Abstract

We conducted interviews with 18 direct market (DM) farmers to explore the implications of the Oregon minimum wage (MW) increase for the state’s DM agricultural sector. How, if at all, will DM farms in the Willamette Valley (OR, USA) adjust their production and marketing practices in response to the MW increase? How will these adjustments affect DM farm viability, farmworkers, the environment, and the communities in which the farms are embedded? This region has a vibrant food system with many small-to-mid sized, diversified farms that sell through direct and intermediated marketing channels. The diversified production and marketing practices of these DM farmers are labor intensive and, in many respects, environmentally friendly. These practices result in relatively high costs and the farmers’ ability to respond by increasing prices is constrained by mainstream retail prices. Most growers reported that they will adjust to the MW increase by reducing their production and marketing costs with a decrease in total labor hours being an important strategy. This study, while small and exploratory, is the first in Oregon (and perhaps nationally) to collect empirical farm-level data about how DM farms will adjust to a MW increase. It sets the stage for future research.

1. Introduction

Increasing the minimum wage (MW) has been a longstanding national campaign in the United States that has gained momentum in recent years [1,2]. Oregon is among the states that have recently raised the state minimum wage through the implementation of a particularly innovative policy that incrementally increases wages over a seven-year period and varies by region: the highest rate in the Portland metro, the lowest rate in non-urban counties, and the “standard rate” in all others (see Appendix A). A large body of literature examines the impacts of MW changes on employment and nonwage adjustments in industries that are heavily reliant on low-wage workers such as fast food and hotels. Few recent studies have examined the impact of MW policies on agriculture, and none on farm-level decision making in response to MW changes.

Direct market agriculture (DM) as a sector provides multiple benefits to society, yet is financially vulnerable due to its small-scale, diverse product mix, quality requirements, and narrow profit margins. Because DM farms have a high reliance on farm and marketing labor, the MW increase may threaten the financial viability of the DM sector relative to other businesses in Oregon. Direct market farmers will be faced with managing tradeoffs across economic, environmental, and social dimensions of their operations and will have to consider labor reductions and nonwage adjustments to survive. In this study, we explore two questions: How, if at all, will direct market farms in the Willamette Valley adjust to the increase in Oregon’s minimum wage? How will these adjustments affect direct market farm viability, farmworkers, the environment, and the communities in which the farms are embedded?

To explore these two questions, first we provide background on the federal MW and the new Oregon MW law. Then, we review the DM sector in Oregon and examine how it fits within the Oregon agricultural landscape. Next, we review the business theory on “channels of adjustment”, which addresses how firms respond to MW increases [3]. Then, we present findings from our 18 Oregon farmer interviews to understand which adjustments they anticipate using to adapt to the MW increase. Finally, we explore the implications for DM farms, their employees, and their communities along economic, environmental, and social dimensions.

1.1. Minimum Wage Laws and Economic Impact

1.1.1. Minimum Wage and Agriculture

Economists have analyzed the impacts of raising the MW since it was first enacted in 1938 as a part of the New Deal Fair Standards Labor Act (FSLA). While agricultural workers were originally exempt from the MW mandate, they have been entitled to at least the federal MW since 1966 [4,5]. While 45 states have their own higher MW laws, 34 states exempt agriculture so that agricultural workers receive the lower federal MW (currently $7.25/h) [4]. Worldwide, agricultural workers earn extremely low wages, despite the hazardous nature of their occupation [6,7]. On average, U.S. farmworkers earned a family income between $20,000 and $24,999 in 2013–2014, with 30% of all farmworkers falling below the federal poverty line [8]. Agricultural workers are “a hidden underpinning of the system that brings us the food we enjoy without ever appearing on food labels” [9] (p. 8).

In 2016, the Oregon State Legislature passed Senate Bill (SB) 1532, an innovative MW increase policy that increases wages incrementally over a seven-year period beginning in July 2016, with rates that vary by region of the state. This MW increase was the first statewide policy of its kind in the U.S., which set higher wage rates in urban areas to mitigate potential rural job losses and account for higher costs of living in urban areas, with New York State following shortly thereafter [10,11]. Amendments to exempt small businesses, agricultural workers, and youth labor were proposed but not adopted.

Farmworkers and their unions supported SB 1532, testifying on farmworkers’ need for a higher wage. The president of Pineros y Campesinos Unidos del Noroeste (PCUN), an Oregon farmworkers union, cited low wages as well as their historical lack of rights at the federal level [12]. Many Oregon agricultural sector businesses opposed the MW increase due to concerns for both their own profitability and the implications for employment in the sector. For example, many farm owners stated that the increased wage would force them to cut positions, often due to increased mechanization [13,14,15]. The president of Oregon Farm Bureau (OFB) testified that the increase would compress all wages, unfairly narrowing the pay difference between experienced and inexperienced workers [16]. Although some legislators anticipated revisiting exemptions for farmworkers or other groups in future legislative sessions, SB 1532 passed without exempting any groups from the increase. Representative Shemia Fagan (District 51—Clackamas) explained that the decision came down to a “hypothetical forecast of harm that we can’t predict… and people living in actual crisis today” [14].

The increased MW creates particular challenges for the DM farm sector in Oregon. Oregon has a vibrant DM farm sector with over $114 million in annual sales from 5227 farms in 2015, representing 15% of farms and roughly 2.3% of agricultural sales in the state [17,18]. Going forward, however, the DM farms, characterized by labor-intensive production and marketing methods and limited ability to set prices, will struggle to remain financially viable.

DM growers must compete within a globalized food system that includes products from commodity-scale U.S. producers and producers in countries that have fewer worker and environmental protections [6]. The DM farms have higher costs of production than their competitors because DM growers tend to grow a highly diversified mix of fresh produce using sustainable environmental practices, largely based on their personal values rather than market forces [19]. In contrast, commodity-scale producers reduce their costs of production by using synthetic inputs and high levels of mechanization, thereby externalizing the environmental costs of production [20,21,22].

DM farmers do benefit from consumer interest in “local” foods and their willingness to pay (WTP) higher prices for both personal reasons (healthier, fresher, and better tasting food) and public reasons (support local farmers, local economies, and environmental practices) [19,23]. DM producers choose among localized direct and intermediated marketing channels based on price premiums, perceived risks, and marketing costs. They typically construct a marketing mix using multiple marketing channels combining, for example, wholesale markets with low marketing costs and low prices and farmers markets with high marketing costs and high prices [24,25]. DM farmers have indicated that although they would like to pay their workers more, they cannot because consumer willingness to pay additional price premiums is constrained by food prices in mainstream retail outlets [26,27]. Combining the higher costs of production in the DM sector with the limited ability to raise prices, Oregon DM farmers face narrow profit margins and difficult tradeoffs in deciding how to adjust to the MW increase.

If DM farm viability is threatened by the MW increase, the sector’s documented economic, social, and environmental benefits may also be in jeopardy. DM production is closely aligned with Lyson’s definition of civic agriculture, which caters to local markets selling products direct to the end consumer; is central to rural communities; focuses on quality over quantity; is more labor- and land-intensive and smaller in scale; and uses site-specific knowledge and practices [21]. DM agriculture as a sector can be considered an economic development strategy, as economic studies have demonstrated the impact of DM farms on local economies, with larger economic multipliers for DM production as compared to other agricultural production and increasing local economic activity by attracting shoppers to businesses near farmers markets [23,28,29,30,31,32]. The environmental benefits of DM production across the landscape stems from its use of diverse crops and production practices that include integrated pest management, hedgerows, cover crops, and other measures to encourage agricultural and natural biodiversity. The environmental benefits of agrobiodiversity include nutrient recycling; control of local microclimates, hydrological processes and pests; and chemical detoxification [33]. In addition, agrobiodiversity builds an adaptive capacity into our food system to address change and unanticipated natural variability [22]. In this way, smaller and more diverse farms provide positive externalities through their economic, social, and environmental benefits.

Thus, while farmworkers and other low-wage workers may benefit from policy interventions such as MW increases, the DM farm employers may face reduced profit margins and therefore struggle to make a living wage themselves. To stay economically viable, DM growers will have to adjust to the increased MW through changing production and/or marketing practices. This in turn may have an impact on the diverse public benefits provided to the communities in which they are embedded.

1.1.2. Impact of Minimum Wage Changes

While Stigler [34] asserted that economic theory implies that MW increases have adverse effects on aggregate employment, most subsequent empirical studies do not support this claim [35,36,37,38,39,40]; however, one study did find a decrease in employment among teenagers and young adults resulting from a MW increase [41]. Most of these studies focused on specific industries that employ low-wage workers, especially restaurants and hotels. In the agricultural sector, Gowers and Hatton [42] found that establishing a MW reduced poverty among farmworkers, and reduced farm employment. Moretti and Perloff [43] found that an increase in the federal MW increases the wage of hourly farmworkers, but not piece-rate workers. Both studies suggest that MW changes function differently in agriculture than other industries. However, there are no previous studies that examine the impact of MW increases specifically on the DM agriculture sector.

Previous studies [35,36,37,38,39,40] have indicated that although aggregate employment may not decrease in response to MW increases, employers do respond to labor cost increases by adopting one or more offsetting actions through recognized channels of adjustment [3]. Businesses can make two types of strategic adjustments to stay competitive in the face of a shock such as wage increases: quality enhancement or cost minimization [44,45]. Quality enhancement strategies focus on increasing product quality in some way, leading to the ability to raise prices [45]. Cost-minimization adjustments reduce overall labor costs by changing wage policies, such as reducing normal wage increases; cutting “nonwage compensation” such as free or discounted meals, on-the-job training, or paid breaks; greater use of part-timers; limiting the availability of overtime hours; increased performance standards; cross-training employees for multitasking; and getting more work from each employee [3,37,45]. Additional cost minimizing adjustments focus on other aspects of the business, such as reducing waste, water, and electricity use [3]. Several MW studies also show that direct labor cost reductions, such as reducing normal wage increases and other compensation, results in wage compression, which occurs when the wage floor increases for the least experienced workers but there are not proportional wage increases for more experienced workers. Thus, the range of salaries becomes compressed [3,46,47].

Because the ability of firms to raise prices is often limited, most firms in previous studies utilized cost minimization adjustments. While previous studies have looked at these changes for restaurants and hotels, there is little research focused on agriculture and none on DM agriculture. Because of important differences between agricultural producers and service industry firms, a decrease in labor hours in the Oregon DM sector could in fact result from a MW increase. Service industry firms and their customers are tied to the jurisdiction where the MW increase occurs. Consumers will make only small changes to their behavior in response to the MW increase in that they will still frequent fast food restaurants and stay in hotels in those locations. For these types of goods, there is little direct competition between low and high MW jurisdictions. In contrast, agricultural products grown in a higher MW jurisdiction compete with similar agricultural products transported from lower MW jurisdictions. Thus, DM farms faced with a MW increase may be limited in their ability to raise prices, forcing them to find ways to reduce their production and marketing costs in order to remain competitive.

2. Materials and Methods

We conducted 18 semi-structured interviews in 2016–2017 with DM growers in the Willamette Valley region of Oregon to assess their attitudes and adjustments to the MW increase. Purposive and snowball sampling were conducted starting from publicly available sources (e.g., farm webpages, farmers market vendor lists, and by visiting farmers markets). Farms selected for this study were diversified (i.e., more than one crop); predominantly produced vegetables, fruit, and/or nuts (some producers had a small meat and/or dairy component to their production); and, sold primarily through direct and/or intermediated marketing channels. This is a small, nonprobability sample, but the selection of participants was purposeful to provide detailed information about the responses of DM farms in the Willamette Valley to Oregon’s new MW increase. The information gathered from these participants may be relevant to similar policy changes in other regions [48].

The purposive method targeted the primary attribute of interest: diverse farm sizes [49]. Because labor costs were of primary concern in this research, the number of employees served as a proxy for the scale of operation. Ex post, we established three size categories to divide the sample into thirds for the purpose of analysis. Small farms were defined as 0–5 farmworkers (n = 7), mid-sized farms had 6–19 farmworkers (n = 5), and large farms had 20 or more farmworkers (n = 6). The number of farmworkers employed at most of the farms varied seasonally; the highest number of employees at any time during the year determined the size category.

Interviews lasted 45–60 minutes in person or over the phone focusing on how, if at all, growers plan to respond to the increased MW and what they have done in the past to stay viable. All interviews were transcribed then coded using the qualitative analysis software, Dedoose, using open, axial, and selective coding methods and were developed in a constant comparative process [49]. Magnitude coding was used in some instances to assess the strength of a viewpoint such as farmer attitudes toward the MW increase [50]. During the coding process, themes emerged to assess how, if at all, the new MW rules would change the profitability of Willamette Valley DM producers and the adjustments they would make.

3. Results: Anticipated Adjustments by Different Sizes of Direct Marketing Farms

As reported below, our respondents display diverse opinions about the MW increase in Oregon. Furthermore, it is important to recognize that this particular policy change is one of many factors that they must consider as they plan the future of their farms. Our interviews did reveal that most farms would make changes in response to the new higher MW.

Consistent with the MW adjustment literature, most respondents focused primarily on cost minimization strategies. While a few mentioned quality enhancement adjustments, most indicated they had limited or no ability to increase prices. While some of the changes may be part of a pre-existing plan, many growers noted that the increase in labor costs accelerates the pace and increases the pressure to adjust their operations. Because interviews occurred in the first several months after Oregon’s MW increase went into effect, many respondents were unsure about their impacts and the adjustments they would make. Regardless, important themes and patterns emerged.

3.1. Overview of the Sample

Table 1 presents the characteristics of the DM farms in the study, which shows that the sample had a range of years in operation and number of operators. We purposefully selected farms that grow more than one variety of vegetables, fruit, and/or nuts, and sold primarily through direct and/or intermediated marketing channels. The majority (78%) farmed under 50 acres. All producers in the study use more than one marketing channel, with 72% participating in farmers markets and 56% selling in regional wholesale markets.

Table 1.

Attributes of Direct Market Farms in Study.

Responses to some questions were provided in ranges because their values vary throughout the season. Some respondents provided their best guesses for certain questions, such as Hired Labor, Acreage, and Labor as a Percentage of Costs, while others furnished an exact number based on records for the prior year. Labor costs as used in this study do not include any charges for own labor/management, nor labor from family members, interns, volunteers, or other unpaid sources. When responses were given in ranges, the highest value was used to represent costs at the “height” of the season. Labor was the largest expense category for all farms, except for the two producers who do not have any employees for part of the year. In those cases, seeds and land were their most significant costs.

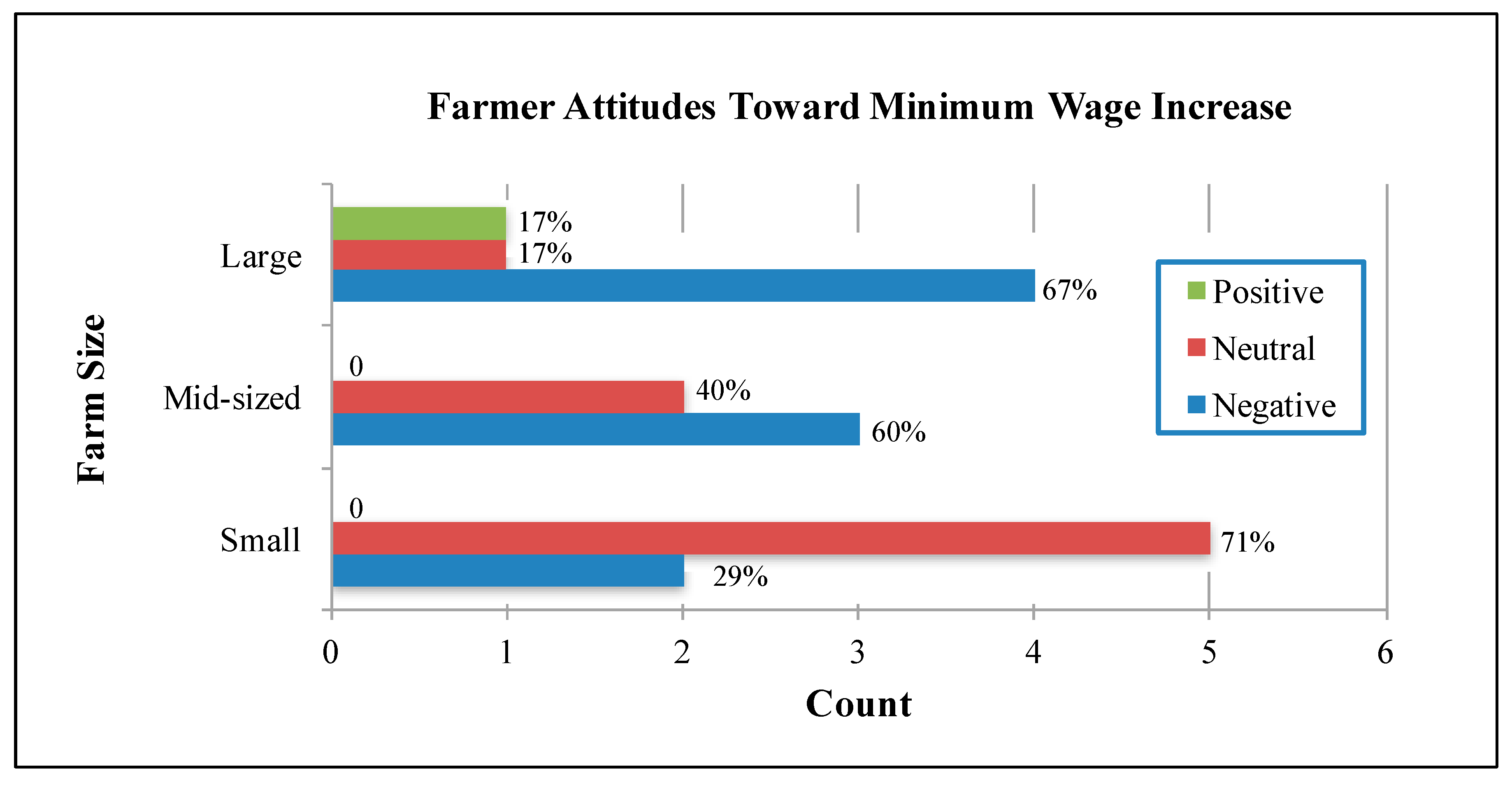

Attitudes toward the MW increase (Figure 1) varied considerably and some farmers expressed a mixed view of the wage increase even within a single interview (these responses were coded as neutral). Overall, neutral (n = 8) and negative (n = 9) were equally common attitudes expressed toward the MW increase across all farm sizes. Because this is a small sample, differences among subgroupings should be interpreted with caution. Figure 1 displays a trend related to farm size: 67% of large farms (i.e., ≥20 employees) and 60% of mid-sized farms (i.e., 6–19 employees) voiced negative attitudes toward the MW increase while 71% of the small farms (i.e., 0–5 employees) had neutral feelings toward the MW increase. Neutral opinions include this statement from Farmer #18, a small-scale producer: “I’m not too worried about [the minimum wage increase] and knowing that it’s going to go up over time, that’s kind of one of our goals for the farm anyway”. Interview responses such as “I don’t really care” or “I’m not really sure how I feel about it” were also coded as neutral responses. Farmer #15, a large-scale producer (i.e., ≥20 employees), was the only respondent to express a strictly positive attitude toward the increase, stating: “I don’t think anybody on the farm makes as much money as they should so I don’t have any problem with paying people more money”.

Figure 1.

Chart Illustrating Minimum Wage Attitude by Farm Size. Notes: The attitudes towards the minimum wage reflect an overall sentiment towards the policy change, despite some variation in attitude within single interview. The attitude categories coded for were: positive, neutral, and negative (N = 18). Farm sizes are Large (≥20 hired laborers), Mid-sized (6–19 hired laborers), and Small (0–5 hired laborers). Percentages total more than 100% in some categories due to rounding.

While the variation in attitudes does not provide much insight into the impact of the MW increase, it highlights the diversity of opinions among farms as they weigh the tradeoffs that they face. Significantly, even those with neutral attitudes toward the policy discussed adjustments they felt they had to make to their farming operation to offset the increased labor costs.

3.2. Cost-Minimization Adjustments in Response to the Minimum Wage Increase

While scholars have not found a negative impact on employment from MW increases in the restaurant industry (although they did find non-wage adjustments) [37,38], findings in this study point to decreases in labor hours in the Oregon DM sector. Specifically, seven out of the eighteen producers indicated that they have or will be reducing employment in the coming years. We attribute this difference in employer response to a structural difference between service industries that compete with other service providers in the same MW jurisdiction and farmers who must compete with products that can be shipped from lower MW jurisdictions.

To reduce labor costs, farms can decrease the total number of employees and/or labor hours throughout the year through various strategies: (1) changing labor procurement or compensation policies; (2) controlling production costs through increasing efficiency and on-farm labor management; or (3) changing marketing channels.

3.2.1. Changing Labor Procurement or Compensation Policies

Labor costs can be most directly controlled through labor procurement and compensation policies, including reducing the total amount of labor employed. One approach to reducing hired labor costs would be to substitute increased family labor; however, only one of the eighteen farms anticipated this specific adjustment. Many farms were looking for other ways to cut back on labor costs. Farmer #12, a farmer in the mid-sized category, stated this approach very clearly: “I think next year we’re going to hire less people, we’re going to try and squeeze as much profitability out of everything that we possibly can”.

Several DM farmers plan to employ more contract laborers as a cost minimization strategy. Contract labor refers to the temporary hiring of a crew, usually at a higher rate than a permanent crewmember because the farmer is also paying the contractor who supplies the laborers. Farmer #17, who operates a large-scale farm, explained the financial logic behind this decision:

[The laborers] might be receiving minimum wage, but I’ll be paying typically twice whatever the minimum is. I might be paying the company $20 per hour and the people might only be getting $10 per hour, but that sounds like, well why would I do that? And it’s because I pay them for a couple days and then they’re gone and I don’t have to pay the insurance, I don’t have to worry about an accident, and I can get what I need and not have to hire somebody for a long-term [position].

While hiring contract laborers can provide savings, growers recognize the full range of implications. Farmer #14 (a small-scale producer) noted that because of her plan to increase the use of contract laborers, “there goes a permanent position for someone [else]”!

Half of all DM producers in this study stated that they started employees above the current minimum wage, as a symbolic gesture that they felt was important. For example, Farmer #1a, a small-scale producer, stated that they started new employees at $10 per hour (current MW wage was $9.75) because “it was more than minimum wage and I’ve always wanted to show through how much we pay someone that we’re committed to them”. Many other growers echoed this sentiment; interestingly, only one of the nine producers making this comment was a mid-sized farmer.

Farmers in general expressed a desire to pay workers fairly, but felt constrained by their own financial circumstances. In other words, as Farmer #12 also described: “I want to be providing a more sustainable living wage for the people who work for me… the truth is right now we are having trouble just staying barely above the minimum wage”. About half of the DM producers interviewed mentioned this tradeoff between the number of employees and the hourly wages paid. Because many of the producers seek to pay higher wages, they have concluded that they will hire fewer people going forward.

Changing compensation policies will likely result in wage compression, as the literature and testimony at the hearings on the legislation suggested. Respondents specifically referred to wage compression multiple times throughout the interviews; six DM farmers discussed moving away from hiring unskilled youth laborers. As Farmer #7 stated, “we hired a lot of kids out of school for the summer [in the past], but as far as value…the output from most of them just does not compute”. Further, Farmer #9 added to this sentiment by stating, “It’s silly for someone out of high school to … make $15/h and someone else that’s been farming for 2–3 years, to pay them $15/h”. Here, Farmer #9 discusses a common theme voiced by those interviewed: with the compression effect of the MW increase, there is a decreased incentive to hire less-experienced, high school aged workers. As Farmer #14 put it, when asked how the MW increase will affect her business: “I’m never gonna hire a high schooler. I mean why would you hire a high schooler for that wage?” This general approach of reducing the hiring of unskilled youth laborers in response to a MW increase is consistent with the results reported by Neumark and Wascher [41]. Overall, only one grower interviewed expressed a desire to hire more high school aged workers as an anticipated adjustment. However, this grower also expressed a particular difficulty in hiring enough employees because he produced a very specific set of crops that did not require hired help until July—by this point in the season most farmworkers seeking employment have already secured positions.

DM producers interviewed also spoke about experience in farm work as an integral trait that they wished they could better compensate. Stated differently, they presented experienced workers as more deserving of the benefits distributed by the MW increase than other subpopulations that may benefit, particularly youth laborers. While producers of all scales discussed this idea, mid-sized farmers mentioned this slightly more than small- or large-scale producers did. For example, Farmer #3a, a mid-sized DM producer, explained a situation in which they tried to determine a starting wage for an experienced farmworker who had particularly valuable additional skills such as welding or mechanics training:

We know that… if [a skilled laborer] is doing agricultural work they’re coming into one of the lowest compensated fields professionally and so if we can accommodate a need that they might have in order to keep them at our place of work because we value them then we try to do that to the best of our abilities.

Farmers #3a and #3b stated that they were willing to go to great lengths to accommodate the needs of particularly skilled and/or experienced workers. Virtually all producers stated that part of the equation for determining the starting wage of new hires is their prior farm work experience. Farmer #18, who operates a small-scale farm, stated: “we are not looking for grunt labor, we are looking for skilled farmers… it requires skill to do farming in a way that makes it pay”. Many producers brought up this notion of wanting the occupation of “farmworker” to be a viable career for people in a long-term sense, not just a summer job—both because they believe that it should be a viable career path, but also because having experienced laborers, even though they earn higher wages, is an important goal. Farmer #5, a large-scale producer, stated:

What we do is we want everybody who works for us to make at least something more than minimum wage so that if we hire a new person they generally start at some small amount above minimum wage and then we also want everybody that works for us to make more every year than they made the year before because every year they have more experience and therefore are more valuable to us…

However, as Farmer #12, a mid-sized producer, stated, having the funds to achieve this has been a huge barrier to retaining skilled labor:

It would be nice to have more experienced people on the farm, but I think we’re sort of caught. I mean we can’t afford to have more highly skilled labor on the farm so we end up with more entry level people… and more turnover, which is ultimately less efficient even though it looks like it costs less in the short term.

Finally, it is important to note that a large majority of producers, especially those that are more distant from the city centers in the Willamette Valley (i.e., Corvallis, Eugene, Portland, and Salem) reported that they face a significant labor shortage. Many of the DM growers interviewed wanted to pay experienced workers more, but simply do not have enough experienced workers applying for their open positions. Thus, while some growers wished to move away from unskilled youth labor, the labor shortage serves as a barrier to doing so for many interviewees.

3.2.2. Controlling Production Costs

With the increased per-unit labor costs resulting from the minimum wage increase, many DM producers are also seeking to reduce the number of labor hours paid. The specific adjustments mentioned to achieve this goal include increasing mechanization, reducing both crop and varietal diversity, and/or changing infrastructure for harvest efficiency.

As shown in Table 2, six farms of all scales anticipate increasing mechanization, with mid-sized farmers expressing this slightly more often. When asked how to reduce production costs, Farmer #2b, a mid-sized producer, stated: “One is mechanization and I think we’ve done a lot, but there’s probably a lot more that we could do. And there’s a lot of pressure to mechanize now with the minimum wage going up so dramatically”.

Table 2.

Stated Production Adjustments.

In a similar vein, when asked what the MW increase means to her farm, Farmer #12, a mid-size producer, indicated that many of the cost-reducing options to compensate for the increased wage conflict with her environmental values:

…you know it probably means spending less money on cover crops, it probably means getting more mechanized and… using a tractor more instead of people, which is fossil fuels and I’m a huge believer in people being connected to the land and working on farms, but I feel like the market is pushing me to mechanize and have fewer people actually working for me.

Reducing the complexity of their farms was another frequent theme. DM farms tend to be highly diversified in order to sell at farmers markets or other outlets, but diversity is also costly because it reduces the producer’s ability to achieve economies of scale. Some reported producing over 50 different crops and crop varieties, for both economic and environmental benefits. Farmer #16, a large-scale producer (i.e., ≥20 employees), started his operation growing only a few different crops, but decided to switch to a highly-diversified model because “instead of just harvesting the traditional 3 to 4 months a year, we’re basically harvesting something almost 12 months a year and that way we keep a small harvest crew and keep busy”. For him and Farmer #8, diversification allowed them to keep a small crew employed all year, which minimizes employee turnover and enables a year-round stream of revenue.

Because diversified production systems can provide environmental benefits and reduce financial risks, numerous respondents indicated that reducing diversity is a difficult decision to make. Nonetheless, many growers specified this as a strategy they would follow. Farmer #12, as an example, provided this discussion of her thought process as she decided to reduce the number of crops she grows the following season:

I’ve done some enterprise budgets and I have a better idea of what’s profitable for us and what’s not… And that should increase profitability significantly to know that information, but it may also decrease the varieties that we are able to grow or the diversity that we’re able to grow, you know, so how do you balance that stuff? Like if some crop that’s important to the rotation is bad for the bottom-line, how do you decide? ...and nobody’s paying for the environmental consequences, obviously, or we wouldn’t be having this problem on the planet that we’re having.

Similarly, Farmer #9 stated that she would be scaling back on tomato varieties because, although they are popular with consumers, they are labor intensive to produce.

Farmers #3a and #3b discussed the specific challenges related to the CSA box model in which many crops are produced and some overproduction results

Farmer #3b: …your revenue on overproduction … is zero. [T]he CSA tends to kind of harbor inefficient techniques it seems like. That’s like what I’m realizing over and over is that it tends to push one, or at least us, to kind of overproduce for insurance.

Farmer #3a: It’s so nerve-wracking to think you don’t have enough … So we’ve always tended to err on the side of overproduction and I think it’s a choice that has lost a lot of money over the years.

Farmers #3a and #3b explained that with the MW increase they felt a lot of pressure to alter their production costs by reducing diversity. However, they also explained that deciding how much diversity to reduce, with the intent of avoiding overproduction, was particularly difficult with the CSA model because members expect a wide assortment of produce in their CSA farm share.

Farmer #12 perfectly summed up the types of tradeoffs the MW increase has caused: “how do you hold on to… trying to be sustainable ecologically and trying to grow healthy food… if you have these other values then how do you hold onto those things and pay people better?”

Modifying infrastructure to increase efficiency was another major adjustment mentioned by growers. The specific modifications varied considerably, including changes to the layouts of packing or washing stations, adding additional coolers, or building new structures. While farmers frequently alter their production and marketing methods in search of greater efficiency, many growers specifically stated that the MW increase would accelerate the rate of change.

3.2.3. Changing Marketing Channels

Changing the farm’s mix of marketing channels was another adjustment discussed by respondents, with three of the large farms considering a decrease in the amount they sell through a regional wholesale distributor. One farmer in the small farm category also discussed reducing sales through the wholesale marketing channel, but had already significantly reduced those sales prior to the MW increase. Farmer #5, who owns and operates a large farm, explained that one of the wholesale distributors he uses surveyed their growers prior to the MW increase before taking a stance on the policy:

[The wholesale distributor] interviewed a bunch of their other farmers and they decided not to support the minimum wage increase and I think it’s because they heard from many of their growers that it was likely that they would have to reduce the amount of crops they could produce for wholesale distribution.

As Farmer #5 explained, the farmer’s profit margins from wholesale sales are smaller because the prices they receive in that channel are lower than in direct to consumer channels. In the wholesale supply chain, labor must be paid in multiples places: the farm, the distribution network, and the grocery store or food service.

In contrast, several DM farmers indicated that they had recently or were considering reducing the farmers market component of their marketing. Farmers market sales can provide lower net returns due to labor and marketing costs and also have variable sales volumes [24]. Farmer #9, who operates a small farm and is not currently selling through a farmers market explained that they had tried a couple years prior to the MW increase, but their attempt only lasted about a month because “it was just way too much work and it was a really new market and that was way way losing money [for us]”. Farmers #3a and #3b also noted that there is a fair bit of waste at the farmers market in order to keep your booth looking full and abundant, which draws consumers. Farmers #3a, #3b and #9 all referred to their observed decline in the CSA model as well, with difficulties in CSA member retention and overproduction to fulfill the desired product diversity. In sum, carefully examining net returns and then reducing marketing channels used was a common strategy adopted by DM growers of all sizes, with the specific strategic responses varying.

3.3. Increasing Revenue: Quality Enhancement and Raising Prices

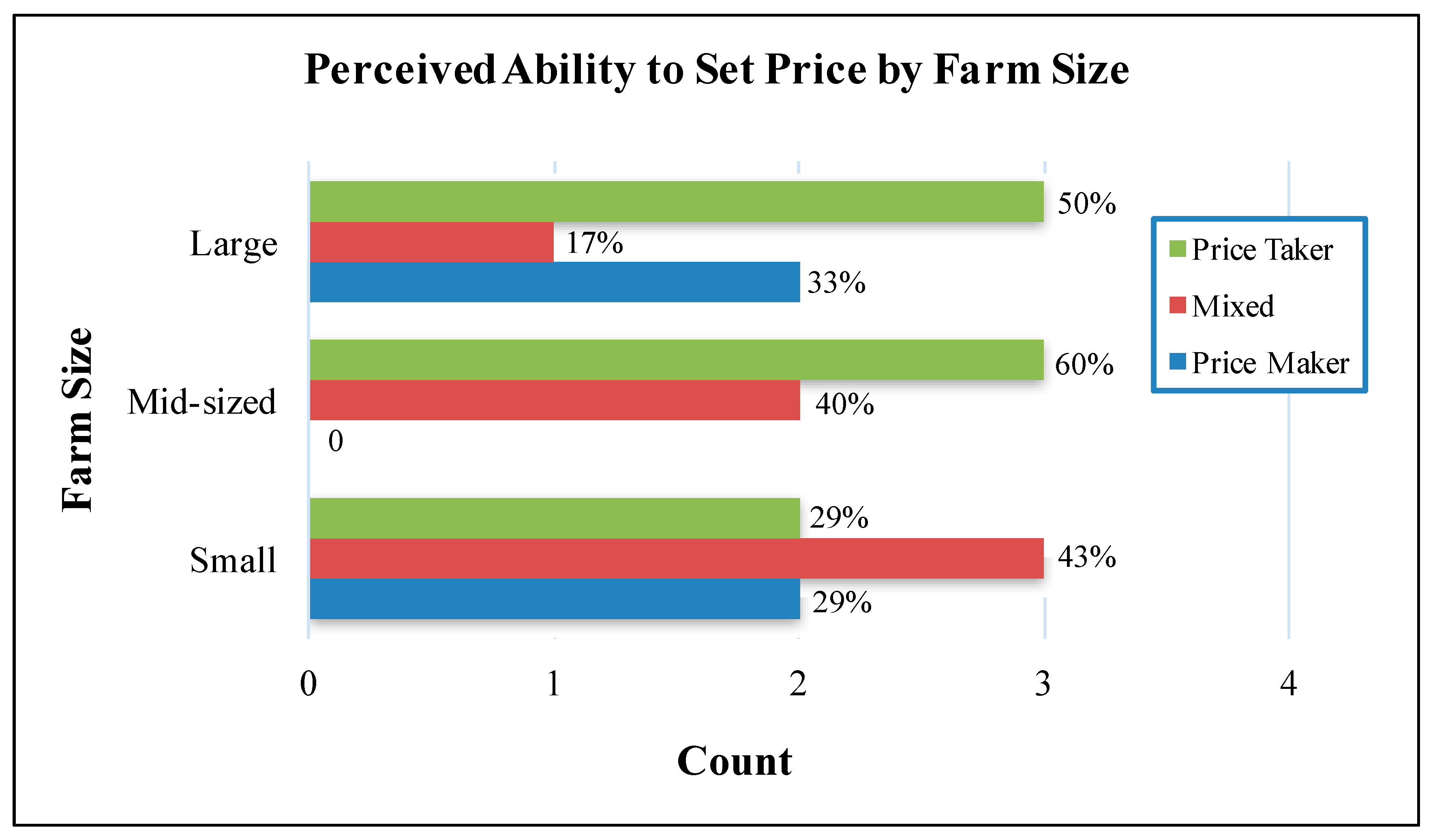

The MW increase would not be a problem for DM farmers if they could fully pass the increased labor cost on to the buyer by raising the price of their goods. Figure 2 presents the degree to which DM producers felt they could set their own prices. Eight of the eighteen DM producers classified themselves as price takers and therefore would be unable to raise prices to cover the increased labor costs. Six producers believed they had some ability to raise prices in order to pass on cost increases while only four of the eighteen viewed themselves as price makers.

Figure 2.

Chart Displaying Perception of Price Taker vs. Price Maker by Farm Size. Notes: This chart displays the absence or presence of each of the Price Taker and Price Maker codes, producers who expressed both are in the Mixed category (N = 18). Farm sizes are Large (≥20 hired laborers), Mid-sized (6–19 hired laborers), and Small (0–5 hired laborers). Percentages total more than 100% in some categories due to rounding.

Farmer #8 is an example of a price taker:

[I’ve been] thinking a lot about how we can pass on increased costs, if we can raise our prices. We’re at the mercy [of others] in the wholesale market, but the retail at the farmers markets, that’s our own decision, if we’re gonna go up or not, but since the big recession in 2008, I don’t think we’ve raised any prices and we’ve actually seen some prices go down so it seems long overdue that we do raise some prices but I don’t know what customers are gonna be willing to pay.

Thus, even though Farmer #8 wanted to respond to the increased MW by raising prices, he did not feel as though that was a realistic option—primarily because of his own prior history as a price taker.

The price taker DM producers felt that they could not set prices due to the competition with other growers and grocery stores. Farmer #9, a small-scale producer, similarly identified consumer WTP as a significant barrier that reduces the farm’s financial viability and her ability to pay the increased labor costs from the MW increase:

We are a nation that prides ourselves on cheap food and we want food to be cheap and the only way you have cheap food is if someone gets screwed along the way, if someone does not make a living, and so it’s either the poor farmworkers or the poor farm owners.

As noted above, some farmers stated both price-taking and price-making abilities at some point during the interview. For example, Farmers #2a and #2b, a mid-sized operation, explained that they do enterprise budgeting to know exactly what they need to charge and have, at most times, been able to charge that price. However, Farmer #2b explained that this ability varies depending on other growers at the farmers market:

A long time ago we grew snow peas and we couldn’t get as good prices as we wanted to because other growers were selling them for less and I talked to those other growers, it was a couple of growers and one of them said, “well, I just grow them because it keeps my crew busy at that time of year when I need some work for them so I don’t really care how much they sell for”. And another grower said, “well we just grow [peas] largely for the pea greens and so the pods themselves are kind of just cream, something extra that we get the out of the plants”. So neither one of them was interested in raising their price to what we needed so we just stopped growing it.

Most of the DM producers who indicated price-making ability also stated that their farm and/or products were highly differentiated, which is a quality enhancement approach. Farmer #13 stated: “I’m always the most expensive [at the farmers markets]… we will have the most expensive peaches, cherries, apples, hazelnuts, but we focus on absolute high quality and certified organic and it works, I mean people love us”. This quality enhancement strategy has provided financial viability for his farm. Farmer #18 also expressed the possibility of raising her prices when needed: “we’re such a niche, we really are, being biodynamic, so we’re basically bringing food to market that is basically of the quality and type I would say of [two larger farms in the area] but we’re smaller and so the farmer is at the market”.

A final point on revenue enhancement is that DM producers are already in a market that demands high quality standards and seeking to improve quality to a higher level will be costly. Becoming certified organic, for example, may be result in higher market prices, but would also require greater production and recordkeeping costs and additional fees.

4. Discussion: Impacts of the Minimum Wage Increase

Oregon DM farms will respond to the state’s MW increase with a variety of adjustments to how they produce and market products. The interviews revealed some significant differences by size of operation, which is important because a vibrant DM sector that sells products through a range of marketing channels is composed of a mix of small to large producers that can satisfy diverse consumer demands [19]. The mid-sized producers who reported the greatest pressure from the MW increase perceive themselves as having little pricing power, and anticipate making more modifications to their operations than producers in the other size categories. Large-scale (i.e., ≥20 employees) also exhibited an overall negative attitude towards the MW increase and plan to make some of the same adjustments as small- and mid-sized operations. Small farms perceived a greater ability to set prices and were more likely to express a neutral attitude toward the MW increase; small producers noted that they often start new employees above the current MW.

Oregon DM producers interviewed for this study recognize that their decisions when adjusting to the MW increase represent difficult tradeoffs for their own farms, their employees and their communities across economic, environmental and social dimensions. They discussed these tradeoffs in terms of their own values while recognizing that their farms contribute to broader community outcomes. The DM producers were equally split between opposing the state’s minimum wage increase and a neutral attitude. As shown in Table 3, producer attitude and ability to set prices are linked, as producers who perceive themselves as price takers are much more likely to oppose the MW increase—75% of self-identified price takers had a negative attitude toward the MW increase (6 out of 8). Of producers with some ability to increase their prices (price makers or mixed), 70% had a positive or neutral attitude toward the MW increase (7 out of 10). Thus, the farmers’ perceived ability to raise their prices as a channel of adjustment is linked to their overall attitude about the MW increase.

Table 3.

Matrix of Producers’ Overall Attitude toward the MW Increase and their Perceived Ability to Set Price.

In addition, several producers of varying sizes discussed relying more on contract labor, which may result in fewer permanent farmworker positions on those operations. The choice to use more contract labor may depend more on cropping systems and timing than on farm size. The impact of such a change depends on how many farmers make this choice and how many farmworkers are affected. The aggregate impact on farmworkers and communities is ambiguous; it depends on the working conditions and wages on those individual farms compared to the contract labor crews. However, the farmers we interviewed recognized the social and economic value of providing stable employment on their farms for their employees and for their communities.

Another key finding in this paper is the significant concern with wage compression resulting from the MW increase. The farmers’ anticipated adjustments were motivated both by the goal of reducing overall labor hours and the desire to maintain the relatively higher wages of their most experience workers. Small farmers seemed particularly outspoken about not hiring high schoolers, which aligns with the desire of these farmers to start workers at higher than minimum wage. However, only one of the nine producers who discussed starting new workers above the current minimum wage was a mid-sized farmer. As noted above, mid-sized farmers seem to perceive great pressure from the increasing MW because they regard themselves as price takers. Thus, while small-scale producers expressed a higher ability to set their prices to adjust to the MW increase, mid-scale producers feel that they are price takers in the broad marketplace for food, competing with large-scale producers who have lower costs per unit of production due to economies of scale.

Mechanization and altering existing infrastructure were prominent cost-minimization and labor-reducing adjustments planned by mid-sized producers. While mid-sized growers have higher labor costs than small-scale producers, they do not have some of the cost minimization strategies in place that the larger growers already have (e.g., higher levels of mechanization and efficient building layouts such as a packing shed or washing station). Because they do not see an opportunity to raise their prices, they are seeking to minimize their labor costs through achieving some of the mechanization strategies that larger-scale producers already have in place. Indeed, mechanization was not frequently mentioned by large-scale DM producers who were already at or near the mechanization maximum on their farm. As one large-scale producer, Farmer #5, explained: “we’re not processed food growers, it’s all fresh market and almost all fresh market produce whether it’s on big farms or little farms or organic or not, almost all fresh market produce has to be hand harvested”.

Both small and mid-sized farms discussed their plans to reduce the range of crops and crop varieties produced, and noted the need to move toward favoring economic viability at the expense of environmental concerns. In another recent Oregon producer survey, the farmers who indicated that they used various environmentally-sensitive production practices were also much more likely to indicate that they chose their production practices because they “align” with their environmental values [19].

The diversity of crops grown by a farm is also related to the marketing channels chosen. A mix of marketing channels can be optimized for each farm depending on their product mix, available channels and prices, hired and owner/family labor, and risk and lifestyle preferences [24]. The added labor costs resulting from the MW increase may force producers to re-evaluate their profitability in each channel. The MW increase may reduce the attractiveness of market options with high labor costs for production and marketing because the farms, in many instances, cannot pass on the higher labor costs in their prices. Some large farms indicated they would reduce their sales through wholesale channels in order to capture a larger portion of the consumer dollar, while small or mid-scale farmers indicated they would pullback from some direct marketing channels in order to reduce both the high labor requirements for marketing and a high level of production diversity. While a change in marketing channels may occur, it is difficult to predict the impacts on farms themselves, and on the communities that access foods through direct marketing channels.

Revenue-related adjustments are limited because most farmers perceive themselves as price takers, limited by consumers WTP as they compete with both grocery stores and even more directly with other vendors at farmers markets and other direct marketing channels. The majority of producers anticipated keeping prices relatively stable, thus increasing the need to seek alternate adjustments to reduce their labor costs. Producers who are able to increase their prices or invest further in quality enhancement such as certifications to further differentiate their products were much less likely to see the MW increase as a threat to their viability.

Farm size is just one variable relevant to the adjustments that farms will make in response to the increase in the MW. Other characteristics such as marketing channels, certifications, crops grown, and years in operation, to name a few, are related to the impact of the MW increase and more research could be done to better understand their influence. In addition, agricultural businesses change constantly to respond to regulatory and market conditions, which makes it difficult to attribute any changes directly to the MW increase.

This study, while small and exploratory, is the first in Oregon (and perhaps nationally) to collect empirical farm-level data about how farms will adjust to the minimum wage. It sets the stage for future research. For example, producers in the Oregon standard wage tier could be compared with those in the Portland Metro and non-urban wage tiers. Additionally, this study could be used as a point of comparison for an analysis three years from now, when the policy is in its mid-term, to identify the changes that were actually implemented over the MW increase period. Because the goal of increasing the MW is to provide financial benefits to low-wage workers, future studies could interview farmworkers to see if this policy was effective in meeting that goal.

5. Conclusions

The MW increase in Oregon affects all businesses, including Oregon’s DM farms. Already struggling with slim profit margins, the adjustments they adopt to cope with higher labor costs will have impacts on the economic and environmental performance of their farms and will have significant social implications for their workers and their communities.

While Card and Krueger [37,38] and subsequent scholars [35,36,39,40] noted that there is not a negative impact on employment from MW increases in the restaurant industry, findings in this study point to decreases in employment in the DM agriculture sector. Similar to previous findings regarding the agricultural sector [42,43], this is likely due to significant differences between restaurants and agriculture: agricultural goods from geographically separate locations are substitutes to a much greater extent than restaurants over similar distances. While we cannot estimate the overall impact on DM employment due to the small sample size and the fact that this study is prospective, seven out of the 18 producers did indicate that they have already or will be reducing labor hours in the coming years. However, while total labor hours on DM farms may decrease, it is important to remember there may not be a net negative impact for farmworkers, as some will receive higher wages.

Some of the major adjustments that lead to a decrease in farm labor hours include increased mechanization, decreased agrobiodiversity, increased use of contract labor, and changes in marketing channels used. In addition, farms anticipate wage compression for the experienced employees. Most DM farmers do not expect to raise prices to cover higher labor costs: many DM producers indicated they are price takers, and others felt that their limited price-making ability was constrained by market prices.

All of these adjustments have impacts for the communities served by DM farms. With researchers such as Dahlberg [22] and Lyson [21] pointing out that direct market, diversified operations are better for the environment and improve the resiliency and adaptability of our food system, there are important repercussions of altering DM production methods to consider. Changing marketing channels, particularly changes away from direct sales or farmers markets, severs the bonds created by “civic agriculture” in the community. Increased prices for DM foods may dampen demand for DM products or put them out of reach for some community members. Employment and wage changes have implications for farmworkers, their families, and the broader employment and income levels within the community.

Acknowledgments

This study was funded by the U.S. Department of Agriculture under National Institute for Food and Agriculture grant 2014-68006-21854. The authors thank two anonymous reviewers’ comments that greatly improved the manuscript.

Author Contributions

Lindsay Trant, Larry Lev, Lauren Gwin, and Christy Anderson Brekken conceived and designed the interviews; Lindsay Trant performed the experiments; Lindsay Trant, Larry Lev, Lauren Gwin, and Christy Anderson Brekken analyzed the data; and Lindsay Trant, Larry Lev, Lauren Gwin, and Christy Anderson Brekken wrote the paper.

Conflicts of Interest

The authors declare no conflict of interest. The founding sponsors had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, and in the decision to publish the results.

Appendix A

Table A1.

Wage Tiers Set by Senate Bill 1532.

Table A1.

Wage Tiers Set by Senate Bill 1532.

| Standard | Portland Metro | Nonurban Counties | |

|---|---|---|---|

| July 2016–June 2017 | $9.75 | $9.75 | $9.50 |

| July 2017–June 2018 | $10.25 | $11.25 | $10.00 |

| July 2018–June 2019 | $10.75 | $12.00 | $10.50 |

| July 2019–June 2020 | $11.25 | $12.50 | $11.00 |

| July 2020–June 2021 | $12.00 | $13.25 | $11.50 |

| July 2021–June 2022 | $12.75 | $14.00 | $12.00 |

| July 2022–June 2023 | $13.50 | $14.75 | $12.50 |

| July 2023 and after | CPI adjusted | +$1.25 | −$1.00 |

Source: Oregon Bureau of Labor and Industries [51].

References

- Rifai, R. US Sees Largest Protests Calling for $15 Minimum Wage. Al, Jazeera. 29 November 2016. Available online: http://www.aljazeera.com/news/2016/11/sees-largest-protests-calling-15-minimum-wage-161129164539058.html (accessed on 13 December 2017).

- Smith, A. Dozens of Protesters Arrested in Fight for $15 Demonstrations. CNN Money, 29 November 2016. Available online: http://money.cnn.com/2016/11/29/news/minimum-wage-protest-arrests/ (accessed on 13 December 2017).

- Hirsch, B.T.; Kaufman, B.E.; Zelenska, T. Minimum wage channels of adjustment. Ind. Relat. 2015, 54, 199–239. [Google Scholar] [CrossRef]

- Rodman, S.O.; Berry, C.L.; Clayton, M.L.; Frattaroli, S.; Neff, R.A.; Rutkow, L. Agricultural exceptionalism at the state level: Characterization of wage and hour laws for US farmworkers. J. Agric. Food Syst. Community Dev. 2016, 6, 89–110. [Google Scholar] [CrossRef]

- Schell, G. Introduction. In The Human Cost of Food: Farmworkers’ Lives, Labor, and Advocacy; Thompson, C.D., Jr., Wiggins, M.F., Eds.; University of Texas Press: Austin, TX, USA, 2002; pp. 2–19. ISBN 0-292-78177. [Google Scholar]

- Oxfam America. Like Machines in the Fields: Workers without Rights in American Agriculture. 2004. Available online: https://www.oxfamamerica.org/static/media/files/like-machines-in-the-fields.pdf (accessed on 13 December 2017).

- Villarejo, D.; McCurdy, S.A.; Bade, B.; Samuels, S.; Lighthall, D.; Williams, D., III. The Health of California’s Immigrant Hired Farmworkers. Am. J. Ind. Med. 2010, 53, 387–397. [Google Scholar] [CrossRef] [PubMed]

- Hernandez, T.; Gabbard, S.; Carroll, D. Findings from the National Agricultural Workers Survey (NAWS) 2013-2014: A Demographic and Employment Profile of United States Farm Workers; Research Report No. 12; United States Department of Labor: Washington, DC, USA, 2016. Available online: https://www.doleta.gov/agworker/pdf/NAWS_Research_Report_12_Final_508_Compliant.pdf (accessed on 13 December 2017).

- Thompson, C.D., Jr. Farmworker Exceptionalism under the Law: How the Legal System Contributes to Farmworker Poverty and Powerlessness. In The Human Cost of Food: Farmworkers’ Lives, Labor, and Advocacy; Thompson, C.D., Jr., Wiggins, M.F., Eds.; University of Texas Press: Austin, TX, USA, 2002; pp. 139–168. ISBN 0-292-78177. [Google Scholar]

- Lam, B. Oregon’s Smart Approach to a Minimum Wage. The Atlantic, 23 February 2016. Available online: https://www.theatlantic.com/business/archive/2016/02/oregon-minimum-wage/470460/ (accessed on 13 December 2017).

- Kirkpatrick, J.; Chico, S. The Minimum Wage in 2017: A Coast-to-Coast Compliance Challenge. Insight: In-Depth Discussion. Littler Mendelson, P.C. 18 November 2016. Available online: https://www.littler.com/files/2016_11_insight_the_minimum_wage_in_2017_-_a_coast-to-coast_compliance_challenge.pdf (accessed on 24 January 2018).

- Ramirez, R. Testimony to House Committee on Business and Labor, 15 February 2016, 5:30 PM. 78th Oregon Legislative Assembly. Available online: https://olis.leg.state.or.us/liz/2016R1/Downloads/CommitteeMeetingDocument/89785 (accessed on 13 December 2017).

- Oregon State Legislature. House Committee on Business and Labor, Agenda and Meeting Materials, 15 February 2016, 8:30 AM, 78th Oregon Legislative Assembly. Available online: https://olis.leg.state.or.us/liz/2016R1/Committees/HBL/2016-02-15-08-30/Agenda (accessed on 13 December 2017).

- Oregon State Legislature. House Committee on Business and Labor, Agenda and Meeting Materials, 15 February 2016, 5:30 PM, 78th Oregon Legislative Assembly. Available online: https://olis.leg.state.or.us/liz/2016R1/Committees/HBL/2016-02-15-17-30/Agenda (accessed on 13 December 2017).

- Oregon State Legislature. Senate Committee on Workforce and General Government, 4 February 2016, 1:00 PM, 78th Oregon Legislative Assembly. Available online: https://olis.leg.state.or.us/liz/2016R1/Committees/SWGG/2016-02-04-13-00/Agenda (accessed on 13 December 2017).

- Bushue, B. Testimony to House Committee on Business and Labor, 15 February 2016, 5:30 PM. 78th Oregon Legislative Assembly. Available online: https://olis.leg.state.or.us/liz/2016R1/Downloads/CommitteeMeetingDocument/87692 (accessed on 13 December 2017).

- Ellis, S. Survey: 167,000 U.S. Farms Sold Food Local in 2015; Capital Press: Salem, OR, USA, 2016; Available online: http://www.capitalpress.com/Business/20161223/survey-167000-us-farms-sold-food-locally-in-2015 (accessed on 13 December 2017).

- US Department of Agriculture National Agricultural Statistics Service. 2016 State Agricultural Overview: Oregon. Available online: https://www.nass.usda.gov/Quick_Stats/Ag_Overview/stateOverview.php?state=OREGON (accessed on 13 December 2017).

- Brekken, C.A.; Parks, M.; Lundgren, M. Oregon producer and consumer engagement in regional food network: Motivations and future opportunities. J. Agric. Food Syst. Community Dev. 2017, 7, 79–103. [Google Scholar] [CrossRef]

- Conner, D.S. Expressing values in agricultural markets: An economic policy perspective. Agric. Hum. Values 2004, 21, 27–35. [Google Scholar] [CrossRef]

- Lyson, T.A. Civic Agriculture: Reconnecting Farm, Food, and Community; Tufts University Press: Medford, MA, USA, 2004; ISBN-13: 978-1-58465-414-8. [Google Scholar]

- Dahlberg, K.A. Pursuing long-term food and agricultural security in the United States: Decentralization, diversification, and reduction of resource intensity. In Food and the Mid-Level Farm; Lyson, T.A., Stevenson, G.W., Welsh, R., Eds.; The MIT Press: Cambridge, MA, USA, 2008; pp. 23–34. ISBN 9780262622158. [Google Scholar]

- Martinez, S.; Hand, M.; Da Pra, M.; Pollock, S.; Ralston, K.; Smith, T.; Vogel, S.; Clark, S.; Lohr, L.; Low, S.; et al. Local Food Systems: Concepts, Impacts, and Issues; Economic Research Report No. 97; United States Department of Agriculture Economic Research Service: Washington, DC, USA, 2010. Available online: https://www.ers.usda.gov/webdocs/publications/46393/7054_err97_1_.pdf?v=42265 (accessed on 13 December 2017).

- LeRoux, M.N.; Schmit, T.M.; Roth, M.; Streeter, D.H. Evaluating marketing channel options for small-scale fruit and vegetable producers. Renew. Agric. Food Syst. 2010, 25, 16–23. [Google Scholar] [CrossRef]

- Hardesty, S.; Leff, P. Determining marketing costs and returns in alternative marketing channels. Renew. Agric. Food Syst. 2009, 25, 24–34. [Google Scholar] [CrossRef]

- Biermacher, J.; Upson, S.; Miller, D.; Pittman, D. Economic Challenges of Small-Scale Vegetable Production and Retailing in Rural Communities: An Example from Rural Oklahoma. J. Food Distrib. Res. 2007, 38, 1–13. [Google Scholar]

- Guthman, J. Agrarian Dreams: The Paradox of Organic Farming in California, 2nd ed.; University of California Press: Oakland, CA, USA, 2014; ISBN 978-0-520-27746-5. [Google Scholar]

- Lurie, S.; Brekken, C. The role of local agriculture in the new natural resource economy (NNRE) for rural economic development. Renew. Agric. Food Syst. 2017. [CrossRef]

- O’Hara, J.K.; Pirog, R. Economic impacts of local food systems: Future research priorities. J. Agric. Food Syst. Community Dev. 2013, 3, 35–42. [Google Scholar] [CrossRef]

- Hardesty, S.; Christensen, L.O.; McGuire, E.; Feenstra, G.; Ingels, C.; Muck, J.; Boorinakis-Harper, J.; Fake, C.; Oneto, S. Economic Impacts of Local Food Producers in the Sacramento Region; University of California Agriculture and Natural Resources: Davis, CA, USA, 2016; Available online: http://sfp.ucdavis.edu/files/238053.pdf (accessed on 13 December 2017).

- Schmit, T.M.; Jablonski, B.B.R.; Mansury, Y. Assessing the Economic Impacts of Local Food System Producers by Scale: A Case Study from New York. Econ. Dev. Q. 2016, 30, 316–328. [Google Scholar] [CrossRef]

- Lev, L.; Brewer, L.; Stephenson, G. Research Brief: How Do Farmers’ Markets Affect Neighboring Business. 2003. Available online: http://smallfarms.oregonstate.edu/sites/default/files/publications/techreports/TechReport16.pdf (accessed on 13 December 2017).

- Altieri, M.A. The ecological role of biodiversity in agroecosystems. Agric. Ecosyst. Environ. 1999, 74, 19–31. [Google Scholar] [CrossRef]

- Stigler, G.J. The Economics of Minimum Wage Legislation. Am. Econ. Rev. 1946, 36, 358–365. [Google Scholar]

- Belman, D.; Wolfson, P.J. What Does the Minimum Wage Do? Upjohn Institute Press: Kalamazoo, MI, USA, 2014; ISBN 9780880994569. [Google Scholar]

- Krueger, A.B. The History of Economic Thought on the Minimum Wage. Ind. Relat. 2015, 54, 533–537. [Google Scholar] [CrossRef]

- Card, D.; Krueger, A.B. Minimum Wages and Employment: A Case Study of the Fast-Food Industry in New Jersey and Pennsylvania. Am. Econ. Rev. 1994, 84, 772–793. [Google Scholar] [CrossRef]

- Card, D.; Krueger, A.B. Minimum Wages and Employment: A Case Study of the Fast-Food Industry in New Jersey and Pennsylvania: Reply. Am. Econ. Rev. 2000, 90, 1397–1420. [Google Scholar] [CrossRef]

- Doucouliagos, H.; Stanley, T.D. Publication Selection Bias in Minimum-Wage Research? A Meta-Regression Analysis. Br. J. Ind. Relat. 2009, 47, 406–428. [Google Scholar] [CrossRef]

- Dube, A.; Lester, T.W.; Reich, M. Minimum Wage Effects across State Borders: Estimates Using Contiguous Counties. Rev. Econ. Stat. 2010, 92, 945–964. [Google Scholar] [CrossRef]

- Neumark, D.; Wascher, W. Employment Effects of Minimum and Subminimum Wages: Panel Data on State Minimum Wage Laws. Ind. Labor Relat. Rev. 1992, 46, 55–81. [Google Scholar] [CrossRef]

- Gowers, R.; Hatton, T.J. The Origins and Early Impact of the Minimum Wage in Agriculture. Econ. Hist. Rev. 1997, 50, 82–103. [Google Scholar] [CrossRef]

- Moretti, E.; Perloff, J.M. Minimum Wage Laws Lower Some Agricultural Wages; IRLE Working Paper No. 84-00; Institute for Research on Labor and Employment: Berkeley, CA, USA, 2000; Available online: https://escholarship.org/uc/item/9b81j9nr (accessed on 13 January 2018).

- Schuler, R.S.; Jackson, S.E. Linking competitive strategies with human resource management practices. Acad. Manag. Exec. 1987, 1, 207–219. [Google Scholar] [CrossRef]

- Brown, D.; Crossman, A. Employer strategies in the face of a national minimum wage: An analysis of the hotel sector. Ind. Relat. 2000, 31, 206–219. [Google Scholar] [CrossRef]

- Goldin, C.; Margo, R.A. The Great Compression: The Wage Structure in the United States at Mid-Century. Q. J. Econ. 1992, 107, 1–34. [Google Scholar] [CrossRef]

- Dube, A.; Naidu, S.; Reich, M. The Economic Effect of a Citywide Minimum Wage. Ind. Labor Relat. Rev. 2007, 60, 522–543. [Google Scholar] [CrossRef]

- Maxwell, J.A. Qualitative Research Design: An Interactive Approach, 3rd ed.; SAGE Publications, Inc.: Thousands Oaks, CA, USA, 2013; ISBN 978-1-4129-8119-4. [Google Scholar]

- Robson, C. Real World Research: A Resource for Users of Social Research Methods in Applied Settings, 3rd ed.; John Wiley & Sons Ltd.: Hoboken, NJ, USA, 2011; ISBN 978-1-118-53150-1. [Google Scholar]

- Saldaña, J. The Coding Manual for Qualitative Researchers, 2nd ed.; SAGE Publications Inc.: Thousand Oaks, CA, USA, 2013; ISBN-10: 1446247376. [Google Scholar]

- Oregon Bureau of Labor and Industries. Oregon Minimum Wage Rate Summary. Available online: https://www.oregon.gov/boli/WHD/OMW/Pages/Minimum-Wage-Rate-Summary.aspx (accessed on 16 March 2017).

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).