National Security as a Value-Added Proposition for Advanced Nuclear Reactors: A U.S. Focus

Abstract

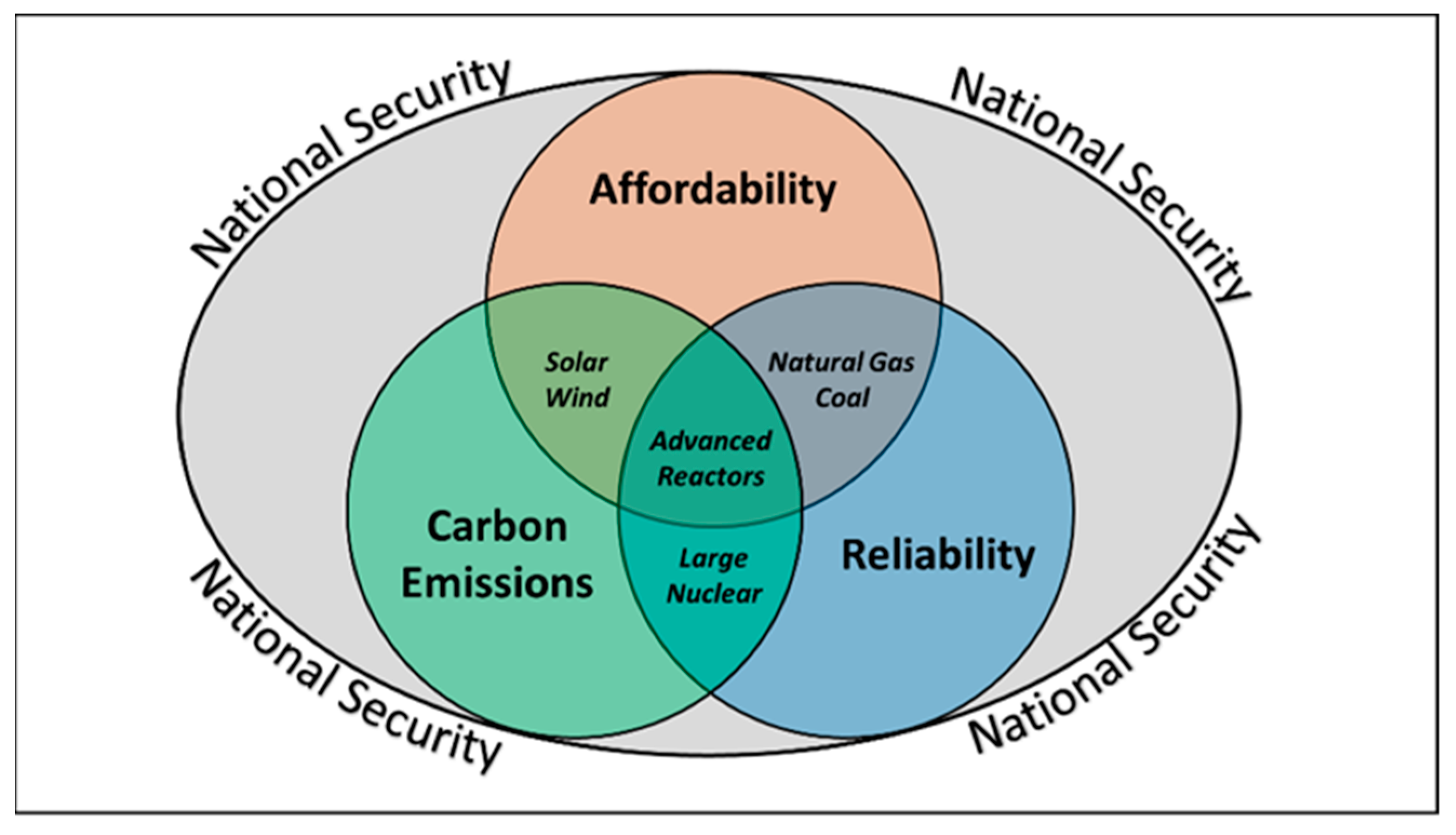

1. Introduction

2. Methods

3. Analysis

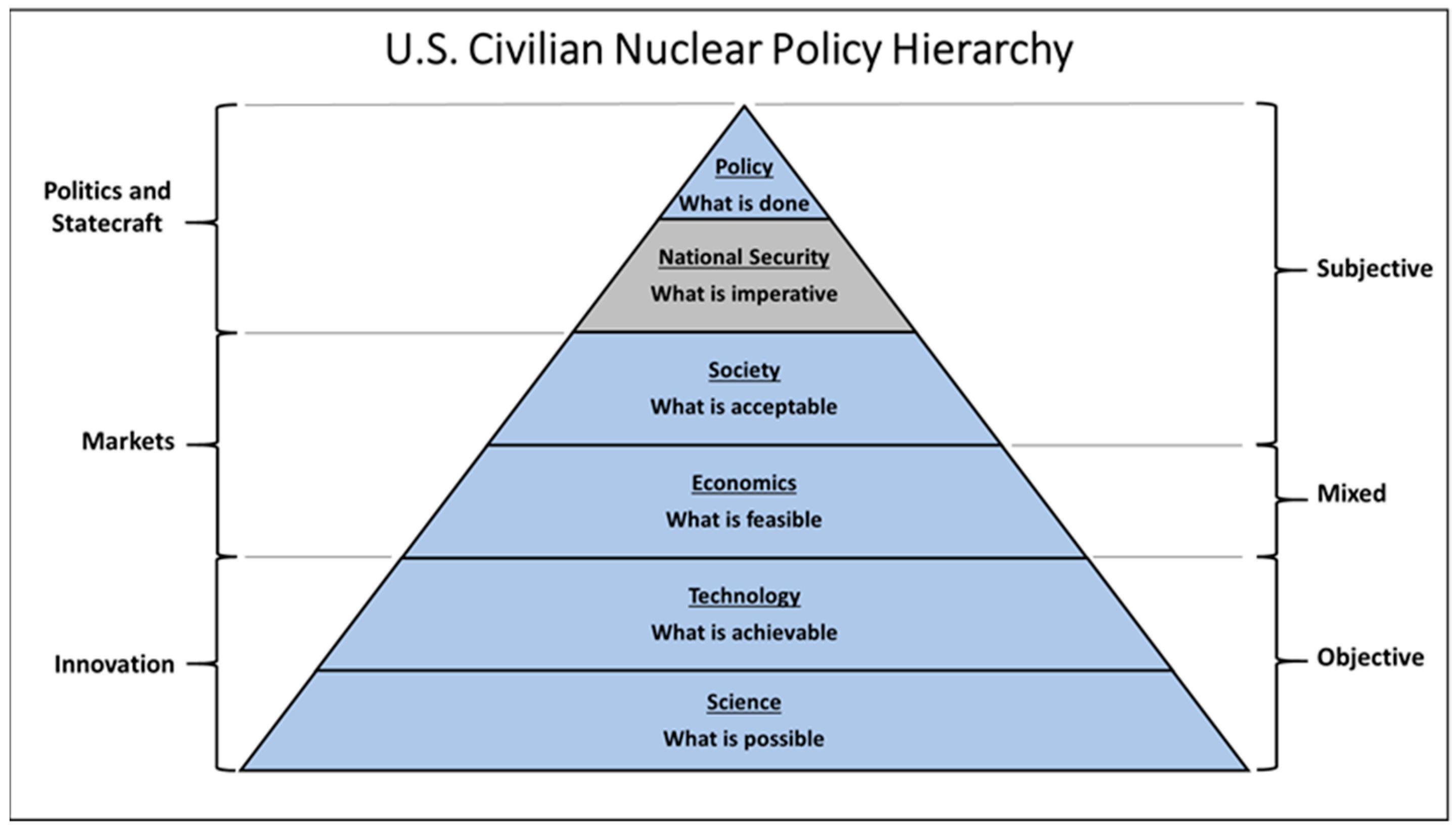

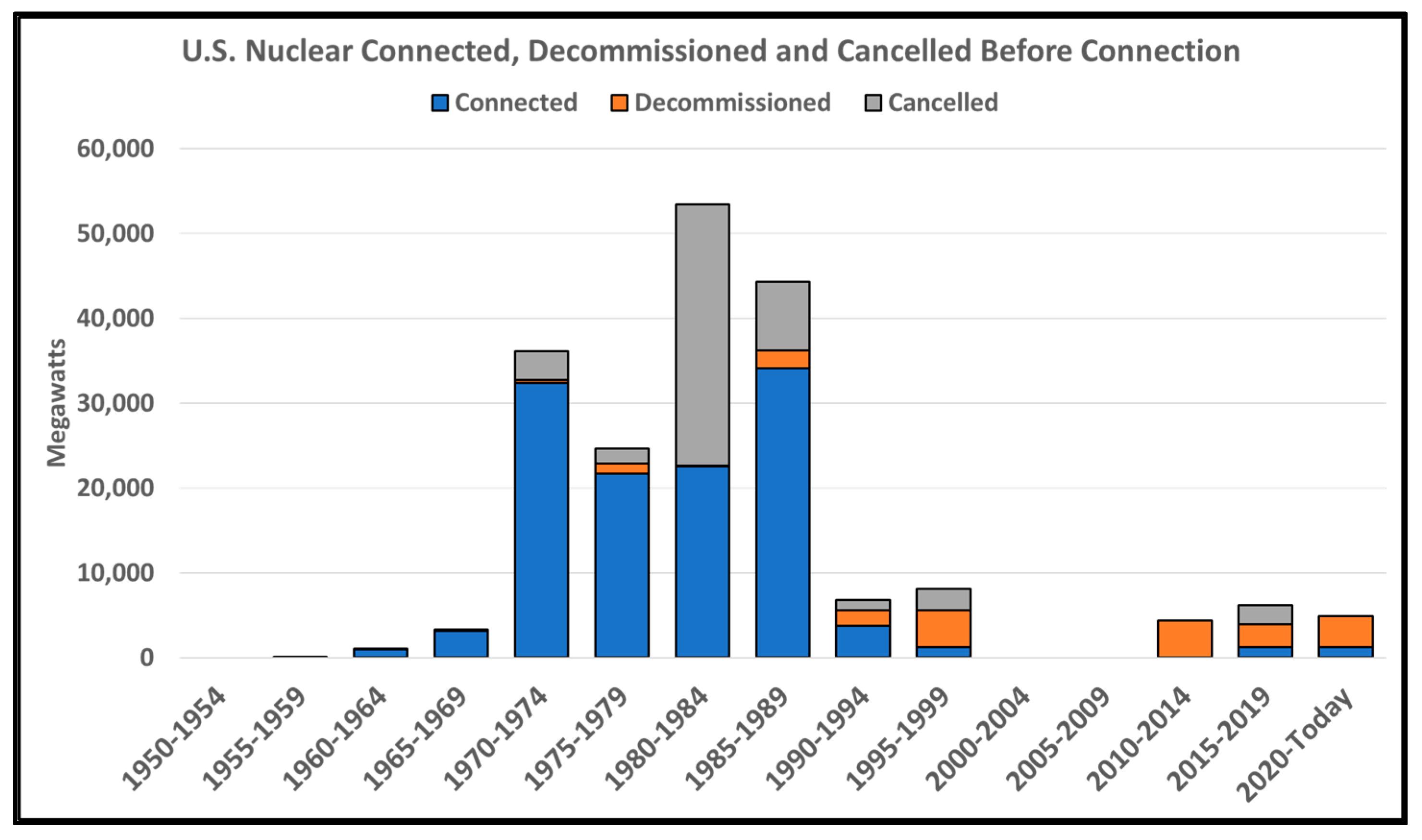

3.1. Innovation: U.S. Civilian Nuclear Power

The Science and Technology of Advanced Nuclear Reactors

- i.

- Additional inherent safety features;

- ii.

- Lower waste yields;

- iii.

- Improved fuel and material performance;

- iv.

- Increased tolerance to loss of fuel cooling;

- v.

- Enhanced reliability or improved resilience;

- vi.

- Increased proliferation resistance;

- vii.

- Increased thermal efficiency;

- viii.

- Reduced consumption of cooling water and other environmental impacts;

- ix.

- The ability to integrate into electric applications and nonelectric applications;

- x.

- Modular sizes to allow for deployment that corresponds with the demand for electricity or process heat; and

- xi.

- Operational flexibility to respond to changes in demand for electricity or process heat and to complement integration with intermittent renewable energy or energy storage [45].

3.2. Markets: Economics and Societal Disposition of U.S. Nuclear Power

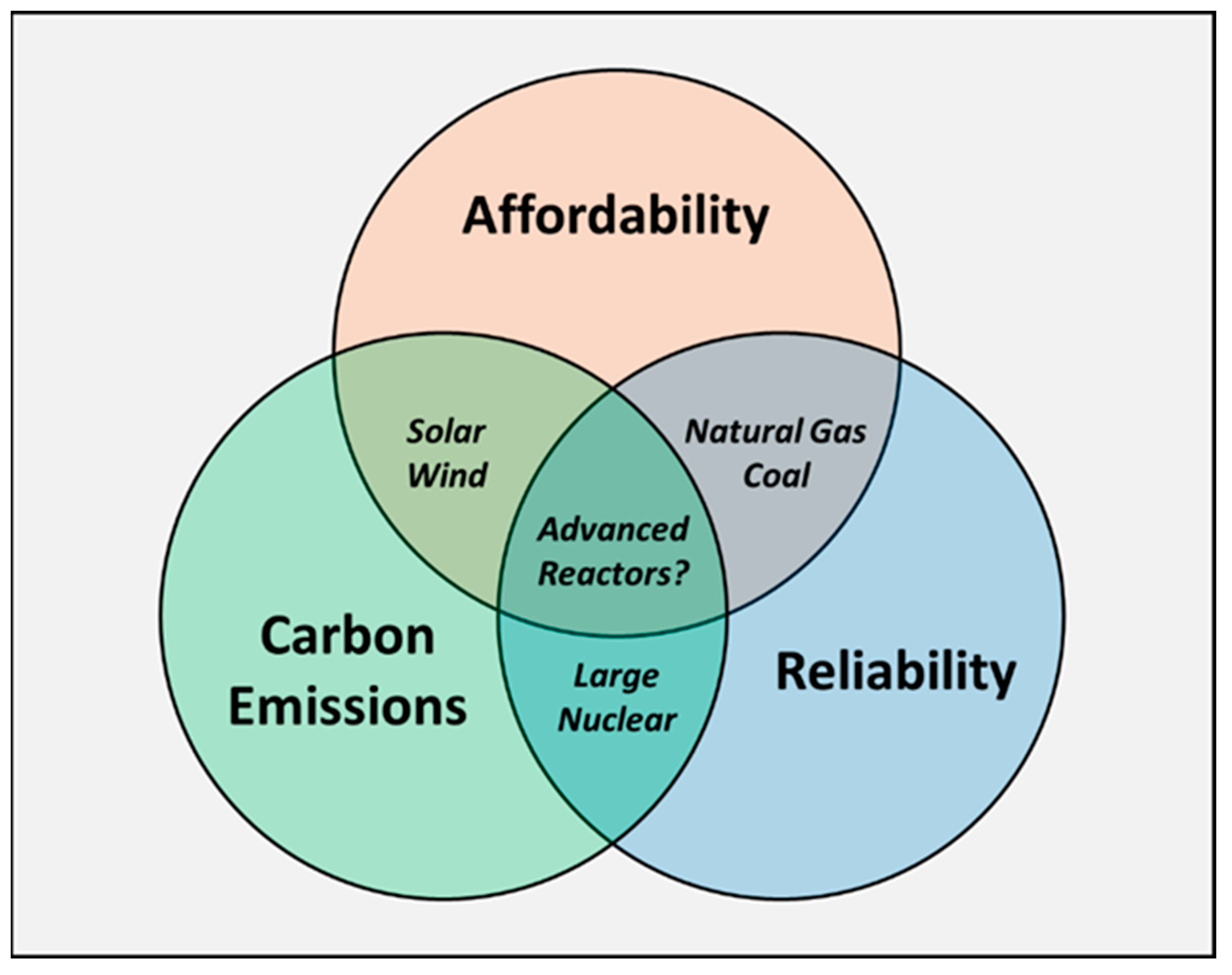

3.2.1. U.S. Nuclear Power Relative to Other Technologies

3.2.2. The Insufficiency of Levelized Cost of Electricity for Nuclear Power

3.2.3. Societal Disposition toward Advanced Nuclear Technology

3.3. Politics and Statecraft: The Gray Area of National Security in the U.S. Nuclear Policy

“In the interests of national security, U.S. programs for the development of the peaceful uses of atomic energy should be directed toward:

a. Maintaining U.S. leadership in the field, particularly in the development and application of atomic power;

b. Using such U.S. leadership to promote cohesion within the free world and to forestall successful Soviet exploitation of the peaceful uses of atomic energy to attract the allegiance of the uncommitted peoples of the world;

c. Increasing progress in developing and applying the peaceful uses of atomic energy in free nations abroad;

d. Assuring continued U.S. access to foreign uranium and thorium supplies;

e. Preventing the diversion to non-peaceful uses of any fissionable materials provided to other countries.

U.S. programs for the development of the peaceful uses of atomic energy should be carried forward as rapidly as the interests of the United States dictate, seeking private financing wherever possible”[104].

4. Discussion and Policy Recommendations

4.1. Domestic Challenges

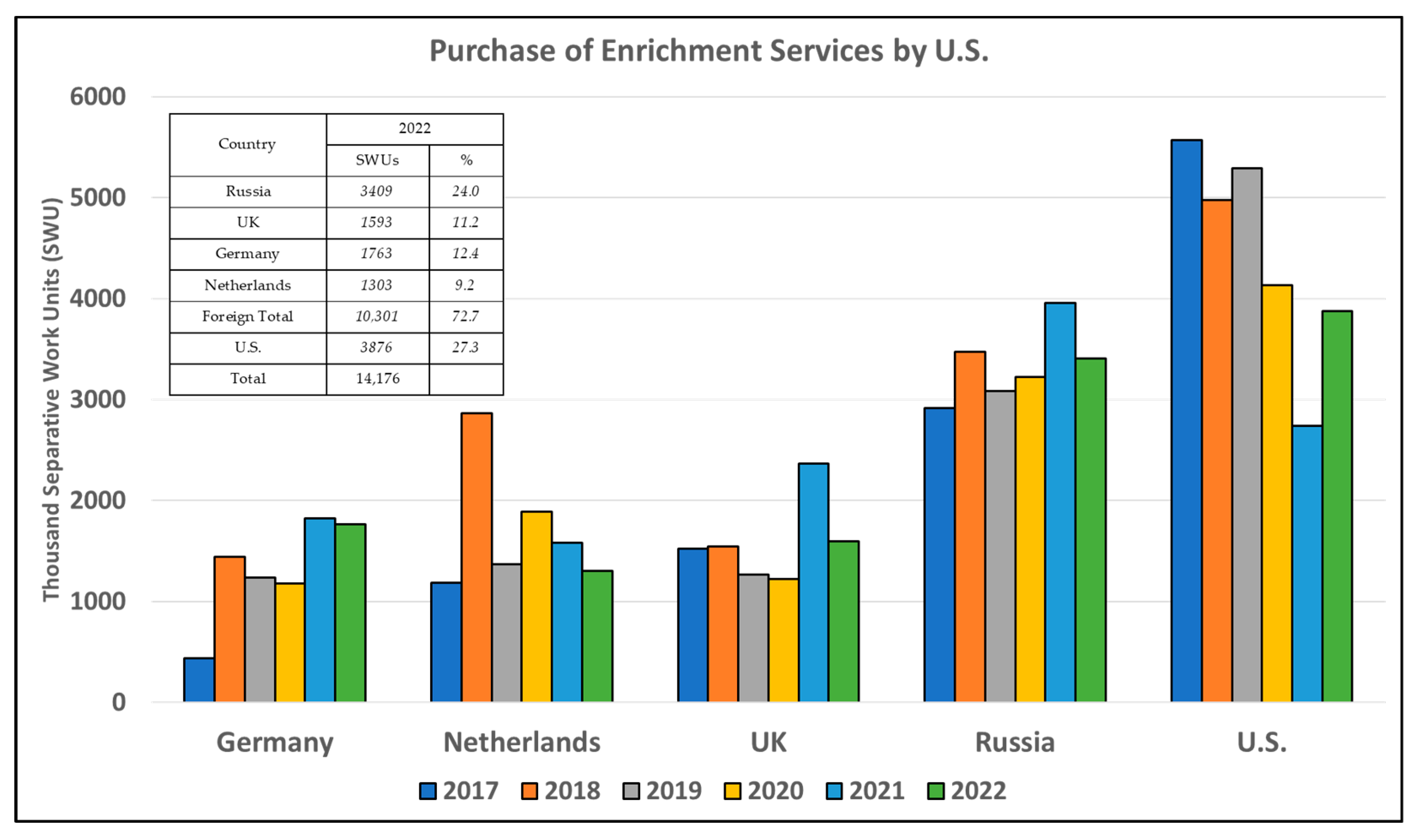

4.2. Global Challenges: U.S. Nuclear Disposition Relative to Other Countries

4.3. Operationalizing the National Security Value of U.S. Advanced Nuclear Power: A Focus on the Industrial Base

5. Conclusions

- The fledgling status of the U.S. advanced nuclear reactors and the U.S. nuclear industrial base and supply chain represent a structural deficiency that should be prioritized. The recommendation here is for the U.S. Congress to engage in ensuring that the capacity of that industrial base can be sustained even when market signals cannot sustain it. While the private utility sector alone may not create sufficient demand signals in these early stages of advanced nuclear reactor development, an option is to leverage the U.S. military bases and installations to create an early and consistent demand signal;

- Charge the U.S. Department of Defense with conducting a nuclear industrial base review to evaluate not only supply chains but also domestic manufacturing capacity and opportunities for mutual collaboration with allied global partners in order to increase economic and industrial efficiencies;

- Shift from a sell-side nuclear vendor model for global exports to a buy-side model brokered by a third-party integrator that can work with multiple U.S. nuclear partners, as identified in the proposed DoD nuclear industrial base review.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Tice, D. Fastest Path to Universal Energy? Let the Market Decide. World Economic Forum, 9 May 2014. Available online: https://www.weforum.org/agenda/2014/05/africa-forum-energy-access-social-entrepreneur/ (accessed on 18 May 2023).

- Bade, G. Electricity Markets: States Reassert Authority over Power Generation. Utility Dive, 15 October 2018. Available online: https://www.utilitydive.com/news/electricity-markets-states-reassert-authority-over-power-generation/539658/ (accessed on 18 May 2023).

- Hartman, D. No Administration, Conservative or Liberal, Should Pick Winners and Losers. National Review, 19 January 2018. Available online: https://www.nationalreview.com/2018/01/conservative-energy-policy-let-market-decide/ (accessed on 18 May 2023).

- United States Climate Alliance. Governors’ Climate Resilience Playbook. 2021. Available online: https://static1.squarespace.com/static/5a4cfbfe18b27d4da21c9361/t/6186adf2875b2e694bdd0434/1636216308401/USCA+2021+Governors%27+Climate+Resilience+Playbook.pdf (accessed on 18 May 2023).

- Gattie, D. U.S. Energy and Electric Power Policy: The National Security Imperative. In Proceedings of the North Dakota Association of Rural Electric Cooperatives Association Annual Meeting, Mandan, ND, USA, 18–20 January 2022. [Google Scholar]

- Wilson, M.M. Poised to Enact Sweeping Energy, Climate Plan. E&E News Energy Wire. 31 March 2022. Available online: https://www.eenews.net/articles/md-poised-to-enact-sweeping-energy-climate-plan/ (accessed on 18 May 2023).

- United States Department of State and the United States Office of the President, 2021. The Long-Term Strategy of the United States: Pathways to Net-Zero Greenhouse Gas Emissions. Washington DC, November 2021. Available online: https://www.whitehouse.gov/wp-content/uploads/2021/10/US-Long-Term-Strategy.pdf (accessed on 18 May 2023).

- Tollefson, J. IPCC’s starkest message yet: Extreme steps needed to avert climate disaster. Nature 2022, 604, 413–414. [Google Scholar] [CrossRef]

- White House Briefing Room. Executive Order on Tackling the Climate Crisis at Home and Abroad. 27 January 2021. Available online: https://www.whitehouse.gov/briefing-room/presidential-actions/2021/01/27/executive-order-on-tackling-the-climate-crisis-at-home-and-abroad/ (accessed on 18 May 2023).

- Solomon, B.D.; Krishna, K. The coming sustainable energy transition: History, strategies, and outlook. Energy Policy 2011, 39, 7422–7431. [Google Scholar] [CrossRef]

- Carley, S.; Konisky, D.M. The justice and equity implications of the clean energy transition. Nat. Energy 2020, 5, 569–577. [Google Scholar] [CrossRef]

- Jacobson, M.Z. 100% Clean, Renewable Energy and Storage for Everything; Cambridge University Press: Cambridge, MA, USA, 2020. [Google Scholar]

- Faturahman, A.; Oktavyra, R.D.; Aris; Widya, T.R.; Habibillah, T.R. Observation of The Use of Renewable Energy Charging Infrastructure in Electric Vehicles. In Proceedings of the 2022 International Conference on Science and Technology (ICOSTECH), Batam City, Indonesia, 3–4 February 2022; pp. 1–9. [Google Scholar] [CrossRef]

- Bruggers, J. New Faces on a Vital National Commission Could Help Speed a Clean Energy Transition. Inside Climate News. 15 February 2022. Available online: https://insideclimatenews.org/news/15022022/ferc-clean-energy-transition/ (accessed on 30 March 2023).

- Tyson, A.; Funk, C.; Kennedy, B. Americans Largely Favor U.S. Taking Steps to Become Carbon Neutral by 2050. Pew Research Center. 1 March 2022. Available online: https://www.pewresearch.org/science/2022/03/01/americans-largely-favor-u-s-taking-steps-to-become-carbon-neutral-by-2050/ (accessed on 21 April 2023).

- Kemp, J. Global Energy Transition Already Well Underway. Reuters, 11 September 2020. Available online: https://www.reuters.com/article/uk-global-energy-kemp-idUKKBN2621W9 (accessed on 21 April 2023).

- Richard, C. Energy Transition Underway as Global Emissions Flatline. Wind Power Monthly, 11 February 2020. Available online: https://www.windpowermonthly.com/article/1673646/energy-transition-underway-global-emissions-flatline (accessed on 21 April 2023).

- S & P Global. What Is Energy Transition? 24 February 2020. Available online: https://www.spglobal.com/en/research-insights/articles/what-is-energy-transition (accessed on 21 April 2023).

- Alvarez, G. More Proof the Clean Energy Transition Is Well Underway: An Oil and Gas Major Embraces Renewables. The Power Line, 4 June 2021. Available online: https://cleanpower.org/blog/more-proof-the-clean-energy-transition-is-well-underway-an-oil-and-gas-major-embraces-renewables/ (accessed on 21 April 2023).

- Nuclear Power in the USA. 2023. World Nuclear Association. Available online: https://www.world-nuclear.org/information-library/country-profiles/countries-t-z/usa-nuclear-power.aspx (accessed on 14 July 2023).

- Peakman, A.; Merk, B. The Role of Nuclear Power in Meeting Current and Future Industrial Process Heat Demands. Energies 2019, 12, 3664. [Google Scholar] [CrossRef]

- Saeed, R.M.; Worsham, E.K.; Choi, B.H.; Joseck, F.C.; Popli, N.; Toman, J.; Mikkelson, D.M. Industrial Requirements Status Report and Down-Select of Candidate Technologies (No. INL/RPT-23-73026-Rev000); Idaho National Laboratory (INL): Idaho Falls, ID, USA, 2023. [Google Scholar]

- International Atomic Energy Agency, 2017. Industrial Applications of Nuclear Energy, IAEA Nuclear Energy Series No. NP-T-4.3. Available online: https://www-pub.iaea.org/MTCD/Publications/PDF/P1772_web.pdf (accessed on 8 August 2023).

- Brown, N.R. Engineering demonstration reactors: A stepping stone on the path to deployment of advanced nuclear energy in the United States. Energy 2021, 238, 121750. [Google Scholar] [CrossRef]

- Bistline, J.; James, R.; Sowder, A. Technology, Policy, and Market Drivers of (and Barriers to) Advanced Nuclear Reactor Deployment in the United States after 2030. Nucl. Technol. 2019, 205, 1075–1094. [Google Scholar] [CrossRef]

- Diaz, M.N. U.S. Energy in the 21st Century: A Primer; Congressional Research Service: Washington, DC, USA, 2021.

- Energy Information Administration. 2023. Electricity Data Browser. Available online: https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=table_1_01 (accessed on 15 May 2023).

- Weinberg, A.M.; Lewis, H.W. The First Nuclear Era: The Life and Times of a Technological Fixer. Phys. Today 1995, 48, 63–64. [Google Scholar] [CrossRef]

- Perry, R.; Alexander, A.J.; Allen, W.; DeLeon, P.; Gándara, A.; Mooz, W.E.; Rolph, E.S.; Siegel, S.; Solomon, K.A. Development and Commercialization of the Light Water Reactor, 1946–1976 (Vol. 2180); Rand Corporation: Santa Monica, CA, USA, 1977; p. 8. [Google Scholar]

- Hargreaves, S. Obama Gives $8 Billion to New Nuke Plants. CNN Money, 16 February 2010. Available online: https://money.cnn.com/2010/02/16/news/economy/nuclear/ (accessed on 15 June 2023).

- United States Nuclear Regulatory Commission. Summer, Unit 3 Combine License No. NPF-94. Available online: https://www.nrc.gov/reactors/new-reactors/large-lwr/col/summer/col3.html (accessed on 12 June 2023).

- United States Nuclear Regulatory Commission. Issued Combined Licenses and Limited Work Authorizations for Vogtle, Units 3 and 4. Available online: https://www.nrc.gov/reactors/new-reactors/large-lwr/col/vogtle.html (accessed on 12 June 2023).

- Amy, J. Third Nuclear Reactor Reaches 100% Power Output at Georgia’s Plant Vogtle. AP News, 29 May 2023. Available online: https://apnews.com/article/nuclear-reactor-georgia-power-plant-vogtle-63535de92e55acc0f7390706a6599d75 (accessed on 31 May 2023).

- Stelloh, T. Construction Halted at South Carolina Nuclear Power Plant. NBC New, 31 July 2017. Available online: https://www.nbcnews.com/news/us-news/construction-halted-south-carolina-nuclear-power-reactors-n788331 (accessed on 15 June 2023).

- House, W. Obama Administration Announces Actions to Ensure That Nuclear Energy Remains a Vibrant Component of the United States. White House Briefing Room, 6 November 2015. Available online: https://obamawhitehouse.archives.gov/the-press-office/2015/11/06/fact-sheet-obama-administration-announces-actions-ensure-nuclear-energy (accessed on 15 June 2023).

- International Atomic Energy Agency. Power Reactor System. Harris-1. Available online: https://pris.iaea.org/PRIS/CountryStatistics/ReactorDetails.aspx?current=704 (accessed on 14 July 2023).

- International Atomic Energy Agency. Power Reactor System. Comanche Peak-2. Available online: https://pris.iaea.org/PRIS/CountryStatistics/ReactorDetails.aspx?current=730 (accessed on 14 July 2023).

- International Atomic Energy Agency. Power Reactor System. Watts Bar-1. Available online: https://pris.iaea.org/PRIS/CountryStatistics/ReactorDetails.aspx?current=699 (accessed on 14 July 2023).

- Reuters. U.S. Nuclear Reactors That Were Cancelled after Construction Began. 31 July 2017. Available online: https://www.reuters.com/article/toshiba-accounting-westinghouse-reactors/factbox-u-s-nuclear-reactors-that-were-canceled-after-construction-began-idINKBN1AG280 (accessed on 12 June 2023).

- International Atomic Energy Agency. United States of America. Available online: https://pris.iaea.org/pris/CountryStatistics/CountryDetails.aspx?current=US (accessed on 12 June 2023).

- Hultman, N.; Koomey, J. Three Mile Island: The driver of US nuclear power’s decline? Bull. At. Sci. 2013, 69, 63–70. [Google Scholar] [CrossRef]

- E Hultman, N.; Koomey, J.G. The risk of surprise in energy technology costs. Environ. Res. Lett. 2007, 2, 034002. [Google Scholar] [CrossRef]

- Komanoff, C. Ten Blows That Stopped Nuclear Power: Reflections on the US Nuclear Industry’s 25 Lean Years; Komanoff Energy Associates: New York, NY, USA, 2005. [Google Scholar]

- Komanoff, C. Power Plant Cost Escalation: Nuclear and Coal Capital Costs, Regulation, and Economics; Van Nostrand Reinhold: New York, NY, USA, 1981. [Google Scholar]

- U.S. House of Representatives. Office of the Law Revision Counsel, United States Code. 42 U.S.C.A § 16271—Title 42, Chapter 149, Subchapter IX, Section 16271, Nuclear Energy. Available online: https://uscode.house.gov/view.xhtml?req=granuleid:USC-prelim-title42-section16271&num=0&edition=prelim (accessed on 15 May 2023).

- International Atomic Energy Agency. Advanced Reactors Information System. Available online: https://aris.iaea.org/ (accessed on 8 August 2023).

- Holt, M. Advanced nuclear reactors: Technology overview and current issues. In Congressional Research Service Report for Congress; Report (No. R45706); CRS: Washington, DC, USA, 2023. [Google Scholar]

- Argonne National Laboratory. Argonne’s Nuclear Science and Technology Legacy—Historical News Releases. Nuclear Engineering Division, 20 December 2011. Available online: https://www.ne.anl.gov/About/hn/news111220.shtml (accessed on 14 June 2023).

- Brook, B.W.; van Erp, J.B.; Meneley, D.A.; Blees, T.A. The case for a near-term commercial demonstration of the Integral Fast Reactor. Sustain. Mater. Technol. 2015, 3, 2–6. [Google Scholar] [CrossRef]

- Till, C.E.; Chang, Y.I. Plentiful Energy: The Story of the Integral Fast Reactor: The Complex History of a Simple Reactor Technoloogy, with Emphasis on Its Scientific Basis for Non-Specialists; Illustrated Edition; Create Space Independent Publishing Platform: Scotts Valley, CA, USA, 2012. [Google Scholar]

- Till, C.E. Plentiful energy and the Integral Fast Reactor story. Int. J. Nucl. Governance, Econ. Ecol. 2006, 1, 212. [Google Scholar] [CrossRef]

- Ingersoll, D.; Houghton, Z.; Bromm, R.; Desportes, C. NuScale small modular reactor for Co-generation of electricity and water. Desalination 2014, 340, 84–93. [Google Scholar] [CrossRef]

- Federal Register, National Archives. NuScale Small Modular Reactor Design Certification, A Rule by the Nuclear Regulatory Commission, 19 January 2023. Available online: https://www.federalregister.gov/documents/2023/01/19/2023-00729/nuscale-small-modular-reactor-design-certification (accessed on 8 June 2023).

- Natrium. Carbon-free Power for the Clean Energy Transition. 2023. Available online: https://natriumpower.com/ (accessed on 8 June 2023).

- Wald, M. With Natrium, Nuclear Can Pair Perfectly with Energy Storage and Renewables. Nuclear Energy Institute, 3 November 2020. Available online: https://www.nei.org/news/2020/natrium-nuclear-pairs-renewables-energy-storage (accessed on 8 June 2023).

- General Electric. GE Hitachi and PRISM Selected for U.S. Department of Energy’s Versatile Test Reactor Program. 13 November 2018. Available online: https://www.ge.com/news/press-releases/ge-hitachi-and-prism-selected-us-department-energys-versatile-test-reactor-program (accessed on 8 June 2023).

- U.S. Department of Energy HALEU Consortium. Office of Nuclear Energy. 8 August 2023. Available online: https://www.energy.gov/ne/us-department-energy-haleu-consortium (accessed on 11 August 2023).

- Singer, S. NRC Authorizes First US High-Assay Low-Enriched Uranium Enrichment Plant Critical for Advanced Reactors. Utility Dive, 22 June 2023. Available online: https://www.utilitydive.com/news/nrc-HALEU-doe-advanced-nuclear-plants/653629/ (accessed on 11 August 2023).

- World Nuclear News. HALEU Fuel Availability Delays Natrium Reactor Project. 15 December 2022. Available online: https://world-nuclear-news.org/Articles/HALEU-fuel-availability-delays-Natrium-reactor-pro (accessed on 15 June 2023).

- Reuters. Dow and X-Energy to build U.S. Gulf Coast Nuclear Demonstration Plant. 1 March 2023. Available online: https://www.reuters.com/business/energy/dow-x-energy-build-us-gulf-coast-nuclear-demonstration-plant-2023-03-01/ (accessed on 8 June 2023).

- Patel, S. X-energy and Dow Will Deploy a 320-MWe e-100 Nuclear Facility at Gulf Coast Site. Power Magazine, 1 March 2023. Available online: https://www.powermag.com/x-energy-and-dow-will-deploy-a-320-mwe-xe-100-nuclear-facility-at-gulf-coast-site/ (accessed on 8 June 2023).

- U.S. Department of Energy. Advanced Reactor Demonstration Program. Office of Nuclear Energy. Available online: https://www.energy.gov/ne/advanced-reactor-demonstration-program (accessed on 15 June 2023).

- Reuters. US Urges Haste on Domestic HALEU Plan as Russia Faces Isolation. 22 March 2022. Available online: https://www.reutersevents.com/nuclear/us-urges-haste-domestic-haleu-plan-russia-faces-isolation (accessed on 8 June 2023).

- Patel, S. DOE Has Chosen Advanced Nuclear Reactor Demonstration Winners. Power Magazine, 8 October 2020. Available online: https://www.powermag.com/doe-has-chosen-advanced-nuclear-reactor-demonstration-winners/ (accessed on 15 June 2023).

- Smyth, H.D. Nuclear Power and Foreign Policy. Foreign Aff. 1956, 35, 20031201. [Google Scholar] [CrossRef]

- Atomic Energy Commission. Remarks Prepared by Lewis L. Strauss, Chairman, United States Atomic Energy Commission, for Delivery at the Founders’ Day Dinner. National Association of Science Writers. New York, New York. 16 September 1954. Available online: https://www.nrc.gov/docs/ML1613/ML16131A120.pdf (accessed on 18 May 2023).

- U.S. Energy Information Administration. Electricity Data Browser. 2023. Available online: https://www.eia.gov/electricity/data/browser/ (accessed on 15 May 2023).

- U.S. Energy Information Administration. Electric Power Monthly. Table 6.07A, Capacity Factors for Utility Scale Generators Primarily Using Fossil Fuels. April, 2023. Available online: https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=table_6_07_a (accessed on 18 May 2023).

- U.S. Energy Information Administration. Electric Power Monthly. Table 6.07B, Capacity Factors for Utility Scale Generators Primarily Using Non-Fossil Fuels. April, 2023. Available online: https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=table_6_07_b (accessed on 18 May 2023).

- Van den Bergh, K.; Delarue, E. Cycling of conventional power plants: Technical limits and actual costs. Energy Convers. Manag. 2015, 97, 70–77. [Google Scholar] [CrossRef]

- Impram, S.; Nese, S.V.; Oral, B. Challenges of renewable energy penetration on power system flexibility: A survey. Energy Strat. Rev. 2020, 31, 100539. [Google Scholar] [CrossRef]

- Stewart, W.R.; Shirvan, K. Construction schedule and cost risk for large and small light water reactors. Nucl. Eng. Des. 2023, 407, 112305. [Google Scholar] [CrossRef]

- Branker, K.; Pathak, M.J.M.; Pearce, J.M. A review of solar photovoltaic levelized cost of electricity. Renew. Sustain. Energy Rev. 2011, 15, 4470–4482. [Google Scholar] [CrossRef]

- Benes, K.J.; Augustin, C. Beyond LCOE: A simplified framework for assessing the full cost of electricity. Electr. J. 2016, 29, 48–54. [Google Scholar] [CrossRef]

- Matsuo, Y. Re-Defining System LCOE: Costs and Values of Power Sources. Energies 2022, 15, 6845. [Google Scholar] [CrossRef]

- Creti, A.; Fabra, N. Supply security and short-run capacity markets for electricity. Energy Econ. 2007, 29, 259–276. [Google Scholar] [CrossRef][Green Version]

- Cramton, P.; Ockenfels, A.; Stoft, S. Capacity market fundamentals. Econ. Energy Environ. Policy 2013, 2, 27–46. [Google Scholar] [CrossRef]

- Schäfer, S.; Altvater, L. A Capacity Market for the Transition towards Renewable-Based Electricity Generation with Enhanced Political Feasibility. Energies 2021, 14, 5889. [Google Scholar] [CrossRef]

- Zachary, S.; Wilson, A.; Dent, C. The Integration of Variable Generation and Storage into Electricity Capacity Markets. Energy J. 2022, 43. [Google Scholar] [CrossRef]

- Mays, J. Missing incentives for flexibility in wholesale electricity markets. Energy Policy 2020, 149, 112010. [Google Scholar] [CrossRef]

- Domínguez-Garabitos, M.A.; Ocaña-Guevara, V.S.; Santos-García, F.; Arango-Manrique, A.; Aybar-Mejía, M. A Methodological Proposal for Implementing Demand-Shifting Strategies in the Wholesale Electricity Market. Energies 2022, 15, 1307. [Google Scholar] [CrossRef]

- Felder, F.A.; Petitet, M. Extending the reliability framework for electric power systems to include resiliency and adaptability. Electr. J. 2022, 35, 107186. [Google Scholar] [CrossRef]

- Lazard. Lazard’s Levelized Cost of Energy Analysis—Version 16.0. Technical Report, Lazard. 2023. Available online: https://www.lazard.com/research-insights/2023-levelized-cost-of-energyplus/ (accessed on 11 August 2023).

- NREL (National Renewable Energy Laboratory). 2023 Annual Technology Baseline; National Renewable Energy Laboratory: Golden, CO, USA, 2023. Available online: https://atb.nrel.gov/ (accessed on 11 August 2023).

- Lovins, A.B. Energy Strategy: The Road Not Taken? Foreign Aff. 1976, 55, 65. [Google Scholar] [CrossRef]

- Sovacool, B.K.; Ramana, M.V. Back to the future: Small modular reactors, nuclear fantasies, and symbolic convergence. Sci. Technol. Hum. Values 2015, 40, 96–125. [Google Scholar] [CrossRef]

- Ramana, M.V. Small Modular and Advanced Nuclear Reactors: A Reality Check. IEEE Access 2021, 9, 42090–42099. [Google Scholar] [CrossRef]

- Friederich, S.; Boudry, M. Ethics of Nuclear Energy in Times of Climate Change: Escaping the Collective Action Problem. Philos. Technol. 2022, 35, 1–27. [Google Scholar] [CrossRef]

- Jacobson, M.Z.; Delucchi, M.A. Providing all global energy with wind, water, and solar power, Part I: Technologies, energy resources, quantities and areas of infrastructure, and materials. Energy Policy 2011, 39, 1154–1169. [Google Scholar] [CrossRef]

- Delucchi, M.A.; Jacobson, M.Z. Providing all global energy with wind, water, and solar power, Part II: Reliability, system and transmission costs, and policies. Energy Policy 2011, 39, 1170–1190. [Google Scholar] [CrossRef]

- Gür, T.M. Review of electrical energy storage technologies, materials and systems: Challenges and prospects for large-scale grid storage. Energy Environ. Sci. 2018, 11, 2696–2767. [Google Scholar] [CrossRef]

- Dowling, J.A.; Rinaldi, K.Z.; Ruggles, T.H.; Davis, S.J.; Yuan, M.; Tong, F.; Lewis, N.S.; Caldeira, K. Role of Long-Duration Energy Storage in Variable Renewable Electricity Systems. Joule 2020, 4, 1907–1928. [Google Scholar] [CrossRef]

- Rogner, H.-H.; Budnitz, R.J.; McCombie, C.; Mansouri, N.; Schock, R.N.; Shihab-Eldin, A. Keeping the Nuclear Energy Option Open; USAEE Working Paper No. 21-488; USAEE: Dayton, OH, USA, 2021. [Google Scholar]

- Brenan, M. Americans’ Support for Nuclear Energy Highest in a Decade. Gallup, 25 April 2023. Available online: https://news.gallup.com/poll/474650/americans-support-nuclear-energy-highest-decade.aspx (accessed on 8 June 2023).

- Leppert, R. Americans Continue to Express Mixed Views about Nuclear Power. Pew Research Center, 23 March 2022. Available online: https://www.pewresearch.org/short-reads/2022/03/23/americans-continue-to-express-mixed-views-about-nuclear-power/ (accessed on 8 June 2023).

- Baron, J.; Herzog, S. Public opinion on nuclear energy and nuclear weapons: The attitudinal nexus in the United States. Energy Res. Soc. Sci. 2020, 68, 101567. [Google Scholar] [CrossRef]

- Bisconti, A.S. Changing public attitudes toward nuclear energy. Prog. Nucl. Energy 2018, 102, 103–113. [Google Scholar] [CrossRef]

- Soni, A. Out of sight, out of mind? Investigating the longitudinal impact of the Fukushima nuclear accident on public opinion in the United States. Energy Policy 2018, 122, 169–175. [Google Scholar] [CrossRef]

- Bisconti, A.S. 2023 National Nuclear Energy Public Opinion Survey: Public Support for Nuclear Energy Stays at Record Level for Third Year in a Row. Bisconti Research, Inc. 2023. Available online: https://www.bisconti.com/blog/public-opinion-2023 (accessed on 8 June 2023).

- Gupta, K.; Nowlin, M.C.; Ripberger, J.T.; Jenkins-Smith, H.C.; Silva, C.L. Tracking the nuclear ‘mood’ in the United States: Introducing a long term measure of public opinion about nuclear energy using aggregate survey data. Energy Policy 2019, 133, 110888. [Google Scholar] [CrossRef]

- Hewlett, R.G.; Anderson Jr, O.E.; Snell, A.H. The New World, 1939/1946: Volume 1 of a History of the United States Atomic Energy Commission. Phys. Today 1962, 15, 62–63. [Google Scholar] [CrossRef]

- Barnard, C.I. A Report on the International Control of Atomic Energy; U.S. Department of State: Washington, DC, USA, 1946.

- Gattie, D.K.; Massey, J.N. Twenty-First-Century US Nuclear Power. Strateg. Stud. Q. 2020, 14, 121–142. [Google Scholar]

- Foreign Relations of the United States (FRUS), 1955–1957, Regulation of Armaments; Atomic Energy, Vol. XX, Ed. David S. Patterson (Washington, DC: Government Printing Office, 1990), Doc. 14, National Security Council Report, NSC 5507/2, 12 March 1955, Encl., Statement of Policy on Peaceful Uses of Atomic Energy, General Considerations. Available online: https://history.state.gov/ (accessed on 26 April 2023).

- Congress.gov. Text-H.R.9757-83rd Congress (1953–1954): An Act to Amend the Atomic Energy Act of 1946, as Amended, and for Other Purposes. 30 August 1954. Available online: https://www.congress.gov/bill/83rd-congress/house-bill/9757/text (accessed on 5 June 2023).

- U.S. Department of State. 123 Agreements Fact Sheet. Bureau of International Security and Nonproliferation. 2022. Available online: https://www.state.gov/fact-sheets-bureau-of-international-security-and-nonproliferation/123-agreements/ (accessed on 18 May 2023).

- The American Presidency Project. 1956 Democratic Party Platform. 13 August 1956. Available online: https://www.presidency.ucsb.edu/documents/1956-democratic-party-platform (accessed on 18 May 2023).

- The American Presidency Project. Republican Party Platform of 1956. 20 August 1956. Available online: https://www.presidency.ucsb.edu/documents/republican-party-platform-1956 (accessed on 18 May 2023).

- Executive Office of the President. Tackling the Climate Crisis at Home and Abroad. Presidential Document E.O. 14008 of 27 January 2021. Available online: https://www.federalregister.gov/documents/2021/02/01/2021-02177/tackling-the-climate-crisis-at-home-and-abroad (accessed on 12 May 2023).

- U.S. Department of Energy. Biden-Harris Administration Announces Major Investment to Preserve America’s Clean Nuclear Energy Infrastructure. 21 November 2022. Available online: https://www.energy.gov/articles/biden-harris-administration-announces-major-investment-preserve-americas-clean-nuclear (accessed on 12 May 2023).

- Shirvan, K.; Hardwick, J.C. Overnight Capital Cost of the next AP1000. Center for Advanced Nuclear Energy Systems (CANES), MIT-ANP-TR-193. Massachusetts Institute of Technology, Cambridge, MA, USA. Available online: https://web.mit.edu/kshirvan/www/research/ANP193%20TR%20CANES.pdf (accessed on 18 May 2023).

- Stewart, W.; Shirvan, K. Capital cost estimation for advanced nuclear power plants. Renew. Sustain. Energy Rev. 2021, 155, 111880. [Google Scholar] [CrossRef]

- Campbell, R.J. The Federal Power Act (FPA) and Electricity Markets; Congressional Research Service: Washington, DC, USA, 2017.

- Holt, M. US Nuclear Plant Shutdowns, State Interventions, and Policy Concerns; Congressional Research Service: Washington, DC, USA, 2022.

- Brown, P.; Holt, M. Financial Challenges of Operating Nuclear Power Plants in the United States; CRS Report R-44715, 14; Congressional Research Service: Washington, DC, USA, 2016.

- Gattie, D.K. U.S. energy, climate and nuclear power policy in the 21st century: The primacy of national security. Electr. J. 2019, 33, 106690. [Google Scholar] [CrossRef]

- Gattie, D.K.; Darnell, J.L.; Massey, J.N. The role of U.S. nuclear power in the 21st century. Electr. J. 2018, 31, 1–5. [Google Scholar] [CrossRef]

- Ichord, R.F., Jr. US Nuclear-Power Leadership and the Chinese and Russian Challenge; Atlantic Council: Washington, DC, USA, 2018. [Google Scholar]

- International Atomic Energy Agency. Power Reactor Information System. Available online: https://pris.iaea.org/PRIS/home.aspx (accessed on 8 May 2023).

- World Nuclear Association. US Nuclear Power Policy. February 2023. Available online: https://world-nuclear.org/information-library/country-profiles/countries-t-z/usa-nuclear-power-policy.aspx (accessed on 18 July 2023).

- Lin, B.; Bae, N.; Bega, F. China’s Belt & Road Initiative nuclear export: Implications for energy cooperation. Energy Policy 2020, 142, 111519. [Google Scholar]

- Pan, Y. Managing the atomic divorce: The challenges of East Central Europe’s nuclear energy decoupling from Russia. Electr. J. 2023, 36, 107241. [Google Scholar] [CrossRef]

- Markard, J.; Bento, N.; Kittner, N.; Nuñez-Jimenez, A. Destined for decline? Examining nuclear energy from a technological innovation systems perspective. Energy Res. Soc. Sci. 2020, 67, 101512. [Google Scholar] [CrossRef]

- U.S. Nuclear Regulatory Commission. Mixed Oxide Fuel Fabrication Facility Licensing. Available online: https://www.nrc.gov/materials/fuel-cycle-fac/mox/licensing.html (accessed on 18 July 2023).

- World Nuclear News. 2018. US MOX Facility Contract Terminated. World Nuclear News, 23 October 2018. Available online: https://world-nuclear-news.org/Articles/US-MOX-facility-contract-terminated (accessed on 18 May 2023).

- U.S. Energy Information Administration. 2023; 2022 Uranium Marketing Annual Report, Table 16. Available online: https://www.eia.gov/uranium/marketing/table16.php (accessed on 8 May 2023).

- Scholvina, S.; Wigellb, M. Power politics by economic means: Geoeconomics as an analytical approach and foreign policy practice. Comp. Strategy 2018, 37, 73–84. [Google Scholar] [CrossRef]

- Carlsson, M.; Oxenstierna, S.; Weissmann, M. China and Russia: A Study on Cooperation, Competition and Distrust; Försvarsanalys, Totalförsvarets Forskningsinstitut (FOI): Stockholm, Sweden, 2015. [Google Scholar]

- Burzynska-Hernandez, O. Action in the Arctic: Lack of US leadership expands opportunities for Russia and China. In Climate Security Risk Briefers; The Center for Climate & Security: Washington, DC, USA, 2021; pp. 42–46. [Google Scholar]

- Cordesman, A.H.; Hwang, G. US Competition with China and Russia: The Crisis-Driven Need to Change US Strategy; Center for Strategic and International Studies (CSIS): Washington, DC, USA, 2020. [Google Scholar]

- Nakano, J. The Changing Geopolitics of Nuclear Energy. A Look at the United States, Russia, and China; Center for Strategic & International Studies: Washington, DC, USA, 2020. Available online: http://csis-website-prod.s3.amazonaws.com/s3fs-public/publication/200416_Nakano_NuclearEnergy_UPDATED%20FINAL.pdf (accessed on 8 May 2023).

- Szulecki, K.; Overland, I. Russian nuclear energy diplomacy and its implications for energy security in the context of the war in Ukraine. Nat. Energy 2023, 8, 413–421. [Google Scholar] [CrossRef]

- Giorgi, A. Russia’s Civil Nuclear Energy Exports: Regional Profiles, Strengths and Weaknesses, and a US Framework to Respond. Doctoral Dissertation, Johns Hopkins University, Baltimore, MD, USA, 2022. [Google Scholar]

- De Blasio, N.; Nephew, R. The Geopolitics of Nuclear Power and Technology; Columbia University in the City of New York: New York, NY, USA, 2017. [Google Scholar]

- Sivaram, V.; Saha, S. The Geopolitical Implications of a Clean Energy Future from the Perspective of the United States; Springer: Cham, Switzerland, 2018; pp. 125–162. [Google Scholar] [CrossRef]

- Andres, R.B.; Breetz, H.L. Small Nuclear Reactors for Military Installations: Capabilities, Costs, and Technological Implications; Institute for National Strategic Studies, National Defense University: Washington, DC, USA, 2011. [Google Scholar]

- King, M.; Huntzinger, L.; Nguyen, T.; Center for Naval Analyses Alexandria Va Resource Analysis Division. Feasibility of Nuclear Power on US Military Installations, 2nd ed.; CNA: Arlington, VA, USA, 2011. [Google Scholar]

- Lee, S.W.; Lee, Y.; Kim, N.; Jo, H. Design of heat pipe cooled microreactor based on cycle analysis and evaluation of applicability for remote regions. Energy Convers. Manag. 2023, 288, 117126. [Google Scholar] [CrossRef]

- Force, I.T. Assessing and Strengthening the Manufacturing and Defense Industrial Base and Supply Chain Resiliency of the United States; US Department of Defense: Washington, DC, USA, 2018.

- Shropshire, D.; Black, G.; Araujo, K. Global Market Analysis of Microreactors; Technical Report; US Department of Energy: Washington, DC, USA, 2021. [CrossRef]

- Finan, A.; Foss, A.; Goff, M.; King, C.; Lohse, C. Nuclear Energy: Supply Chain Deep Dive Assessment; US Department of Energy: Washington, DC, USA, 2022. [CrossRef]

- Peters, H.M.; Nicastro, L. Defense Primer: The National Technology and Industrial Base; IF11311; Congressional Research Service: Washington, DC, USA, 2023. Available online: https://crsreports.congress.gov/product/pdf/IF/IF11311/11 (accessed on 18 May 2023).

- Kozeracki, J.; Vlahoplus, C.; Scott, K.; Bates, M.; Valderrama, B.; Bickford, E.; Stuhldreher, T.; Foss, A.; Fanning, T.; Crane, D.; et al. Pathways to Commercial Liftoff: Advanced Nuclear; US Department of Energy: Washington, DC, USA, 2023.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Design Characteristics of Advanced Nuclear Reactors | ||

|---|---|---|

| Fuel Material |

| |

| Coolant |

|

|

| Moderator |

|

|

| Fuel Form |

|

|

| Reactor Type |

| |

| Fuel Cycle |

| |

| Reactor Size |

| |

| Neutron Spectrum |

| |

| Energy Resource, Technology | Energy Resource Properties & Power Plant Operation Characteristics | |

|---|---|---|

| Coal |

|

|

| Natural Gas Combined Cycle |

|

|

| Natural Gas Turbine |

|

|

| Nuclear |

|

|

| Utility-Scale Solar and Onshore Wind |

|

|

| Technology | Unsubsidized LCOE ($/MWhr) |

|---|---|

| Solar PV--Residential Rooftop | 117–282 |

| Solar PV--Commercial & Industrial | 49–185 |

| Solar PV--Utility-Scale | 24–96 |

| Geothermal | 61–102 |

| Wind (Onshore) | 24–75 |

| Wind (Offshore) | 72–140 |

| Gas Peaking | 115–221 |

| Nuclear | 141–221 |

| Coal | 68–166 |

| Natural Gas Combined Cycle | 39–101 |

| Number of Reactors Since 2000 | ||

|---|---|---|

| Country | Connected to Grid | Under Construction |

| China | 52 | 21 |

| Russia | 13 | 3 |

| India | 12 | 8 |

| South Korea | 11 | 3 |

| Japan | 5 | 2 |

| Pakistan | 6 | 0 |

| Czech Republic | 2 | 0 |

| Ukraine | 2 | 2 |

| Argentina | 1 | 1 |

| Belarus | 2 | 0 |

| Brazil | 1 | 1 |

| Iran | 1 | 1 |

| UAE | 3 | 1 |

| US | 2 | 1 |

| Romania | 1 | 0 |

| Bangladesh | 0 | 2 |

| Finland | 1 | 0 |

| France | 0 | 1 |

| Slovakia | 1 | 1 |

| Taiwan | 0 | 0 |

| Turkey | 0 | 4 |

| UK | 0 | 2 |

| Total | 116 | 54 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gattie, D.; Hewitt, M. National Security as a Value-Added Proposition for Advanced Nuclear Reactors: A U.S. Focus. Energies 2023, 16, 6162. https://doi.org/10.3390/en16176162

Gattie D, Hewitt M. National Security as a Value-Added Proposition for Advanced Nuclear Reactors: A U.S. Focus. Energies. 2023; 16(17):6162. https://doi.org/10.3390/en16176162

Chicago/Turabian StyleGattie, David, and Michael Hewitt. 2023. "National Security as a Value-Added Proposition for Advanced Nuclear Reactors: A U.S. Focus" Energies 16, no. 17: 6162. https://doi.org/10.3390/en16176162

APA StyleGattie, D., & Hewitt, M. (2023). National Security as a Value-Added Proposition for Advanced Nuclear Reactors: A U.S. Focus. Energies, 16(17), 6162. https://doi.org/10.3390/en16176162