1. Introduction

Developing a sustainable, competitive, safe and low-emission energy system is one of the goals of the climate and energy policy carried out by the European Union (EU). A systemic approach to this issue allows singling out a few detailed goals whose gradual achievement by the EU and its member states will enable reaching climate neutrality by 2050 and a transformation of energy sectors of individual member states into low-emission ones. This entails: (1) reducing greenhouse gas emissions; (2) creating an internal EU energy market; (3) increasing the share of RES energy in gross final energy consumption; and (4) increasing energy efficiency [

1]. There is no doubt that the sole diversification of sources of energy from fossil fuels and supporting the development of renewable energy sources is not the only way to counteract the global energy market disruption caused by COVID-19 and Russia–Ukraine conflict. Minimizing energy supply interruptions is also possible through behavioural changes (motivated by financial or legal measures) in energy consumers. New energy infrastructure and system may also be built to save energy. Reducing energy consumption is the cheapest and safest way to reduce reliance on fossil fuels and to improve energy security, competitiveness and stability of the EU itself and its member states. It needs to be noted that ensuring energy efficiency together with renewable energy are today a foundation of a sustainable energy policy [

2]. There is no doubt that solely seeking energy sources will not allow achievement of energy security if the very process of using this energy is not optimised. Cost-saving actions may be one of the key factors to reduce the import of energy to neighbouring states, and mainly to slow down the process of exhaustion of national energy sources, which also allows the achievement of energy independence.

Directive 2012/27/EU of the European Parliament and of the Council of 25 October 2012 on energy efficiency amending directives 2009/125/EC and 2010/30/EU and repealing Directives 2004/8/EC and 2006/32/EC [

3] amended by directive (EU) 2018/2002 of the European Parliament and of the Council of 11 December 2018 [

4] (the short form “Directive 2018/2002/EU” will be used for clarity of the discussion, which means the current content of Directive 2012/27/EU and is now the relevant law) assumed achievement of energy savings of at least 32.5% in the EU by 2030 based on projections made in 2007, which showed a primary energy consumption in 2030 of 1887 Mtoe and a final energy consumption of 1416 Mtoe. Intensification of institutional actions by the EU in terms of ensuring an adequate level of energy efficiency proves the crucial role of pro-saving activities and activities that rationalize energy consumption to achieve a climate neutral economy by 2050. The amended directive on energy efficiency extends the obligation to save energy for the period from 1 January 2021 to 31 December 2030 and further years. In each year of the period covered with the obligation (2021–2030), member states are required to achieve cumulative end-use energy savings, equivalent to new savings of at least 0.8% of final energy consumption in this period and in further years. As a result, the EU projected that in 2020 primary energy consumption will not be greater than 1.483 million tonnes of oil equivalent (Mtoe), and that final energy consumption will not be greater than 1.086 Mtoe. Relations between existing primary and final energy consumption with regard to the limits given are presented in

Figure 1. Therefore, there is no surprise that a binding goal for 2030 is at least a 32.5% reduction in relation to the reference scenario drawn up by the European Commission [

5]. This means that in 2030, primary energy consumption will not be greater than 1.273 Mtoe, and final energy consumption will be no more than 956 Mtoe (based on projections made in 2007). Achievement of these values is highly probable given the existing data for 2012–2021 presented in

Figure 1.

Establishing results that are binding on each member state in terms of energy efficiency achieved was associated with member states being able to apply measures typical to the field of policy conducted to apply energy-effective technology or techniques that results in a reduction in final energy consumption. They also include binding measures that impose an obligation to apply specific technologies or techniques or agreements under which participants in economic transactions or local government units will commit to implement actions that facilitate efficiency. Setting up such a system which obliges entities to ensure energy efficiency must be a result of joining an unambiguous and cohesive national legislation along with implementing acts, which will translate into indisputable regulations of rights and obligations of individual participants of the energy market and then into a comprehensive internal policy. The certainty about the legal status and adjusting to the current economic and social realities means that institutions and instruments that result from legal regulations will constitute an essential factor for a correct functioning of the system that commits to energy efficiency according to the EU’s policy and law-making. The directive referred to above created a possibility for member states to achieve their particular goals for energy savings by implementing alternative measures (Article 7b of Directive 2018/2002/EU). If member states decide to do so, they should ensure, without prejudice to the provisions of Article 7(4) and (5) of Directive 2018/2002/EU, that savings required under Article 7(1) Directive 2018/2002/EU are achieved by final consumers.

One such measure for member states is to encourage the conclusion of energy performance contracts, which allows operation of specialist entities called energy service companies (ESCOs). ESCOs’ fundamental objective is to provide measures to improve energy efficiency, which may reduce the amount of energy required for production and service provision. Implementation of energy services offered by ESCOs is possible thanks to the contract referred to above. The objective of this contract is to perform energy services on market terms that aim to implement energy efficiency measures. ESCOs provide energy efficiency services that may involve, in particular, improvement of energy characteristics of a building or renovation of a heating system or an exchange of potentially ineffective devices. To generalize, it may be concluded that the model of ESCOs’ operation indeed means that energy or financial savings that result from measures and ESCOs remuneration are to be interrelated with the efficiency of measures implemented. The contract discussed here is one of the key means that will influence the success of EU policy in this aspect next to building smart energy grids to boost efficiency of energy transfer and to improve the position of an electricity consumer and to encourage him to be active on the market. Thus, energy efficiency will grow due to a conscious use of energy by numerous groups of consumers. There is no doubt that improvement of energy efficiency requires activity in many different dimensions, especially in the horizontal aspect, which will affect both the economy and society through energy efficiency and also its more rational use. The activities to boost energy efficiency of buildings, products, devices, installations and processes allow a reduction in costs of energy use and prove that single, individual and bottom-up initiatives are the most crucial for energy efficiency.

Such a framework at the EU level must be contrasted with the internal policy of one member state, Poland.

The basic aim of Poland’s energy policy is energy security whilst ensuring competitiveness of the economy, energy efficiency and reduction in the energy sector’s impact on the environment. Energy security in the Polish approach means a state of the economy in which consumers’ current and future demand for fuels and energy is covered soundly, both in technical and economic terms, while maintaining requirements of environmental protection. Basic values, criteria and guidelines for the Polish energy policy, put in place largely by energy law regulations, directly fit in the expectations of the European sustainable development [

6]. However, the Polish market looks different when it comes to the development of the ESCO markets against EU member states. Based on data for 2017–2019, the Polish ESCO market was recognized in 2020 as modest, though developing (next to Bulgaria, Ireland and Lithuania) [

7]. One of the reasons of this state of affairs was the insufficient use of technical advisors and lack of guaranteed funds [

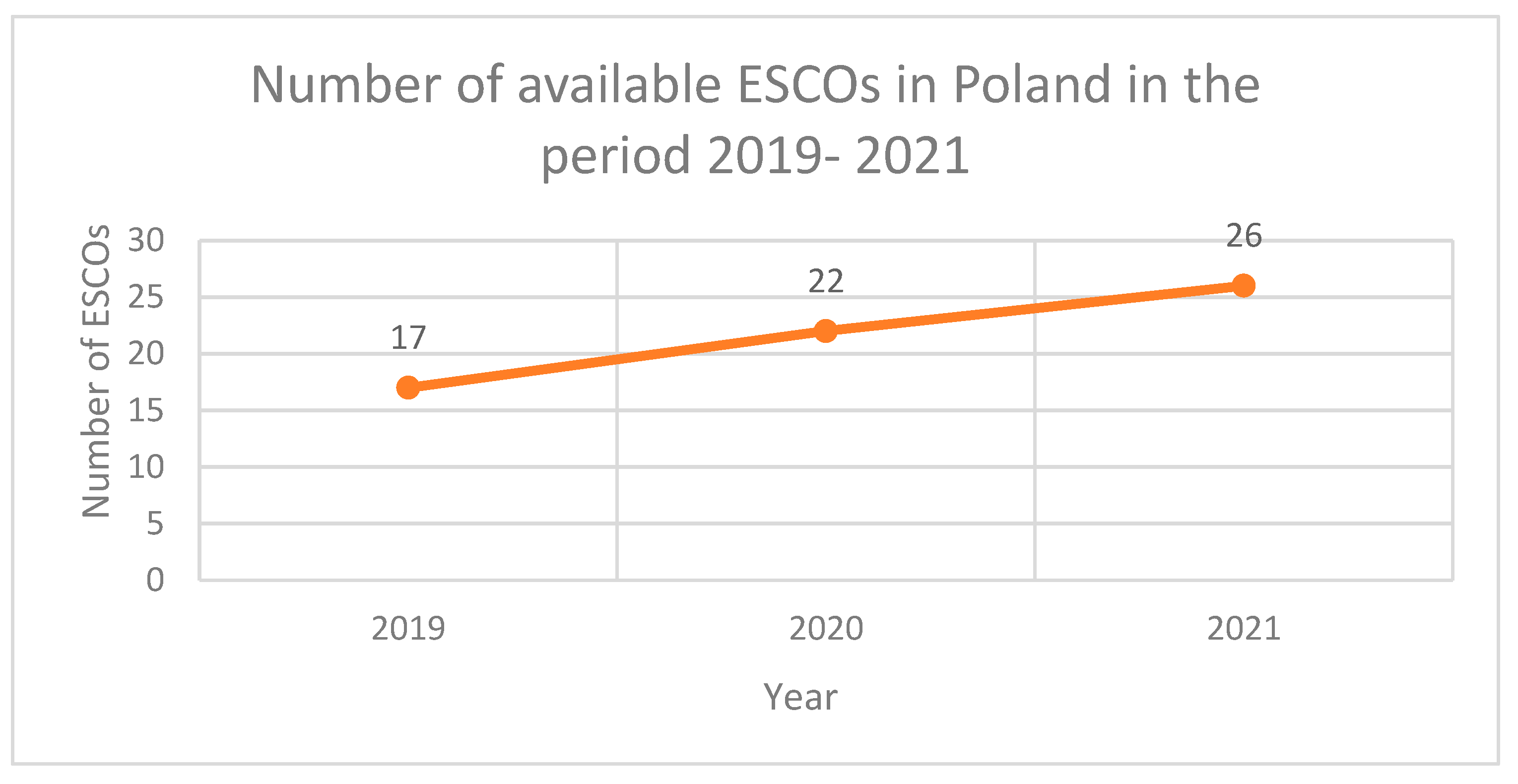

7]. On the other hand, prognosis for 2020–2023 may appear to be more optimistic than in the previous period. Poland, next to Finland and Spain, may accelerate market growth trends. This prediction is reflected in

Figure 2, which presents an increase in the number of ESCOs at the end of each year in Poland.

One of the main recommendations from the EU for Poland was to clarify the impact of EPCs on public debt, especially that appropriate solutions started to appear at the EU level. We must note that Europe’s Statistical Office (Eurostat) allowed, as early as in 2017, an off-balance sheet recording, which made it more attractive for the public sector to use contracts signed with ESCOs. According to Eurostat’s 2017 guidance on off-government balance sheet recording for EPCs, such recording could apply to these contracts if the contractor is considered as the economic owner [

8].

The act of 20 April 2021 on amending the Energy Efficiency Act and certain other acts (Dz. U. (Journal of Laws) 2021 item 868) [

9], which when it comes to EPC-related changes entered into force only on 1 January 2022, implements Directive 2018/2002/EU. The amendments introduced in the Energy Efficiency Act mainly intended not only to adjust the existing regulations on energy efficiency into the EU law, but also to overcome current limitations and challenges. So far, the Polish legislation has been developing the energy efficiency certificates system and avoided facilitation of application of other alternative tools that allowed progress in energy use efficiency. This is best seen in the example of the EPC. It has inspired legal doubts under provisions of the Energy Efficiency Act (EEA) of 20 May 2016 which has been in force since 2021 and of the Public–Private Partnership Act (PPPA) of 19 December 2008, which encourage public institutions to apply EPCs. This was associated with imposing additional obligations on public institutions, such as the following: (1) conducting efficiency assessment (Article 3a PPPA); (2) bringing in the party’s own contribution (Article 7(1) PPPA), and with determining remuneration according to the availability of the subject of the project (Article 7(2) PPPA) and maximum amounts of financial obligations that affect the level public finances (Article 17, Article 18 and Article 18a PPPA). Public sector units found the lack of official guidelines to execute EPCs problematic.

The discussed amendment is key for the issues analysed here because it changes the content of Article 7 EEA by adding other editorial units (paragraph), that is, (3) and (6). They refer to barriers discussed before, associated with a lack of or an insufficient amount of funds for ESCO projects and they resolve legal doubts concerning EEA and PPPA. At the moment, the obligations resulting from energy performance contracts do not affect the level of government debt or the public finance deficit in a situation where the energy service provider bears most of the risk of building and the risk of obtaining a guaranteed level of average annual energy savings taking into account the influence of factors, such as guarantees or financing by the said provider and allocation of assets when the agreement expires on the above risks. It also clarifies relations between PPPA and EEA, which at the moment are based on the principle of applying PPPA to EPCs only in cases not regulated in the EEA. By default, the choice of the supplier and the very performance of an EPC has been made more flexible. It also imposes a certain obligation on the minister responsible for climate matters. He must publish, in the Public Information Bulletin, the guidelines on signing energy performance contracts and information including the number of such contracts that has been concluded, along with likely average annual final energy savings, thanks to the implementation of pro-efficiency projects.

The EEA, amended in 2021, also introduced a national goal of final energy savings, which is implemented from 1 January 2021 till 31 December 2030.

The national goal set for 2030 will be pursued by means of the energy efficiency certificates scheme and alternative measures. They are understood to be programmes and instruments that serve to improve energy efficiency and that are financed from the state budget, budgets of local government units, the EU budget and funds from aids provided by the member states of the European Free Trade Agreement, funds of the National Funds for Environmental Protection and Water Management and funds of Voivodship environmental protection and water management. This external and internal financial support for projects that encourage improvement of energy efficiency by default is to inspire pro-efficiency actions by covering related costs. The key issue here is ensuring that the highest possible energy effect is reached, which may be carried out by using the financing model based on the aforementioned EPC. The Polish legislator assumes that an energy service company provides a service that improves energy efficiency of the beneficiary, while the remuneration (reimbursement of costs) for the service is obtained from the savings achieved by lowering the costs of energy used as a result of the introduced solutions. Such a contract model may be applied both in the public and the private sector.

In light of the above, it seems reasonable to ask the following research question: Will the current (after 1 January 2022 in line with the current EU guidelines and regulations) amended Polish normative EPC model lead to a breakthrough of the difficulties, so far diagnosed at the EU level, present on the Polish ESCOs market for public sector units in promoting and executing EPCs?

2. Research Method

This study adopts research methods which are typical to the field of EPC, described in detail by Zhang and Yuan [

10]. They show that case study, theoretical/mathematical analysis, and survey were the most applied research methods, and modelling and simulation, descriptive analysis, statistical analysis, and cost–benefit analysis were the most applied data analysis methods in EPC research. Analysis by Zhang and Yuan [

10] also showed that there are five main study topics in EPC research: 1. Implementation of EPC projects; 2. EPC mechanisms and business models; 3. Decision-making in EPC projects; 4. ESCOs in EPC projects; and 5. Risk management in EPC projects. In this paper, the crucial point is that EPC is examined in isolation from industry practice as the article focuses on an analysis of the legal framework which, by regulating the manner in which an EPC is concluded, allocates the rights and obligations of the parties to that contract and the rules of liability for the performance of the EPC. It investigated how this is going to shape such market practice. For this reason, the analysis carried out here fits into the new fields of research which were previously overlooked, focusing on areas other than energy, environment, engineering, business and economic analysis [

11], which are beginning to be explored in general [

12,

13,

14]. Indeed, it is about the legal framework and its role in application of EPC. For these reasons, the methods indicated are not alternatives to other methods, but are complementary to them, as they allow the research problem outlined to be analysed from a different research perspective that will highlight more the role of the legislator and the government in the application of the EPC. Hence, the primary source of the subject matter for the research was the regulations in force in Poland. When investigating the source material (texts of binding legal), research methods specific to legal sciences, classified as social sciences, were also used. Out of the main research methods applied in Polish scholarship, that is, the method of investigation of the law in force and the investigation of the historical evolution of a law and legal comparison, the first method was employed here [

15]. This research method focuses on the analysis and interpretation of legal provisions as they are. However, it does not only encompasses these aspects. This method also takes into account the views expressed in the literature and judicial decisions. Moreover, it refers to the objectives and values that the legal provisions are intended to serve or specifically protect. This was also an argument for the use of the statistical research method mentioned above. It should also be emphasised that the primary method referred to above makes it possible to assess the current state of the law (de lege lata conclusions) and to propose changes to this law in the future (de lege ferenda conclusions). For the purpose of interpreting legal regulations and creating legal norms on their basis, the derivational concept of legal interpretation created by professor Maciej Zieliński [

16] was used. It is expressed in the Latin maxim “omnia sunt interpretanda” [everything is subject to interpretation]. The process of legal interpretation begins with a linguistic analysis, the task of which is to determine the meaning of the expressions used in the legal text (legal regulations). It is particularly important in this concept to distinguish between a legal norm (understood as an independent editorial unit of a legal text that takes the form of a sentence in the grammatical sense) and a legal standard (as a result of the process of interpreting the legal text, which determines the behaviour of the addressee in a specific manner under specific circumstances). The process of interpretation is only completed when a clear and unambiguous legal norm is obtained in terms of its content, scope of regulation and application. This is due to the fact that legislative texts are drawn up at the descriptive level and read at the normative level (addressee, circumstances, and imperative/prohibition of a given behaviour), which inherently causes imprecision due to the ambiguity of the language in which the legislative text is drawn up [

17]. The research methods described above, which are used in this article, also allow us to situate the analyses conducted in the direction defined by Zhang and Yuan as the implementation of EPC projects in general, and in particular as an attempt to outline the factors influencing the implementation of EPC projects in public institutions and the main barriers to the promotion of EPC projects related to legal regulations [

10]. It should be emphasised that public administration bodies that implement internal (economic, and social) policies act on the basis and within the limits of the law—“

Certum est, quod is committit in legem, qui legis verba complectens contra legis nititur voluntatem” [it is certain that the one who understands the words of the law but acts contrary to its intention, violates the law].

Furthermore, descriptive analysis was used to analyse data, which was helpful in identifying EPC’s problems and measures. It should be noted, however, that the research carried out here is theoretical in nature. The statistical compilations expressed in the form of figures are for illustrative purposes only and are not based on the results of our own empirical research, as they are derived from publicly available databases (e.g., Eurostat). Their main purpose is to synthesise the economic or political context in order to better visualise and assess the adequacy of the current Polish legal regulations in terms of building a new EPC model and to assess its relevance to the ESCOs market.

3. Discussion

3.1. Legal Determinants as Factors That Adjust Barriers and Limitations in ESCO

The occurrence, already determined in the literature, of the main barriers to the development of the ESCOs market in the Polish economic and legal environment should be fully acknowledged. The most important ones include the lack of awareness of the importance of energy efficiency (disinformation and lack of knowledge), the lack of adequate models of project financing, the lack of an evaluation method for the energy savings of retrofit measures, and also legal regulations, including those that apply to public procurement, that preclude/impede the use of ESCOs (flawed legislation) [

18,

19,

20,

21]. It has also been noticed that the legislation and public forms of support, including support for public procurement processes, play a crucial role in the development of the ESCOs industry and also affect the policy that encourages conclusion of efficiency performance contracts [

22]. Thus, legal policies, which may be expressed in public policy interventions or in public–private partnerships, may eliminate market failures and barriers, which stop not only the development of investment in energy efficiency, but most of all prevent the ESCOs from achieving their optimal level [

23,

24]. The rank of identifying factors is so profound that, depending on internal determinants, it may either impede or encourage the development of ESCOs’ activity, especially where business models are based on energy performance contracting [

25,

26,

27,

28]. However, given the perspective of public institutions, two factors resound here that may be specified by a shared legal and economic denomination. On one hand, improvement of the public property and infrastructure’s energy efficiency is associated with the requirement to invest in technology that ensures reimbursement of expenses, even in the long run [

14,

29], which is an economic decision. However, on the other hand, such a decision has its legal implications related to government debt and the obligation to maintain a certain financial discipline, even though the model of operation of ESCOs may reduce the financial burden of a public entity because EPC-related savings are typically guaranteed [

25,

30,

31]. We must also agree with the results of research carried out following the example of energy performance contracting in China by Ruan, Gao and Mao. Their findings report that legal considerations that shape the policy of the EPC support system in the form of “financial incentive or tax preference” may not play a key role in the dynamics of the development of EPC projects or in igniting the activity of this economic sector. Ruan, Gao and Mao claim that, among other things, these factors usually affect the phase of project implementation, hence, at the stage of designing it is impossible to state unambiguously whether such support will be ultimately given [

32]. However, it must be emphasized that establishing mutual relations between different factors that affect the development of the EPC is a highly complex issue that is difficult to prove. Poland’s case is an example, where the legal considerations had to be the first step to stimulate the growth of the ECP’s market and PPC projects, because the previous legal formula made it impossible to develop these projects, especially in the scale of state and self-governance institutions. Polish barriers to ESCOs development could, in the future, yield a status determined by Jensen, Nielsen and Hansen in Danish municipalities, where in-house energy-efficient retrofitting projects might be more profitable for the municipality rather than ESCO contracts [

33].

The literature has seen attempts to point to remedies in the form of various initiatives which states could undertake to make the use of pro-efficiency projects that are part of the EPC and ESCOs services more attractive [

7,

31,

33,

34,

35]. Some of them require amendment of the existing law to adapt public procurement to existing conditions and the implementation of new financial mechanisms (such as the already mentioned incentives or tax preferences) [

31,

33]. The specificity of the issue under analysis also fits into the more general problem identified by Georgios and Flouros. [

36]. According to the authors, Poland belongs to the category of member states defined as “Foot-Dragging” in long-term strategies in energy and climate (next to Bulgaria, Croatia, Latvia, Luxembourg, and Malta). The development of the EPC and energy efficiency depends on the level of compliance with the European Commission’s directions and recommendations in each member state’s national energy and climate plans. This is why the legal environment is so crucial in this matter, as it determines the success of the implementation of solutions aimed at energy transition in the EU [

36]. Without a well-defined legal framework, which also implies the need for a new EPC model, achieving a climate-neutral economy by 2050 is in all probability, unlikely. However, proper adoption of the new legislation into the national legal system is more difficult than may be expected [

37].

3.2. The New EPC Model and Existing Forms of Supporting Energy Efficiency in Poland

So far, the development of energy efficiency took place through the energy efficiency certificates scheme. These certificates are called “white certificates” in the industry. Pursuant to Article 20 EEA, improvement of energy efficiency is still carried out by the system of these energy efficiency certificates. They are issued by the president of the Energy Regulatory Office (ERO) and awarded to entities that carry out projects that serve to improve energy efficiency. However, the amount of savings must be officially verified and confirmed by an independent audit. White certificates have a crucial feature in the fact that they apply to transferable property rights that are traded on stock markets. To streamline the trading in these property rights, entities obliged to carry out energy efficiency improvement projects with end-users obtain energy efficiency certificates and present them for remission, which in turn leads to obtaining the required final energy savings. Unfortunately, the energy efficiency certificates scheme in place now has turned out to be insufficient. One of the reasons for this state of affairs is awarding such certificates only for projects that aimed to improve energy efficiency with the assumption that the minimum threshold of energy savings at 10 toe will be crossed. In practice, implementation of pro-efficiency projects in cooperation with end-users was prevented.

Thus, alternative measures that are the domain of policy, programmes and funds from the environmental protection fund had to admitted, especially amendments of legislation on agreements for the improvement of energy efficiency, which also serve to implement the goals set out by the EU law. The determination of these barriers and limitations that are present in the Polish ESCOs market along with the new challenges specified in Directive 2018/2002/EU means that the law-maker must specify the situations in which EPCs do not contribute to increasing the government debt. This is the main problem when it comes to ESCOs projects in the public sector. Moreover, it is an even more pressing issue since pursuant to Article 18 of Directive 2018/2002/EU, the public sector still has the obligation to promote EPCs. Member states support the energy services market in appropriate cases; they facilitate the correct functioning of the energy services market by taking actions, where necessary, to remove regulatory and non-regulatory barriers which make the use of energy performance contracts more difficult. The European Commission, when assessing the implementation of Article 18 of Directive 2018/2002/EU, pointed out that there are many regulatory barriers in Poland which still need to be removed and stronger promotion of EPCs in the public sector is requisite. Therefore, in general, the regulation of Article 7 EEA was expanded to cover additional regulations that specify when implementation of EPCs will not increase government debt. The certainty of public entities in this regard should contribute to increased interest in EPCs among public sector entities. By doing so, public sector entities will be able to count part of the remuneration paid to the EPC provider (from the obtained energy savings) towards investment expenses, or expenses that do not affect the budgetary surplus.

3.3. New EPC Model and Obligations of Public Entities That Affect the Government Debt

As the EU assumes, pursuant to Article 2(27) of Directive 2018/2002/EU EPC means “a contractual arrangement between the beneficiary and the provider of an energy efficiency improvement measure, verified and monitored during the whole term of the contract, where investments (work, supply or service) in that measure are paid for in relation to a contractually agreed level of energy efficiency improvement or other agreed energy performance criterion, such as financial savings”. There is no doubt that Article 7(1) and (2) corresponds to this definition. In the Polish legal realities, EPCs are a basis to implement and operate a project that serves to improve energy efficiency by a public sector unit 7(1). Pursuant to Article 7(1), on the other hand, the minimum content of such a contractual agreement that determines the substantively essential elements of the content of the agreement (essentaili neglitii) and the possibility to qualify it as EPC, refers to specifying:

- (1)

attainable energy savings as a result of implementation of a project or projects of the same kind that serve to improve energy efficiency while taking into account the energy efficiency improvement measure; and

- (2)

ways to decide the remuneration, amount of which is dependent on energy savings obtained as a result of implementation of projects that serve to improve energy efficiency.

We must also note that the existing EPC model is understood as a model of implementation and financing of a project that serves to improve energy efficiency since the very moment EEA entered into force was supposed to be one of the measures to improve energy efficiency and that was to be complied with by public sector units when carrying out their public tasks (Article 6(1) and (2)(1) EEA).

However, at the moment, the existing formula which clearly did not meet the requirements of EPC beneficiaries, was modified. After 1 January 2022, obligations under an energy efficiency improvement agreement do not affect the level of government debt or public finance sector deficit, if the energy service provider bears the majority of the construction risk and the risk of achieving a guaranteed level of annual average energy savings. This is stated explicitly in Article 7(3) EEA. This is mainly about a sensitive problem of qualifying remuneration of the contractor, the amount of which is still dependent on energy savings obtained through the implementation of a project that improves energy efficiency. Hence, such a solution should not be qualified as a debt title counted towards the government debt, and even more so, it should not affect the public finances sector debt indicator. In this approach too, obligations under the EPC are not taken into account when establishing the public finances sector deficit, thus, it should not be taken into account when calculating expenses and revenues of public finances entities. Nevertheless, such measures are possible only in a specific situation which is an essential difference between the old and the existing EPC model. Exclusion of obligations under the EPC when calculating the amount of government debt and deficit is only possible if there is a specific distribution of obligations and risks in place between the beneficiary (public institution) and service provides (ESCO) involved in the implementation of a project which is the object of the EPC. A provider of services associated with energy use must bear the greater part of the risk of building and the risk of obtaining a guaranteed level of average energy savings, taking into account the impact of factors,, such as provider’s guarantees and financing of energy consumption-related services and allocation of assets after the termination of the agreement (Article 7(3) EEA). To avoid doubts associated with the practical application of the term “the greater part of the risk of building and the risk of guaranteed level of average annual energy savings”, which is to determine directly the model of the statutorily modified contractual balance between the EPC parties, Article 7(5) EEA lays down a competence norm for the minister responsible for matters of regional development. This minister shall, in agreement with the competence measures for climate matters and having asked the opinion of the President of Statistics Poland, specify, by way of a regulation, the scope of the risks referred to in Article 7(3) EEA.

Taking into account the content of the regulation of the Minister of Regional Funds and Policy of 22 December 2021 on the scope of the risk of building and the risk of obtaining a guaranteed level of average annual energy savings and detailed factors when assessing them (which for clarity will be hereinafter referred to as Energy Efficiency Risks Regulation, EERR), we may say that the content of each EPC should not only refer to two independent criteria that make up the scope of risks resting with the EPC parties and the determination that their greater part rests with the service provider; it should refer to specific factors that enable assessment of these risks.

There is no doubt that the EERR understands risk of building as incidents that cause a change in the costs or dates of creating new assets and improvement of the existing ones, in particular associated with finalising individual construction stages, which involve payment made by the public sector entity for the benefit of an energy service provider with the reimbursement of costs borne by a public sector entity by an energy service provider (Article 2(2) and (6) EERR). In turn, the risk of obtaining the guaranteed level of average annual energy savings covers events identified in the energy performance contract, which results in a failure to obtain a guaranteed level of average annual energy savings, in particular those associated with maintaining adequate standards when it comes to exploiting the new fixed assets or with verification of a public sector unit of the efficiency of a new fixed asset in relation to the guaranteed level of average annual energy savings (Article 3(2) and (10) EERR). However, as already pointed out, the mere diagnosis of risks when carrying out a project that serves to improve energy efficiency is not enough to exclude the impact of obligations that result from energy performance contracts on the level of government debt and the public finance deficit. When assessing the risk of building and the risk of obtaining a guaranteed level of average annual energy savings, it will take into account particular factors, such as the share of public measures in investment outlays made by the energy service supplier for the creation on new fixed assets or for the improvement of existing ones, rules for settlement in the event of failure to achieve the level of energy savings assumed in the energy performance contract, or guarantees issued by a public sector entity or energy service supplier that apply to securing the risk of building or the risk of obtaining a guaranteed level of average annual energy savings (Article 4(1), (4) and (11) EERR).

As may already be assumed, the more preferential conditions does an EPC create for a public institution, expressed especially in such modelling of the content that ensures that the interest of this individual is more protected in situations where there is a likelihood of incorrect performance of the EPC or of failure to achieve assumed results, the more likely it will be that EPC obligations will not be counted towards the government debt or the public sector deficit. However, given that EPC projects require a longer time horizon and also the fact that remuneration of a service provider takes the form of a success fee for obtaining maximum energy effect by a public entity, it will become necessary to create an attractive system of remunerating these providers. This remuneration will bring motivation and reasoning to the provider so that he may take on most of the risks that go along with projects that serve to improve energy efficiency. Remuneration or reimbursement of costs is paid to the provider out of the very savings obtained from reducing costs of the energy used that result from implemented solutions. Of course, these requirements, especially EERR, will not apply to EPCs in which the public finances sector entity distributes the risk of responsibility for a correct implementation of pro-efficiency solutions differently. Specific clarification in the wording of Article 7(3) EEA of when the use of EPC contracts does not result in an increase in public debt should increase interest in such contracts among public sector entities, as they will determine this impact when shaping the content of EPCs.

3.4. A New EPC Model and Public–Private Partnership

We may assume that EEA amendment of 1 January 2022 greatly settled legal doubts relating to problems of the applications of the laws to EPCs and ESCOs. These laws include the following: 1. EEA; 2. PPPA; and 3. Public Procurement Act. At the moment, application of PPPA to EPC-related matters was limited only to issues not regulated in EEA, excluding certain PPPA provisions that in fact caused controversy in pro-efficiency projects. This already follows directly from Article 7(6) EEA. As a result, a public institution (future beneficiary of an ESCO project) is no longer obliged to the following:

- (1)

carry out an assessment of the efficiency of implementation of a project as part of a public–private partnership compared to the efficiency of its implementation somehow, in particular when only using public funds. Apart from that, it was necessary as part of this audit to take into account the planned division of tasks and risks between the public entity and the private partner, the estimated costs of the project life cycle and the time necessary to implement the project (Article 3a PPPA);

- (2)

bring in their own contribution as part of cooperation to achieve the goal of the project (Article 7(1) PPPA);

- (3)

determine remuneration of a private partner, which was mostly dependent on the real use or actual availability of the project’s subject matter (Article 7(2) PPPA);

- (4)

observe the total amount, specified by statute, up to the value of which government authorities may make financial commitments in a given year on the basis of public–private partnership act (Article 17 PPPA);

- (5)

obtain permission from the minister responsible for matters of public finances to finance a project from the state budget in the amount not exceeding PLN 1,000,000 (Article 18 PPPA);

- (6)

apply Article 18a PPPA, pursuant to which obligations resulting from a public–private partnership do not affect the level of public debt and the deficit of the public finances sector when the private partner bears most of the risk of building and majority of the risk of availability or risk of demand and maximum amounts of financial obligations on the level of finances.

This legislative measure meant that provisions which did not respect the essence and specific characteristics of this type of services did not need to apply to EPC and to using ESCO services. The obligation referred to in

Section 1 to carry out an assessment of the efficiency of implementation of a future project by the private entity meant that using its services was questioned. Since a detailed audit of efficiency of implementation of such types of project with their own efforts and at their own expense before a decision to conclude an EPC is made, information and data must be obtained that usually may be an effect of an ESCO activity. Therefore, if a public institution had appropriate knowledge about the factors that consume energy non-rationally and about how to solve this situation, then the use of EPCs had no point if the public institution could achieve the same result through public procurement, thanks to the knowledge they gained through the audit. The public–private partnership agreement is usually applied when project’s expected efficiency cannot be obtained in any other way. Public institutions are obliged to apply public procurement, which is a basic form of establishing contractual relations with participants of economic trading whose objects is for the commissioner to obtain supplies and services from the selected building contractor. In light of the above, resignation from EPCs in favour of a public procurement should not raise any doubts, if as a result of the audit referred to above, a public entity has a concrete solution at hand that could be achieved this way too.

Even if as a result of the audit under Article 3a PPPA, the public entity had the knowledge that it should apply ESCO due to the scale of the project and its specific characteristics, which was not achieved under public procurement, then a problem against the financial aspect of the future project surfaced. Existing solutions diverted from the EPC construction, whose obligatory element, as opposed to PPPs, is not the obligation of the beneficiary of the pro-effectiveness service to bring in their own contribution. Moreover, service provider’s remuneration usually takes the form of a success fee, thus requiring the provider to take actions that ensure maximum energy efficiency as it will directly translate to the remuneration paid. In this regard, the possibility to model EPCs content according to commonly recognized specific characteristics of this type of contractual relation was restored.

4. Conclusions

Summing up this discussion, we need to point out that the EPC model in force in Poland since 1 January 2022 will theoretically constitute a means of improving energy efficiency in public sector units. The currently applicable laws in EEA clearly establish a legal regulation applicable to assessing the conclusion and execution of projects by ESCOs.

We may point out that it satisfied not only the barriers and limitations reported and diagnosed in Polish conditions (described in more detail in part I), but its normative model corresponds to the EU law and trends expressed in the literature (part II). The example of the Polish ESCOs market in the theoretical approach will be one of the factors that inspire ESCOs’ activity, especially from the perspective of public entities. It is mainly possible because the activity of public institutions is based on law and is contained within its boundaries, especially when administering public property where the person who has public funds may perhaps bear not disciplinary (organizational) liability for potential errors, but also—in the case of gross violations—criminal liability.

The question asked in the first part of this paper get an affirmative answer. The statutory model of energy performance contracting can be a means of improving energy efficiency in public sector units, but under certain conditions.

We must clearly state that the current (post 1 January 2022) amended Polish EPC model has led to the breaking of barriers on the Polish ESCOs market (so far determined in the EU) for the public sector entities in promoting and implementing EPCs. This means that at the moment, the relation between obligations under EPCs and government debt and public deficit are referred to directly or naturally after meeting certain conditions. The exclusion of EPC liabilities in public debt and deficit calculations is only possible if the distribution of responsibilities and risks between the beneficiary (public institution) and the service provider (ESCO) for the performance of the project, that is the subject of the EPC, is shaped in a specific way. The ESCO must bear most of the construction risk and the risk of achieving a guaranteed level of annual average energy savings, taking into account the impact of factors, such as guarantees and financing by the ESCO and the allocation of assets at the end of the contract. In order to avoid doubts about the practical use in contracts of the ambiguous term “the majority of the construction risk and the risk of achieving a guaranteed level of annual average energy savings”, which is supposed to directly determine the shape of the statutorily modified contractual balance between the parties to the EPC, Article 7 (5) EEA obliges the minister responsible for regional development to define the scope of these risks. As a result, it should be pointed out that the content of each EPC should not only refer to two independent criteria making up the scope of risks incumbent on the parties to the EPC, but also, in order to establish that the majority of them rest with the service provider, it should refer to specific factors making it possible to assess these risks. This means that the mere identification of risks in the implementation of an energy efficiency project is not sufficient to exclude the impact of obligations arising from energy efficiency contracts on the level of government debt and the deficit of the public finance sector. When assessing the construction risk and the risk of achieving a guaranteed level of annual average energy savings, special consideration will be given to factors, such as the share of public funds in the investment expenditure incurred by the energy efficiency provider for the production of new fixed assets or the improvement of existing ones. The more preferential the conditions for a public body, especially in the formulation of the content, such that the interest of this body will be more protected in situations involving the possibility of incorrect implementation of the EPC or failure to achieve the intended results, the more likely it will be that the obligations from the EPC will be excluded from inclusion in the public debt and public sector deficit. Of course, the indicated requirements, especially from the EERR, will not apply to those EPCs in which the public finance sector entity distributes the risks of responsibility for the correct implementation of the pre-efficiency measures differently. As a result, it is the beneficiary of a pro-efficiency service, taking the decision to implement an ESCO project, that will be able to decide (when drafting the content of an EPC) whether it will affect the level of government debt and the public finances sector deficit.

The overlapping regulations concerning the correct procedure for implementing projects under EPC (EEA; PPPA; and Public Procurement Act) were clearly separated. In matters not regulated by the EEA, the provisions of the Public–Private Partnership Act of 19 December 2008 and the provisions of the Public Procurement Law shall apply to the EPC financed in whole or in part by the supplier of energy consumption services, including the procedure for the selection of that supplier. This legislative intervention made it possible to exclude the application to EPCs and the use of ESCO services of provisions that did not respect the essence and specificity of this type of service. The exclusion of the need to precede the decision to conclude an EPC with a detailed audit of the effectiveness of the implementation of this type of project at the institution’s own effort and expense made it possible to avoid the duplication of activities that can usually be the result of an ESCO. In this way, the public institution does not have adequate knowledge of the factors that consume energy irrationally and the potential way to solve this situation, which is one of the reasons for concluding an EPC. From this point of view, if a public institution, using its own resources, identifies an irrational energy use problem and is able to provide a solution to the situation, then it can already achieve this on its own through a public procurement. A public–private partnership contract, on the other hand, is usually used when the expected efficiency of a project cannot be achieved by other means.

Also, a method was created to remove disinformation and discrepancies in action strategies of various public institutions, which arose due to the lack of an official (ministerial or governmental) internal policy. At the moment, the minister responsible for climate matters is obliged to publish (in the Public Information Bulletin on the website of a relevant office) the guidelines concerning the conclusion of energy performance contracts. Moreover, the same authority is to present the minister responsible for climate matters until 31 March, the following information: (1) the number of energy performance contracts signed, and (2) average annual final energy consumption savings attainable due to the implementation of projects to improve energy efficiency and the period in which these savings were obtained for the previous calendar year. Moreover, thanks to the amendment of the EEA, the Eurostat guidelines and norms of the EERR, the scope of risks and their assessment, which will have a prime impact in their assessment, need to take into account EPC obligations for issues associated with public funds. However, it is important to emphasise that the new legal model of energy performance contracting that is in line with the current EU guidelines and regulations cannot ultimately be a sufficient factor to increase the number and level of implementation of ESCO projects in public sector units in Poland. The theoretically analysed EPC model resulting from EEA corresponds to the needs determined so far. However, even though this regulation in question has been in force for a year now, the minister responsible for climate matters has not published in the Public Information Bulletin, the guidelines on concluding energy performance contracts. Practical doubts also appear in relation to the nominal model,, taking into consideration factors when assessing the risk of building and the risk of obtaining a guaranteed level of average annual energy savings. These savings will be crucial in determining the incredibly vague term referring to the service supplier (ESCO), who in certain circumstances is supposed to bear “the most of the risk of building and the risk of obtaining a guaranteed level of average yearly energy savings taking into account the influence of factors, such as guarantees or financing by the said provider and allocation of assets when the agreement expires on the above risks”. It is not ruled out that the legislator, trying to counteract one barrier on the ESCO market, might have created a basis for creating a new limitation associated with the fact that it will not be profitable for ESCO interests to take on the major part of the risk of building and the risk of obtaining a guaranteed level of average annual energy savings. Naturally, it is a preliminary diagnosis at this stage of implementation of the new regulation, although it has been identified in the literature referred to in part II.

To sum up, we may point out that the legal policies in the Polish circumstances have allowed the creation of a theoretical EPC model which steps up to face the most pressing problems. Introduction of amendments in Article 7 EEA has allowed a clarification of the situations in which an EPC has no effect on increasing government debt, which was one of the key barriers to EPC application in the public sector, especially at the local level. Therefore, we may expect that relevant amendments to clarify regulations under which the government debt does not increase when executing EPCs will contribute to increased interest in such contracts among public sector entities.

EPC was more precisely differentiated against public–private partnership, especially in a statistical approach. Relying only on the method of remuneration was not a clear factor that differentiated EPCs from public–private partnership agreements, especially when it comes to classification of a project as an EPC in the statistical approach. At the moment, the EEA moves away from the term “private partner” used in the EPC to denote the other party and instead adopts the term “energy service provider”. Therefore, we may say that the new EPC model is a result of ensuring a stable legal environment for projects devoted to improve energy efficiency and to implement the 2017 Eurostat guidance note on EPC-related accounting.

{kind=link}

{kind=link}