1. Introduction

Innovation is one of the fundamental driving forces for the sustainable development of the world. Researchers have reached a consensus that uninterrupted long-term R&D investment can create better innovation results than short-term [

1,

2]. Therefore, maintaining sustainable R&D investment is critical for the sustainable development of the world [

2]. However, because of the long-term nature and the asymmetric information, R&D investment is readily subject to financial constraints [

3,

4].

Much research has been done to explore factors that can maintain sustainable R&D investment under financial constraints, such as cash flow [

5], leverage reduction [

6], equity financing [

5,

7,

8], corporate tax reform [

9], fixed asset sales [

10], working capital management [

11], credit lines [

12], managerial risk-taking incentives [

13], public subsidies [

14], foreign acquisitions [

2], environmental regulations [

15], and political connections [

2]. The EBSCO and Web of Science databases were searched with “R&D” and “financial constraints” keywords with the purpose of a mapping state of the art, yielding the following relevant studies presented in

Table 1.

From the review of existing literature, the following research gaps still exist. First of all, the research perspective of existing researches is within the enterprise, or from the institution environment. Research from the perspective of enterprise between enterprises is still lacking.

Secondly, existing researches are mainly based on the full sample of enterprises or large enterprises, and there are few studies on SMEs. Due to the limitations of size and low-transparency financial statements, factors (like stock issues, fixed asset sales, foreign acquisitions etc.) are difficult to apply to SMEs to maintain the sustainability of R&D investment. In this field of research, research on SMEs is still lacking.

Relatedly, the effect of trade credit between enterprises played in the allocation of financial resources has been widely discussed [

17,

18]. Financial resources are allocated to enterprises through formal financial intermediaries. This is the initial allocation of financial resources. Financial resources may also be reassigned subsequently. Trade credit has an important effect on the secondary distribution of financial resources. Enterprises that have easy access to initial allocation of financial resources can use trade credit to provide financial support to enterprises which have difficulty in obtaining external financing [

19].

Drawing from the above discussion, this paper attempts to study the effect of trade credit in R&D investment of SMEs under financial constraints. As far as we know, no previous researches have been done to study the relationship between trade credit and the sustainable R&D investment of SMEs under financial constraints. This paper collected listed Chinese SMEs’ data from 2007 to 2014 and studied the relationship between trade credit and R&D investment based on the Euler equation developed by Laeven [

20], which had been widely used in the relevant researches [

21,

22,

23,

24]. The results show that SMEs experience financial constraints on their R&D investments; trade credit can maintain the sustainability of R&D investment in SMEs under financial constraints; the effect of trade credit is more significant for private SMEs than the non-private SMEs; the effect of trade credit is more significant during periods of tight monetary policy. Furthermore, several robust tests were conducted, including changing the data structure by only retaining samples with five-consecutive-years data, and using a propensity score matching model. The conclusions still held.

This paper makes the following contributions to the literature.

First, the article confirms a new factor that can maintain sustainable R&D investment for SMEs. Allen et al. [

25] proposed that the Chinese economy may rely more on informal financing mechanisms. For example, Ding et al. [

26] studied the effect of operating capital on the investments of Chinese enterprises in fixed assets. Based on that view, this paper examined the role of trade credit as an informal financing factor to maintain sustainable R&D investment from the perspective of enterprise between enterprises.

Second, ownership discrimination is the common factor involved in studying China. Given the process of economic transformation, ownership is one of the most important factors in the study of Chinese enterprises. Guariglia and Liu [

27] found that R&D activities of private Chinese firms are constrained by the internal financing, whereas in state-owned and collective enterprises’ R&D activities are the least constrained. Meanwhile, monetary policy is closely connected to the dynamic scale of trade credit since monetary policy affects enterprises’ cash stock, as well as financing and investing decisions, directly determining the degree of trade credit demand.

The paper’s structure is as follows.

Section 2 proposes the hypotheses related to R&D investment of SMEs under financial constraints. Research design is in

Section 3.

Section 4 reports the empirical results.

Section 5 discusses the conclusions.

4. Empirical Results and Discussion

4.1. Test and Method

4.1.1. Unit Root Test

The Fish-PP test is equivalent to the robust ADF test in the situation of heteroscedasticity. We also report Moon and Perron’s (2004) second-generation panel unit root test, which takes account of cross-sectional dependence. As shown in

Table 5, we can use these variables to regress without worrying about the problem of spurious regression.

4.1.2. Tests of Regression Estimation

Table 5 aggregates the result of the multicollinearity test (VIFs) and the heteroscedasticity test which are reported for each regression model in

Table 6. All the VIFs are lower than 10, which means that multicollinearity does not influence the analysis. In addition, compared to long panel data, for which the regression results are more affected by serial correlation, the short panel data used in this article, which have a time period of only eight years, are more influenced by heteroscedasticity. The heteroscedasticity test shows that the chi-squared value is significant at the 1% level.

4.1.3. The Endogeneity and the Estimation Method

To solve the potential endogeneity problem, we used the lag terms of relevant variables as instrumental variables. To ensure the efficiency of the instrumental variables, only one higher-order lag was adopted and at most, the three-lag values of the dependent variable were chosen as instrumental variables. Meanwhile, to address the autocorrelation problem of error terms, we added the first-order lag of dependent variables in the model. Moreover, we choose the system GMM to overcome the problem of weak instrumental variables [

24].

4.2. Empirical Results

The empirical results of this article are composed of two parts. One is the relaxing effect of trade credit on the R&D investment of SMEs, and the other is the contextual effect of ownership and monetary policy. The empirical results are shown in

Table 7.

Laeven [

20] argued that, β

4, the coefficient of internal funds (CF), would be below 0 if the investment behavior of enterprises was free from financial constraints. However, the regression result in Model (1) shows that β

4 is above 0 and significant. This finding indicates that Chinese SMEs experience financial constraints in the process of R&D investment. Accordingly, Hypothesis 1 is supported. Hadlock and Piercen [

40] find that firm size is a good predictor of financial constraints. Because of the problems of adverse selection and moral hazard, SMEs use less external finance than large firms, and they rely more on internal cash flow and bank loans [

41]. Andrieș et al. [

42] also found that higher competition facilitates credit access for SMEs in European countries. Consistent with the above researches, the conclusion of Model (1) also indicates that the uncertainty and long-term characteristics of R&D investment make it easier for SMEs in China to encounter financial constraints.

The coefficient of CF/K*NCR in Model (2) is significantly negative at the significance level of 1%, which is the opposite of that for the coefficients of CF/K. This result indicates that increasing trade credit decreases the sensitivity of R&D investment to cash flows, which means the trade credit can maintain sustainable R&D investment of SMEs under financial constraints. Hypothesis 2 is supported. Campello et al. [

43] found that trade credit can ameliorate the impact of the crisis on corporate profits and employment when the bank loans have been reduced. Levine et al. [

44] found that trade credit can help profits and the employment of firms when banking crises occur. Our findings are consistent with the view that trade credit can be an alternative source of finance for firms under financial constraints.

Model (3) reports the result of regression Equation (3) to test whether the ownership of SMEs will influence the effect of trade credit. In Model (3), the coefficient of CF/K*NCR*State is significantly negative. This finding indicates that the effect of trade credit is more obvious for private SMEs than non-private SMEs. Hypothesis 3 is supported. Lack of financing channels is a major constraint on R&D in China, especially for private enterprises according to Howell [

9]. Weng and Sderbom [

4] showed that the internal capital for R&D expenditure is more extensively relied on by private enterprises than by non-private ones, which explains why private enterprises’ R&D expenditure decisions are subject to financial constraints. The results of our study are consistent with their findings and confirm the existence of a “political pecking order” in China’s credit market.

Model (4) reports the result of regression Equation (4) to test whether monetary policy will influence the effect of trade credit. The coefficient of CF/K* NCR* MP is significantly negative. This finding indicates that the effect of trade credit is more obvious during a tight monetary-policy period. Dajcman (2016) [

45] found that monetary policy measures can affect bank loans through the credit channel, the bank capital channel, and the risk-taking channel. When the financial resources from formal financial intermediaries are reduced, enterprises will rely more on the distribution of secondary financial resources in the form of trade credit. Consistent with existing research [

45], we confirm the effect of trade credit during a period of negative shock in monetary policy.

Furthermore, Model (5) reports the result of regression Equation (4) when the firms are private (State = 1). The coefficient of CF/K*NCR*MP *State is still significantly negative. However, in Model (6), which reports the result of regression Equation (4) when the firms are non-private (State = 0), the coefficient of CF/K*NCR*MP *State is not significantly even at a significance level of 10%. Compared with Model (5) and Model (6), this finding indicates that under a situation of tight monetary policy, the effect of trade credit is stronger for Chinese private SMEs. Hypothesis 4 is supported.

In addition to multivariate measures of trade credit, we conducted regression by changing the data structure to ensure the robustness of the results. Although the number of observations decreases by 1137 after reserving samples with five consecutive years, the time series can be more representative, and the relaxing effect of trade credit on R&D investment can be better reflected in continuous years. The empirical results are shown in

Table 8.

From

Table 8, the existence of financial constraints reflected by the coefficient of CF/K in Model (7), the effect of trade credit reflected by the coefficient of CF/K *NCR and CF/K

t*CR in Models (8), the effect of ownership reflected by the coefficient of CF/K*NCR*State in Model (9), the effect of monetary policy reflected by the coefficient of CF/K*NCR*MP in Model (10), and the joint effect of ownership and monetary policy reflected by the coefficient of CF/K

t*NCR *MP in Model (11) and Model (12) all show the same results as those reported in

Table 4. Moreover, the coefficient and the significance level are all improved since the samples with consecutive years can better reveal the effect. Therefore, we conclude that the results of this study are robust and unaffected by changing the sample size and data structure.

We also add the fixed effect model and the random effect model in

Table 9 as the robust test to compare with the results from GMM estimations. The results of this study are robust and unaffected by changing the estimation model.

4.3. Counterfactual Robust Test Based on Propensity Score Matching (PSM)

This article uses the system GMM to test the relaxing effect of trade credit on the R&D investments of SMEs. However, we cannot use this method to observe both the high conditions of trade credits and the low conditions of trade credits of a given enterprise simultaneously. It may cause a problem of missing data. The consequence is that we cannot be sure whether the high R&D investment of a given enterprise is entirely attributable to the higher trade credit of this enterprise compared to the trade credits of other enterprises. However, if we can confirm that the R&D investment for the same enterprise is higher in its high condition of trade credit than its low condition of trade credit, then the selection bias caused by different conditions of trade credit can be avoided.

Based on a counterfactual framework, we divided the sample enterprises into a group with high trade credit having an NCR equal to or above zero and a group with a low trade credit having an NCR below zero. If the difference between these two groups can be explained by the same variables set in advance, then we can use the variables to pair the samples level by level so that the two paired sample groups differ only in trade credit while remaining the same in other aspects. Finally, we can confirm the causal relationship between trade credit and R&D investment while avoiding the selection bias caused by missing data. Compared to the time-consuming stratified pairing by a single factor, PSM (Propensity Score Matching) is more efficient for multi-factor matching by concentrating several factors into one index: the propensity score (PS).

Under the given sample feature of

X, the conditional probability of an enterprise’s high trade credit is as follows:

Di is an index function, assigned the value of one to act as the treatment group if the trade credit is high (NCR ≥ 0); otherwise, it is assigned the value of zero to act as the control group if the trade credit is low (NCR < 0).

X is the matching variable, which determines whether enterprises are in a situation with high or low trade credits. Referring to a current study on trade credit, this article chooses variables that may affect trade credit of enterprises, such as the proportion of available mortgage assets (F/A), secured bank loans (LOAN), the growth rate of the operating revenue (GROWTH), the operating cash flow (OCFL) etc. If the trade-credit situation is random, we can use a binary choice model to estimate the situation, letting

Pr[

Di = 1|

Xi] represent the probability of high trade credit under

X. Furthermore, we can match the treatment group and the control group according to their similarity of probability, whose efficiency depends on conditional independence and overlapping assumption. The Average Treatment Effect of trade credit on R&D investment is as follows:

N1 is the number of enterprises in the treatment group. There are various weight indexes of

w(

i,

j) for different matching methods. Since kernel matching does not have the problem of invalid standard deviation [

46], this article adopts this approach to conduct PSM. The formula of weight shows as follows, with h representing bandwidth, and

K representing the kernel function:

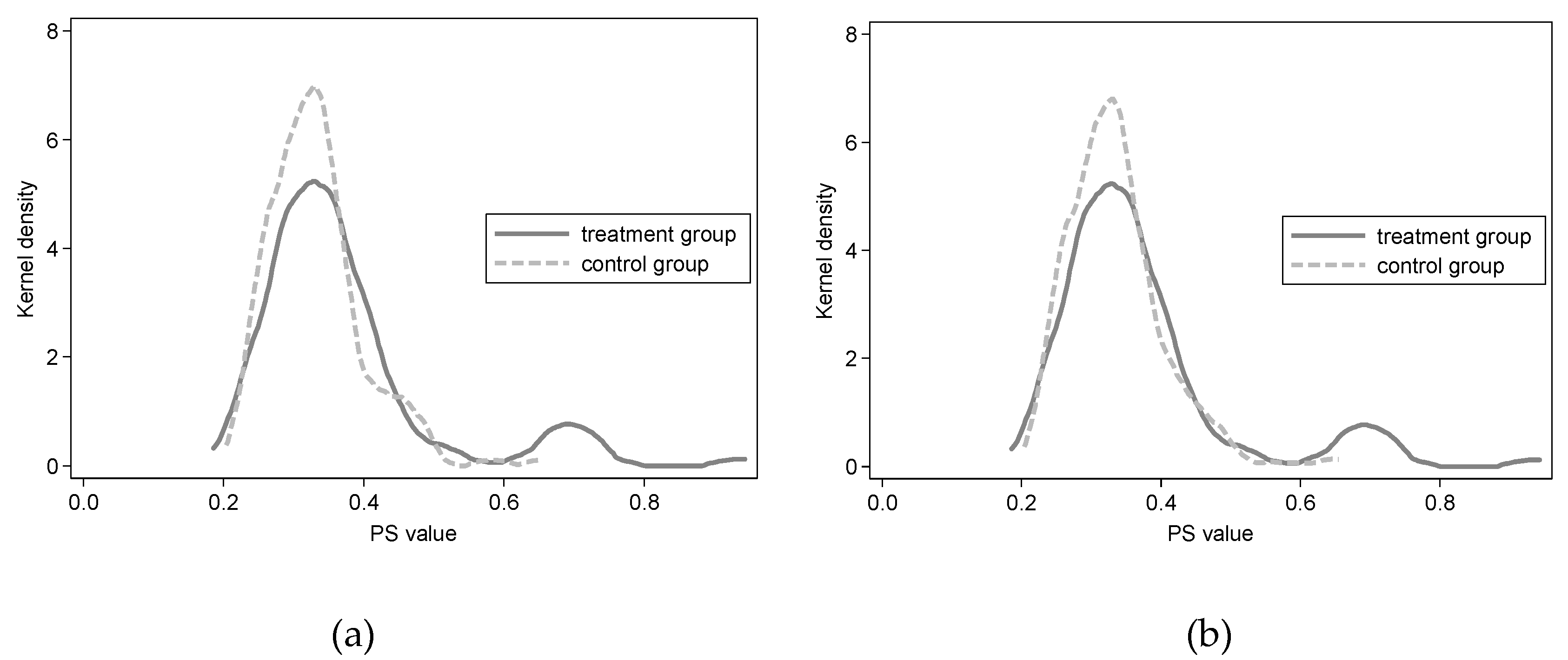

Figure 1 depicts the kernel density distribution of propensity scores for high trade credit (treatment group) and low trade credit (control group). Sub-diagrams (a) and (b) represent the kernel density functions of the PS values of each group before and after matching, respectively. In comparison, the probability distributions of the PS values of the treatment and control groups are closer after matching. This finding indicates that adopting kernel matching under the probit model is effective. Moreover, we achieved similar results under the logit model; those results are not presented separately here.

As

Table 10 shows, the difference between the ATT of the treatment group and the control group after PSM is −0.0036 and −0.0035 in the probit model and the logit model, and their T values are both significant at a significance level of 5%. This means that under the situation of financial constraints and internal funds fluctuation, enterprises will use trade credit for R&D investment at high adjustment costs, which is consistent with the empirical result of the regression. Therefore, we can confirm that trade credit can maintain sustainable R&D investment of SMEs under financial constraints after considering the counterfactual situation.

The reported standard errors are deduced by assuming that the propensity scores are the real values, whereas the assumption of the standard errors’ homoscedasticity is likely to be false. Moreover, the potential bias from a small sample size could also affect the conclusion. Thus, this article reports the standard errors using the bootstrap method. The steps of the bootstrap method are as follows: (1) repeatedly draw random samples with size n as empirical samples from the original samples; (2) calculate the ATT of empirical samples using the kernel matching method; (3) repeat the above two steps 500 times to obtain 600 empirical statistics of ATT, ATT

1, ATT

2, …, ATT

500; and (4) calculate the standard deviation of the 500 ATT values to obtain the standard error of the ATT statistic of the original samples. From the last two columns of

Table 10, the Z values all remain significant at the significance level of 1% under the probit and logit models, even when using the bootstrap standard errors.

To test the balance of matching, we followed Smith and Todd [

47] to calculate the standard deviations between the treatment group and the control group based on the matching variables after kernel matching.

As shown in

Table 11, the percentage biases are all below 20%, which will not cause the matching to fail [

48], proving the appropriateness of matching variables and kernel matching. The matching results meet the requirement of matching balance.

After considering the counterfactual situation, we can still obtain the same conclusion, which is consistent with the results of the system GMM.

5. Conclusion and Discussion

SMEs are the indispensable players for promoting sustainable R&D investment. R&D investment has positive impacts on financial performance in both the current and the lag periods [

49]. Therefore, it is very important to research the subject of sustainable R&D investment of SMEs under financial constraints. Based on existing research, this paper takes Chinese listed SMEs between 2007 to 2014 as samples to test empirically the relaxing effect of trade credit on R&D investment under financial constraints. The results show that SMEs in China are typically trapped by severe financial constraints. As an informal financing factor, trade credit can relax financial constraints of R&D investment for Chinese SMEs. Furthermore, private enterprises are more reliant than non-private enterprises on the relaxing effect of trade credit, and this effect is stronger during periods of tight monetary policy. Our results also can be generalized to other developing countries like China with GDP per capita below the World Bank Standards.

The conclusion of this study is significant for both micro business management and macro policy formulation:

First, SMEs in developing countries should regulate their financial management and establish a perfect system to disclose adequate information related to finance and R&D activities. In this way, both the enterprises’ credit risks and the banks as well as other external creditors’ information-searching costs can be reduced. Banks and investors will be more confident in enterprises’ R&D and will provide enough funds for R&D investment.

Second, SMEs in developing countries should build regional cooperation networks and industry alliances to ensure an adequate trade-credit supply. They can make full use of the effect of industrial agglomeration and relieve the financial constraints of R&D investments by cooperating with upstream and downstream enterprises in the long run and receiving an adequate supply of trade credit.

Third, different monetary policies will exert influence not only on SMEs’ financing environment through bank loans but also on the role of alternative informal financing channels such as trade credit. Therefore, the government should consider the chain reaction of a given monetary policy and comprehensively consider the orientation and change range of its policy so that it can avoid the negative economic reactions caused by a range that is either too loose or too short when making monetary policy.

Further research can be undertaken in the following directions. First, our regressions are only based on the Euler equation model, so it would be interesting to test whether the results are robust when using other models. Second, informal financing channels are also important in other developing countries, so it would be interesting for researchers in these counties to test whether the results are robust. Third, to rule out the impact of equity financing, we used listed firms, so it would be interesting to test whether the results also hold for unlisted firms. Fourth, some studies have emphasized making a distinction between “research” (R) and “development” (D). However, the data from listed firms in China prevented us from conducting such an exercise.

Finally, limited by research power, we did not consider the issues of location and company sector of activity in this paper. They are issues worthy of future research.

{kind=link}