1. Introduction

Driven by climate change [

1,

2], storms and other forest disturbances have increased in frequency in Europe in the last few decades [

3], especially in Northern and Central-Eastern Europe, where two storms per year have occurred on average from 1950 [

2,

4,

5]. Given the vast areas involved in numerous countries and the hundreds of millions of m

3 of windthrown wood (

Table 1), storms can have wide ecological and economic impacts on forest ecosystems and forest markets, as well as industry, community infrastructure and services [

4].

At the end of October 2018, the Vaia storm, an extraordinary event for the whole country, hit more than one million hectares of forests in Northeastern Italy and caused the loss of millions of m

3 of wood. Vaia was the largest storm ever recorded in Italy, as those occurring before had involved “only” hundreds of thousands of m

3 of wood (the great 1966 flood caused the loss of 700 thousand m

3 in the Province of Trento; hurricane Viviane felled 100 thousand m

3 in the northwestern area in 1990; a storm in Tuscany blew down 300,000 m

3 in 2015) [

2,

6,

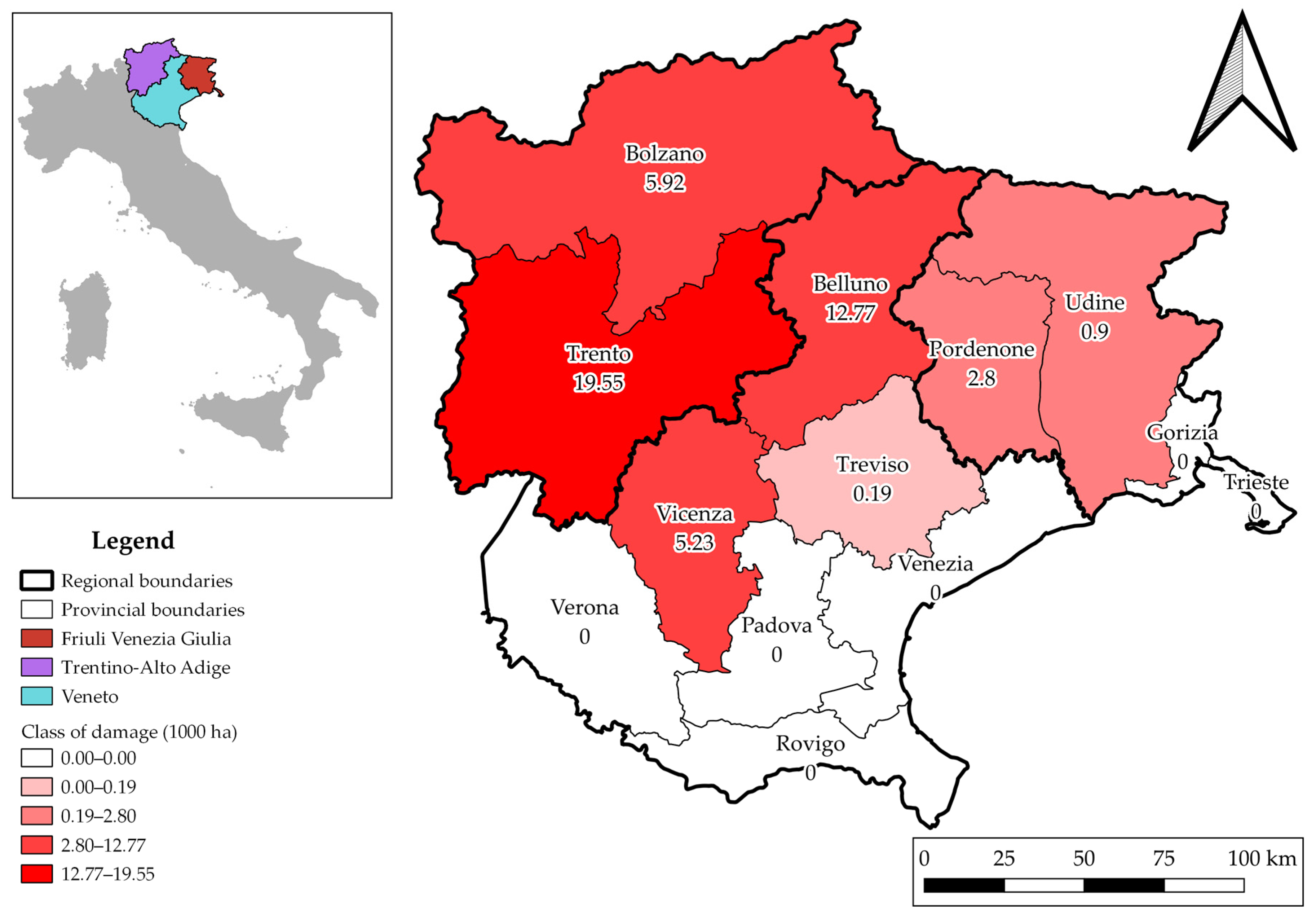

7]. In the most heavily impacted areas, i.e., the Provinces of Trento, Bolzano Vicenza, Belluno and Treviso, more than 34 thousand hectares of forests were blown over [

7,

8].

Figure 1 depicts the impacts of Vaia in the area.

Northeastern Italy is an important timber production and processing area. Around eight hundred and fifty forest logging companies operate here, buying and processing local woodlots or working as harvesting contractors for other companies. The roundwood market is mostly regional, and the buyers are local sawmills or woodworking companies (joineries, small furniture companies). The area trades roundwood towards the nearby Austrian and Slovenian borders, where larger timber processing capacities exist. Vaia overloaded the local markets with unprecedented quantities of roundwood, challenging the capability of forest owners to deal with large sales of windthrown material, of small logging companies to carry out salvage logging and of local authorities to provide adequate support for the process. Hence, expectations are that the impacts of Vaia disturbed or disrupted the existing market structures and forest value chains, as occurred with similar events in Northern and Central Europe.

Since their occurrence, forest storms have engaged forest economics researchers in efforts to assess their impacts and the factors affecting them. Gardiner et al. [

4] showed that the United Kingdom, France, Germany, Denmark and Sweden were the most impacted countries in Europe from 1950 to 2010. The higher vulnerability to storms of these countries is due to various factors, including a greater exposure to western winds, which are a major cause of storms in Europe, and the predominant coniferous composition of stands. Studies on the many facets of storm damage on European forests highlighted that economic impacts can be assessed through claims made against insurance [

9] or through reports on the removal of wood material and its destination published by regional and local authorities, while social impacts such as casualties or disrupted electricity supplies can be inferred from the media [

6].

Motta et al. [

2] explored the main factors explaining the damage provoked by Vaia and compared it to four other major storm events across Europe, showing that site and climatic conditions played a major role in this case: for example, the pure spruce stands of the Fiemme Valley in Trentino Alto Adige are historically susceptible to wind damage because of microclimatic and topographic conditions, and forest composition and structure. A new database of wind disturbances in European forests named FORWIND, also including data on Vaia, was published at the end of 2019 [

10], with information on more than 80 thousand spatially delineated areas disturbed by wind in the period 2000–2018. This database enables comparisons amongst storm events across Europe.

Windthrow events are typically followed by a fall in roundwood prices, with connected effects on procurement that can last months or even years [

4,

11]. Changes in price may depend on (1) the amount of windthrow timber; (2) the possibility to increase exports and reduce imports of roundwood; (3) the possibility to store roundwood; (4) the extent of utilization capacity in the local forest-based industries; (5) the price elasticity of demand and (6) the quality of salvage harvests [

11]. Gardiner et al. [

4], Schwarzbauer et al. [

11] and González-Gomez et al. [

12] studied price trends in spruce-dominated Central European markets, showing that the drop in price fluctuates in intensity and duration. Toth et al. [

13] showed that a larger quantity of calamity logging available on the market in respect to ordinary times affected the timber price drop in the Czech Republic. Nieuwenhuis et al. [

14] documented the same drop in Ireland following a storm in 1997. Eriksson et al. [

15] reported that in Sweden and Nordic countries, spruce sawlogs prices fell after the Gudrun storm in 2005 until the 2010s and did not regain ante-storm prices. Conifer timber is not the only wood affected by market price fluctuations; however, studying the dynamics of beech (

Fagus sylvatica L.) roundwood prices in Central European markets, Kożuch et al. [

16] found that yearly price variation was more due to political and economic instabilities (i.e., the economic crisis in 2008/09) than to extreme natural events. Regarding the quality of salvage harvest timber, the issue still remains widely uncovered across the literature for what concerns wood mechanical properties. More often, the timber quality issue has been connected to loss of timber value [

17], where damaged or broken stems result in trees which are less marketable than uprooted trees, even though they can be partially recovered depending on the point of breakage [

18]. In order to prevent quality loss but also to avoid pest attacks and fires, research has pointed out that, when stored and piled up, salvage timber needs to maintain high moisture content [

19] Wood decay is hence a function of various factors, including elevation and latitude, temperature, how long the wood has been in contact with the soil, soil composition and permeability and tree species [

20].

Studying the economic effects of storms on forest areas is essential to assess their overall impacts on society and markets. In particular, prices are important market signals as they affect local timber supply and demand. Therefore, identifying their variations, magnitude and trends over time will help to cast light on the conditions in which roundwood sellers and buyers operate in the years after the storm. These aspects have been studied in Northern and Central European areas, historically affected by storms, but very little is known on areas hit by large storms only in more recent times, such as Italy in the case of the Vaia storm.

The aim of this paper is to fill this research gap by taking stock of how the Vaia storm changed the availability of roundwood and affected its price in four local markets in Northeastern Italy. This area is important for the country, as it accounts for 40% of the total Italian forest area and 60% of national roundwood production; it is also a specialized secondary wood processing area, with 25 thousand enterprises and 100 thousand workers, including construction and furniture [

7,

21,

22].

The study focuses on spruce as the key economic species for the area and analyzes trends of roundwood prices in a time span ranging from September 2017 to December 2019. Vaia, which occurred at the end of October 2018, is the watershed event dividing the before-Vaia (bV) and after-Vaia (aV) periods. The research is exploratory as price series bV and aV in the four local markets are not fully available or complete. In fact, local roundwood markets in the area, and in Italy in general, are opaque: it is challenging to obtain information on timber prices, as most of the transactions occur through local negotiations and are not fully recorded or collected by the regional or central forest authorities.

2. Materials and Methods

2.1. Forest Characteristics and Timber Sale Modalities in Northeastern Italy

The area covered by the study includes the Italian geographical regions of Trentino-Alto Adige, Veneto and Friuli Venezia Giulia. The total forest and other wooded land area of these four regions covers 1.58 million ha (INFC2005), for the largest part classified as alpine forest, the rest as mountainous beech forest and thermophilus deciduous forest [

23]. The whole area was an active World War I conflict zone, which led to clearing of many forests in the 1915–1920 period. At the end of the war, the area was reforested, mostly with pure Norway spruce, considered the most suitable species for the context [

24,

25]. Since the last national forest inventory in 2005, the forest area in Northeastern Italy has increased by 36 thousand ha (INFC2015) [

7].

From the administrative perspective, forests in the area are controlled by four different administrative jurisdictions, with different authorities responsible for designing and implementing forest policies: (i) the Province of Trento; (ii) the Province of Bolzano (together, they form the Trentino-Alto Adige Region); (iii) the Veneto Region, and (iv) the Friuli Venezia Giulia Region. This administrative division dates back to the 1970s and, together with environmental, historical and socioeconomic conditions, is responsible for the differences in the development of the forest sector in the four areas, which can hence be considered four distinct local markets: in each one, buyers are mostly local logging companies or sawmills, which also process the timber locally. Thus, also the price dynamics occur mostly within the local market. However, it is not unusual that logging companies move from one market to the other, so some fractions of timber and other wood products also enter regional and supra-regional (Northeastern Italian) markets. In addition, as previously mentioned, the whole of Northeastern Italy, especially the Veneto Region and Province of Bolzano, also trade with Austrian and Slovenian sawmills.

Figure 2 reports details of forest and non-forest area for each jurisdiction (from now on, also called “local market” or “local areas”), showing a similar extent of forest area (a) but a different percentage of the total land area (b), with the Province of Trento being the most forested of the four.

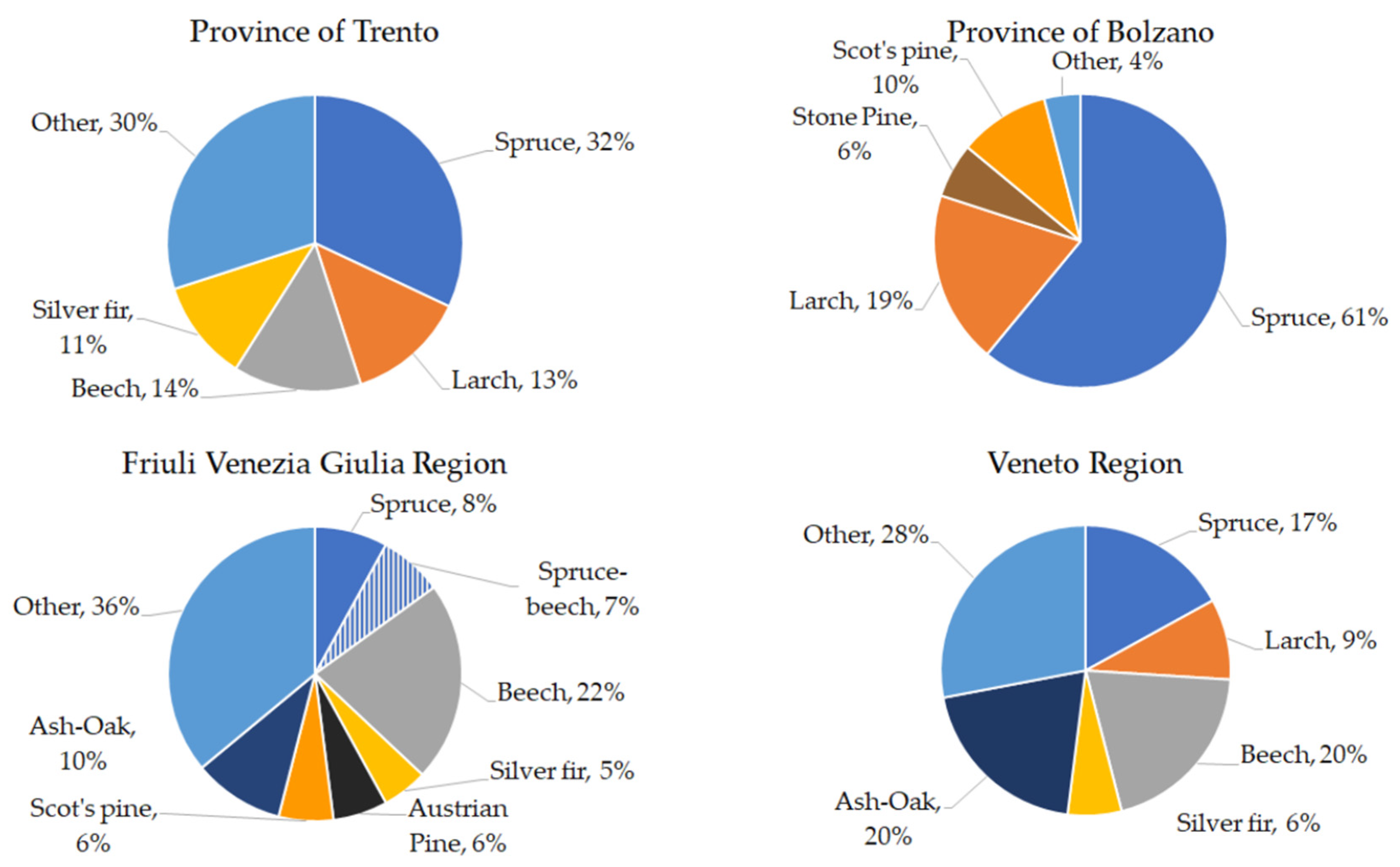

The forest composition includes a few main species: Norway spruce (

Picea abies (L.) H. Karst.), larch (

Larix decidua Mill.), silver fir (

Abies alba Mill.), stone pine (

Pinus cembra L.), Scot’s pine (

P. sylvestris L.), Austrian pine (

P. nigra Arnold), beech (

Fagus sylvatica L.), ash (

Fraxinus L. spp.) and oak (

Quercus L. spp.) [

7,

26,

27,

28]. Details for each jurisdiction are reported in

Figure 3, showing that spruce is the dominant species in the Provinces of Trento and Bolzano, with larch and other conifers also being well represented. In the case of the Veneto Region and Friuli Venezia Giulia Region, the forest composition is more diversified and has a higher presence of broadleaves. Indeed, both Veneto and Friuli Venezia Giulia include wide portions of flat and hilly land, where climatic conditions are more favorable to broadleaves, while Trento and Bolzano are wholly mountainous and with a continental climate more favorable to conifers.

Coniferous forests in Northeastern Italy tend to be typically unevenly aged and managed under a single-tree silvicultural system aiming for continuous forest cover, with harvesting periods within 10–15 years. Beech and other deciduous forests are instead managed under a shelterwood system with 120–140-year rotations.

Slopes in Alpine areas usually do not allow high levels of mechanization. On milder slopes (less than 30–35%) or smoother terrain, ground-based harvesting systems are preferred. With higher slopes and rough terrains, cable-based harvest systems are used for forest operations. Heavy forest machines such as harvesters and forwarders are generally not used, in favor of motor manual felling and delimbing by operator with chainsaw and transportation by skidding. According to FAOStat, in 2017, 2018 and 2019, Italy harvested, respectively 2212, 2206 and 7527 thousand m

3 of industrial roundwood. Although apparently showing the effect of Vaia in 2019, such data are estimates, based on models. Not many data are available at a more local level.

Table 2 reports recent data of increments and timber harvests and highlights the low harvesting rates that characterize Northeastern Italy forest management, well below the European average of 62–67%.

Regarding the type of ownership, the situation is heterogeneous (

Table 3): only in the Province of Trento does the share of public ownership (i.e., owned by the province and the municipality, the State having negligible forest ownership in Italy) largely exceed private ownership, whereas in the other local areas, private ownership prevails.

Forest owners in Northeastern Italy mainly sell wood by two different modalities: either standing or at the roadside. The first modality is used when owners do not have internal timber harvesting capacities: this often occurs with small public owners, including some municipalities and collective properties; the reference price is the stumpage price. The felling and harvesting operations are then undertaken by companies that buy standing timber, fell and harvest it and re-sell it at the roadside. The second modality is used when forest owners have internal harvesting capacities: this can be the case with large owners, who fell and harvest the wood with their own forest workers or through contractors and sell it to processors directly at the roadside or deposit (roadside or deposit price—from now on, “roadside price”). When the forest owner selling timber is a public owner, e.g., a municipality, the sale must occur through public auctions and auction notices that have to be made available publicly, sometimes also on the web. Other forest owners, e.g., collective properties or forest commons (community-owned forests), may also use public auctions for selling timber as a tool to increase local market competition.

2.2. Data

In order to take stock of the after-Vaia situation of local roundwood markets in Northeastern Italy, information on areas and timber volumes affected by the storm, quantity entering the market, number of sales and price trends was needed. The research relies on both secondary and primary data.

Full-scale secondary data on windthrow areas and volumes and shares of roundwood already harvested and placed on the market were extracted from official Vaia reports published by the forest authorities in the four jurisdictions. Two reports were available for the Province of Trento [

35,

36]; two for the Province of Bolzano [

37,

38] plus additional information from the 2019 annual report for agriculture and forest activities [

31] and additional specifications on 57 post-Vaia auctions [

39]; one report was available for the Veneto Region [

40]; no official reports were available for the Friuli Venezia Giulia Region, only some information from local newspapers [

41].

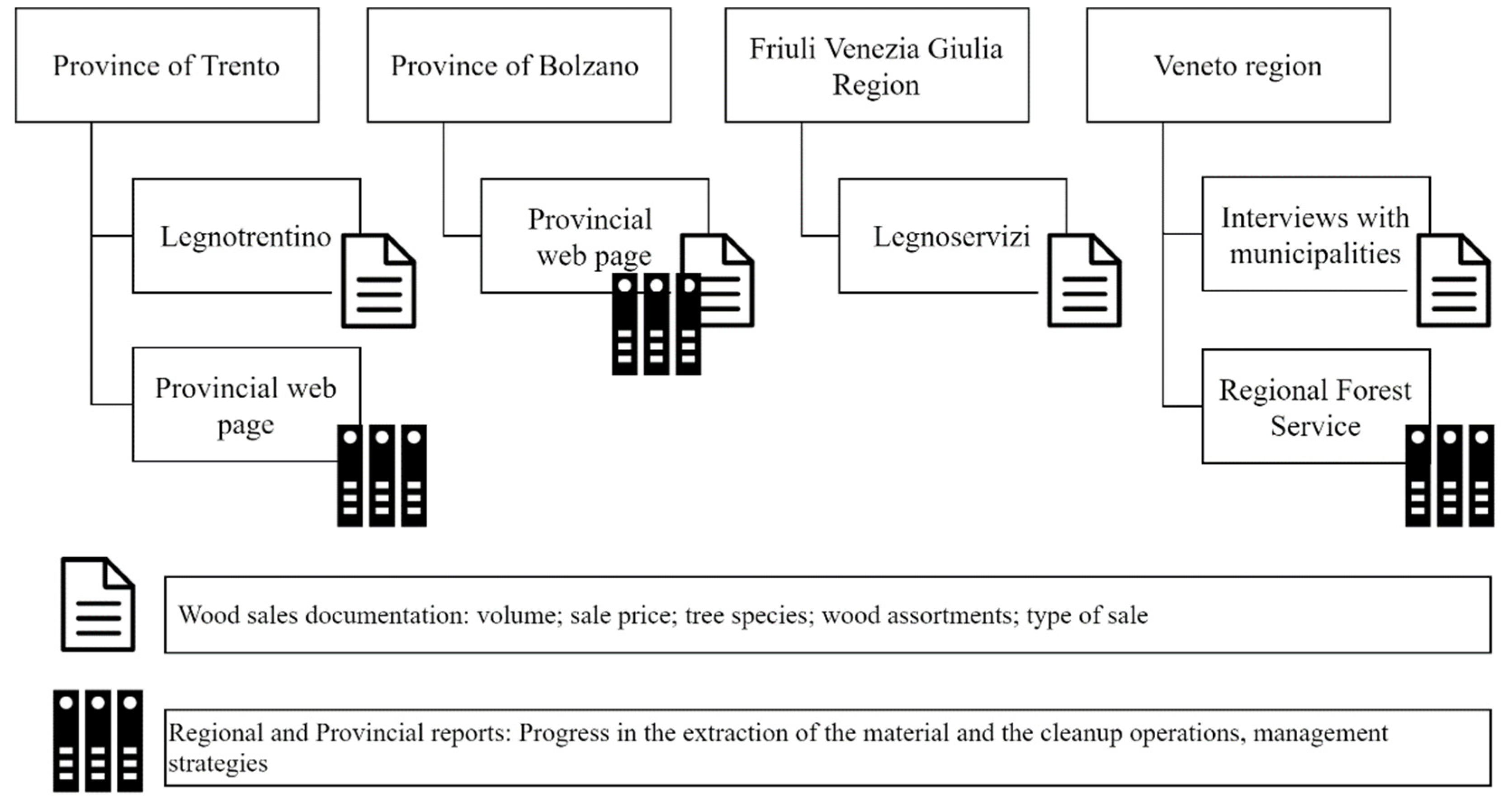

Primary data on number of wood sales and their volumes and prices in two periods—before-Vaia (bV) and after-Vaia (aV)—were then gathered on sales of municipalities or community-owned forests, for which public disclosure of sale data is mandatory. Different approaches and sources were used for the four local markets (

Figure 4):

Province of Trento: data were extracted from the web portal Legnotrentino (

www.legnotrentino.it (accessed on 23 October 2020)), an e-commerce initiative promoted by the Province of Trento since 2017 and open to forest owners willing to sell local timber online; the web portal deals with nearly all sales of public owners (province and municipalities) and is the main reference for timber prices in the Province of Trento. Its coverage of the local market is estimated at between 50 and 80% of all timber sold in the province [

42]. Data on 1345 sales were found and extracted (

Table 4).

Province of Bolzano: data were extracted from the web portal of the Bolzano Province (

http://www.provincia.bz.it/agricoltura-foreste/bosco-legno-malghe/legno/prezzi-del-tondame.asp (accessed on 23 October 2020)), existing since 2000 and performing the same role as Legnotrentino for the public forest owners of the Province of Bolzano (i.e., the province and municipalities). The coverage of the local market is more limited than for Trento, given that public forest owners only own 29% of the forest area. Data on 306 sales were found and extracted (

Table 4).

Veneto Region: no aggregate e-commerce market initiative is available; data were obtained through a web survey of wood auction notices published by individual municipalities and, when information was not available on the web, through direct interviews with municipal officers whenever possible. Clearly, this approach provided a partial picture of the timber sales in the Region before and after Vaia. Data on 85 sales were gathered (

Table 4).

Friuli Venezia Giulia Region: no aggregate e-commerce market initiative is available; the data were provided by Legnoservizi, a private company managing the wood sales on behalf of the regional authority since 2015. The data are systematically collected; hence, they provide a reliable picture of the situation; however, only data on total annual volume sold and annual mean prices per assortment are gathered.

For each individual sale, the information used in the analysis was:

date of the sale (to place it in one of the two periods, bV or aV);

volume of timber sold in m3;

species—whether spruce or other species (e.g., silver fir, larch, stone pine or beech);

wood assortment: we considered two groups of timber assortments, defined, for the purpose of the paper, as (1) “sawlogs”, namely roundwood which will be used to produce sawn wood, for boards, beams and veneer; the local standard measure for sawlogs is 4.20 m for length and 25–30 cm and above for diameter; (2) other less valuable assortments, which includes roundwood of smaller size used for pulpwood, fuelwood, wood for energy as well as packaging;

sale modality: whether stumpage or roadside/deposit;

price (€/m3), obtained by dividing the total sale value by its volume.

The analysis focuses on spruce timber assortments and compares the bV and aV trends. MS Excel was used for data computation and processing. Information on wood assortment and species was aggregated per each individual sale: spruce sawlogs (focus of the analysis) on the one hand and other less valuable assortments of spruce and other species on the other (from now on, “others”). The bV period was defined as from September 2017 to October 2018, while the aV from November 2018 to December 2019. In order to build spruce time series, mean monthly price was calculated as a basis for the trends by multiplying the adjudication price for the volume per each sale in a month; the products were summed and divided by the sum of the volumes sold in the month. Finally, an empirical assessment was attempted of the capacity of our survey to capture a good share of the aV market situation. This percentage indicator, labeled as “coverage of survey data”, was estimated by comparing the harvested (or sold) aV volume obtained from the survey with the harvested aV volume resulting from secondary data (official reports). The distribution of number of sales per area, species/assortment and modality is reported in

Table 4.

Descriptive statistics related to sales modalities were available for the Province of Trento, the Province of Bolzano and the Veneto Region; these are reported in

Appendix A as well as an ANOVA performed for the two series of the Province of Trento.

4. Discussions

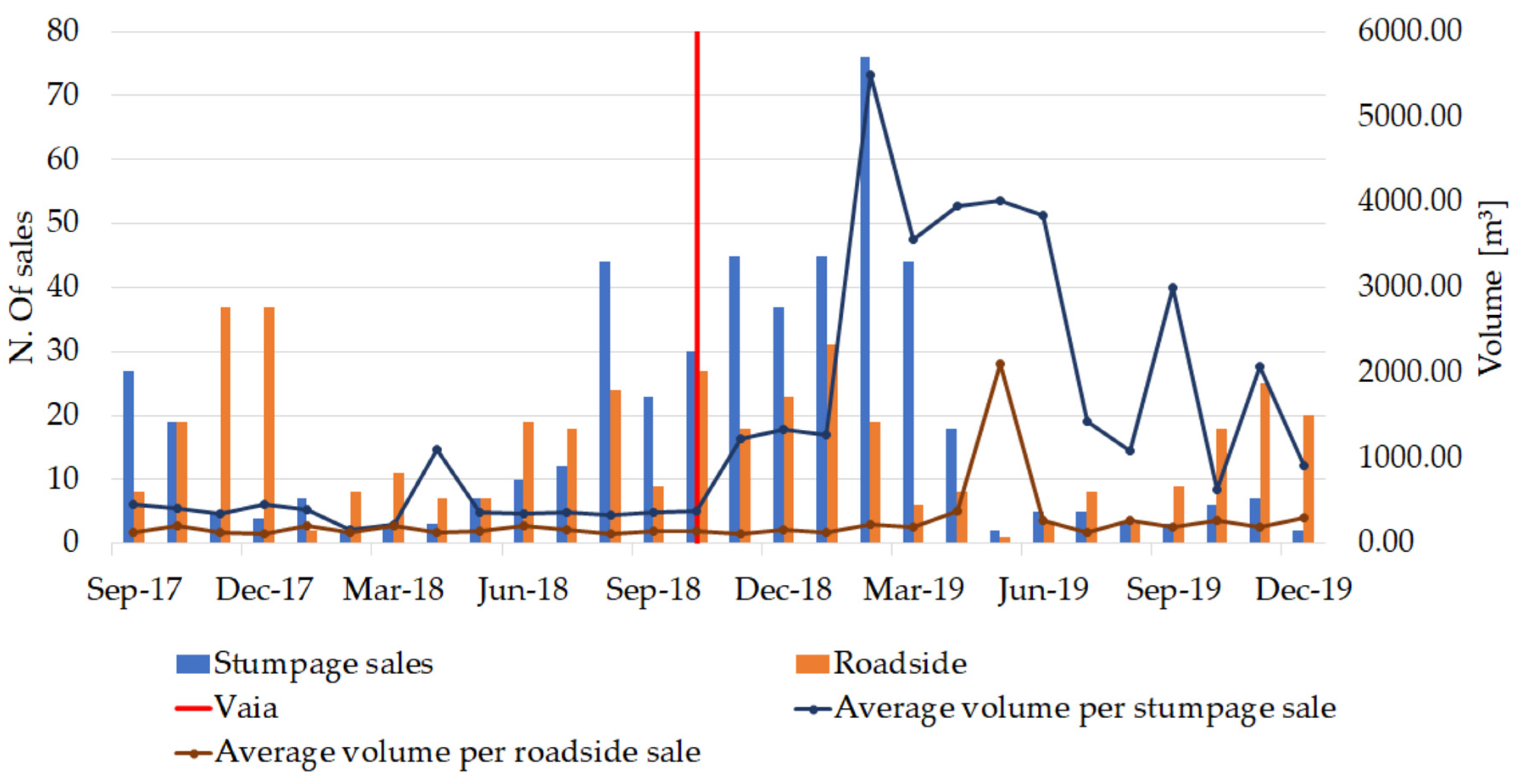

Results from the four areas confirm that Vaia had a strong impact on Northeastern Italy: according to our data, nearly fifty thousand hectares of forests were affected and more than nine million m

3 of wood were felled in total. This quantity is disruptive for the local markets, given that, according to FAO estimates, the total industrial roundwood production for the whole of Italy in the five years before Vaia fluctuated around 2.0–2.1 million m

3. Data from three areas out of four show that, if compared with ordinary forest management and harvesting, the number of roundwood sale events, the total volume and mean size of each sale increased in the fourteen months after Vaia. The increase in wood supply was accompanied by a decline in local roundwood prices. Although we cannot directly relate the decrease in price to the increase in quantity, as no analytical supply models were constructed, these results are in line with the findings of other research on storm-induced market changes [

4,

11,

12,

13,

14,

15]. Therefore, as occurred in Northern and Central European countries, we can expect that actors in the local wood chains will have to face both short- and long-term economic impacts in the years to come. Firstly, short-term impacts occurred because forest owners were forced to sell windthrown material at an average price instead of at differentiated roadside prices according to assortment types. This involved an immediate loss. Secondly, the literature has shown that storms yield medium–long-term effects that could lead to persisting market stagnation. We have no data beyond fourteen months after Vaia but could expect lower prices in the medium term until all the Vaia wood surplus has been cleared, sold and processed. In Austria and Germany, for example, the sawlog price index went down after 1990 and never again reached its initial values until the 2010s [

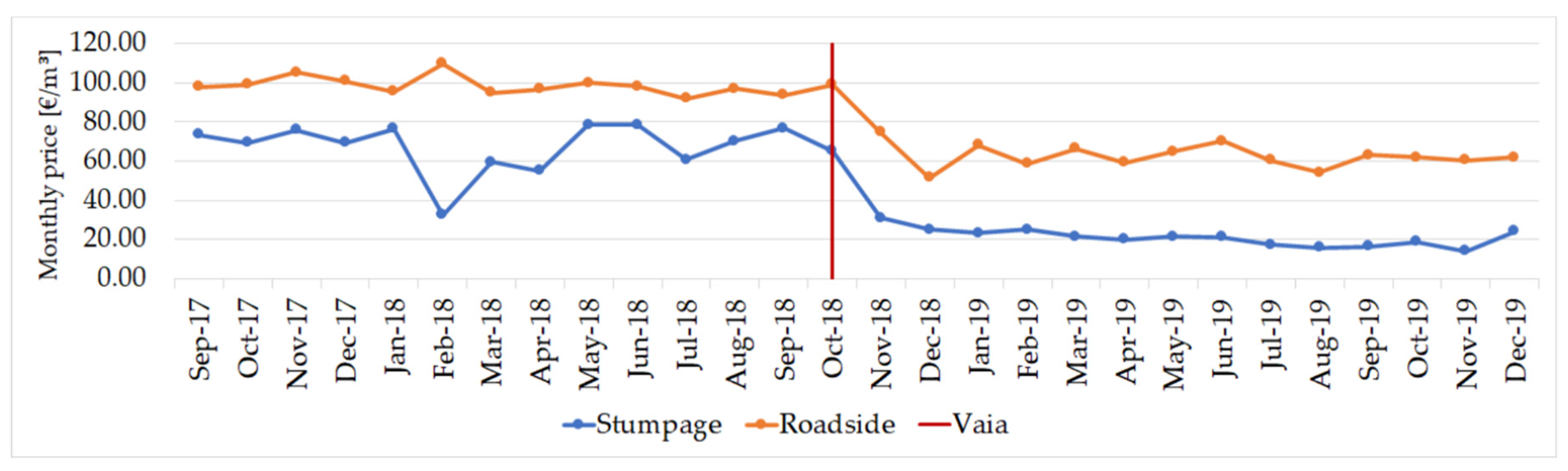

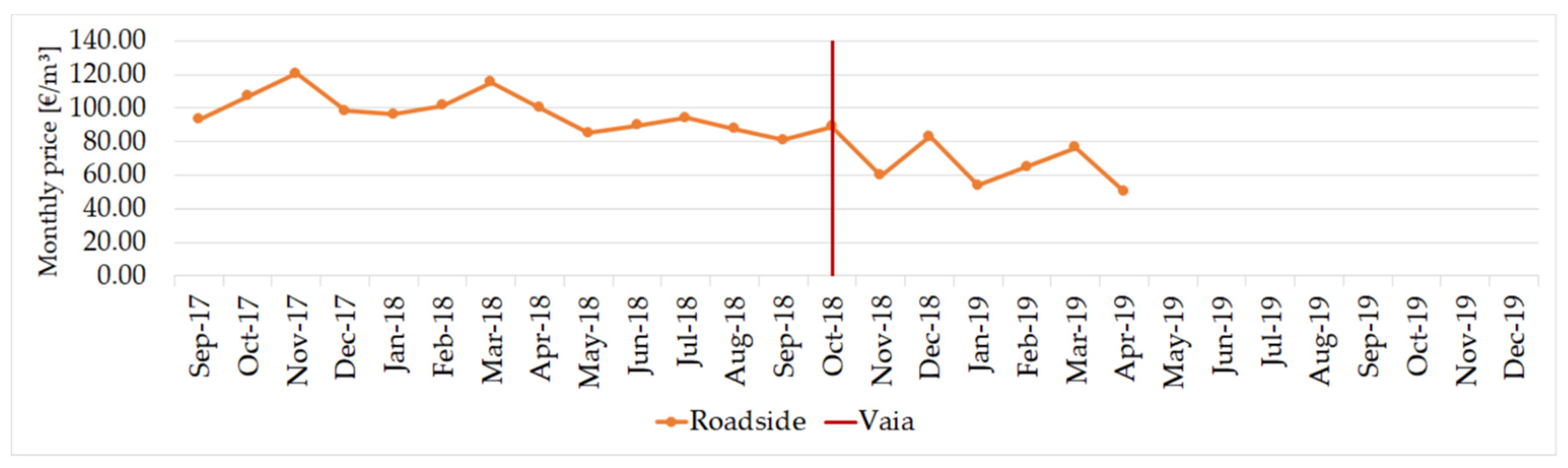

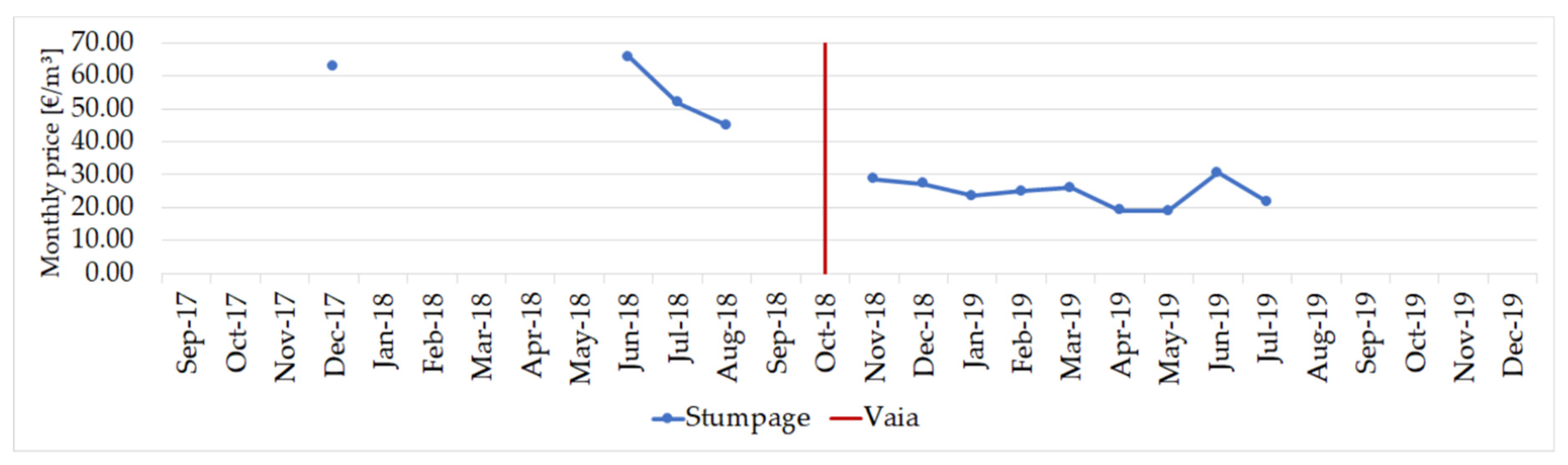

11]. Thirdly, in the long run, the effect of existing forest planning regulations also has to be taken into account. According to our estimates, Vaia forced forest owners to harvest a wood volume that, in the Veneto Region, is eighteen times larger than the volume of annual allowable cut. Hence, in order to allow recovery of the forest stocks, forest authorities may freeze authorizations for ordinary cuts even for decades, causing shortages of timber supply that might locally push up prices over several years, displacing local forest enterprises and possibly increasing import flows.

Although showing common trends, the survey data from Northeastern Italy revealed that the price and volume changes had different magnitudes and temporal distribution in the four local markets. This can be seen when comparing standing timber sale prices and roadside prices: the first sale modality has experienced a higher loss due principally to costs and duration of salvage operations. Those forest owners who could afford to pay for the salvage operations might have sold timber at the roadside to gain added value on the sale. The quantity of timber sold at the roadside was considerably lower compared to standing timber sales.

In line with Schwarzbauer and Rauch [

11], who have argued that the extent and direction of changes in prices after a storm depend on the combined and complex interplay of several factors and measures, the following aspects have emerged in the studied areas:

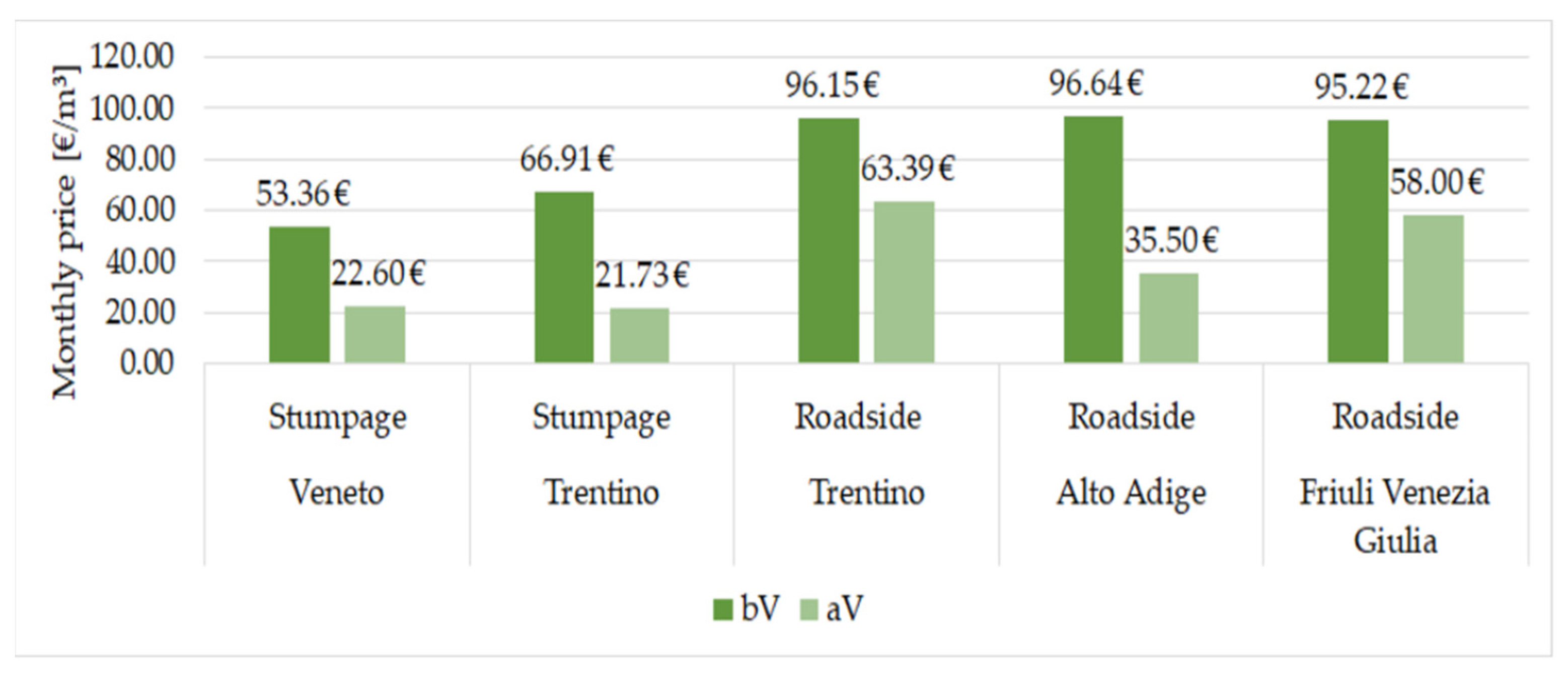

the quantity of surplus timber placed on the market: in Trento Province, Veneto and Friuli, the volumes increased and prices decreased accordingly; this is consistent with expectations; in Bolzano, a decrease in price occurred but did not seem connected with an increase in volume; in our view, this is because the volume data coming from the survey are partial and did not capture the majority of aV sales, which were by private forest owners;

the possibility to store roundwood: the forest authorities in the Province of Trento engaged actively in timber stocking areas: seventy-five new areas equipped with irrigation systems to maintain the wood quality were built by the end of 2019 [

44,

45]; this storage system helped to maintain the viability of the salvage wood [

19] but also allowed a timely and more regular placement of roundwood on the market and a better control of saturation effects;

the extent of utilization capacity by local forest-based industries: salvage loggings require specialized companies and yield returns to scale for medium-large enterprises. Local logging companies with suitable skills and size were available in the Province of Trento, where only one fourth of forest contractors involved in Vaia salvage logging came from outside the area [

36]. This local presence, together with the strict control by the local authorities on the respecting of contractual deadlines to clear the forest, contributed to successfully clearing and selling two thirds of the windthrown timber within two years after Vaia. This, combined with the stocking capacity, restrained the economic impacts on the market and minimized the risk of negative ecological impacts connected to pest attacks;

the possibility to increase exports of roundwood: unlike in the Province of Trento, there was not a sufficient local logging capacity in the Veneto Region; hence, the harvesting and clearing process relied mostly on external logging companies, also coming from abroad. Finding the logging companies and completing the contractual procedures required more time; hence, the clearing and selling process was slowed down, with the outcome that only one fourth of the windthrown timber was cleared (harvested) within two years after Vaia. This also resulted in a loss of value added from the timber processing, which was exported out of the region;

the quality of salvage harvests: as in other windfall events, only a certain proportion of trees were broken [

17], but still both broken and uprooted trees result in lower quality compared to ordinary yields [

18]; to compensate logging companies, several public forest owners in the Province of Trento offered them free harvesting of all the material smaller than 18 cm in diameter, which could be chipped and sold; this also minimized abandonment of wood wastes in the forests. However, in impacted areas at higher altitudes, the snow cover and presence in winter of 2019 and of 2020 contributed to maintaining the wood’s moisture content [

19], making it viable for a longer period;

the direct provision of financial support to forest owners: in all four areas, local authorities provided financial support to forest owners to carry out salvage logging, usually more expensive than forest harvesting operations. Funds from the 2014–20 Rural Development Program measures were used [

31,

38,

43,

46,

47];

other initiatives: after Vaia, municipalities in the four areas received emergency funds from the central government, which also offered support by civil protection personnel and machinery/equipment. Later, the State distributed funds from the European Solidarity Fund [

48]. Municipalities organized specific training for forest operators to strengthen their skills for working in the difficult the post-Vaia conditions. Crowdfunding campaigns were also promoted by the civil society [

49,

50].

Clearly, many of these factors and measures were aimed at different objectives than directly controlling price losses, i.e., clearing of the forests in the shortest time possible to minimize bark beetle attacks, securing safety of communities and infrastructure, ensuring access to areas for tourist purposes, restoring high value landscapes and supporting rural development in general. However, the interaction amongst them and with other local factors also possibly affected price trends. Our data cannot explain this, and counterfactual data are not available for the individual areas, but monitoring price trends also in the future and gathering more data would be worthwhile, in order to assess the specific effectiveness of some measures also on the roundwood markets.

5. Conclusions

The paper aimed at assessing how the Vaia storm changed the availability of roundwood and affected its price in Northeastern Italy by analyzing data in four distinct local markets. This was achieved by comparing roundwood price trends before and after the Vaia storm. The results estimated the economic impacts in terms of both roundwood availability and prices, showing declining trends in line with the literature.

A weakness of the work lies in the differences in the availability of longitudinal data on volumes, number of sales and prices for the four areas: more complete series were available in areas where timber prices are monitored continuously and stored on web portals, such as the Province of Trento and, to some extent, the Province of Bolzano. In contrast, data were scarce and fragmented for the other two areas, i.e., the Veneto Region and Friuli Venezia Giulia Region. Because of the heterogeneity of data, it was not possible to perform statistical analysis or modeling; hence, medium- and long-term effects and identification of factors and measures affecting them could not be directly inferred but only hypothesized based on the literature. Given this shortage of data, the work also contributes towards providing original information on the initial impacts of the Vaia storm in a systematic way at a large area scale.

The shortage of data in the area highlights the strategic importance of initiatives such as e-commerce platforms, including those in the Provinces of Trento and Bolzano. Not only do they support the development of competitive markets, but they also help to store fundamental information on volumes and price trends, which proves useful for dealing with future post-event market strategies. Indeed, both the Veneto Region (

www.portalelegnoveneto.it (accessed on 23 October 2020)) and Friuli-Venezia Giulia Region are today developing their own web portals. In the future, e-commerce initiatives should be developed not only at regional or provincial levels but also at interregional scale, which might help Northeastern Italy to emerge as a single market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}