Relationship of Ethical Leadership, Corporate Social Responsibility and Organizational Performance

Abstract

1. Introduction

2. Literature Review

2.1. Franchise Industry

2.2. Ethical Leadership

2.3. Corporate Social Responsibility

2.4. Organizational Performance

2.5. Research Hypothesis Development

3. Methods

3.1. Sample and Data Collection

3.2. Operationalization of Variables

4. Results

4.1. Profile of Respondents

4.2. Data Analysis

4.3. Testing Hypothesized Structural Models

4.4. Hypothesis Testing

4.5. Mediation Test

5. Discussion

6. Conclusions

7. Limitations and Recommendations

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Waddock, S. Parallel universes: Companies, academics, and the progress of corporate citizenship. Bus. Soc. Rev. 2004, 109, 5–42. [Google Scholar] [CrossRef]

- Du, S.; Bhattacharya, C.B.; Sen, S. Corporate social responsibility and competitive advantage: Overcoming the trust barrier. Manag. Sci. 2011, 57, 1528–1545. [Google Scholar] [CrossRef]

- Du, S.; Swaen, V.; Lindgreen, A.; Sen, S. The roles of leadership styles in corporate social responsibility. J. Bus. Ethics 2013, 114, 155–169. [Google Scholar] [CrossRef]

- Font, X.; Garay, L.; Jones, S. Sustainability motivations and practices in small tourism enterprises in European protected areas. J. Clean. Prod. 2016, 137, 1439–1448. [Google Scholar] [CrossRef]

- Palazzo, G.; Scherer, A. Corporate legitimacy as deliberation: A communicative framework. J. Bus. Ethics 2006, 66, 71–88. [Google Scholar] [CrossRef]

- Garay, L.; Font, X. doing good to do well? Corporate responsibility reasons, practices and impacts in small and medium accommodation enterprises. Int. J. Hosp. Manag. 2012, 31, 329–337. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Admin. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Hoffman, A.J.; Bazerman, M.H. Changing practice on sustainability: Understanding and overcoming the organizational and psychological barriers to action. In Organizations and the Sustainability Mosaic. Crafting Long-Term Ecological and Societal Solutions; Edward Elgar: Cheltenham, UK; Northampton, MA, USA, 2007; pp. 84–105. [Google Scholar]

- Daft, R.L.; Weick, K.E. Toward a model of organizations as interpretation systems. Acad. Manag. Rev. 1984, 9, 284–295. [Google Scholar]

- Child, J. Strategic choice in the analysis of action, structure, organizations and environment: Retrospect and prospect. Organ. Stud. 1997, 18, 43–76. [Google Scholar] [CrossRef]

- Sharma, S. Managerial interpretations and organizational context as predictors of corporate choice of environmental strategy. Acad. Manag. J. 2000, 43, 681–697. [Google Scholar] [CrossRef]

- Graci, S.; Dodds, R. Why go green? The business case of environmental commitment in the Canadian hotel industry. Anatolia 2008, 19, 251–270. [Google Scholar] [CrossRef]

- Lee, Y.K.; Kim, S.; Kim, M.S.; Lee, J.H.; Lim, K.T. Relational bonding strategies in the franchise industry: The moderating role of duration of the relationship. J. Bus. Ind. Mark. 2015, 30, 830–841. [Google Scholar] [CrossRef]

- Mittal, S.; Dhar, R.L. Effect of green transformational leadership on green creativity: A study of tourist hotels. Tour. Manag. 2016, 57, 118–127. [Google Scholar] [CrossRef]

- Waldman, D.A.; Siegel, D.S. Defining the socially responsible leader. Leadersh. Q. 2008, 19, 117–131. [Google Scholar] [CrossRef]

- Pless, N.M.; Maak, T.; Stahl, G.K. Developing responsible global leaders through international service-learning programs: The Ulyssess experience. Acad. Manag. Learn. Edu. 2011, 10, 237–260. [Google Scholar] [CrossRef]

- Maak, T.; Pless, N.M. Responsible leadership in a stakeholder society: A relational perspective. J. Bus. Ethics 2006, 66, 99–115. [Google Scholar] [CrossRef]

- Waldman, D.A.; Siegel, D.S.; Javidan, M. Components of CEO transformational leadership and corporate social responsibility. J. Manag. Stud. 2006, 43, 1703–1725. [Google Scholar] [CrossRef]

- Groves, K.S.; LaRocca, M.A. Responsible leadership outcomes via stakeholder CSR values: Testing a values-centered model of transformational leadership. J. Bus. Ethics 2011, 98, 37–55. [Google Scholar] [CrossRef]

- Brown, M.E.; Treviño, L.K.; Harrison, D.A. Ethical leadership: A social learning perspective for construct development and testing. Organ. Behav. Hum. Decis. 2005, 97, 117–134. [Google Scholar] [CrossRef]

- Walumbwa, F.O.; Mayer, D.M.; Wang, P.; Wang, H.; Workman, K.; Christensen, A.L. Linking ethical leadership to employee performance: The roles of leader-member exchange, self-efficacy, and organizational identification. Organ. Behav. Hum. Decis. 2011, 115, 204–213. [Google Scholar] [CrossRef]

- Zhu, W.; May, D.R.; Avolio, B.J. The impact of ethical leadership behavior on employee outcomes: The roles of psychological empowerment and authenticity. J. Leadersh. Organ. Stud. 2004, 11, 16–26. [Google Scholar]

- Eisenbeiss, S.A.; van Knippenberg, D.; Fahrbach, C.M. Doing well by doing good? Analyzing the relationship between CEO ethical leadership and firm performance. J. Bus. Ethics 2015, 128, 635–651. [Google Scholar] [CrossRef]

- Christie, P.M.J.; Kwon, I.W.G.; Stoeberl, P.A.; Baumhart, R. A cross-cultural comparison of ethical attitudes of business managers: India Korea and the United States. J. Bus. Ethics 2003, 46, 263–287. [Google Scholar] [CrossRef]

- Hofstede, G.; Hofstede, G.J. Cultures and Organizations: Software of the Mind, 2nd ed.; McGraw Hill: New York, NY, USA, 2005; ISBN 9780071439596. [Google Scholar]

- Badrinarayanan, V.; Suh, T.; Kim, K.M. Brand resonance in franchising relationships: A franchisee-based perspective. J. Bus. Res. 2016, 69, 3943–3950. [Google Scholar] [CrossRef]

- Youn, H.; Hua, N.; Lee, S. Does size matter? Corporate social responsibility and firm performance in the restaurant industry. Int. J. Hosp. Manag. 2015, 51, 127–134. [Google Scholar] [CrossRef]

- Avey, J.B.; Palanski, M.E.; Walumbwa, F.O. When leadership goes unnoticed: The moderating role of follower self-esteem on the relationship between ethical leadership and follower behavior. J. Bus. Ethics 2011, 98, 573–582. [Google Scholar] [CrossRef]

- Treviño, L.K.; Weaver, G.R.; Reynolds, S.J. Behavioral ethics in organizations: A review. J. Manag. 2006, 32, 951–990. [Google Scholar] [CrossRef]

- Bass, B.M.; Steidlmeier, P. Ethics, character, and authentic transformational leadership behavior. Leadersh. Q. 1999, 10, 181–217. [Google Scholar] [CrossRef]

- Ciulla, J.B. Ethics, the Heart of Leadership; Praeger Publishers: Santa Barbara, CA, USA, 2004; ISBN 9781440830655. [Google Scholar]

- Demirtas, O.; Akdogan, A.A. The effect of ethical leadership behavior on ethical climate, turnover intention, and affective commitment. J. Bus. Ethics 2015, 130, 59–67. [Google Scholar] [CrossRef]

- Palanski, M.E.; Yammarino, F.J. Integrity and leadership: A multi-level conceptual framework. Leadersh. Q. 2009, 20, 405–420. [Google Scholar] [CrossRef]

- Yukl, G.A. Leadership in Organizations, 5th ed.; Prentice Hall: Englewood Cliffs, NJ, USA, 2002; ISBN 9780130323125. [Google Scholar]

- Bandura, A. Social Foundations of Thought and Action; Free Press: Englewood Cliffs, NJ, USA, 1986; ISBN 9780138156145. [Google Scholar]

- Brown, M.E.; Treviño, L.K. Ethical leadership: A review and future directions. Leadersh. Q. 2006, 17, 595–616. [Google Scholar] [CrossRef]

- Font, X.; Guix, M.; Bonilla-Priego, M.J. Corporate social responsibility in cruising: Using materiality analysis to create shared value. Tour. Manag. 2016, 53, 175–186. [Google Scholar] [CrossRef]

- Lee, Y.K.; Kim, Y.; Lee, K.H.; Li, D.X. The impact of CSR on relationship quality and relationship outcomes: A perspective of service employees. Int. J. Hosp. Manag. 2012, 31, 745–756. [Google Scholar] [CrossRef]

- Zhang, D.; Ma, Q.; Morse, S. Motives for corporate social responsibility in Chinese food companies. Sustainability 2018, 10, 117. [Google Scholar] [CrossRef]

- Wallich, H.C.; McGowan, J.J. Stockholder interest and the corporation’s role in social policy. In A New Rationale for Corporate Social Policy; Committee for Economic Development: Washington, DC, USA, 1970; pp. 39–59. [Google Scholar]

- Carini, C.; Comincioli, N.; Poddi, L.; Vergalli, S. Measure the performance with the market value added: Evidence from CSR companies. Sustainability 2017, 9, 2171. [Google Scholar] [CrossRef]

- Coles, T.; Fenclova, E.; Dinan, C. Tourism and corporate social responsibility: A critical review and research agenda. Tour. Manag. Perspect. 2013, 6, 122–141. [Google Scholar] [CrossRef]

- Lee, Y.K.; Nor, Y.S.; Choi, J.W.; Kim, S.; Han, S.H.; Lee, J.H. Why does franchisor social responsibility really matter? Int. J. Hosp. Manag. 2016, 53, 49–58. [Google Scholar] [CrossRef]

- Carroll, A.B. A three dimensional conceptual model of corporate social performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horizon. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Garriga, E.; Melé, D. Corporate social responsibility theories: Mapping the territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Park, S.Y.; Lee, S. Financial rewards for social responsibility: A mixed picture for restaurant companies. Cornell Hosp. Q. 2009, 50, 168–179. [Google Scholar] [CrossRef]

- Ye, C.; Cronin, J.J.; Peloza, J. The role of corporate social responsibility in consumer evaluation of nutrition informational disclosure by retail restaurants. J. Bus. Ethics 2015, 130, 313–326. [Google Scholar] [CrossRef]

- Fraj-Andrés, E.; Martinez-Salinas, E.; Matute-Vallejo, J. A multidimensional approach to the influence of environmental marketing and orientation on the firm’s organizational performance. J. Bus. Ethics 2009, 88, 263–286. [Google Scholar] [CrossRef]

- González-Benito, J.; González-Benito, Ó. Environmental proactivity and business performance: An empirical analysis. Omega 2005, 33, 1–15. [Google Scholar] [CrossRef]

- Miles, M.P.; Covin, J.G. Environmental marketing: A source of reputational, competitive, and financial advantage. J. Bus. Ethics 2000, 23, 299–311. [Google Scholar] [CrossRef]

- Zhang, Z. Developing a model of quality management methods and evaluating their effects on business performance. Total Qual. Manag. 2000, 11, 129–137. [Google Scholar] [CrossRef]

- Kotler, P. Marketing Management: Analysis, Planning, Implementation and Control, 8th ed.; Prentice-Hall: London, UK, 1994; ISBN 9780137228515. [Google Scholar]

- Menon, A.; Menon, A.; Chowdhury, J.; Jankovish, J. Evolving paradigm for environmental sensitivity in marketing programs: A synthesis of theory and practice. J. Mark. Theory Pract. 1999, 7, 1–15. [Google Scholar] [CrossRef]

- Menguc, B.; Ozanne, L.K. Challenges of the “green imperative”: A natural resource-based approach to the environmental orientation-business performance relationship. J. Bus. Res. 2005, 58, 430–438. [Google Scholar] [CrossRef]

- Tang, Z.; Hull, C.E.; Rothenberg, S. How corporate social responsibility engagement strategy moderates the CSR-financial performance relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Kim, W.G.; Brymer, R.A. The effects of ethical leadership on manager job satisfaction, commitment, behavioral outcomes, and firm performance. Int. J. Hosp. Manag. 2011, 30, 1020–1026. [Google Scholar] [CrossRef]

- Thomas, T.; Schermerhom, J.R.; Dienhart, J.W. Strategic leadership of ethical behavior in business. Acad. Manag. Exec. 2004, 18, 56–66. [Google Scholar] [CrossRef]

- Hambrick, D.C. Upper echelons theory: An update. Acad. Manag. Rev. 2007, 32, 334–343. [Google Scholar] [CrossRef]

- Finkelstein, S.; Hambrick, D.C.; Canella, A.A. Strategic Leadership: Theory and Research on Executives, Top Management Teams, and Boards; Oxford University Press: Oxford, UK, 2009; ISBN 9780195162073. [Google Scholar]

- Carpenter, M.A.; Geletkanycz, M.A.; Sanders, W.G. Upper echelons research revisited: Antecedents, elements, and consequences of top management team composition. J. Manag. 2004, 30, 749–778. [Google Scholar] [CrossRef]

- Abdullah, M.I.; Ashraf, S.; Sarfraz, M. The organizational identification perspective of CSR on creative performance: The moderating role of creative self-efficacy. Sustainability 2017, 9, 2125. [Google Scholar] [CrossRef]

- Lai, C.S.; Chiu, C.J.; Yang, C.F.; Pai, D.C. The effects of corporate social responsibility on brand performance: The mediating effect of industrial brand equity and corporate reputation. J. Bus. Ethics 2010, 95, 457–469. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Chen, Y.S. The driver of green innovation and green image—Green core competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2007, 85, 136–137. [Google Scholar]

- Hubbard, G. Measuring organizational performance: Beyond the triple bottom line. Bus. Strateg. Environ. 2009, 18, 177–191. [Google Scholar] [CrossRef]

- Zhu, Y.; Sun, L.Y.; Leung, A.S.M. Corporate social responsibility, firm reputation, and firm performance: The role of ethical leadership. Asia Pac. J. Manag. 2014, 31, 925–947. [Google Scholar] [CrossRef]

- Manner, M.H. The impact of CEO characteristics on corporate social performance. J. Bus. Ethics 2010, 93, 53–72. [Google Scholar] [CrossRef]

- Fair Trade Commission. The Franchise Industry. 2015. Available online: http://franchise.ftc.go.kr/franchise/statistics.jsp (accessed on 10 October 2017).

- Bergeron, F.; Raymond, L.; Rivard, S. Ideal patterns of strategic alignment and business performance. Inf. Manag. 2004, 41, 1003–1020. [Google Scholar] [CrossRef]

- Schein, E. Organizational Culture and Leadership, 3rd ed.; Jossey-Bass: San Francisco, CA, USA, 2004; ISBN 9780787968458. [Google Scholar]

- Chosun Biz The ratio of female executives, SK 2%, LG 1.9%...it may be reverse discrimination against males, 2016. Available online: http://biz.chosun.com/site/data/html_dir/2013/02/18/2013021802217.html (accessed on 8 November 2017).

- Lee, E.M.; Park, S.Y.; Lee, H.J. Employee perception of CSR activities: Its antecedents and consequences. J. Bus. Res. 2013, 66, 1716–1724. [Google Scholar] [CrossRef]

- Anderson, J.C.; Gerbing, D.W. Structural equation modeling in practice: A review and recommended two-step approach. Psychol. Bull. 1988, 103, 411–423. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Pers. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef] [PubMed]

- Angus-Leppan, T.; Metcalf, L.; Benn, S. Leadership styles and CSR practices: An examination of sensemaking, institutional drivers and CSR leadership. J. Bus. Ethics 2010, 93, 189–213. [Google Scholar] [CrossRef]

- Lee, Y.K.; Choi, J.W.; Moon, B.Y.; Babin, B.J. Codes of ethics, corporate philanthropy, and employee responses. Int. J. Hosp. Manag. 2014, 39, 97–106. [Google Scholar] [CrossRef]

- Frumkin, P. Food under fire. Nation’s Restaurant News. 17 May 2010, Volume 44, pp. 23–24. Available online: http://www.nrn.com/archive/food-under-fire (accessed on 8 February 2018).

- Farrington, T.; Curran, R.; Gori, K.; O’Gorman, K.D.; Queenan, J. Corporate social responsibility: Reviewed, rated, revised. Int. J. Contemp. Hosp. Manag. 2017, 29, 30–47. [Google Scholar] [CrossRef]

- Skarlicki, D.P.; Latham, G.P. Leadership training in organizational justice to increase citizenship behavior within a labor union: A replication. Pers. Psychol. 1997, 50, 617–633. [Google Scholar] [CrossRef]

- Tenbrunsel, A.E.; Smith-Crowe, K.; Umphress, E.E. Building houses on rocks: The role of the ethical infrastructure in organizations. Soc. Justice Res. 2003, 16, 285–307. [Google Scholar] [CrossRef]

- Hu, H.H.; Parsa, H.G.; Self, J. The dynamics of green restaurant patronage. Cornell Hosp. Q. 2010, 51, 344–362. [Google Scholar] [CrossRef]

- Maon, F.; Lindgreen, A.; Swaen, V. Designing and implementing corporate social responsibility: An integrative framework grounded in theory and practice. J. Bus. Ethics 2009, 87, 71–89. [Google Scholar] [CrossRef]

{kind=link}

| Constructs and Items | Standardized Loading | t-Value |

|---|---|---|

| Economic CSR (α = 0.773) | ||

| Our business has a procedure in place to respond to every customer complaint. | - | - |

| We continuously improve the quality of our products. | - | - |

| We use customer satisfaction as an indicator of our business performance. | 0.727 | Fixed |

| We have been successful at maximizing profits. | 0.684 | 8.602 |

| We strive to lower operating costs. | 0.787 | 9.651 |

| We closely monitor employee’s productivity. | - | - |

| Top management establishes long-term strategies for our business. | - | - |

| Legal CSR (α = 0.854) | ||

| Managers are informed about relevant environmental laws. | 0.757 | Fixed |

| All our products meet legal standards. | 0.764 | 10.887 |

| Our contractual obligations are always honored. | 0.801 | 11.488 |

| The managers of this organization try to comply with the law. | - | - |

| Our company seeks to comply with all laws regulating hiring and employee benefits. | 0.769 | 10.978 |

| We have programs that encourage the diversity of our workplace (in terms of age, gender or race). | - | - |

| Ethical CSR (α = 0.873) | ||

| Our business has a comprehensive code of conduct. | - | - |

| Members of our organization follow professional standards. | 0.820 | Fixed |

| Top managers monitor the potential negative impacts of our activities in our community. | 0.834 | 13.697 |

| We are recognized as a trustworthy company. | 0.767 | 12.178 |

| Fairness toward co-workers and business partners is an integral part of our employee evaluation process. | 0.761 | 12.053 |

| A confidential procedure is in place for employees to report any misconduct at work. | - | - |

| Philanthropic CSR (α = 0.923) | ||

| The corporation tries to improve perception of its business conduct. | 0.898 | Fixed |

| The corporation tries to help the poor. | 0.950 | 22.187 |

| The corporation tries to contribute toward bettering the local community. | 0.861 | 17.608 |

| The corporation tries to fulfill its social responsibility. | 0.767 | 14.013 |

| Constructs and Items | Standardized Loading | t-Value |

|---|---|---|

| Ethical leadership (α = 0.964) | ||

| Conducts his/her personal life in an ethical manner. | 0.791 | Fixed |

| Defines success not just by results but also the way that they are obtained. | 0.935 | 15.930 |

| Listens to what employees have to say. | - | - |

| Disciplines employees who violate ethical standards. | 0.957 | 16.472 |

| Makes fair and balanced decisions. | 0.911 | 15.318 |

| Can be trusted. | - | - |

| Discusses business ethics or values with employees. | - | - |

| Sets an example of how to do things the right way in terms of ethics. | 0.869 | 14.302 |

| Has the best interests of employees in mind. | - | - |

| When making decisions, asks “what is the right thing to do?” | - | - |

| CSR (α = 0.964) | ||

| Economic CSR. | 0.750 | Fixed |

| Legal CSR. | 0.884 | 12.939 |

| Ethical CSR. | 0.876 | 12.805 |

| Philanthropic CSR. | 0.857 | 12.494 |

| Operational performance (α = 0.965) | ||

| Final production costs. | - | - |

| Product quality. | 0.833 | Fixed |

| Innovation capacity in new product development. | 0.850 | 14.292 |

| Pace of new product launching and range of products in catalogue. | 0.836 | 13.947 |

| Costs effiiciency. | 0.664 | 10.141 |

| Commercial performance (α = 0.877) | ||

| Corporate reputation. | 0.875 | Fixed |

| Alignment between company’s offer and market expectations. | 0.864 | 17.000 |

| Successful launching of new products onto the markets. | 0.816 | 15.205 |

| Corporate and brand image. | 0.916 | 19.298 |

| Customer loyalty. | - | - |

| Customer satisfaction. | 0.889 | 18.014 |

| Economic performance (α = 0.919) | ||

| Firm’s profitability. | 0.909 | Fixed |

| Sales growth. | - | - |

| Firm’s economic results. | 0.891 | 19.554 |

| Profit before tax. | 0.874 | 18.641 |

| Market share. | 0.898 | 19.961 |

| Construct | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| 1. Ethical leadership | 1 | ||||

| 2. CSR | 0.650 ** | 1 | |||

| 3. Operational performance | 0.582 ** | 0.602 ** | 1 | ||

| 4. Commercial performance | 0.512 ** | 0.616 ** | 0.703 ** | 1 | |

| 5. Economic performance | 0.515 ** | 0.509 ** | 0.625 ** | 0.742 ** | 1 |

| Mean | 3.998 | 5.018 | 4.875 | 5.092 | 4.742 |

| SD | 1.453 | 1.052 | 1.089 | 1.202 | 1.337 |

| AVE | 0.800 | 0.711 | 0.639 | 0.761 | 0.798 |

| CCR | 0.952 | 0.908 | 0.875 | 0.941 | 0.940 |

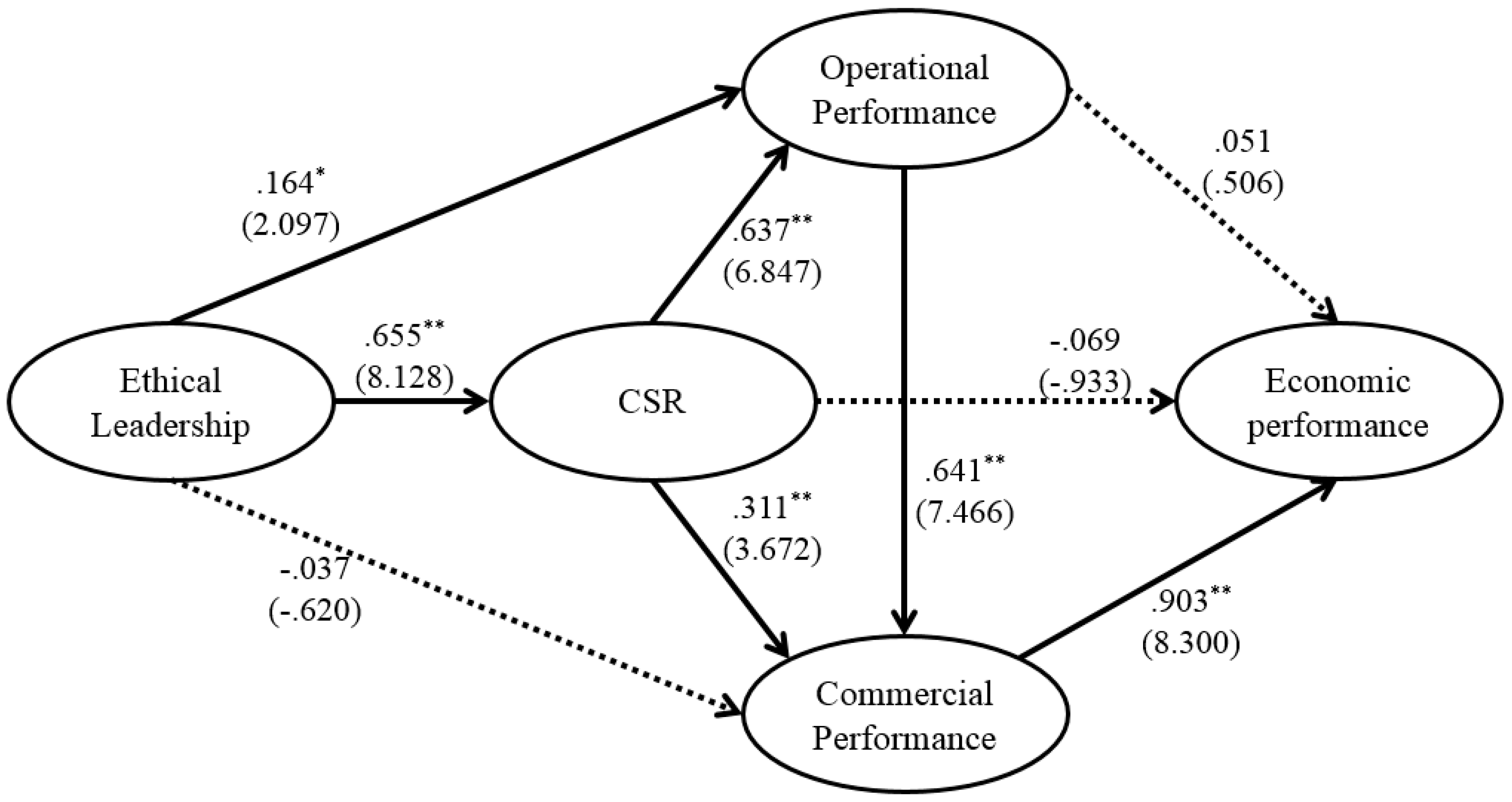

| Path | Standardized Estimates | Standardized Error | t-Value |

|---|---|---|---|

| Ethical leadership → CSR | 0.655 ** | 0.056 | 8.128 |

| Ethical leadership → Operational performance | 0.164 * | 0.063 | 2.097 |

| Ethical leadership → Commercial performance | −0.037 | 0.054 | −0.620 |

| CSR → Operational performance | 0.637 ** | 0.108 | 6.847 |

| CSR → Commercial performance | 0.311 ** | 0.110 | 3.672 |

| CSR → Economic performance | −0.069 | 0.109 | −0.933 |

| Operational performance → Commercial performance | 0.641 ** | 0.096 | 7.466 |

| Operational performance → Economic performance | 0.051 | 0.128 | 0.506 |

| Commercial performance → Economic performance | 0.903 ** | 0.125 | 8.300 |

| Endogenous variables | SMC (R2) | ||

| CSR | 0.429 | ||

| Operational performance | 0.570 | ||

| Commercial performance | 0.762 | ||

| Economic performance | 0.801 |

| Path | Indirect Effect | Direct Effect | LL CIs (95%) | UL CIs (95%) | Z-Value | Mediating Role |

|---|---|---|---|---|---|---|

| Ethical leadership → CSR → Operational performance | 0.576 ** | 0.164 ** | 0.319 | 0.558 | 5.210 | Partial mediator |

| CSR → Operational performance → Commercial performance | 0.408 ** | 0.311 ** | 0.289 | 0.558 | 5.018 | Partial mediator |

| CSR → Commercial performance → Economic performance | 0.682 ** | −0.069 | 0.546 | 0.845 | 3.331 | Full mediator |

| Operational performance → Commercial performance → Economic performance | 0.579 ** | 0.051 | 0.426 | 0.817 | 5.519 | Full mediator |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kim, M.-S.; Thapa, B. Relationship of Ethical Leadership, Corporate Social Responsibility and Organizational Performance. Sustainability 2018, 10, 447. https://doi.org/10.3390/su10020447

Kim M-S, Thapa B. Relationship of Ethical Leadership, Corporate Social Responsibility and Organizational Performance. Sustainability. 2018; 10(2):447. https://doi.org/10.3390/su10020447

Chicago/Turabian StyleKim, Min-Seong, and Brijesh Thapa. 2018. "Relationship of Ethical Leadership, Corporate Social Responsibility and Organizational Performance" Sustainability 10, no. 2: 447. https://doi.org/10.3390/su10020447

APA StyleKim, M.-S., & Thapa, B. (2018). Relationship of Ethical Leadership, Corporate Social Responsibility and Organizational Performance. Sustainability, 10(2), 447. https://doi.org/10.3390/su10020447