3.2. Analysis of the Variables Involved in Forest Fires

As we have stated previously, we are looking for a multivariate discount function based on the relationship between hazard rate and instantaneous discount rate. We use data on forest fires by cause and state from 2002 to 2012 in order to calculate discount functions for every state (with global data for all the causes) or for every cause (with global data for all the states). For this reason, we first use the chi square to test the relationship between the variables “cause of burning” and “state” for significance. In effect,

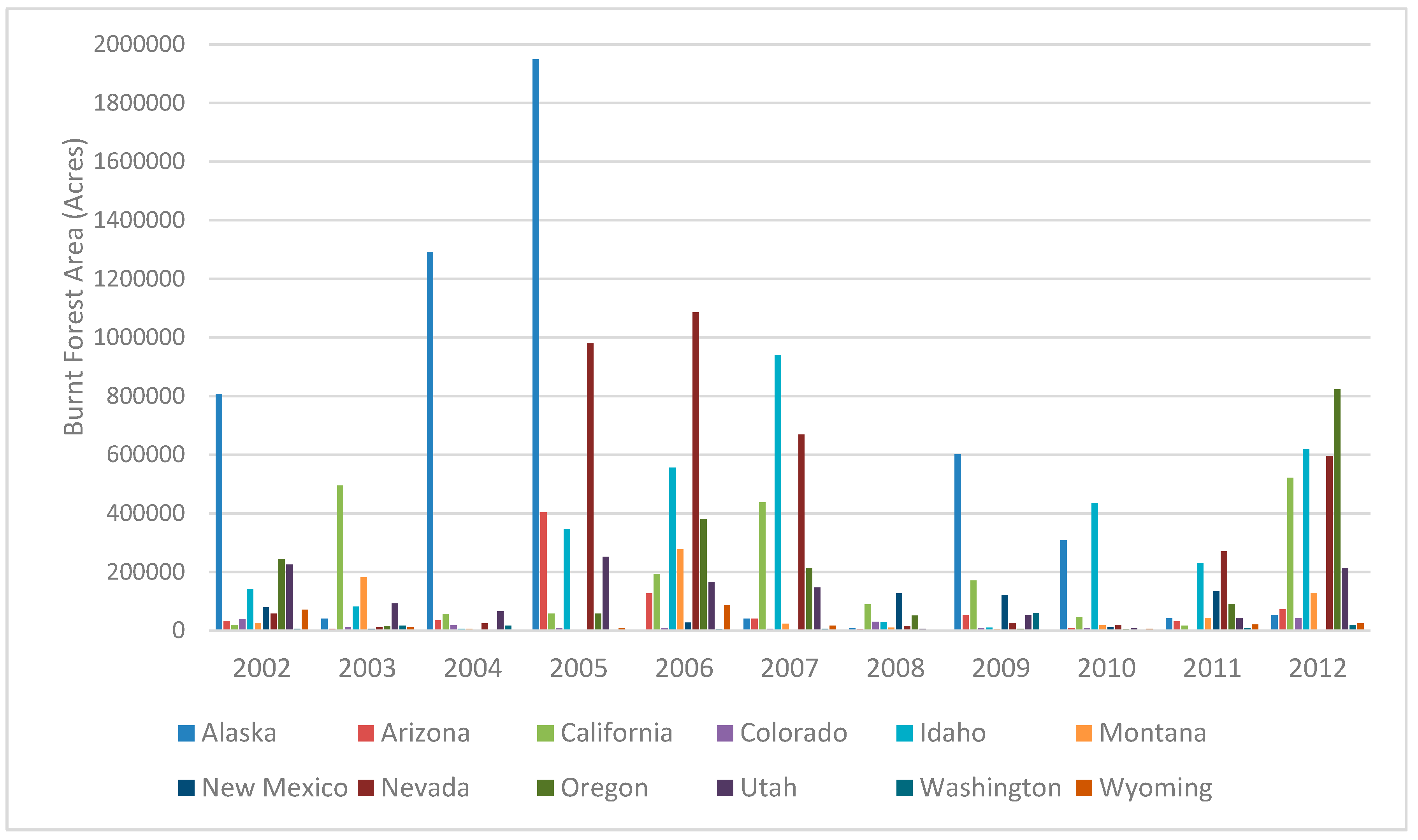

Table 4 shows the data for the number of burned acres by state and cause.

The question is whether there is a significant relationship between cause and state. To determine this, we shall follow these steps:

First, state the null hypothesis: there is no relationship between fire cause and state. We test this hypothesis using contingency tables.

Second, compute the expected frequency for each cell based on the assumption that there is no relationship. These expected frequencies are computed from the totals shown in

Table 4 as follows:

where

is the expected frequency for cell

,

is the total for the

i-th row,

is the total for the

j-th column, and

n is the total number of observations, in our case 39,368,327.94. As an example, we could calculate the expected frequency for the number of burnt acres due to human causes in Alabama:

Table 5 shows the expected frequencies for each cause in all the states.

Third, compute the chi square and degrees of freedom. The significance test is conducted by computing the chi square as follows:

On the other hand, the number of degrees of freedom is equal to , where r is the number of rows and c is the number of columns. In this case, the number of degrees of freedom is . As the theoretical value of the chi square, , at a 95% significance level is located between 101.879 and 107.522, we can deduce that the null hypothesis of no relationship between fires cause and state can be rejected.

Given this result, we have to study next the degree of association between these two variables. We follow [

42] to explain several coefficients to assess the degree of association between two variables, “none of which appears to be completely satisfactory”:

1. Pearson’s contingency coefficient,

P, defined by:

Its value is located between 0 and , where . In our case, and . So, there exists a certain association between both variables. This coefficient has the disadvantage that, even in the case of complete association, the value of P depends on the number of rows and columns. To solve this restriction the following coefficient has been suggested.

2. Tschuprow’s contingency coefficient,

, defined by:

It is located between 0 and 1, being 0 in case of complete independence. This only attains a value of 1 in the case of complete association when but cannot do so if . In our example, .

In the following modification suggested by Cramer, the unity can be obtained for all values of r and c in the case of complete association.

3. Cramer’s contingency coefficient,

C, defined by:

Its value is located between 0 and 1. In our case, .

These three suggested coefficients have no obvious probabilistic interpretation. The coefficient we introduce next is interpretable in a predictive sense. The rationale behind Goodman and Kruskal’s lambda measures is: “How much does a knowledge of the classification of one of the variables improve one’s ability to predict the classification on the other variable?” [

43].

4. Goodman and Kruskal’s index of predictive ability lambda,

, defined by:

where

is the overall modal frequency of the dependent variable

Y, and

is the sum of modal frequencies on the dependent variable

Y within separate categories of the independent variable X.

is the relative decrease in the probability of an error in guessing the category of one variable, having information about the predictor variable. Its value is located between 0 and 1, being 1 when no error is made (and consequently there is complete predictive association). A disadvantage of the lambda measures is that the values of indices may be misleadingly low when the marginal distribution is far from being uniform [

36].

In our example, one has . So we only have a decrease of 11% in the error made when guessing the cause of a fire produced in a certain state. This means that the association between the variables “state” and “cause of the forest fire” is low.

We think that, in our case, the independent variable should be the state and the dependent variable the cause. Nevertheless, and just to verify it, we can reverse the variables

A and

B. In this case, we will have

, suitable for predictions of

A form

B:

In our case, we obtain . Despite the previously established limitations, both values are low. And we can complement these results with those obtained for the other indices we have previously calculated in order to state that there is a low association between the variables; therefore we can conclude and suppose in what follows that the variables are independent.

3.3. Calculation of Discount Rates

In the analysis presented in

Section 3.2, we have statistically shown that there is no association between the causes of forest fires (1: human, 2: natural, and 3: unknown) and the states in USA (from Alabama to Wyoming) since the Goodman and Kruskal’s indexes are 0.11 and 0.08. Consequently, we can derive a discount function for each cause which can be applied to discount the social benefits generated by investment on reforestation either in a state, in a group of states, or all in states in the USA. More specifically, because of their suitability for modeling rates of increasing or decreasing hazard rates, we are going to use discount functions that belong to the family of generalized exponential discounting, defined by:

Before starting the process of fitting data, we have observed that the hazard rate corresponding to causes 1 and 3 is decreasing and so the hyperbolic discounting is appropriate to fit them. However, the hazard rate corresponding to cause 2 is increasing and so the hyperbolic discounting does not apply. For this reason, we have used instead the family of generalized exponential discount functions which, depending on the sign of one of its two parameters, can describe an increasing or decreasing discount rate.

To calculate the values of

α and

β of this function, we use a linear regression, starting from the data of burnt forest surface due to cause

i over the total forest surface. This way, we obtain the following results by causes (1, 2, and 3):

and

Table 6 shows the estimated parameters of Equation (17) by using a linear regression and by reporting the results of the regression, specifically, the significance of coefficients.

As indicated, they can be applied to every state or group of states which agree to fight against a concrete cause of forest fires for a given period (say from 2015 to 2030). Indeed, the discount rates using exponential discounting, deduced for each cause and year, are shown in

Table 7.

Observe that the discount rates for cause 2 (natural) are increasing, whilst the discount rates for causes 1 and 3 (human and unknown) are decreasing and that these percentages are only a part of the total discount rate to be applied per cause and year. As stated in

Section 1, we have considered only the problem of determining the discount function derived from the hazard rate of the system, one of the two components of Equation (1) which displays the expression of the total discount rate.

In this paper, we have calculated the part of the discount rate due to the failure of forests caused by fires. Forest fire is just one of several forest investment hazards. Severe damages can be caused by pests, insects, grazing, air-borne pollution (such as ozone), soil acidification, etc. Following [

44] the main hazards in forests are storms, snow, insects, and fire. But fire is a major disturbance to forests all over the world. On the other hand, in this paper the purely financial component of the discount rate has not been included since this is not the objective of this manuscript. The reason for using a diminishing component of the discount rate (due to fires) is because a decreasing hazard rate is expected, as is usual when studying the reliability of systems. In effect, [

45] shows that the average area burned per year by forest fires in the five largest countries in southern Europe (France, Italy, Spain, Greece, and Portugal) has decreased during the period of 2000–2017. At this point, we must insist in that this paper only analyzes the component of the discount rate due to the hazard rate caused by fires and not the other components (financial, hazard rate due to pests, etc.) which, as just reported, must be diminishing. However, it is possible that the overall discount could be eventually increasing.

The equation to calculate the total discount rate for each cause

ik, taking into account Equation (1) and using exponential discounting, would be:

where

is the discount function due to the

k-th cause (

k = 1, 2, and 3) and

the discount rate due to the remainder of causes involved in the valuation process. Analogously, this analysis could be addressed by states and years instead of causes and years. In this case, the discount functions would be independent of causes and then a global policy without distinguishing among causes could be applied in each state.

Starting from the discount functions by causes, we could obtain a unique multivariate discount function using as weighting coefficients in Equation (10) the inverse of budgets intended to prevent each of the causes. Unfortunately, we do not have this information at our disposal, but we propose this idea and its possible application by decision-makers, when using a hazard approach in the valuation of forest investment.

Nevertheless, to illustrate how to calculate a multivariate discount function using our hazard rate approach, we will use the information on forest fires not by cause, but following the type of burned area (National Forests and the rest of forests), and the obtained discount functions will be weighted inversely proportional to the number of visitors to each area. We will use data from the USDA Forest Service [

46] on registered visits to National Forests and to the rest of forests. From the available data on visits for the period 2008–2012, we have an annual estimation of 160,973,000 National Forest visits and 8,070,000 wilderness visits. This makes a total of 169,043,000 visits per year.

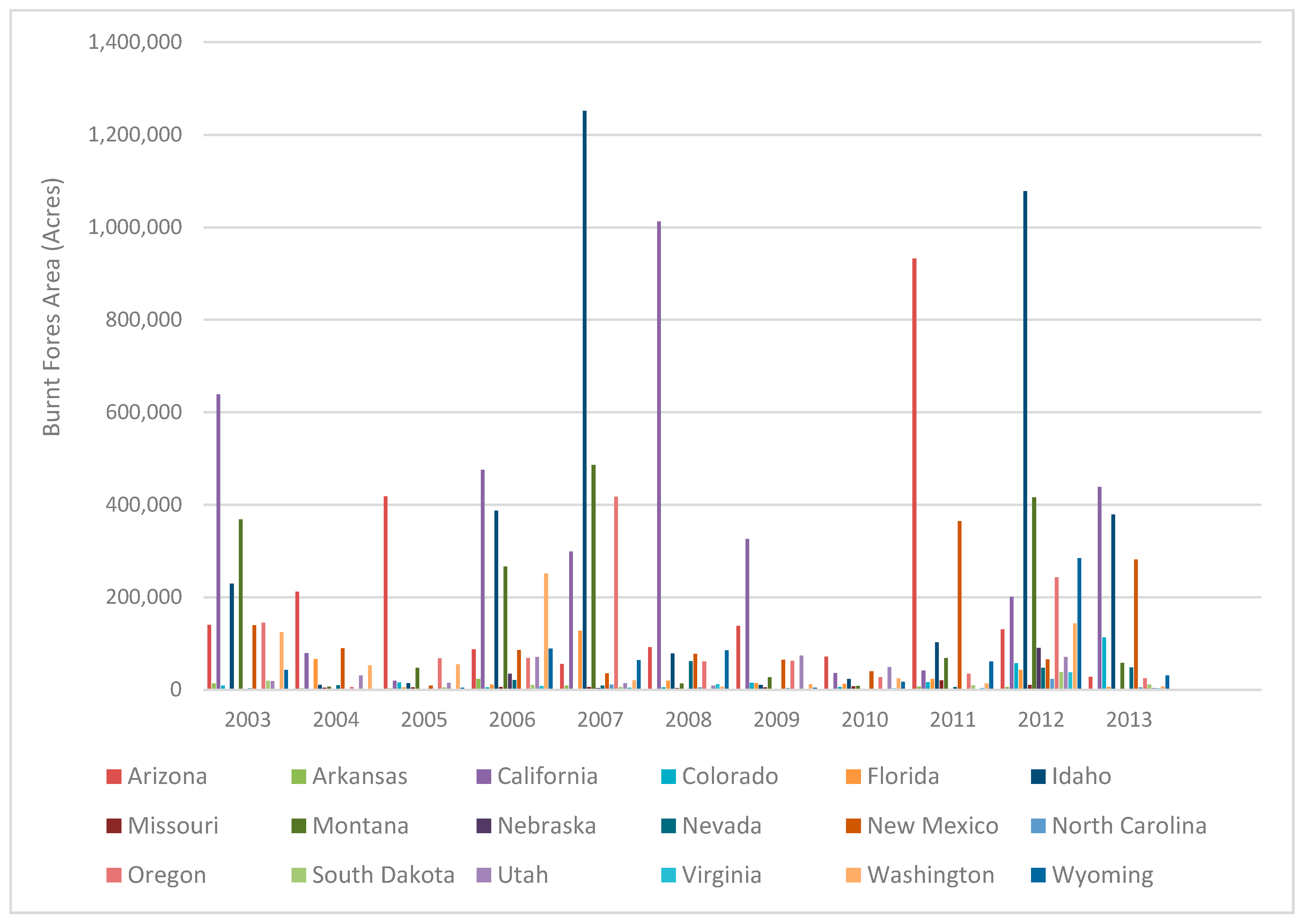

This way, our multivariate hazard rate will take into account the hazard rate for National Forests and the hazard rate for the rest of forests. So we have to take into account now the data on forest fires and forest surface from National Forests and from the rest of forests (see

Table 8).

Following the same procedure as before, we obtain the hazard rate and then the global discount function (from the National Forest and the rest of forests discount functions). Using formulae (7) and (10), we have:

where

and

.

The discount rates, using exponential discounting, are shown in

Table 9.

Observe that the obtained discount rates are decreasing over time and that these percentages are only a part of the total discount rate, as explained previously in the case of the discount rates per cause.

We could calculate the total discount rate

i as we have done for the discount rates per cause. Thus, adapting Equation (21) we will have:

where

is the global discount function and

the discount rate due to the remainder of causes involved in the valuation process. As we have already noted, we are not going to analyze the discount function due to the remainder of causes. But, we think that, taking into account the literature reviewed in the introduction and the discount rates used by several governments, the discount rates due to the remainder of causes must be also decreasing, or at least constant, which will result in a decreasing total discount rate.

These results are in line with the recommendations from several authors about using decreasing discount rates for projects with very long-term impacts, as in the case of investments in afforestation. Specifically, in forestry financial analysis, we agree with Hepburn and Koundouri [

14] in that “moreover forest managers will no doubt realize that the implementation of a declining discount rate scheme is not only important for the economic value of future timber products. It is also crucial in determining the net present value of forestry benefits that people derive from forest services, such as extraction of genetic material, tourism, protection of watersheds, support of other ecosystems, carbon storage, etc.”

Lastly, we would like to make a remark regarding the age of the forests. In our opinion, older forest stands have a greater probability of fire (less distance between trees, more near the cities, the majority of them are recreational areas, etc.). In effect, [

47] recognize that the age distribution of stands in a region can be used to estimate the fire frequency by assuming a frequency distribution such as the negative exponential or the Weibull. From another point of view, [

48] analyzed the probability of fire occurrence in forest stands of Catalonia (Spain) and showed that the predictors used in their model support previous findings which state that “stands resembling mature sparse even-aged forests have a lower fire risk than dense and multi-layered stands”. On the other hand, [

49] quantify the relationship between forest stand age and fire severity in forest burned in south-eastern Australia in 2009. Using probit regression analysis, they identified a strong relationship between the age of a mountain ash forest and the severity of damage in forests subject to fires under extreme weather conditions.

Also related with the age of forests, tree density can influence the probability of fire. In this way, [

50] demonstrate that if the forest density is too low or too high, the wind effect has no impact on fire spread patterns.

Thus, taking into account the former paragraphs and the end of the previous item, we could propose the following variant of the hyperbolic discounting:

where

k > 0,

m > 0 and

d0 is the moment of valuation, and

d is the age of the burned forest. Observe that, in this case, the instantaneous discount rate

is also decreasing which leads to a declining discount rate.

{kind=link}

{kind=link}