Contingent Factors and Sustainable Performance Measurement (SPM) Practices of Malaysian Electronics and Electrical Companies

Abstract

1. Introduction

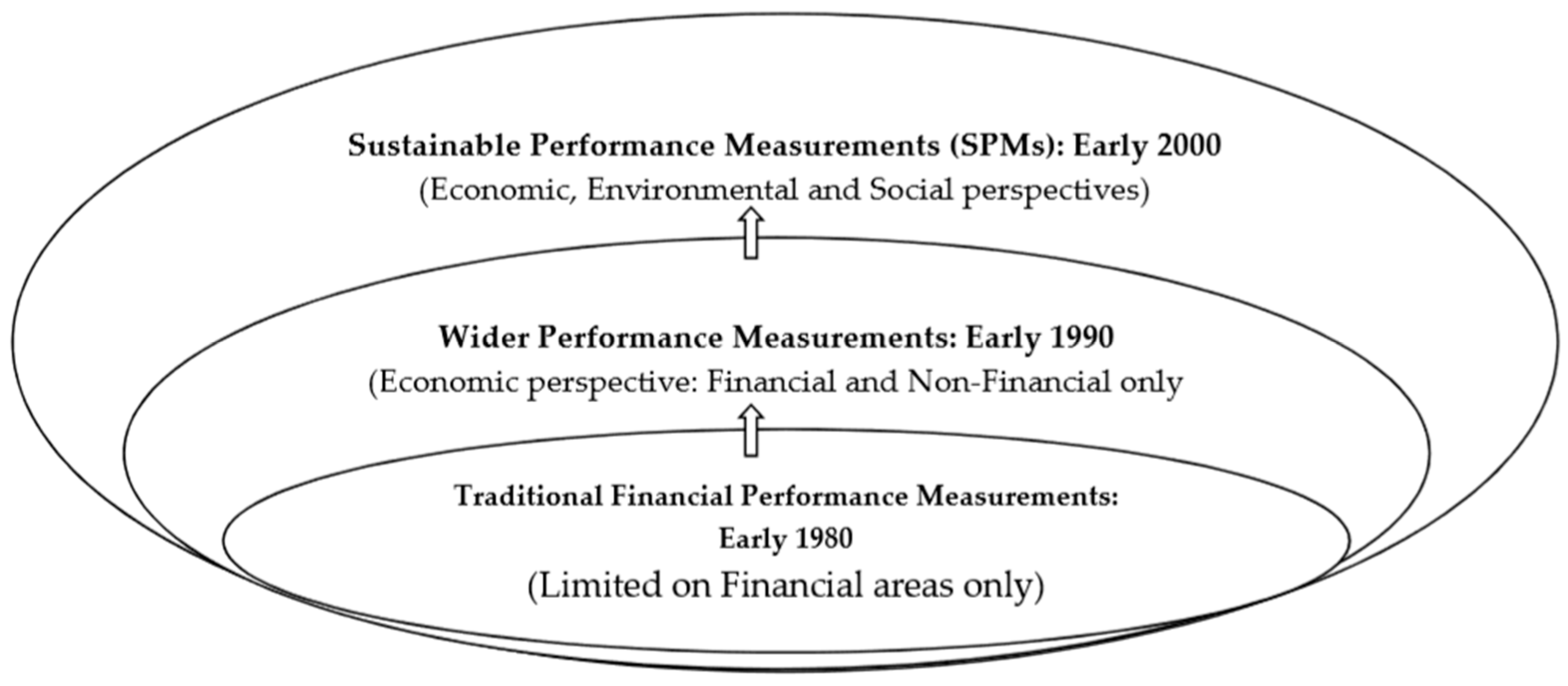

1.1. Development of Performance Measurement Practices

1.2. Research Objectives

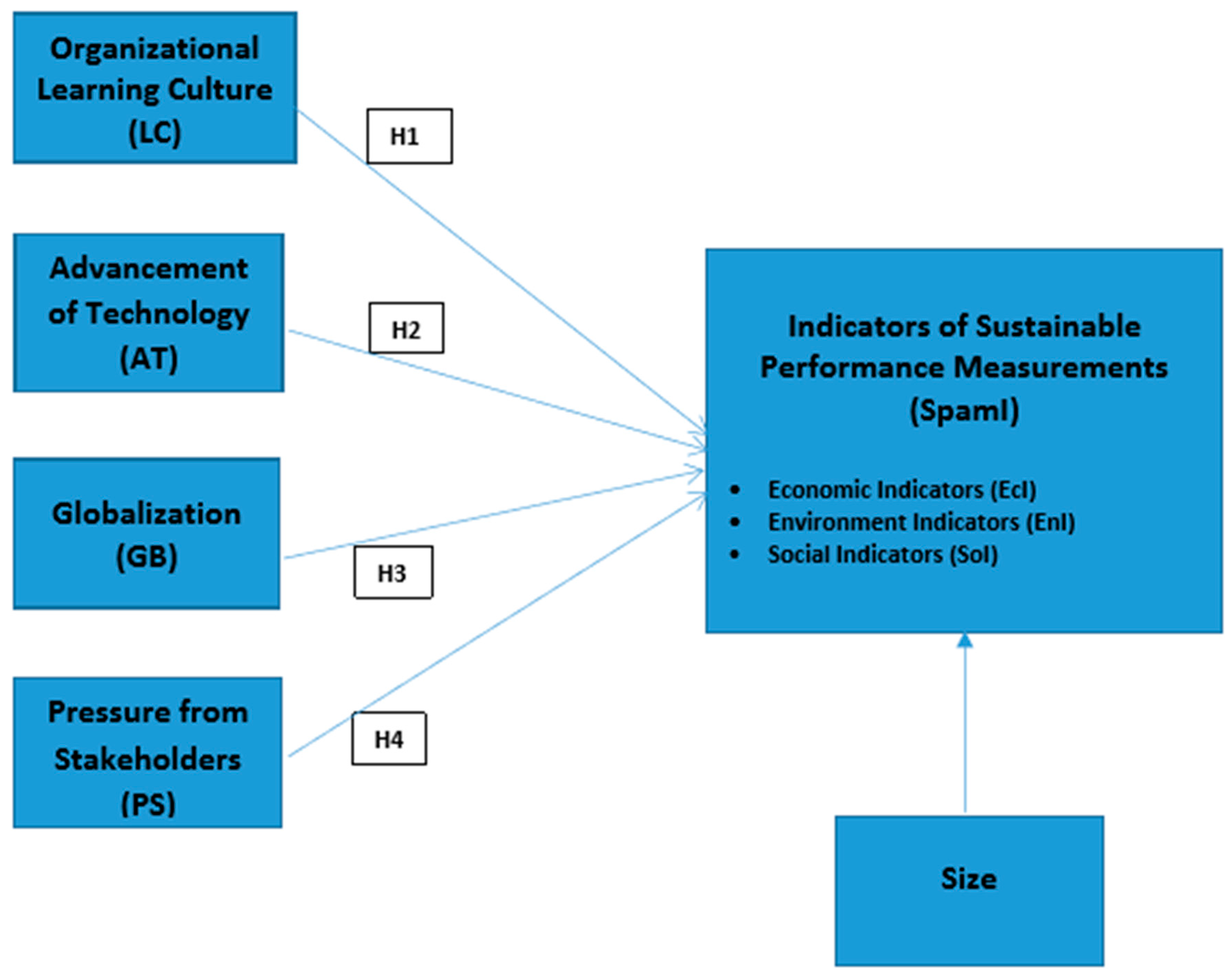

2. Research Model Based on Theoretical Foundations

3. Sustainable Performance Measurement (SPM) Practices

3.1. Economic Indicators

3.2. Environmental Indicators

3.3. Social Indicators

3.4. Control Variable

4. Development of Hypotheses Based on the Research Model

4.1. Organizational Learning Culture and SPMs

4.2. Advancement of Technology and SPMs

4.3. Globalization and SPMs

4.4. Pressure from Stakeholders and SPMs

4.5. Malaysian Manufacturing Firms as Population of Study

5. Methodologies

6. The Result

6.1. Non-Response Bias

6.2. Descriptive Statistics

6.3. Reliability

6.4. Structural Equation Modelling

7. Discussion

7.1. Contributions and Implications of the Study

7.2. Limitations and Areas for Future Research

7.3. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

Appendix A1. Organisation Profile

Appendix A2. Respondent’s Profile

Appendix A3. Organization’s Critical Success Factors

Appendix A4. Characteristics and Outcomes of Sustainable Performance Measurements (SPMs) Model

References

- MITI. Fact Sheet. 2012. Available online: http://www.miti.gov.my/index.php/pages/view/2497 (accessed on 5 January 2017).

- Bloomberg 2011. Available online: https://www.bloomberg.com/news/articles/2011-03-07/lynas-s-nick-curtis-builds-fortune-with-bet-on-rare-earths (accessed on 18 February 2017).

- Mining Weekly. 2012. Available online: http://www.miningweekly.com/article/australia-imposes-mining-tax-after-two-year-battle-2012-03-19 (accessed on 28 June 2017).

- Stede, W.A.V.D. How to become sustainable. MIA Account. Today 2010, 23, 32–34. [Google Scholar]

- Mandelbaum, D.G. Corporate Sustainability Strategies. Temple J. Sci. Technol. Environ. Law 2007, 26, 27–42. [Google Scholar]

- GRI. 2010. Available online: https://www.globalreporting.org (accessed on 19 September 2017).

- ASR (Asian Sustainability Rating). Sustainability in Asia, ESG Reporting Uncovered; Responsible Research; Asian Sustainability Rating: Singapore, 2010; p. 14. [Google Scholar]

- MIDA, Malaysian Industrial Development Authority. 2014. Available online: www.mida.gov.my/home/electrical-and-electronic/posts/ (accessed on 28 September 2017).

- Khalifah, A.N.; Jaafar, Z.; Adam, R. Processing Trade, Exporting and Efficiency of Establishments in Malaysia’s E&E Industry. In Proceedings of the 13th International Convention of the East Asian Economic Association Grand Copthorne Hotel, Singapore, 19–20 October 2012. Convention Theme. [Google Scholar]

- Hart, S. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Epstein, M.J. Making Sustainability Work: Best Practices in Managing and Measuring Corporate Social, Environmental, and Economic Impacts; Greenleaf Publishing: Sheffield, UK, 2008. [Google Scholar]

- Lecy, J.D.; Schmitz, H.P.; Swenlund, H. Non-Governmental and not-for-profit organizational effectiveness: A modern synthesis. Voluntas Int. J. Volunt. Non-Profit Organ. 2012, 23, 434–457. [Google Scholar] [CrossRef]

- Bobe, C.M.; Dragomir, V.D. The sustainability policy of five leading European retailers. Account. Manag. Inf. Syst. 2010, 9, 268–283. [Google Scholar]

- Hockerts, K. Eco-efficient service innovation: Increasing business-ecological efficiency of products and services. In Charter M., Greener Marketing: A Global Perspective on Greener Marketing Practice; Greenleaf Publishing: Sheffield, UK, 1999; pp. 95–108. [Google Scholar]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Owen, G. Integrated reporting: A review of developments and their implications for the accounting curriculum. Account. Educ. 2013, 22, 340–356. [Google Scholar] [CrossRef]

- Tencati, A. 24 Corporate Reporting. In A Handbook of Corporate Governance and Social Responsibility; Gower Publishing: New York, NY, USA, 2016; p. 413. [Google Scholar]

- Burritt, R.L.; Hahn, T.; Schaltegger, S. Towards a comprehensive framework for environmental management accounting: Links between business actors and environmental management accounting tools. Aust. Account. Rev. 2002, 12, 39–50. [Google Scholar] [CrossRef]

- Székely, F.; Knirsch, M. Responsible leadership and corporate social responsibility: Metrics for sustainable performance. Eur. Manag. J. 2005, 23, 628–647. [Google Scholar] [CrossRef]

- Perrini, F.; Tencati, A. Sustainability and Stakeholder Management: The Need for New Corporate Performance Evaluation and Reporting Systems. Bus. Strategy Environ. 2006, 15, 296–308. [Google Scholar] [CrossRef]

- Onyali, C.I.; Okafor, T.G.; Benjamin, O. Effectiveness of triple bottom-line disclosure practice in Nigeria-Stakeholders perspective. Eur. J. Account. Audit. Finance Res. 2015, 3, 45–61. [Google Scholar]

- Deloitte CFO Insights. Sustainability: Developing Key Performance Indicators, Measuring Sustainability Is the Bottom Line. 2009. Available online: www.deloitte.com/us/cfocenter (accessed on 14 October 2016).

- Jones, P.; Comfort, D.; Hillier, D. Corporate social responsibility and the UK’s top ten retailers. Int. J. Retail Distrib. Manag. 2005, 33, 882–892. [Google Scholar] [CrossRef]

- Fauzi, H.; Idris, K.M. The relationship between CSR and financial performance: New evidence from Indonesia Companies. Issues Soc. Environ. Account. 2009, 3, 66–87. [Google Scholar] [CrossRef]

- Erol, I.; Sencer, S.; Sari, R. A new fuzzy multi-criteria framework for measuring sustainability performance of a supply chain. Ecol. Econ. 2011, 70, 1088–1100. [Google Scholar] [CrossRef]

- Buchholz, R. Principles of Environmental Management: The Greening of Business; Prentice Hall: Englewood Cliffs, NJ, USA, 1993. [Google Scholar]

- Welford, R. Cases in Environmental Management and Business Strategy; Pitman: London, UK, 1994. [Google Scholar]

- Jaffe, A.B.; Peterson, S.R.; Portney, P.R.; Stavins, R.N. Environmental regulations and the competitiveness of U.S. manufacturing. What does the evidence tell us? J. Econom. Lit. 1995, 33, 132–163. [Google Scholar]

- Porter, M.; Van der Linde, C. Green and competitive: Ending the stalemate. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar]

- King, A.A.; Lenox, M.J. Does it really pay to be green? An empirical study of firm environmental and financial performance. J. Ind. Ecol. 2001, 5, 105–116. [Google Scholar] [CrossRef]

- Schaltegger, S.; Synnestvedt, T. The link between ‘green’ and economic success: Environmental management as the crucial trigger between environmental and economic performance. J. Environ. Manag. 2002, 65, 339–346. [Google Scholar]

- Jayanti, R.K.; Gowda, M.R. Sustainability dilemmas in emerging economies. IIMB Manag. Rev. 2014, 26, 130–142. [Google Scholar] [CrossRef]

- Wyeth, G.B.; Nulkar, G. Sustainability in emerging markets: Evidence from India. Sustain. J. Record 2014, 7, 109–115. [Google Scholar] [CrossRef]

- Manrique, S.; Martí-Ballester, C.P. Analyzing the effect of corporate environmental performance on corporate financial performance in developed and developing countries. Sustainability 2017, 9, 1957. [Google Scholar] [CrossRef]

- Burgess, T.F.; Ong, T.S.; Shaw, N.E. Traditional or contemporary? The prevalence of performance measurement system types. Int. J. Product. Perform. Manag. 2007, 56, 583–602. [Google Scholar] [CrossRef]

- Saxena, R.; Khandelwal, R.K. Can Green Marketing be used as a tool for Sustainable Growth? A Study Performed on Consumers in India- An Emerging Economy. Int. J. Environ. Cult. Econ. Soc. Sustain. 2010, 6, 277–291. [Google Scholar] [CrossRef]

- Chenhall, R.H.; Langfield-Smith, K. Multiple perspectives of performance measures. Eur. Manag. J. 2007, 25, 266–282. [Google Scholar] [CrossRef]

- Rejc, A. Toward contingency theory of performance measurement. J. East Eur. Manag. Stud. 2004, 9, 243–264. [Google Scholar] [CrossRef]

- Betts, T.K.; Wiengarten, F.; Tadisina, S.K. Exploring the impact of stakeholder pressure on environmental management strategies at the plant level: What does industry have to do with it? J. Clean. Prod. 2015, 92, 282–294. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Freeman, R. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Scholtens, B. A note on the interaction between corporate social responsibility (CSR) and financial performance. Ecol. Econ. 2008, 68, 46–55. [Google Scholar] [CrossRef]

- Kitzmueller, M.; Shimshack, J. Economic perspectives on corporate social responsibility. J. Econ. Lit. 2012, 50, 51–84. [Google Scholar] [CrossRef]

- Ferreira, A.; Moulang, C.; Hendro, B. Environmental management accounting and innovation: An exploratory analysis. Accounting, Audit. Account. J. 2010, 23, 920–948. [Google Scholar] [CrossRef]

- Nayha, A.; Horn, S. Environmental sustainability–aspects and criteria in forest bio-refineries. Sustain. Account. Manag. Policy J. 2012, 3, 161–185. [Google Scholar] [CrossRef]

- Ilinitch, A.Y.; Soderstrom, N.S.; Thomas, T.E. Measuring corporate environmental performance. J. Account. Public Policy 1998, 17, 383–408. [Google Scholar] [CrossRef]

- Bartolomeo, M.; Bennettl, M.; Bouma, J.J.; Heydkamp, P.; James, P.; Wolters, T. Environmental management accounting in Europe: Current practice and potential. Eur. Account. Rev. 2000, 9, 31–52. [Google Scholar] [CrossRef]

- Marc, J.E. Implementing Corporate Sustainability: Measuring and Managing Social and Environmental Impacts. Strateg. Financ. 2008, 89, 24–31. [Google Scholar]

- John, M. Environmental sustainability: A definition for environmental professionals. J. Environ. Sustain. 2011, 1, 19–27. [Google Scholar]

- IFAC. International Guidance Document of EMA, IFAC. 2005. Available online: http://www.ifac.org (accessed on 23 September 2017).

- Hanson, J.D.; Melnyk, S.A.; Calantone, R.J. Core values and environmental management. Greener Manag. Int. 2004, 46, 29–40. [Google Scholar] [CrossRef]

- Govindarajulu, N.; Daily, B.F. Motivating employees for environmental improvement. Ind. Manag. Data Syst. 2004, 104, 364–372. [Google Scholar] [CrossRef]

- Gilbert, G.R.; Veloutsou, C.; Goode, M.M.H.; Moutinho, L. Measuring customer satisfaction in the fast food industry: A cross-national approach. J. Serv. Mark. 2004, 18, 371–383. [Google Scholar] [CrossRef]

- Ramus, C. Organizational support for employees: Encouraging creative ideas for environmental sustainability. Calif. Manag. Rev. 2001, 43, 85–105. [Google Scholar] [CrossRef]

- Kuo, Y.K. Organizational commitment in an intense competition environment. Ind. Manag. Data Syst. 2012, 113, 39–56. [Google Scholar] [CrossRef]

- Gadenne, D.; Mia, L.; Sands, J.; Winata, L.; Hooi, G. The influence of sustainability performance management practices on organisational sustainability performance. J. Account. Organ. Chang. 2012, 8, 210–235. [Google Scholar] [CrossRef]

- Maletič, M.; Maletič, D.; Gomišček, B. The impact of sustainability exploration and sustainability exploitation practices on the organisational performance: A cross-country comparison. J. Clean. Prod. 2016, 138, 158–169. [Google Scholar] [CrossRef]

- Wadongo, B.; Abdel-Kader, M. Contingency theory, performance management and organisational effectiveness in the third sector: A theoretical framework. Int. J. Product. Perform. Manag. 2014, 63, 680–703. [Google Scholar] [CrossRef]

- Kitazawa, S.; Sarkis, J. The relationship between ISO 14000 and continuous source reduction. Int. J. Oper. Prod. Manag. 2000, 20, 225–248. [Google Scholar] [CrossRef]

- Sita Nirmala Kumaraswamy, K.; Chitale, C.M. Collaborative knowledge sharing strategy to enhance organizational learning. J. Manag. Dev. 2012, 31, 308–322. [Google Scholar] [CrossRef]

- Chabowski, B.R.; Mena, J.A.; Gonzalez-Padron, T.L. The structure of sustainability research in marketing, 1958–2008: A basis for future research opportunities. J. Acad. Mark. Sci. 2011, 39, 55–70. [Google Scholar] [CrossRef]

- Jabar, J.; Soosay, C.; Santa, R. Organisational learning as an antecedent of technology transfer and new product development: A study of manufacturing firms in Malaysia. J. Manuf. Technol. Manag. 2011, 22, 25–45. [Google Scholar] [CrossRef]

- Luca, N.R.; Suggs, L.S. Strategies for the social marketing mix: A systematic review. Soc. Mark. Q. 2010, 16, 122–149. [Google Scholar] [CrossRef]

- Drejer, A. Integrating Product and Technology Development. Eur. J. Innov. Manag. 2004, 3, 125–136. [Google Scholar] [CrossRef]

- Figueiredo, P.N. Does technological learning pay off? Inter-firm differences in technological capability-accumulation paths and operational performance improvement. Res. Policy 2002, 31, 73–94. [Google Scholar] [CrossRef]

- Horbach, J. Determinants of environmental innovation—New evidence from German panel data sources. Res. Policy 2008, 37, 163–173. [Google Scholar] [CrossRef]

- Link, A.N.; Siegel, D.S. Unions and technology adoption: A qualitative analysis of the use of real-time control systems. J. Labour Res. 2002, 23, 615–630. [Google Scholar] [CrossRef]

- Slack, N.; Chambers, S.; Johnston, R. Chapter 8: Process Technology. Pearson Education: Operation Management (4th Ed.). Available online: http://wps.pearsoned.co.uk/ema_uk_he_slack_opsman _4/17/4472/1144941.cw/index.html (accessed on 18 February 2018).

- Dedhia, P.; Doshi, H.; Rane, M. Low Powered Solar ECG with ZigBee Based Bio-Telemetry. J. Technol. Innov. Renew. Energy 2012, 1, 23. [Google Scholar] [CrossRef]

- Teh, B.H.; Jaffar, N.; Ong, T.S. Sustainable Performance Measurement (SPMs) Model: Effects of Product Technology and Process Technology. Pertan. J. Soc. Sci. Hum. 2015, 23, 35–103. [Google Scholar]

- Zachary, M.A.; McKenny, A.; Short, J.C.; Payne, G.T. Family business and market orientation construct validation and comparative analysis. Fam. Bus. Rev. 2011, 24, 233–251. [Google Scholar] [CrossRef]

- Chung, J.E.; Huang, Y.; Jin, B.; Sternquist, B. The impact of market orientation on Chinese retailers’ channel relationships. J. Bus. Ind. Mark. 2011, 26, 14–25. [Google Scholar] [CrossRef]

- Hill, Wee and Udayasankar International Business: An Asian Perspective; Mcgraw-Hill: New York, NY, USA, 2012.

- Mourdoukoutas, P.; Mourdoukoutas, P. Bundling in a semi-global economy. Eur. Bus. Rev. 2004, 16, 522–530. [Google Scholar] [CrossRef]

- Hunt, S.D.; Madhavaram, S. Teaching Marketing Strategy: Using Resource-Advantage Theory as an Integrative Theoretical Foundation. J. Mark. Educ. 2006, 28, 93–105. [Google Scholar] [CrossRef]

- Sharma, S.; Henriques, I. Stakeholder Influences on Sustainable practices in the Canadian Forest Products Industry. Strateg. Manag. J. 2005, 26, 159–180. [Google Scholar] [CrossRef]

- Ahmad, N.N.N.; Sulaiman, M. Environmental disclosure in Malaysian annual report: A legitimacy theory perspectives. Int. J. Commer. Manag. 2004, 14, 44–58. [Google Scholar] [CrossRef]

- Carlman, I. The rule of sustainability and planning adaptivity. Sustain. Coastal Zone Manag. 2013, 34, 163–168. [Google Scholar] [CrossRef]

- ACCA Professional Accountant Paper P1 BBP Learning Media; BPP Learning Media: London, UK, 2010; Chapter 1; p. 56.

- Bursa Malaysia. Media Release. 2010. Available online: http://bursa.listedcompany.com/newsroom/Media_Release_ 23Nov2010.pdf (accessed on 5 April 2017).

- Hess, D.; Warren, D.E. The meaning and meaningfulness of corporate social initiatives. Bus. Soc. Rev. 2008, 113, 163–197. [Google Scholar] [CrossRef]

- Awang, Z. Structural Equation Modeling Using AMOS Graphic; Penerbit Universiti Teknologi MARA: Selangor, Malaysia, 2012. [Google Scholar]

- Rosen, M.A.; Kashawy, H.A. Sustainable Manufacturing and Design: Concepts, practices and needs. Sustainability 2012, 4, 154–174. [Google Scholar] [CrossRef]

- Heng, T.B.; Lee, C.L.; Foong, Y.P.; Ong, T.S. A framework of a sustainable performance measurements (SPMS) model for the Malaysian electronic and electrical industry. World Appl. Sci. J. 2012, 20, 107–119. [Google Scholar] [CrossRef]

- Ferreira, A.; Otley, D. Design and Use of Management Control Systems: An Analysis of the Interaction between Design Misfit and Intensity of Use; Working Paper; Chartered Institute of Public Finance and Accountancy (CIPFA): London, UK, 2010. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Commodities and Others | Manufacturers |

|---|---|---|

| 1970 | 92% | 8% |

| 1979 | 82% | 18% |

| 1991 | 39% | 61% |

| 2000 | 20% | 80% |

| 2009 | 22% | 78% |

| 2014 | 21% | 79% |

| 2015 | 20% | 80% |

| Jan–Sept 2016 | 17% | 83% |

| Construct/Variables | Operationalization |

|---|---|

| Contingent Factors | |

| (1) Organizational Learning Culture (LC) | (1) Ensure employees understand SPMs |

| (2) Employees’ understanding of SPMs is high | |

| (3) Employee opportunity to learn SPMs | |

| (4) Employee opportunity to practice the SPMs | |

| (5) Company does not fully utilize its expertise | |

| (6) Company has enough expertise to cope with the changes | |

| (7) Learning as a key to improvement | |

| (8) Key personnel involved in performance reporting process | |

| (9) Plenty of employees involved in the performance reporting process | |

| (10) Performance reporting process is formal | |

| (11) Transparent performance reporting | |

| (2) Advancement of Technology (AT) | (1) Product complexity |

| (2) Expansion of product range | |

| (3) Standardized products | |

| (4) Utilization of parts or components | |

| (5) Mass/line production | |

| (6) Unique and customized products | |

| (7) Capital intensity | |

| (3) Globalization (GB) | (1) Frequency of changes in marketing practices |

| (2) Obsolescence of product | |

| (3) Unpredictability of competitors’ actions | |

| (4) High entrants of competitors | |

| (5) Unpredictable change in customer demand | |

| (6) Unpredictable change in consumer taste | |

| (7) Engagement in international trade | |

| (8) Collaboration with foreign companies | |

| (9) The major customers’ group target in Western countries | |

| (4) Pressure from Stakeholders (PS) | (1) Business-friendly rules and regulations |

| (2) Environmentally and socially friendly rules and regulations | |

| (3) Increased mandatory rules for environmental and social needs | |

| (4) Freedom in doing business | |

| (5) Consideration of shareholder interest | |

| (6) Consideration of a wide range of stakeholders’ interests | |

| (7) Growing pressure from stakeholders’ demands | |

| (8) Influence of employees | |

| (9) Influence of government | |

| (10) Influence of pressure groups | |

| (11) Influence of media | |

| Indicators of SPMs (SpamI) | |

| Economic Indicators (EcI) | (1) The revenue earned by the company |

| (2) The interest of the shareholders | |

| (3) The interest of the employees | |

| (4) The interest of the government | |

| Environment Indicators (EnI) | (1) The productivity of resources |

| (2) The intensity of renewable resources | |

| (3) Reuse or recycling of resources | |

| (4) Intensity of waste management | |

| (5) Intensity of pollution or omission | |

| (6) Investment in awareness and protection on environmental sustainability | |

| Social Indicators (SoI) | (1) The issue of labour or employment |

| (2) The productivity of employees | |

| (3) The equality of employees | |

| (4) Satisfaction of customer | |

| (5) Initiative on community and corporate philanthropy | |

| Control Variable | |

| Size | No. of full-time employees |

| Item | No. of Companies |

|---|---|

| The Electrical and Electronics Association of Malaysia (TEEAM) | 1600 |

| Federation of Malaysian Manufacturers (FMM) | 2135 |

| Final list from both TEEAM and FMM | 2212 |

| Selected sample size (50% of the final list) | 1106 |

| Received questionnaire | 255 |

| Final sample after filtering | 217 |

| Response rate based on final useable responses | 19.7% |

| Variable | Response | Number of Cases | Mean | Standard Deviation | Std. Error Mean | Mean Difference |

|---|---|---|---|---|---|---|

| Organizational learning culture (LC) | Early | 130 | 3.748 | 1.111 | 0.133 | 0.088 |

| Late | 87 | 3.660 | 0.931 | 0.132 | ||

| Advancement of technology (AT) | Early | 130 | 3.710 | 1.073 | 0.123 | 0.061 |

| Late | 87 | 3.649 | 0.989 | 0.140 | ||

| Globalization (GB) | Early | 130 | 3.478 | 1.032 | 0.123 | 0.037 |

| Late | 87 | 3.441 | 0.941 | 0.133 | ||

| Pressure from stakeholders (PS) | Early | 130 | 3.579 | 0.925 | 0.111 | 0.036 |

| Late | 87 | 3.543 | 0.887 | 0.125 | ||

| Indicators of SPMs (SpmI) | Early | 130 | 3.970 | 0.982 | 0.115 | 0.046 |

| Late | 87 | 3.924 | 0.956 | 0.110 |

| Frequency | Percentage (%) | ||

|---|---|---|---|

| Location | Klang Valley | 135 | 62.2 |

| Non-Klang Valley | 82 | 37.8 | |

| Total | 217 | 100.0 | |

| Ownership | Malaysian-owned | 149 | 68.6 |

| Joint-Venture | 34 | 15.7 | |

| Foreign-owned | 34 | 15.7 | |

| Total | 217 | 100.0 | |

| Age (Operational Year *) | New (≤10 years) | 63 | 29.0 |

| Middle (11 to 20 years) | 67 | 30.9 | |

| Old (>20 years) | 87 | 40.1 | |

| Total | 217 | 100.0 | |

| Size (No. of employees *) | Small (≤74 full-time employees) | 113 | 52.1 |

| Medium (75 to ≤200 full-time employees | 36 | 16.6 | |

| Large (≥200 employees) | 68 | 31.3 | |

| Total | 217 | 100.0 | |

| Ref | Central Tendency | Variability | Others | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Mean | Median | Mode | S.D. | Variance | Range | Minimum | Maximum | ||

| Factors Influencing SPMs # | |||||||||

| (1) Organisational Learning Culture | LC | 3.71 | 4 | 4 | 0.98 | 0.97 | 4 | 1 | 5 |

| (2) Advancement of Technology | AT | 3.63 | 4 | 4 | 0.98 | 0.96 | 4 | 1 | 5 |

| (3) Globalization | GB | 3.45 | 3 | 3 | 1.02 | 1.03 | 4 | 1 | 5 |

| (4) Pressure from stakeholders | PS | 3.55 | 4 | 4 | 1.10 | 1.20 | 4 | 1 | 5 |

| Indicators of SPMs * (SpmI) | |||||||||

| (1) Economic Indicators | EcI | 4.13 | 4 | 4 | 0.81 | 0.66 | 4 | 1 | 5 |

| (2) Environmental Indicators | EnI | 3.73 | 4 | 4 | 0.94 | 0.89 | 4 | 1 | 5 |

| (3) Social Indicators | SoI | 4.08 | 4 | 4 | 0.82 | 0.67 | 4 | 1 | 5 |

| Construct | Pre-Fitness Adjustment | Post-Fitness Adjustment | ||||

|---|---|---|---|---|---|---|

| Cronbach Alpha | CR | AVE | Cronbach Alpha | CR | AVE | |

| Factors influencing SPMs | ||||||

| Organizational Learning Culture (LC) | 0.823 | 0.976 | 0.434 | 0.928 | 0.969 | 0.656 |

| Advancement of Technology (AT) | 0.788 | 0.973 | 0.428 | 0.840 | 0.946 | 0.706 |

| Globalization (GB) | 0.720 | 0.969 | 0.381 | 0.826 | 0.933 | 0.508 |

| Pressure form stakeholders (PS) | 0.923 | 0.989 | 0.542 | 0.929 | 0.953 | 0.648 |

| Indicators of SPMs (SpmI) | ||||||

| Indicators of SPMs (SpmI) | 0.777 | 0.976 | 0.557 | 0.865 | 0.975 | 0.567 |

| Economic (EcI) | 0.572 | 0.954 | 0.368 | 0.725 | 0.971 | 0.508 |

| Environment (EnI) | 0.785 | 0.978 | 0.467 | 0.861 | 0.974 | 0.563 |

| Social (SoI) | 0.607 | 0.938 | 0.237 | 0.703 | 0.964 | 0.531 |

| LC | AT | GB | PS | SpmI | |

|---|---|---|---|---|---|

| LC | 1.000 | ||||

| AT | 0.635 | 1.000 | |||

| GB | 0.595 | 0.556 | 1.000 | ||

| PS | 0.603 | 0.550 | 0.528 | 1.000 | |

| SpmI | 0.242 | 0.485 | 0.378 | 0.466 | 1.000 |

| Fit Statistics | Initial Measurement Model | Modified Measurement Model |

|---|---|---|

| Chi-square (χ2) | 4210.438 | 548.099 |

| Degree of Freedom (df) | 1363 | 259 |

| P-Value | 0.000 | 0.000 |

| RMSEA | 0.098 | 0.072 |

| GFI | 0.543 | 0.840 |

| AGFI | 0.502 | 0.799 |

| CFI | 0.622 | 0.903 |

| TLI | 0.603 | 0.888 |

| NFI | 0.530 | 0.833 |

| x2/df | 3.089 | 2.116 |

| Coefficients | Standard Error | Critical Ratio (C.R.) | P Value | |||

|---|---|---|---|---|---|---|

| SpmI | <--- | LC | 0.017 | 0.193 | 0.087 | 0.930 |

| SpmI | <--- | AT | −0.299 | 0.142 | −2.104 | 0.104 |

| SpmI | <--- | GB | 0.454 | 0.112 | 4.056 | 0.000 *** |

| SpmI | <--- | PS | 0.580 | 0.166 | 3.511 | 0.000 *** |

| SpmI | <--- | Size | 0.003 | 0.073 | 1.563 | 0.118 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ong, T.S.; Teh, B.H.; Lee, A.S. Contingent Factors and Sustainable Performance Measurement (SPM) Practices of Malaysian Electronics and Electrical Companies. Sustainability 2019, 11, 1058. https://doi.org/10.3390/su11041058

Ong TS, Teh BH, Lee AS. Contingent Factors and Sustainable Performance Measurement (SPM) Practices of Malaysian Electronics and Electrical Companies. Sustainability. 2019; 11(4):1058. https://doi.org/10.3390/su11041058

Chicago/Turabian StyleOng, Tze San, Boon Heng Teh, and Ah Suat Lee. 2019. "Contingent Factors and Sustainable Performance Measurement (SPM) Practices of Malaysian Electronics and Electrical Companies" Sustainability 11, no. 4: 1058. https://doi.org/10.3390/su11041058

APA StyleOng, T. S., Teh, B. H., & Lee, A. S. (2019). Contingent Factors and Sustainable Performance Measurement (SPM) Practices of Malaysian Electronics and Electrical Companies. Sustainability, 11(4), 1058. https://doi.org/10.3390/su11041058