A New Framework for Assessing the Sustainability Reporting Disclosure of Water Utilities

Abstract

:1. Introduction

2. Theoretical Background

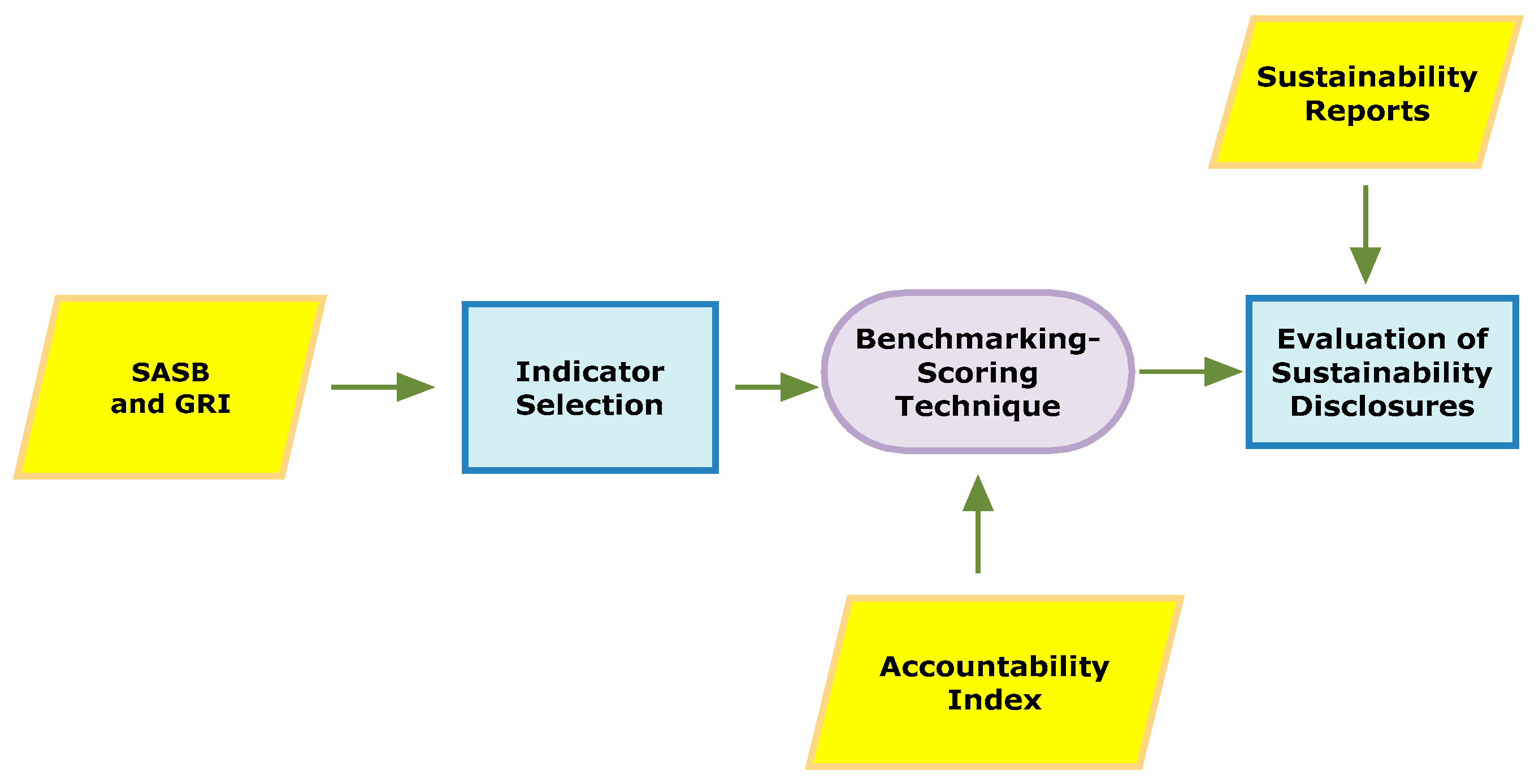

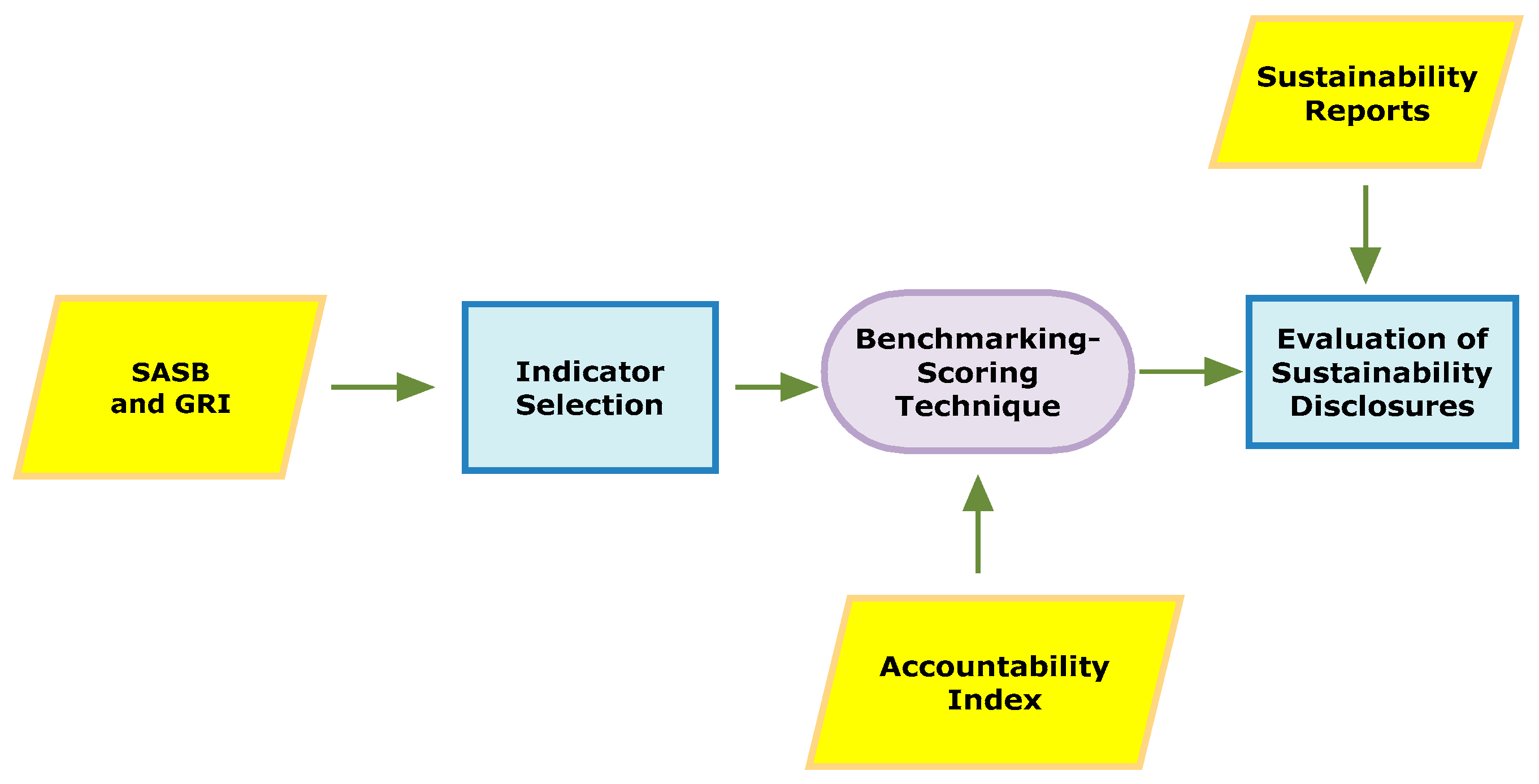

3. Research Methodology

3.1. Indicators’ Selection

3.2. Scoring System

- 0 points (Level 0): when information is not mentioned for a specific indicator;

- 1 point (Level 1): when qualitative information is mentioned for a specific indicator or when a quantitative indicator is present but not exactly in the form required by the standard;

- 2 points (Level 2): when quantitative information is mentioned for a specific indicator as required by the corresponding standard;

- 3 points (Level 3): when the report provides information which shows the progress of water utility‘s performance for a specific indicator (e.g., there is at least the previous year’s indicator to benchmark present performance).

3.3. Sample Selection

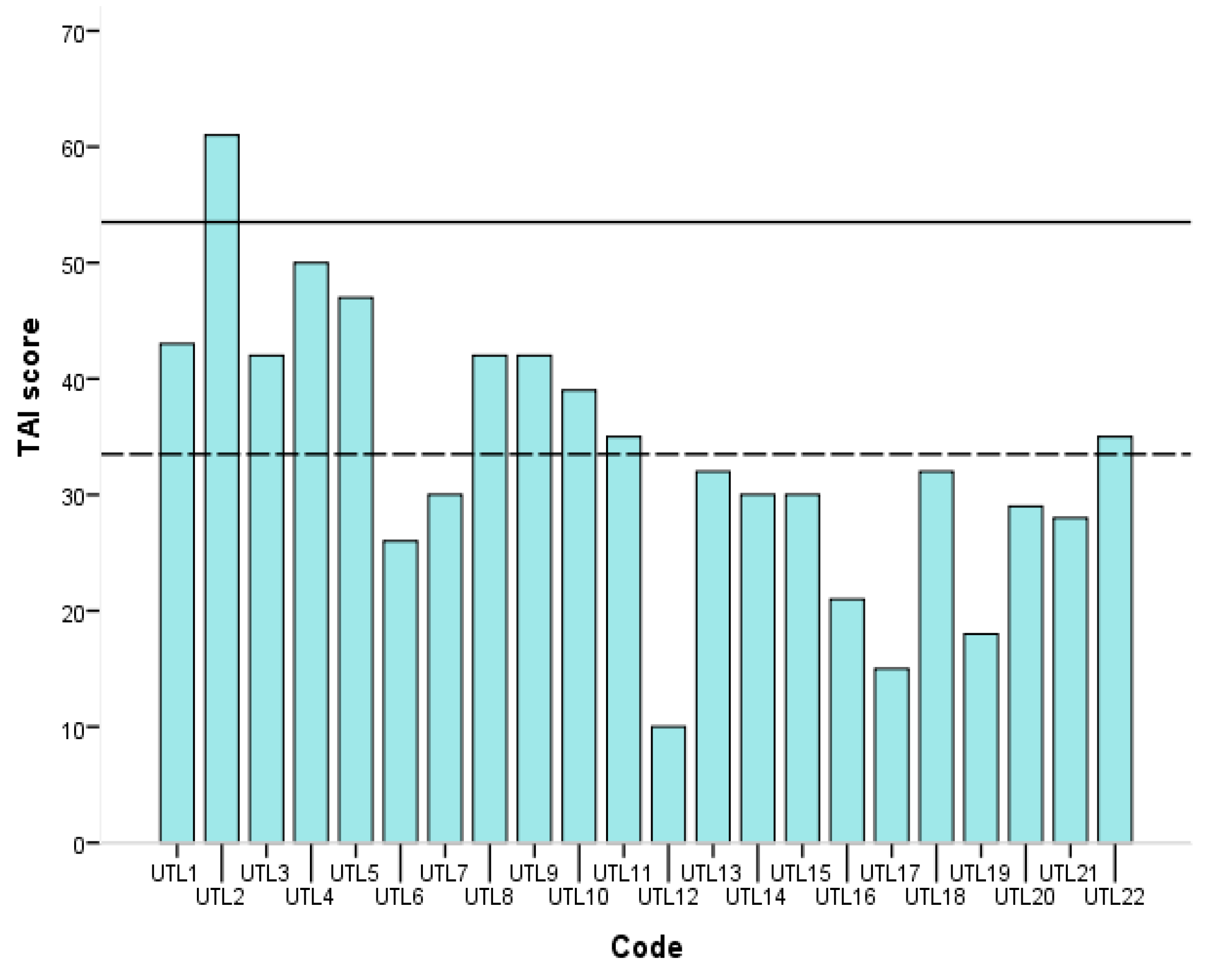

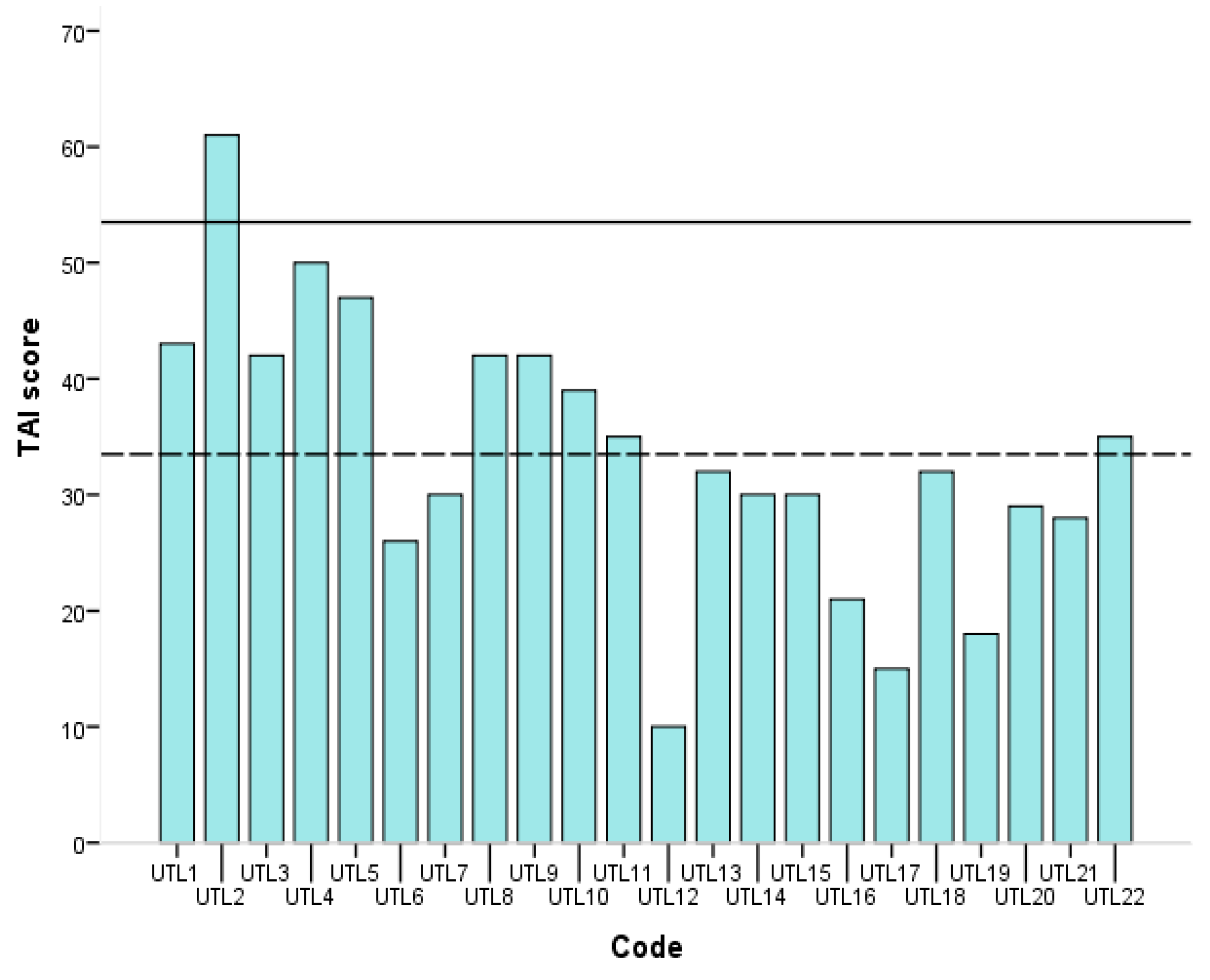

4. Data Analysis and Discussion

5. Conclusions

Author Contributions

Conflicts of Interest

References

- Bebbington, J.; Higgings, C.; Frame, B. Initiating sustainable development reporting: Evidence from New Zealand. Account. Audit. Account. J. 2009, 22, 588–625. [Google Scholar] [CrossRef]

- Belal, A.R.; Owen, D.L. The views of corporate managers on the current state of, and future prospects for, social reporting in Bangladesh: An engagement based study. Account. Audit. Account. J. 2007, 20, 472–494. [Google Scholar] [CrossRef]

- O’Dwyer, B. Managerial perceptions of corporate social disclosure: An Irish story. Account. Audit. Account. J. 2002, 15, 406–436. [Google Scholar] [CrossRef]

- Spence, C. Social and environmental reporting and hegemonic discourse. Account. Audit. Account. J. 2007, 20, 855–882. [Google Scholar] [CrossRef]

- Cantele, S. The trend of sustainability reporting in Italy: Some evidence from the last decade. Int. J. Econ. 2014, 6, 381–405. [Google Scholar] [CrossRef]

- Mio, C.; Venturelli, A. Non-financial Information About Sustainable Development and Environmental Policy in the Annual Reports of Listed Companies: Evidence from Italy and the UK. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 340–358. [Google Scholar] [CrossRef]

- Mio, C. Corporate social reporting in Italian multi-utility companies: An empirical analysis. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 247–271. [Google Scholar] [CrossRef]

- D’Andrea, A. Applying GRI Sustainability Reporting in the Water Sector: Evidences from an Italian Company. Int. J. Bus. Adm. 2017, 8, 10. [Google Scholar] [CrossRef]

- Baldwin, C.; Uhlmann, V. Accountability in planning for sustainable water supplies in South East Queensland. Aust. Plan. 2010, 47, 191–202. [Google Scholar] [CrossRef]

- Marie Lauesen, L. How well are water companies engaged in CSR? A critical cross-geographical discourse analysis. Soc. Responsib. J. 2014, 10, 115–136. [Google Scholar] [CrossRef]

- Greiling, D.; Traxler, A.A.; Stötzer, S. Sustainability reporting in the Austrian, German and Swiss public sector. Int. J. Public Sect. Manag. 2015, 28, 404–428. [Google Scholar] [CrossRef]

- Kiparsky, M.; Sedlak, D.L.; Thompson, B.H., Jr.; Truffer, B. The innovation deficit in urban water: The need for an integrated perspective on institutions, organizations, and technology. Environ. Eng. Sci. 2013, 30, 395–408. [Google Scholar] [CrossRef] [PubMed]

- Pahl-Wostl, C. Towards sustainability in the water sector–The importance of human actors and processes of social learning. Aquat. Sci. Res. Bound. 2002, 64, 394–411. [Google Scholar] [CrossRef]

- Marques, R.C.; da Cruz, N.F.; Pires, J. Measuring the sustainability of urban water services. Environ. Sci. Policy 2015, 54, 142–151. [Google Scholar] [CrossRef]

- Schaefer, A. Contrasting institutional and performance accounts of environmental management systems: Three case studies in the UK water and sewerage industry. J. Manag. Stud. 2007, 44, 506–535. [Google Scholar] [CrossRef]

- Arnold, M. The lack of strategic sustainability orientation in German water companies. Ecol. Econ. 2015, 117, 39–52. [Google Scholar] [CrossRef]

- Deegan, C. Introduction: The legitimising effect of social and environmental disclosures—A theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Greiling, D.; Grüb, B. Sustainability reporting in Austrian and German local public enterprises. J. Econ. Policy Reform 2014, 17, 209–223. [Google Scholar] [CrossRef]

- United Nations General Assembly. Transforming Our World: The 2030 Agenda for Sustainable Development, Resolution A/70/L.1, 2015. Available online: https://sustainabledevelopment.un.org/content/documents/21252030%20Agenda%20for%20Sustainable%20Development%20web.pdf (accessed on 20 November 2017).

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar]

- Porter, M.E.; Kramer, M.R. Strategy & society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Porter, M.E.; Kramer, M.R. The Big Idea: Creating Shared Value. How to reinvent capitalism—and unleash a wave of innovation and growth. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Lehman, G. Disclosing new worlds: A role for social and environmental accounting and auditing. Account. Organ. Soc. 1999, 24, 217–241. [Google Scholar] [CrossRef]

- Chen, J.C.; Roberts, R.W. Toward a more coherent understanding of the organization–society relationship: A theoretical consideration for social and environmental accounting research. J. Bus. Ethics 2010, 97, 651–665. [Google Scholar] [CrossRef]

- Tomaževič, N.; Tekavčič, M.; Peljhan, D. Towards excellence in public administration: Organisation theory-based performance management model. Total Qual. Manag. Bus. Excell. 2017, 28, 578–599. [Google Scholar] [CrossRef]

- Clarke, J.; Gibson-Sweet, M. The use of corporate social disclosures in the management of reputation and legitimacy: A cross sectoral analysis of UK Top 100 Companies. Bus. Ethics Eur. Rev. 1999, 8, 5–13. [Google Scholar] [CrossRef]

- Von Schwedler, M. CSR in the UK Water Industry: ‘Doing the Right Thing’? A Case Study. Soc. Environ. Account. J. 2011, 31, 125–137. [Google Scholar] [CrossRef]

- Molinos-Senante, M.; Marques, R.C.; Pérez, F.; Gómez, T.; Sala-Garrido, R.; Caballero, R. Assessing the sustainability of water companies: A synthetic indicator approach. Ecol. Indic. 2016, 61, 577–587. [Google Scholar] [CrossRef]

- Tregidga, H.; Milne, M.J. From sustainable management to sustainable development: A longitudinal analysis of a leading New Zealand environmental reporter. Bus. Strateg. Environ. 2006, 15, 219–241. [Google Scholar] [CrossRef]

- Larrinaga-Gonzélez, C.; Pérez-Chamorro, V. Sustainability accounting and accountability in public water companies. Public Money Manag. 2008, 28, 337–343. [Google Scholar] [CrossRef]

- Palme, U.; Tillman, A.M. Sustainable development indicators: How are they used in Swedish water utilities? J. Clean. Prod. 2008, 16, 1346–1357. [Google Scholar] [CrossRef]

- Linneman, M.H.; Hoekstra, A.Y.; Berkhout, W. Ranking water transparency of Dutch Stock-listed companies. Sustainability 2015, 7, 4341–4359. [Google Scholar] [CrossRef]

- Kleinman, G.; Kuei, C.-H.; Lee, P. Using formal concept analysis to examine water disclosure in corporate social responsibility reports. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 241–356. [Google Scholar] [CrossRef]

- Lambooy, T. Corporate social responsibility: Sustainable water use. J. Clean. Prod. 2011, 19, 852–866. [Google Scholar] [CrossRef]

- Askham, T.M.; Van der Poll, H.M. Water Sustainability of Selected Mining Companies in South Africa. Sustainability 2017, 9, 957. [Google Scholar] [CrossRef]

- Nikolaou, I.E.; Kourouklaris, G.; Tsalis, T.A. A framework to assist the financial community in incorporating water risks into their investment decisions. J. Sustain. Financ. Invest. 2014, 4, 93–109. [Google Scholar] [CrossRef]

- Krippendorff, K. Content Analysis: An Introduction to Its Methodology; Sage: Thousand Oaks, CA, USA, 2013. [Google Scholar]

- Milne, M.J.; Adler, R.W. Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar] [CrossRef]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- SASB. Water Utilities Sustainability Accounting Standard, Sustainability Accounting Standards Board. March 2016. Available online: https://www.sasb.org/wpcontent/uploads/2016/03/IF0103_WaterUtilities_Standard.pdf (accessed on 20 October 2017).

- GRI 303: Water 2016. Available online: https://www.globalreporting.org/standards/gri-standards-download-center/?g=38662903-539c-4e4b-b76f-7a105c475de0 (accessed on 20 October 2017).

- GRI 306: Effluents and Waste 2016. Available online: https://www.globalreporting.org/standards/gri-standards-download-center/?g=38662903-539c-4e4b-b76f-7a105c475de0 (accessed on 20 October 2017).

- Pinto, F.S.; Simões, P.; Marques, R.C. Raising the bar: The role of governance in performance assessments. Util. Policy 2017, 49, 38–47. [Google Scholar] [CrossRef]

- Nikolaou, I.E.; Tsalis, T.A. Development of a sustainable balanced scorecard framework. Ecol. Indic. 2013, 34, 76–86. [Google Scholar] [CrossRef]

- Tsalis, T.; Avramidou, A.; Nikolaou, I.E. A social LCA framework to assess the corporate social profile of companies: Insights from a case study. J. Clean. Prod. 2017, 164 (Suppl. C), 1665–1676. [Google Scholar] [CrossRef]

- Demertzidis, N.; Tsalis, T.A.; Loupa, G.; Nikolaou, I.E. A benchmarking framework to evaluate business climate change risks: A practical tool suitable for investors decision-making process. Clim. Risk Manag. 2015, 10, 95–105. [Google Scholar] [CrossRef]

- Global Reporting Initiative. Sustainability Disclosure Database Data Legend. 2015. Available online: https://www.globalreporting.org/SiteCollectionDocuments/GRI-Data-Legend-Sustainability-Disclosure-Database-Profiling.pdf (accessed on 20 October 2017).

{kind=link}

{kind=link}

| Description | Description | ||||

|---|---|---|---|---|---|

| Aspect A:Water withdrawal | Aspect G: Drinking Water Quality | ||||

| A1 | Total volume of water withdrawal by source (surface water, groundwater) | Qnt | G1 | Drinking Water Quality | Qnt |

| A2 | Total volume or % of water purchased from a third party | Qnt | G2 | Number of health-based and non-health-based quality violations | Qnt |

| Aspect B: Water sources significantly affected and water scarcity | Aspect H: Complaints and grievance mechanism | ||||

| B1 | Total number of water sources significantly affected by withdrawal by type | Qnt | H1 | Number of customer complaints regarding pricing | Qnt |

| B2 | Size of the water source | Qnt | H2 | Number of customer complaints regarding water quality issues | Qnt |

| B3 | Total fresh water sourced from regions with High or Extremely High Baseline Water Stress | Qnt | H3 | Number of customer complaints regarding disruptions to water supply | Qnt |

| B4 | Indication of withdrawal from nationally or internationally protected areas, or biodiversity areas | Qlt | H4 | Discussion of how considerations of fair pricing and access are integrated into determinations of rate structures | Qlt |

| B5 | Value or importance of the water source to local communities and indigenous population | Qlt | Aspect I: End-use efficiency and water protection initiatives | ||

| Aspect C:Water recycled/reused and discharged | I1 | Customer water savings from efficiency measures by market | Qnt | ||

| C1 | Total volume of water recycled and reused | Qnt | I2 | Education/cooperation programs or campaigns which aim to inform the local community about the value of drinking water | Qlt |

| C2 | Percentage of water recycled and reused (Potable reuse) | Qnt | Aspect J: Distribution network efficiency | ||

| C3 | Percentage of water recycled and reused (Non-potable reuse) | Qnt | J1 | Water pipe replacement rate | Qnt |

| C4 | Total volume of planned and unplanned water discharges by destination | Qnt | J2 | Volume of non-revenue real water losses | Qnt |

| Aspect D: Activity metrics | Aspect K: Network resiliency and impacts from climate change | ||||

| D1 | Number of residential customers | Qnt | K1 | Water treatment capacity located in) Special Flood Hazard Areas or foreign equivalent | Qnt |

| D2 | Number of non-residential customers | Qnt | K2 | Volume of sanitary sewer overflows (SSO), percentage recovered | Qnt |

| D3 | Volume of water delivered | Qnt | K3 | Number of service disruptions | Qnt |

| D4 | Average volume of wastewater treated per day | Qnt | K4 | Number of people affected by disruptions | Qnt |

| D5 | Length of transportation and distribution lines | Qnt | K5 | Average duration of disruption | Qnt |

| Aspect E: Energy Management | K6 | Discussion of efforts to identify and manage risks and opportunities related to the impact of climate change on the distribution network | Qlt | ||

| E1 | Total energy consumed | Qnt | |||

| E2 | Percentage of grid electricity | Qnt | |||

| E3 | Percentage of renewable energy | Qnt | |||

| E4 | Percentage of energy consumed per source | Qnt | |||

| E5 | Total CO2 emissions | Qnt | |||

| Aspect F: Effluent Quality | |||||

| F1 | Water discharges quality and the treatment method | Qnt | |||

| F2 | Number of incidents of non-compliance with water effluent quality | Qnt | |||

| Aspects | Description | Number of Indicators | Max Score | Threshold Score | |

|---|---|---|---|---|---|

| Qualitative (Scoring Scale: 0–1) | Quantitative (Scoring Scale: 0–3) | ||||

| A | Water withdrawal | 0 | 2 | 6 | 3 |

| B | Water sources significantly affected and water scarcity | 2 | 3 | 11 | 5.5 |

| C | Water recycled/reused and discharged | 0 | 4 | 12 | 6 |

| D | Activity metrics | 0 | 5 | 15 | 7.5 |

| E | Energy Management | 0 | 5 | 15 | 7.5 |

| F | Effluent Quality | 0 | 2 | 6 | 3 |

| G | Drinking Water Quality | 0 | 2 | 6 | 3 |

| H | Complaints and grievance mechanism | 1 | 3 | 10 | 5 |

| I | End-use efficiency and water protection initiatives | 1 | 1 | 4 | 2 |

| J | Distribution network efficiency | 0 | 2 | 6 | 3 |

| K | Network resiliency and impacts from climate change | 1 | 5 | 16 | 8 |

| Total Indicators | 5 | 34 | 107 | 53.5 | |

| Water Utilities’ Characteristics | Number of Water Utilities | Reports’ Characteristics | Number of Reports | ||

|---|---|---|---|---|---|

| Industry sector | Water utilities | 9 | External assurance | No | 14 |

| Multiutilities | 13 | Yes | 8 | ||

| Listing status | Non listed water utilities | 17 | Average number of pages of the examined reports | 126 | |

| Listed utilities | 5 | ||||

| Size of utilities | Small and Medium-sized Enterprises (SME) | 9 | Reports’ Year | 2015 | 3 |

| Large | 13 | 2016 | 19 | ||

| Average number of reports | 6 | ||||

| Information Quality Levels | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Level 0L | Level 1 | Level 2 | Level 3 | Level 0 | Level 1 | Level 2 | Level 3 | ||

| A1 | 6 | 3 | 2 | 11 | E5 | 5 | 0 | 4 | 13 |

| A2 | 15 | 1 | 1 | 5 | F1 | 2 | 14 | 4 | 2 |

| B1 | 8 | 0 | 13 | 1 | F2 | 17 | 4 | 0 | 1 |

| B2 | 19 | 0 | 3 | 0 | G1 | 1 | 12 | 7 | 2 |

| B3 | 19 | 2 | 1 | 0 | G2 | 12 | 1 | 6 | 3 |

| B4 | 14 | 8 | 0 | 0 | H1 | 13 | 7 | 0 | 2 |

| B5 | 20 | 2 | 0 | 0 | H2 | 14 | 6 | 0 | 2 |

| C1 | 16 | 2 | 2 | 2 | H3 | 10 | 6 | 1 | 5 |

| C2 | 22 | 0 | 0 | 0 | H4 | 8 | 14 | 0 | 0 |

| C3 | 20 | 1 | 1 | 0 | I1 | 15 | 7 | 0 | 0 |

| C4 | 16 | 3 | 2 | 1 | I2 | 9 | 13 | 0 | 0 |

| D1 | 2 | 2 | 8 | 10 | J1 | 14 | 6 | 0 | 2 |

| D2 | 11 | 4 | 3 | 4 | J2 | 4 | 8 | 2 | 8 |

| D3 | 2 | 0 | 5 | 15 | K1 | 22 | 0 | 0 | 0 |

| D4 | 2 | 19 | 0 | 1 | K2 | 21 | 0 | 0 | 1 |

| D5 | 0 | 0 | 11 | 11 | K3 | 15 | 0 | 4 | 3 |

| E1 | 3 | 0 | 7 | 12 | K4 | 20 | 1 | 0 | 1 |

| E2 | 15 | 0 | 5 | 2 | K5 | 17 | 0 | 3 | 2 |

| E3 | 16 | 0 | 4 | 2 | K6 | 15 | 7 | 0 | 0 |

| E4 | 13 | 5 | 1 | 3 | |||||

| Indicators | Average Score | Max Score | Threshold Score | Indicators | Average Score | Max Score | Threshold Score |

|---|---|---|---|---|---|---|---|

| A1 | 1.82 | 3 | F1 | 1.27 | 3 | ||

| A2 | 0.82 | 3 | F2 | 0.32 | 3 | ||

| ASPECT_A | 2.64 | 6 | 3 | ASPECT_F | 1.59 | 6 | 3 |

| B1 | 1.32 | 3 | G1 | 1.45 | 3 | ||

| B2 | 0.27 | 3 | G2 | 1.00 | 3 | ||

| B3 | 0.18 | 3 | ASPECT_G | 2.45 | 6 | 3 | |

| B4 | 0.36 | 1 | H1 | 0.59 | 3 | ||

| B5 | 0.09 | 1 | H2 | 0.55 | 3 | ||

| ASPECT_B | 2.23 | 11 | 5.5 | H3 | 1.05 | 3 | |

| C1 | 0.55 | 3 | H4 | 0.64 | 1 | ||

| C2 | 0 | 3 | ASPECT_H | 2.82 | 10 | 5 | |

| C3 | 0.14 | 3 | I1 | 0.32 | 3 | ||

| C4 | 0.45 | 3 | I2 | 0.59 | 1 | ||

| ASPECT_C | 1.14 | 12 | 6 | ASPECT_I | 0.82 | 4 | 2 |

| D1 | 2.18 | 3 | J1 | 0.55 | 3 | ||

| D2 | 1.00 | 3 | J2 | 1.64 | 3 | ||

| D3 | 2.50 | 3 | ASPECT_J | 2.18 | 6 | 3 | |

| D4 | 1.00 | 3 | K1 | 0 | 3 | ||

| D5 | 2.50 | 3 | K2 | 0.14 | 3 | ||

| ASPECT_D | 9.18 | 15 | 7.5 | K3 | 0.77 | 3 | |

| E1 | 2.27 | 3 | K4 | 0.18 | 3 | ||

| E2 | 0.73 | 3 | K5 | 0.55 | 3 | ||

| E3 | 0.64 | 3 | K6 | 0.32 | 1 | ||

| E4 | 0.73 | 3 | ASPECT_K | 1.95 | 16 | 8 | |

| E5 | 2.14 | 3 | |||||

| ASPECT_E | 6.50 | 15 | 7.5 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cantele, S.; Tsalis, T.A.; Nikolaou, I.E. A New Framework for Assessing the Sustainability Reporting Disclosure of Water Utilities. Sustainability 2018, 10, 433. https://doi.org/10.3390/su10020433

Cantele S, Tsalis TA, Nikolaou IE. A New Framework for Assessing the Sustainability Reporting Disclosure of Water Utilities. Sustainability. 2018; 10(2):433. https://doi.org/10.3390/su10020433

Chicago/Turabian StyleCantele, Silvia, Thomas A. Tsalis, and Ioannis E. Nikolaou. 2018. "A New Framework for Assessing the Sustainability Reporting Disclosure of Water Utilities" Sustainability 10, no. 2: 433. https://doi.org/10.3390/su10020433

APA StyleCantele, S., Tsalis, T. A., & Nikolaou, I. E. (2018). A New Framework for Assessing the Sustainability Reporting Disclosure of Water Utilities. Sustainability, 10(2), 433. https://doi.org/10.3390/su10020433