Carbon Tax in Taiwan: Path Dependence and the High-Carbon Regime

Abstract

1. Introduction

2. Theoretical Framework: Path Dependence and the High-Carbon Regime

2.1. Path Dependence: The Carbon Lock-In Effect

2.2. The East Asian Factor

3. Methods

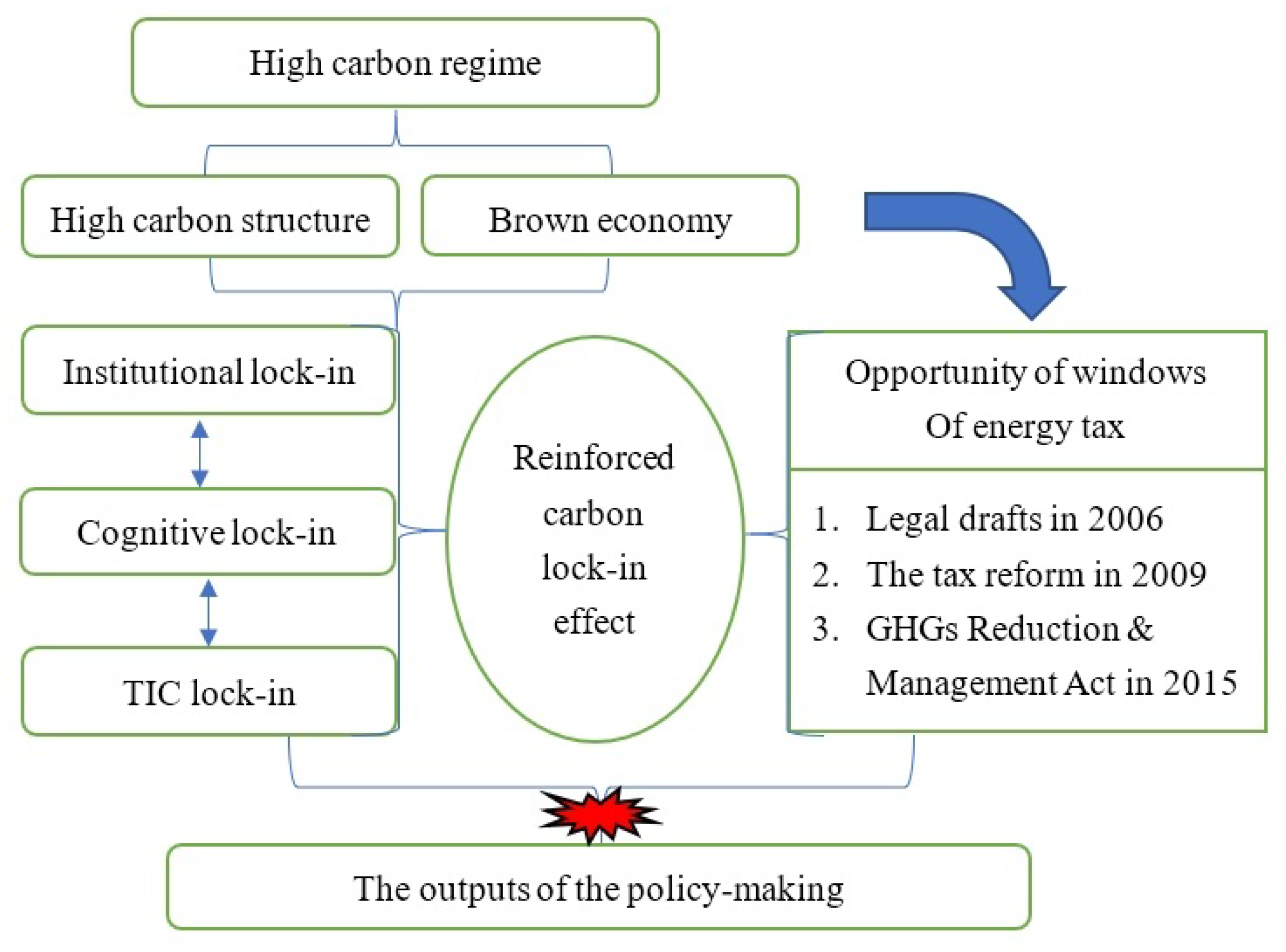

3.1. Identification of the High-Carbon Regime and the Carbon Lock-In Effect

3.2. Data Collection

4. Analysis

4.1. High-Carbon Regime

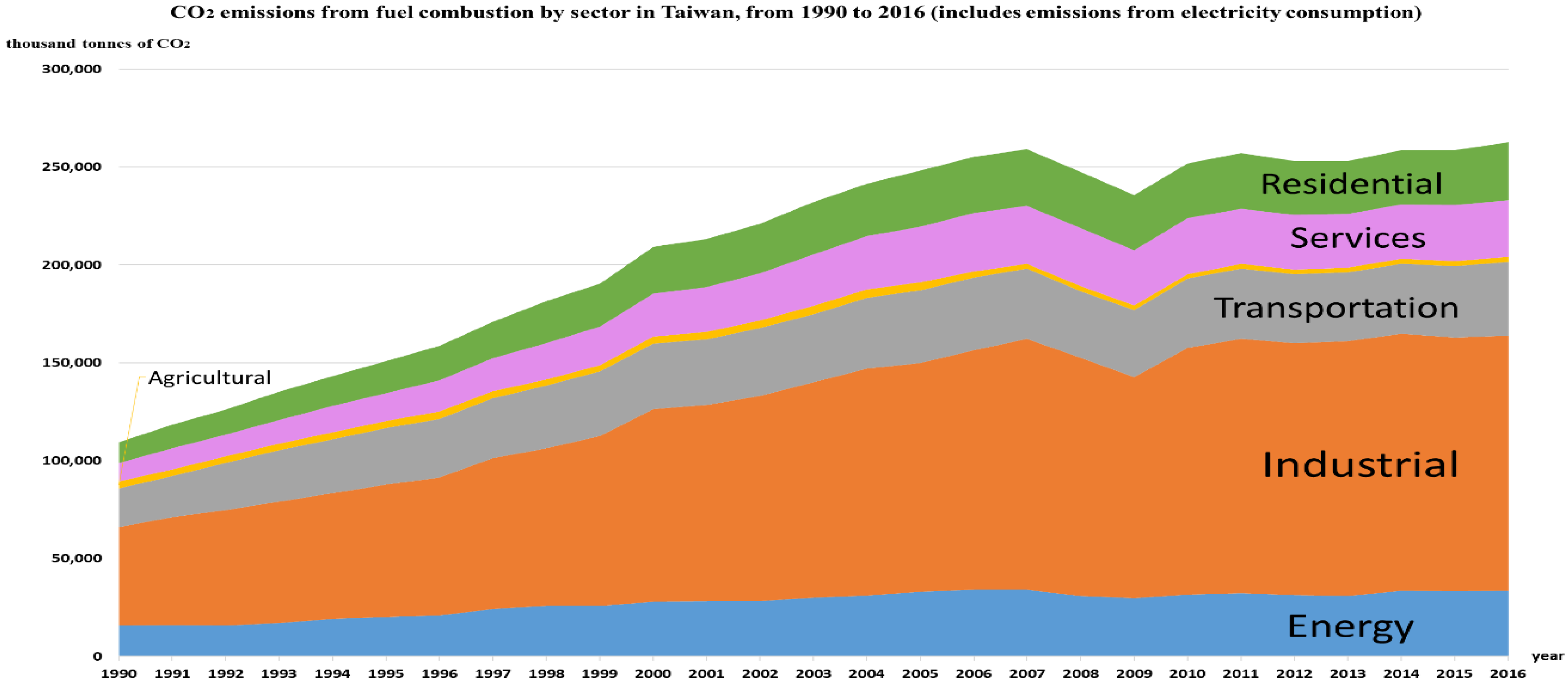

4.1.1. Raising the Curtain on Taiwan’s High-Carbon Economy

4.1.2. The Carbon Lock-In Effect within Taiwan’s Brown Economy

The Institutional Carbon Lock-In Effect

The Cognitive Aspect of the Carbon Lock-In Effect

The Carbon Lock-In Effect of the TIC Complex

4.2. Three Lost Windows of Opportunity

4.2.1. Three Windows of Opportunity

First Window of Opportunity: Taiwan’s First Move to Draft Energy Taxation Legislation (1998–2006)

Second Window of Opportunity: Tax Reformation Period (2007–2014)

Third Window of Opportunity: The Greenhouse Gas Reduction and Management Act (2015–2020)

4.2.2. Lack of Pressure from Social Movements

5. Discussion and Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Organization | No. of Respondents | Date |

|---|---|---|

| Government organization | ||

| Environmental Protection Administration, R.O.C. | 1 | 24 June 2020 |

| 1 | ||

| 1 | ||

| National Development Council | 1 | 29 July 2021 |

| Ministry of Finance, R.O.C. | 1 | 24 August 2021 |

| Ministry of Economic Affairs, R.O.C. | 2 | 24 August 2021 |

| Legislative Department | ||

| Legislator | 2 | 24 June 2020 |

| 2 | 29 July 2021 | |

| Legislator’s office | 1 | 3 July 2020 |

| Industry organizations | ||

| Chinese National Federation of Industries | 1 | 24 June 2020 |

| 1 | 29 July 2021 | |

| Chinese Petroleum Institute | 1 | 29 July 2021 |

| China Steel Corporation | 1 | 24 August 2021 |

| CPC Corporation, Taiwan | 1 | 24 August 2021 |

| Taipei Computer Association | 1 | 24 August 2021 |

| Research institutions (NGO/University/Think tanks) | ||

| Green Citizens’ Action Alliance | 1 | 24 June 2020 |

| 1 | 23 September 2021 | |

| Taiwan Youth Climate Coalition | 1 | 24 August 2021 |

| Greenpeace | 1 | 23 September 2021 |

| Citizen of the Earth, Taiwan | 1 | 3 July 2020 |

| 1 | 23 September 2021 | |

| National Taipei University of Business | 1 | 24 June 2020 |

| 1 | 23 September 2021 | |

| National Taipei University | 1 | 23 September 2021 |

| Academia Sinica | 1 | 24 June 2020 |

| 1 | 23 September 2021 | |

| Total | 29 |

References

- World Bank. State and Trends of Carbon Pricing Mechanism. 2020. Available online: https://openknowledge.worldbank.org/handle/10986/33809 (accessed on 12 December 2020).

- Chou, K.T. Sociology of Climate Change: High Carbon Society and Its Transformation Challenge; National Taiwan University Press: Taipei, Taiwan, 2017. [Google Scholar]

- International Energy Agency. CO2 Emissions from Fuel Combustion. 2019. Available online: https://www.oecd-ilibrary.org/energy/co2-emissions-from-fuel-combustion-2019_2a701673-en (accessed on 12 December 2020).

- Aklin, M.; Urpelainen, J. Political competition, path dependence, and the strategy of sustainable energy transitions. AJPS 2013, 57, 643–658. [Google Scholar] [CrossRef]

- Voß, J.P.; Kemp, R.; Bauknecht, D. Reflexive Governance: A View on an Emerging Path. In Reflexive Governance for Sustainable Development; Elgar: Cheltenham, UK, 2006; pp. 419–437. [Google Scholar]

- Rip, A. A co-evolutionary approach to reflexive governance—And its ironies. In Reflexive Governance for Sustainable Development; Elgar: Cheltenham, UK, 2006; pp. 82–100. [Google Scholar]

- Unruh, G.C. Understanding carbon lock-in. Energy Policy 2000, 28, 817–830. [Google Scholar] [CrossRef]

- Seto, K.C.; Davis, S.J.; Mitchell, R.B.; Stokes, E.C.; Unruh, G.; Ürge-Vorsatz, D. Carbon lock-in: Types, causes, and policy implications. Annu. Rev. Environ. Resour. 2016, 41, 425–452. [Google Scholar] [CrossRef]

- Lehmann, P.; Creutzig, F.; Ehlers, M.H.; Friedrichsen, N.; Heuson, C.; Hirth, L.; Pietzcker, R. Carbon lock-out: Advancing renewable energy policy in Europe. Energies 2012, 5, 323–354. [Google Scholar] [CrossRef]

- Unruh, G.C. Escaping carbon lock-in. Energy Policy 2002, 30, 317–325. [Google Scholar] [CrossRef]

- Aghion, P.; Hepburn, C.; Teytelboym, A.; Zenghelis, D. Path Dependence, Innovation and the Economics of Climate Change. Policy Paper. 2014. Available online: https://www.lse.ac.uk/granthaminstitute/publication/path-dependence-innovation-and-the-economics-of-climate-change/ (accessed on 12 December 2020).

- Pierson, P. Increasing returns, path dependence, and the study of politics. Am. Political Sci. Rev. 2000, 94, 251–267. [Google Scholar] [CrossRef]

- Rotmans, J.; Loorbach, D. Towards a Better Understanding of Transitions and Their Governance: A Systemic and Reflexive Approach. In Transitions to Sustainable Development: New Directions in the Study of Long-Term Transformative Change; Routledge: New York, NY, USA, 2010; pp. 105–199. [Google Scholar]

- Kasa, S. Policy networks as barriers to green tax reform: The case of CO2-taxes in Norway. Environ. Politics 2000, 9, 104–122. [Google Scholar] [CrossRef]

- Svendsen, G.T.; Daugbjerg, C.; Hjøllund, L.; Pedersen, A.B. Consumers, industrialists and the political economy of green taxation: CO2 taxation in OECD. Energy Policy 2001, 29, 489–497. [Google Scholar] [CrossRef]

- Klenert, D.; Mattauch, L.; Combet, E.; Edenhofer, O.; Hepburn, C.; Rafaty, R.; Stern, N. Making carbon pricing work for citizens. Nat. Clim. Change 2018, 8, 669–677. [Google Scholar] [CrossRef]

- Kawakatsu, T.; Rudolph, S.; Lee, S. The Japanese carbon tax and the challenges to low-carbon policy cooperation in east Asia. In Tax Law and the Environment: A Multidisciplinary and Worldwide Perspective; Lexington Books: Littlefield, TX, USA, 2018; pp. 85–103. [Google Scholar]

- Kim, E.S. The politics of climate change policy design in Korea. Environ. Politics 2016, 25, 454–474. [Google Scholar] [CrossRef]

- Dent, C.M. Renewable Energy in East Asia: Towards a New Developmentalism; Routledge: London, UK, 2014. [Google Scholar]

- Dent, C.M. East Asia’s new developmentalism: State capacity, climate change and low-carbon development. Third World Q 2018, 39, 1191–1210. [Google Scholar] [CrossRef]

- Kim, S.Y.; Thurbon, E. Developmental environmentalism: Explaining South Korea’s ambitious pursuit of green growth. PAS 2015, 43, 213–240. [Google Scholar] [CrossRef]

- Kameyama, Y. Climate Change Policy in Japan: From the 1980s to 2015; Routledge: New York, NY, USA, 2017. [Google Scholar]

- Proposal on Japan’s Long-Term Growth Strategy under the Paris Agreement. 2019. Available online: https://www.keidanren.or.jp/en/policy/2019/022.html (accessed on 2 February 2021).

- Hasegawa, T.; Fujimori, S.; Takahashi, K.; Masui, T. Scenarios for the risk of hunger in the twenty-first century using Shared Socioeconomic Pathways. Environ. Res. Lett. 2015, 10, 014010. [Google Scholar] [CrossRef]

- Hasegawa, K. Continuities and discontinuities of Japan’s political activism before and after the Fukushima disaster. In Social Movements and Political Activism in Contemporary Japan; Routledge: London, UK, 2018; pp. 115–136. [Google Scholar]

- Sugiman, T. Lessons learned from the 2011 debacle of the Fukushima nuclear power plant. Public Underst. Sci. 2014, 23, 254–267. [Google Scholar] [CrossRef]

- Aldrich, D.P. Rethinking civil society–state relations in Japan after the Fukushima accident. Polity 2013, 45, 249–264. [Google Scholar] [CrossRef]

- Kingston, J. After 3.11: Imposing Nuclear Energy on a Skeptical Japanese Public 3.11. 2014. Available online: https://apjjf.org/2014/11/23/Jeff-Kingston/4129/article.html (accessed on 2 February 2021).

- Matsumoto, M. “Structural disaster” long before Fukushima: A hidden accident. Dev. Soc. 2013, 42, 165–190. [Google Scholar] [CrossRef]

- Funabashi, H. Why the Fukushima nuclear disaster is a man-made calamity. Int. J. Jpn. Sociol. 2012, 21, 65–75. [Google Scholar] [CrossRef]

- Ku, D. The anti-nuclear movement and ecological democracy in South Korea. In Energy Transition in East Asia: A Social Science Perspective; Routledge: London, UK, 2017; pp. 28–44. [Google Scholar]

- Chou, K.T. Tri-helix energy transition in Taiwan. Energy Transition. In Energy Transition in East Asia: A Social Science Perspective; Routledge: London, UK, 2018; pp. 34–54. [Google Scholar] [CrossRef]

- Chou, K.T.; Liou, H.M. Analysis on energy intensive industries under Taiwan’s climate change policy. Renew. Sustain. Energy Rev. 2012, 16, 2631–2642. [Google Scholar] [CrossRef]

- International Energy Agency. Energy-Related Emissions of CO2 Statistic and Analysis. 2020. Available online: https://www.moeaboe.gov.tw/ECW/populace/news/wHandNews_File.ashx?file_id=18440 (accessed on 12 December 2020).

- Chou, K.T.; Liou, H.M. Climate change governance in Taiwan: The transitional gridlock by a high-carbon regime. In Climate Change Governance in Asia; Routledge: London, UK, 2020; pp. 27–56. [Google Scholar] [CrossRef]

- International Energy Agency. Electricity Information. 2019. Available online: https://iea.blob.core.windows.net/assets/8237c23b-1fde-41a8-ba8b-9d136f0eafef/Electricity_documentation.pdf (accessed on 12 December 2020).

- NUS Consulting Group. 2005–2006 International Water Report & Cost Survey. 2006. Available online: https://www.vewin.nl/SiteCollectionDocuments/Nieuws%202007/2006WaterSurvey-NUS.pdf (accessed on 2 February 2021).

- International Water Association. Total Charge Drinking Water for 160 Cities in 2015 for a Consumption of 200 M3. 2015. Available online: http://waterstatistics.iwa-network.org/graph/9 (accessed on 12 December 2020).

- The Conference Board. Manufacturing Hourly Compensation Costs. 2006. Available online: https://conference-board.org/ilcprogram (accessed on 12 December 2020).

- Martinez-Covarrubias, J.; Garza-Reyes, J.A. Establishing framework: Sustainable transition towards a low-carbon economy. In The Low Carbon Economy; Palgrave Macmillan: London, UK, 2017; pp. 15–31. [Google Scholar]

- Low-Carbon Heat Solutions for Heavy Industry: Sources, Options, and Costs Today. 2019. Available online: https://www.earth.columbia.edu/projects/view/1995 (accessed on 12 December 2020).

- China National Federation of Industries. The CNFI White Paper 2008—Issue on Industry; CNFI: Taipei, Taiwan, 2008; Available online: http://www.cnfi.org.tw/front/bin/ptdetail.phtml?Part=2008-2&Category=100003 (accessed on 17 October 2022).

- China National Federation of Industries. The CNFI White Paper 2015—Issue on Industry; CNFI: Taipei, Taiwan, 2015; Available online: http://www.cnfi.org.tw/front/bin/ptdetail.phtml?Part=2015-2&Category=100003 (accessed on 17 October 2022).

- China National Federation of Industries. The CNFI White Paper 2016—Issue on Industry; CNFI: Taipei, Taiwan, 2016; Available online: http://www.cnfi.org.tw/front/bin/ptdetail.phtml?Part=2016-2&Category=100003 (accessed on 17 October 2022).

- Sun, M.T. Taiwan Economic Review and Outlook in 2015–2016. TIER Mon. 2016, 39, 65–72. [Google Scholar]

- Carbon Disclosure Project. 2021. Available online: https://www.cdp.net/en/scores (accessed on 12 December 2020).

- China National Federation of Industries. The CNFI White Paper 2012—Issue on Industry; CNFI: Taipei, Taiwan, 2012; Available online: http://www.cnfi.org.tw/front/bin/ptdetail.phtml?Part=2012-2&Category=100003 (accessed on 17 October 2022).

- Tung, G.H. Professional Lies: Nuclear Electricity Industry Discourse Transition and Environmental Crisis. 2014. Available online: https://rsprc.ntu.edu.tw/zh-tw/m01-3/en-trans/84-professional-lie.html (accessed on 12 December 2020).

- Tseng, C.-W. Research on Energy Taxation. Ministry of Finance’s Taxation Reform Commission. 1989. Available online: http://nccur.lib.nccu.edu.tw/handle/140.119/71962 (accessed on 12 December 2020).

- Shaw, D.-K.; Hunang, Y.-H. Project Report: Research on Green Taxation. Investigated. 2008. Available online: https://www.grb.gov.tw/search/planDetail?id=1647469 (accessed on 12 December 2020).

- Shyu, C.W. Taiwan’s Governance and Policy on Responding to Climate Change. HSSNQ 2014, 15, 25–32. [Google Scholar] [CrossRef]

- Lu, I.-J. Conclusion on National Energy Conference: Progress and Review Report. 2009. Available online: https://e-info.org.tw/node/42533 (accessed on 12 December 2020).

- Bureau of Energy. The Era of Paying for the Environment: A Brief Introduction of Carbon Tax. 2003. Available online: https://magazine.twenergy.org.tw/Cont.aspx?CatID=31&ContID=362 (accessed on 12 December 2020).

- National Council for Sustainable Development. R.O.C. Strategic Guidelines on Sustainable Development. 2000. Available online: https://nsdn.epa.gov.tw/taiwan-sdgs/taiwan-agenda-21 (accessed on 12 December 2020).

- Bureau of Energy. An Environmental Sound Taxation on Carbon. 2005. Available online: https://magazine.twenergy.org.tw/Cont.aspx?CatID=28&ContID=872 (accessed on 12 December 2020).

- Bureau of Energy. Views of the Ministry of Economic Affairs on the Promotion of Energy Tax. Energy Magazine. 2006. Available online: https://magazine.twenergy.org.tw/Cont.aspx?CatID=28&ContID=1051 (accessed on 12 December 2020).

- China Technical Consultants Inc foundation. Workshop Minutes: The Introduction of the Energy Tax. 2007. Available online: https://www.ctci.org.tw/8838/research/26382/26448/ (accessed on 2 December 2020).

- Cheng, C.-F. Energy Tax Will Be Levied as Soon as Next Year: Progressively Increasing in the Following 9 Years. 2006. Available online: https://news.ltn.com.tw/news/politics/paper/89583 (accessed on 12 December 2020).

- Environmental Information Center. Ministry of Finance: The Timing Is Not Right Now for the Energy Tax. 2006. Available online: https://e-info.org.tw/node/5218 (accessed on 2 December 2020).

- Fan, C.F. Analyzing the Energy Tax Act Bill. Taiwan Law Rev. 2009, 174, 88–100. [Google Scholar]

- Energy Tax Should Not Be Levied. 2006. Available online: http://www.cnfi.org.tw/front/bin/ptlist.phtml?Category=100221 (accessed on 12 December 2020).

- Lin, Y.-C. Two Ministers of Finance, Chuan Lin and Chih-Chin Ho, Both Urged to Introduce Energy Tax to Cover the National Treasury. 2012. Available online: https://www.new7.com.tw/SNewsView.aspx?Key&i=TXT20120606151414G6Y&p=186 (accessed on 2 December 2020).

- Environmental Information Center. CO2 Emissions in 2025 Will Return to 2000. 2008. Available online: https://e-info.org.tw/node/32037 (accessed on 2 December 2020).

- Environmental Information Center. Reducing Carbon Emissions. Liang Qiyuan: Nuclear Energy, Energy Taxation and International Cooperation. 2009. Available online: https://e-info.org.tw/node/42492 (accessed on 2 December 2020).

- Kao, C.-H. Energy Tax Caused at Least 200,000 People to Lose Their Jobs. 2009. Available online: https://ec.ltn.com.tw/article/paper/328195 (accessed on 2 December 2020).

- Merit Times. The Steel Industry Deemed the Carbon Tax to Have a Great Impact. 2009. Available online: https://www.merit-times.com/NewsPage.aspx?unid=150730 (accessed on 2 December 2020).

- Kao, W.-Y. Business Groups Strongly Opposed the Energy Tax. 2012. Available online: https://www.chinatimes.com/newspapers/20120819000271-260102?chdtv (accessed on 2 December 2020).

- Atomic Energy Council, Executive Yuan. The Study of Energy/Carbon Tax Scheme and Tax Rate Setting Methods. 2014. Available online: https://www.aec.gov.tw/share/file/information/pOuINmZh3uxRNotY~~WAYg.pdf (accessed on 2 December 2020).

- Liu, T.-Y.; Chou, Y.-F.; Li, P.-H. The Maintenance of Integrated Energy and Economic Model and Relevant Strategy Assessment (2/3). 2015. Available online: https://www.grb.gov.tw/search/planDetail?id=8211321 (accessed on 2 December 2020).

- Tseng, C.-J. Please Listen to Me. 2015. Available online: https://magazine.twenergy.org.tw/Cont.aspx?CatID=19&ContID=2439 (accessed on 2 December 2020).

- Executive Yuan. Conclusion on the Fourth National Energy Conference. 2014. Available online: http://www.twnwea.org.tw/Files/b17d1459-b22a-4d38-b9c6-3c552dbbd848.pdf (accessed on 12 December 2020).

- Huang, T.-R.; Tang, Y. The Introduction of a Carbon Tax Will Push Industrial Upgrading. 2015. Available online: https://www.chinatimes.com/newspapers/20150526000413-260114?chdtv (accessed on 2 December 2020).

- China National Federation of Industries. Raised the Issue of Power Shortage, Gu Chengyun Called on the New Government to Sit Down and Talk. 2016. Available online: https://www.taiwannews.com.tw/ch/news/2908902 (accessed on 12 December 2020).

- Van Stekelenburg, J.; Klandermans, B.; Van Dijk, W.W. Context matters: Explaining how and why mobilizing context influences motivational dynamics. J. Soc. Issues 2009, 65, 815–838. [Google Scholar] [CrossRef]

- Bureau of Energy. National Electricity Resources Supply and Demand Report 2022; BOE: Taipei, Taiwan, 2022. Available online: https://www.moeaboe.gov.tw/ECW/populace/content/wHandMenuFile.ashx?menu_id=20851&file_id=10995 (accessed on 17 October 2022).

- China National Federation of Industries. The CNFI White Paper 2021; CNFI: Taipei, Taiwan, 2021; Available online: http://www.cnfi.org.tw/front/bin/ptdetail.phtml?Part=20210812-1&Category=100003 (accessed on 17 October 2022).

- Xu, R.; Xu, B. Exploring the effective way of reducing carbon intensity in the heavy industry using a semiparametric econometric approach. Energy 2022, 243, 123066. [Google Scholar] [CrossRef]

- Xu, B.; Luo, Y.; Xu, R.; Chen, J. Exploring the driving forces of distributed energy resources in China: Using a semiparametric regression model. Energy 2021, 236, 121452. [Google Scholar] [CrossRef]

| IPP (Installed Capacity) | Shareholding Ratio | Investor GHG Emissions (Mt Tons) in 2015 | Contribution Ratio of Investor Emissions to National Emissions in 2015 1 |

|---|---|---|---|

| Mai-Liao Power Plant (Coal) (1.8 GW) | 100% | Formosa Plastics: 55.1576 (including Formosa Plastics (8.8976), Nan Ya Plastics (6.293), Formosa Chemical and Fiber Corp (10.612), and Formosa Petrochemical (29.355)) | 21.3% of total national emissions |

| He-Ping Power Plant (Coal) (1.3 GW) | 70% | Taiwan Cement Company: 5.237 | 2.03% of total national emissions |

| IPP (Investor) | Power Generated (TWh) to Emission Levels (Mt) in 2015 | Contribution Ratios of Power Generation and Emissions to Total Thermal Power Plants |

|---|---|---|

| Mai-Liao Power Plant (Formosa Plastics) | 13.731:12.05 | 8% and 10.82% |

| He-Ping Power Plant (Taiwan Cement Company) | 9.3375:7.693 | 5.44% and 7.15% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chou, K.-T.; Liou, H.-M. Carbon Tax in Taiwan: Path Dependence and the High-Carbon Regime. Energies 2023, 16, 513. https://doi.org/10.3390/en16010513

Chou K-T, Liou H-M. Carbon Tax in Taiwan: Path Dependence and the High-Carbon Regime. Energies. 2023; 16(1):513. https://doi.org/10.3390/en16010513

Chicago/Turabian StyleChou, Kuei-Tien, and Hwa-Meei Liou. 2023. "Carbon Tax in Taiwan: Path Dependence and the High-Carbon Regime" Energies 16, no. 1: 513. https://doi.org/10.3390/en16010513

APA StyleChou, K.-T., & Liou, H.-M. (2023). Carbon Tax in Taiwan: Path Dependence and the High-Carbon Regime. Energies, 16(1), 513. https://doi.org/10.3390/en16010513