Economic Competitiveness of Small Modular Reactors in a Net Zero Policy

Abstract

1. Introduction

2. Small Modular Reactors

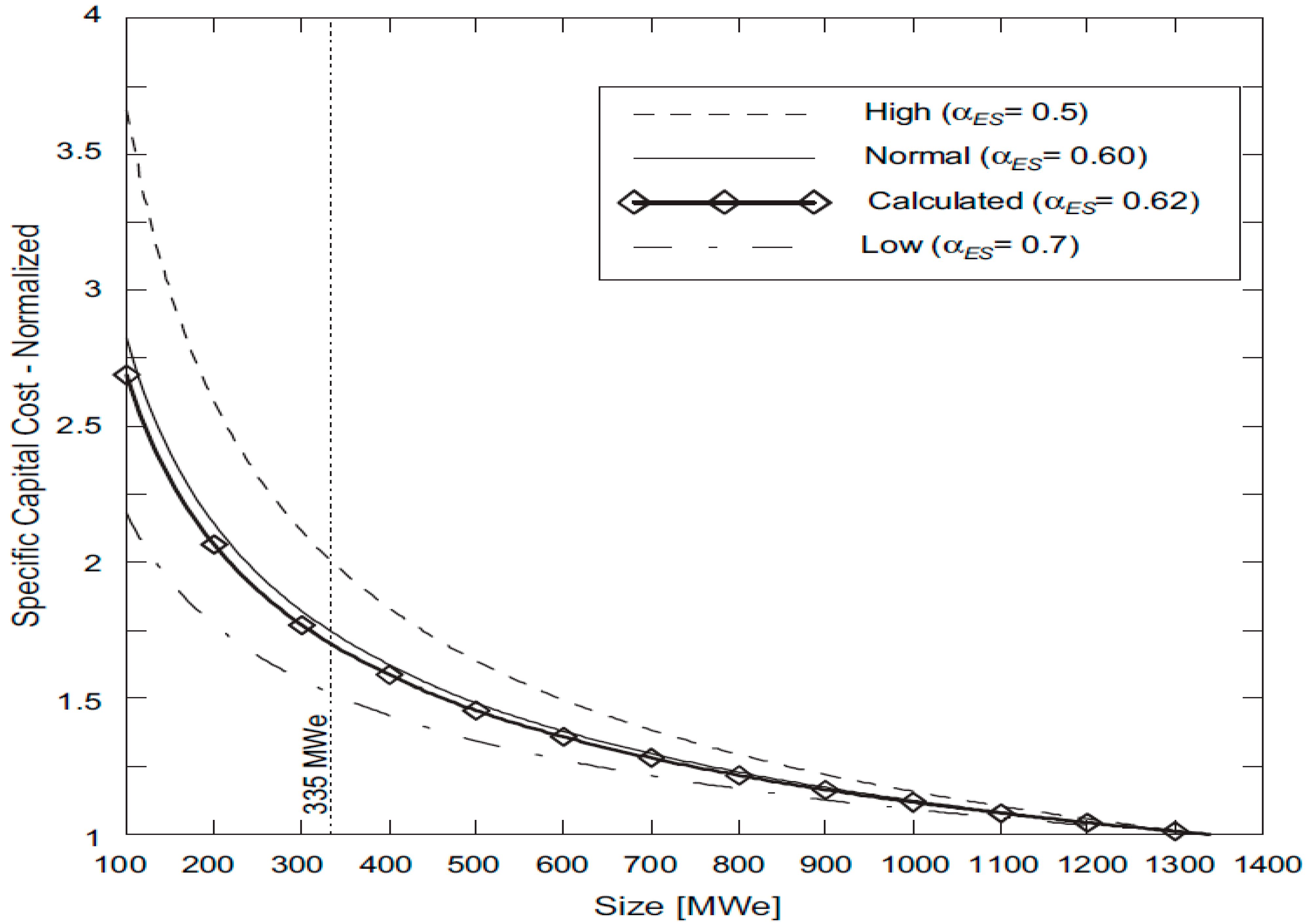

Economy of Scale

- (a)

- Constructing multiple units in the same place could reduce costs because the site studies correspond to the same place, and only licensing permits will be required;

- (b)

- If the construction is undertaken sequentially, the first operating plant can provide resources for the subsequent reactors in construction;

- (c)

- Minimizing construction time helps reduce capital interest;

- (d)

- Smaller size permits better planning to fit the electricity demand, reducing the required investment;

- (e)

- By making modularization, the design is simpler, and the construction time is reduced.

3. Methodology

- TEG is the average annual generation of electricity in MWh;

- PI is the overnight cost of the investment per installed capacity in USD/MWe;

- i is the discount rate;

- N is construction time in years;

- wk is the share investment per year;

- is the economic life of the plant.

- : net cash inflow during the period t;

- : total initial investment cost;

- : discount rate;

- t: number of periods.

4. Results

5. Additional Issues

5.1. Licensing

- Typology of licensing approach;

- Duration and predictability of the licensing process;

- Regulatory harmonization and international certification;

- Manufacturing license;

- Ad hoc legal and regulatory framework.

5.2. Nuclear Infraestructure

5.3. Industrial Applications

6. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

References

- Goldberg, S.M.; Rosner, R. Nuclear Reactors: Generation to Generation; Academy of Sciences USA: Cambridge, MA, USA, 2011; Available online: https://www.amacad.org/sites/default/files/academy/pdfs/nuclearReactors.pdf (accessed on 20 November 2024).

- GE Hitachi Nuclear Energy. The ABWR Plant General Description. 2007. Available online: https://www.gevernova.com/content/dam/gevernova-nuclear/global/en_us/documents/large-modular-boiling-water-reactors/ABWR-General-Description-Book.pdf (accessed on 25 October 2024).

- IAEA Power Reactor Information System. 2023. Available online: https://pris.iaea.org/pris/ (accessed on 15 June 2024).

- US-NRC Nuclear Reactors Licensing. 2024. Available online: https://www.nrc.gov/reactors/operating/licensing/renewal/subsequent-license-renewal.html (accessed on 8 June 2024).

- IAEA. Energy, Electricity and Nuclear Power Estimates for the Period up to 2050. 2023. Available online: https://www.iaea.org/publications/15487/energy-electricity-and-nuclear-power-estimates-for-the-period-up-to-2050 (accessed on 10 June 2024).

- IAEA. Nuclear Energy for a Net Zero World. 2021. Available online: https://www.iaea.org/sites/default/files/21/10/nuclear-energy-for-a-net-zero-world.pdf (accessed on 15 October 2024).

- IEA. World Energy Outlook 2022. November 2022. Available online: https://www.iea.org/reports/world-energy-outlook-2022 (accessed on 15 June 2024).

- Electrical Power Research Institute. Advanced Light Water Reactor Utility Requirements Document. TR-016780. 1999. Available online: https://www.epri.com/research/products/TR-016780-V3R8 (accessed on 15 January 2025).

- European Utility Requirements for LWR Nuclear Power Plants, Revision E. December 2016. Available online: https://www-pub.iaea.org/MTCD/publications/PDF/P1500_CD_Web/htm/pdf/topic3/3S01_P.%20Berbey_PM.pdf (accessed on 15 January 2025).

- Electrical Power Research Institute. Utility Requirements Document Expanded to Include Small Modular Reactors. 3002004884. 2014. Available online: https://www.energy.gov/ne/articles/advanced-nuclear-technology-advanced-light-water-reactors-utility-requirements-document (accessed on 15 January 2025).

- IAEA. Small Modular Reactors Catalogue 2024. 2024. Available online: https://aris.iaea.org/Publications/SMR_catalogue_2024.pdf (accessed on 15 January 2025).

- Carelli, M.D.; Garrone, P.; Locatelli, G.; Mancini, M.; Mycoff, C.; Trucco, P.; Ricotti, M.E. Economic features of integral, modular, small-to-medium size reactors. Prog. Nucl. Energy 2010, 52, 403–414. [Google Scholar] [CrossRef]

- Rothwell, G.; Ganda, F. Electricity Generating Portfolios with Small Modular Reactors. Argonne National Laboratory. 2014. Available online: https://www.energy.gov/ne/articles/electricity-generating-portfolios-small-modular-reactors-0 (accessed on 15 June 2024).

- IEA. Projected Cost of Generating Electricity, Edition 2020. Available online: https://www.iea.org/reports/projected-costs-of-generating-electricity-2020 (accessed on 15 June 2024).

- Alonso, G.; Bilbao, S.; del Valle, E. Economic competitiveness of small modular reactors versus coal and combined cycle plants. Energy 2016, 116, 867–879. [Google Scholar] [CrossRef]

- IAEA. Expansion Planning for Electrical Generating Systems. A Guidebook. 1984. Available online: https://www-pub.iaea.org/MTCD/Publications/PDF/TRS1/TRS241_Web.pdf (accessed on 15 June 2024).

- IEA. Electricity 2024—Analysis and Forecast to 2026. January 2024. Available online: https://iea.blob.core.windows.net/assets/6b2fd954-2017-408e-bf08-952fdd62118a/Electricity2024-Analysisandforecastto2026.pdf (accessed on 17 July 2024).

- Asuega, A.; Limb, B.J.; Quinn, J.C. Techno-economic analysis of advanced small modular nuclear reactors. Appl. Energy 2023, 334, 120669. [Google Scholar] [CrossRef]

- Rahmanta, M.A.; Harto, A.W.; Agung, A.; Ridwan, M.K. Nuclear Power Plant to Support Indonesia’s Net Zero Emissions: A Case Study of Small Modular Reactor Technology Selection Using Technology Readiness Level and Levelized Cost of Electricity Comparing Method. Energies 2023, 16, 3752. [Google Scholar] [CrossRef]

- Van Hee, N.; Peremans, H.; Nimmegeers, P. Economic potential and barriers of small modular reactors in Europe. Renew. Sustain. Energy Rev. 2024, 203, 114743. [Google Scholar] [CrossRef]

- Liu, Z.; Fan, J. Technology readiness assessment of small modular reactor (SMR) designs. Prog. Nucl. Energy 2014, 70, 20–28. [Google Scholar] [CrossRef]

- Sainati, T.; Locatelli, G.; Brookes, N. Small Modular Reactors: Licensing constraints and the way forward. Energy 2015, 82, 1092–1095. [Google Scholar] [CrossRef]

- Zhong, Z.; Burhan, M.; Choon, K.; Cui, X.; Chen, Q. Low-temperature desalination driven by waste heat of nuclear power plants: A thermo-economic analysis. Desalination 2024, 576, 117325. [Google Scholar] [CrossRef]

- Alonso, G.; Del Valle, E.; Ramirez, J.R. Desalination in Nuclear power Plants, 1st ed.; Woodhead Publishing: Sawston, UK; Elsevier: Amsterdam, The Netherlands, 2020; ISBN 9780128200216/9780128226445. [Google Scholar]

- Al-Othman, A.; Darwish, N.N.; Qasim, M.; Tawalbeh, M.; Darwish, N.A.; Hilal, N. Nuclear desalination: A state-of-the-art review. Desalination 2019, 457, 39–61. [Google Scholar] [CrossRef]

- Khan, S.U.; Khan, S.U.; Haider, S.; El-Leathy, A.; Rana, U.A.; Danish, S.; Ullah, R. Development and techno-economic analysis of small modular nuclear reactor and desalination system across Middle East and North Africa region. Desalination 2017, 406, 51–59. [Google Scholar] [CrossRef]

- Priego, E.; Alonso, G.; del Valle, E.; Ramirez, R. Alternatives of Steam Extraction for Desalination Purposes Using SMART Reactor. Desalination 2017, 413, 199–216. [Google Scholar] [CrossRef]

- Alonso, G.; Vargas, S.; del Valle, E.; Ramirez, R. Alternatives of seawater desalination using nuclear power. Nucl. Eng. Des. 2012, 245, 39–49. [Google Scholar] [CrossRef]

- Abushamah, H.A.S. Nuclear District Cooling System: Evaluation and Optimization. Ph.D. Thesis, University of West Bohemia, Plzeň, Czech Republic, 2023. [Google Scholar]

- Jamaluddin, K.; Rafidah, S.; Alwi, W.; Manan, Z.A.; Hamzah, K.; Kleměs, J.J.; Zailan, R. Optimal nuclear trigeneration system considering life cycle costing. J. Clean. Prod. 2022, 370, 133399. [Google Scholar] [CrossRef]

- Rämä, M.; Leurent, M.; Devezeaux de Lavergne, J.-G. Flexible nuclear co-generation plant combined with district heating and a large-scale heat storage. Energy 2020, 193, 116728. [Google Scholar] [CrossRef]

- Leurenta, M.; Da Costa, P.; Jasseranda, F.; Rämäc, M.; Persson, U. Cost and climate savings through nuclear district heating in a French urban area. Energy Policy 2018, 115, 616–630. [Google Scholar] [CrossRef]

- Colmenar-Santos, A.; Rosales-Asensio, E.; Borge-Diez, D.; Blanes-Peiró, J.J. District heating and cogeneration in the EU-28: Current situation, potential and proposed energy strategy for its generalization. Renew. Sustain. Energy Rev. 2016, 62, 621–639. [Google Scholar] [CrossRef]

- Nuclear Energy Agency. The Role of Nuclear Power in the Hydrogen Economy: Cost and Competitiveness; No. 7630; NEA: Paris, France, 2022; Available online: https://www.oecd-nea.org/upload/docs/application/pdf/2022-09/7630_the_role_of_nuclear_power_in_the_hydrogen_economy.pdf (accessed on 15 January 2025).

- International Atomic Energy Agency. Hydrogen Production with Operating Nuclear Power Plants, Business Case. 2023. Available online: https://www.iaea.org/system/files/2023_h2_bc_booklet_web.pdf (accessed on 15 January 2025).

- Zhang, Z.; Dong, Y.; Li, F.; Zhang, Z.; Wang, H.; Huang, X.; Li, H.; Liu, B.; Wu, X.; Wang, H.; et al. The Shandong Shidao Bay 200 MWe High-Temperature Gas-Cooled Reactor Pebble-Bed Module (HTR-PM) Demonstration Power Plant: An Engineering and Technological Innovation. Engineering 2016, 2, 112–118. [Google Scholar] [CrossRef]

- Alonso, G.; Ramirez, R.; del Valle, E.; Castillo, R. Process Heat Cogeneration Using a High Temperature Reactor. Nucl. Eng. Des. 2014, 280, 137–143. [Google Scholar] [CrossRef]

- Alonso, G.; Ramirez, R.; Latifi, M.S. Technical and economic analysis of a pebble bed modular reactor with nitrogen coolant. Prog. Nucl. Energy 2023, 163, 104843. [Google Scholar] [CrossRef]

- Oettingen, M. Modelling of the reactor cycle cost for thorium-fuelled PWR and environmental aspects of a nuclear fuel cycle. Geol. Geophys. Environ. 2019, 45, 207–217. [Google Scholar] [CrossRef]

- International Atomic Energy Agency. Small Modular Reactors: A New Nuclear Energy Paradigm. 2024. Available online: https://nucleus.iaea.org/sites/smr/Shared%20Documents/Small%20Modular%20Reactors%20a%20new%20nuclear%20energy%20paradigm.pdf (accessed on 15 January 2025).

- Hidayatullah, H.; Susyadi, S.; Subki, M.H. Design and technology development for small modular reactors—Safety expectations, prospects and impediments of their deployment. Prog. Nucl. Energy 2015, 79, 127–135. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Scenario | Global Electricity Supply (TWh) | Nuclear Energy Supply (TWh) | Nuclear Share (%) | Nuclear Capacity (GW) |

|---|---|---|---|---|

| 2021 | 28,334 | 2776 | 9.79 | 364 |

| STEPS 2050 | 49,845 | 4260 | 8.54 | 559 |

| APS 2050 | 61,268 | 5103 | 8.32 | 670 |

| NZE 2050 | 73,232 | 5810 | 7.90 | 762 |

| Large Reactor | SMR | |

|---|---|---|

| Power MW | 1340.00 | 335.00 |

| Proper Uses * MW | 48.00 | 37.49 |

| Overnight Cost USD/kW | 4250 | 4505 |

| 5355 | ||

| Fuel USD/MWh | 9 | 9 |

| Operation and Maintenance USD/MWh | 14 | 14 |

| Construction Time years (investment share) | 5 (23.50%, 38.10%, 17.70%, 16.70%, 4%) | 3 (60%, 20%, 20%) |

| Average Plant Factor % | 90 | 90 |

| Reactor operational time years | 60 | 60 |

| Large Reactor | SMR | |||

|---|---|---|---|---|

| Overnight Cost (USD/kW) | 4250 | 4505 | 5355 | |

| Discount Rate | ||||

| Levelized Cost of Electricity (USD/MWh) | 3% | 41.13 | 47.24 | 51.81 |

| 5% | 54.80 | 59.42 | 66.29 | |

| 7% | 69.82 | 73.46 | 82.98 | |

| 10% | 95.08 | 96.98 | 110.94 | |

| Overnight Cost (USD/kW) | DR (%) | TLEC (USD/MWh) | IRR (%) | Benefit/Cost | NPV (Millions of USD) | Recovery Time (Years) |

|---|---|---|---|---|---|---|

| Large Reactor 4250 | 3 | 41.13 | 8.90 | 2.70 | 10,813.88 | 11.49 |

| 5 | 54.80 | 8.38 | 1.63 | 4302.56 | 16.04 | |

| 7 | 69.82 | 7.88 | 1.11 | 840.49 | 28.96 | |

| 10 | 95.08 | 7.19 | 0.76 | −1921.48 | Not recovery | |

| SMR 4505 | 3 | 47.24 | 9.02 | 2.91 | 3097.88 | 11.51 |

| 5 | 59.42 | 8.63 | 1.92 | 1562.16 | 14.20 | |

| 7 | 73.46 | 8.27 | 1.36 | 651.21 | 19.18 | |

| 10 | 96.98 | 7.75 | 0.90 | −186.47 | Not recovery | |

| SMR 5355 | 3 | 51.81 | 7.68 | 2.44 | 2786.67 | 14.20 |

| 5 | 66.29 | 7.34 | 1.61 | 1232.37 | 18.48 | |

| 7 | 82.98 | 7.01 | 1.14 | 302.06 | 29.50 | |

| 10 | 110.94 | 6.56 | 0.75 | −566.16 | Not recovery |

| Overnight Cost (USD/kW) | DR (%) | TLEC (USD/MWh) | IRR (%) | Benefit/Cost | NPV (Millions of USD) | Recovery Time (Years) |

|---|---|---|---|---|---|---|

| Large Reactor 4250 | 3 | 41.13 | 13.37% | 4.46 | 21,908.17 | 6.41 |

| 5 | 54.8 | 12.65% | 2.63 | 11,063.78 | 8.06 | |

| 7 | 69.82 | 11.97% | 1.73 | 5318.30 | 10.68 | |

| 10 | 95.08 | 11.02% | 1.10 | 771.56 | 22.45 | |

| SMR 4505 | 3 | 47.24 | 14.09% | 4.85 | 6240.45 | 6.45 |

| 5 | 59.42 | 13.52% | 3.21 | 3753.33 | 7.34 | |

| 7 | 73.46 | 12.99% | 2.30 | 2307.28 | 8.51 | |

| 10 | 96.98 | 12.23% | 1.54 | 1022.22 | 11.36 | |

| SMR 5355 | 3 | 51.81 | 12.15% | 4.08 | 5929.24 | 7.82 |

| 5 | 66.29 | 11.65% | 2.70 | 3423.54 | 9.07 | |

| 7 | 82.98 | 11.18% | 1.93 | 1958.13 | 10.85 | |

| 10 | 110.94 | 10.52% | 1.28 | 642.53 | 16.17 |

| Overnight Cost (USD/kW) | DR (%) | TLEC (USD/MWh) | IRR (%) | Benefit/Cost | NPV (Millions of USD) | Recovery Time (Years) |

|---|---|---|---|---|---|---|

| Large Reactor 4250 | 3 | 41.13 | 17.18% | 6.24 | 33,205.20 | 4.42 |

| 5 | 54.8 | 16.30% | 3.64 | 17,948.55 | 5.38 | |

| 7 | 69.82 | 15.47% | 2.36 | 9877.94 | 6.72 | |

| 10 | 95.08 | 14.31% | 1.44 | 3513.80 | 10.34 | |

| SMR 4505 | 3 | 47.24 | 18.59% | 6.79 | 9383.02 | 4.49 |

| 5 | 59.42 | 17.87% | 4.50 | 5944.49 | 4.96 | |

| 7 | 73.46 | 17.19% | 3.23 | 3963.34 | 5.55 | |

| 10 | 96.98 | 16.23% | 2.17 | 2230.91 | 6.72 | |

| SMR 5355 | 3 | 51.81 | 16.14% | 5.71 | 9071.81 | 5.40 |

| 5 | 66.29 | 15.50% | 3.78 | 5614.70 | 6.05 | |

| 7 | 82.98 | 14.90% | 2.71 | 3614.19 | 6.88 | |

| 10 | 110.94 | 14.05% | 1.82 | 1851.22 | 8.67 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alonso, G. Economic Competitiveness of Small Modular Reactors in a Net Zero Policy. Energies 2025, 18, 922. https://doi.org/10.3390/en18040922

Alonso G. Economic Competitiveness of Small Modular Reactors in a Net Zero Policy. Energies. 2025; 18(4):922. https://doi.org/10.3390/en18040922

Chicago/Turabian StyleAlonso, Gustavo. 2025. "Economic Competitiveness of Small Modular Reactors in a Net Zero Policy" Energies 18, no. 4: 922. https://doi.org/10.3390/en18040922

APA StyleAlonso, G. (2025). Economic Competitiveness of Small Modular Reactors in a Net Zero Policy. Energies, 18(4), 922. https://doi.org/10.3390/en18040922