Ammonia and Biogas from Anaerobic and Sewage Digestion for Novel Heat, Power and Transport Applications—A Techno-Economic and GHG Emissions Study for the United Kingdom

,

,

Abstract

:1. Introduction

2. Materials and Methods

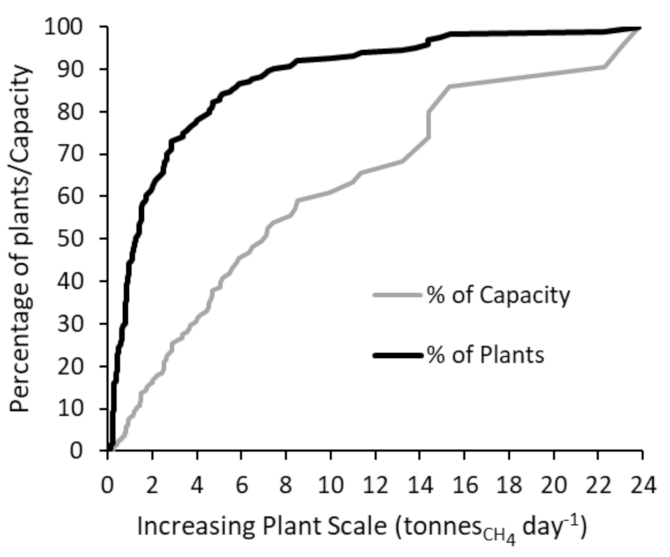

2.1. Economic Analysis with Scale

2.2. Interpretation for Anaerobic Digestion Sites

2.3. CAPEX

2.3.1. Overall

2.3.2. H2 Transport Fuel: Scenario 1

2.3.3. H2 Grid Injection: Scenario 2

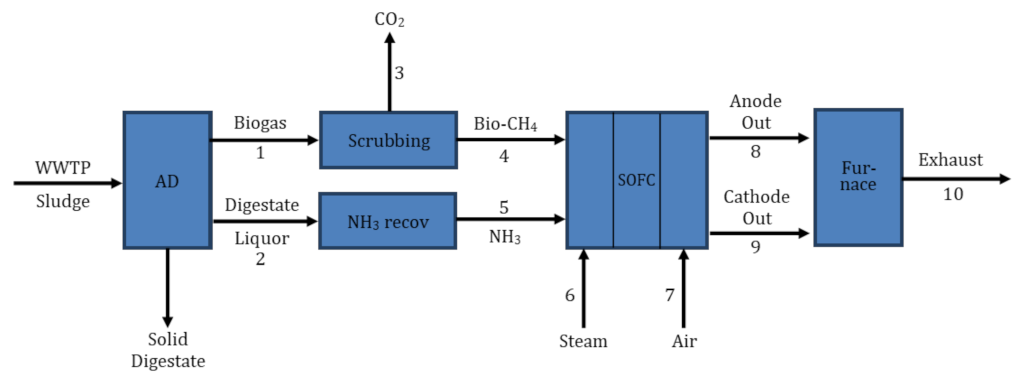

2.3.4. SOFC: Scenario 3

2.4. OPEX

2.4.1. Overall

2.4.2. H2 Transport Fuel: Scenario 1

2.4.3. H2 Grid Injection: Scenario 2

2.5. Income Streams

2.5.1. H2 Transport Fuel: Scenario 1

2.5.2. H2 Grid Injection: Scenario 2

2.5.3. SOFC: Scenario 3

2.6. Greenhouse Gas Emission Analysis

3. Results

3.1. H2 Production Overview

3.2. Scenario 1: H2 for Transport

3.3. Scenario 2: H2 for Grid Injection

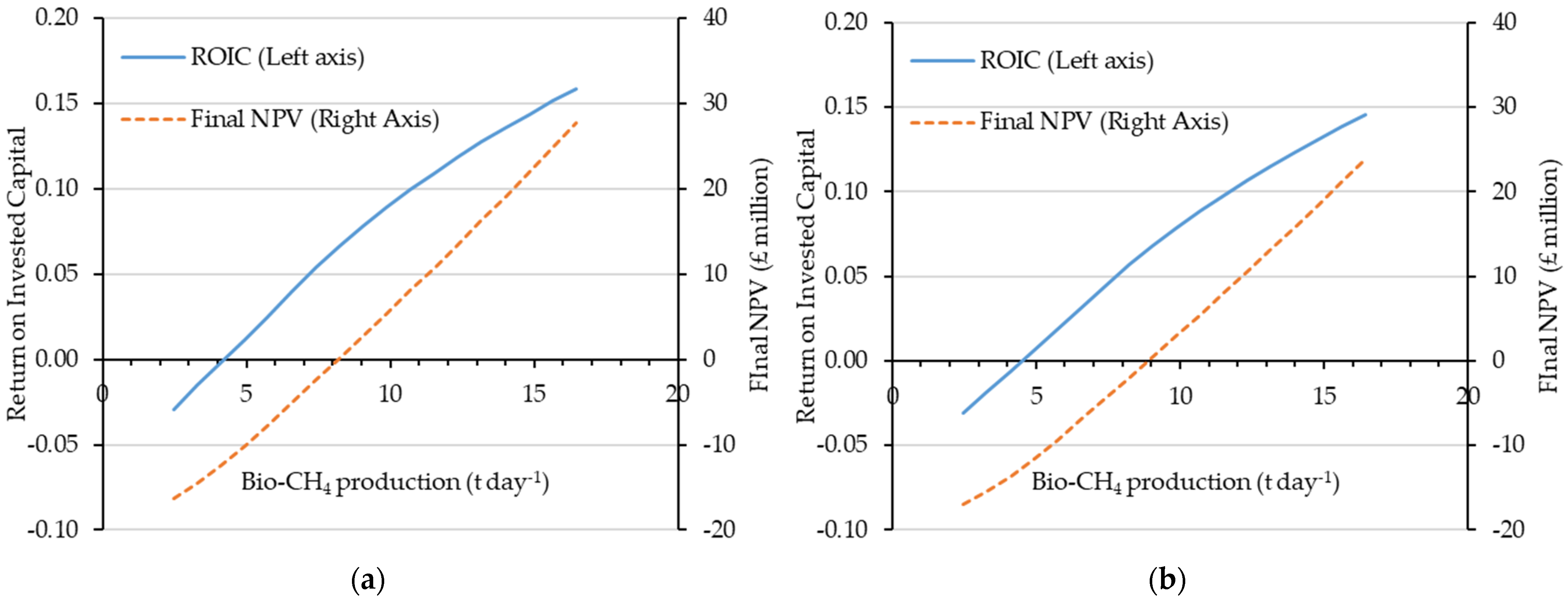

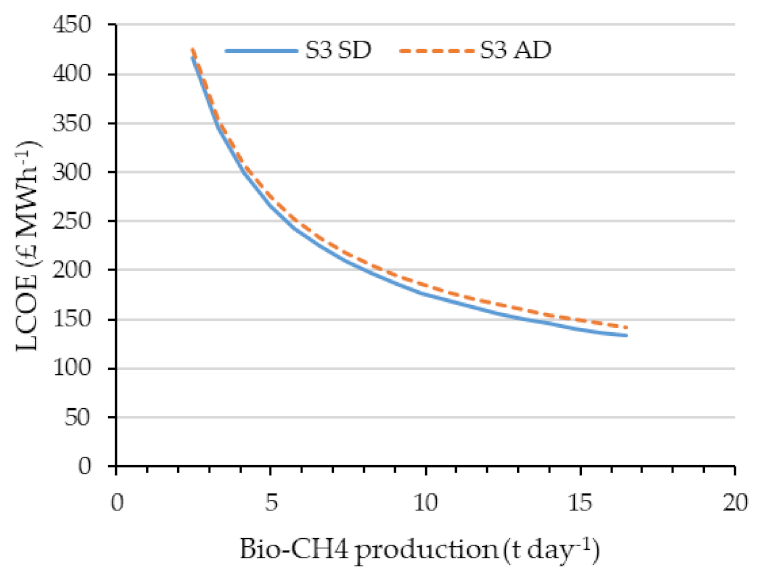

3.4. Scenario 3: SOFC Operation

3.5. Direct Scenario Comparison

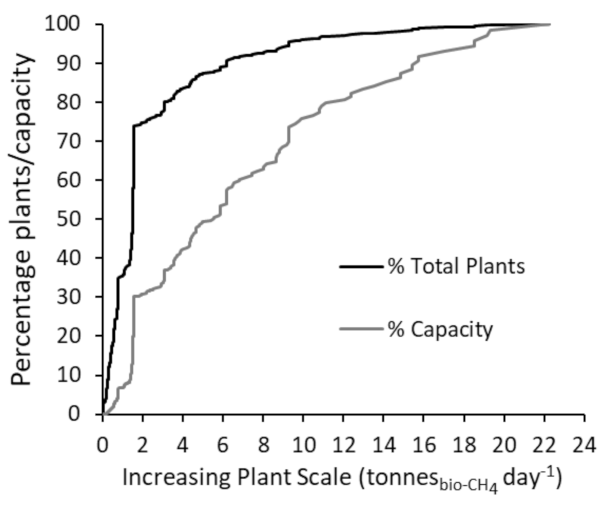

3.6. Applicability to the Current UK Landscape

3.7. Greenhouse Gas Emission Analysis

4. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Department for Business Energy and Industrial Strategy (BEIS). Digest of United Kingdom Energy Statistics: Capacity of, and Electricity Generated from, Renewable Sources. Available online: https://www.gov.uk/government/statistics/digest-of-uk-energy-statistics-dukes-2020 (accessed on 24 May 2021).

- Department of Business Energy & Industrial Strategy. Renewable Sources Used to Generate Electricity and Heat; Electricity Generated from Renewable Sources 1990 to 2019. Available online: https://www.gov.uk/government/statistics/renewable-sources-of-energy-chapter-6-digest-of-united-kingdom-energy-statistics-dukes#full-publication-update-history (accessed on 24 May 2020).

- UN Climate Change Conference COP26: The Glasgow Climate Pact. Available online: https://ukcop26.org/wp-content/uploads/2021/11/COP26-Presidency-Outcomes-The-Climate-Pact.pdf (accessed on 9 January 2022).

- NNFCC. Anaerobic Digestion Deployment in the United Kingdom: Sixth Annual Report. Available online: https://www.nnfcc.co.uk/publications/report-anaerobic-digestion-deployment-in-the-uk (accessed on 24 May 2020).

- Grasham, O.; Dupont, V.; Camargo-Valero, M.A.; García-Gutiérrez, P.; Cockerill, T. Combined ammonia recovery and solid oxide fuel cell use at wastewater treatment plants for energy and greenhouse gas emission improvements. Appl. Energy 2019, 240, 698–708. [Google Scholar] [CrossRef]

- Grasham, O.; Dupont, V.; Cockerill, T.; Camargo-Valero, M.A.; Twigg, M.V. Hydrogen: Via reforming aqueous ammonia and biomethane co-products of wastewater treatment: Environmental and economic sustainability. Sustain. Energy Fuels 2020, 4, 5835–5850. [Google Scholar] [CrossRef]

- Babson, D.M.; Bellman, K.; Prakash, S.; Fennell, D.E. Anaerobic digestion for methane generation and ammonia reforming for hydrogen production: A thermodynamic energy balance of a model system to demonstrate net energy feasibility. Biomass Bioenergy 2013, 56, 493–505. [Google Scholar] [CrossRef]

- Xu, L.; Dong, F.; Zhuang, H.; He, W.; Ni, M.; Feng, S.P.; Lee, P.H. Energy upcycle in anaerobic treatment: Ammonium, methane, and carbon dioxide reformation through a hybrid electrodeionization–solid oxide fuel cell system. Energy Convers. Manag. 2017, 140, 157–166. [Google Scholar] [CrossRef]

- Gherghel, A.; Teodosiu, C.; De Gisi, S. A review on wastewater sludge valorisation and its challenges in the context of circular economy. J. Clean. Prod. 2019, 228, 244–263. [Google Scholar] [CrossRef]

- Koop, S.H.A.; van Leeuwen, C.J. The challenges of water, waste and climate change in cities. Environ. Dev. Sustain. 2017, 19, 385–418. [Google Scholar] [CrossRef] [Green Version]

- Northumbrian Water Northumbrian Water Secure Funding for Project to Turn Ammonia into Fuel. Available online: https://www.nwg.co.uk/news-and-media/news-releases/northumbrian-water-secure-funding-for-project-to-turn-ammonia-into-fuel/ (accessed on 9 January 2022).

- Massara, T.M.; Malamis, S.; Guisasola, A.; Baeza, J.A.; Noutsopoulos, C.; Katsou, E. A review on nitrous oxide (N2O) emissions during biological nutrient removal from municipal wastewater and sludge reject water. Sci. Total Environ. 2017, 596–597, 106–123. [Google Scholar] [CrossRef] [PubMed]

- International Energy Agency (IEA). Net Zero by 2050—A Roadmap for the Global Energy Sector. Available online: https://www.iea.org/reports/net-zero-by-2050 (accessed on 24 May 2020).

- Northern Gas Networks. H21 Leeds City Gate. Available online: https://h21.green/projects/h21-leeds-city-gate/ (accessed on 24 May 2018).

- HyDeploy. About HyDeploy. Available online: https://hydeploy.co.uk/about/ (accessed on 24 May 2018).

- International Energy Agency (IEA). The Future of Hydrogen. Available online: http://www.technologyreview.com/news/425492/the-future-of-hydrogen-cars/ (accessed on 24 May 2020).

- US Department of Energy; Office of Energy Efficiency and Renewable Energy; Fuel Cell Technologies Office. 2017 H2@ Scale Workshop Report. Available online: https://www.energy.gov/eere/fuelcells/downloads/2017-h2-scale-workshop (accessed on 24 May 2020).

- Watson, S.D.; Lomas, K.J.; Buswell, R.A. Decarbonising domestic heating: What is the peak GB demand? Energy Policy 2019, 126, 533–544. [Google Scholar] [CrossRef]

- Quarton, C.J.; Samsatli, S. Should we inject hydrogen into gas grids? Practicalities and whole-system value chain optimisation. Appl. Energy 2020, 275, 115172. [Google Scholar] [CrossRef]

- Muthukumar, M.; Rengarajan, N.; Velliyangiri, B.; Omprakas, M.A.; Rohit, C.B.; Raja, U.K. The development of fuel cell electric vehicles—A review. Mater. Today Proc. 2021, 45, 1181–1187. [Google Scholar] [CrossRef]

- Perna, A.; Minutillo, M.; Micco, S.D.; Jannelli, E. Design and Costs Analysis of Hydrogen Refuelling Stations Based on Different Hydrogen Sources and Plant Configurations. Energies 2022, 15, 541. [Google Scholar] [CrossRef]

- IRENA Hydrogen: A Renewable Energy Perspective. Available online: https://irena.org/publications/2019/Sep/Hydrogen-A-renewable-energy-perspective (accessed on 24 May 2020).

- D’Adamo, I.; Falcone, P.M.; Gastaldi, M.; Morone, P. RES-T trajectories and an integrated SWOT-AHP analysis for biomethane. Policy implications to support a green revolution in European transport. Energy Policy 2020, 138, 111220. [Google Scholar] [CrossRef]

- Harvey, L.D.D. Clarifications of and improvements to the equations used to calculate the levelized cost of electricity (LCOE), and comments on the weighted average cost of capital (WACC). Energy 2020, 207, 118340. [Google Scholar] [CrossRef]

- OFWAT. The Cost of Capital for the Water Sector at PR19. Available online: https://www.ofwat.gov.uk/publication/europe-economics-the-cost-of-capital-for-the-water-sector-at-pr19/ (accessed on 9 January 2022).

- Tribe, M.A. Scale Economies and the “0.6 Rule”. Eng. Costs Prod. Econ. 1986, 10, 271–278. [Google Scholar] [CrossRef]

- Investopedia. Return on Invested Capital (ROIC) Definition. Available online: https://www.investopedia.com/terms/r/returnoninvestmentcapital.asp (accessed on 9 January 2022).

- Mauboussin, M.J.; Callahan, D. Calculating Return on Invested Capital. Glob. Financ. Strateg. 2014, 23, 113. [Google Scholar]

- Rubert, T.; Road, G.; Ab, A.; Carlo, M. Levelised cost of energy—A theoretical justification and critical assessment. Energy Policy 2019, 124, 169–179. [Google Scholar] [CrossRef]

- Garrido, J.M.; Fdz-Polanco, M.; Fdz-Polanco, F. Working with energy and mass balances: A conceptual framework to understand the limits of municipal wastewater treatment. Water Sci. Technol. 2013, 67, 2294. [Google Scholar] [CrossRef]

- Mulder, A. The quest for sustainable nitrogen removal technologies. Water Sci. Technol. 2003, 48, 67–75. [Google Scholar] [CrossRef] [Green Version]

- Aspen Plus Economic Analyzer Aspen Technology; John Wiley & Sons: Hoboken, NJ, USA, 2017.

- Peters, M.S.; Timmerhaus, K.D.; West, R.E. Heat-Transfer Equipment—Design and Costs. In Plant Design and Economics for Chemical Engineers; McGraw-Hill: New York, NY, USA, 2004; pp. 642–754. ISBN 0071240446. [Google Scholar]

- Bank of England. Inflation Calculator. Available online: https://www.bankofengland.co.uk/monetary-policy/inflation/inflation-calculator?number.Sections%5B0%5D.Fields%5B0%5D.Value=150000&start-year=736.5&end-year=1075 (accessed on 11 January 2019).

- Barbera, E.; Menegon, S.; Banzato, D.; D’Alpaos, C.; Bertucco, A. From biogas to biomethane: A process simulation-based techno-economic comparison of different upgrading technologies in the Italian context. Renew. Energy 2018, 135, 663–673. [Google Scholar] [CrossRef]

- Penev, M.; Saur, G.; Hunter, C.; Zuboy, J. H2A Hydrogen Production Model: Version 3. 2018 User Guide. Available online: https://www.nrel.gov/hydrogen/h2a-production-archive.html (accessed on 24 May 2020).

- Kaiwen, L.; Bin, Y.; Tao, Z. Economic analysis of hydrogen production from steam reforming process: A literature review. Energy Sources Part B Econ. Plan. Policy 2018, 13, 109–115. [Google Scholar] [CrossRef]

- Bright, A.; Bulson, H.; Henderson, A.; Sharpe, N.; Dorstewitz, H.; Pickering, J. An Introduction to the Production of Biomethane Gas and Injection to the National Grid. Available online: https://silo.tips/download/an-introduction-to-the-production-of-biomethane-gas-and-injection-to-the-nationa (accessed on 9 January 2022).

- Department of Energy & Climate Change. Biomethane into the Gas Network: A Guide for Producers. Available online: https://webarchive.nationalarchives.gov.uk/ukgwa/20121217150421/http:/decc.gov.uk/assets/decc/whatwedo/ukenergysupply/energymarkets/gas_markets/nonconventional/1_20091229125543_e_@@_biomethaneguidance.pdf (accessed on 9 January 2022).

- MosayebNezhad, M.; Mehr, A.S.; Gandiglio, M.; Lanzini, A.; Santarelli, M. Techno-economic assessment of biogas-fed CHP hybrid systems in a real wastewater treatment plant. Appl. Therm. Eng. 2018, 129, 1263–1280. [Google Scholar] [CrossRef]

- Batelle Memorial Institute. Manufacturing Cost Analysis of 100 and 250 kW Fuel Cell Systems for Primary Power and Combined Heat and Power Applications; U.S. Department of Energy: Columbus, OH, USA, 2017.

- Turton, R.; Bailie, R.C.; Whiting, W.B.; Shaeiwitz, J.A. Estimation of Manufacturing Costs. In Analysis, Synthesis, and Design of Chemical Processes; Turton, R., Bailie, R.C., Whiting, W.B., Shaeiwitz, J.A., Eds.; Prentice Hall: Upper Saddle River, NJ, USA, 2008; ISBN 9780135129661. [Google Scholar]

- Glass Door Salary: Process Engineer. Available online: https://www.glassdoor.co.uk/Salaries/process-engineer-salary-SRCH_KO016.htm (accessed on 17 November 2018).

- Office for National Statistics (ONS). Wages and Salaries Annual Growth Rate%. Available online: https://www.ons.gov.uk/economy/grossdomesticproductgdp/timeseries/kgq2/qna (accessed on 27 November 2018).

- Rotunno, P.; Lanzini, A.; Leone, P. Energy and economic analysis of a water scrubbing based biogas upgrading process for biomethane injection into the gas grid or use as transportation fuel. Renew. Energy 2017, 102, 417–432. [Google Scholar] [CrossRef]

- Department of Business Energy & Industrial Strategy. Gas and Electricity Prices in the Non-Domestic Sector. Available online: https://www.gov.uk/government/statistical-data-sets/gas-and-electricity-prices-in-the-non-domestic-sector (accessed on 8 March 2019).

- Galli, F.; Lai, J.J.; De Tommaso, J.; Pauletto, G.; Patience, G.S. Gas to Liquids Techno-Economics of Associated Natural Gas, Bio Gas, and Landfill Gas. Processes 2021, 9, 1568. [Google Scholar] [CrossRef]

- Reuter, B.; Faltenbacher, M.; Schuller, O.; Whitehouse, N.; Whitehouse, S. New Bus ReFuelling for European Hydrogen Bus Depots: High-Level Techno-Economic Project Summary Report. Available online: http://newbusfuel.eu/wp-content/uploads/2017/03/NewBusFuel_D4.2_High-level-techno-economic-summary-report_final.pdf (accessed on 9 January 2022).

- The United Kingdom Department of Transport. Renewable Transport Fuel Obligation Guidance Part One Process Guidance Moving Britain Ahead. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/694277/rtfo-guidance-part-1-process-guidance-year-11.pdf (accessed on 24 May 2020).

- Ofgem. Non-Domestic RHI Tariff Table (Q3 2020/21). Available online: https://www.ofgem.gov.uk/publications/non-domestic-rhi-tariff-table (accessed on 24 May 2021).

- Ofgem. State of the Energy Market 2019. Available online: https://www.ofgem.gov.uk/publications-and-updates/state-energy-market-2019 (accessed on 24 May 2021).

- Ofgem Green Gas Certification Scheme (GGCS) Response to Ofgem’s Default Tariff Cap: Statutory Consultation. Available online: https://www.ofgem.gov.uk/sites/default/files/docs/2018/10/green_gas_certification_scheme_-_response_0.pdf (accessed on 24 May 2020).

- Department for Business Energy and Industrial Strategy (BEIS). CFD Auction Allocation Round One. Available online: https://www.gov.uk/government/publications/contracts-for-difference-cfd-allocation-round-one-outcome (accessed on 24 May 2018).

- Department for Business, E.& I.S. 2020 Government Greenhouse Gas Conversion Factors for Company Reporting Methodology Paper for Conversion Factors; Stationary Office: London, UK, 2020.

- Willmann, V. Aberdeen Hydrogen Bus Project. Available online: http://www.zemo.org.uk/assets/presentations/7 (accessed on 24 May 2020).

- Andrews, J.; Chambers, B.; Davey, A.; Galetti, S.; Hobson, J.; Hunt, D.; Thorman, R.; Walkerm, I. Carbon Accounting in the Water Industry; Non-CO2 Emissions; UKWIR: London, UK, 2009. [Google Scholar]

- Post, U. Parliamentary Office of Science and Technology Carbon Footprint of Heat Generation. Carbon Footpr. Heat Gener. 2016, 523, 16. [Google Scholar]

- Aspen Plus Aspen Technology; John Wiley & Sons: Hoboken, NJ, USA, 2017.

- National Grid Annual Report and Accounts 2018/19. Available online: https://www.nationalgrid.com/document/124642/download (accessed on 24 May 2020).

- Dodds, P.E.; Demoullin, S. Conversion of the UK gas system to transport hydrogen. Int. J. Hydrogen Energy 2013, 38, 7189–7200. [Google Scholar] [CrossRef] [Green Version]

- Quarton, C.J.; Samsatli, S. Power-to-gas for injection into the gas grid: What can we learn from real-life projects, economic assessments and systems modelling? Renew. Sustain. Energy Rev. 2018, 98, 302–316. [Google Scholar] [CrossRef]

- National Grid Climate Change Adaptation: Second Round Response. Available online: https://www.gov.uk/government/publications/climate-adaptation-reporting-second-round-national-grid (accessed on 24 May 2020).

- Cambridge Economic Policy Associates Ltd. 10 Year Review of the Iron Mains Replacement Programme. Available online: https://www.hse.gov.uk/research/rrhtm/rr888.htm (accessed on 24 May 2020).

- UK Houses of Parliament. Decarbonising the Gas Network, Postnote. Available online: https://researchbriefings.files.parliament.uk/documents/POST-PN-0565/POST-PN-0565.pdf (accessed on 24 May 2020).

- Department for Business Energy and Industrial Strategy (BEIS). Electricity Generation Cost Report 2020. Available online: https://www.gov.uk/government/publications/beis-electricity-generation-costs-2020 (accessed on 9 March 2021).

- NNFCC Anaerobic Digestion Deployment in the UK: Seventh Annual Report. Available online: https://www.nnfcc.co.uk/publications/report-anaerobic-digestion-deployment-in-the-uk (accessed on 9 March 2021).

- Anaerobic Digestion and Bioresources Association AD MAP. Available online: https://adbioresources.org/about-ad/ad-map (accessed on 7 December 2020).

- Department for Business Energy and Industrial Strategy (BEIS). Renewable Electricity Capacity and Generation. Available online: https://www.gov.uk/government/statistics/energy-trends-section-6-renewables (accessed on 24 May 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Function (GBP/kW−1) | |

|---|---|

| Stack CAPEX | 2093 |

| Stack replacement | 434 |

| Clean-up system CAPEX | 450 |

| DC/AC inverter | 220 |

| Source | Factor | Unit | Ref. |

|---|---|---|---|

| Electricity grid | 257.9 | gCO2e/kWh | [40] |

| High quality heat | 210 | gCO2e/kWh | [39] |

| Bus emissions | 1282 | gCO2e/km | [40] |

| H2 bus fuel requirement | 9 | kg H2/100 km | [41] |

| Domestic heat | 180 | gCO2e/kWh | [40] |

| N2O emissions | 0.002 | kg of N (as N2O)/kg N diverted | [42] |

| Aeration abatement | 4.57 | kWh/kg of oxidised N | [15] |

| Stream | H2O | NH3 | CH4 | H2 | CO | CO2 | Temp (°C) | Press (Bar) |

|---|---|---|---|---|---|---|---|---|

| 1 | - | - | 343.1 | - | - | 506.1 | 23 | - |

| 2 | 27,538 | 50.3 | - | - | - | - | 23 | 1 |

| 3 | - | - | - | - | - | 506.1 | 23 | 1 |

| 4 | - | - | 95.2 | - | - | - | 23 | 1 |

| 5 | - | - | 247.9 | - | - | - | 995 | 25 |

| 6 | - | 45.2 | - | - | - | - | 900 | 25 |

| 7 | 853.5 | - | - | - | - | - | 900 | 25 |

| 8 | 523.2 | 0.3 | 5.2 | 105.9 | 317.0 | 167.5 | 1000 | 22.5 |

| 9 | 328.5 | 0.3 | 5.2 | 127.7 | 14.4 | 643.1 | 244 | 13.3 |

| 10 | - | 0.3 | 5.2 | 12.8 | 14.4 | 643.1 | 23 | 1 |

| 11 | - | - | - | 114.9 | - | - | 23 | 1 |

| Stream | H2O | NH3 | CH4 | O2 | N2 | CO | CO2 | H2 | Temp (°C) | Press (Bar) |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | - | - | 343.1 | - | - | - | 506.1 | - | 23 | - |

| 2 | 27,538 | 50.3 | - | - | - | - | - | - | 23 | 1 |

| 3 | - | - | - | - | - | - | 506.1 | - | 23 | 1 |

| 4 | - | - | 343.1 | - | - | - | - | - | 700 | 1.1 |

| 5 | 18.8 | 45.6 | - | - | - | - | 79.1 | - | 700 | 1.1 |

| 6 | 963 | 0.01 | - | - | - | - | - | - | 700 | 1.1 |

| 7 | - | - | - | 5409 | 17,815 | - | - | - | 867 | 1.1 |

| 8 | 1611 | - | - | - | 46.4 | 287.5 | 568.5 | 24.0 | 910 | 1.08 |

| 9 | - | - | - | 4335 | 17,815 | - | - | - | 910 | 1.08 |

| 10 | 1825 | - | - | 3982 | 17,861 | - | 1020 | - | 1075 | 1 |

| SD | Methane Limit (Tonnes day−1) | Number of Plants | Total Methane (Tonnes day−1) | H2 Production (Tonnes day−1) | SOFC Power Generation (MWh day−1) |

|---|---|---|---|---|---|

| S1 | 7.1 | 19 | 249 | 83 | |

| S2 | 17.0 | 3 | 69 | 23 | |

| S3 | 9.2 | 13 | 202 | 0 | 1425 |

| S2b | 11.3 | 11 | 181 | 61 | |

| AD | |||||

| S1 | 8.2 | 42 | 511 | 171 | |

| S2 | 20.0 | 1 | 22 | 7 | |

| S3 | 10.0 | 23 | 338 | 2388 | |

| S2b | 12.5 | 15 | 247 | 83 |

| S1 (g CO2e/kg bio-CH4) | S2 (g CO2e/kg bio-CH4) | S3 (g CO2e/kg bio-CH4) | |||

|---|---|---|---|---|---|

| Net process power | 729 | Net process power | 356 | Net process power | −1821 |

| High quality heat | 600 | High quality heat | 600 | Power Improvement | −698 |

| NH3 Diversion | −391 | NH3 Diversion | −391 | NH3 diversion | −391 |

| Abated bus emissions | −4822 | Abated Domestic Heat | −2009 | ||

| AD power replacement | 1122 | AD power replacement | 1122 | ||

| SD Total | −4275 | −1444 | −2212 | ||

| SD Improvement | −3153 | −321 | −1090 | ||

| AD Total | −3616 | −784 | −1552 | ||

| AD Improvement | −2493 | 339 | −430 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Grasham, O.; Dupont, V.; Cockerill, T.; Camargo-Valero, M.A. Ammonia and Biogas from Anaerobic and Sewage Digestion for Novel Heat, Power and Transport Applications—A Techno-Economic and GHG Emissions Study for the United Kingdom. Energies 2022, 15, 2174. https://doi.org/10.3390/en15062174

Grasham O, Dupont V, Cockerill T, Camargo-Valero MA. Ammonia and Biogas from Anaerobic and Sewage Digestion for Novel Heat, Power and Transport Applications—A Techno-Economic and GHG Emissions Study for the United Kingdom. Energies. 2022; 15(6):2174. https://doi.org/10.3390/en15062174

Chicago/Turabian StyleGrasham, Oliver, Valerie Dupont, Timothy Cockerill, and Miller Alonso Camargo-Valero. 2022. "Ammonia and Biogas from Anaerobic and Sewage Digestion for Novel Heat, Power and Transport Applications—A Techno-Economic and GHG Emissions Study for the United Kingdom" Energies 15, no. 6: 2174. https://doi.org/10.3390/en15062174

APA StyleGrasham, O., Dupont, V., Cockerill, T., & Camargo-Valero, M. A. (2022). Ammonia and Biogas from Anaerobic and Sewage Digestion for Novel Heat, Power and Transport Applications—A Techno-Economic and GHG Emissions Study for the United Kingdom. Energies, 15(6), 2174. https://doi.org/10.3390/en15062174