Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana

Abstract

:1. Introduction

- (i)

- whether mobile money services really serve low-income people [13],

- (ii)

- how the use of mobile money relates to individuals’ volumes of domestic payments, and

- (iii)

- whether access to mobile money payment services increases individuals’ likelihood of participating in a formal economy in a sustainable way [21].

2. Hypotheses

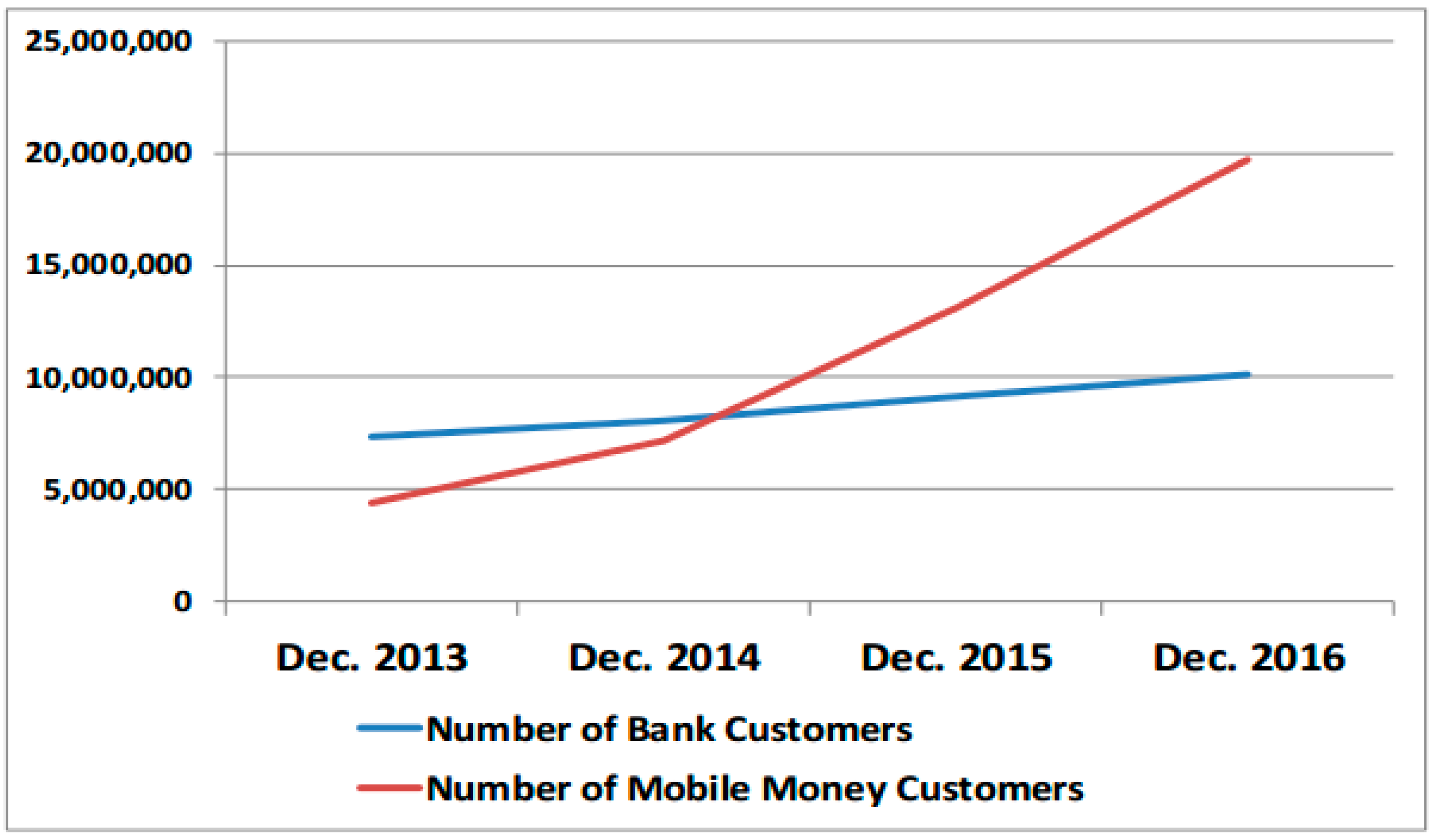

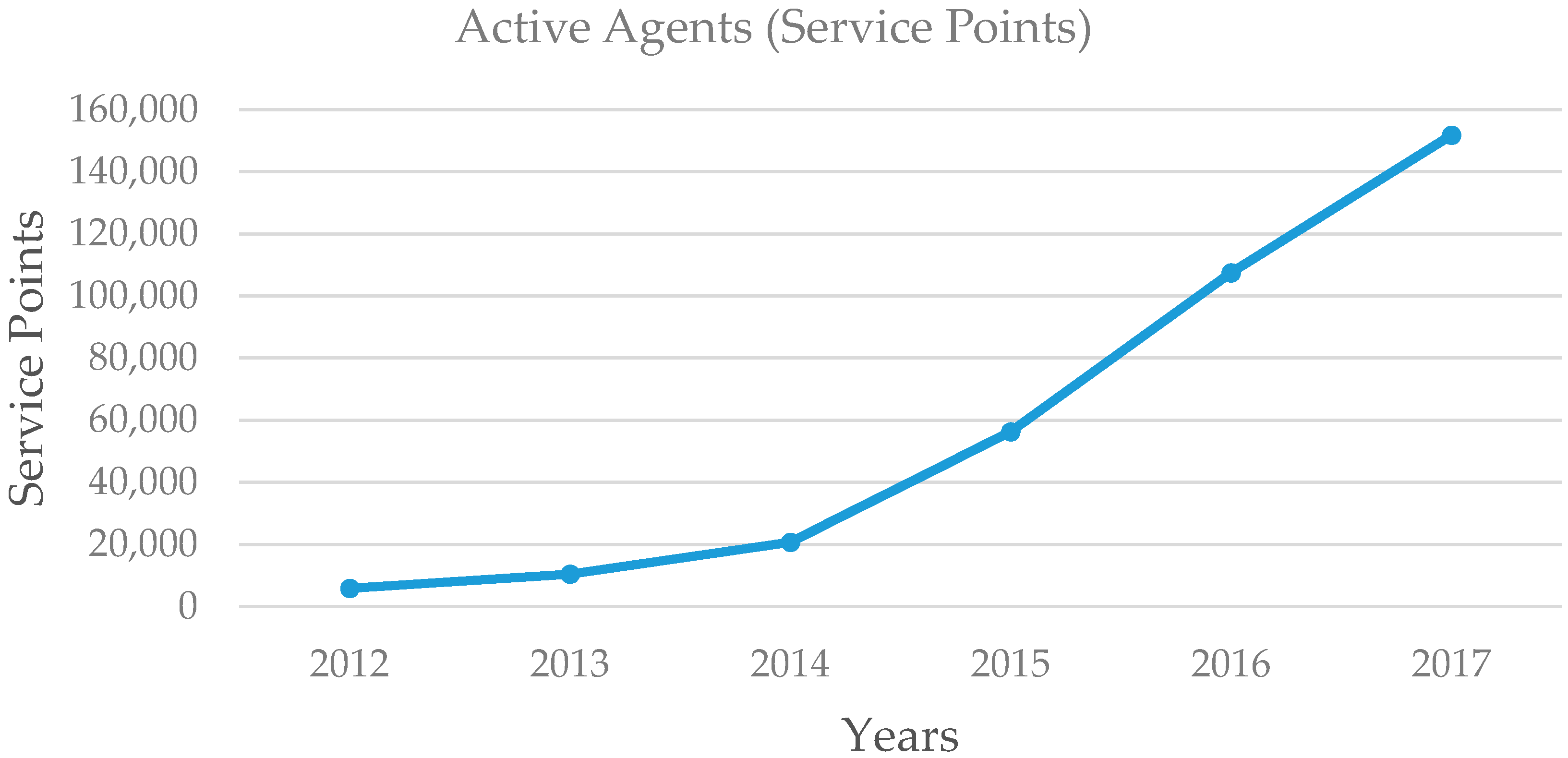

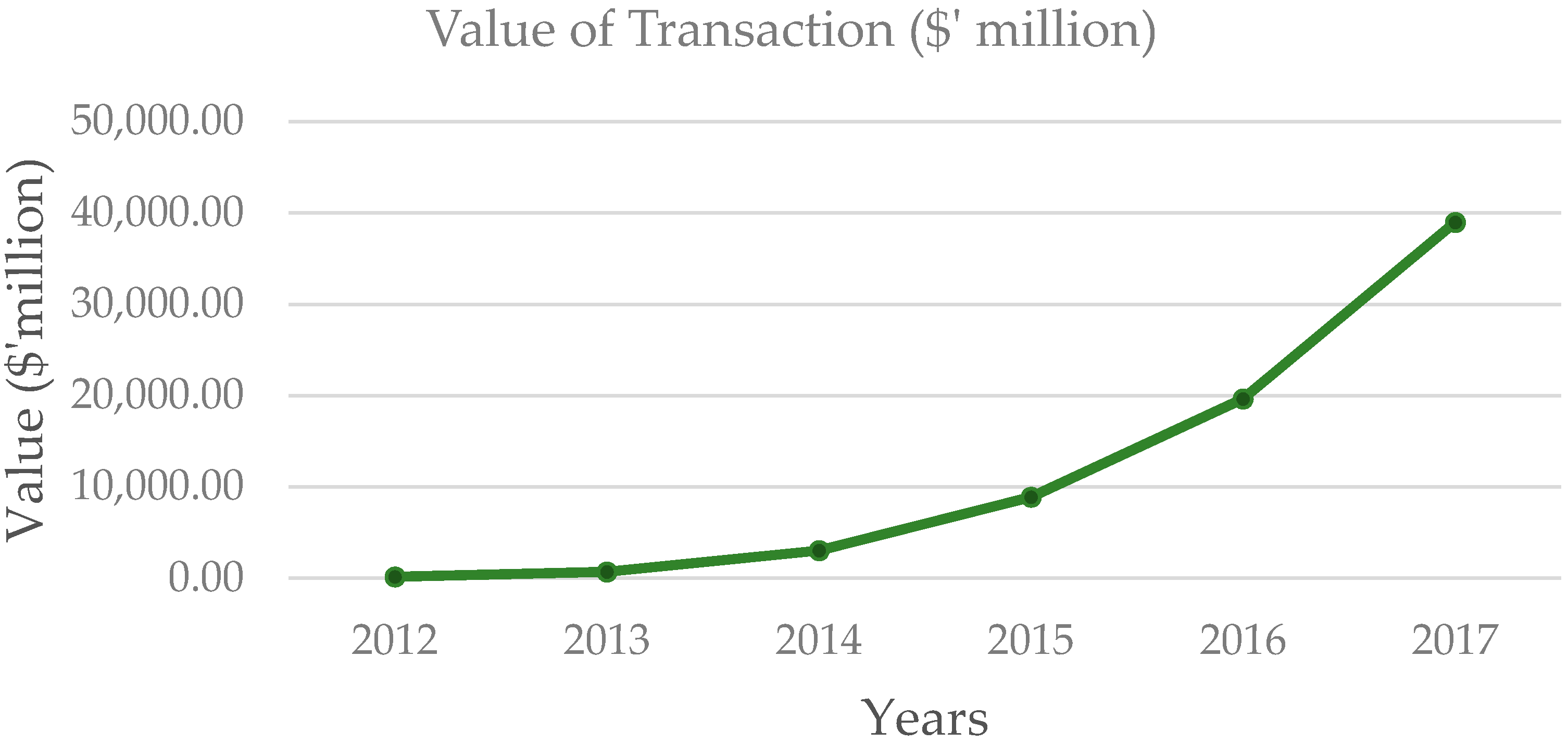

3. Trends and Mechanisms of Mobile Money in Ghana

4. Methodology

4.1. Data Collection

4.2. Estimation Strategy

5. Estimation Results

5.1. Who Uses Mobile Money?

5.2. Impacts of Mobile Money

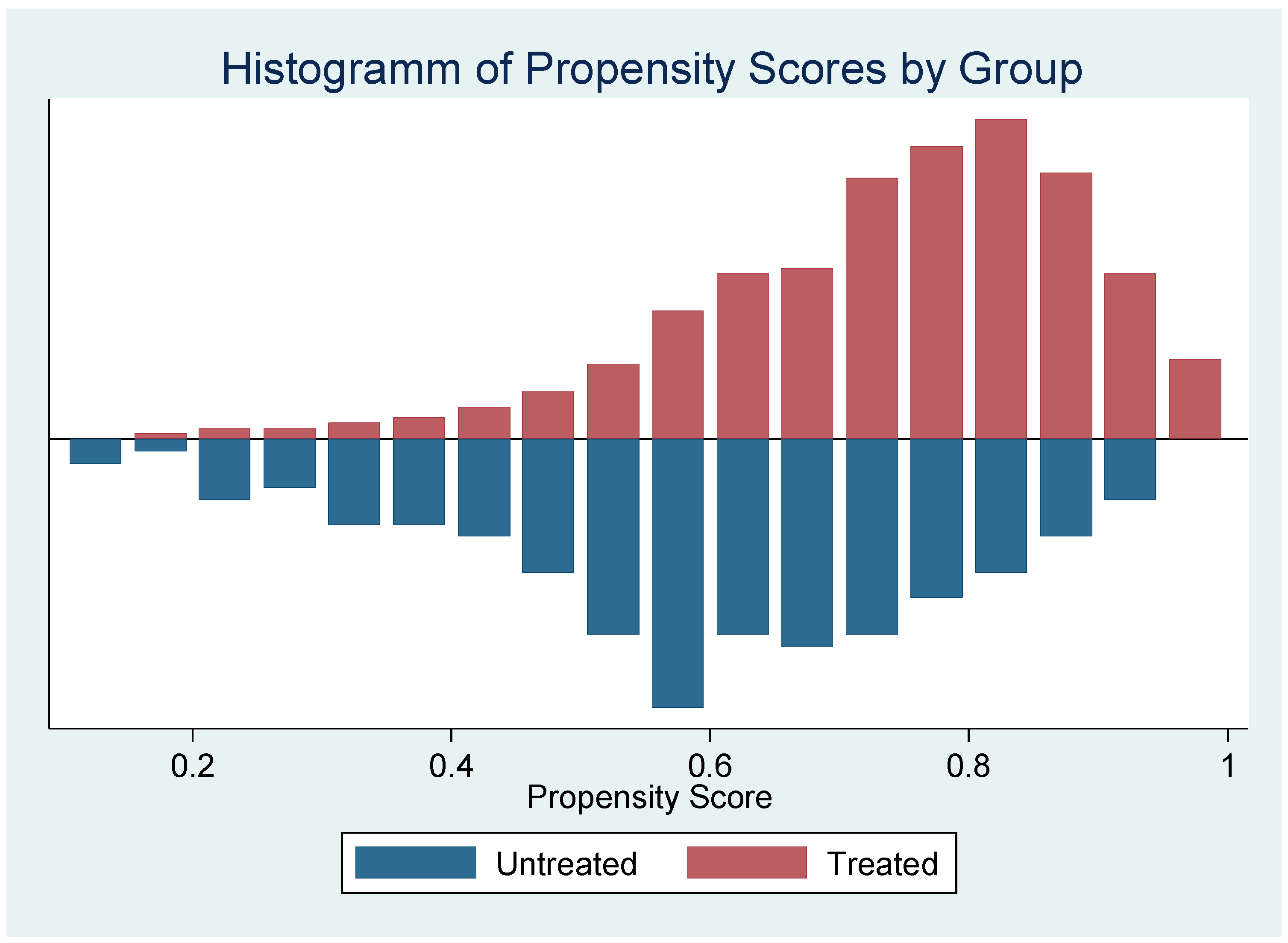

PSM Results

5.3. Inverse Propensity-Score Weighting Regression Results

5.3.1. Impact on Payments

5.3.2. Impact on Remittances

5.3.3. Impact on Investments

5.3.4. Impact on Savings

5.3.5. Impact on Consumption

6. Discussion

7. Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Supposed That You Are to Choose between Two Amounts to Receive: a Smaller Amount Today and a Bigger Amount Later. Which Option Do You Prefer? | A or B | ||

|---|---|---|---|

| Option A, Today | Option B, in 3 Months’ Time | ||

| TP1 | GH¢10.00 | GH¢12 | |

| TP2 | GH¢10.00 | GH¢14 | |

| TP3 | GH¢10.00 | GH¢16 | |

| TP4 | GH¢10.00 | GH¢18 | |

| TP5 | GH¢10.00 | GH¢20 | |

| TP6 | GH¢10.00 | GH¢22 | |

| TP7 | GH¢10.00 | GH¢24 | |

| TP8 | GH¢10.00 | GH¢26 | |

| TP9 | GH¢10.00 | GH¢28 | |

| TP10 | GH¢10.00 | GH¢30 | |

Appendix B

| Supposed That You Are to Choose between Two Amounts to Receive: a Smaller Amount Today and a Bigger Amount Later. Which Option Do You Prefer? | A or B | ||

|---|---|---|---|

| Option A, in 3 Months’ Time | Option B, in 6 Months’ Time | ||

| TP1 | GH¢10.00 | GH¢12 | |

| TP2 | GH¢10.00 | GH¢14 | |

| TP3 | GH¢10.00 | GH¢16 | |

| TP4 | GH¢10.00 | GH¢18 | |

| TP5 | GH¢10.00 | GH¢20 | |

| TP6 | GH¢10.00 | GH¢22 | |

| TP7 | GH¢10.00 | GH¢24 | |

| TP8 | GH¢10.00 | GH¢26 | |

| TP9 | GH¢10.00 | GH¢28 | |

| TP10 | GH¢10.00 | GH¢30 | |

Appendix C

| Project A | Project B | A or B | ||

|---|---|---|---|---|

| You Obtain for Sure: | 50% Chance of Obtaining: | 50% Chance of Obtaining: | ||

| RG1 | GH¢5.00 | GH¢12.00 | GH¢0 | |

| RG2 | GH¢6.00 | GH¢12.00 | GH¢0 | |

| RG3 | GH¢7.00 | GH¢12.00 | GH¢0 | |

| RG4 | GH¢8.00 | GH¢12.00 | GH¢0 | |

| RG5 | GH¢9.00 | GH¢12.00 | GH¢0 | |

| RG6 | GH¢10.00 | GH¢12.00 | GH¢0 | |

| RG7 | GH¢11.00 | GH¢12.00 | GH¢0 | |

| RG8 | GH¢12.00 | GH¢12.00 | GH¢0 | |

Appendix D

| Variable | Definition | Unit of Measurement | Hypothesized Relationship |

|---|---|---|---|

| Outcome Variables | |||

| User | This is a categorical variable that indicates 1 if an individual has ever used mobile money to undertake any transaction, and 0 otherwise | Dummy | |

| Payment sent | The total value of money paid for goods and services received in the last 12 months | Continuous | |

| Payments received | The total value of money received for goods and services given out in the last 12 months | Continuous | |

| Remittances sent | The total value of cash and in-kind gift given out in the last 12 months, without expecting to be paid back | Continuous | |

| Remittances received | The total value of cash and in-kind gift received in the last 12 months, that would not be paid back | Continuous | |

| Investment in microbusiness | Total value of money spent to start, run a business, or acquire an asset for a business for income-generating activity | Continuous | |

| Investment in education | Total value of money spent by the respondent for educating him/herself, spouse, children, a household member, or any non-household member in the last 12 months | Continuous | |

| Investment in health | Total value of money spent by the respondent for him/herself, spouse, children, a household member, or non-household member | Continuous | |

| Savings | Total value of money saved in the last 12 months. | Continuous | |

| Consumption | Total value of money spent on food, water, electricity, gas, and rent, for him/herself and household members in the past 12 months | Continuous | |

| Independent variables | |||

| Age | This variable indicates how old an individual is. | Years | +/− |

| Male | This indicates the gender of an individual. 1 if the individual is a man, and 0 if the individual is a woman | dummy | +/− |

| Years of schooling | The number of years an individual spent formally in school | Years | + |

| Household size | The number of people living in a house together and sharing the same housekeeping arrangement | Discrete | + |

| Non-household dependents | Persons who do not belong to the household of the respondent; however, they depend on the respondent for a living. | Discrete | + |

| Married | Indicates the marital status of the respondent. 1 when the respondent is married, and 0 otherwise | Dummy | +/− |

| Minutes to the nearest vendor | Indicates the number of minutes of walk it takes the respondent to get to the nearest mobile-money service point | Minutes | − |

| Discount rate | This is the respondent’s individual discount rate, which is calculated based on his/or her rate of time preference. | Index | +/− |

| Present bias | The tendency of a respondent to give stronger weight to payoffs that are closer to now, than a future payoff. | Dummy | +/− |

| Risk-averse | Respondent preference to take risk | Index | − |

| Migrant | Indicates the migrant status of the respondent. 1 if a respondent is born in the Ashanti Region, and 0 otherwise | Dummy | + |

| Formal employment | Indicates whether the respondent is formally employed or not. 1 if a respondent is in formal employment, and 0 otherwise | Dummy | + |

| Self-employment | Indicates the self-employment status of a respondent. It is 1 if a respondent is self-employed and 0 otherwise. | Dummy | − |

| Years of work | Number of years a respondent has worked after school. | Years | + |

| First heard about mobile money (months ago) | Indicates the number of months since a respondent has heard about mobile money. | Months | + |

| Minutes to bank | The minutes of walk it takes a respondent to get to the nearest bank. | Minutes | + |

| Rural | Indicates a location dummy, 1, when the respondent lives in a rural area, and 0 otherwise. | Dummy | + |

| Urban | Indicates a location dummy, 1 if a respondent resides in an urban area, and 0 otherwise. | Dummy | − |

| Total financial | The value of total financial assets owned by the respondents | Continuous | + |

| Physical assets | The value of total physical assets owned by the household of the respondent | Continuous | + |

References

- Demirguc-Kunt, A.; Klapper, L.; Singer, D.; Van Oudheusden, P. The Global Findex Database 2014: Measuring Financial Inclusion around the World; World Bank Group: Washington, DC, USA, 2015. [Google Scholar]

- The World Bank Development Research Group, Better than Cash Alliance, & Bill & Melinda Gates Foundation. The Opportunities of Digitizing Payments How digitization of Payments, Transfers, and Remittances Contributes to the G20 Goals of Broad-Based Economic Growth, Financial Inclusion, and Women’s Economic Empowerment. 2014. Available online: http://siteresources.worldbank.org/EXTGLOBALFIN/Resources/85196381332259343991/G20_Report_Final_Digital_payments.pdf (accessed on 19 February 2018).

- Klapper, L.; El-Zoghbi, M.; Hess, J. Achieving the Sustainable Development Goals—The Role of Financial Inclusion; CGAP: Washington, DC, USA, 2016. [Google Scholar]

- Robert, C.; Tilman, E.; Nina, H. Financial inclusion and development: Recent impact evidence. Focus Note 2014, 92, 1–12. Available online: http://www.cgap.org/sites/default/files/FocusNote-Financial-Inclusion-and-Development-April-2014.pdf (accessed on 1 May 2018).

- Aghion, P.; Bolton, P. A Theory of Trickle-Down Growth and Development. Rev. Econ. Stud. 1997, 64, 151–172. [Google Scholar] [CrossRef]

- Beck, T.; Demirguc-Kunt, A.; Levine, R. Finance, Inequality, and the Poor. J. Econ. Growth 2007, 12, 27–49. [Google Scholar] [CrossRef]

- Angelucci, M.; Karlan, D.; Zinman, J. Microcredit impacts: Evidence from a Randomized Microcredit Program Placement Experiment by Compartamos Banco. Am. Econ. J. Appl. Econ. 2015, 7, 151–182. [Google Scholar] [CrossRef]

- Yunus, M. Creating a World without Poverty: Social Business and the Future of Capitalism. Glob. Urban Dev. 2008, 4, 1–19. [Google Scholar]

- Augsburg, B.; De Haas, R.; Harmgart, H.; Meghir, C. The impacts of microcredit: Evidence from Bosnia and Herzegovina. Am. Econ. J. Appl. Econ. 2015, 7, 183–203. [Google Scholar] [CrossRef]

- Banerjee, A.; Duflo, E.; Glennerster, R.; Kinnan, C. The miracle of microfinance? Evidence from a randomized evaluation. Am. Econ. J. Appl. Econ. 2015, 7, 22–53. [Google Scholar] [CrossRef]

- Crépon, B.; Devoto, F.; Duflo, E.; Parienté, W. Estimating the Impact of Microcredit on Those Who Take It up: Evidence from a Randomized Experiment in Morocco. Am. Econ. J. Appl. Econ. 2015, 7, 123–150. [Google Scholar] [CrossRef]

- Karlan, D.; Zinman, J. Microcredit in Theory and Practice: Using Randomized Credit Scoring for Impact Evaluation. Science 2011, 332, 1278–1284. [Google Scholar] [CrossRef] [PubMed]

- Evaluation, A.; Bank, W.; Support, G.; Inclusion, F.; Households, L. Financial Inclusion: A Foothold on the Ladder toward Prosperity? An Evaluation of World Bank Group Support for Financial Inclusion for Low-Income Households and Microenterprises. 2015. Available online: http://ieg.worldbankgroup.org/sites/default/files/Data/Evaluation/files/financialinclusion.pdf (accessed on 19 February 2018).

- Suri, T.; Jack, W. The long-run poverty and gender impacts of mobile money. Science 2016, 354, 1288–1292. [Google Scholar] [CrossRef] [PubMed]

- Munyegera, G.K.; Matsumoto, T. Mobile Money, Remittances, and Household Welfare: Panel Evidence from Rural Uganda. World Dev. 2016, 79, 127–137. [Google Scholar] [CrossRef]

- Jack, W.; Suri, T. Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. Am. Econ. Rev. 2014, 104, 183–223. [Google Scholar] [CrossRef]

- Suri, T.; Jack, W.; Stoker, T.M. Documenting the birth of a financial economy. Proc. Natl. Acad. Sci. USA 2012, 109, 10257–10262. [Google Scholar] [CrossRef] [PubMed]

- Blumenstock, J.; Eagle, N.; Fafchamps, M. Risk Sharing over the Mobile Phone Network: Evidence from Rwanda. Available online: https://aae.wisc.edu/mwiedc/papers/2011/blumenstock_joshua.pdf (accessed on 23 February 2018).

- Batista, C.; Vicente, P.C. Introducing Mobile Money in Rural Mozambique: Evidence from a Field Experiment. Nova Africa. 2012. Available online: https://doi.org/10.2139/ssrn.2384561 (accessed on 1 May 2018).

- Aker, J.C.; Wilson, K. Can Mobile Money be used to Promote Savings? Evidence from Preliminary Research Northern Ghana. FEBS J. 2013, 281, 1–11. [Google Scholar]

- Dupas, P.; Robinson, J. Savings Constraints and Microenterprise Development: Evidence from a Field Experiment in Kenya. Am. Econ. J. Appl. Econ. 2013, 5, 163–192. [Google Scholar] [CrossRef]

- Collins, D.; Morduch, J.; Rutherford, S.; Ruthven, O. Portfolios of the Poor: How the World’s Poor Live on $2 a Day; Princeton University Press: Princeton, NJ, USA, 2009. [Google Scholar]

- Kelly, S.E.; Rhyne, E. By the Numbers. High-Performance Composites. Available online: https://doi.org/10.1038/scientificamerican0514-20a (accessed on 24 February 2018).

- Blumenstock, J.E.; Eagle, N.; Fafchamps, M. Airtime transfers and mobile communications: Evidence in the aftermath of natural disasters. J. Dev. Econ. 2016, 120, 157–181. [Google Scholar] [CrossRef]

- Dupas, P.; Robinson, J. Why don’ the poor save more? Evidence from health savings experiments. Am. Econ. J. Appl. Econ. 2013, 103, 1138–1191. [Google Scholar]

- Bauchet, J.; Marshall, C.; Starita, L.; Thomas, J.; Yalouris, A. Latest Findings from Randomized Evaluations of Microfinance. December 2011, pp. 1–27. Available online: https://www.cgap.org/sites/default/files/CGAP-Forum-Latest-Findings-from-Randomized Evaluations-of-Microfinance-Dec-2011.pdf (accessed on 24 February 2014).

- Bank of Ghana. Impact of Mobile Money on the Payment System in Ghana: An Econometric Analysis 2017. Available online: https://www.bog.gov.gh/privatecontent/Public_Notices/Impact of Mobile Money on the Payment Systems in Ghana.pdf (accessed on 13 October 2017).

- Page, M.; Molina, M.; Jones, G.; Makarov, D. The Mobile Economy. 2013. Available online: https://www.gsma.com/newsroom/wp-content/uploads/2013/12/GSMA-Mobile-Economy-2013.pdf (accessed on 24 February 2018).

- Holt, C.A.; Laury, S.K. Risk Aversion and Incentive Effects. Am. Econ. Rev. 2002, 92, 1644–1655. [Google Scholar] [CrossRef]

- Tanaka, T.; Camerer, C.F.; Nguyen, Q. Risk and Time Preferences: Linking Experimental and Household Survey Data from Vietnam. Am. Econ. Rev. 2010, 100, 557–571. [Google Scholar] [CrossRef]

- Tanaka, Y.; Munro, A. Regional variation in risk and time preferences: Evidence from a large-scale field experiment in rural Uganda. J. Afr. Econ. 2014, 23, 151–187. [Google Scholar] [CrossRef]

- Tobbin, P.; Kuwornu, J.K. Adoption of Mobile Money Transfer Technology: Structural Equation Modeling Approach. Eur. J. Bus. Manag. 2011, 3, 59–78. [Google Scholar]

- Bauer, H.H.; Reichardt, T.; Barnes, S.J.; Neumann, M.M. Driving consumer acceptance of mobile marketing: A theoretical framework and empirical study. J. Electron. Commer. Res. 2005, 6, 181–192. [Google Scholar]

- Caliendo, M.; Kopeinig, S. Some Practical Guidance for the Implementation of Propensity Score Matching. J. Econ. Surv. 2008, 22, 31–72. [Google Scholar] [CrossRef]

- Ravallion, M. Chapter 59 Evaluating anti-poverty programs. In Handbook of Development Economics; Development Research Group, The World Bank: Washington, DC, USA, 2007; Volume 4, pp. 3787–3846. ISBN 978-0-44-453100-1. [Google Scholar]

- Heckman, J.J.; Ichimura, H.; Todd, P. Matching as an Econometric Evaluation Estimator. Rev. Econ. Stud. 1998, 65, 261–294. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Inverse probability weighted estimation for general missing data problems. J. Econ. 2007, 141, 1281–1301. [Google Scholar] [CrossRef]

- Robins, J.M.; Rotnitzky, A. Semiparametric Efficiency in Multivariate Regression Models with Missing Data. J. Am. Stat. Assoc. 1995, 90, 122–129. [Google Scholar] [CrossRef]

- Hirano, K.; Imbens, G.W.; Ridder, G. Efficient Estimation of Average Treatment Effects Using the Estimated Propensity Score. Econometrica 2003, 71, 1161–1189. [Google Scholar] [CrossRef]

- Hirano, K.; Imbens, G. Estimation of causal effects using propensity score weighting: An application to data on right heart catheterization. Health Serv. Outcomes Res. Methodol. 2001, 2, 259–278. [Google Scholar] [CrossRef]

- Suzuki, A.; Mano, Y.; Abebe, G. Earnings, Savings, and Happiness from Working in a Labor-intensive Export Sector: Unskilled Workers in the Cut Flower Industry in Ethiopia. 2016. Available online: https://editorialexpress.com/cgibin/conference/download.cgi?db_name=CSAE2016&paper_id=701 (accessed on 1 February 2018).

| Variable | 1 Mobile-Money Users (N = 388) | 2 Non-Users (N = 169) | 3 p-Value of Difference |

|---|---|---|---|

| Age (years) | 31.5 | 35.2 | 0.00 *** |

| (11.18) | (14.29) | ||

| Education (years) | 9.62 | 7.54 | 0.00 *** |

| (3.86) | (4.41) | ||

| Gender (1 = male) | 0.5 | 0.56 | 0.19 |

| (0.50) | (0.50) | ||

| Married (1 = yes) | 0.39 | 0.52 | 0.01 ** |

| (0.49) | (0.50) | ||

| Migrant (1 = yes) | 0.32 | 0.34 | 0.67 |

| (0.47) | (0.48) | ||

| Risk-averse (1–8: 8, most risk-averse) | 7.24 | 7.18 | 0.81 |

| (2.25) | (2.29) | ||

| Discount rate | 0.33 | (0.34) | 0.24 |

| (0.16) | (0.16) | ||

| Present bias | −0.02 | −0.003 | 0.15 |

| (0.12) | (0.14) | ||

| Minutes of walk to the nearest vendor | 4.17 | 4.94 | 0.08 * |

| (4.29) | (5.42) | ||

| Household size | 3.53 | 3.22 | 0.12 |

| (2.22) | (2.12) | ||

| Non-household dependents | 0.48 | 0.39 | 0.15 |

| (0.67) | (0.60) | ||

| Employment status | 0.86 | 0.85 | 0.59 |

| (0.02) | (0.36) | ||

| Work experience (years) | 6.13 | 8.53 | 0.01 ** |

| (9.09) | (10.44) | ||

| First heard about mobile money (months ago) | 43.1 | 32.96 | 0.00 ** |

| (20.68) | (20.33) | ||

| Percentage of friends on mobile money | 67.6 | 50.8 | 0.00 *** |

| (4.89) | (2.85) |

| Variable | 1 Mobile-Money Users (N = 388) | 2 Non-Users (N = 169) | 3 p-Value of Difference |

|---|---|---|---|

| Ownership of Bank Account | 0.61 | 0.37 | 0.00 *** |

| (0.49) | (0.49) | ||

| Ownership of Mobile-Money Account | 0.54 | 0.02 | 0.00 *** |

| (0.50) | (0.13) | ||

| Payments Sent (last 30 days (GH¢)) | 1945.26 | 1062.51 | 0.00 *** |

| (2888.24) | (1201.32) | ||

| Payments Sent (last 12 months (GH¢)) | 15,133.86 | 7727.41 | 0.04 * |

| (45,538.13) | (7895.03) | ||

| Mobile Money Sent (all transactions, last 12 months (GH¢)) | 453.6 | 0 | 0.07 * |

| (3347.28) | |||

| Mobile Money Received (all transactions last 12 months (GH¢)) | 375.63 | 0 | 0.08 * |

| (2785.29) | |||

| Respondents’ Income (last 30 days (GH¢)) | 786.05 | 367.68 | 0.02 * |

| (2238.83) | (592.59) | ||

| Respondents’ Income (last 12 months (GH¢)) | 9249.30 | 5868.09 | 0.01 ** |

| (15,236.96) | (8065.06) | ||

| Remittance and Gifts Sent (last 12 months (GH¢)) | 285.97 | 141.24 | 0.00 *** |

| (527.40) | (317.60) | ||

| Remittance and Gifts Received (last 12 months (GH¢)) | 322.99 | 144.09 | 0.00 *** |

| (589.67) | (327.15) | ||

| Investment in Micro-Enterprise, Land, and Buildings | 4510.73 | 702.81 | 0.23 |

| (41,434.89) | (2190.07) | ||

| Investment in Education (last 12 months (GH¢)) | 1533.92 | 972.96 | 0.23 |

| (5799.43) | (2550.15) | ||

| Investment in Health (GH¢) | 390.17 | 347.36 | 0.60 |

| (856.85) | (969.08) | ||

| Total Savings (GH¢) | 1500.36 | 447.73 | 0.11 |

| (8643.36) | (1606.36) | ||

| Total Financial Assets (GH¢) | 1572.63 | 1051.41 | 0.13 |

| (4345.09) | (1591.46) | ||

| Household Total Physical Assets (GH¢) | 603,210 | 1,398,726 | 0.39 |

| (4,714,307) | (16,900,000) | ||

| Consumption (last 30 days in (GH¢)) | 571.84 | 453.84 | 0.01 * |

| (555.99) | (374.34) | ||

| Consumption (last 12 months in (GH¢)) | 5409.31 | 4126.36 | 0.03 * |

| (7347.99) | (4605.49) |

| Variables | 1 (Logit) | 2 (Probit) |

|---|---|---|

| User | User | |

| ln (Financial assets) | 0.028 | 0.016 |

| (0.067) | (0.039) | |

| Age | −0.017 * | −0.011 * |

| (0.010) | (0.006) | |

| Male | −0.572 *** | −0.330 *** |

| (0.211) | (0.123) | |

| Years of schooling | 0.103 *** | 0.062 *** |

| (0.027) | (0.016) | |

| Household size | 0.147 ** | 0.082 ** |

| (0.059) | (0.033) | |

| Non-household dependents | 0.335 ** | 0.201 ** |

| (0.165) | (0.095) | |

| Married | −0.497 ** | −0.287 ** |

| (0.246) | (0.145) | |

| Minutes to the nearest vendor | −0.034 * | −0.020 * |

| (0.020) | (0.012) | |

| First heard about mobile money (months ago) | 0.025 *** | 0.014 *** |

| (0.006) | (0.003) | |

| Discount rate | −0.485 | −0.325 |

| (0.690) | (0.412) | |

| Present bias | −1.040 | −0.607 |

| (0.872) | (0.516) | |

| Risk-averse | 0.004 | 0.002 |

| (0.043) | (0.026) | |

| Constant | −0.429 | −0.200 |

| (0.710) | (0.412) | |

| Pseudo R2 | 0.121 | 0.120 |

| Observations | 557 | 557 |

| Variable | (1) |

|---|---|

| ln (Amount through Mobile Money) | |

| ln (Financial assets) | 0.198 ** |

| (0.0955) | |

| Age | 0.0148 |

| (0.0184) | |

| Male | −0.517 |

| (0.327) | |

| Years of schooling | 0.0333 |

| (0.0415) | |

| Household size | 0.117 |

| (0.0792) | |

| Non-household dependents | 0.980 *** |

| (0.267) | |

| Married | −0.378 |

| (0.418) | |

| Minutes to the nearest vendor | −0.0262 |

| (0.0397) | |

| First heard about mobile money (months ago) | 0.0194 *** |

| (0.00746) | |

| Discount rate | 0.892 |

| (1.067) | |

| Present bias | −0.752 |

| (1.361) | |

| Risk-averse | 0.0578 |

| (0.0640) | |

| Constant | −1.652 |

| (1.120) | |

| Observations | 388 |

| R-squared | 0.089 |

| No. of Significant Variable | Pseudo R2 | p-Value LR * Test | Mean Bias | |

|---|---|---|---|---|

| Impact of Mobile Money on | ||||

| Payments Sent | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 1 | 0.007 | 0.854 | 4.6 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Payments Received | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Remittance Sent | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Remittance Received | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Investment in Microbusiness | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Investment in Education | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Investment in Health | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.9 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Savings | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Consumption | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.2 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.968 | 4.2 |

| Radius caliper (0.1) | 1 | 0.006 | 0.914 | 4.3 |

| Outcome Variables (Yearly) | Propensity-Score Matching | |

|---|---|---|

| (1) Kernel Common Trim | (2) Radius Caliper | |

| ln (Payments Sent) | 0.509 *** | 0.479 *** |

| (0.126) | (0.118) | |

| ln (Payments Received) | 0.488 *** | 0.503 *** |

| (0.138) | (0.137) | |

| ln (Remittance Sent) | 1.418 *** | 1.439 *** |

| (0.324) | (0.291) | |

| ln (Remittance Received) | 1.147 *** | 1.117 *** |

| (0.382) | (0.352) | |

| ln (Investment in Micro-Enterprises, Land and Buildings) | 1.771 *** | 1.730 *** |

| (0.361) | (0.381) | |

| ln (Investments in Education) | 0.954 * | 1.045 * |

| (0.459) | (0.458) | |

| ln (Investment in Health) | 0.223 | 0.253 |

| (0.241) | (0.241) | |

| ln (Savings) | 1.548 *** | 1.567 *** |

| (0.353) | (0.339) | |

| ln (Consumption) | 0.296 * | 0.310 * |

| (0.134) | (0.115) | |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | ln Payment Sent | ln Payments Received | ln Remittance Sent | ln Remittance Received |

| User | 0.399 *** | 0.308 ** | 1.312 *** | 0.733 ** |

| (0.119) | (0.141) | (0.287) | (0.326) | |

| ln (Financial assets) | 0.135 *** | 0.131 *** | 0.198 ** | −0.001 |

| (0.043) | (0.047) | (0.089) | (0.102) | |

| Age | 0.021 *** | 0.006 | 0.011 | −0.035 * |

| (0.006) | (0.006) | (0.015) | (0.012) | |

| Male | 0.053 | 0.256 * | 0.558 ** | −0.235 |

| (0.108) | (0.139) | (0.264) | (0.286) | |

| Years of schooling | 0.019 | 0.021 | 0.045 | 0.011 |

| (0.012) | (0.017) | (0.041) | (0.045) | |

| Household size | 0.079 *** | 0.061 * | 0.048 | −0.058 |

| (0.0251) | (0.031) | (0.068) | (0.066) | |

| Non-household dependents | 0.199 *** | 0.257 *** | 0.348 | −0.175 |

| (0.077) | (0.091) | (0.225) | (0.196) | |

| Married | 0.038 | −0.002 | −0.735 ** | −0.475 |

| (0.118) | (0.161) | (0.315) | (0.390) | |

| Minutes to the nearest vendor | −0.017 | −0.033 | 0.040 * | 0.041 |

| (0.010) | (0.020) | (0.024) | (0.035) | |

| Discount rate | −0.910 *** | −0.324 | 0.189 | 1.179 |

| (0.290) | (0.422) | (0.925) | (0.973) | |

| Present bias | 1.253 *** | −0.214 | 0.622 | −1.171 |

| (0.335) | (0.482) | (1.176) | (1.098) | |

| Risk-averse | 0.020 | 0.044 | −0.072 | −0.153 *** |

| (0.021) | (0.031) | (0.045) | (0.053) | |

| ln (Physical assets) | 0.109 *** | 0.147 *** | 0.051 | 0.118 |

| (0.032) | (0.032) | (0.070) | (0.078) | |

| Migrant | −0.256 * | 0.055 | −0.537 * | 0.070 |

| (0.132) | (0.143) | (0.305) | (0.325) | |

| Formal employment | 0.199 | 0.604 ** | −0.751 | −1.817 *** |

| (0.334) | (0.305) | (0.806) | (0.692) | |

| Self-employment | 0.131 | −0.058 | −0.176 | −0.471 |

| (0.161) | (0.167) | (0.349) | (0.443) | |

| Years of work | 0.008 | 0.001 | 0.035 * | 0.013 |

| (0.008) | (0.009) | (0.020) | (0.022) | |

| First heard about mobile money (months ago) | −0.002 | 0.002 | 0.0128 * | 0.0200 *** |

| (0.003) | (0.004) | (0.007) | (0.008) | |

| Minutes to bank | −0.000 | −0.002 | 0.001 | −0.007 |

| (0.002) | (0.002) | (0.004) | (0.005) | |

| Rural | −0.107 | 0.060 | −0.170 | 0.480 |

| (0.111) | (0.176) | (0.341) | (0.375) | |

| Urban | −0.142 | 0.185 | −0.872 ** | −0.842 ** |

| (0.148) | (0.171) | (0.367) | (0.403) | |

| Constant | 5.811 *** | 4.914 *** | −0.041 | 3.230 *** |

| (0.427) | (0.578) | (0.985) | (1.183) | |

| Observations | 557 | 557 | 557 | 557 |

| R-squared | 0.379 | 0.264 | 0.213 | 0.170 |

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| ln Investment in Business | ln Investment in Education | ln Investment in Health | ln Savings | ln Consumption | |

| User | 1.029 *** | 1.218 *** | 0.218 | 1.363 *** | 0.240 ** |

| (0.336) | (0.375) | (0.245) | (0.330) | (0.116) | |

| ln (Financial assets) | 0.212 ** | 0.294 ** | 0.092 | 0.551 *** | 0.048 |

| (0.088) | (0.128) | (0.068) | (0.092) | (0.036) | |

| Age | 0.049 *** | 0.076 *** | 0.039 *** | −0.018 | 0.013 ** |

| (0.018) | (0.021) | (0.012) | (0.015) | (0.006) | |

| Male | 0.214 | −0.298 | −0.698 *** | 0.447 | 0.084 |

| (0.336) | (0.322) | (0.221) | (0.305) | (0.109) | |

| Years of schooling | −0.007 | −0.027 | −0.007 | 0.077 | 0.004 |

| (0.040) | (0.061) | (0.028) | (0.051) | (0.013) | |

| Household size | 0.175 ** | 0.462 *** | 0.132 *** | −0.115 | 0.068 ** |

| (0.077) | (0.082) | (0.043) | (0.077) | (0.033) | |

| Non-household dependents | 0.647 ** | 0.585 ** | 0.227 | 0.804 *** | 0.101 |

| (0.276) | (0.258) | (0.169) | (0.256) | (0.093) | |

| Married | −0.190 | 0.246 | −0.177 | −0.266 | 0.048 |

| (0.362) | (0.482) | (0.286) | (0.366) | (0.142) | |

| Minutes of walk to the nearest vendor | 0.009 | −0.041 | −0.047 ** | 0.040 | −0.013 |

| (0.034) | (0.034) | (0.023) | (0.032) | (0.011) | |

| Discount rate | 0.130 | −2.253 * | −1.007 | 1.712 * | −0.837 *** |

| (0.988) | (1.190) | (0.787) | (1.022) | (0.299) | |

| Present bias | −0.826 | 4.050 *** | −0.194 | −0.559 | 1.180 *** |

| (1.402) | (1.311) | (0.854) | (1.408) | (0.310) | |

| Risk-averse | −0.012 | 0.004 | −0.022 | −0.041 | 0.033 |

| (0.058) | (0.060) | (0.046) | (0.065) | (0.021) | |

| ln (Physical assets) | 0.382 *** | 0.089 | 0.018 | 0.222 ** | 0.085** |

| (0.092) | (0.098) | (0.069) | (0.091) | (0.034) | |

| Migrant | −0.302 | −0.461 | −0.002 | −0.546 | −0.171 |

| (0.352) | (0.382) | (0.267) | (0.339) | (0.134) | |

| Formal employment | −0.578 | 0.027 | −1.810 * | 1.720 | −0.272 |

| (0.552) | (1.557) | (0.997) | (1.155) | (0.537) | |

| Self-employment | 1.479 *** | −0.598 | −0.004 | 0.182 | −0.112 |

| (0.362) | (0.499) | (0.279) | (0.395) | (0.136) | |

| Years of work | −0.005 | 0.047 ** | 0.012 | 0.057 *** | 0.007 |

| (0.022) | (0.020) | (0.015) | (0.020) | (0.010) | |

| First heard about mobile money (months) | 0.011 | 0.007 | 0.015 *** | 0.007 | −0.003 |

| (0.008) | (0.010) | (0.006) | (0.009) | (0.003) | |

| Minutes to bank | −0.000 | 0.003 | 0.002 | −0.004 | −0.001 |

| (0.004) | (0.006) | (0.003) | (0.005) | (0.002) | |

| Rural | 0.917 ** | −0.544 | 0.634 ** | −0.330 | −0.209 * |

| (0.371) | (0.443) | (0.300) | (0.398) | (0.126) | |

| Urban | 0.153 | 0.318 | 0.559 * | 0.405 | −0.188 |

| (0.445) | (0.457) | (0.328) | (0.410) | (0.159) | |

| Constant | −6.522 *** | −2.823 * | 1.624 * | −4.444 *** | 6.483 *** |

| (1.018) | (1.446) | (0.838) | (1.103) | (0.395) | |

| Observations | 557 | 557 | 557 | 557 | 553 |

| R-squared | 0.298 | 0.334 | 0.171 | 0.280 | 0.196 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Apiors, E.K.; Suzuki, A. Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana. Sustainability 2018, 10, 1409. https://doi.org/10.3390/su10051409

Apiors EK, Suzuki A. Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana. Sustainability. 2018; 10(5):1409. https://doi.org/10.3390/su10051409

Chicago/Turabian StyleApiors, Emmanuel Kwablah, and Aya Suzuki. 2018. "Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana" Sustainability 10, no. 5: 1409. https://doi.org/10.3390/su10051409

APA StyleApiors, E. K., & Suzuki, A. (2018). Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana. Sustainability, 10(5), 1409. https://doi.org/10.3390/su10051409