A Review on Decentralized Finance Ecosystems

Abstract

1. Introduction

2. Literature Review

2.1. Traditional Finance (TradFi)

2.2. Blockchain Technology in the Financial Industry

2.3. DeFi

- DeFi can potentially reduce transaction costs and offer alternatives to traditional financial intermediaries.

- Through DeFi-based financial services, individuals can connect directly with one another, enabling more affordable and accessible access to basic financing [12].

- DeFi facilitates secure crypto asset transfer and management, granting users control and transparency over their financial assets.

- DeFi’s composability allows for the assembly of building blocks to create novel services, such as stablecoins for yield farming and generating returns.

- DeFi tokens in the market display varying degrees of efficiency, with many investors acquiring them for their utility rather than solely for speculative purposes.

2.4. TradFi and CeFi

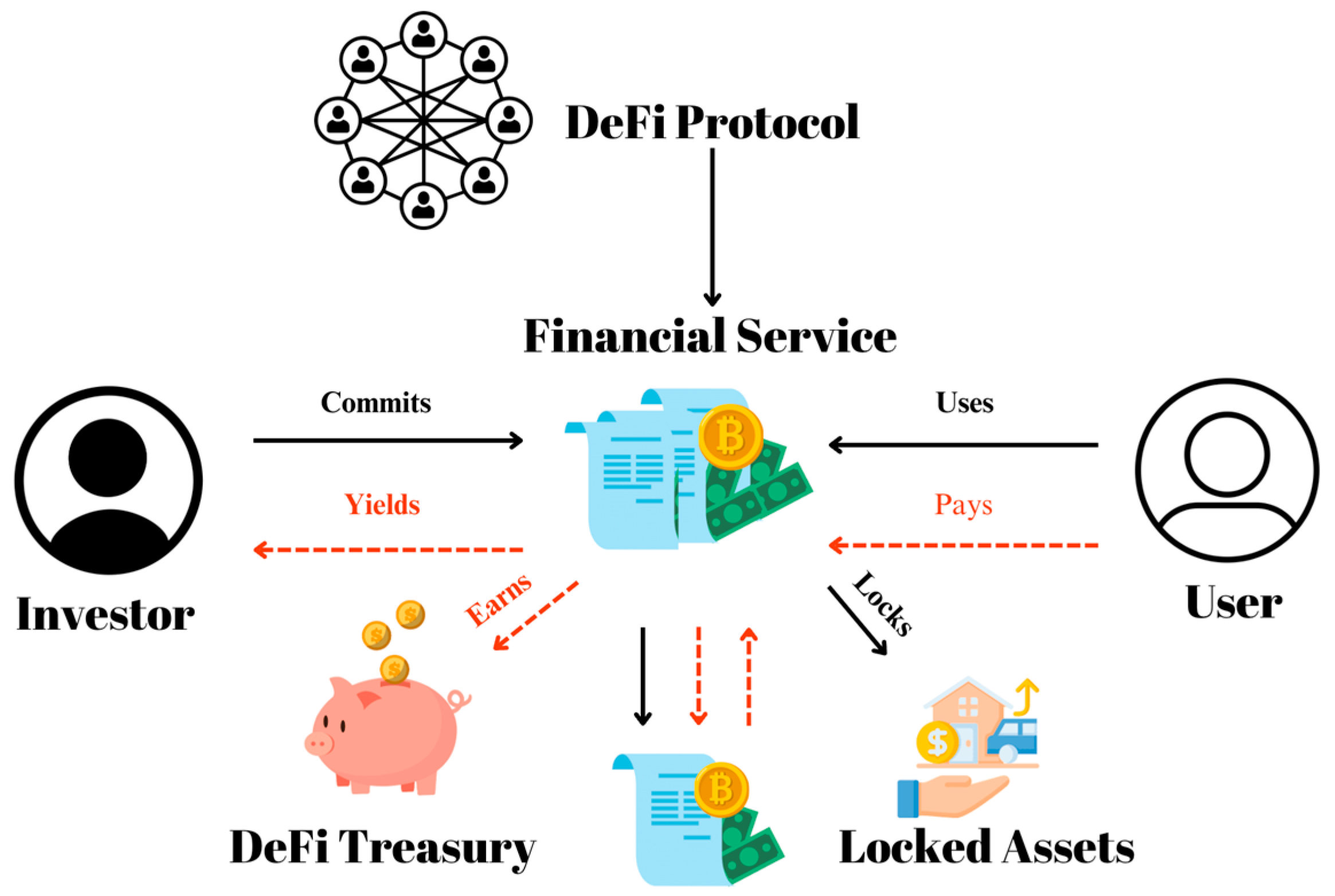

2.5. DeFi Market Mechanism

- ○

- Protocol: A collection of smart contracts encompassing various facets like PLFs, AMMs, or yield aggregators. These protocols offer open, noncustodial, permissionless, and composable financial services in exchange for nominal fees levied on asset movements, such as borrowing or swapping [36].

- ○

- Investor: This participant assumes the underlying protocol risk, including potential misbehavior, impermanent loss, or rug-pulls, in return for passive income. Their primary role involves depositing assets and providing liquidity to these financial services [36].

- ○

- User: Typically, users interact with the protocol in real time, not expecting extended responses. However, in the case of yield aggregators, users may also function as investors. Users initiate asset movements and pay interest rates to the protocol [36].

- ○

- Financial Service: The linchpin of the entire protocol, this entity locks assets, fulfills asset movement requests, and safeguards against protocol misuse. Additionally, it can act as an investor by leveraging other DeFi protocols, ultimately delivering yields and earnings to other participants [36].

2.6. Smart Contract Role in DeFi

2.7. Peer-to-Peer Transaction in DeFi

2.8. Tokenization Mechanism

3. Methodology

- ○

- Scope: This encompasses a broader range of applications, including enhancements to existing business processes (such as technology, advantages, security, risk, and benefit) and support for new products or innovations. Additionally, it delves into the comparison between DeFi and TradFi in the financial industry.

- ○

- Financial Instruments: DeFi aims to recreate TradFi products through smart contracts for P2P operation; however, there are still new challenges and innovations in DeFi.

- ○

- Risk and Regulation: DeFi’s decentralized and permissionless nature potentially introduces certain risks that are not present in TradFi. We present a lucid discussion of the manifestation of risks in the DeFi ecosystem.

3.1. Information Discovery

- What are the DeFi key features?

- What are set the key features that enable DeFi ecosystem disruption?

- What are the benefits of using DeFi for the financial industry?

- What is DeFi Challenge in the financial industry?

- What are the ethnographic aspects of DeFi adoption, e.g., user behavior and regulatory view?

- What DeFi products/services could disrupt or collaborate with TradFi-compatible products/services?

- What are the threats of adopting DeFi in the financial industry?

- How do we manage the risks of DeFi adoption threats?

- Knowledge and Use Case of DeFi Ecosystem: This category encompasses journals, conference papers, and white papers that discuss information or knowledge about DeFi systems, as well as the various use cases that occur within the DeFi ecosystem.

- DeFi Technology: In this category, we explore the foundational technologies in DeFi, including blockchain, smart contracts, and other relevant technologies that underpin the functioning of DeFi platforms.

- Challenges and Opportunities of DeFi: This category addresses the challenges faced by DeFi, such as regulatory hurdles, and also explores the opportunities that DeFi presents, including transparency, accessibility, low-cost services, and self-custody options.

- DeFi and TradFi: This category focuses on the relationship between DeFi and TradFi and provides a comparative analysis of the two financial systems.

- Risk in DeFi: In this category, we examine the various risks associated with DeFi, including bugs, hackers, and fraud, and analyze their potential impacts on the DeFi ecosystem.

- Total Value Locked (TVL): The total value locked in DeFi witnessed substantial growth. In 2020, it expanded by 14×, and in 2021, it more than quadrupled, reaching a peak value of USD 112.07 billion [84].

- DeFi Derivatives: The DeFi derivatives market, still in its nascent stages, has shown remarkable growth. At the end of 2020, its total value locked (TVL) was around USD 25 billion and is estimated to be 10×greater than the global GDP [85].

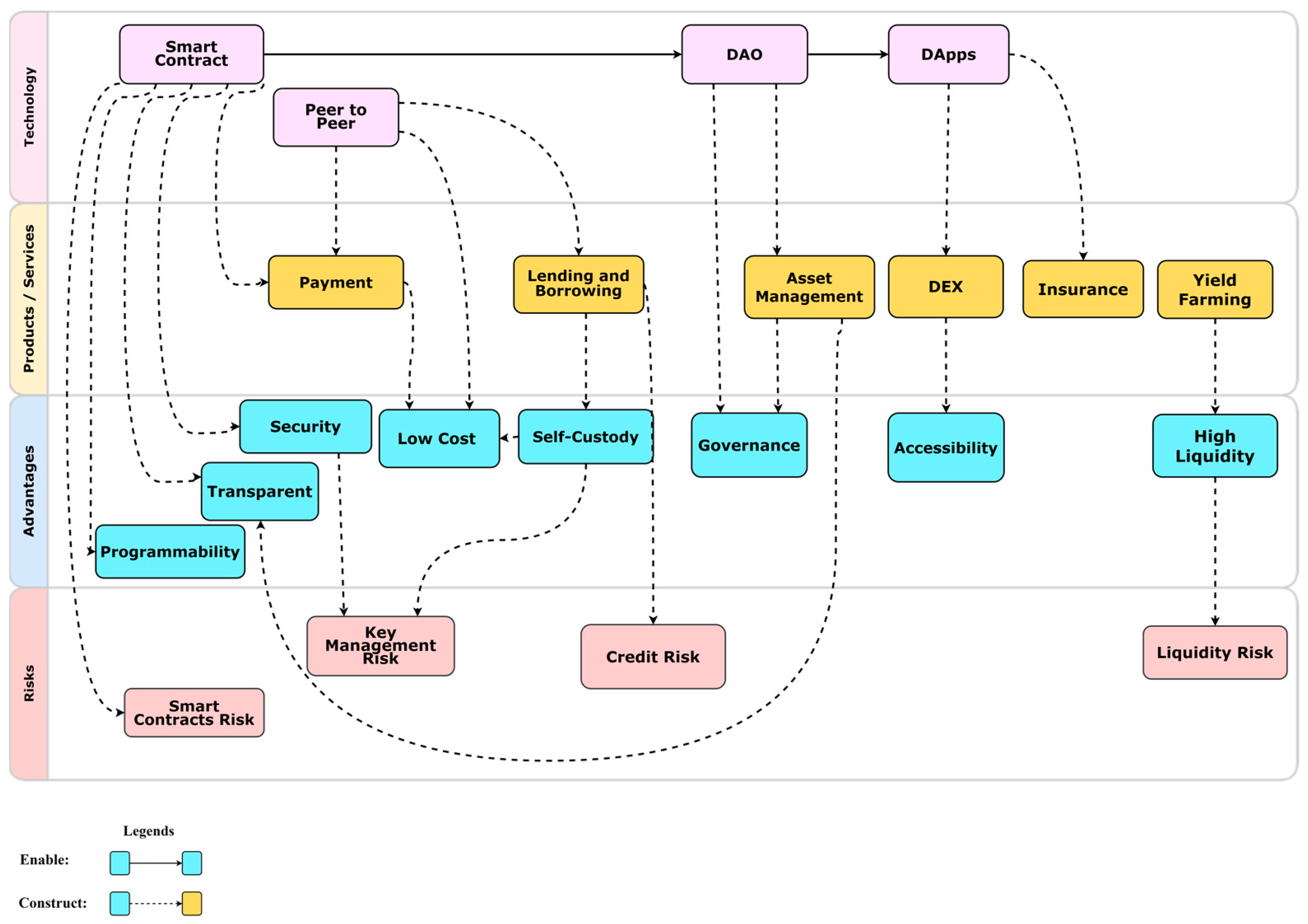

3.2. Taxonomy Formulation

4. The Taxonomy

4.1. Technology

4.1.1. Peer-to-Peer

4.1.2. Smart Contract

Decentralized Autonomous Organization

Decentralized Applications (DApps)

4.2. Product/Services

4.2.1. Payments

4.2.2. Lending and Borrowing

4.2.3. Asset Management

4.2.4. Insurance

4.2.5. Stablecoin

- ○

- Fiat-Collateralized: In the fiat-collateralized mechanism, stablecoins are pegged to a fixed amount of fiat currency, usually USD, and this is achieved through a network of banks that hold the fiat collateral. This approach is not decentralized, and stablecoins like USDT and USDC are examples of this mechanism [55].

- ○

- Crypto Asset-Collateralized: In the context of stablecoins, a common stabilization mechanism involves using a crypto asset as collateral to back each unit of the stablecoin. Stablecoin requires a mechanism to protect against fluctuations in the value of the collateral. One example of such a stablecoin is DAI, which is pegged to 1 USD. To obtain a newly created DAI, a user must provide a greater amount of cryptocurrency as collateral than the value of the DAI requested [41].

4.2.6. Staking

4.2.7. Yield Farming

4.2.8. Decentralized Exchanges (DEXs)

4.3. Advantages

4.3.1. Benefits

Self-Custody

Accessibility

Security

Low Cost

High Liquidity

4.3.2. Features

Transparent Transaction

Programmability

Tokenization

Governance

4.4. Risks

4.4.1. Technical Risks

Smart Contracts Risk

Miner Risks

Transaction Risks

4.4.2. Financial Risks

Liquidity Risk

Market Risk

Credit Risk

4.4.3. Operational Risks

Composability Risk

Key Management Risk

4.4.4. Legal and Regulatory Risk

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Dhillon, V.; Metcalf, D.; Hooper, M. Blockchain Enabled Applications; Springer Science and Business Media LLC: Dordrecht, The Netherlands, 2017. [Google Scholar] [CrossRef]

- Pal, A.; Tiwari, C.K.; Behl, A. Blockchain technology in financial services: A comprehensive review of the literature. J. Glob. Oper. Strateg. Sourc. 2021, 14, 61–80. [Google Scholar] [CrossRef]

- Li, W.; Bu, J.; Li, X.; Peng, H.; Niu, Y.; Zhang, Y. A survey of DeFi security: Challenges and opportunities. J. King Saud Univ.—Comput. Inf. Sci. 2022, 34, 10378–10404. [Google Scholar] [CrossRef]

- Raffaele, T.; Matteo, P.; Mario, T.; Alberto, M. The contribution of blockchain technologies to anti-corruption practices: A systematic literature review. Bus. Strategy Environ. 2023, 33, 4–18. [Google Scholar] [CrossRef]

- Aquilina, M.; Frost, J.; Schrimpf, A. Decentralised Finance (DeFi): A Functional Approach. SSRN Electron. J. 2023, 1–26. [Google Scholar] [CrossRef]

- Mohan, V. Automated market makers and decentralized exchanges: A DeFi primer. Financ. Innov. 2022, 8, 20. [Google Scholar] [CrossRef]

- Gudgeon, L.; Perez, D.; Harz, D.; Livshits, B.; Gervais, A. The Decentralized Financial Crisis. In Proceedings of the 2020 Crypto Valley Conference on Blockchain Technology (CVCBT 2020), Rotkreuz, Switzerland, 11–12 June 2020; pp. 1–15. [Google Scholar] [CrossRef]

- Truchet, M. Decentralized Finance (DeFi): Opportunities, Challenges and Policy Implications. 2022, pp. 69–76. Available online: https://www.eurofi.net/wp-content/uploads/2022/05/eurofi_decentralized-finance-defi_opportunities-challenges-and-policy-implications_paris_february-2022.pdf (accessed on 31 December 2023).

- Naggar, M. Real World Assets: The Bridge between TradFi and DeFi; Binance: Shanghai, China, 2023. [Google Scholar]

- Mnohoghitnei, I.; Horobeț, A.; Belașcu, L. Bitcoin is so Last Decade—How Decentralized Finance (DeFi) could Shape the Digital Economy. Eur. J. Interdiscip. Stud. 2022, 14, 87–99. [Google Scholar] [CrossRef]

- Steiner, G.H.J.-M.; Bhaumik, A. Defi Explained: The Case of Decentralized Exchanges; Vinzenz Treytl (ABC Research): Vienna, Austria, 2022. [Google Scholar]

- Tabarrok, A.; Cowen, T. Cryptoeconomics. 2022. Available online: https://marginalrevolution.com/wp-content/uploads/2022/05/Cryptoeconomics-Modern-Principles.pdf (accessed on 31 December 2023).

- Metelski, D.; Sobieraj, J. Decentralized Finance (DeFi) Projects: A Study of Key Performance Indicators in Terms of DeFi Protocols’ Valuations. Int. J. Financ. Stud. 2022, 10, 108. [Google Scholar] [CrossRef]

- Alamsyah, A.; Syahputra, S. The Taxonomy of Blockchain-based Technology in the Financial Industry. F1000Res 2023, 12, 457. [Google Scholar] [CrossRef] [PubMed]

- Zetzsche, D.A.; Arner, D.W.; Buckley, R.P. Decentralized Finance (DeFi). SSRN Electron. J. 2020, 6, 172–203. [Google Scholar] [CrossRef]

- Erina, A. 4 Key Findings in CoinGecko’s DeFi Survey. Available online: https://www.coingecko.com/learn/defi-survey (accessed on 17 March 2023).

- Kumar, M.; Nikhil, N.; Singh, R. Decentralising finance using decentralised blockchain oracles. In Proceedings of the 2020 International Conference for Emerging Technology (INCET 2020), Belgaum, India, 5–7 June 2020; pp. 1–4. [Google Scholar] [CrossRef]

- Grassi, L.; Lanfranchi, D.; Faes, A.; Renga, F.M. Do we still need financial intermediation? The case of decentralized finance—DeFi. Qual. Res. Account. Manag. 2022, 19, 323–347. [Google Scholar] [CrossRef]

- Carapella, F.; Dumas, E.; Gerszten, J.; Swem, N.; Wall, L. Decentralized Finance (DeFi): Transformative Potential & Associated Risks. Financ. Econ. Discuss. Ser. 2022, 2022, 1–33. [Google Scholar] [CrossRef]

- Clark, M. DeFi vs. Traditional Finance: A Comparative Study. Available online: https://blockchainreporter.net/defi-vs-traditional-finance-a-comparative-study/ (accessed on 12 January 2024).

- Angell, P. What Is The Difference between DeFi, CeFi and TradFi? Available online: https://screenrant.com/defi-vs-cefi-vs-tradfi-differences-explained/ (accessed on 31 December 2023).

- Yousaf, I.; Nekhili, R.; Gubareva, M. Linkages between DeFi assets and conventional currencies: Evidence from the COVID-19 pandemic. Int. Rev. Financ. Anal. 2022, 81, 102082. [Google Scholar] [CrossRef]

- Gorkhali, A.; Chowdhury, R. Blockchain and the Evolving Financial Market: A Literature Review. J. Ind. Integr. Manag. 2022, 7, 47–81. [Google Scholar] [CrossRef]

- Trivedi, S.; Mehta, K.; Sharma, R. Systematic Literature Review on Application of Blockchain Technology in E-Finance and Financial Services. 2021. Available online: http://jotmi.org (accessed on 30 December 2023).

- Patel, R.; Migliavacca, M.; Oriani, M.E. Blockchain in banking and finance: A bibliometric review. Res. Int. Bus. Financ. 2022, 62, 101718. [Google Scholar] [CrossRef]

- Alamsyah, A.; Hakim, N.; Hendayani, R. Blockchain-Based Traceability System to Support the Indonesian Halal Supply Chain Ecosystem. Economies 2022, 10, 134. [Google Scholar] [CrossRef]

- Christidis, K.; Devetsikiotis, M. Blockchains and Smart Contracts for the Internet of Things. IEEE Access 2016, 4, 2292–2303. [Google Scholar] [CrossRef]

- Habib, G.; Sharma, S.; Ibrahim, S.; Ahmad, I.; Qureshi, S.; Ishfaq, M. Blockchain Technology: Benefits, Challenges, Applications, and Integration of Blockchain Technology with Cloud Computing. Future Internet 2022, 14, 341. [Google Scholar] [CrossRef]

- Alamsyah, A.; Widiyanesti, S.; Wulansari, P.; Nurhazizah, E.; Dewi, A.S.; Rahadian, D.; Ramadhani, D.P.; Hakim, M.N.; Tyasamesi, P. Blockchain traceability model in the coffee industry. J. Open Innov. Technol. Mark. Complex. 2023, 9, 100008. [Google Scholar] [CrossRef]

- Wust, K.; Gervais, A. Do you need a blockchain? In Proceedings of the 2018 Crypto Valley Conference on Blockchain Technology (CVCBT 2018), Zug, Switzerland, 20–22 June 2018; pp. 45–54. [Google Scholar] [CrossRef]

- Schueffel, P. DeFi: Decentralized Finance—An Introduction and Overview. J. Innov. Manag. 2021, 9, I–XI. [Google Scholar] [CrossRef]

- Xu, T.A.; Xu, J.; Lommers, K. DeFi vs. TradFi: Valuation Using Multiples and Discounted Cash Flow. October 2022. Available online: http://arxiv.org/abs/2210.16846 (accessed on 31 December 2023).

- Piñeiro-Chousa, J.; Šević, A.; González-López, I. Impact of social metrics in decentralized finance. J. Bus. Res. 2023, 158, 113673. [Google Scholar] [CrossRef]

- Bank for Consultative Group on Risk Management. Consultative Group on Risk Management Central Bank Digital Currency (CBDC) Information Security and Operational Risks to Central Banks. 2023. Available online: www.bis.org (accessed on 31 December 2023).

- Voshmgir, S. Token Economy: How the Web3 Reinvents the Internet; Token Kitchen: Alentejo, Portugal, 2020; Volume 1. [Google Scholar]

- Xu, T.A.; Xu, J. A Short Survey on Business Models of Decentralized Finance (DeFi) Protocols. arXiv 2022, arXiv:2202.0774. [Google Scholar] [CrossRef]

- Li, Z.; Xiao, B.; Guo, S.; Yang, Y. Securing Deployed Smart Contracts and DeFi With Distributed TEE Cluster. IEEE Trans. Parallel Distrib. Syst. 2023, 34, 828–842. [Google Scholar] [CrossRef]

- Bidry, M.; Ouaguid, A.; Hanine, M. Enhancing E-Learning with Blockchain: Characteristics, Projects, and Emerging Trends. Future Internet 2023, 15, 293. [Google Scholar] [CrossRef]

- Bahga, A.; Madisetti, V.K. Blockchain Platform for Industrial Internet of Things. J. Softw. Eng. Appl. 2016, 9, 533–546. [Google Scholar] [CrossRef]

- Kim, H.; Kim, H.S.; Park, Y.S. Perpetual Contract NFT as Collateral for DeFi Composability. IEEE Access 2022, 10, 126802–126814. [Google Scholar] [CrossRef]

- Sorin, E.; Bobo, L.; Pinson, P. Consensus-Based Approach to Peer-to-Peer Electricity Markets with Product Differentiation. IEEE Trans. Power Syst. 2019, 34, 994–1004. [Google Scholar] [CrossRef]

- Schär, F. Decentralized finance: On blockchain-and smart contract-based financial markets. Fed. Reserve Bank St. Louis Rev. 2021, 103, 153–174. [Google Scholar] [CrossRef]

- Tian, Y.; Lu, Z.; Adriaens, P.; Minchin, R.E.; Caithness, A.; Woo, J. Finance infrastructure through blockchain-based tokenization. Front. Eng. Manag. 2020, 7, 485–499. [Google Scholar] [CrossRef]

- Swinkels, L. Empirical evidence on the ownership and liquidity of real estate tokens. Financ. Innov. 2023, 9, 45. [Google Scholar] [CrossRef]

- Chopra, N.; Han, A. Tokenization The Foundation of Digital Financial Markets; SecuritySenses: London, UK, 2023. [Google Scholar]

- Didenko, A.N. Decentralised Finance—A Policy Perspective; CPA Australia Ltd.: Hong Kong, China, 2022. [Google Scholar]

- Bartoletti, M.; Chiang, J.H.Y.; Lluch-Lafuente, A. A Theory of Automated Market Makers in Defi. Log. Methods Comput. Sci. 2022, 18, 1–12. [Google Scholar] [CrossRef]

- Makarov, I.; Schoar, A. Nber Working Paper Series Cryptocurrencies and Decentralized Finance (Defi). 2022. Available online: http://www.nber.org/papers/w30006 (accessed on 30 December 2023).

- Meegan, X.; Koens, T. Lessons Learned from Decentralised Finance (DeFi); Blockchain@Ing.Com: Amsterdam, The Netherlands, 2021; pp. 1–20. [Google Scholar]

- Ozili, P.K. Assessing global interest in decentralized finance, embedded finance, open finance, ocean finance and sustainable finance. Asian J. Econ. Bank. 2022, 7, 197–216. [Google Scholar] [CrossRef]

- Radix, H.; Layer, F.; Developers, D. Radix DeFi White Paper; Radix Foundation Ltd.: Cardiff, Wales, 2020; pp. 1–31. [Google Scholar]

- Werner, S.; Perez, D.; Harz, D.; Knottenbelt, W.J. SoK: Decentralized Finance (DeFi). arXiv 2022, arXiv:2101.08778. [Google Scholar]

- Carre, S.; Gabriel, F. Security and Credit in Proof-of-Stake DeFi Protocols. SSRN Electron. J. 2022, 103, 1–36. [Google Scholar] [CrossRef]

- Chen, Y.; Bellavitis, C. Decentralized Finance: Blockchain Technology and the Quest for an Open Financial System (July 3, 2019). Stevens Institute of Technology School of Business Research Paper. Available online: https://ssrn.com/abstract=3418557 (accessed on 30 December 2023).

- Gudgeon, L.; Werner, S.; Perez, D.; Knottenbelt, W.J. DeFi Protocols for Loanable Funds: Interest Rates, Liquidity and Market Efficiency. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies (AFT 2020), New York, NY, USA, 21–23 October 2020; pp. 92–112. [Google Scholar] [CrossRef]

- Hassan, S.; De Filippi, P. Decentralized autonomous organization. Internet Policy Rev. 2021, 10, 1–10. [Google Scholar] [CrossRef]

- Heimbach, L.; Wang, Y.; Wattenhofer, R. Behavior of Liquidity Providers in Decentralized Exchanges. arXiv 2021, arXiv:2105.13822. [Google Scholar]

- Pham, V.B.; Trinh, T.D. Analysis Model for Decentralized Lending Protocols. In Proceedings of the 11th International Symposium on Information and Communication Technology, Hanoi, Vietnam, 1–3 December 2022; pp. 405–412. [Google Scholar] [CrossRef]

- Rajput, S.; Singh, A.; Khurana, S.; Bansal, T.; Shreshtha, S. Blockchain Technology and Cryptocurrenices. In Proceedings of the 2019 Amity International Conference on Artificial Intelligence (AICAI 2019), Dubai, United Arab Emirates, 4–6 February 2019; pp. 909–912. [Google Scholar] [CrossRef]

- Schneider, B.; Ballesteros, R.; Moriggl, P.; Asprion, P.M. Decentralized Autonomous Organizations—Evolution, Challenges, and Opportunities. In Proceedings of the PoEM’2022 Workshop and Models at Work Papers, London, UK, 23–25 November 2022; Volume 3298. [Google Scholar]

- Sims, A. Blockchain and Decentralised Autonomous Organisations (DAOs): The Evolution of Companies? SSRN Electron. J. 2020, 96, 423–458. [Google Scholar] [CrossRef]

- Xu, J.; Feng, Y. Reap the Harvest on Blockchain: A Survey of Yield Farming Protocols. IEEE Trans. Netw. Serv. Manag. 2022, 20, 858–869. [Google Scholar] [CrossRef]

- Yan, W.; Zhou, W. Is blockchain a cure for peer-to-peer lending? Ann. Oper. Res. 2023, 321, 693–716. [Google Scholar] [CrossRef]

- Zhang, Y.; Kasahara, S.; Shen, Y.; Jiang, X.; Wan, J. Smart contract-based access control for the internet of things. IEEE Internet Things J. 2019, 6, 1594–1605. [Google Scholar] [CrossRef]

- Dabaja, F.; Dahlberg, T.; Uddin, G.S. Decentralized Finance and the Crypto Market: Indicators and Correlations. 2021. Available online: www.liu.se (accessed on 30 December 2023).

- Ryabov, O.; Golubev, A.; Goncharova, N. Decentralized Finance (Defi) As the Basis for the Transformation of the Financial Sector of the Future. In Proceedings of the 3rd International Scientific Conference on Innovations in Digital Economy, Saint Petersburg, Russia, 14–15 October 2021; pp. 387–394. [Google Scholar] [CrossRef]

- Visa. DeFi: The New Frontier of Finance; Visa: San Francisco, CA, USA, 2022. [Google Scholar]

- Wronka, C. Financial crime in the decentralized finance ecosystem: New challenges for compliance. J. Financ. Crime 2023, 30, 97–113. [Google Scholar] [CrossRef]

- Chohan, U.W. Decentralized Finance (DeFi): An Emergent Alternative Financial Architecture (January 26, 2021). Critical Blockchain Research Initiative (CBRI) Working Papers. Available online: https://ssrn.com/abstract=3791921 (accessed on 30 December 2023).

- Khan, B.; Syed, T. Recent progress in blockchain in public finance and taxation. In Proceedings of the 2019 8th International Conference on Information and Communication Technologies (ICICT 2019), Karachi, Pakistan, 16–17 November 2019; pp. 36–41. [Google Scholar] [CrossRef]

- Kurka, J. Do cryptocurrencies and traditional asset classes influence each other? Financ. Res. Lett. 2019, 31, 38–46. [Google Scholar] [CrossRef]

- Makridis, C.A.; Fröwis, M.; Sridhar, K.; Böhme, R. The rise of decentralized cryptocurrency exchanges: Evaluating the role of airdrops and governance tokens. J. Corp. Financ. 2023, 79, 102358. [Google Scholar] [CrossRef]

- Qin, K.; Zhou, L.; Afonin, Y.; Lazzaretti, L.; Gervais, A. CeFi vs. DeFi—Comparing Centralized to Decentralized Finance; Association for Computing Machinery: New York, NY, USA, 2021; Volume 1. [Google Scholar]

- Cai, W.; Wang, Z.; Ernst, J.B.; Hong, Z.; Feng, C.; Leung, V.C.M. Decentralized Applications: The Blockchain-Empowered Software System. IEEE Access 2018, 6, 53019–53033. [Google Scholar] [CrossRef]

- Yue, Y.; Li, X.; Zhang, D.; Wang, S. How cryptocurrency affects economy? A network analysis using bibliometric methods. Int. Rev. Financ. Anal. 2021, 77, 101869. [Google Scholar] [CrossRef]

- Aspembitova, A.T.; Bentley, M.A. Oracles in Decentralized Finance: Attack Costs, Profits and Mitigation Measures. Entropy 2023, 25, 60. [Google Scholar] [CrossRef] [PubMed]

- Rjoub, H.; Adebayo, T.S.; Kirikkaleli, D. Blockchain technology-based FinTech banking sector involvement using adaptive neuro-fuzzy-based K-nearest neighbors algorithm. Financ. Innov. 2023, 9, 65. [Google Scholar] [CrossRef]

- Grigo, J.; Hansen, P.; Patz, A.; von Wachter, V. Decentralized Finance (DeFi)—A new Fintech Revolution? 2020. Available online: https://www.bitkom.org/sites/default/files/2020-07/200729_whitepaper_decentralized-finance.pdf (accessed on 31 December 2023).

- Karim, S.; Lucey, B.M.; Naeem, M.A.; Uddin, G.S. Examining the interrelatedness of NFTs, DeFi tokens and cryptocurrencies. Financ. Res. Lett. 2022, 47, 102696. [Google Scholar] [CrossRef]

- Kaur, S.; Singh, S.; Gupta, S.; Wats, S. Risk analysis in decentralized finance (DeFi): A fuzzy-AHP approach. Risk Manag. 2023, 25, 13. [Google Scholar] [CrossRef]

- Markcan. Is A Bug In A Web3 Smart Contract Part of the Contract? Available online: https://markn.ca/2022/is-a-bug-in-a-web3-smart-contract-part-of-the-contract/ (accessed on 25 April 2023).

- Obadia, A. Flashbots: Frontrunning the MEV Crisis|Flashbots. Available online: https://medium.com/flashbots/frontrunning-the-mev-crisis-40629a613752 (accessed on 5 May 2023).

- Statista. DeFi—Worldwide|Statista Market Forecast. Available online: https://www.statista.com/outlook/fmo/digital-assets/defi/worldwide (accessed on 10 January 2024).

- Emergen Research. Navigating Decentralized Finance (DeFi) Market Size 2023: Share Insights, Future Demand and Forecast till 2032|LinkedIn. Available online: https://www.linkedin.com/pulse/navigating-decentralized-finance-defi-market-size-2023-tmxqf/ (accessed on 10 January 2024).

- Chung, J. DeFi Market Commentary|May 2022|Consensys. Available online: https://consensys.io/blog/defi-market-commentary-may-2022 (accessed on 10 January 2024).

- Howarth, J. Top 5 DeFi Trends for 2024–2026. Available online: https://explodingtopics.com/blog/defi-trends (accessed on 10 January 2024).

- Hedera. DeFi Trends to Watch for In 2023|Hedera. Available online: https://hedera.com/learning/decentralized-finance/defi-trends (accessed on 10 January 2024).

- Meyer, E.A.; Welpe, I.M.; Sandner, P. Decentralized Finance—A System Literature Review and Research Directions. 2022. Available online: https://aisel.aisnet.org/ecis2022_rp/25 (accessed on 30 December 2023).

- Rikken, O.; Janssen, M.; Kwee, Z. The ins and outs of decentralized autonomous organizations (DAOs) unraveling the definitions, characteristics, and emerging developments of DAOs. Blockchain Res. Appl. 2023, 4, 100143. [Google Scholar] [CrossRef]

- Aiden, S.; Werbach, K. Decentralized Autonomous Organizations: Beyond the Hype. In Proceedings of the World Economic Forum, Davos-Klosters, Switzerland, 22–26 May 2022; pp. 1–24. [Google Scholar]

- Wu, K. An Empirical Study of Blockchain-based Decentralized Applications. arXiv 2019, arXiv:1902.04969. [Google Scholar] [CrossRef]

- Fluid. FLUID—Major Use Cases in DeFi. Available online: https://www.fluid.finance/news-detail/major-use-cases-in-defi/ (accessed on 22 May 2023).

- Lu, Q.; Tran, A.B.; Weber, I.; O’Connor, H.; Rimba, P.; Xu, X.; Staples, M.; Zhu, L.; Jeffery, R. Integrated model-driven engineering of blockchain applications for business processes and asset management. Softw. Pract. Exp. 2021, 51, 1059–1079. [Google Scholar] [CrossRef]

- Klages-Mundt, A.; Harz, D.; Gudgeon, L.; Liu, J.Y.; Minca, A. Stablecoins 2.0: Economic Foundations and Risk-based Models. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies (AFT 2020), New York, NY, USA, 21–23 October 2020; pp. 59–79. [Google Scholar] [CrossRef]

- Sheikh, H.; Azmathullah, R.M.; Rizwan, F. Proof-of-Work vs. Proof-of-Stake: A Comparative Analysis and an Approach to Blockchain Consensus Mechanism. Int. J. Res. Appl. Sci. Eng. Technol. 2018, 887, 2321–9653. [Google Scholar]

- Lehar, A.; Parlour, C.A. Decentralized Exchange: The Uniswap Automated Market Maker. J. Financ. Forthcom. Available online: https://ssrn.com/abstract=3905316 (accessed on 30 December 2023).

- Pal, O.; Alam, B.; Thakur, V.; Singh, S. Key management for blockchain technology. ICT Express 2021, 7, 76–80. [Google Scholar] [CrossRef]

- Ogiela, M.R.; Ogiela, L. Cognitive cryptography techniques for intelligent information management. Int. J. Inf. Manag. 2018, 40, 21–27. [Google Scholar] [CrossRef]

- Ante, L. Liquidity Shocks, Token Returns and Market Capitalization in Decentralized Finance (DeFi) Markets. 2022. Available online: https://ssrn.com/abstract=4183105 (accessed on 30 December 2023).

- Gates, M. Blockchain: Ultimate Guide to Understanding Blockchain, Bitcoin, Cryptocurrencies, Smart Contracts and the Future of Money; CreateSpace Independent Publishing Platform: Scotts Valley, CA, USA, 2017; pp. 3–5. [Google Scholar]

- Laurent, P.; Chollet, T.; Burke, M.; Seers, T. The tokenization of assets is disrupting the financial industry. Inside Mag. 2018, 19, 62–67. [Google Scholar]

- Zwitter, A.; Hazenberg, J. Decentralized Network Governance: Blockchain Technology and the Future of Regulation. Front. Blockchain 2020, 3, 1–12. [Google Scholar] [CrossRef]

- McCarthy, S. Stewards and Gatekeepers: Human and Technological Agency in the Governance of DeFi Protocols. SSRN Electron. J. 2023. [Google Scholar] [CrossRef]

- Aramonte, S.; Huang, W.; Schrimpf, A. DeFi Risks and the Decentralisation Illusion; BIS: Delhi, India, 2021. [Google Scholar]

- Weingärtner, T.; Fasser, F.; Reis Sá da Costa, P.; Farkas, W. Deciphering DeFi: A Comprehensive Analysis and Visualization of Risks in Decentralized Finance. J. Risk Financ. Manag. 2023, 16, 454. [Google Scholar] [CrossRef]

- Rodriguez, J. The 5 Big Risk Vectors of DeFi. Available online: https://www.coindesk.com/layer2/2022/02/03/the-five-big-risk-vectors-of-defi/ (accessed on 11 January 2024).

- BIS Innovation Hub Eurosystem Centre; De Nederlandsche Bank; The Deutsche Bundesbank. Project Atlas: Mapping the World of Decentralised Finance; BIS: Delhi, India, 2023. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sources | Total Publication Number | Filtered Publication |

|---|---|---|

| Academic Sources:ScienceDirect, Google Scholar, MDPI, IEEE, Emerald Insight, SSRN, and Springer Science | 4.248 | 50 |

| Product/Services Sources:White papers | 10 | 10 |

| Nonacademic Sources:Websites, Medium, CoinGecko, CoinMarketCap, and Ethereum | 8 | 8 |

| Total | 4.266 | 68 |

| Topic Categories | Authors/Year | Reference |

|---|---|---|

| Knowledge and Use Case of the DeFi Ecosystem | (Bartoletti et al., 2022; Didenko, 2022; Kumar et al., 2020; Makarov & Schoar, 2022; Meegan & Koens, 2021; Ozili, 2022; Radix et al., 2020; Schär, 2021; Schueffel, 2021; Vincent et al., 2022; Zetzsche et al., 2020) | [15,17,31,42,46,47,48,49,50,51]. |

| DeFiTechnology | (Aquilina et al., 2023; Bahga & Madisetti, 2016; Carre & Gabriel, 2022; Chen, 2019; Gudgeon, Werner, et al., 2020; Hassan & De Filippi, 2021; Heimbach et al., 2021; Metelski & Sobieraj, 2022; Mohan, 2022; Pham & Trinh, 2022; Raffaele et al., 2023; Rajput et al., 2019; Schneider et al., 2022; Sims, 2020; Sorin et al., 2019; Voshmgir, 2020; Werner et al., 2022; Wust & Gervais, 2018; J. Xu & Feng, 2022; Yan et al., 2023; Yousaf et al., 2022; Zhang et al., 2019; Gorkhali & Chowdhury, 2022, Trivedi et al., 2021, Patel et al., 2022) | [4,5,6,13,23,24,25,35,39,41,52,53,54,55,56,57,58,59,60,61,62,63,64]. |

| Challenges and Opportunities of DeFi | (Dabaja et al., 2021; Li et al., 2022; Ryabov et al., 2021; Swinkels, 2023; Tabarrok & Cowen, 2022; Truchet et al., 2022; Steiner & Bhaumik, 2022; Visa, 2022; Wronka, 2023) | [3,8,11,12,44,65,66,67,68] |

| DeFi and TradFi | (Cai et al. 2018; Carapella et al. 2022; Chohan 2021; Grassi et al. 2022; Khan & Syed 2019; Kurka 2019; Makridis et al. 2023; Mnohoghitnei et al. 2022; Naggar 2023; Pal et al. 2021; Qin et al. 2021; Wang 2018; Xu & Xu, 2022; Yue et al. 2021) | [2,9,10,18,19,36,69,70,71,72,73,74,75]. |

| Risk in DeFi | (Aspembitova & Bentley 2023; Fluid 2022; Grigo et al. 2020; Karim et al. 2022; Kaur et al. 2023; Markcan 2022; Obadia 2020) | [76,77,78,79,80,81]. |

| Taxonomy Study | Summary |

|---|---|

| A survey of DeFi security: Challenges and opportunities (2022) [3]. | This study uses literature analysis vulnerabilities methodology to identify challenges and opportunities within the technical and security domains of DeFi. The research systematically analyzes DeFi security, gathering optimization strategies across the data, network, consensus, smart contract, and application layers. |

| DeFi: Decentralized Finance—An Introduction and Overview (2021) [31]. | This study uses literature review methodology to focus on the characteristics of DeFi and offers examples within the DeFi landscape. The research takes a broad view of the characteristics of DeFi without delving into a more in-depth exploration of the concept or mechanism of the overall ecosystem of DeFi. |

| A Short Survey on Business Models of Decentralized Finance Protocols (2022) [36]. | This study uses literature review methodology to delve into DeFi protocol business models, elucidating the intricacies of various types, namely protocols for loanable funds (PLFs), decentralized exchanges (DEXs), and yield aggregators. The research provides comprehensive insights into the distinctive business models employed by these DeFi protocols. |

| Decentralized Finance—A System Literature Review and Research Directions (2022) [87]. | This study uses a literature review methodology, concentrating on DeFi and exploring academic research directions within the DeFi domain. The research categorizes DeFi-related literature into three levels of abstraction (micro, meso, and macro) to provide a comprehensive and structured analysis of the subject. |

| Decentralized Finance (DeFi): Transformative Potential & Associated Risks (2021) [66]. | This study uses a qualitative methodology that centers on the transformative potential and associated risks of DeFi. Its approach is a more general view of transformative potential and associated risks. The taxonomy comprises three dimensions: blockchain basics, DeFi products and services, and risk implications of DeFi. |

| Do we still need financial intermediation? The case of decentralized finance—DeFi (2022) [18]. | This study uses a twofold qualitative methodology in the literature, which concentrates on the role of technology in financial intermediation, with a specific focus on the case of DeFi. It contributes to the debate between algorithms and human involvement, probing the necessity of TradFi intermediaries in the face of evolving technological landscapes. |

| This Taxonomy | This study employs literature reviews and phenomenological research, uniquely integrating insights from five previous DeFi taxonomy references. Each publication focuses on its respective field and contributes to taxonomy construction. Our approach seeks the most recent information, enhancing the taxonomy’s completeness and clarity. For instance, our taxonomy complements the information lacking in taxonomy by [66], considering differences in research years. Differences in research years ensure that our insights are updated, accounting for the rapid growth of DeFi and providing a more current perspective. An additional example is the study titled “Decentralized Finance—A Systematic Literature Review and Research Directions” [87], which features a more structured taxonomy incorporating micro, meso, and macro layers. In contrast, our taxonomy prioritizes practicality for the industry, establishing relationships between dimensions and interconnectedness. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alamsyah, A.; Kusuma, G.N.W.; Ramadhani, D.P. A Review on Decentralized Finance Ecosystems. Future Internet 2024, 16, 76. https://doi.org/10.3390/fi16030076

Alamsyah A, Kusuma GNW, Ramadhani DP. A Review on Decentralized Finance Ecosystems. Future Internet. 2024; 16(3):76. https://doi.org/10.3390/fi16030076

Chicago/Turabian StyleAlamsyah, Andry, Gede Natha Wijaya Kusuma, and Dian Puteri Ramadhani. 2024. "A Review on Decentralized Finance Ecosystems" Future Internet 16, no. 3: 76. https://doi.org/10.3390/fi16030076

APA StyleAlamsyah, A., Kusuma, G. N. W., & Ramadhani, D. P. (2024). A Review on Decentralized Finance Ecosystems. Future Internet, 16(3), 76. https://doi.org/10.3390/fi16030076