Emerging Trends and Innovation Modes of Internet Finance—Results from Co-Word and Co-Citation Networks

Abstract

1. Introduction

2. Materials and Methods

2.1. Data Source

2.2. Citespace

3. Co-Word Analysis

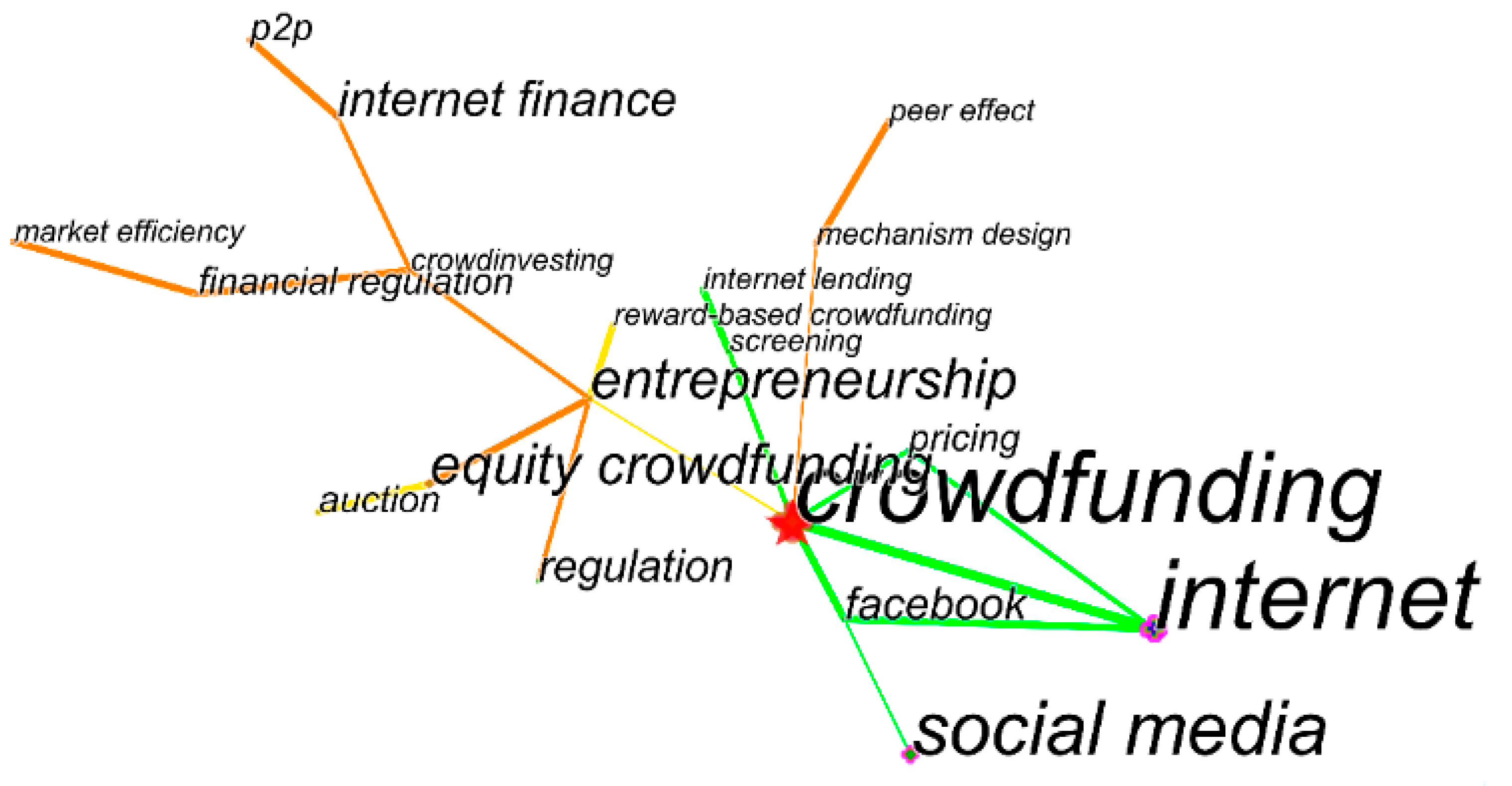

3.1. Main Modes of Internet Finance

3.2. Further Analysis of the Research Perspective

4. Co-Citation Analysis

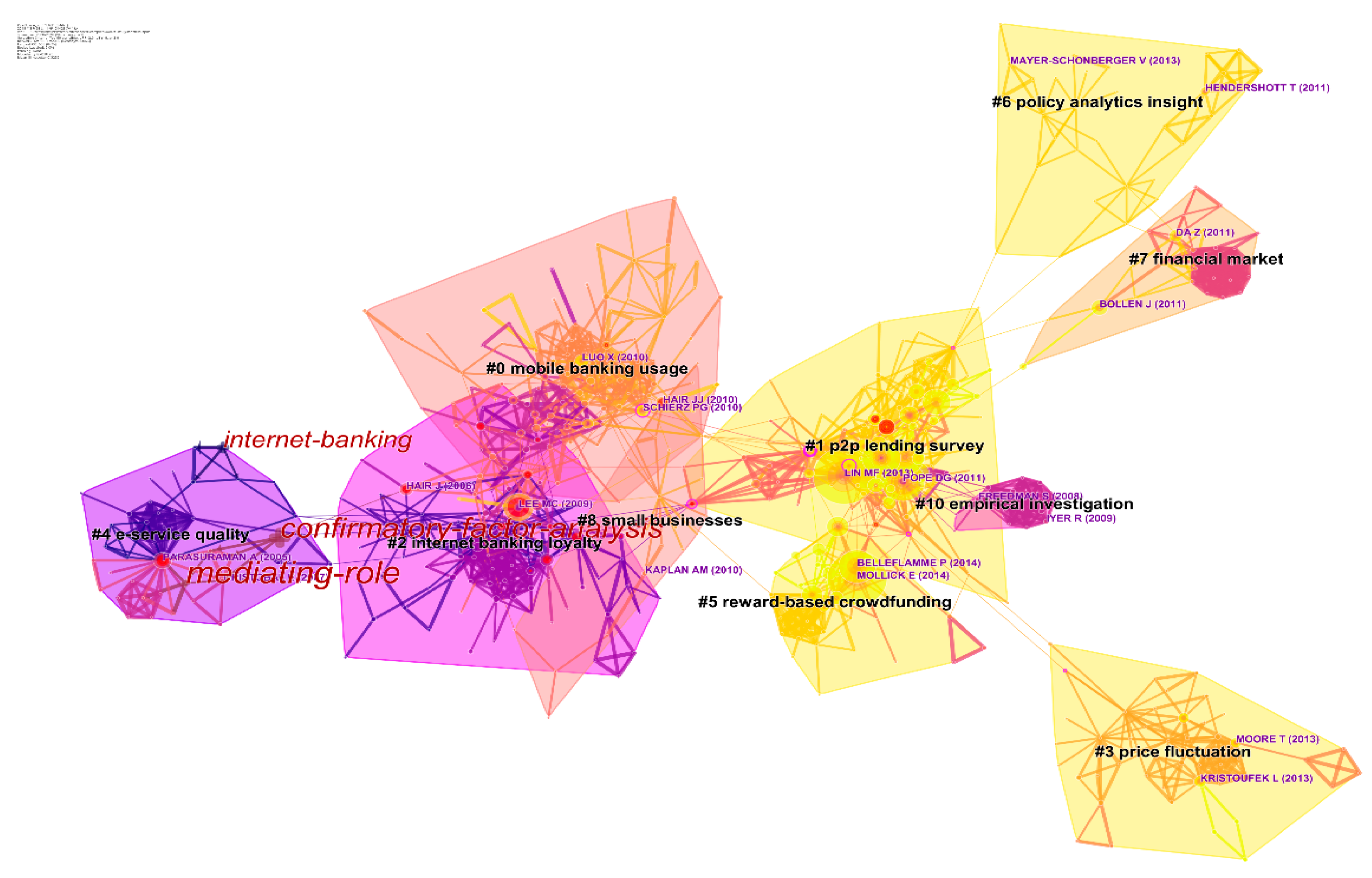

4.1. Main Topics of Each Mode

4.1.1. Internet Bank

4.1.2. P2P Lending

4.1.3. Crowdfunding

4.1.4. Digital Currency

4.1.5. Big Data Finance

4.1.6. Others

4.2. Duration of Each Mode

4.3. The Latest Research Hotspot

5. Major Findings and Outlook

5.1. Major Findings

- Internet banking. Research related to Internet banking is the earliest. In the early days, it mainly studied the influence of various factors such as risk perception, perceived benefits, attitudes and perceived usefulness on user adoption of Internet bank. Later studies focused on the impact of factors such as trust, security, authentication and customer service quality on user loyalty and user usage depth of Internet bank and the research goal turned to the use of mobile banking. The research angle expands from the perspective of the earliest interests and trust to national culture, from the perspective of developed countries to developing countries.

- P2P lending and crowdfunding. The researches of P2P lending and crowdfunding are still developing, which still have potential to explore. And research hotspot focused on these modes. In terms of P2P lending, the content of its research is related to P2P lending success factors like ethnic differences, information asymmetry, herd effect and default prediction. And the main research content is information asymmetry, which is also a research hotspot. As for crowdfunding, one main research content refers to determinants of project crowdfunding success such as information on crowdfunding project sponsors, the quality of crowdfunding projects, the types of crowdfunding projects and investor satisfaction and donors’ behavior. Other research contents include the design of crowdfunding mechanism, the influence of social network on crowdfunding and the use of equity crowdfunding or product crowdfunding. We can study crowdfunding from the perspective of investors, regulators and sponsors.

- Big data finance, fintech and digital currency. The third stage involves fintech, big data finance and digital currency. Their research content is small but constantly enriched and developed. The rapid development of bitcoin has brought the research upsurge of digital currency. Its essence is the main research direction of price decision-making mechanism. The current research on fintech mainly is using big data to predict changes in asset market.

5.2. Outlook

- Information asymmetry in P2P lending is the latest research hotspot and it will continue to develop. The emergence of big data related technologies may solve this problem.

- There will be new research hotspots in the field of crowdfunding. For example, crowdfunding as a financing method is naturally suitable for microfinance and therefore has great help for China’s rural poverty alleviation. But because of the risk of crowdfunding, if there is corresponding crowdfunding insurance, then crowdfunding may enter a stage of rapid development. Of course, the pricing of crowdfunding insurance is also very difficult and requires further study.

- Fintech is still in the first stage and will also develop its own research content, such as artificial intelligence assisted analysis and forecasting market in financial technology, inclusive finance and supervision of emerging content. Artificial intelligence analysis of financial market trends has broad prospects. It can use tens of thousands of indicators to predict capital markets such as stock markets by training automatic screening indicators. And it can be combined with big data to obtain indicators that are difficult to quantify, such as investor sentiment and consumer sentiment, to make predictions more accurate.

- Big data finance can help analyze the credit status of individuals. The combination of big data and artificial intelligence can accurately judge the credit status of individuals and the judgment of each individual will form the credit status of groups, enterprises, regions and countries. And the impact of macroeconomic policies on individuals can be visualized, helping us to make better investment decisions and government policies.

- Digital currency can reduce transaction costs but needs to avoid risks. Digital currency may break a country’s limits in the way it consumes a lot of power before it understands it needs to change. In addition, due to the borderless nature of digital currency, we also need to constantly update the regulatory approach.

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Loubere, N. China’s Internet Finance Boom and Tyrannies of Inclusion. China Perspect. 2017, 4, 9–18. [Google Scholar] [CrossRef]

- Xie, P.; Zou, C. Research on Internet Finance Model. J. Financ. Res. 2012, 12, 11–22. [Google Scholar]

- Qiao, H.; Chen, M.; Xia, Y. The Effects of the Sharing Economy: How Does Internet Finance Influence Commercial Bank Risk Preferences? Emerg. Mark. Financ. Trade 2018, 54, 3013–3029. [Google Scholar] [CrossRef]

- Luo, C.; Li, M.; Peng, P.; Fan, S. How Does Internet Finance Influence the Interest Rate? Evidence from Chinese Financial Markets. Dutch J. Financ. Manag. 2018, 2, 01. [Google Scholar] [CrossRef][Green Version]

- Huang, R.H. Online P2P Lending and Regulatory Responses in China: Opportunities and Challenges. Eur. Bus. Organ. Law Rev. 2018, 19, 63–92. [Google Scholar] [CrossRef]

- Luo, M. Analysis of six models of Internet finance. High-Technol. Ind. 2014, 3, 56–59. [Google Scholar]

- Hanafizadeh, P.; Keating, B.W.; Khedmatgozar, H.R. A systematic review of Internet banking adoption. Telemat. Inform. 2014, 31, 492–510. [Google Scholar] [CrossRef]

- Martinez-Climent, C.; Zorio-Grima, A.; Ribeiro-Soriano, D. Financial return crowdfunding: Literature review and bibliometric analysis. Int. Entrep. Manag. J. 2018, 14, 527–553. [Google Scholar] [CrossRef]

- Huang, T.; Zhao, Y. Revolution of securities law in the Internet Age: A review on equity crowd-funding. Comput. Law Secur. Rev. 2017, 33, 802–810. [Google Scholar] [CrossRef]

- Agarwal, S.; Kumar, S.; Goel, U. Stock market response to information diffusion through Internet sources: A literature review. Int. J. Inf. Manag. 2019, 45, 118–131. [Google Scholar] [CrossRef]

- Cai, C.W. Disruption of financial intermediation by FinTech: A review on crowdfunding and blockchain. Account. Financ. 2018, 58, 965–992. [Google Scholar] [CrossRef]

- Milian, E.Z.; Spinola, M.D.M.; De Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Chen, C.M. CiteSpace II: Detecting and visualizing emerging trends and transient patterns in scientific literature. J. Am. Soc. Inf. Sci. Technol. 2006, 57, 359–377. [Google Scholar] [CrossRef]

- Chen, C.M.; Hu, Z.G.; Liu, S.B.; Tseng, H. Emerging trends in regenerative medicine: A scientometric analysis in CiteSpace. Expert Opin. Biol. Ther. 2012, 12, 593–608. [Google Scholar] [CrossRef] [PubMed]

- Small, H. Co-citation in the scientific literature: A new measure of the relationship between two documents. J. Am. Soc. Inf. Sci. 1973, 24, 265–269. [Google Scholar] [CrossRef]

- Bauin, S. Aquaculture: A Filed by Bureaucratic Fiat. In Mapping the Dynamics of Science and Technology: Sociology of Science in the Real World; Law, J., Rip, A., Callon, M., Eds.; Macmillan Press Ltd: London, UK, 1986; pp. 124–141. [Google Scholar]

- Qin, H. Knowledge Discovery through Co-Word Analysis. Libr. Trends 1999, 48, 133–159. [Google Scholar]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Chen, C.M. Science Mapping: A Systematic Review of the Literature. J. Data Inf. Sci. 2017, 2, 1–40. [Google Scholar] [CrossRef]

- Kleinberg, J. Bursty and hierarchical structure in streams. Data Min. Knowl. Discov. 2003, 7, 373–397. [Google Scholar] [CrossRef]

- Saxton, G.D.; Wang, L.L. The Social Network Effect: The Determinants of Giving Through Social Media. Nonprofit Volunt. Sect. Q. 2014, 43, 850–868. [Google Scholar] [CrossRef]

- Hornuf, L.; Neuenkirch, M. Pricing shares in equity crowdfunding. Small Bus. Econ. 2017, 48, 795–811. [Google Scholar] [CrossRef]

- Zetzsche, D.; Preiner, C. Cross-Border Crowdfunding: Towards a Single Crowdlending and Crowdinvesting Market for Europe. Eur. Bus. Organ. Law Rev. 2018, 19, 217–251. [Google Scholar] [CrossRef]

- Hornuf, L.; Schmitt, M.; Stenzhorn, E. Equity crowdfunding in Germany and the United Kingdom: Follow-up funding and firm failure. Corp. Gov. Int. Rev. 2018, 26, 331–354. [Google Scholar] [CrossRef]

- Jancenelle, V.E.; Javalgi, R.G. The effect of moral foundations in prosocial crowdfunding. Int. Small Bus. J. Res. Entrep. 2018, 36, 932–951. [Google Scholar] [CrossRef]

- Burtch, G.; Hong, Y.; Liu, D. The Role of Provision Points in Online Crowdfunding. J. Manag. Inf. Syst. 2018, 35, 117–144. [Google Scholar] [CrossRef]

- Zheng, H.; Xu, B.; Wang, T.; Chen, D. Project Implementation Success in Reward-Based Crowdfunding: An Empirical Study. Int. J. Electron. Commer. 2017, 21, 424–448. [Google Scholar] [CrossRef]

- Liu, X.; Huang, F.; Yeung, H. The regulation of illegal fundraising in China. Asia Pac. Law Rev. 2018, 26, 77–100. [Google Scholar] [CrossRef]

- Kim, G.; Shin, B.; Lee, H.G. Understanding dynamics between initial trust and usage intentions of mobile banking. Inf. Syst. J. 2009, 19, 283–311. [Google Scholar] [CrossRef]

- Lee, M.-C. Factors influencing the adoption of Internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electron. Commer. Res. Appl. 2009, 8, 130–141. [Google Scholar] [CrossRef]

- Gefen, D.; Karahanna, E.; Straub, D.W. Trust and TAM in online shopping: An integrated model. MIS Q. 2003, 27, 51–90. [Google Scholar] [CrossRef]

- Yiu, C.S.; Grant, K.; Edgar, D. Factors affecting the adoption of Internet banking in Hong Kong—Implications for the banking sector. Int. J. Inf. Manag. 2007, 27, 336–351. [Google Scholar] [CrossRef]

- Mohammadi, H. A study of mobile banking usage in Iran. Int. J. Bank Mark. 2015, 33, 733–759. [Google Scholar] [CrossRef]

- Aldas-Manzano, J.; Ruiz-Mafe, C.; Sanz-Blas, S.; Lassala-Navarre, C. Internet banking loyalty: Evaluating the role of trust, satisfaction, perceived risk and frequency of use. Serv. Ind. J. 2011, 31, 1165–1190. [Google Scholar] [CrossRef]

- Aldas Manzano, J.; Lassala Navarre, C.; Ruiz Mafe, C.; Sanz Blas, S. Determinants of loyalty to online banking services. Cuad. De Econ. Y Dir. De La Empresa 2011, 14, 26–39. [Google Scholar]

- Gerrard, R.; Hiabu, M.; Kyriakou, I.; Nielsen, J.P. Communication and personal selection of pension saver’s financial risk. Eur. J. Oper. Res. 2018, 274, 1102–1111. [Google Scholar] [CrossRef]

- Sripalawat, J.; Thongmak, M.; Ngramyarn, A. M-banking in metropolitan bangkok and a comparison with other countries. J. Comput. Inf. Syst. 2011, 51, 67–76. [Google Scholar]

- Mortimer, G.; Neale, L.; Hasan, S.F.E.; Dunphy, B. Investigating the factors influencing the adoption of m-banking: A cross cultural study. Int. J. Bank Mark. 2015, 33, 545–570. [Google Scholar] [CrossRef]

- Lin, C.; Conghoang, N. Exploring e-payment adoption in vietnam and taiwan. J. Comput. Inf. Syst. 2011, 51, 41–52. [Google Scholar]

- Lin, M.; Prabhala, N.R.; Viswanathan, S. Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-to-Peer Lending. Manag. Sci. 2013, 59, 17–35. [Google Scholar] [CrossRef]

- Pope, D.G.; Sydnor, J.R. What’s in a Picture? Evidence of Discrimination from Prosper.com. J. Hum. Resour. 2011, 46, 53–92. [Google Scholar] [CrossRef]

- Zhang, J.; Liu, P. Rational Herding in Microloan Markets. Manag. Sci. 2012, 58, 892–912. [Google Scholar] [CrossRef]

- Chen, D.; Lai, F.; Lin, Z. A trust model for online peer-to-peer lending: A lender’s perspective. Inf. Technol. Manag. 2014, 15, 239–254. [Google Scholar] [CrossRef]

- Xia, Y.; Liu, C.; Liu, N. Cost-sensitive boosted tree for loan evaluation in peer-to-peer lending. Electron. Commer. Res. Appl. 2017, 24, 30–49. [Google Scholar] [CrossRef]

- Zhao, H.; Ge, Y.; Liu, Q.; Wang, G.; Chen, E.; Zhang, H. P2P Lending Survey: Platforms, Recent Advances and Prospects. Acm Trans. Intell. Syst. Technol. 2017, 8, 72. [Google Scholar] [CrossRef]

- Belleflamme, P.; Lambert, T.; Schwienbacher, A. Crowdfunding: Tapping the right crowd. J. Bus. Ventur. 2014, 29, 585–609. [Google Scholar] [CrossRef]

- Mollick, E. The dynamics of crowdfunding: An exploratory study. J. Bus. Ventur. 2014, 29, 1–16. [Google Scholar] [CrossRef]

- Ahlers, G.K.C.; Cumming, D.; Guenther, C.; Schweizer, D. Signaling in Equity Crowdfunding. Entrep. Theory Pract. 2015, 39, 955–980. [Google Scholar] [CrossRef]

- Burtch, G.; Ghose, A.; Wattal, S. An Empirical Examination of the Antecedents and Consequences of Contribution Patterns in Crowd-Funded Markets. Inf. Syst. Res. 2013, 24, 499–519. [Google Scholar] [CrossRef]

- Lee, E.; Lee, B. Herding behavior in online P2P lending: An empirical investigation. Electron. Commer. Res. Appl. 2012, 11, 495–503. [Google Scholar] [CrossRef]

- Zheng, H.; Xu, B.; Wang, T.; Xu, Y. An empirical study of sponsor satisfaction in reward-based crowdfunding. J. Electron. Commer. Res. 2017, 18, 269–285. [Google Scholar]

- Xu, B.; Zheng, H.; Xu, Y.; Wang, T. Configurational paths to sponsor satisfaction in crowdfunding. J. Bus. Res. 2016, 69, 915–927. [Google Scholar] [CrossRef]

- Cholakova, M.; Clarysse, B. Does the Possibility to Make Equity Investments in Crowdfunding Projects Crowd Out Reward-Based Investments? Entrep. Theory Pract. 2015, 39, 145–172. [Google Scholar] [CrossRef]

- Galak, J.; Small, D.; Stephe, A.T. Microfinance decision making: A field study of prosocial lending. J. Mark. Res. 2011, 48, S130–S137. [Google Scholar] [CrossRef]

- Boehme, R.; Christin, N.; Edelman, B.; Moore, T. Bitcoin: Economics, Technology and Governance. J. Econ. Perspect. 2015, 29, 213–238. [Google Scholar] [CrossRef]

- Barber, B.M.; Odean, T. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. Rev. Financ. Stud. 2008, 21, 785–818. [Google Scholar] [CrossRef]

- Kristoufek, L. BitCoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era. Sci. Rep. 2013, 3, 3415. [Google Scholar] [CrossRef]

- Polasik, M.; Piotrowska, A.I.; Wisniewski, T.P.; Kotkowski, R.; Lightfoot, G. Price Fluctuations and the Use of Bitcoin: An Empirical Inquiry. Int. J. Electron. Commer. 2016, 20, 9–49. [Google Scholar] [CrossRef]

- Ciaian, P.; Rajcaniova, M.; Kancs, D.A. The digital agenda of virtual currencies: Can BitCoin become a global currency? Inf. Syst. E-Bus. Manag. 2016, 14, 883–919. [Google Scholar] [CrossRef]

- Fry, J.; Cheah, E.-T. Negative bubbles and shocks in cryptocurrency markets. Int. Rev. Financ. Anal. 2016, 47, 343–352. [Google Scholar] [CrossRef]

- Bollen, J.; Mao, H.; Zeng, X. Twitter mood predicts the stock market. J. Comput. Sci. 2011, 2, 1–8. [Google Scholar] [CrossRef]

- Da, Z.; Engelberg, J.; Gao, P. In Search of Attention. J. Financ. 2011, 66, 1461–1499. [Google Scholar] [CrossRef]

- Preis, T.; Moat, H.S.; Stanley, H.E. Quantifying Trading Behavior in Financial Markets Using Google Trends. Sci. Rep. 2013, 3, 1684. [Google Scholar] [CrossRef] [PubMed]

- Kyriakou, I.; Mousavi, P.; Nielsen, J.P.; Scholz, M. Forecasting benchmarks of long-term stock returns via machine learning Open Access. Ann. Oper. Res. 2019. [Google Scholar] [CrossRef]

- Moat, H.S.; Curme, C.; Avakian, A.; Kenett, D.Y.; Stanley, H.E.; Preis, T. Quantifying Wikipedia Usage Patterns Before Stock Market Moves. Sci. Rep. 2013, 3, 1801. [Google Scholar] [CrossRef]

- Luo, X.; Li, H.; Zhang, J.; Shim, J.P. Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decis. Support Syst. 2010, 49, 222–234. [Google Scholar] [CrossRef]

- Tipu, S.A.A. Academic publications on innovation management in banks (1998–2008): A research note. Innov. Organ. Manag. 2011, 13, 236–260. [Google Scholar]

- Belleflamme, P.; Omrani, N.; Peitz, M. The economics of crowdfunding platforms. Inf. Econ. Policy 2015, 33, 11–28. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Malhotra, A. E-S-QUAL—A multiple-item scale for assessing electronic service quality. J. Serv. Res. 2005, 7, 213–233. [Google Scholar] [CrossRef]

- Barrutia, J.M.; Charterina, J.; Gilsanz, A. E-service quality: An internal, multichannel and pure service perspective. Serv. Ind. J. 2009, 29, 1707–1721. [Google Scholar] [CrossRef]

- Hendershott, T.; Jones, C.M.; Menkveld, A.J. Does Algorithmic Trading Improve Liquidity? J. Financ. 2011, 66, 1–33. [Google Scholar] [CrossRef]

- Kauffman, R.J.; Kim, K.; Lee, S.-Y.T.; Hoang, A.-P.; Ren, J. Combining machine-based and econometrics methods for policy analytics insights. Electron. Commer. Res. Appl. 2017, 25, 115–140. [Google Scholar] [CrossRef]

- Kaplan, A.M.; Haenlein, M. Users of the world, unite! The challenges and opportunities of Social Media. Bus. Horiz. 2010, 53, 59–68. [Google Scholar] [CrossRef]

- He, W.; Wang, F.-K.; Zha, S. Enhancing social media competitiveness of small businesses: Insights from small pizzerias. New Rev. Hypermedia Multimed. 2014, 20, 225–250. [Google Scholar] [CrossRef]

- Kauffman, R.J.; Riggins, F.J. Information and communication technology and the sustainability of microfinance. Electron. Commer. Res. Appl. 2012, 11, 450–468. [Google Scholar] [CrossRef]

- Freedman, S.; Jin, G.Z. Do Social Networks Solve Information Problems for Peer-to-Peer Lending? Evidence from Prosper.com; Elsevier: Amsterdam, The Netherlands, 2008. [Google Scholar] [CrossRef]

- Berger, S.; Gleisner, F. Emergence of Financial Intermediaries in Electronic Markets: The Case of Online P2P Lending. Bus. Res. 2009, 2, 39–65. [Google Scholar] [CrossRef]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Liu, D.; Brass, D.; Lu, Y.; Chen, D. Friendships in online peer-to-peer lending: Pipes, prisms and relational herding. MIS Q. 2015, 39, 729–742. [Google Scholar] [CrossRef]

- Jolliffe, I.; Hair, J.; Anderson, R. Multivariate Data Analysis with Readings. J. R. Stat. Soc. Ser. A (Stat. Soc.) 1988, 151, 558. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Number | Number of Records | Search Settings |

|---|---|---|

| #7 | 2877 | #6 Refined by: DOCUMENT TYPES: (Article) |

| #6 | 2990 | #5 Refined by: WoS CATEGORIES: (Management OR Business OR Economics OR Business Finance OR Communication) |

| #5 | 8910 | #4 Refined by: PUBLICATION YEARS (2008-2018) |

| #4 | 10743 | #3 OR #2 OR #l |

| #3 | 3615 | TS = (Internet Bank OR Online Bank OR Electronic Bank OR E-Bank OR Internet-Based Bank) |

| #2 | 3615 | TS = (Internet Banking OR Online Banking OR Electronic Banking OR E-Banking OR Internet-Based Banking) |

| #1 | 7649 | TS = (Internet Financ* OR Online Financ* OR Electronic Finance* OR E-Financ* OR Internet-Based Financ*) |

| Keywords | Number of Lines | ||

|---|---|---|---|

| Blue and Purple | Red and Green | Yellow and Orange | |

| Internet bank | 2 | 2 | 0 |

| E-commerce1 | 2 | 2 | 1 |

| Crowdfunding | 0 | 3 | 2 |

| P2P lending | 0 | 4 | 4 |

| Digital currency | 0 | 0 | 4 |

| Fintech | 0 | 0 | 4 |

| Keywords | Content | Reference | Citations1 |

|---|---|---|---|

| The influence of social network on crowdfunding | [20] | 48 | |

| Pricing | Pricing of crowdfunding advertisement | [21] | 20 |

| Auction | The role of auction in equity-based crowdfunding | [21] | 8 |

| Regulation | Regulation of cross-border crowdfunding | [22] | 6 |

| Equity crowdfunding | The impact of market regulation and agency risk | [23] | 4 |

| Entrepreneurship | The influence of moral ethics on crowdfunding | [24] | 4 |

| Mechanism design | Key point of designing crowdfunding mechanism | [25] | 1 |

| Reward-based Crowdfunding | Factors influencing the success of crowdfunding | [26] | 1 |

| Financial regulation | Difference between crowdfunding and illegal fundraising | [27] | 1 |

| Cluster ID | Cited Reference | Citing Reference | ||||

|---|---|---|---|---|---|---|

| Cites1 | Reference | Year | Coverage2 | Reference | Year | |

| #0 Mobile bank usage | 13 | [28] | 2009 | 17 | [32] | 2015 |

| 13 | [65] | 2010 | 12 | [36] | 2011 | |

| 12 | [18] | 2009 | 11 | [37] | 2015 | |

| #2 Internet banking loyalty | 31 | [29] | 2009 | 20 | [33] | 2011 |

| 14 | [30] | 2003 | 19 | [34] | 2011 | |

| 14 | [31] | 2007 | 14 | [66] | 2011 | |

| #1 P2P lending survey | 56 | [39] | 2013 | 18 | [44] | 2017 |

| 41 | [40] | 2011 | 12 | [67] | 2015 | |

| 36 | [41] | 2012 | 9 | [42] | 2014 | |

| #5 Reward-based Crowdfunding | 53 | [46] | 2014 | 30 | [25] | 2017 |

| 34 | [45] | 2014 | 18 | [50] | 2017 | |

| 20 | [48] | 2013 | 6 | [52] | 2015 | |

| #3 Price fluctuation | 11 | [56] | 2013 | 30 | [57] | 2016 |

| 10 | [54] | 2013 | 28 | [58] | 2016 | |

| 9 | [55] | 2015 | 4 | [59] | 2106 | |

| #7 Financial market. | 16 | [60] | 2011 | 30 | [62] | 2013 |

| 13 | [61] | 2011 | 22 | [64] | 2013 | |

| #4 E-service quality | 17 | [68] | 2005 | 30 | [69] | 2009 |

| #6 Policy analytics insight | 8 | [70] | 2011 | 26 | [71] | 2017 |

| #8 Small business | 13 | [72] | 2010 | 26 | [73] | 2014 |

| #10 Empirical investigation | 33 | [74] | 2012 | 6 | [75] | 2008 |

| Reference | Year | Strength1 | Begin | End | 2008–20182 |

|---|---|---|---|---|---|

| [76] | 2009 | 3.4235 | 2015 | 2018 | ▂▂▂▂▂▂▂▃▃▃▃ |

| [78] | 2015 | 2.7834 | 2016 | 2018 | ▂▂▂▂▂▂▂▂▃▃▃ |

| [79,80] | 2010 | 4.3255 | 2014 | 2016 | ▂▂▂▂▂▂▃▃▃▂▂ |

| [29] | 2009 | 3.5534 | 2015 | 2016 | ▂▂▂▂▂▂▂▃▃▂▂ |

| [77] | 2014 | 3.2422 | 2015 | 2016 | ▂▂▂▂▂▂▂▃▃▂▂ |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, X.; Yuan, J.; Shi, Y.; Sun, Z.; Ruan, J. Emerging Trends and Innovation Modes of Internet Finance—Results from Co-Word and Co-Citation Networks. Future Internet 2020, 12, 52. https://doi.org/10.3390/fi12030052

Li X, Yuan J, Shi Y, Sun Z, Ruan J. Emerging Trends and Innovation Modes of Internet Finance—Results from Co-Word and Co-Citation Networks. Future Internet. 2020; 12(3):52. https://doi.org/10.3390/fi12030052

Chicago/Turabian StyleLi, Xiaoyu, Jiahong Yuan, Yan Shi, Zilai Sun, and Junhu Ruan. 2020. "Emerging Trends and Innovation Modes of Internet Finance—Results from Co-Word and Co-Citation Networks" Future Internet 12, no. 3: 52. https://doi.org/10.3390/fi12030052

APA StyleLi, X., Yuan, J., Shi, Y., Sun, Z., & Ruan, J. (2020). Emerging Trends and Innovation Modes of Internet Finance—Results from Co-Word and Co-Citation Networks. Future Internet, 12(3), 52. https://doi.org/10.3390/fi12030052