Abstract

According to the European University Association, nowadays financial sustainability is one of the key challenges for Higher Education Institutions. The financial sustainability of public universities is threatened by cutbacks in public funding and by society’s growing demand for improvements to the volume and quality of services provided. A recent reform in Italy has determined that universities are required to move to accrual accounting, starting from the assumption that this system responds more effectively to issues relating to financial stability control. This paper evaluates whether the new financial reporting system is better placed to represent the universities’ conditions of financial sustainability. Moreover, specific measures have been developed to investigate which financial strategies, if any, have been adopted in Italian universities to react to the new competitive context. Working in collaboration with practitioners from the HE sector, the research team developed a framework based on specific financial ratios to assess the financial sustainability of these institutions and to analyse their financial strategies. The findings reveal that, notwithstanding some common features, there are significant variations between Italian universities and they are addressing the new challenges with a range of different approaches.

1. Introduction

Sustainability is generally conceived as the combination of variously interrelated economic, social, and environmental aspects; the three sectors are often presented as three interconnected rings [1]. With reference to corporations, discussions on sustainable development often prioritize sustaining economic growth and profit in the face of environmental and social disruption [2]. A relevant body of literature examines the effects that current corporate propensity for social and environmental aspects has on a business’s profitability [3,4], thus implicitly embracing a view where environmental and social issues have the aim of supporting economic performance. However, when we speak of the ways of financing investment into sustainability, is important to distinguish between green and sustainable finance. Where the first one is specifically devoted to environmental objectives [5], the latter refers to any form of financial service integrating environmental, social, and governance (ESG) criteria into the business, or investment decisions for the lasting benefit of both clients and society. In particular, green finance aim to finance projects and initiatives that, starting from the environment, encourage the development of a more sustainable economy [6]; moreover, through its activities it also creates a helpful environment for innovative business [7]. In this sense, it acquires greater importance to understand the different financial instruments and actors [8,9] that can be used in the processes of green finance, taking into account even the process activated by public institutions [10]. Whether sponsors are public or private, they need to make a choice between two alternative instruments: The more classical corporate finance, where the sponsor utilizes all its disposable assets, or the project finance, a new instrument where sponsors create a brand new entity, often with private participation [11].

Nevertheless, when considering public sector organizations, a different perspective has to be adopted, as profitability is not an objective in this context. Rather, the aim of public spending is to achieve social and environmental outcomes [12]. The economic facet of sustainability is a prerequisite for continuity in service delivery to ensure that the social and environmental dimensions of development are also met.

What is usually referred to as economic sustainability at macro and meso level can be expressed as financial sustainability at the micro level, i.e., the single institution. This is now a central issue for most public sector organizations [13]. In many countries, the decrease in available financial resources threatens their public institutions’ capacity to provide valuable services to the general public, as well as to preserve material resources, such as long-term assets, and leave them for the next generations. The shortage in financial resources is often joined by requests for better services, thus obliging public sector organizations to embark upon processes of radical change. Internationally, New Public Management (NPM) policies have provided the most widespread answer to the growing requests of taxpayers for more efficient and effective public organizations [14,15,16]. In this respect, accounting systems play a central role, providing managers with the information they need to assess the financial sustainability of public institutions.

This paper explores the issue of financial sustainability with reference to Higher Education Institutions (HEIs) in Italy. According to the European University Association ‘financial sustainability will be one of the key challenges for universities in the next decade: Only those institutions that have sound financial structures and stable income flows will be able to fulfil their multiple missions and respond to the current challenges in an increasingly complex and global environment. Indeed, financial sustainability is not an end in itself; it aims to ensure a university’s goals are reached by guaranteeing that the institution produces sufficient income to enable it to invest in its future academic and research activities’ [17]. Financial sustainability in HEIs therefore consists of three factors: (a) cost containment; (b) income diversification; and (c) sufficient, reliable, and sustainable public funding with appropriate accountability mechanisms. Ultimately, the two constituent elements for financial sustainability in universities are their capacity to attract funds from both government and alternative sources and to be efficient in the execution of their activities.

Over the past ten years, the introduction of a performance-based funding system has stimulated competition for public funds among HEIs [18]. As a consequence, performance measurement has gained in relevance within universities. In addition, the reform of the university accounting system is also contributing to the shift towards a new model of university: An institution that legitimizes itself by being strongly engaged with societal needs and that is accountable for its financial sustainability.

According to the law no. 168/1989, Italian universities were free to adopt their preferred accounting system: With very few exceptions, universities opted for cash accounting, the method predominant in the public sector. The subsequent approval of Law no. 240/2010 enforced the introduction of accrual accounting. The reform was further strengthened by Legislative Decree no. 18/2012, which set out precise guidelines for implementing the new system. Moreover, in January 2014, the Ministry of Education issued Decree no. 19/2014, detailing the accounting standards and the financial reporting rules.

The aim of this paper is to assess whether the new financial reporting system can provide a better picture of the conditions of financial sustainability. To address this purpose, we are proposing a model to analyse the financial performance and position of universities within the context of an accrual-based accounting system. Early evidence comes from an analysis of the first financial statements released by ten Italian public universities after the reform was introduced. This is an opportunity to investigate what financial strategies, if any, HEIs adopt to react to the new competitive landscape emerging from the combined effect of reduced government funds and the introduction of the performance-based funding system.

The paper is structured as follows: After introducing the recent developments in the Italian HE system in Section 2, we then analysed the pertinent literature in Section 3. Section 4 deals with the methodology. The model developed to analyse the financial statements is explained in Section 5, while data collected from universities are presented and discussed in Section 6. The last Section covers the conclusions.

2. Italian Higher Education and Quest for Financial Sustainability

The Italian Higher Education system (HES) has undergone deep reforms over the past ten years. These changes concern nearly every aspect of university life, from their funding systems, the composition and functions of institutional bodies, their academic recruitment procedures, their performance audit processes, the structure of their degree programs and even their accounting systems. All these changes have the common purpose of improving efficiency and effectiveness in HEIs. Similar trends are observed in other countries, although the governance of HE systems varies from country to country [19].

The reform process has changed the organizational rules that regulate the way HEIs function and the governance of the HE system as a whole. Before introducing this reform, central government did not intervene in the design of universities’ goals. These were defined by the academic governance bodies which were the real coordinating mechanism at both institutional and systemic level. Under the new governance process, the Ministry for Education could draw on three important levers to influence the strategies set by universities: (i) a performance-based funding system, (ii) system-wide goals that universities are expected to pursue, and (iii) performance assessed through a national agency.

Despite the government’s demand for better performance, public funding for universities has been reduced. The Italian government’s support to universities fell by 20% in real monetary value from 2008 to 2014 [20]. Their main source of finance (FFO, Ordinary Financing Fund) was reduced by 7.4% between 2009 and 2016; these cutbacks in resource were very challenging for universities, considering that most of their costs are fixed. The new funding system, coupled with cuts in available resources, has boosted competition among universities, meaning that financial sustainability has become an imperative. As Guthrie [21] and Parker and Guthrie [22] projected in the early 1990s, ‘financial discipline’ and ‘efficiency’ have become central to public sector accountability, and universities are now expected to increase their income while lowering their costs. The NPM philosophy of cost containment, outcome maximization and accountability for results has been extended to the world of HE.

Three financial strategies, or combinations thereof, emerged from the analysis, and can enhance financial sustainability:

- (a)

- Domestic Competition Strategy, i.e., the university adopts the strategic goals defined by the Italian Department of HE, where the reasoning is to increase their performance-related part of the governmental block grants. Currently, the main performance measures cover number of students and researcher productivity. Italian universities are in direct competition with each other.

- (b)

- Financial Autonomy Strategy [23], i.e., tapping into alternative sources of funds to counter changes in income. The main streams of income other than government grants are often competitive research grants and market-oriented/for-profit operations (spin-off companies, contracts with corporations…).

- (c)

- Efficiency Improvement Strategy, i.e., cutting costs while avoiding reductions to the quality and volume of services delivered.

With reference to the first strategy, past experience indicates that the Italian ministry makes frequent changes to the performance measures for allocating funds [24]. This variability in competition rules risks hindering longer term planning, thus relegating this strategy to the short-term perspective.

The second strategy is based on better exploiting knowledge and technologies developed within the institution. In Europe, the most widespread strategies set by universities to foster income diversification include establishing spin-off companies and focusing on lifelong learning activities. A much less common strategy is to develop for-profit operations managed by the university itself [17]. With their move towards more targeted funding, governments have increased their steering power over universities, and this can then curtail the latter’s ability to act autonomously. Diversifying revenue streams would thus produce two effects: (a) by counterbalancing the reduction of government funding transfers, income diversification would protect areas that are crucial in terms of fulfilling the universities’ institutional missions, and (b) this would allow universities to regain autonomy. Some scholars argue, however, that income diversification leads to commercialization. Far from offering support to research and education, such a financial strategy would become forcibly embedded within university core values and culture, so that over time ‘universities’ missions, objectives and associated strategies evolve into being increasingly short term, financial, and growth oriented’ [25].

The third policy, i.e., cost reductions, can only help to increase the institutions’ survival prospects in the short term, but cannot lay the groundwork for future growth. Nevertheless, searching for efficiency by cutting spending and budget constraints seems the most suitable policy for institutions unaccustomed to competition and which adopt, as required in the public sector under national law, pre-authorization budgets.

In the light of the abovementioned three financial strategies, the following sections describe an analysis conducted on the financial statements published by ten Italian universities. The new HEI financial reporting model reflects the same structure implemented in for-profit companies. This is a clear indication that the Italian legislator has been informed by the narrative whereby ‘business-like’ universities are more efficient and accountable. The shift from cash to accrual accounting meant that, for the first time in Italy, it has been possible to examine the HEIs’ financial performance.

3. Financial Reporting and the Analysis of Financial Sustainability in Universities: Literature Analysis

Italy’s new accounting system became effective in 2014, although the reform was introduced four years earlier (Law 240/2010). In Italy, the debate on the introduction of accrual accounting has engendered a remarkable body of literature. Most studies deal with technical aspects [26,27,28,29,30] and the organizational consequences of this change [31]. Although the issue of financial sustainability has been examined [32], there is still a lack of studies on the interpretation of financial information.

Woelfel [33] proposed the first framework to analyse university financial sustainability through specific performance measures. The accounting system used in US colleges and universities has since changed, but some of these indicators are still in use. Sazonov et al. [34] proposed other indicators for financial sustainability, mostly focused on working capital, fixed assets, and the sources of capital in universities. The (now defunct) Higher Education Funding Council for England (HEFCE) considered the following performance indicators: (a) total income, (b) operating surplus as % of total income, (c) historical cost surplus as % of total income, (d) cash flow from operating activities as % of total income, (e) net liquidity as number of days’ expenditure, (f) external borrowing as % of total income, (g) discretionary reserves as % of total income [35].

The financial indicators suggested by scholars and consultancy firms are given in Table 1. Each indicator provides information on one specific aspect of financial sustainability. Identifying the constitutive requisites of financial sustainability is as important as the design of the indicators themselves. KPMG [36] suggests five topics:

Table 1.

Summary of literature on financial ratios for Higher Education (HE).

- (1)

- Financial Viability: The ability of an institution to continue to achieve its operating objectives and fulfil its mission over the long term;

- (2)

- Profitability: The determination of whether an institution receives more or less than it spends in an operating cycle;

- (3)

- Liquidity: The ability of an institution to satisfy its short-term obligations with existing assets;

- (4)

- Ability to Borrow: The ability of an institution to assume additional debt;

- (5)

- Capital Resources: An institution’s financial and physical capital base supporting its operations.

The comparability of financial statements is another central issue for public stakeholders. Fischer et al. [38] noted that, in the USA, accounting standards for HEIs allow considerable flexibility in measuring operating performance. This variability, introduced to account for differences among public and private institutions, results in limited harmonization between accounting choices and little comparison possible among financial measures. The coexistence of two standard setters, FASB and GASB, has further accentuated this problem [39]. Christiaens and De Wielemaker [40] observed a similar situation in Belgium, where the vague accounting rules for specific issues (e.g., fixed assets and their depreciation, inventory, libraries, art patrimony) leads to poor compliance with regulations and a deficit in comparability.

4. Methodology

This study is part of a research project developed in collaboration with 19 Italian universities that ran from March to October 2015. The purpose was to define a framework to interpret accrual-based accounting information. Universities joined the research project on a voluntary basis, and were aware that their participation implied the accomplishment of some demanding tasks, i.e., the reclassification of financial statements to extract significant data. The data were gathered between June and October 2015. At that time, the only financial statements available were for 2014, as these were the first set released after the shift to accrual accounting. Only ten of the 19 universities involved in the project were able to discuss their 2014 financial statements and prepare their reclassified statements within the agreed deadline. It is worth noting that, in the early stages of introducing the new accounting system, many universities faced technical problems and delays to the change process. Several of those involved in the project also experienced such difficulties. It was therefore possible to conduct the analysis on only ten institutions.

The financial analysis model was developed in three steps, and each phase started with a plenary session involving the research team and practitioners from the HEIs. The research team presented the project at the first plenary session and outlined it to the other participants, i.e., 49 executives from 19 universities. The practitioners consisted of accountants and accounting information recipients (e.g., general directors), all participants were well-informed about the accounting system reform, as they were personally involved in the process of change within their universities. In the first session, the group discussed the information to be provided through the financial statement analysis and appropriate hypotheses were made about what information reasonably matters for the different classes of stakeholders. The discussions brought up the need to reclassify the financial statements, since the participants noted that the financial statements prepared according to Decree 19/2012 did not provide some pertinent items of financial information (the contribution of the various activities to the operating margin, labour cost breakdown, and the institution’s financial leverage). Moreover, the legislator defined a very detailed layout, a situation that increases complexity and hinders the main financial trends from being recognized.

The research team developed a first draft of the reclassified statements and tested it in two universities. The purpose of the reclassified layout was to improve transparency without creating excessive work for the administrative departments reclassifying the financial statements. This draft was presented to the other practitioners at the second plenary session, gathering input from the participants to amend the original draft and put together an improved version of the reclassified statements. The schemes of these statements are available on request.

The participants were then asked to reclassify their universities’ balance sheets and statements of financial performance according to the methodology agreed with the research team. The 19 HEIs involved in the project received the final model of the reclassified statements, along with the instructions to complete this task. Because not all universities prepare a cash flow statement, this was not taken into consideration. In the meanwhile, the research team prepared a set of financial ratios deemed fit for meeting the stakeholders’ needs for information. The research team was only able to collect ten sets of reclassified financial statements, because nine universities were unable to complete the task by the due date agreed at the start of the project. The research team calculated the financial ratios using the ten sets of financial statements. After collecting the data, the research team presented the analysis results at the last plenary session; the research project participants then suggested several further ratios. The complete set of ratios is presented in the next section of this paper and, compared to the existing literature, we have used a greater number of ratios. Moreover, these ratios conform to the accrual accounting system, while the traditional financial performance ratios included in Table 1 are mostly derived from a cash-based system. This is an important difference, because the general aim of the project was to examine whether the new accounting system would be able to provide information about the institutions’ financial sustainability.

During the whole process, the authors provided their support to the administrative departments at the HEIs, in part to improve the comparability of financial data as far as possible. In Table 2 are resumed the different phases of the research process.

Table 2.

The different phases of the research.

5. Framework for Financial Analysis in Universities

According to IPSAS 1 (par. 15) [41], “the objectives of general purpose financial reporting in the public sector should be to provide information useful for decision making, and to demonstrate the accountability of the entity for the resources entrusted to it”. To comply with this purpose, the accounting system must provide information on: (a) sources, allocation, and uses of financial resources; (b) how the entity financed its activities and met its cash requirements; (c) the entity’s capability to finance its activities and meet its liabilities; (d) its financial situation and any changes in it; (e) the entity’s performance—and so future viability—in terms of service costs, efficiency, and accomplishments.

In the perspective of the Italian Department of HE, the move to accrual accounting was expected to provide greater control over the institutions’ financial position and performance. However, interpreting the financial statements presented by public institutions is not as simple as it may seem. The transfer to business-like accounting techniques does not imply that the logics used in the financial analysis of for-profit entities are also suitable public sector organizations. Because the mission of public institutions is a different one, this suggests that they should adopt a different approach. The literature emphasizes the relationship between performance measures and strategy [42,43,44], and measures of financial performance make no exception to this general rule. Assessing the financial performance and financial position of a public university requires taking into consideration its special kind of operation, its competitive environment, and its key success factors. Thus, defining what information is relevant for the stakeholders is a prerequisite for identifying a suitable financial statement analysis methodology. University stakeholders come in very diverse classes and, reasonably, they have varying and sometimes contrasting needs and are interested in having different information. Many stakeholders probably pay greater attention to the different aspects relating to the social and environmental impacts of the HEIs’ activity. Students are likely to be more interested in post-graduate employment rates and in the quality of teaching and ancillary services, while corporations ask for research, innovation, and quality of education. Employees, the academic community, and local institutions are probably interested in other aspects. For the purposes of the present study, however, the relevance of financial information was the only aspect considered; the research group therefore made assumptions about the type of financial information to be provided by an HEI to its stakeholders. Unfortunately, the stakeholders themselves often have no clear idea of what financial information they need, and this is normally the case for students, the general public, and most university employees.

Conversely, stakeholders who do have management-type expertise often ask for accounting data which they consider to be relevant simply because it is so in the for-profit environment. This happens, for instance, when businessmen are appointed to university boards, which since the reform is certainly not a rare occurrence in Italy. There is a tangible risk that they can misinterpret performance measures, as they do not consider the public sector’s peculiar aspects.

These considerations suggested that specific financial ratios had to be developed to analyse university financial statements. As mentioned above, all the parties involved in the project were asked to identify the core aspects of financial analysis processes in HEIs, with reference to the various stakeholders. The conclusions of this discussion are given in Table 3:

Table 3.

2 Key aspects of financial statements analysis in Higher Education Institutions (HEIs).

As stated above, the type of financial statements introduced with the reform (Decree 19/2012) does not provide some of the measures that stakeholders supposedly need. The research group was of the opinion that, by reclassifying the statements, this would help to solve the problem at least partially. The key questions for the reclassification were:

- Funding from the Ministry of HE contains a performance-related part and this was kept separate so that its trend could be analysed over several financial periods. Universities adopting a ‘domestic competition strategy’ must stress this point.

- Unlike corporations, universities benefit from significant amounts of unearned income. This unearned income can originate from different kinds of transactions, and so this item can include elements with different meanings. The research team identified three different classes of unearned income, deciding to show them separately to improve transparency. The three classes are (a) ‘unearned income on research projects’, corresponding to the financial resources available for future research undertakings; (b) ‘unearned income on funds from government for investments in fixed assets’, which are deferred to future financial periods to balance future depreciation of assets; and (c) ‘other unearned income’.

- The reclassified income statement shows the margin on for-profit activity, as this can be used to assess the level of financial support, if any, for institutional undertakings. This aspect is particularly important for universities which are trying to diversify their sources of income in view of improving their financial sustainability.

- Labour costs for academics and administrative staff have been kept distinct. Moreover, both were detailed in order to highlight the portions pertinent to permanent contract costs and to fixed-term contract costs. The higher the percentage of fixed-term contracts, the more feasible are cost containment strategies (i.e., the third strategy mentioned above).

- The distinction between the most important classes of receivables, i.e., sums owed by the Ministry and by the students. With reference to the latter, their nominal value and the provision for bad debt are presented separately, as universities are expected to manage the problem of unpaid student fees independently.

Not even the reclassified financial statements, however, provide all relevant information mentioned in Table 3: The value of resources allocated to research activities, rather than to teaching or knowledge transfer activities, cannot be deduced from the financial statements. However, the financial statements provide many financial data that, if appropriately used to calculate ratios, are relevant for the stakeholders. The ratios used for the analysis are illustrated in Table 4.

Table 4.

Financial Ratios to analyse the universities’ financial statements.

With reference to these ratios, three aspects must be highlighted:

- (a)

- In HE, financial performance reflects the institutions’ capacity to cover costs or, potentially, to accumulate resources for future growth. A positive bottom line in its income statement indicates that the institution is able to build up resources to be used in future financial periods. On the contrary, a negative margin reflects a reduction in capital retained in previous years, meaning that resources consumed in the given period exceed resources received in the same period. Management should examine these losses and plan to use previously accumulated capital, provided that the quantity/quality of services delivered can be duly measured.

- (b)

- The approach used to assess corporate financial leverage does not fit the model of public institutions. Corporations can benefit from an increase in debts when the return on invested capital exceeds the cost of borrowings. This is never the case for public sector organizations, where investments do not in general produce any profit. In this context, the university’s governing bodies should bear in mind the fact that decisions about increasing interest-bearing liabilities will inevitably reduce their net assets, because income from new investments cannot cover interest expenses. Since borrowings are not a lever for increasing return on investments, taking on the additional financial risk of new debts must have the purpose of pursuing other objectives, i.e., improving research and/or teaching outcomes.

- (c)

- The values of some ratios can indicate that a particular financial strategy has been adopted. When ratios B.1 and/or A.3 are particularly high, this denotes a strategy of revenue diversification and self-sufficiency. Ratio D.2 indicates the willingness to take financial risks in order to develop institutional undertakings, thus, it is reasonable to assume that a high debt to equity ratio is consistent with a strategy of self-sufficiency.

High values for ratios B.3 and B.4 reveal a strategy of competition for Ministry funds, pursuing excellence in the goals it sets. On this point, the two universities offering postgraduate courses only (SA and SS) cannot be compared because they compete for performance-related funds on different bases.

In order to recognize whether a strategy to improve efficiency has been adopted, the analysis should extend over a series of financial periods. This was not possible in this study because there were no accrual-based financial statements for past periods for most of the universities involved. Moreover, the research project was conducted in 2015 and its aim was to define a framework to analyse financial statements and it was beyond the objectives of this project to detect clusters of universities that had adopted different strategies for financial sustainability. For this reason, and in consideration of the workload necessary to reclassify the financial statements, it was not possible to collect more data over the following years. It would certainly be helpful if the Ministry of HE decides to undertake similar initiatives in the future. Looking at the available data, flexibility in labour costs is the main signal that a university is able to adopt a strategy of cost containment.

6. Results

The universities involved in the project form a diversified group, including quite large universities with a lengthy historical tradition (e.g., University of Firenze/UF; Technical University of Milan (Politecnico di Milano)/PM), as well as very small recently established universities (University of Aosta/UDA). Six universities are located in northern Italy, two in central Italy, and one in Sardinia. The positioning of these universities within the HE sector is also different; five are typical generalist universities (UDA, UB, UT, UF, US), three are technical or specialized universities (UV, PM, PT), and two are research-oriented universities with mainly doctoral and postdoctoral students (SA, SS). The main features of each university involved in the research are set out in Table 5.

Table 5.

Main features of the 10 HEIs analysed.

Results summarizing the values of 19 ratios for the 10 HEIs are shown in Table 6.

Table 6.

Results of analysis.

The assessment of the universities’ financial sustainability is the first and more general purpose for the financial analysis. In this perspective, sustainability depends on the institutions’ capacity to avoid losses, as well as being able to meet their obligations. The ratios in classes A and D display the institution’s economic situation and capital structure, respectively. With reference to the former aspect, data reveal that the almost HEIs produced positive margins (EBIT), with the only exception being the University of Sassari, which instead incurred a loss. This is a negative signal, although only repeated losses over a long period is a clear indication of unsustainability. IUAV, the school of architecture and design in Venice, presented a different situation, as it was able to balance negative margins for its institutional activity against profits from its commercial ventures. This is an example of how diversifying income can enhance sustainability.

The second condition for financial sustainability concerns capital structure. In the public sector, where investment is not supposed to produce profits and is unlikely to do so, a low debt to equity ratio is a necessary condition for sustainability. Any capital invested does not generate the income to cover debt interest. As was to be expected, Italian HEIs present very strong capital structures. Only three universities have substantial debt, i.e., the two technical universities of Milan and Turin and SISSA. This of course could indicate a higher appetite for risk and a more entrepreneurial approach.

The second purpose of our analysis was to reveal what financial strategies, if any, were the Italian universities adopting to react to the challenges arising from the cutbacks in government resources and intensified competition. Some of the financial ratios can be associated to the specific financial strategies referred to in Section 2.

The first strategy, ‘domestic competition’, means that universities compete for Ministry funds by striving to excel in the objectives defined by central government in the three main missions set out for HEIs (teaching, research, and the transfer of knowledge). Ratios B3 and B4 show the percentage of funds allocated by the Ministry to each university depending on its performance. The two indicators, therefore, reveal whether a university is successful in achieving the Ministry’s goals. The data indicate that there is no correlation between the two ratios. The reason for this is that funds which are not performance-related are allocated on a historical basis. Ratio B.4 shows that UF and PM are more competitive on the Italian HE market, thus benefiting from a higher share of performance-based funds. Ratio E1 can be interpreted as a measure of whether prospective improvements are possible, as it compares the value of financial resources already accumulated for research projects against the annual revenue from research. Therefore, when the ratio is 1, the university can carry on research projects for one year even without receiving further funding for its research. To the extent that available financial resources can lead to significant research outputs, the university’s reputation and ranking within the competitive HE arena can improve. Our analysis indicates that the University of Trieste was in a particularly favourable position in this respect.

The second strategy—‘financial autonomy’—aims at reducing the university’s dependence on government funding. Income diversification incomes improves the institution’s financial stability even if there are public funding cutbacks. Ratio B1, which measures the percentage of self-generated revenue over total incomes (Ratio B1), is a simple indicator of the universities’ financial autonomy. Ratio B2 indicates how far competitive research grants contribute to the institution’s financial autonomy. The S. Anna (SA) School and the two technical universities (PM and PT) show the highest level of autonomy. Ratio B3 indicates that the S. Anna School achieves this result mainly through its research activity, while teaching is more important to the financial autonomy of the latter two. Financial autonomy is much lower in generalist universities.

The third strategy is based on the university’s search for conditions of higher efficiency. It, therefore, encompasses staff productivity and cost containment measures. Ratio C1 compares the cost for administrative staff with that for academic staff, where the higher the index, the lower are the university’s efficiency conditions, considering that virtuous universities should use as few resources as possible on administrative operations and focus all their efforts on teaching, research, and the transfer of knowledge. Ratios C4, C5, and C6 correlate human resources (volume and costs) with the various kinds of self-generated revenue, thus revealing staff productivity conditions and, here also, S. Anna and the two technical universities performed best. As specified above, if cost-reduction strategies are to be detected from the analysis of the institutions’ financial statements, this requires a comparative analysis over different periods (horizontal analysis). The fact that the preceding years’ income statements were unavailable meant that it was not possible to carry out this exercise. It follows that the most significant variable considered in this perspective is labour cost flexibility. Surprisingly, several universities use fixed-term contracts extensively, while others have a very rigid labour cost structure. This makes it more difficult to reduce costs at all significantly over the coming years, especially when considering that the cost of labour makes up 70% of the total operating costs, on average. The rigidity of the cost structure combined with public funding transfer cutbacks can undermine the institutions’ financial sustainability. Alternative policies to contain costs may refer to costs related to facilities or to student financial support.

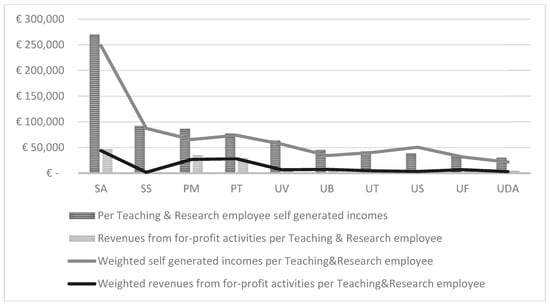

The economic differences from one geographic area to another can influence productivity assessments [45]. It is reasonable to assume that universities based in regions with higher GDP per capita have greater opportunities to attract financial resources from local and regional governments as well as from private companies; these universities are also potentially more attractive to students. Rather than being more virtuous, these universities may simply benefit from an ingrained competitive advantage. Weighting the ratios by regional GDP can mitigate this effect (i.e., Ratio × 1/Regional GDP per capita/National GDP per capita). The results of this analysis are given in Figure 1, where research-oriented universities (SA and SS) and the technical universities confirm their proclivity for financial autonomy. US operates in Sardinia, the weakest region among those considered in this group: By weighting its ratios, it was possible to give it a higher rank.

Figure 1.

Income per T&R staff compared with weighted income per T&R employee.

7. Conclusions

The paper proposes a model for the analysis of universities’ financial sustainability. This is a critical issue for most public organizations: Financial weaknesses would undermine other facets of sustainability, i.e., social and environmental sustainability. The model for the analysis is based on specific financial ratios, whose aim is to analyze the organization’s current situation and not also to predict future conditions of financial sustainability.

In Italy, the recent shift to accrual-based accounting for Higher Education Institutions has aimed at improving the transparency of financial reporting on organizations’ financial sustainability. Some universities had been able to release in 2015 the financial reports for the year 2014 in accordance with the new rules, thus anticipating by one year the deadline imposed by the ministry.

We analyzed the financial data of 10 Italian universities for the year 2014 in order to check the main assumption underlying the accounting reform, i.e., that the new financial reporting system can provide more information on organizations’ financial sustainability compared to the previous cash-based reporting system. Furthermore, some ratios were identified aiming at detecting signals of the strategies adopted by universities to improve their conditions of financial sustainability in a context of gradual public funding cutback.

Practitioners from 19 HEIs participated to the definition of the financial ratios. Five aspects of universities’ performances were investigated: Margins on institutional and on commercial activities, capability to attract funds, labor cost and productivity, financial position, funds available for future research activities. All these aspects influence the organizations’ financial sustainability.

The new annual reports provide information that were not available in the previous cash-based reporting system: In particular, it is now possible to extrapolate how much institutional and commercial activities contribute to the financial sustainability of the organization as a whole. However, some information has been lost due to the shift to the new system: Modified cash accounting enabled the analysis of the destination of resources, which is not possible with the new system that classifies expenses by nature. Thus, the new financial reporting system does not allow external stakeholders to detect the amount of resources used for research, teaching, or knowledge transfer. The new classification is more relevant for the purpose of managing the organization than for the evaluation of the results—even social outcomes—achieved.

The analysis of the financial statements of 10 universities let emerge some common elements and some differences as well. The most important correspondences regard the capital structures and the sources of incomes: All universities have small debts and their incomes mostly depend on budget allocations from the central government. Thus, the framework used in this analysis allows to confirm that Italian HEIs’ financial sustainability is quite strong, although dependent on government funding.

The financial dependence on central government represents a disadvantage for universities: Because of their highly rigid cost structure, they can hardly bear reductions of incomes. We suggest that HEIs may adopt three strategies to enhance their financial sustainability in such a context: (a) domestic competition strategy, aiming at increasing the performance-related part of government’s block grants; (b) financial autonomy strategy, based on the differentiation of incomes; and (c) efficiency improvement strategy, based on cost reductions. These strategies of financial sustainability are not mutually exclusive; nonetheless, findings reveal that some institutions are focused more than others on the strategy of self-sufficiency. Data reveal that polytechnics and research-oriented universities are more proactive in generating their own incomes: In particular, universities specialized in doctoral and post-doctoral programs, as well as polytechnics, are more capable of attracting non-governmental funds, while other organizations strive to compete on the goals defined by the ministry in the performance-based funding system. This result is crucial to understand how institutions are reacting heterogeneously to a common setting, characterized by sharp reductions in budget allocations from the central government.

Further in-depth exams of the different strategies would be useful. In particular, the contribution of for-profit activities to the overall financial performance is evidenced separately, but no information was available on the nature of the activities generating the margin: Whether spin-off companies, contracts with private firms or other activities. Lack of data hindered this kind of analysis.

Lack of data limited also the possibility to recognize signals of a strategy of efficiency improvement: To this aim, further analysis should be made on data series referring to more financial periods. An analysis conducted on the financial statements of different financial periods would allow more precise exams of the effects of the different strategies on organizations’ financial sustainability.

The paper paves the way for further developments that will be part of future research in the area. First, exploring factors that are associated with the likelihood of adopting a certain strategy would be possible. Calculating more ratios to capture trends over different periods would increase the understanding of the strategies adopted by HEIs.

The analysis of the financial data of universities is a central issue also for the ministry of HE. The ‘Technical Commission’ that defined the accounting standards and the financial reporting rules for universities should now develop a framework for the analysis of all financial data. If the Commission indicated a set of indicators to be periodically calculated (also beyond the ones proposed here, and clearly stating rubrics for calculations), this would accelerate the process of establishing a common language to compare the financial performance of HEIs in a wider framework. Lastly, focus groups and qualitative research can be conducted to understand how similar governing bodies use data to inform decisions. While retrospective in nature, data from Financial Reports can be used as a reference target to be integrated with internal management control systems. From this perspective, interviews with key actors of HEIs will allow understanding how financial targets enter into the scene in formalized strategic planning processes.

Author Contributions

Conceptualization, F.D.C. and G.M.; Formal analysis, G.M.; Investigation, G.M. and T.A.; Methodology, G.M.; Supervision, G.C.; Writing—original draft, F.D.C. and G.M.; Writing—review & editing, T.A. and F.D.C.

Funding

This research received no external funding.

Acknowledgments

A previous version of this paper has been presented in the EGPA annual conference in Utrecht (NL), August 2016. Authors are grateful to the discussant and the participants for their useful comments. All eventual errors are our solely responsibility.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Giddings, B.; Hopwood, B.; O’Brien, G. Environment, Economy and Society: Fitting Them Together into Sustainable Development. Sustain. Dev. 2002, 10, 187–196. [Google Scholar] [CrossRef]

- Boyer, R.H.W.; Peterson, N.D.; Arora, P.; Cladwell, K. Five Approaches to Social Sustainability and an Integrated Way Forward. Sustainability 2016, 8, 878. [Google Scholar] [CrossRef]

- Aupperle, K.; Carroll, A.B.; Hatfield, J. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- Albertini, E. Does Environmental Management Improve Financial Performance? A Meta-Analytical Review. Organ. Environ. 2013, 26, 431–457. [Google Scholar] [CrossRef]

- Falcone, P.M.; Sica, E. Assessing the opportunities and challenges of green finance in Italy: An analysis of the biomass production sector. Sustainability 2019, 11, 517. [Google Scholar] [CrossRef]

- Höhne, N.; Khosla, S.; Fekete, H.; Gilbert, A. Mapping of Green Finance Delivered by IDFC Members in 2011; Ecofys: Cologne, Germany, 2012. [Google Scholar]

- Owen, R.; Brennan, G.; Lyon, F. Enabling investment for the transition to a low carbon economy: Government policy to finance early stage green innovation. Curr. Opin. Environ. Sustain. 2018, 31, 137–145. [Google Scholar] [CrossRef]

- Mazzucato, M.; Semieniuk, G. Financing renewable energy: Who is financing what and why it matters. Technol. Forecast. Soc. Chang. 2018, 127, 8–22. [Google Scholar] [CrossRef]

- Foray, D.; Mowery, D.C.; Nelson, R.R. Public R&D; and social challenges: What lessons from mission R&D; programs? Res. Policy 2012, 41, 1697–1702. [Google Scholar]

- Mazzucato, M. The Entrepreneurial State; Anthem Press: London, UK, 2013. [Google Scholar]

- Steffen, B. The importance of project finance for renewable energy projects. Energy Econ. 2018, 69, 280–294. [Google Scholar] [CrossRef]

- Borgonovi, E.; Compagni, A. Sustaining Universal Health Coverage: The Interaction of Social, Political and Economic Sustainability. Value Health 2013, 16, S34–S38. [Google Scholar] [CrossRef]

- Pollitt, C.; Bouckaert, G. Public Management Reform: A Comparative Analysis, 2nd ed.; Oxford University Press: Boston, MA, USA, 2004. [Google Scholar]

- Olson, O.; Humphrey, C.; Guthrie, J. International Experiences with “New” Public Financial Management (NPFM) Reforms: New World? Small World? Better World? In Global Warning: Debating International Developments in New Public Financial Management; Olson, O., Humphrey, C., Guthrie, J., Eds.; Capelen Akademisk Forlag As: Oslo, Norway, 1998. [Google Scholar]

- Jansen, E.P. New Public Management: Perspectives on Performance and the Use of Performance Information. Financ. Account. Manag. 2008, 24, 169–191. [Google Scholar] [CrossRef]

- Kohtamäki, V. How do Higher Education Institutions Enhance their Financial Autonomy? Examples from Finnish Polytechnics. High. Educ. Q. 2011, 65, 164–185. [Google Scholar] [CrossRef]

- Caruana, J.; Brusca, I.; Caperchione, E.; Cohen, S.; Manes Rossi, F. (Eds.) Financial Sustainability of Public Sector Entities: The Relevance of Accounting Frameworks; Palgrave Macmillan: London, UK, 2019. [Google Scholar]

- EUA. Impact of the Economic Crisis on European Universities Update: First Semester. 2011. Available online: http://www.eua.be/Libraries/governanceautonomyfunding/NL_June_2011_with_map.pdf (accessed on 24 July 2017).

- Capano, G. Government Continues to Do Its Job: A Comparative Study of Governance Shifts in the Higher Education Sector. Public Adm. 2011, 89, 1622–1642. [Google Scholar] [CrossRef]

- EUA. Public Funding Observatory. 2014. Available online: http://www.eua.be/Libraries/governance-autonomy-funding/PFO_analysis_2014_final.pdf (accessed on 30 July 2017).

- Manes Rossi, F. Massification, Competition and Organizational Diversity in Higher Education: Evidence from Italy. Stud. High. Educ. 2010, 35, 277–300. [Google Scholar] [CrossRef]

- Guthrie, J. Australian Public Business Enterprises: Analysis of Changing Accounting, Auditing and Accountability Regimes. Financ. Account. Manag. 1993, 9, 101–114. [Google Scholar] [CrossRef]

- Parker, L.D.; Guthrie, J. The Australian Public Sector in the 1990s: New Accountability Regimes in Motion. Int. Account. Audit. Tax. 1993, 2, 59–81. [Google Scholar] [CrossRef]

- Mussari, R.; Sostero, U. Il processo di cambiamento del sistema contabile nelle università: Aspettative, difficoltà e contraddizioni. Azienda Pubblica 2014, 2, 121–143. [Google Scholar]

- Cantele, S.; Campedelli, B. Il performance-based funding nel sistema universitario italiano: Un’analisi degli effetti della programmazione triennale. Azienda Pubblica 2013, 3, 309–332. [Google Scholar]

- Parker, L.D. Contemporary University Strategising: The Financial Imperative. Financ. Account. Manag. 2013, 29, 1–25. [Google Scholar] [CrossRef]

- Modugno, G.; Tivan, M. Il Patrimonio vincolato nel bilancio degli atenei: Significato, funzionamento contabile delle poste, implicazioni gestionali. Azienda Pubblica 2015, 4, 359–376. [Google Scholar]

- Coran, G.; Pilonato, S. Criticità e limiti del budget nel nuovo sistema contabile universitario. Azienda Pubblica 2015, 3, 309–331. [Google Scholar]

- Tieghi, M.; Gigli, S. L’introduzione della Contabilità Economico-Patrimoniale negli Atenei: Un commento su alcune opzioni esercitate e alcune possibili proposte di miglioramento. Azienda Pubblica 2015, 1, 13–31. [Google Scholar]

- Agasisti, T.; Catalano, G.; Di Carlo, F.; Erbacci, A. Accrual accounting in Italian universities: A technical perspective. Int. J. Public Sect. Manag. 2015, 28, 494–508. [Google Scholar] [CrossRef]

- Paolini, A.; Soverchia, M. La programmazione delle università italiane si rinnova: Riflessioni e primi riscontri empirici. Azienda Pubblica 2015, 3, 287–308. [Google Scholar]

- Modugno, G.; Di Carlo, F. Financial Sustainability of Higher Education Institutions: A Challenge for the Accounting System. In Financial Sustainability of Public Sector Entities; Palgrave Macmillan: Cham, Switzerland, 2019; pp. 165–184. [Google Scholar]

- Woelfel, C.J. Financial Statement Analysis for Colleges and Universities. J. Educ. Financ. 1987, 12, 86–98. [Google Scholar]

- Sazonov, S.P.; Kharlamova, E.E.; Chekhovskaya, I.A.; Polyanskaya, E. Evaluating Financial Sustainability of Higher Education Institutions. Asian Soc. Sci. 2015, 11, 34–40. [Google Scholar] [CrossRef]

- HEFCE. Financial Health of the Higher Education Sector, 2012–2013 to 2015–16 Forecasts. 2013. Available online: www.hefce.ac.uk (accessed on 26 August 2018).

- KPMG. Financial Ratio Analysis Project, Final Report, 1996, Prepared on Behalf of U.S. Department of Education; KPMG: Amstelveen, The Netherlands, 1996. [Google Scholar]

- Moody’s, U.S. Not-for-Profit Private and Public Higher Education: Rating Methodology; Moody’s Investors Service: New York, NY, USA, 2011. [Google Scholar]

- Fischer, M.; Gordon, T.P.; Greenlee, J.T.; Keating, E.K. Measuring Operations: An Analysis of U.S. Private Colleges and Universities’ Financial Statements. Financ. Account. Manag. 2004, 2, 129–151. [Google Scholar] [CrossRef]

- Fischer, M.; Marsh, T. Two Accounting Standard Setters: Divergence Continues for Nonprofit Organizations, Journal of Public Budgeting. Account. Financ. Manag. 2012, 24, 429–465. [Google Scholar]

- Christiaens, J.; De Wielemaker, E. Financial Accounting Reform in Flemish Universities: An Empirical Study of The Implementation. Financ. Account. Manag. 2003, 19, 267–4424. [Google Scholar] [CrossRef]

- IPASB. IPSAS 1: Presentation of Financial Statements; IPASB: Santa Barbara, CA, USA, 2006. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. Using the Balanced Scorecard as a Strategic Management System. Harvard Business Review, January–February; 1996, 75–85.

- Kaplan, R.S. Strategic performance measurement and management in non-profit organizations. Nonprofit Manag. Lead. 2001, 11, 353–370. [Google Scholar] [CrossRef]

- Simons, R. Levers of control: How Managers Use Innovative Control Systems to Drive Strategic Renewal; Harvard Business School Press: Boston, MA, USA, 1995. [Google Scholar]

- Lelo, K.; Monni, S.; Tomassi, F. Urban inequalities in Italy: A comparison between Rome, Milan and Naples. Entrep. Sustain. Issues 2018, 6, 939–957. [Google Scholar] [CrossRef]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).