1. Introduction

Since 2010, national and international government institutions responsible for producing economic statistics on environmental governance and economic development have been pointing to the need to incorporate the contribution of nature to the income and capital of nations, although to date, these concerns have brought about advances as regards environmental refinement in the application of the statistical office standard System of National Accounts (SNA) [

1,

2,

3,

4,

5,

6,

7,

8,

9,

10,

11]. One of the main challenges complicating the extension of the System of National Accounts (SNA) to explicitly incorporate the environment as an economic production factor is the consistency of the inclusion of values for products with and without market prices, when extending the SNA to estimate the real contributions of nature to the national product and social total income, as well as to evaluate the depletion and degradation of nature through government policy implementation. Another of the challenges regards the limits of environmental valuations in situations of ‘critical’ (threshold) amounts of renewable biophysical environmental assets.

In the SNA the net value added (NVASNA) of the economic activities does not include natural growth (NG) in the own-account gross capital formation (GCF) as a final product, and omits the environmental work in progress used (WPeu) from the intermediate consumption (IC). These omissions lead to a NVASNA bias associated with the timing of their measurement, which is avoided in this study by refining the standard System of National Accounts (rSNA), which includes their measurement in the NVArSNA.

The coordinated response of the governmental statistical offices to the demand for extending the indicator of SNA net value added (NVA

SNA), involves the development of the satellite System of Environmental Economic Accounting—Experimental Ecosystem Accounting (SEEA-EEA) [

12,

13] (currently in progress), with the aim of explicitly measuring the contributions of ecosystems services and environmental assets to the national product and income [

14]. Until now, the guidelines in the SEEA-EEA process have focused on the conceptualization of the economic variables of ecosystem services and environmental assets, based on the consumer preferences evidenced in the transactions observed in formal markets and other simulated transactions (using stated or revealed preferences methods). Nevertheless, “the SEEA-EEA (…) provides the first framing, from a national accounting perspective, for the integration of information on ecosystem services and ecosystem assets. This framing is (...) a general understanding of the logic and motivation for the valuation of ecosystem services. It is recognized, however, that the precise description of the relationships between ecosystem assets, ecosystem services and the associated production, consumption and balance sheet [capital account] information in the standard national accounts [SNA] is subject to ongoing discussion. (…) a more precise and commonly agreed framing is required to support discussion and exchange on this issue” [

15] (p. 11). This incipient development of the structure of SEEA-EEA accounts linked to the SNA makes it difficult to meet institutional demands for its implementation by national governments. The brief description of the sequence of SEE-AEEA and SNA accounts compared in [

16] does not permit a detailed discussion on what its future development might be. The most recent draft dealing with the design of the SEEA-EEA Model C proposes the ecosystem as an institutional sector composed of public products without registering manufactured costs [

16].

With respect to the SEEA-EEA, our Agroforestry Accounting System (AAS) incorporates the government institutional sector, and considers the ecosystem as a production factor and not as an institutional sector [

17]. The variable that is the backbone of the conceptual design of the AAS is the environmental income at social price.

The three methodologies, the SNA, SEEA EEA, and AAS, follow the same principle for valuing the final products of the economic activities according to the observed transaction price in formal or simulated markets. The SNA can be applied to any economic and spatial unit, although it is only currently applied by governments at scales larger than corporate scale, usually at regional territorial scale and more generally at a national scale. The SEEA-EEA is a system of accounts which is not currently normalized since it is still under development. The novelty of the SEEA-EEA is that its design is expected to be applicable for any given scale, ecosystem type, and ecosystem services of individual products from each type of ecosystem. The AAS can be applied to any economic unit, special unit, and type of ecosystem. In this study, we have limited the application to the rSNA and our extended AAS methodology integrates rSNA.

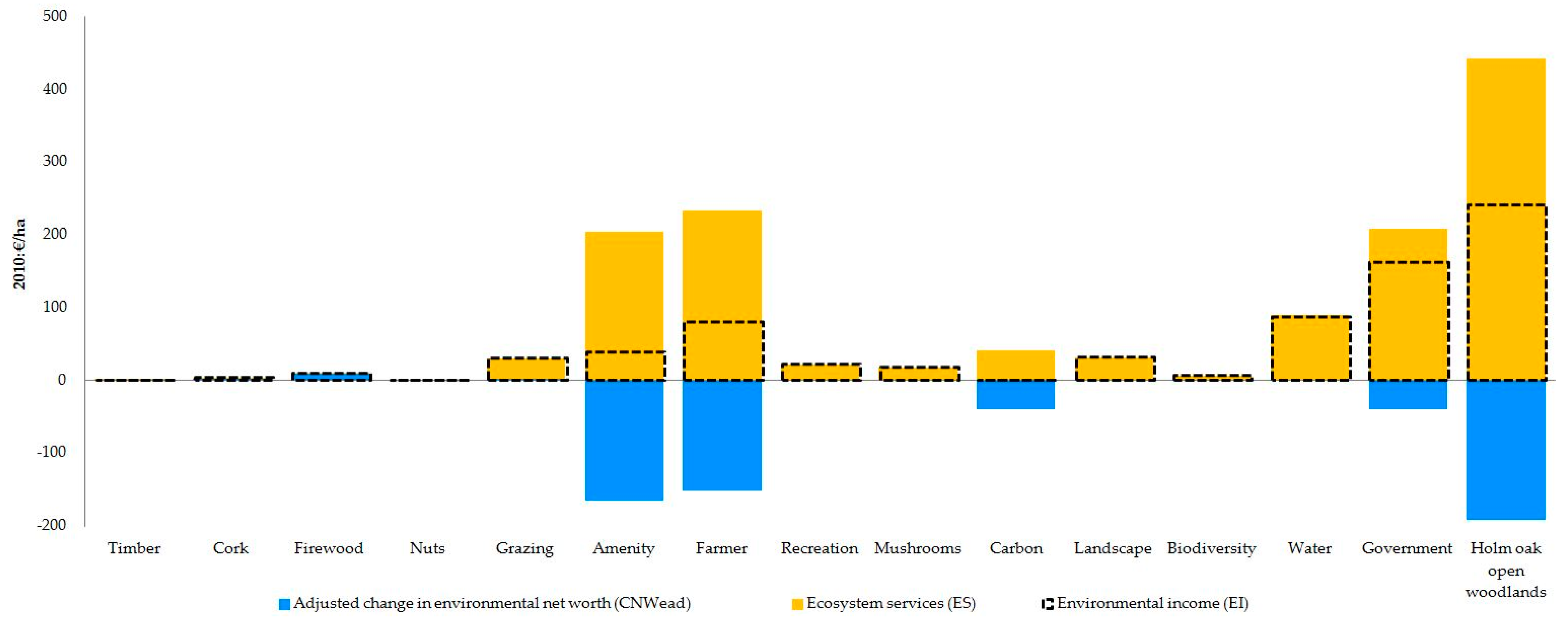

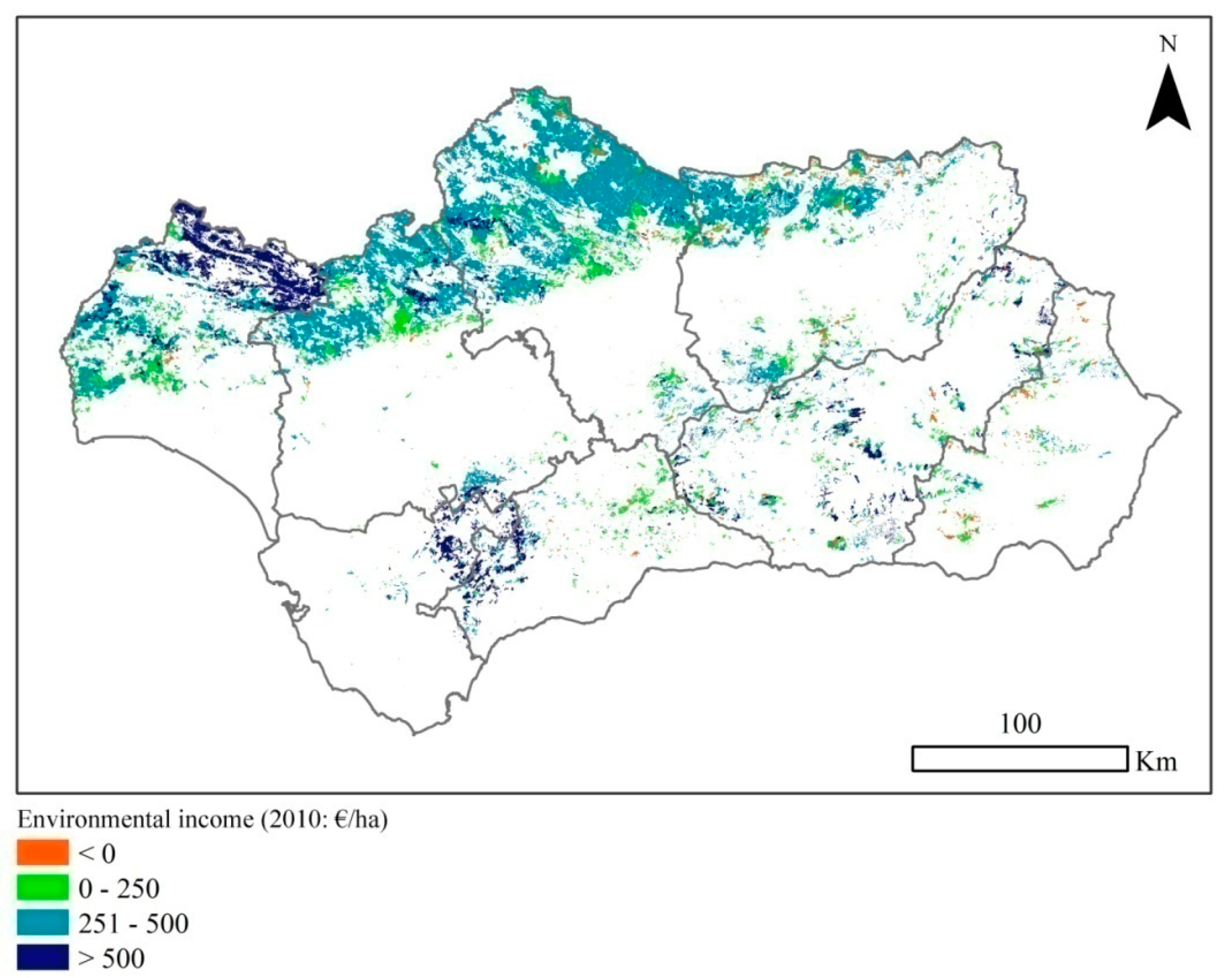

This study focuses on the comparison of the results for rSNA and AAS environmental incomes measured in the holm oak open woodlands (HOW) of the region of Andalusian-Spain (for detailed descriptions of institutional, physical and yielding characteristics of Spanish and Andalusian HOW see

Supplementary Materials Text S1,

Tables S1 and S2 and [

18]). The rSNA net value added (NVA

rSNA) modified the NVA

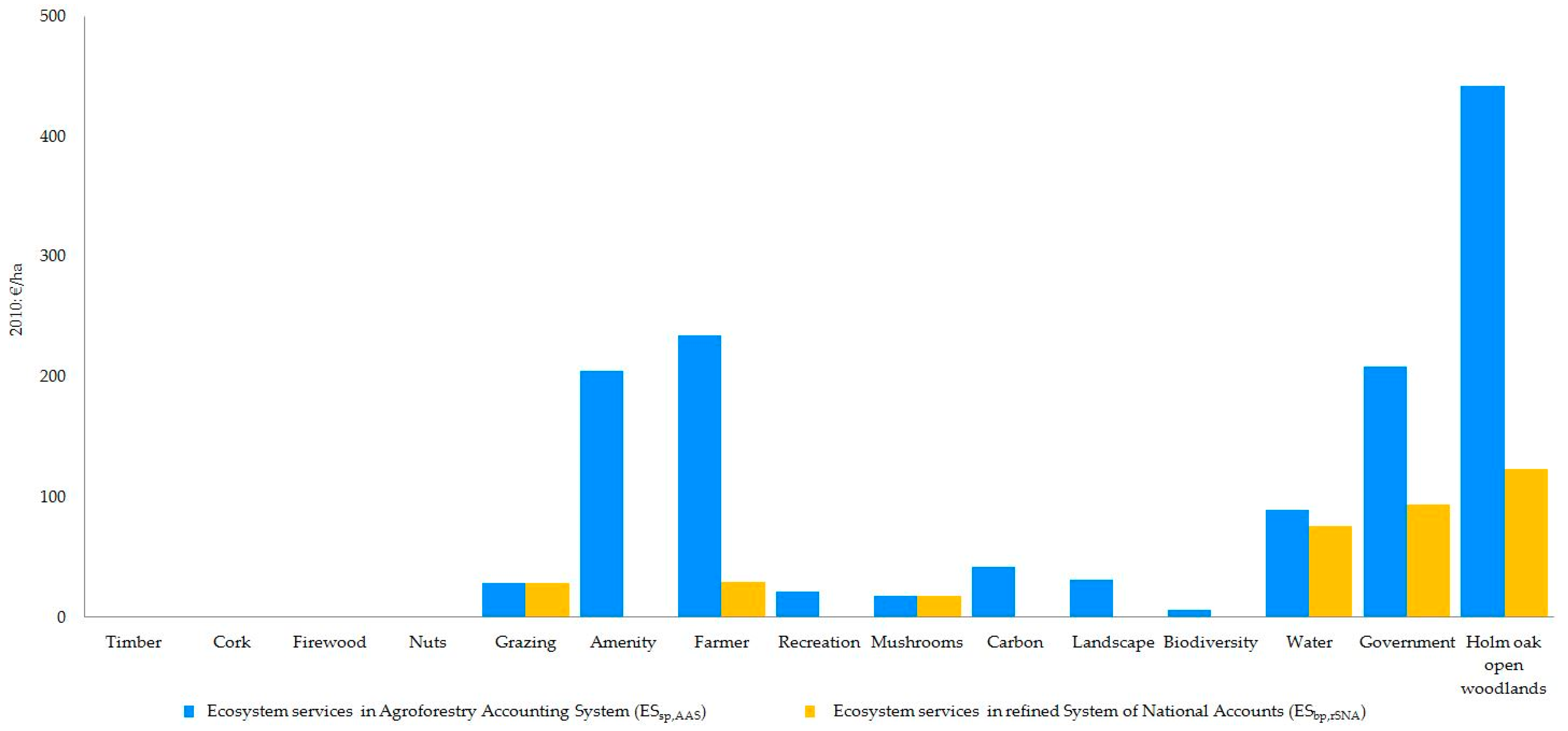

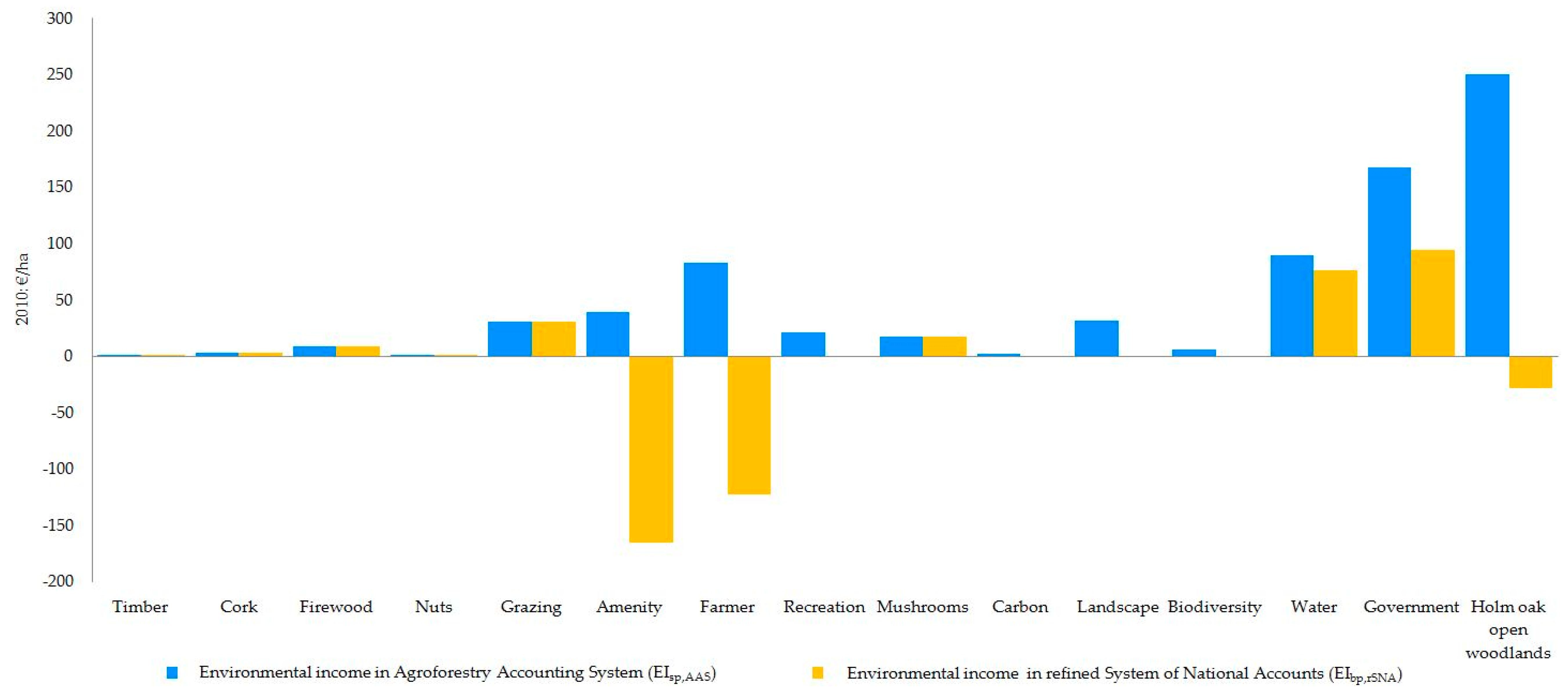

SNA by uncovering natural growth (NG) and environmental work in progress used (WPeu). In the AAS and rSNA methodologies, the changes in the environmental assets are explicitly incorporated in the environmental income estimates for the economic activities valued in the Andalusian HOW, except forest carbon activity, which is omitted in the rSNA. The HOW economic activities measured using the AAS and rSNA, produce 12 and 8 environmental incomes respectively.

The AAS and rSNA methodologies were applied to the measurement of environmental income at regional scale (Andalucia), measuring that of forests and other forest lands (including natural grasslands) at producer price [

17], cork oak (

Quercus suber L.) open woodlands at social price [

19], and that of holm oak

dehesa case studies (farm scale) at social price [

20]. This study focuses on a comparison of the applications of the AAS and rSNA to estimate gross and net value added, ecosystem services, changes in environmental assets, total income, and environmental incomes at basic and social prices in the Andalusian HOW at regional scale. The individual economic activities valued are those which are privately-owned by farmers—namely, timber, cork, firewood, nuts, grazing (by game species and livestock), conservation forestry, landowner residential services, and private amenities—along with those which are publicly-owned by government in the form of collective ownership—namely, fire services, water supply, mushrooms, forest carbon, free-access recreation, landscape conservation, and threatened wild biodiversity preservation (see activities conceptualization in

Supplementary Text S2). The residential, conservation forestry and fire service economic activities do not use products and services from the environmental assets production factors.

The concept of social price refers in this study to the incorporation (with the valuation at producer prices) of the ordinary own non-commercial intermediate consumption of services: amenity auto-consumption (SSncooa) and donation (SSncood) imputed to the HOW amenity and landscape activities. These SSncooa/d come from the non-commercial intermediate product of services generated by amenity auto-consumption (ISSnca) and donation (ISSncd) associated with the HOW hunting and livestock activities omitted in this study.

The AAS and rSN,A applied to the HOW, coincide with regard to the estimated physical quantities for the economic activities, except that the rSNA omits the forest carbon activity. They differ in terms of prices of the ordinary final products without market prices (private amenities, public recreation service, landscape service, and threatened wild biodiversity service), the valuation of the NVArSNA at basic price and the NVAAAS at social price.

The term environmental income has been employed previously by other authors without measuring the changes in environmental assets in the context of family-scale subsistence economies as a synonym of resource rent in [

21] (p. 53), and also assimilated to the gross value added in the absence of opportunity costs of self-employed labor and either null or token employment of manufactured capital [

22] (p. 41). Our concept of environmental income refers to the ‘gifts’ of nature that accrue from ecosystem services and adjusted change in environmental asset, integrated consistently into the estimate of social total income of the HOW accruing from the individual activities valued. The valuation of the ordinary environmental net operating margin (NOMeo), conditioned to the priority of remuneration for labor cost and ordinary manufactured net operating margin, allows the consistent integration of the environmental incomes (EI) measured by rSNA (EI

rSNA) in the AAS (EI

AAS.). As with the total income (TI), the environmental income comprises a residual term of the production account, the NOMeo, and another residual term of the environmental asset account; namely, the environmental asset revaluation (EAr) for the period. In order to overcome the shortcomings of the official SNA, the measurement of these two environmental income components is key when applying the rSNA and extended AAS accounting frameworks.

The measurement of total income (TI) and its factorial distribution follows an order of priority which conditions the remuneration of the three conventional production factors, namely labor, manufactured capital, and environmental asset. The order of priority for remunerations of the production factors in the first possible transaction of a total product consumption (TPc) of an activity is assumed to be: ordinary labor cost (LCo) first, ordinary manufactured net operating margin (NOMmo) second, and ordinary environmental net operating margin (NOMeo) third. The residual remuneration of the NOMeo of nature-based activities in the last position implies that the values cannot be negative. The government voluntarily renounces the remuneration of the ordinary manufactured net operating margin (NOMmoG) of the immobilized manufactured capital in the public activities. From these pre-conditions it can be deduced that the ecosystem services cannot contain negative values (ES ≥ 0), given the positive values for products of environmental work in progress used (WPeu). Consequently, the rSNA ordinary manufactured net operating margin (NOMmorSNA) of the private amenity activity and public activities can only present values equal to or less than zero. We assume that public consumers with free access to recreational services and gathering of wild products do not incur manufactured costs.

Among the conceptual advances of the AAS with respect to the rSNA is the fact that the valuation of individual products is presented at social price, when they are affected by the ordinary own non-commercial intermediate consumption of services of private amenity auto-consumption (SSncooa) and donation (SSncood) by HOW activities which are used as inputs to the private amenity and landscape services activities. In our HOW, the rSNA application is made possible thanks to the availability of our own data on full-cycle biological natural growth of the holm oaks and other tree species associated with the predominant holm oaks at tiles scale. However, our slight modification in the rSNA does not affect the value of the final products consumption recorded by the SNA, although it does affect the durable products accumulated in the production process due to the incorporation of natural growth for the period, and it also affects the net value added for the period due to the incorporation of woody products extracted of timber and firewood (WPeu) in the intermediate consumption. This study’s two most significant practical innovations are the measurement of the theoretical concept of capital gain (omitted in the SNA), to be added to the net value added, thus obtaining the social total income in the rSNA and the environmental income estimate linked to ecosystem services and adjusted change in environmental net worth (CNWead).

The applied contribution is to compare rSNA and AAS, in order to show that the former does not record the totality of the economic value of the activities measured and that it omits others. This is the case for the forest carbon activity, as the other 14 activities compared are the same, after our refinement of the standard SNA. The results confirm that the rSNA, by conceptual definition, cannot measure ecosystem services and environmental assets of the products without market prices. The comparison demonstrates that the scientific knowledge exists to avoid the failure of the market to measure the economic contribution of nature to the total income of the period, and we present the results of our AAS compared with the rSNA for the same variables and the same type of ecosystem, in this study, the holm oak open woodlands of Andalusia.

The physical sustainability of the HOW is forecasted based on scheduled future natural/induced regeneration. The biological cycles are as prescribed by forestry legislation on the management of Quercus genus species in Andalusia and felling of holm oaks is only permitted where there is a government authorized land use change. Commercial harvesting rotations are not regulated in the case of conifers and broadleaf timber producing species (eucalyptus and poplar mainly) and management plans for these species include stand persistence without land use change, except where unforeseen destruction occurs (e.g., catastrophic forest fires).

Although the landowners are not obliged to replant the trees, we assume that the scheduled future conservation silviculture applied will renew the current area (tiles) of woodland in Andalusia where holm oak woodland predominates [

17,

23].

The environmental incomes from the total products valued by the AAS at social price represent the scheduled sustainable economic contributions of management by farmers and government of the environmental assets of the Andalusian HOW. A valuation of the environmental assets at the closing of the period is assumed to correspond to the forecast regeneration of the trees in the current area over the complete biological/commercial cycle, along with the absence of any loss of currently threatened wild biological species. Under these conditions, the ecological sustainability of future management of the HOW is integrated into the expected results for the future resource rents.

The AAS and rSNA applications are based on information from land use tiles of the third National Forest Inventory for Andalusia and the Forest Map of Spain [

24], showing a predominance of holm oak open woodlands (HOW). The HOW predominate in 22,281 tiles of the Forest Map of Spain (FMS), which covers an area of 1,408,170 hectares (see

Supplementary Text S1,

Tables S1 and S2 and [

18]).

The physical data on estimated flows and stocks are for the year 2010. We have omitted the hunting and livestock activities from those valued in the holm oak open woodlands (HOW) as regional scale information was not available. For explanatory purposes we have included the SSncooc/a/d, where c is government compensation, a is private landowner amenity auto-consumption, and d is public landowner donation for the omitted hunting and livestock activities, which we assume to have been used by the HOW amenity and landscape activities valued.

In this application, we do not take into account the existence of a contractual right/liability of the owner for improving/maintaining the threshold of a given natural asset at the closing of the period. Thus, no loan/debt is generated for the increase/loss of natural assets derived from the economic activities and hence the net worth of the HOW does not comprise financial assets.

There are both private and public owners of the land, with different economic rationales. We assume that the economic rationale of the private owners includes auto-consumption of private amenities. It is accepted that the production function of the private amenity and landscape activities uses the ordinary own intermediate consumption of services (SSoo). They are composed of ordinary own commercial intermediate consumption of services consumption of services compensation (SSncooc), amenity auto-consumption (SSncooa), and donation (SSncood). The government fire service activity and the private landowner residential and forestry conservation activities supply commercial intermediate product of services (ISSc). The omitted hunting and livestock activities produce non-commercial intermediate products of services compensation (ISSncc), amenity auto-consumption (ISSnca), and donation (ISSncd). The latter is originated from the public landowner activities. In the HOW, these three ISSnc are generated by the hunting and livestock activities.

The government is the owner and manager in representation of the collective public activities. In the HOW, the public activities are those which are regulated and managed by the government, providing free consumption of the final products to both active and passive consumers. The economic rationale of the government implies registering ordinary own non-commercial intermediate consumption of services compensations (SSncooc) and donations (SSncood) in the public activities that use them, in this study, they are used by the landscape activity. The government is able to accept voluntary negative values in recurrent periods for the ordinary manufactured net operating margin (NOMmo) of a public activity. The main logic for the conservation of a unique biological variety in danger of extinction, based on the concept of valuing the existence of a unique genetic variety which is not industrially reproducible, is a governmental precautionary behavior. However, the omission of current consumer preferences is not complete because democratic governments must consider the tolerable social cost of avoiding the nature variety irreversible loss. Nevertheless, there is a general consensus on the diverse rationales for the integrated conservationist management of the HOW among the economic actors, as reflected in the following quote: “From a production perspective, always effected in a way that focuses on restoring the balance between environment and business [sustainable management] (square brackets are not in the original text), allowing a profitability which facilitates reinvestment in the environment (...), actively organizing the maintenance of the natural scenario in which we carry out our agroforestry activity, with the certainty of achieving the economic return for our labor” [

25] (p. 10). Although, in principle, all the actors accept this conservationist perspective, controversy arises among the owners, the government and the consumers when attempting to put into practice their perceptions on the concepts of economic profitability and environmental asset conservation. We are faced with numerous subjective interpretations when attempting to apply sustainable management of renewable natural resources in a way that is coherent with ecological and economic sciences.

Section 2 summarizes the AAS and rSNA accounting frameworks applied to holm oak open woodlands.

Section 3 describes and compares the main environmental economic results obtained from the application of the two accounting frameworks to the Andalusia HOW.

Section 4 discuss the key findings and policy implications of applying the extended AAS to overcoming the standard SNA nature hidden contribution to total income in this HOW application.

Section 5 concludes with the major results, findings, and policy challenges.

4. Discussion

4.1. We Cannot Consume the Ecosystem Services but Rather their Ordinary Final Product

In this study, as regards the economic analysis of ecosystem services we have referred exclusively to the renewable products appropriated by farmers and the government. It is accepted that the economic production functions can only employ inputs (intermediate consumptions) and cost of environmental asset use (natural) being their physical contribution sufficient for their inclusion [

17,

30]. Capital use cost is defined in this case as the sum of the fixed capital consumption and the normal income from capital invested in the ordinary final production. Consequently, the economic analysis of the ecosystem services goes beyond their economic value and from our perspective, the final product consumption is at the center of the analysis of the contribution of nature to the value of the nature based products consumption.

The production functions of an ordinary final product in the SNA ignore the zero price natural inputs but in contrast, admit the residual values, regardless of sign, for net mixed income and net operating surplus in a consistent manner. Thus, we can consider that it is consistent with the SNA methodology to take into account the zero value natural intermediate consumptions so as to make the physical quantities of the production factors consistent with their final products consumption. The fact that the ecosystem service is an income from the gifted natural resource (environmental asset) means that its residual economic value will be greater than or equal to zero (since the farmers and government do not incur manufactured production costs in their appropriation).

The SEEA-EEA implicitly accept that products without manufactured costs can be integrated in the economic activities since “the production boundary is expanded relative to the SNA reflecting that the supply of goods and services by ecosystems is considered additional production” [

12] (p. 88). Here, in order for the additional products to be valued consistently with respect to those of the SNA, the ecosystem institutional sector must only refer to government public products without manufactured costs.

The AAS maintains the dependency on the nature based ordinary final products, even where the resource rent is zero, since people enjoy the consumption of these products without knowing the remunerations of the production factors which contribute to their market or simulated price. In other words, we cannot consume the ecosystem service of an economic activity, but we can consume the ordinary final product to which it contributes physically and/or economically. It is inconsistent from the perspective of consumption of an ordinary product to conclude that “if no [resource] rent is earned [embedded], the concept of [net] value added will represent no more than that which could be earned in alternative employment, and will as such not reflect any dependency on the natural resource” [

22] (p. 41). The zero value of the resource rent does not nullify the ecological dependence, which makes it possible to obtain a manufactured net value added embedded in the value of the product consumption, the existence of which is only viable due to the physical consumption of the environmental intermediate input supplied by the ecosystem. This would be the case of grazing, if it is considered as an environmental input consumed by the HOW game species which, even though it has a zero transaction price. This gives rise to the existence of a resource rent for market transactions of game captures which, in the case of the HOW, allows us to match the resource rent for game captures to the value of the grazing consumption, and to the net value added due to the absence of manufactured costs.

The supply of stored water with commercial economic use is another example where the resource rent coincides with the value of the product in the HOW due to the absence of manufactured costs.

In the case of harvesting free access wild products, the net mixed income must be estimated and the factorial distribution of the net mixed income must be derived from the local markets and the motivation of the picker. In the HOW, the recreational mushroom pickers do not incur intermediate consumptions or cost for manufactured capital use, and it is assumed that they do not incur opportunity costs for the time employed on the visit; therefore, the values of the ordinary product, the ecosystem service, and the net value added coincide.

In all the examples described, there is a constant in the ecosystem service estimates for an individual product which consists of starting from the first possible transaction value of the ordinary product. This criterion is followed by the estimates of intermediate consumptions and the capital use cost, and finally the ecosystem service is estimated as a residual value. All types of relationship are possible among the values of the product, the ecosystem service resource rent and the net value added, but all equivalence must be consistent with the concept of total income. In short, the existence of an ecosystem institutional sector is an instrumental construction, the justification for which lies more in political convention than a scientific necessity derived from the production function.

4.2. Ecosystem Service and Income Valuations: Producer versus Social Prices

In this study, the AAS methodology is applied to fifteen economic activities (hunting, livestock, and agriculture activities are omitted) at regional scale in holm oak open woodlands in Andalusia in 2010, with the novelty of comparing producer prices (market and simulated) and social prices. The results reveal notable overvaluations at producer prices in comparison to social prices of the net/gross added values of the private amenity and landscape economic activities, as well as of the aggregate farmer, government, and total HOW activities. The ecosystem services and the environmental income of the private amenity, along with their aggregate values for farmers and total for the HOW are affected. The results for the ecosystem services and the environmental incomes of the individual activities of the government are not affected by the change in the type of price used in the valuations.

The comparison of the results for the valuations of ecosystem services and incomes at producer price in the rSNA reveal notable undervaluation compared to the AAS estimates at social price. The differences revealed in the comparisons of environmental assets estimated by the AAS and rSNA are due to the valuation at production cost of the final products consumption without market prices in the rSNA and at simulated revealed/declared price in the AAS, as well as to the omission of the carbon activity in the rSNA.

4.3. Lack of Investment in Conservation Forestry in Holm Oak Woodlands

The commercial products of the HOW do not generally provide competitive monetary profits at producer (market) prices; the justification for the market price of the HOW can only be found in the auto-consumption of amenities (recreation) by non-industrial owners. In other words, the private family owners pay themselves the monetary opportunity cost of the production of amenity services auto-consumed exclusively in their properties, when they incur in voluntarily accepted monetary opportunity costs. The public administration also recognizes this economic value of the dehesa owner’s amenities. Spanish land law establishes that to buy or expropriate a rural property it is possible to pay up to a maximum of twice what it would be worth, if only the profits from its commercial exploitation are considered, since the legislators recognize that the other half of its market price corresponds to the benefit from the non-commercial flow of private amenities of the owner.

It is unusual for owners to invest in order to benefit the consumption of future generations without receiving government compensations, given that competitive profitability results are mainly due to the amenities, and these are not affected in the short and medium term by the current rate of degradation of the HOW taking into account the historical variations in the price of land [

29]. It is worth noting the modest investment in conservation forestry by a group of large private dehesa operations [

20]. The private owner prefers to invest in land and livestock, which contribute in the short to medium term to increasing the available monetary profitability [

29,

31,

32]. Plantations do not provide monetary benefits for the generation of the owner who undertakes the plantation. The high level of uncertainty associated with the generation of future profits from the plantation is the main factor underlying the uncertainty of the gain in net worth in the present for the future yield. However, the future owner who harvests the products of the historical plantations will be the beneficiary of the largest ordinary environmental operating margins, as the historical costs of the conservation forestry will have been amortized. In other words, the conservation of the HOW can be considered a public service, which is represented in this study by the landscape activity. In this context, the words of the editor of the influential publication ‘Our Common Future’ are of relevance with respect to the need for government to have consistent information on sustainable management and contributions of natural resources to the total income of the HOW when drawing up their policies: “Politics that disregard science and knowledge will not stand the test of time. Indeed, there is no other basis for sound political decisions than the best available scientific evidence. This is especially true in the fields of resource management and environmental protection” [

33] (p. 457).

4.4. Does the SEEA-EEA Provide Concepts for Measuring Environmental Income?

From our perspective of the conceptualization of ecosystem accounting, it is necessary to admit the nature-based government activities, both direct and indirect. It makes little sense that an economic rationale should be admissible in the case of farmer activities but not the government public activities affected in their management and regulations by manufactured costs. The SEEA-EEA criterion which refers to the fact that “the production boundary is expanded relative to the SNA reflecting that the supply of goods and services by ecosystems is considered additional production” [

12] (p. 88) is consistent from the perspective of including an ecosystem institutional sector only for public products consumption, without regulations and without government costs. In return, a debatable limitation is incurred; namely, the exclusion of the government sector which, in the case of the HOW, is an ecosystem service provider of similar importance to the farmers. Furthermore, it renders unnecessary the inclusion of a non-human institutional sector which provides free ordinary economic products to humans, independently of the farmers [

16].

Our response to the question that provides the heading to this section is that we cannot know whether the SEEA-EEA in their current incipient stage of development will include standard guidelines for the nature-based government activities as a whole. If they were not included, the SEEA-EEA would not be able to measure the environmental income of ecosystems of the type valued at a national level which are produced with government manufactured costs.

The debate concerning the conceptual design of ecosystem accounting has so far centered on the valuations of ecosystem services and their respective environmental assets derived from the prices of transactions observed in formal or simulated markets based on consumer preferences. Although a detailed development of the SEEA-EEA accounting structure is not available, the reference of [

16] (Table 6, p. 33) allows us to outline a provisional interpretation of the concept of extending the economic activities with respect to the SNA. These authors take into consideration the institutional sector of corporations (e.g., timber) and add the ecosystem public services produced without manufactured costs (e.g., air filtration). Should we understand, therefore, that the SNA valuation of public goods and services of nature-based government services is maintained at production cost and therefore the value of their ecosystem services is zero. This interpretation does not appear to be coherent, and we understand from what the authors state in the above cited reference that they are referring to an example of the application of the SEEA-EEA to two specific products, which cannot be generalized to embrace public products with manufactured production costs. It would also not make sense to present the values for products of the corporations and only the ecosystem services for the public products with and without manufactured production costs.

Since the purpose of the SEEA-EEA is to explicitly specify the valuations of the ecosystem services of ordinary individual products and their respective environmental assets, it can be concluded that the ultimate aim of the SEEA-EEA is the estimation of the environmental incomes of the individual economic activities valued for the ecosystem types of the spatial unit considered.

To date, the SEEA-EEA does not explicitly mention the environmental income of the ecosystems, but gives the measurements separately for the ecosystem services (ES) and the change in environmental asset (CEA) of the individual product. These two variables added together give the value of the environmental income, and depending on the specific accounting conventions of the environmental production and balance accounts, the CEA is adjusted in the case of certain individual products in order to give the adjusted change in environmental net worth (CNWead) according to the environmental work in progress used (WPeu), as we have shown in

Section 2 and

Supplementary Text S3. Thus, we arrive at the general expression of the environmental income (EI) as the sum of the ES and the CNWead of the individual product. All the information that we require to measure the environmental income is provided by the variables ES and EAg proposed by the authors of SEEA-EEA discussion papers ([

16] Table 6, p.33, [

34] Section 4.1, pp. 20–23). Other authors also implicitly estimate the environmental income, the value of the environmental assets depending on the discounted benefits (ecosystem services) and the capital gain (change in environmental asset) [

35,

36].

We can simplify the definition of the concept of environmental income as the value of the ecosystem service of a stationary state nature-based activity, given that in this situation the value of the CEA/CNWead is zero. Beyond the stationary state of the ecosystem activity, the EI represents the maximum possible consumption of the ES of the individual ecosystem product which we can permit without reducing its value at the opening of the period.

It seems strange that no SEEA-EEA applications have so far been produced by other authors which include measurements of ecosystem services for one or various ecosystem types and the respective changes in the environmental assets of the products incorporated in a single indicator such as the environmental income of the ecosystems and which is integrated in the standard SNA at national/regional scale. In [

18], a simplified AAS application is presented comparing the results with our refined version of the SEEA-EEA sequence of accounts proposed by [

16] (Table 6, p. 33). The application in [

18] is based on the data from the production and balance accounts in this HOW study to develop the format of the sequences in [

16], the purpose of which is to compare the refined rSNA, rSEEA-EEA, and simplified sAAS systems.

The AAS and rSNA applications in this study reveal that the measurement of environmental incomes in the HOW may be derived directly based on the total products that are generated by the activities valued in the HOW territory of Andalusia by the institutional sectors of the farmers and the government, the latter including the ecosystem sector of the SEEA-EEA.

The consistency of the comparisons of the AAS and rSNA results based on the theoretical concept of total income shows that the SNA can be extended with the ultimate aim of estimating the environmental income, (i) modifying the inconsistent application of the production cost in the valuation of products without market prices, substituting it for the marginal price of the simulated demand of active and passive consumers; and (ii) extending the measurement of society total income by incorporating the capital gain in the net value added (operating income).

4.5. Valuing the Ecosystem Service as a Residual Value

In the SEEA-EEA, independent estimates (not linked to the total income accounts) of ecosystem services and changes in the environmental assets risk incurring bias as regards remunerations of the manufactured incomes generated in the type of ecosystem valued. The fact that the ecosystem service is a residual value together with other operating incomes of a consumed product means that prior estimation is necessary of the priority remunerations for manufactured incomes of the individual ecosystem product valued. Ecosystem service estimates using non-residual procedures are common, and in these cases the situation may arise where the arbitrarily assigned value of the ecosystem service of a consumed product exceeds the value of its net value added, which would be a conceptually inconsistent result. For example, [

37] estimate that if family-scale shepherds in Iteimia (Tunisia) with free access to grazing attributed themselves a remuneration for their self-employed work equal to 81% of that received by a local forestry worker. This implies that the ecosystem service of grazing would be dissipated. If the shepherds in Itemia were willing to work as employees, earning 60% of the current earnings of forest workers, the ecosystem service of grazing would be 0.07 €/UF o 36.95 €/ha. Other authors estimate the grazing resource rent as the energy substitute of the market price of barley, which would mean paying the self-employed wage rate at 38% of the forestry employee wage rate of 0.37 €/h at the time of the Iteimia study.

4.6. Policy Implications

In a world where the property rights over global goods and damages tend to be regulated, the divide as regards free public goods is diminishing. In other words, the economic accounts for global society should incorporate public products and costs appropriated directly or indirectly by the government, without market price, and produced within the national territory in the period, valuing them at simulated marginal prices derived from the active and passive consumer demand globally. However, the government institutions specialized in the regulations of the System of National Accounts (SNA) oppose the extension of the economic activities and the substitution of valuations of public and private products without market price at production cost for the simulated marginal value according to consumer demand. This situation has ultimately led to the public debate which has given rise to the satellite proposal in the process of the System of Environmental Economic Accounting-Experimental Ecosystem Accounting (SEEA-EEA) [

12,

13]. This subsidiarity of the SEEA-EEA with respect to the SNA can be avoided by extending the SNA with the ultimate goal of measuring the total income. The economic accounts of the global society make the existence of a satellite SEEA-EEA unnecessary as the former directly provides consistent measurements of the environmental income of the ecosystem types which exist in the national territory and the planet as a whole. In the absence of global compensations among governments for appropriated environmental products and assets of the ecosystems, the design and application of environmental accounts for ecosystem types, such as the HOW studied here, can be applied at national scale and multinational regional scales as the European Union.

Public consumers demand that farmers and governments maintain/improve the offer of public goods and services. This demand will continue increasing, although we will continue to see a process of internalization through the market for public goods and services in which the rights of economic use will change to a private property regime. In this double process of growth of government and market supply of nature-based products, there are technical and institutional factors which determine the local division of economic activities between corporations and government. The government will continue to take exclusive responsibility in cases where consumer exclusion is highly costly or where consumer exclusion is impossible due to the nature of the product; hence, such products will continue to be consumed freely by citizens [

38]. In these circumstances, the government—in representation of the public consumers—compensates the owners for the unwanted loss of profit involved in meeting the demands of the public consumers, previously agreed with the government.

The payment of compensation should be linked to the existence of sustainable management practices with regard to renewable natural resources. Continual management which is often necessary for grazing land in the Mediterranean (scrub control, pruning, periodical sowing, etc.) is one of the necessary conditions for the conservation of the HOW cultural landscape. From this perspective, should payment be extended to owners where loss of profit occurs through any cultural practice favoring the many nature-based products such as game species, firewood from thinning/pruning, apiculture products, and free-access products such as wild mushrooms and asparagus? Government compensations with the ultimate goal of HOW conservation should be based on the concept of cultural landscape, for example, as defined by the [

39], and payment to the owner should be legitimized having previously determined the consumers’ willingness to pay a tax for the services of cultural landscape conservation to a degree assumed bio-physically sustainable in the long term.

The government could use the landscape tax to finance the loss of profit not accepted by the owners of the land and livestock for HOW activities which produce intermediate services used as inputs in the production of additional public service provision. Thus, the thinning/pruning undertaken as part of landscape management should be compensated given the public benefits associated with cultural landscape conservation. Honey production should also be compensated for the intermediate services which it produces in the landscape, but only for the loss of profit not accepted by the hive owner. Compensation could be paid to owners where wild mushroom and asparagus picking takes place, on the condition that a plan agreed with the government is put in place which is proved to encourage future production for commercial or recreational picking.

According to the local institutional agreements reached, the owners may receive compensation without having to make additional investment for allowing mushroom/asparagus pickers access to the farm, although in such cases there would be no loss of commercial profit to the owner but there could be a loss of private amenity service for the non-industrial owner.

An illustrative example of the complexity involved in implementing agreed compensation policies is that of the exclusion from compensations of most of the areas of woody grazing in Spain. Compensations under the Common Agricultural Policy (CAP) of the European Union continue to suffer from its philosophy based around livestock and crops, without conditioning these compensations to the sustainability of the management practices employed for renewable natural resources on the farms. This commercial principle in the CAP of dealing with the final agricultural and livestock products results in the intermediate outputs of managed wild grazing (fruit, leaves, and twigs) being ignored, as is the case of holm oak open woodland (HOW), where the fruit (acorns) and leaves/twigs from regeneration, pruning, etc. are consumed by game species, cattle, and other wild animals. This situation of ‘commodity tragedy’ under the CAP means that silvopastoral landscape grazing does not form part of the CAP, except indirectly through compensations for extensive husbandry. Grazing is also invisible in the net value added estimated in the government economic accounts for agriculture and forestry [

6].

In a recent report analyzing the limitations of CAP direct payments for areas of woody pasture, the authors consider that the current guidelines of the CAP, which under certain circumstances recognize the right of HOW to compensation for livestock grazing, present limitations which should be mitigated by generalizing the compensations paid for woody grazing. The justification for this recommendation is that such a policy would clearly have favorable social, economic, and environmental effects [

40].

The design of the CAP still does not explicitly include the payment of compensations for non-commercial intermediate products of the HOW which contribute to public goods and services consumed freely by European citizens. It would seem that the compensations under the CAP which indirectly affect the production of grazing in the HOW do not fulfill the criteria of equity and mitigation of the ‘free rider’ behavior of the active and passive consumers of HOW public products, while at the same time the standard of living of owners and employees is negatively impacted. The paradox of this decline in the commercial products of their farms is that it is taking place at the same time as the public products derived from the economic activities in the HOW are increasingly valued by public consumers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}