D.; Youngman, J.F. New audit partner identification rules may offer opportunities and benefits. Bus. Horiz. 2017, 60, 507–518. [Google Scholar] [CrossRef]

- Donelson, D.C.; Ege, M.S.; McInnis, J.M. Internal control weaknesses and financial reporting fraud. Audit. A J. Pract. Theory 2017, 36, 45–69. [Google Scholar] [CrossRef]

- Lail, B.; MacGregor, J.; Marcum, J.; Stuebs, M. Virtuous Professionalism in Accountants to Avoid Fraud and to Restore Financial Reporting. J. Bus. Ethics 2017, 140, 687–704. [Google Scholar] [CrossRef]

- Atagan, G.; Kavak, A. Relationship between fraud auditing and forensic accounting. Int. J. Contemp. Econ. Adm. Sci. 2017, 7, 194–223. [Google Scholar]

- Juric, D.; O’Connell, B.; Rankin, M.; Birt, J. Determinants of the Severity of Legal and Employment Consequences for CPAs Named in SEC Accounting and Auditing Enforcement Releases. J. Bus. Ethics 2018, 147, 545–563. [Google Scholar] [CrossRef]

- Wilson, A.B.; McNellis, C.; Latham, C.K. Audit firm tenure, auditor familiarity, and trust: Effect on auditee whistleblowing reporting intentions. Int. J. Audit. 2018, 22, 113–130. [Google Scholar] [CrossRef]

- Wells, J. Occupational Fraud and Abuse; Obsidian Publising Company: Austin, TX, USA, 1997. [Google Scholar]