Development and Upstream Integration of the Photovoltaic Industry Value Chain in Mexico

, ,

, ,

Abstract

1. Introduction

2. Energy Security and the PV Industry

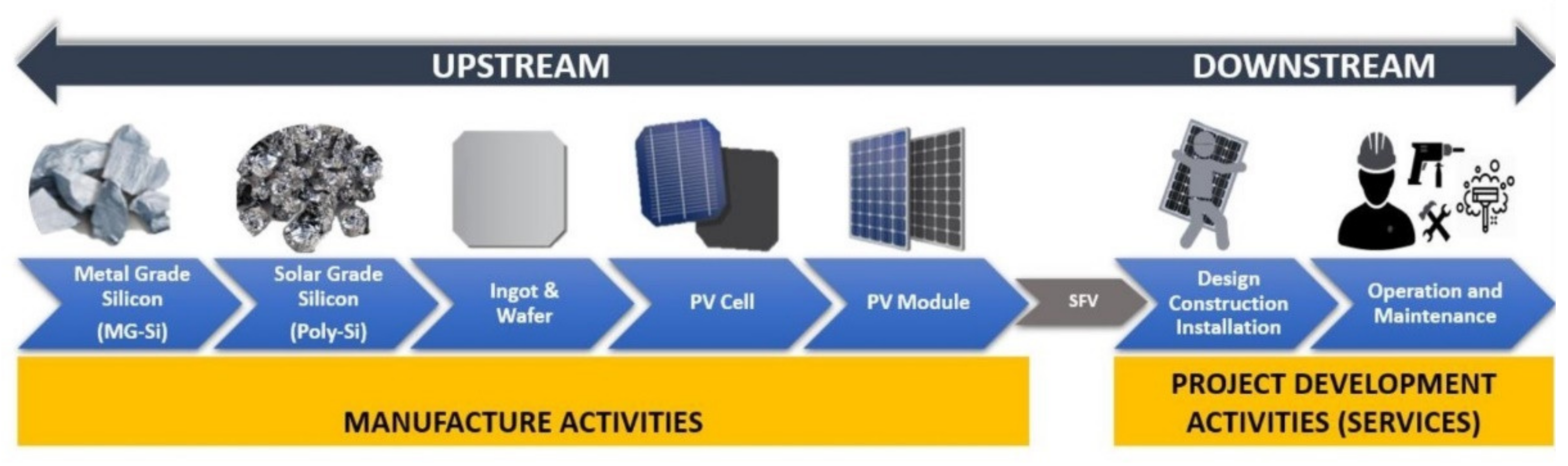

3. PV Industry Value Chain Development in Mexico

4. Materials and Methods

- First, the year 2018 was established as the reference year, since the year had sufficient information to represent the current structure and production capacity of the PV industry upstream value chain in Mexico.

- Second, through a bottom-up cost model, the total manufacturing cost for the VCPVIM, the minimum sale price or minimum sustainable price (MSP) and the national content proportion were estimated for the reference year.

- Third, through a techno-economic analysis that considers technological progress and economies of scale, the total manufacturing cost for the VCPVIM, the minimum sale price or minimum sustainable price (MSP) and the national content proportion were estimated for the base and alternative scenarios.

- Finally, the socioeconomic and environmental benefits were estimated and evaluated for each scenario, focusing on job generation, added value and the link of the development of the VCPVIM with the fulfillment of the nationally determined contributions.

4.1. Scenarios Construction

4.1.1. Reference Year

4.1.2. Base Scenario

4.1.3. Alternative Scenario

4.2. Calculations

4.2.1. Cost Model

4.2.2. Sustainable Minimum Price Model (MSP)

4.2.3. National Content Proportion Model

4.2.4. Socioeconomic Benefits Model

5. Results

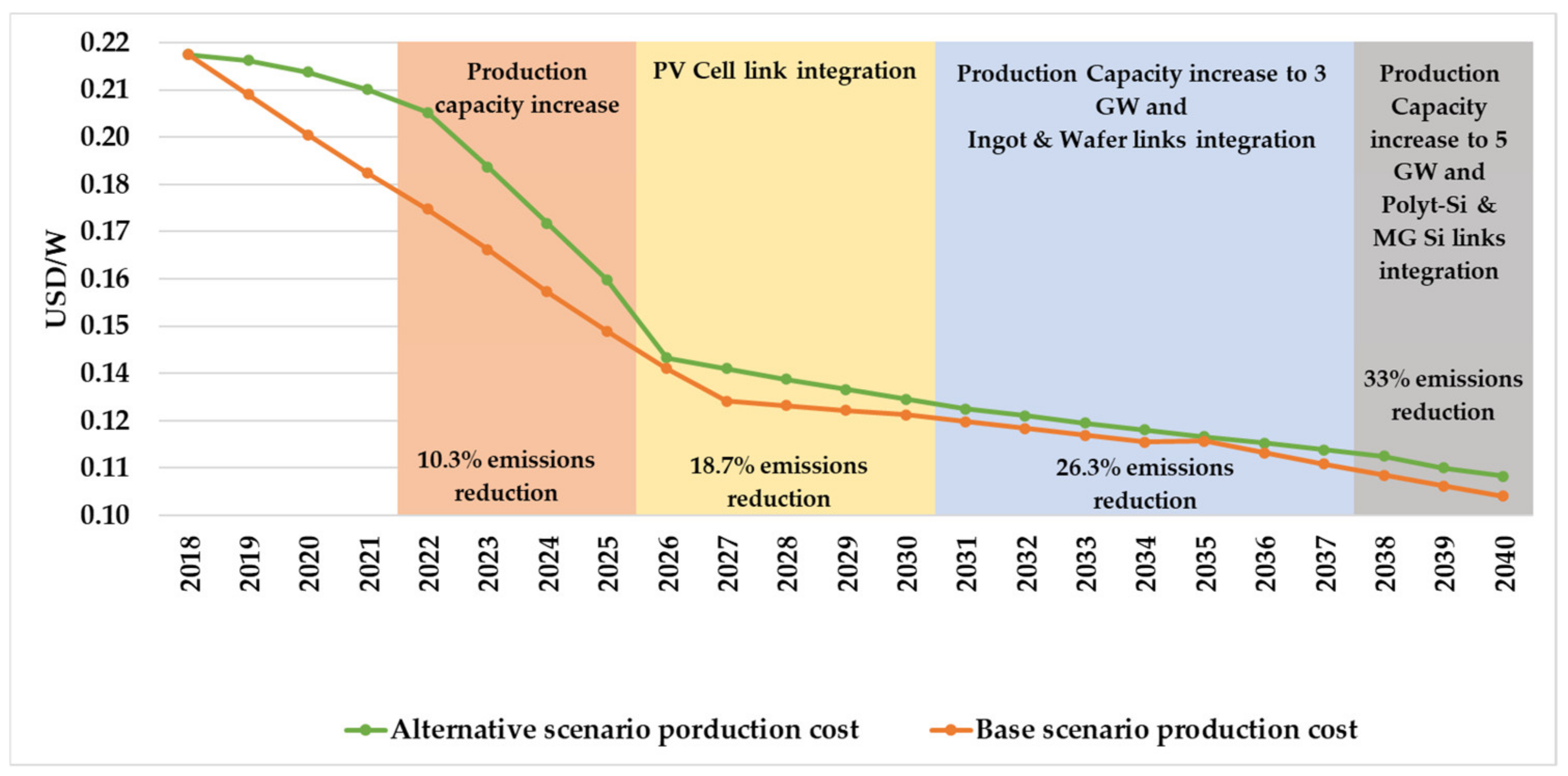

5.1. Baseline Scenario

5.2. Alternative Scenario

6. Conclusions

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| AS | Alternative Scenario |

| BS | Baseline Scenario |

| CINVESTAV | Spanish acronym for Center for Research and Advanced Studies |

| CFV | PV cells |

| CG | Centralized Generation |

| CVD | Chemical Vapor Deposition |

| Cz | Czochralski |

| DG | Distributed Generation |

| GHG | Greenhouse Gases |

| GW | Giga Watt |

| GWh | Giga Watt Hour |

| MFV | PV modules |

| MG-Si | Magnesium Silicide |

| MSP | Minimum Sustainable Price |

| MtCO2e | Million Tons of Carbon Dioxide Equivalent |

| MUSD | Million US Dollar |

| MW | Megawatt |

| O&M | Operations and maintenance |

| PCN | Proportion of national content |

| PCNB | Proportion of national content in the final good of the link |

| PCNM | Proportion of the value of national materials used to manufacture the final good of the link |

| Poly-Si | Polycrystalline silicon |

| PV | Photovoltaic |

| USD | US Dollar |

| VCPVIM | Value Chain of the PV Industry in Mexico |

| W | Watt |

References

- Porter, M. Competitive Strategy: The Core Concepts. In Competitive Advantage: Creating and Sustaining Superior Performance; The Free Press. A Division of Macmillan, Inc.: New York, NY, USA, 1985; p. 32. ISBN 0-02-925090-0. [Google Scholar]

- Kaplinsky, R.; Morris, M. A Handbook for Value Chain Research; University of Sussex, Institute of Development Studies: Brighton, UK, 2002; p. 113. [Google Scholar]

- Food and Agriculture Organization of the United Nations (FAO). Guidelines for Value Chain Analysis. Available online: https://www.fao.org/3/bq787e/bq787e.pdf (accessed on 9 December 2022).

- Helmsing, B.; Vellema, S. Value Chains Governance and Inclusive Endogenous Development: Towards a Knowledge Agenda; Development Policy Review Network (DPRN): Amsterdam, The Netherlands, 2011; p. 63. [Google Scholar]

- Bijman, J.; Ton, G. Producer Organisations and Value Chains. Capacit. Org. 2008, 34, 16. [Google Scholar]

- United States Agency for International Development (USAID). A Synthesis of Practical Lessons from Value Chain Projects in Conflict-Affected Environments, Report Value Chain Development in Conflict Affected Environments Project; USAID: Washington, DC, USA, 2008; p. 42.

- Bolwig, S. Integrating Poverty and Environmental Concerns into Value-Chain Analysis: A Conceptual Framework. Dev. Policy Rev. 2010, 28, 173–194. [Google Scholar] [CrossRef]

- Department for International Development (DFID). Private Sector Development Strategy Prosperity for All: Making Markets Work; DFID: London, UK, 2008; p. 52.

- Grossmann, H.; Bagwitz, D.; Elges, R.; Kruk, G.; Lange, R. Sustainable Economic Development in Conflict-Affected Environments: A Guidebook. Available online: https://reliefweb.int/report/world/sustainable-economic-development-conflict-affected-environments-guidebook (accessed on 9 December 2022).

- Chang, H. Industrial Policy: Can We Go beyond an Unproductive Confrontation? In Proceedings of the Annual World Bank Conference on Development Economics 2010, Global, Seoul, Republic of Korea, 22–24 June 2009; p. 27. [Google Scholar]

- Comisión Económica para América Latina y el Caribe (CEPAL). Theory and Practice of Industrial Policy. Evidence from the Latin American Experience; CEPAL: Santiago de Chile, Chile, 2009; p. 51. [Google Scholar]

- Lim, G.; Teo, J.K. Climbing the Economic Ladder: The Role of Outward Foreign Direct Investment. J. Asian Public Policy 2018, 12, 312–329. [Google Scholar] [CrossRef]

- Horner, R.; Alford, M. The Roles of the State in Global Value Chains: An Update and Emerging Agenda; GDI Working Paper 2019-036; The University of Manchester: Manchester, UK, 2019; p. 26. [Google Scholar]

- Altenburg, T.; Assmann, C. Green Industrial Policy: Concept, Policies, Country Experiences; UN Environment; German Development Institute/Deutsches Institut für Entwicklungspolitk (DIE): Geneva, Switzerland; Bonn, Germany, 2017; p. 240. [Google Scholar]

- United Nations Industrial Development Organization (UNIDO). Industrial Development Report 2018. Demand for Manufacturing: Driving Inclusive and Sustainable Industrial Development; UNIDO: Vienna, Austria, 2017; p. 274. ISBN 978-92-1-106455-1. [Google Scholar]

- Fay, M.; Hallegatte, S.; Vogt-Schilb, A.; Rozenberg, J.; Narloch, U.; Kerr, T.M. Decarbonizing Development: Three Steps to a Zero-Carbon Future. Climate Change and Development; World Bank Publications: Washington, DC, USA, 2015; ISBN 1-4648-0606-3. [Google Scholar]

- Srai, J.S.; Harrington, T.S.; Tiwari, M.K. Characteristics of Redistributed Manufacturing Systems: A Comparative Study of Emerging Industry Supply Networks. Int. J. Prod. Res. 2016, 54, 6936–6955. [Google Scholar] [CrossRef]

- Hsu, J.; Chuang, Y.P. International Technology Spillovers and Innovation: Evidence from Taiwanese High-Tech Firms. J. Int. Trade Econ. Dev. 2014, 23, 387–401. [Google Scholar] [CrossRef]

- Schwab, K. The Fourth Industrial Revolution. Economía 2016, XVI, 194–197. [Google Scholar]

- Borbonus, S. Generating Socio-Economic Values from Renewable Energies; Institute for Advanced Sustainability Studies (IASS): Postdam, Germany, 2017; p. 32. [Google Scholar]

- Zawaydeh, S. Economic, Environmental and Social Impacts of Development of Energy from Sustainable Resources—Case Study; World Energy Engineering Congress: Orlando, FL, USA, 2015; p. 21. [Google Scholar]

- International Renewable Energy Agency (IRENA). The Socio-Economic Benefits of Solar and Wind Energy; IRENA: Abu Dhabi, United Arab Emirates, 2014; p. 108. [Google Scholar]

- International Energy Agency (IEA). Renewables 2020. Analysis and Forecast to 2025; IEA: Paris, France, 2020; p. 172. [Google Scholar]

- International Renewable Energy Agency (IRENA). Global Energy Transformation: A Roadmap to 2050; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2019; p. 52. ISBN 978-92-9260-121-8. [Google Scholar]

- Wang, X.; Barnett, A. The Evolving Value of Photovoltaic Module Efficiency. Appl. Sci. 2019, 9, 1227. [Google Scholar] [CrossRef]

- Powell, D.M.; Fu, R.; Horowitz, K.; Basore, P.A.; Woodhouse, M.; Buonassisi, T. The Capital Intensity of Photovoltaics Manufacturing: Barrier to Scale and Opportunity for Innovation. Energy Environ. Sci. 2015, 8, 3395–3408. [Google Scholar] [CrossRef]

- Okioga, I.T.; Wu, J.; Sireli, Y.; Hendren, H. Renewable Energy Policy Formulation for Electricity Generation in the United States. Energy Strategy Rev. 2018, 22, 365–384. [Google Scholar] [CrossRef]

- Zou, H.; Du, H.; Ren, J.; Sovacool, B.K.; Zhang, Y.; Mao, G. Market Dynamics, Innovation, and Transition in China’s Solar Photovoltaic (PV) Industry: A Critical Review. Renew. Sustain. Energy Rev. 2017, 69, 197–206. [Google Scholar] [CrossRef]

- Ayoo, C. Towards Energy Security for the Twenty-First Century. In Energy Policy; Taner, T., Ed.; Intechopen: London, UK, 2020; p. 26. ISBN 978-1-78923-874-7. [Google Scholar]

- European Commission. A Clean Planet for All. A European Long-Term Strategic Vision for a Prosperous, Modern, Competitive and Climate Neutral Economy; European Commission: Brussels, Belgium, 2018; p. 25. [Google Scholar]

- Hache, E. Do Renewable Energies Improve Energy Security in the Long Run? Int. Econ. 2018, 156, 127–135. [Google Scholar] [CrossRef]

- International Renewable Energy Agency (IRENA). NDCs in 2020: Advancing Renewables in the Power Sector and Beyond; IRENA: Abu Dhabi, United Arab Emirates, 2019; p. 40. ISBN 978-92-9260-168-3. [Google Scholar]

- García-Gusano, D.; Iribarren, D. Prospective Energy Security Scenarios in Spain: The Future Role of Renewable Power Generation Technologies and Climate Change Implications. Renew. Energy 2018, 126, 202–209. [Google Scholar] [CrossRef]

- Wang, B.; Wang, Q.; Wei, Y.M.; Li, Z.P. Role of Renewable Energy in China’s Energy Security and Climate Change Mitigation: An Index Decomposition Analysis. Renew. Sustain. Energy Rev. 2018, 90, 187–194. [Google Scholar] [CrossRef]

- International Renewable Energy Agency (IRENA). Future of Solar Photovoltaic: Deployment, Investment, Technology, Grid Integration and Socio-Economic Aspects (A Global Energy Transformation: Paper); International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2019; p. 73. ISBN 978-92-9260-156-0. [Google Scholar]

- International Renewable Energy Agency (IRENA). Renewable Energy and Jobs: Annual Review 2019; IRENA: Abu Dhabi, United Arab Emirates, 2019; p. 40. [Google Scholar]

- Brown, M.; Wang, Y.; Sovacool, B.; D’Agostino, A. Forty Years of Energy Security Trends: A Comparative Assessment of 22 Industrialized Countries. Energy Res. Soc. Sci. 2014, 4, 64–77. [Google Scholar] [CrossRef]

- Silberglitt, R.S.; Bartis, J.T.; Chow, B.G.; An, D.L.; Brady, K. Critical Materials: Present Danger to U.S. Manufacturing; Rand Corporation: Santa Monica, CA, USA, 2013; ISBN 0-8330-7927-1. [Google Scholar]

- Lunde Seefeldt, J. Lessons from the Lithium Triangle: Considering Policy Explanations for the Variation in Lithium Industry Development in the “Lithium Triangle” Countries of Chile, Argentina, and Bolivia. Polit. Policy 2020, 48, 727–765. [Google Scholar] [CrossRef]

- European Commission. Report on Critical Raw Materials and the Circular Economy; Publications Office of the European Union: Brussels, Belgium, 2018; p. 78. ISBN 978-92-79-94626-4. [Google Scholar]

- Solar Energy Industries Association (SEIA). The Solar+ Decade & American Renewable Energy Manufacturing. 100 GW by 2030; Solar Energy Industries Association: Washington, DC, USA, 2020; p. 10. [Google Scholar]

- Shum, R.Y. Heliopolitics: The International Political Economy of Solar Supply Chains. Energy Strateg. Rev. 2019, 26, 100390. [Google Scholar] [CrossRef]

- Greentech InDetail. Polysilicon: Supply, Demand & Implications for the PV Industry; Greentech Media Inc.: Boston, MA, USA, 2008; p. 134. [Google Scholar]

- Bernreuter, J. Polysilicon Manufacturers: How the Ranking of the Top Ten Producers Has Been Whirled around Since 2004. Available online: https://www.bernreuter.com/polysilicon/manufacturers/ (accessed on 12 December 2022).

- Comisión Nacional de Hidrocarburos (CNH). Análisis de Reservas de Hidrocarburos 1P, 2P, 3P. Available online: https://www.gob.mx/cms/uploads/attachment/file/460767/Analisis_de_Reservas_1P_2P_3P_2019._vf-cnh-web.pdf (accessed on 12 December 2022).

- Secretaría de Energía (SENER). Balance Nacional de Energía 2018; SENER: Mexico City, Mexico, 2019; p. 125.

- de la Vega-Navarro, A. Énergies Fossiles et Énergies Renouvelables: La Place Du Mexique Dans l’ Intégration et La Transition Énergétique En Amérique Du Nord; Centre d’études et de recherches internationales, Université de Montréal: Montreal, QC, Canadá, 2017; p. 52. [Google Scholar]

- Winzer, C. Conceptualizing Energy Security. Energy Policy 2012, 46, 36–48. [Google Scholar] [CrossRef]

- Valentine, S.V. Emerging Symbiosis: Renewable Energy and Energy Security. Renew. Sustain. Energy Rev. 2011, 15, 4572–4578. [Google Scholar] [CrossRef]

- Jun, E.; Kim, W.; Chang, H. The Analysis of Security Cost for Different Energy Sources. Appl. Energy 2009, 86, 1894–1901. [Google Scholar] [CrossRef]

- Yergin, D. Ensuring Energy Security. Foreign Aff. 2006, 85, 69–82. [Google Scholar] [CrossRef]

- Intharak, N.; Julay, J.; Nakanishi, S.; Matsumoto, T.; Sahid, E.; Aquino, A. A Quest for Energy Security in the 21st Century; Asia Pacific Energy Research Centre: Tokyo, Japan, 2007; p. 113. [Google Scholar]

- Badea, A.; Rocco, S.; Tarantola, S.; Bolado, R. Composite Indicators for Security of Energy Supply Using Ordered Weighted Averaging. Reliab. Eng. Syst. Saf. 2011, 96, 651–662. [Google Scholar] [CrossRef]

- Grande-Acosta, G.; Islas-Samperio, J. Towards a Low-Carbon Electric Power System in Mexico. Energy Sustain. Dev. 2017, 37, 99–109. [Google Scholar] [CrossRef]

- García-Gusano, D.; Iribarren, D.; Garraín, D. Prospective Analysis of Energy Security: A Practical Life-Cycle Approach Focused on Renewable Power Generation and Oriented towards Policy-Makers. Appl. Energy 2017, 190, 891–901. [Google Scholar] [CrossRef]

- Sandor, D.; Fulton, S.; Engel-Cox, J.; Peck, C.; Peterson, S. System Dynamics of Polysilicon for Solar Photovoltaics: A Framework for Investigating the Energy Security of Renewable Energy Supply Chains. Sustainability 2018, 10, 160. [Google Scholar] [CrossRef]

- International Renewable Energy Agency (IRENA). REN 21. Renewables 2017 Global Status Report; IRENA: Paris, France, 2017; p. 302. ISBN 978-3-9818107-6-9. [Google Scholar]

- Johansson, B. Security Aspects of Future Renewable Energy Systems-A Short Overview. Energy 2013, 61, 598–605. [Google Scholar] [CrossRef]

- Klitkou, A.; Coenen, L. The Emergence of the Norwegian Solar Photovoltaic Industry in a Regional Perspective. Eur. Plan. Stud. 2013, 21, 1796–1819. [Google Scholar] [CrossRef]

- Dewald, D.; Truffer, B. Market Formation in Technological Innovation Systems—Diffusion of Photovoltaic Applications in Germany. Ind. Innov. 2011, 18, 285–300. [Google Scholar] [CrossRef]

- Gallagher, J.; Lopez, C.; Mah, J.; McGarrigle, A.; McGarrigle, P.; Olien, L. Alberta’s Solar PV Value Chain Opportunities; Solas Energy Consulting Inc.: Calgary, AB, Canada, 2018; p. 63. [Google Scholar]

- Sustainable Energy Authority of Ireland (SEAI). Ireland’s Solar Value Chain Opportunity; SEAI: Dublin, Ireland, 2017; p. 78. [Google Scholar]

- Johnson, O. Promoting Green Industrial Development through Local Content Requirements: India’s National Solar Mission. Clim. Policy 2016, 16, 178–195. [Google Scholar] [CrossRef]

- Meckling, J.; Hughes, L. Protecting Solar: Global Supply Chains and Business Power. New Polit. Econ. 2018, 23, 88–104. [Google Scholar] [CrossRef]

- Secretaría de Energía (SENER). Estrategia Nacional de Energía 2013–2027; SENER: Mexico City, México, 2013; p. 74.

- Diario Oficial de la Federación (DOF). Ley de La Industria Eléctrica. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5355986&fecha=11/08/2014#gsc.tab=0 (accessed on 12 December 2022).

- Diario Oficial de la Federación (DOF). Ley de Hidrocarburos. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5355989&fecha=11/08/2014#gsc.tab=0 (accessed on 12 December 2022).

- International Energy Agency (IEA). Solar PV Module Manufacturing and Demand 2014–2020. Available online: https://www.iea.org/data-and-statistics/charts/solar-pv-module-manufacturing-and-demand-2014-2020 (accessed on 12 December 2022).

- VDMA Photovoltaic Equipment. International Technology Roadmap for Photovoltaic (ITRPV)–2019 Results; VDMA: Frankfurt am Main, Germany, 2020; p. 88. [Google Scholar]

- Oliveira, V.D.D. Tapping of Metallurgical Silicon Furnaces–A Brief Comparison between Continuous and Discontinuous Processes; Furnace Tapping Conference 2018; Southern African Institute of Mining and Metallurgy: Kruger Park, South Africa, 2018; p. 13. [Google Scholar]

- Xakalashe, B.S.; Tangstad, M. Silicon Processing: From Quartz to Crystalline Silicon Solar Cells. In Proceedings of the Southern African Pyrometallurgy 2011 International Conference, Johannesburg, South African, 6–9 March 2011; p. 18. [Google Scholar]

- Myrvågnes, V. Analyses and Characterization of Fossil Carbonaceous Materials for Silicon Production. Ph.D. Thesis, Norwegian University of Science and Technology Faculty of Natural Sciences and Technology Department of Materials Science and Engineering, Torgarden, Norway, 2008; p. 248. [Google Scholar]

- National Renewable Energy Laboratory (NREL). Crystalline Silicon Photovoltaic Module Manufacturing Costs and Sustainable Pricing: 1H 2018 Benchmark and Cost Reduction Roadmap; NREL: Washington, DC, USA, 2020; p. 58.

- Fu, R.; James, T.L.; Woodhouse, M. Economic Measurements of Polysilicon for the Photovoltaic Industry: Market Competition and Manufacturing Competitiveness. IEEE J. Photovolt. 2015, 5, 515–524. [Google Scholar] [CrossRef]

- Kumar, A.; Bieri, M.; Reindl, T.; Aberle, A.G. Economic Viability Analysis of Silicon Solar Cell Manufacturing: Al-BSF versus PERC. Energy Procedia 2017, 130, 43–49. [Google Scholar] [CrossRef]

- REN21. Renewables 2020 Global Status Report; REN21 Secretariat: Paris, France, 2020; p. 367. ISBN 978-3-948393-00-7. [Google Scholar]

- Hannen, P. China Shakes PV World. Available online: https://www.pv-magazine.com/2018/06/05/china-shakes-pv-world/ (accessed on 10 November 2021).

- Shaw, V. China Releases New Provisions for PV Development in 2018. PV Magazine, 1 June 2018. Available online: https://www.pv-magazine.com/2018/06/01/china-releases-new-provisions-for-pv-development-in-2018/ (accessed on 12 November 2021).

- International Energy Agency (IEA PVPS). Trends in Photovoltaic Applications 2019; IEA PVPS: Rheine, Germany, 2019; p. 98. [Google Scholar]

- Clean Energy Council (CEC). Clean Energy Australia Report 2019. Clean Energy Council: Melbourne, Asutralia, 2019; p. 82. [Google Scholar]

- MERCOM. Clean Energy Insights, India’s Rooftop Solar Market–Where Is It Now and Where Is It Going? Available online: https://mercomindia.com/rooftop-solar-where-its-going-intersolar/ (accessed on 10 December 2021).

- SolarPowerEurope SolarPower Europe’s Global Market Outlook 2019–2023. Available online: https://www.solarpowereurope.org/insights/webinars/global-market-outlook-solar-2019-2023 (accessed on 26 February 2022).

- Centro de Investigación y de Estudios Avanzados del Instituto Politécnico Nacional (CINVESTAV). Historia Del Departamento de Ingeniería Eléctrica. Available online: https://ie.cinvestav.mx/conoce-ie/historia (accessed on 12 October 2020).

- Iniciativa Climática México (ICM). Instituto Nacional de Eletricidad y Energías Limpial (INEEL). Cadena de Valor de La Generación Distribuida Fotovoltaica En México; ICM, INEEL: Mexico City, México, 2019; p. 131.

- Bellini, E. Nadie Dijo Fácil: Industria En América Latina. Available online: https://www.pv-magazine-latam.com/2018/09/12/nadie-dijo-facil-industria-en-america-latina/ (accessed on 12 December 2022).

- Secretaría de Economía. Registro de Proveedores de La Industria Eléctrica. Available online: http://www.proveedores-energia.economia.gob.mx/regprov/#/busquedaPublica/electrica (accessed on 13 August 2018).

- Islas-Samperio, J.M.; Grande-Acosta, G.K.; Carrasco-González, F.; Valenzuela, J.M. La Era Fotovoltaica En México, 1st ed.; Reflexio, Academia y Comunicación, S. de R.L. y C.V.: Mexico City, México, 2020; ISBN 978-607-97089-2-4. [Google Scholar]

- Sánchez-Juárez, A.; Martínez-Escobar, D.; de la Luz Santos Magdaleno, R.; Ortega-Cruz, J.; Sánchez-Pérez, P.A. Aplicaciones Fotovoltaicas de La Energía Solar En Los Sectores Residencial, Servicio e Industrial, 1st ed.; Mazón, J.T., Ed.; Consejo Nacional de Ciencia y Tecnología (CONACYT): Mexico City, Mexico, 2017; p. 316. ISBN 978-5-230-41732-3.

- Auditoria Superior de la Federación (ASF). Informe Del Resultado de La Fiscalización Superior de La Cuenta Pública 2011. Available online: https://www.asf.gob.mx/uploads/55_Informes_de_auditoria/Mensaje_IRCP_2011.pdf (accessed on 12 December 2022).

- Asociación Mexicana de Energía Solar (ASOLMEX). Centrales Solares. Available online: https://asolmex.org/centrales-solares/ (accessed on 12 November 2020).

- Comisión Reguladora de Energía (CRE). Contratos Interconexión de Pequeña y Mediana Escala/Generación Distribuida Solicitudes de Interconexión de Centrales Eléctricas Con Capacidad Menor a 0.5 MW; CRE: Mexico City, México, 2022; p. 8.

- Instituto Nacional de Ecología y Cambio Climático (INECC). Inventario Nacional de Emisiones de Gases y Compuestos de Efecto Invernadero (INEGYCEI), 1990–2020; INECC: Mexico City, México, 2022.

- Secretaría de Energía (SENER). Balance Nacional de Energía 2017; SENER: Mexico City, México, 2018; p. 129.

- Secretaría de Energía (SENER). Programa de Desarrollo Del Sistema Eléctrico Nacional (PRODESEN) 2019–2033. Available online: https://www.gob.mx/sener/articulos/prodesen-2019-2033-221654 (accessed on 12 December 2022).

- Secretería de Energía (SENER). Mapa de Ruta Tecnológica Para La Industria Solar Fotovoltaica; SENER: Mexico City, México, 2017; p. 72.

- Instituto Mexicano del Petróleo (IMP). Reporte de Inteligencia Tecnológica-Energía Solar Fotovoltaica; IMP: Mexico City, México, 2017; p. 84.

- Instituto Mexicano del Petróleo (IMP). Cartera de Necesidades de Innovación y Desarrollo Tecnológico: Energía Solar Fotovoltaica; Towards Energy Security for the Twenty-First Century; IMP: Mexico City, México, 2017; p. 39.

- Castellanos, S.; Santibañez-Aguilar, J.E.; Shapiro, B.B.; Powell, D.M.; Peters, I.M.; Buonassisi, T.; Kammen, D.M.; Flores-Tlacuahuac, A. Sustainable Silicon Photovoltaics Manufacturing in a Global Market: A Techno-Economic, Tariff and Transportation Framework. Appl. Energy 2018, 212, 704–719. [Google Scholar] [CrossRef]

- Comisión de Estudios del Sector Privado para el Desarrollo Sustentable (CESPEDES); C.C.E. (CCE). Estudio de Energías Limpias En México 2018–2032; CESPEDES, CCE: Mexico City, Mexico, 2015; p. 72.

- The Energy and Resources Institute (TERI). Policy Paper on Solar PV Manufacturing in India: Silicon Ingot & Wafer-PV Cell-PV Module; TERI: New Delhi, India, 2019; p. 33. [Google Scholar]

- Secretaría de Energía (SENER). Sistema de Información Geográfica (SIE). Estadísticas Energéticas Nacionales. Balance Nacional de Energía. Available online: https://sie.energia.gob.mx/ (accessed on 30 June 2018).

- FerroAlloyNet. Silicon Metal Market Information. Available online: https://www.ferroalloynet.com/siliconmetal/ (accessed on 13 December 2022).

- US. Geological Survey (USGS). Mineral Industry Surveys—Silicon in September 2020; USGS: Reston, VA, USA, 2020.

- PVinsights. PV Industry Supplies Spot Prices. Available online: http://pvinsights.com/ES/ (accessed on 18 October 2020).

- Alibaba. Categories. Metals & Alloys/Chemicals/Rubber & Plastics. Available online: https://cutt.ly/m0z0a5Q (accessed on 16 March 2022).

- Comisión Federal de Electricidad (CFE). Tarifas Eléctricas Para El Sector Industrial a Nivel Nacional. Available online: https://app.cfe.mx/Aplicaciones/CCFE/Tarifas/TarifasCREIndustria/Industria.aspx (accessed on 13 April 2019).

- Sistema Nacional de Empleo (SNE). Estadísticas de Carreras Profesionales Por Área. Available online: http://www.observatoriolaboral.gob.mx/static/estudios-publicaciones/Ingenierias.html (accessed on 20 October 2019).

- Instituto Nacional de Estadística y Geografía (INEGI). Banco de Información Económica. Salarios En México Por Subsector de Actividad de En La Industria Manufacturera. Available online: https://www.inegi.org.mx/sistemas/bie/ (accessed on 12 January 2020).

- Centro Nacional de Control de Energía (CENACE). Programa de Ampliación y Modernización de La Red Nacional de Transmisión y Redes Generales de Distribución Del Mercado Eléctrico Mayorista 2019–2033; CENACE: Mexico City, Mexico, 2019; p. 576.

- Instituto Nacional de Estadística y Geografía (INEGI). Matriz Insumo-Producto 2017 Base 2013. Available online: https://www.inegi.org.mx/programas/mip/2013/ (accessed on 20 August 2017).

- Kavlak, G.; McNerney, J.; Trancik, J.E. Evaluating the Causes of Cost Reduction in Photovoltaic Modules. Energy Policy 2018, 123, 700–710. [Google Scholar] [CrossRef]

- Maycock, P.D. Cost Reduction in PV Manufacturing: Impact on Grid-Connected and Building-Integrated Markets. Sol. Energy Mater. Sol. Cells 1997, 47, 37–45. [Google Scholar] [CrossRef]

- Nemet, G.F. Beyond the Learning Curve: Factors Influencing Cost Reductions in Photovoltaics. Energy Policy 2006, 34, 3218–3232. [Google Scholar] [CrossRef]

- VDMA. Photovoltaic Equipment International Technology Roadmap for Photovoltaics (ITRPV)—2017 Results; VDMA: Frankfurt am Main, Germany, 2018; p. 71. [Google Scholar]

- Maycock, P.; Bradford, T. PV Technology, Performance, and Cost, 2007 Update; Prometheus Institute for Sustainable Development and PV Energy Systems: Cambridge, MA, USA, 2007. [Google Scholar]

- Goodrich, A.; Hacke, P.; Wang, Q.; Sopori, B.; Margolis, R.; James, T.L.; Woodhouse, M. A Wafer-Based Monocrystalline Silicon Photovoltaics Road Map: Utilizing Known Technology Improvement Opportunities for Further Reductions in Manufacturing Costs. Sol. Energy Mater. Sol. Cells 2013, 114, 110–135. [Google Scholar] [CrossRef]

- National Renewable Energy Laboratory (NREL). Solar PV Manufacturing Cost Analysis: U.S. Competitiveness in a Global Industry; NREL: Washington, DC, USA, 2011; p. 45.

- Needleman, D.B.; Poindexter, J.R.; Kurchin, R.C.; Marius Peters, I.; Wilson, G.; Buonassisi, T. Economically Sustainable Scaling of Photovoltaics to Meet Climate Targets. Energy Environ. Sci. 2016, 9, 2122–2129. [Google Scholar] [CrossRef]

- Powell, D.M.; Winkler, M.T.; Goodrich, A.; Buonassisi, T. Modeling the Cost and Minimum Sustainable Price of Crystalline Silicon Photovoltaic Manufacturing in the United States. IEEE J. Photovolt. 2013, 3, 662–668. [Google Scholar] [CrossRef]

- Fazzari, M.C.; Petersen, B.C. Working Capital and Fixed Investement: New Evidence on Financing Constraints. Rand J. Econ. 1993, 24, 328–342. [Google Scholar] [CrossRef]

- Diario Oficil de la Federación (DOF). Acuerdo Por El Que Se Establece La Metodología Para La Medición Del Contenido Nacional En Asignaciones y Contratos Para La Exploración y Extracción de Hidrocarburos, Así Como Para Los Permisos En La Industria de Hidrocarburos. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5368123&fecha=13/11/2014#gsc.tab=0 (accessed on 12 December 2022).

- Diario Oficial de la Federación (DOF). Reglas Para La Determinación, Acreditación y Verificación Del Contenido Nacional de Los Bienes Que Se Ofertan y Entregan En Los Procedimientos de Contratación, Así Como Para La Aplicación Del Requisito de Contenido Nacional En La Contratación de Obras Públicas. Available online: https://dof.gob.mx/nota_detalle.php?codigo=5163202&fecha=14/10/2010#gsc.tab=0 (accessed on 12 December 2022).

- Diario Oficial de la Federación (DOF). Acuerdo Por El Que Se Establecen Las Reglas Para La Determinación y Acreditación Del Grado de Contenido Nacional, Tratándose de Procedimientos de Contratación de Carácter Nacional. Available online: https://www.gob.mx/cms/uploads/attachment/file/50539/A162.pdf (accessed on 12 December 2022).

- Torre Cepeda, L.E.; Alvarado Ruiz, J.A.; Quiroga Treviño, M. Matrices Insumo-Producto Regionales: Una Aplicación al Sector Automotriz En México; Banco de Mexico: Mexico City, Mexico, 2017; p. 48. [Google Scholar]

- Diario Oficial de la Federación (DOF). Ley de Transición Energética. Available online: https://dof.gob.mx/nota_detalle.php?codigo=5421295&fecha=24/12/2015#gsc.tab=0 (accessed on 12 December 2022).

- United Nations Framework Convention on Climate Change (UNFCC). Intended Nationally Determined Contributions (INDCs). México. Available online: http://unfccc.int/files/adaptation/application/pdf/all__parties_indc.pdf (accessed on 12 December 2022).

- International Renewable Energy Agency (IRENA). Renewable Energy and Jobs–Annual Review 2020; IRENA: Abu Dhabi, United Arab Emirates, 2020; p. 44. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| No. | Company | Country | Production Capacity (tons) |

|---|---|---|---|

| 1 | Tongwei | China | 96,000 |

| 2 | GCL-Poly Energy | China | 88,000 |

| 3 | Wacker Chemie | Germany | 81,000 |

| 4 | Xinte Energy | China | 80,000 |

| 5 | Daqo Group | China | 80,000 |

| 6 | East Hope New Energy | China | 80,000 |

| 7 | OCI | South Korea | 36,500 |

| 8 | Hemlock | USA | 36,000 |

| 9 | Asia Silicon | China | 20,000 |

| 10 | REC Silicon | Norway | 20,000 |

| 11 | Dunan PV Techonolgy | China | 10,000 |

| 12 | Otras | Others | 70,000 |

| No. | Company | Mexican State | Production Capacity (MW) |

|---|---|---|---|

| 1 | IUSASOL | Estado de México | 500 |

| 2 | ERDM Solar | Veracruz | 200 |

| 3 | Solarever | Hidalgo | 100 |

| 4 | Xtender Solar | Baja California | 150 |

| 5 | SAYA | Aguascalientes | 100 |

| 6 | Solartec | Guanajuato | 100 |

| 7 | Solarsol | Yucatán | 20 |

| 8 | Solarvatio | Oaxaca | 6 |

| 9 | Sydemex Solar | Colima | 6 |

| Mexican State | Installed Capacity (MW) | PV Plants (#) | PV Generation (GWh) | |||

|---|---|---|---|---|---|---|

| Centralized Generation | Distributed Generation | Centralized Generation | Distributed Generation | Centralized Generation | Distributed Generation | |

| Aguascalientes | 915 | 62 | 8 | 6467 | 2590 | 117 |

| Baja California | 46 | 64 | 2 | 10,388 | 130 | 112 |

| Baja California Sur | 56 | 21 | 3 | 1632 | 159 | 38 |

| Campeche | 0 | 12 | 0 | 1515 | 0 | 18 |

| Chiapas | 0 | 13 | 0 | 1637 | 0 | 21 |

| Chihuahua | 622 | 136 | 16 | 21,062 | 1761 | 252 |

| Ciudad de México | 2 | 103 | 1 | 13,967 | 6 | 176 |

| Coahuila | 842 | 85 | 5 | 10,960 | 2384 | 147 |

| Colima | 0 | 36 | 0 | 6451 | 0 | 60 |

| Durango | 303 | 36 | 15 | 4106 | 858 | 66 |

| Estado de México | 19 | 120 | 2 | 10,143 | 54 | 202 |

| Guanajuato | 314 | 118 | 5 | 12,880 | 889 | 220 |

| Guerrero | 0 | 18 | 0 | 2432 | 0 | 31 |

| Hidalgo | 118 | 15 | 2 | 1399 | 334 | 26 |

| Jalisco | 128 | 308 | 4 | 49,949 | 362 | 557 |

| Michoacán | 0 | 90 | 0 | 13,574 | 0 | 152 |

| Morelos | 0 | 32 | 0 | 5301 | 0 | 58 |

| Nayarit | 0 | 38 | 0 | 5626 | 0 | 66 |

| Nuevo León | 30 | 218 | 1 | 29,177 | 85 | 351 |

| Oaxaca | 0 | 14 | 0 | 1635 | 0 | 22 |

| Puebla | 221 | 36 | 1 | 4615 | 626 | 62 |

| Queretaro | 1 | 40 | 1 | 6676 | 3 | 74 |

| Quintana Roo | 2 | 28 | 2 | 3969 | 6 | 44 |

| San Luis Potosí | 564 | 39 | 4 | 5653 | 1597 | 69 |

| Sinaloa | 0 | 59 | 0 | 4122 | 0 | 103 |

| Sonora | 1231 | 84 | 15 | 8998 | 3485 | 151 |

| Tabasco | 0 | 13 | 0 | 1529 | 0 | 20 |

| Tamaulipas | 0 | 34 | 0 | 3448 | 0 | 54 |

| Tlaxcala | 220 | 3 | 1 | 280 | 623 | 6 |

| Veracruz | 0 | 51 | 0 | 6502 | 0 | 75 |

| Yucatán | 52 | 87 | 2 | 12,458 | 147 | 131 |

| Zacatecas | 345 | 17 | 3 | 1955 | 977 | 32 |

| Total | 6031 | 2031 | 93 | 270,506 | 17,076 | 3513 |

| Variable/Input | Cost/Parameter | References | |

|---|---|---|---|

| MFV efficiency | 18.4 | % | [69,73,102,103] |

| Poly-Si total material consumption | 0.1 | g/μm | |

| Poly-Si use per CFV | 3.0 | g/W | |

| CFV thickness | 160 | Μm | |

| Number of CFV per MFV | 60 | CFV | |

| MFV output | 310 | Wp | |

| CFV | 0.094 | USD/W | [104] |

| Aluminum frame | 1.25 | USD/m | [73,105] |

| Silicone sealant | 0.06 | ||

| Back Sheet (EVA) | 2.3 | USD/m2 | |

| Encapsulant | 1.1 | ||

| Glass sheet | 3.9 | ||

| Connector tapes | 0.9 | ||

| Junction Box | 3.4 | USD/MFV | |

| Potting agent | 1.3 | ||

| Electricity | 0.058 | USD/kWh | [106,107,108] |

| Operator wage | 0.6 | USD/h | |

| Technician wage | 0.8 | USD/h | |

| Supervisor wage | 2.6 | USD/h | |

| Total equipment yield | 96 | % | [69,73] |

| Year | Cumulative Production Capacity(MW) | Average Cumulative Production Capacity (MW) | AGR a |

|---|---|---|---|

| 2006 | 100 | 100 | 0.000 |

| 2007 | 300 | 400 | 3.000 |

| 2008 | 300 | 350 | −0.125 |

| 2009 | 550 | 417 | 0.190 |

| 2010 | 550 | 450 | 0.080 |

| 2011 | 550 | 470 | 0.044 |

| 2012 | 650 | 500 | 0.064 |

| 2013 | 655 | 522 | 0.044 |

| 2014 | 1180 | 604 | 0.157 |

| 2015 | 1180 | 668 | 0.106 |

| 2016 | 1180 | 720 | 0.077 |

| 2017 | 1180 | 761 | 0.058 |

| 2018 | 1180 | 796 | 0.046 |

| 2018 | 2024 | 2030 | 2040 | |

|---|---|---|---|---|

| Cumulative capacity (MW) | ||||

| Conventional energy | 54,492 | 70,426 | 78,403 | 95,704 |

| Solar PV | 6293 | 17,582 | 26,740 | 82,299 |

| Centralized | 5377 | 15,254 | 20,824 | 54,299 |

| Distributed | 916 | 2328 | 5916 | 28,000 |

| Other clean energies | 18,714 | 32,374 | 38,940 | 56,643 |

| Cumulative generation (GWh) | ||||

| Conventional energy | 232,995 | 270,543 | 308,958 | 402,367 |

| Solar PV | 4042 | 30,606 | 53,876 | 165,816 |

| Centralized | 3454 | 26,554 | 41,956 | 109,402 |

| Distributed | 588 | 4052 | 11,920 | 56,414 |

| Other clean energies | 79,704 | 118,988 | 142,919 | 193,255 |

| Generation share (%) | ||||

| Conventional energy | 73.7 | 64.4 | 61.1 | 52.8 |

| Solar PV | 1.3 | 7.3 | 10.7 | 21.8 |

| Other clean energies | 25.0 | 28.3 | 28.2 | 25.4 |

| GHG emissions (MtCO2e) | ||||

| No clean energy increase | 102.0 | 781.6 | 1593.0 | 3301.1 |

| With clean energy increase | 102.0 | 634.5 | 1195.3 | 2286.6 |

| Year | National Demand | Production Capacity | Imports | Assembling Cost | CFV Cost (Imported) | MSP | Sales | Imports |

|---|---|---|---|---|---|---|---|---|

| (MW) | (USD/W) | |||||||

| 2018 | 6293 | 1182 | 5111 | 0.217 | 0.094 | 0.249 | 294.3 | 1001.8 |

| 2019 | 4727 | 1182 | 3545 | 0.207 | 0.090 | 0.237 | 280.5 | 659.5 |

| 2020 | 3610 | 1182 | 2428 | 0.197 | 0.085 | 0.226 | 266.7 | 428.7 |

| 2021 | 732 | 1182 | - | 0.187 | 0.081 | 0.215 | 253.6 | - |

| 2022 | 246 | 1182 | - | 0.178 | 0.077 | 0.204 | 241.1 | - |

| 2023 | 849 | 1182 | - | 0.167 | 0.073 | 0.192 | 227.2 | - |

| 2024 | 1125 | 1182 | - | 0.157 | 0.068 | 0.180 | 212.7 | - |

| 2025 | 1142 | 1182 | - | 0.147 | 0.064 | 0.168 | 199.0 | - |

| 2026 | 1135 | 1182 | - | 0.137 | 0.059 | 0.158 | 186.3 | - |

| 2027 | 1128 | 1182 | - | 0.129 | 0.056 | 0.148 | 175.0 | - |

| 2028 | 1494 | 1182 | - | 0.128 | 0.055 | 0.147 | 173.4 | - |

| 2029 | 2172 | 1182 | - | 0.127 | 0.055 | 0.145 | 171.8 | - |

| 2030 | 2087 | 1182 | 290 | 0.125 | 0.054 | 0.144 | 170.3 | 32.8 |

| 2031 | 2735 | 2182 | 553 | 0.124 | 0.054 | 0.142 | 310.1 | 61.9 |

| 2032 | 2902 | 2182 | 720 | 0.122 | 0.053 | 0.140 | 305.7 | 79.7 |

| 2033 | 3071 | 2182 | 889 | 0.120 | 0.052 | 0.138 | 301.3 | 97.3 |

| 2034 | 4470 | 2182 | 2288 | 0.119 | 0.051 | 0.136 | 297.0 | 247.5 |

| 2035 | 5056 | 2182 | 2874 | 0.119 | 0.051 | 0.136 | 297.7 | 307.4 |

| 2036 | 5723 | 2182 | 3541 | 0.116 | 0.050 | 0.133 | 290.3 | 373.6 |

| 2037 | 6481 | 2182 | 4299 | 0.113 | 0.049 | 0.130 | 283.1 | 447.6 |

| 2038 | 7344 | 2182 | 5162 | 0.110 | 0.048 | 0.127 | 276.1 | 530.2 |

| 2039 | 8328 | 2182 | 6146 | 0.108 | 0.047 | 0.123 | 269.3 | 622.7 |

| 2040 | 9449 | 3182 | 6267 | 0.105 | 0.045 | 0.120 | 383.1 | 626.7 |

| Total | 82,299 | 38,186 | 44,113 | - | - | - | 5865.4 | 5517.4 |

| National Content Proportion Type | VCPVIM Link |

|---|---|

| MFV | |

| PCNM | 0.06 |

| PCNM + PCNB | 0.08 |

| PCN | 0.08 |

| Sector | Multiplier | Employment (#) | Added Value (MUSD) | |

|---|---|---|---|---|

| Employment | Added Value | |||

| Construction industry | 0.00025 | 4.61 | 36,778 | 688.3 |

| Manufacture of cardboard and paper products | 0.000029 | 0.61 | 257 | 4.3 |

| Grocery and food wholesale | 0.000351 | 6.95 | 5004 | 88.7 |

| Grocery and food retail sale | 0.000115 | 2.30 | 1641 | 29.3 |

| Direct | 1025 | 756.5 | ||

| Total | 44,706 | 1567.2 | ||

| Year | National Demand | Production Capacity | Imports | Assembling Cost | MSP | Sales | Imports |

|---|---|---|---|---|---|---|---|

| (MW) | (USD/W) | ||||||

| 2018 | 6293 | 1182 | 5111 | 0.217 | 0.249 | 294.3 | 1001.8 |

| 2019 | 4727 | 1182 | 3545 | 0.211 | 0.243 | 287.1 | 659.5 |

| 2020 | 3610 | 1182 | 2428 | 0.205 | 0.237 | 280.0 | 428.7 |

| 2021 | 732 | 1182 | - | 0.200 | 0.231 | 273.0 | - |

| 2022 | 246 | 2182 | - | 0.183 | 0.213 | 464.2 | - |

| 2023 | 849 | 2182 | - | 0.182 | 0.212 | 462.3 | - |

| 2024 | 1125 | 2182 | - | 0.181 | 0.211 | 460.4 | - |

| 2025 | 1142 | 2182 | - | 0.179 | 0.210 | 458.5 | - |

| 2026 | 1135 | 2182 | - | 0.165 | 0.193 | 422.1 | - |

| 2027 | 1128 | 2182 | - | 0.163 | 0.192 | 418.6 | - |

| 2028 | 1494 | 2182 | - | 0.161 | 0.190 | 415.0 | - |

| 2029 | 2172 | 2182 | - | 0.159 | 0.189 | 411.5 | - |

| 2030 | 2087 | 2182 | - | 0.157 | 0.187 | 408.0 | - |

| 2031 | 2735 | 3182 | - | 0.127 | 0.151 | 481.5 | - |

| 2032 | 2902 | 3182 | - | 0.125 | 0.150 | 476.6 | - |

| 2033 | 3071 | 3182 | - | 0.123 | 0.148 | 471.7 | - |

| 2034 | 4470 | 3182 | - | 0.122 | 0.147 | 466.8 | - |

| 2035 | 5056 | 3182 | - | 0.120 | 0.145 | 462.0 | - |

| 2036 | 5723 | 3182 | - | 0.119 | 0.144 | 457.3 | - |

| 2037 | 6481 | 3182 | 2753 | 0.117 | 0.142 | 452.6 | 286.6 |

| 2038 | 7344 | 5182 | 2162 | 0.115 | 0.140 | 724.2 | 222.1 |

| 2039 | 8328 | 5182 | 3146 | 0.112 | 0.137 | 711.6 | 318.8 |

| 2040 | 9449 | 5182 | 4267 | 0.110 | 0.135 | 699.3 | 426.7 |

| Total | 82,299 | 62,186 | 23,412 | - | - | 10,458.7 | 3344.1 |

| VCPVIM Integrated Links and Year of Integration | |||||

|---|---|---|---|---|---|

| 2018 | 2026 | 2031 | 2038 | 2040 | |

| MFV | MFV+CFV | MFV+CFV+Ingot | MFV+CFV+Ingot+Poly-Si+MG-Si | MFV+CFV+Ingot+Poly-Si+MG-Si | |

| Material/input/parameter | (USD/W) | ||||

| MG-Si | - | - | - | - | - |

| Poly-Si * | - | - | 0.018 | - | - |

| Ingot * | - | 0.032 | - | - | - |

| CFV * | 0.094 | - | - | - | - |

| Materials | 0.102 | 0.079 | 0.080 | 0.074 ** | 0.069 ** |

| Depreciation | 0.012 | 0.012 | 0.013 | 0.013 | 0.013 |

| Maintenance | 0.003 | 0.004 | 0.004 | 0.006 | 0.006 |

| Labor | 0.004 | 0.005 | 0.004 | 0.008 | 0.008 |

| Electricity | 0.002 | 0.008 | 0.008 | 0.014 | 0.014 |

| Total cost | 0.217 | 0.140 | 0.127 | 0.115 | 0.110 |

| MSP | 0.249 | 0.164 | 0.151 | 0.140 | 0.135 |

| Reduction due to integration and/or development | (%) | ||||

| Technological progress | 0.0 | 12.4 | 15.9 | 32.3 | 35.5 |

| Economies of scale | 0.0 | 0.0 | 11.7 | 13.7 | 13.8 |

| Integrated Links | ||||

|---|---|---|---|---|

| 2018 | 2026 | 2031 | 2038 | |

| MFV | MFV+CFV | MFV+CFV+Ingot | MFV+CFV+ Ingot+ Poly-Si+MG-Si | |

| VCPVIM Link | ||||

| MFV | 6% | 100% | 100% | 100% |

| CFV | 0 | 45% | 100% | 100% |

| Ingot | 0 | 0 | 28% | 73% |

| Poly-Si | 0 | 0 | 0 | 100% |

| MG-Si | 0 | 0 | 0 | 60% |

| Integrated Links | ||||

|---|---|---|---|---|

| 2018 | 2026 | 2031 | 2038 | |

| MFV | MFV+CFV | MFV+CFV+ Ingot | MFV+CFV+ Ingot+Poly-Si+MG-Si | |

| VCPVIM link | ||||

| MFV | 0.08 | 0.46 | 0.41 | 0.38 |

| CFV | 0.0 | 0.22 | 0.26 | 0.26 |

| Ingot | 0.0 | 0.0 | 0.09 | 0.09 |

| Poly-Si | 0.0 | 0.0 | 0.0 | 0.12 |

| MG-Si | 0.0 | 0.0 | 0.0 | 0.04 |

| PCN Total | 0.08 | 0.68 | 0.76 | 0.89 |

| Sector | Multiplier | Employment (#) | Added Value (MUSD) | |

|---|---|---|---|---|

| Employment | Added Value | |||

| Construction Industry | 0.0000308 | 5.77 | 373,179 | 6984.2 |

| Felling of trees | 0.0000306 | 0.93 | 123 | 3.7 |

| Coal mining | 0.0000121 | 0.74 | 25 | 1.5 |

| Metal ore mining | 0.00000913 | 0.98 | 2269 | 245.9 |

| Non-metallic mineral mining | 0.0000465 | 0.98 | 30 | 0.6 |

| Mining related services | 0.00000758 | 0.59 | 1905 | 149.1 |

| Gas supply through pipelines to the final consumer | 0.00000000130 | 0.45 | 0 | 0.4 |

| Manufacture of cardboard and paper products | 0.0000292 | 0.61 | 538 | 11.3 |

| Manufacture of petroleum and coal products | 0.000303 | 5.32 | 159 | 2.8 |

| Manufacture of basic chemicals | 0.0000715 | 1.77 | 12,470 | 332.0 |

| Manufacture of paints, coatings and adhesives | 0.0000141 | 0.43 | 110 | 3.4 |

| Manufacture of other chemical products | 0.0000217 | 0.52 | 4,815 | 121.1 |

| Manufacture of plastic products | 0.0000415 | 0.76 | 4,747 | 86.8 |

| Manufacture of refractory clay and mineral-based products | 0.0000183 | 0.37 | 505 | 10.1 |

| Manufacture of glass and glass products | 0.0000189 | 0.50 | 3438 | 90.3 |

| Basic aluminum industry | 0.00000674 | 0.35 | 1586 | 83.8 |

| Manufacture of agricultural machinery and equipment, for construction and for the extractive industry | 0.00000923 | 0.34 | 37 | 1.4 |

| Manufacture of machinery and equipment for the metalworking industry | 0.0000122 | 0.35 | 339 | 9.6 |

| Manufacture of electrical power generation and distribution equipment | 0.0000110 | 0.27 | 2068 | 49.9 |

| Manufacture of other electrical equipment and accessories | 0.0000151 | 0.39 | 7595 | 215.9 |

| Grocery and food wholesale | 0.000351 | 6.95 | 23,559 | 423.8 |

| Grocery and food retail sale | 0.000115 | 2.30 | 7726 | 140.1 |

| Direct | 10,364 | 3194.2 | ||

| Total | 457,586 | 12,161.9 | ||

| Scenario Period | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| PVIVCM Link | 2019–2021 | 2022–2025 | 2026–2030 | 2031–2037 | 2038–2040 | |||||

| Production Capacity | ||||||||||

| 1182 MW | 2182 MW | 2182 MW | 3182 MW | 5182 MW | ||||||

| Jobs (#) | Added Value (MUSD) | Jobs (#) | Added Value (MUSD) | Jobs (#) | Added Value (MUSD) | Jobs (#) | Added Value (MUSD) | Jobs (#) | Added Value (MUSD) | |

| MFV | 4410 | 270 | 27,246 | 1177 | 14,169 | 913 | 37,804 | 1865 | 104,488 | 3640 |

| CFV | 0 | 0.0 | 0 | 0.0 | 63,103 | 1736 | 41,830 | 1491 | 162,672 | 3973 |

| Ingot | 0 | 0.0 | 0 | 0.0 | 0 | 0.0 | 31,868 | 1268 | 50,606 | 1350 |

| Poly-Si | 0 | 0.0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0 | 116,960 | 2593 |

| MG-Si | 0 | 0.0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0 | 22,860 | 592 |

| Total | 4410 | 270 | 27,246 | 1177 | 77,272 | 2649 | 111,502 | 4624 | 457,586 | 12,162 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Birlain-Escalante, M.O.; Islas-Samperio, J.M.; Vega-Navarro, Á.d.l.; Morales-Acevedo, A. Development and Upstream Integration of the Photovoltaic Industry Value Chain in Mexico. Energies 2023, 16, 2072. https://doi.org/10.3390/en16042072

Birlain-Escalante MO, Islas-Samperio JM, Vega-Navarro Ádl, Morales-Acevedo A. Development and Upstream Integration of the Photovoltaic Industry Value Chain in Mexico. Energies. 2023; 16(4):2072. https://doi.org/10.3390/en16042072

Chicago/Turabian StyleBirlain-Escalante, Mariano O., Jorge M. Islas-Samperio, Ángel de la Vega-Navarro, and Arturo Morales-Acevedo. 2023. "Development and Upstream Integration of the Photovoltaic Industry Value Chain in Mexico" Energies 16, no. 4: 2072. https://doi.org/10.3390/en16042072

APA StyleBirlain-Escalante, M. O., Islas-Samperio, J. M., Vega-Navarro, Á. d. l., & Morales-Acevedo, A. (2023). Development and Upstream Integration of the Photovoltaic Industry Value Chain in Mexico. Energies, 16(4), 2072. https://doi.org/10.3390/en16042072