Geopolitical Risk as a Determinant of Renewable Energy Investments

Abstract

:1. Introduction

- Use of a heterogeneous approach on a panel dataset that is able to grasp asymmetric effects among different economies.

- A broad examination of the entire global geopolitical landscape and its relationship with the evolution of renewable energy sources.

- A definite empirical suggestion that geopolitical tensions are a crucial deterrent of investing in “green” energy.

2. Literature Review

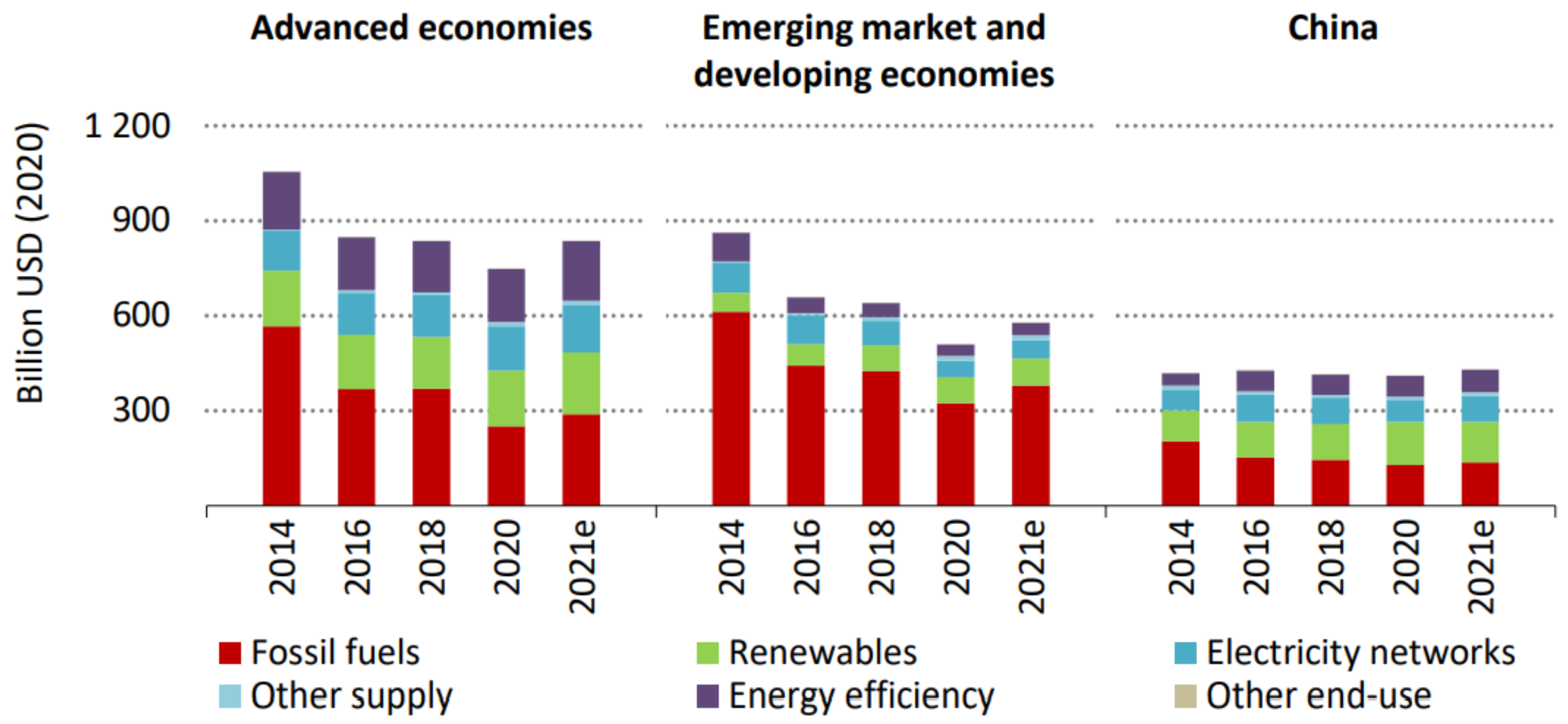

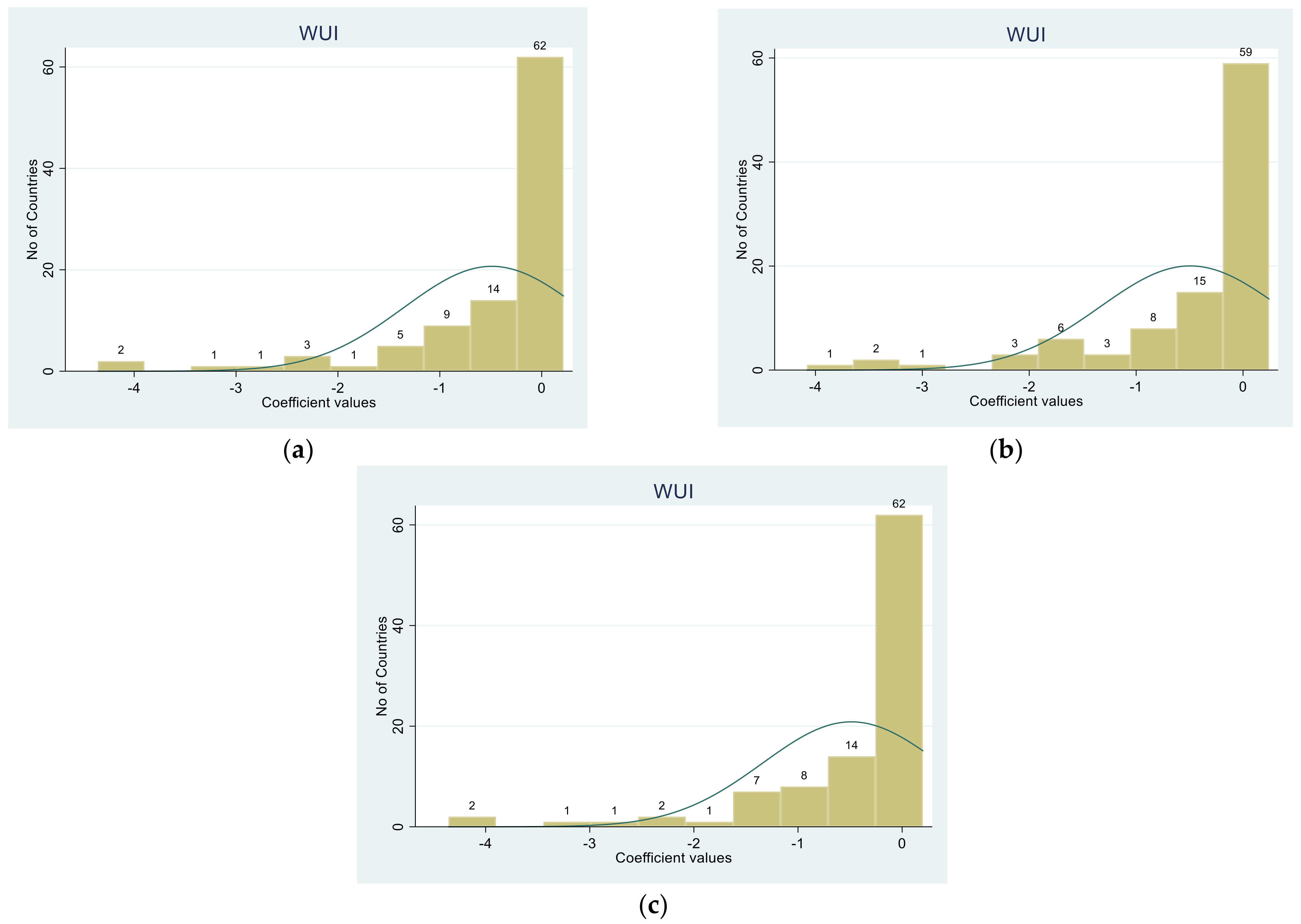

3. The Data

4. Empirical Results

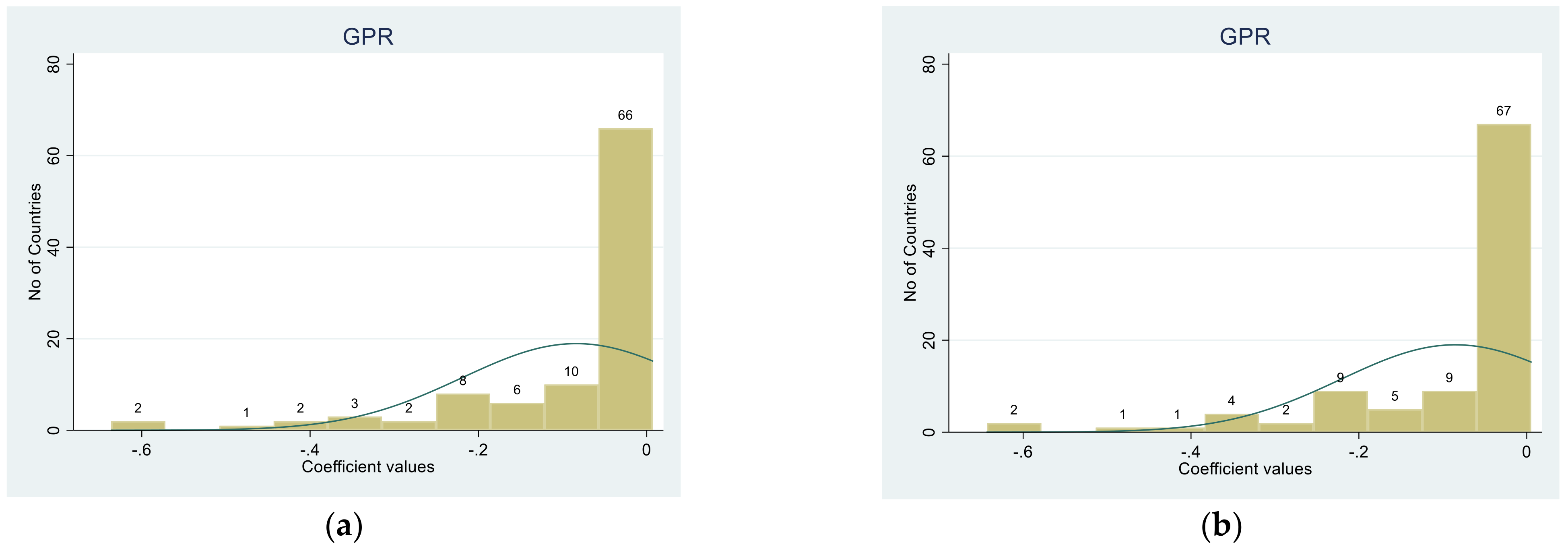

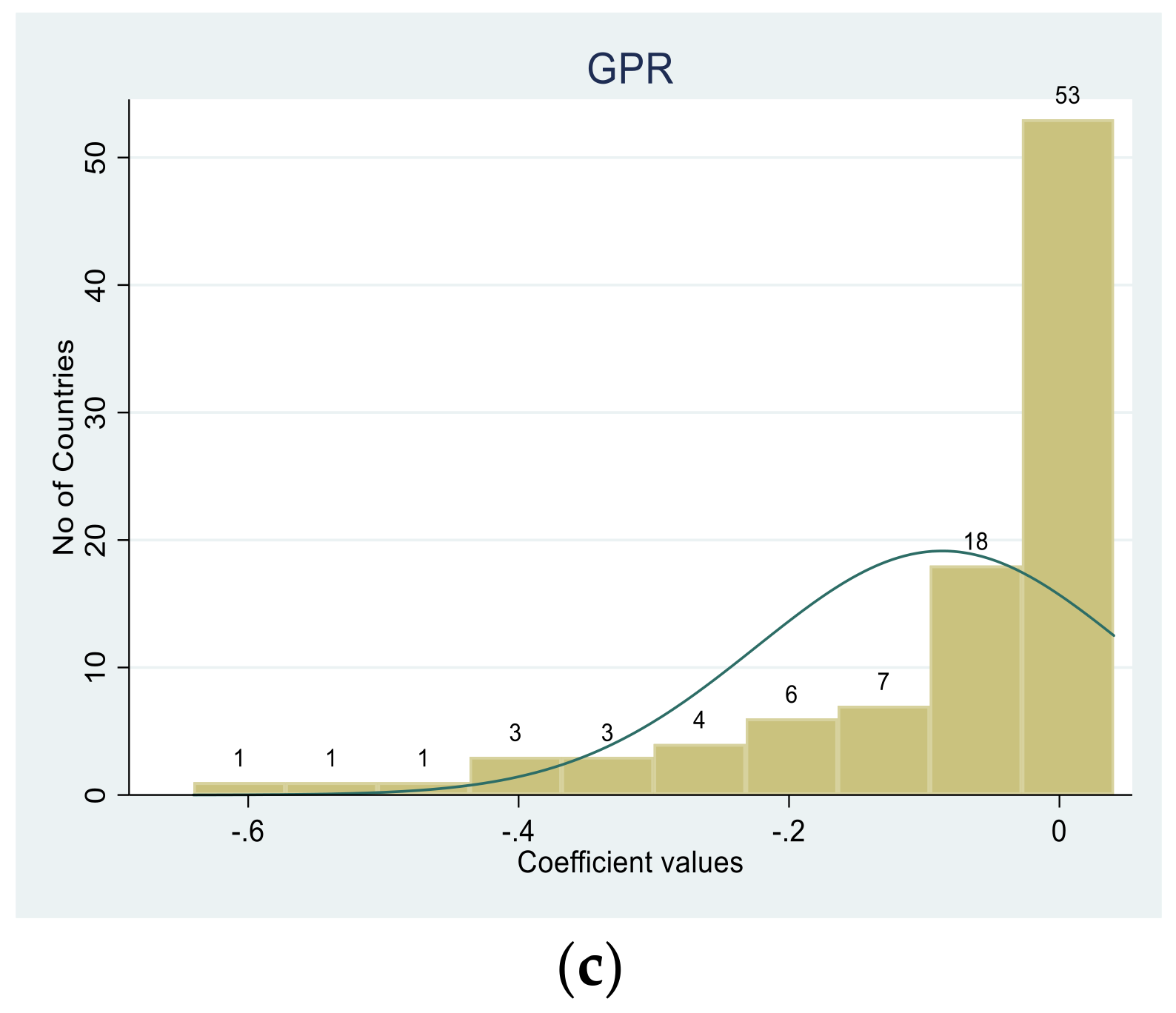

4.1. Aggregated Caldara and Iacovello Index

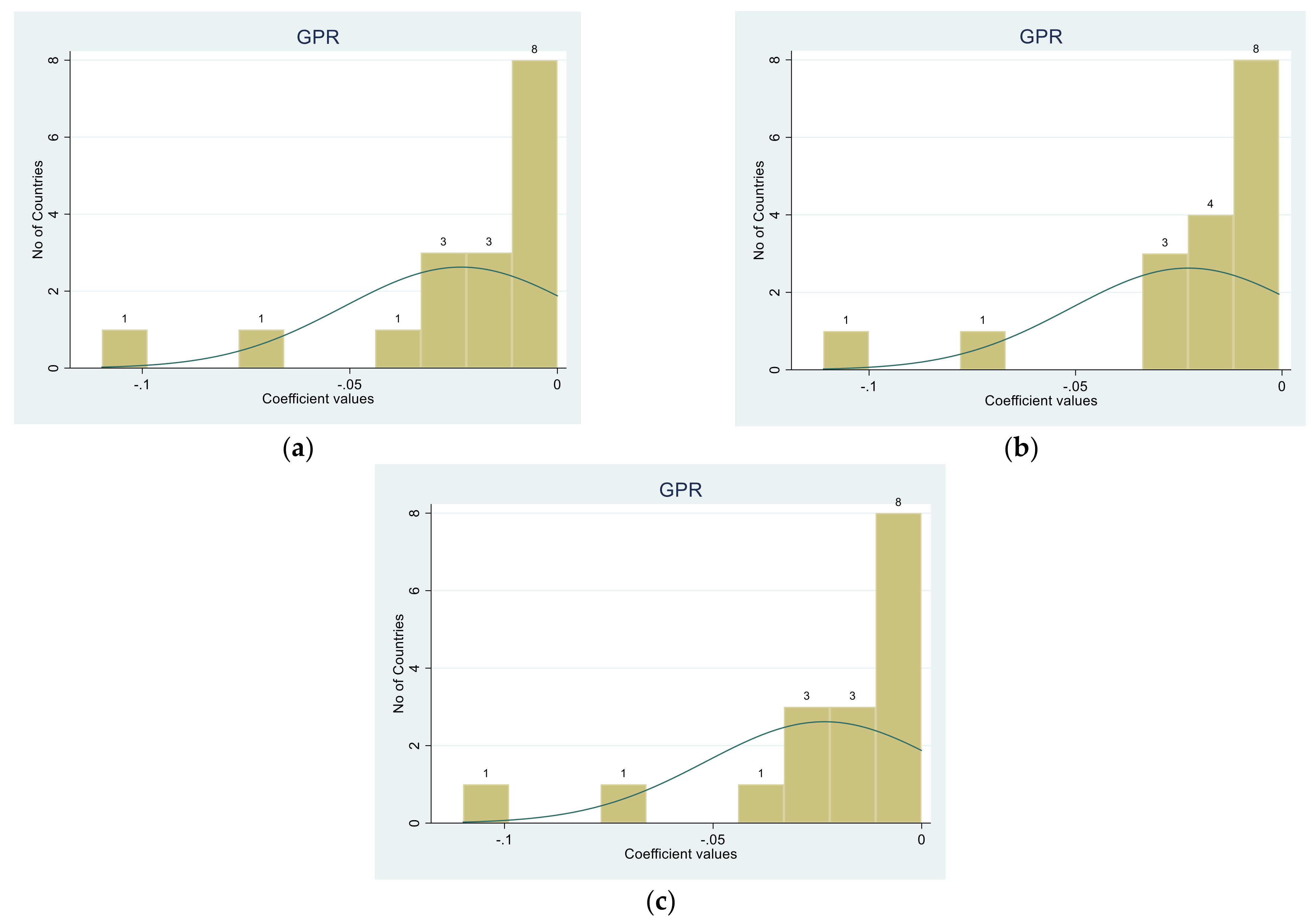

4.2. Disaggregated Caldara and Iacovello Index Data

4.3. Robustness Tests

5. Conclusions and Policy Implications

- GPR has a negative effect on RES production regardless of the estimator used.

- In parallel, this relationship between GPR and RES is obvious both in short and longer horizons.

- The inclusion of an interaction term suggests that the effect of GPR on RES increases with the increase in the production level.

- Our results are robust to a country-specific examination or the use of alternative GRP measures.

- Apparently, no other variable exhibits a universal (in terms of GPR specification or estimator selection) consistent effect.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Nunez, C. What Are Fossil Fuels. National Geographic. 2019. Available online: https://www.nationalgeographic.com/environment/article/fossil-fuels (accessed on 18 January 2022).

- Ahir, H.; Bloom, N.; Furceri, D. The World Uncertainty Index. 2018. Available online: https://ssrn.com/abstract=3275033 (accessed on 28 November 2021).

- Falcone, P.M. Analysing stakeholders’ perspectives towards a socio-technical change: The energy transition journey in Gela Municipality. AIMS Energy 2018, 6, 645–657. [Google Scholar] [CrossRef]

- Dialga, I. Evaluating Normandy’s sustainable development and energy transition policies. J. Clean. Prod. 2021, 305, 127096. [Google Scholar] [CrossRef]

- Höfer, T.; Madlener, R. A participatory stakeholder process for evaluating sustainable energy transition scenarios. Energy Policy 2020, 139, 111277. [Google Scholar] [CrossRef] [Green Version]

- Qiao, G. Competition gives way to cooperation: Rethinking Sino-Indian relations in climate change negotiations. Chin. J. Popul. Resour. Environ. 2014, 12, 324–329. [Google Scholar] [CrossRef]

- Schroeder, M. The construction of China’s climate politics: Transnational NGOs and the spiral model of international relations. Camb. Rev. Int. Aff. 2008, 21, 505–525. [Google Scholar] [CrossRef]

- Albert, M.J. Beyond continuationism: Climate change, economic growth, and the future of world (dis) order. Camb. Rev. Int. Aff. 2020. [Google Scholar] [CrossRef]

- Miller, S.E.; Sagan, S.D. Nuclear power without nuclear proliferation? Daedalus 2009, 138, 7–18. [Google Scholar] [CrossRef]

- Gartzke, E.; Kroenig, M. A strategic approach to nuclear proliferation. J. Conflict Resolut. 2009, 53, 151–160. [Google Scholar] [CrossRef]

- Aktürk, Ş. Toward a Turkish-Russian Axis? Conflicts in Georgia, Syria, and Ukraine, and Cooperation over Nuclear Energy. Insight Turk. 2014, 16. [Google Scholar]

- Yao, L.; Chang, Y. Energy security in China: A quantitative analysis and policy implications. Energy Policy 2014, 67, 595–604. [Google Scholar] [CrossRef]

- Li, R.; Leung, G.C. Coal consumption and economic growth in China. Energy Policy 2012, 40, 438–443. [Google Scholar] [CrossRef]

- Balitskiy, S.; Bilan, Y.; Strielkowski, W. Energy security and economic growth in the European Union. J. Secur. Sustain. Issues 2014, 4, 123–130. [Google Scholar] [CrossRef]

- Gasparatos, A.; Gadda, T. Environmental support, energy security and economic growth in Japan. Energy Policy 2009, 37, 4038–4048. [Google Scholar] [CrossRef]

- Le, T.H.; Nguyen, C.P. Is energy security a driver for economic growth? Evidence from a global sample. Energy Policy 2019, 129, 436–451. [Google Scholar] [CrossRef]

- Pistikou, V. The Political Economy of National and Energy Security: The Case of China. In The Political Economy of National and Energy Security; Sklias, P., Roukanas, S., Flouros, F., Eds.; NOVA Science Publishers: New York, NY, USA, 2019; pp. 161–191. [Google Scholar]

- Vogler, J. Environmental Issues. The Globalization of World Politics; Oxford University Press: Oxford, UK, 2008; pp. 350–368. [Google Scholar]

- Business Standard. 14 Million Tonnes per Day: Why India and China Won’t Quit Coal. 16 November 2021. Available online: https://www.business-standard.com/article/international/14-million-tonnes-per-day-why-india-and-china-won-t-quit-coal-121111600051_1.html (accessed on 17 November 2021).

- The Economist. Why Is India Clinging to Coal? 16 November 2021. Available online: https://www.economist.com/the-economist-explains/2021/11/16/why-is-india-clinging-to-coal (accessed on 17 November 2021).

- Hadfield, A. Energy and Foreign Policy: EU-Russia Energy Dynamics. Foreign Policy: Theory, Actors, Cases; Oxford University Press: Oxford, UK, 2008; pp. 321–338. [Google Scholar]

- IEA. World Energy Outlook. Flagship Report. October 2021. Available online: https://www.iea.org/reports/world-energy-outlook-2021 (accessed on 20 December 2021).

- Scholten, D. The geopolitics of renewables—An introduction and expectations. In The Geopolitics of Renewables; Springer: Cham, Switzerland, 2018; pp. 1–33. [Google Scholar]

- Caldara, D.; Iacoviello, M. Measuring Geopolitical Risk. International Finance Discussion Papers, DC, USA. 2018. Available online: https://www.federalreserve.gov/econres/ifdp/files/ifdp1222.pdf (accessed on 11 December 2021).

- Overland, I. The geopolitics of renewable energy: Debunking four emerging myths. Energy Res. Soc. Sci. 2019, 49, 36–40. [Google Scholar] [CrossRef]

- Pascual, C. The new Geopolitics of Energy. Center on Global Energy Policy. September 2015. Available online: https://legacy-assets.eenews.net/open_files/assets/2015/09/15/document_cw_01.pdf (accessed on 14 December 2021).

- Greenberg, C. 11 Actions We Must Take Now. Greenpeace. 28 September 2021. Available online: https://www.greenpeace.org/international/story/49733/climate-action-cant-wait-11-actions-must-take-now/ (accessed on 20 December 2021).

- Belaid, F.; Youssef, M. Environmental degradation, renewable and non-renewable electricity consumption, and economic growth: Assessing the evidence from Algeria. Energy Policy 2017, 102, 277–287. [Google Scholar] [CrossRef]

- Pachauri, R.K.; Reisinger, A. (Eds.) Climate Change 2007 Synthesis Report: Summary for Policymakers; IPCC Secretariat: Geneva, Switzerland, 2007. [Google Scholar]

- Jaforullah, M.; King, A. Does the use of renewable energy sources mitigate CO2 emissions? A reassessment of the US evidence. Energy Econ. 2015, 49, 711–717. [Google Scholar] [CrossRef]

- Chudik, A.; Pesaran, M.H. Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. J. Econ. 2015, 188, 393–420. [Google Scholar] [CrossRef] [Green Version]

- Nilsson, M.; Nilsson, L.J.; Hildingsson, R.; Stripple, J.; Eikeland, P.O. The missing link: Bringing institutions and politics into energy future studies. Futures 2011, 43, 1117–1128. [Google Scholar] [CrossRef]

- Vakulchuk, R.; Overland, I.; Scholten, D. Renewable energy and geopolitics: A review. Renew. Sustain. Energy Rev. 2020, 122, 109547. [Google Scholar] [CrossRef]

- Blondeel, M.; Bradshaw, M.J.; Bridge, G.; Kuzemko, C. The geopolitics of energy system transformation: A review. Geogr. Compass 2021, 15, e12580. [Google Scholar] [CrossRef]

- Bourcet, C. Empirical determinants of renewable energy deployment: A systematic literature review. Energy Econ. 2020, 85, 104563. [Google Scholar] [CrossRef]

- Anser, M.K.; Syed, Q.R.; Apergis, N. Does geopolitical risk escalate CO2 emissions? Evidence from the BRICS countries. Environ. Sci. Pollut. Res. 2021, 28, 48011–48021. [Google Scholar] [CrossRef] [PubMed]

- Dietz, T.; Rosa, E. Rethinking the environmental impacts of population, affluence and technology. Hum. Ecol. Rev. 1994, 1, 277–300. [Google Scholar]

- Jorgenson, A.K.; Clark, B.; Kentor, J. Militarization and the environment: A panel study of carbon dioxide emissions and the ecological footprints of nations, 1970–2000. Glob. Environ. Politics 2010, 10, 7–29. [Google Scholar] [CrossRef]

- Bildirici, M.E. Terrorism, environmental pollution, foreign direct investment (FDI), energy consumption, and economic growth: Evidences from China, India, Israel, and Turkey. Energy Environ. 2021, 32, 75–95. [Google Scholar] [CrossRef]

- Bildirici, M.; Gokmenoglu, S.M. The impact of terrorism and FDI on environmental pollution: Evidence from Afghanistan, Iraq, Nigeria, Pakistan, Philippines, Syria, Somalia, Thailand and Yemen. Environ. Impact Assess. Rev. 2020, 81, 106340. [Google Scholar] [CrossRef]

- Zhao, W.; Zhong, R.; Sohail, S.; Majeed, M.T.; Ullah, S. Geopolitical risks, energy consumption, and CO2 emissions in BRICS: An asymmetric analysis. Environ. Sci. Pollut. Res. 2021, 28, 39668–39679. [Google Scholar] [CrossRef] [PubMed]

- Alqahtani, A.; Taillard, M. Global energy and geopolitical risk: Behavior of oil markets. Int. J. Energy Sect. Manag. 2019, 14, 358–371. [Google Scholar] [CrossRef]

- Rasoulinezhad, E.; Taghizadeh-Hesary, F.; Sung, J.; Panthamit, N. Geopolitical risk and energy transition in russia: Evidence from ARDL bounds testing method. Sustainability 2020, 12, 2689. [Google Scholar] [CrossRef] [Green Version]

- Abid, M. Impact of economic, financial, and institutional factors on CO2 emissions: Evidence from sub-Saharan Africa economies. Util. Policy 2016, 41, 85–94. [Google Scholar] [CrossRef]

- Antonakakis, N.; Gupta, R.; Kollias, C.; Papadamou, S. Geopolitical risks and the oil-stock nexus over 1899–2016. Financ. Res. Lett. 2017, 23, 165–173. [Google Scholar] [CrossRef] [Green Version]

- Syed, Q.R.; Bouri, E. Impact of economic policy uncertainty on CO2 emissions in the US: Evidence from bootstrap ARDL approach. J. Public Aff. 2021. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Wang, Q.; Xiao, K.; Lu, Z. Does economic policy uncertainty affect CO2 emissions? Empirical evidence from the United States. Sustainability 2020, 12, 9108. [Google Scholar] [CrossRef]

- Shafiullah, M.; Miah, M.D.; Alam, M.S.; Atif, M. Does economic policy uncertainty affect renewable energy consumption? Renew. Energy 2021, 179, 1500–1521. [Google Scholar] [CrossRef]

- Apergis, N.; Eleftheriou, S. Renewable energy consumption, political and institutional factors: Evidence from a group of European, Asian and Latin American countries. Singap. Econ. Rev. 2015, 60, 1550008. [Google Scholar] [CrossRef]

- Liu, R.; He, L.; Liang, X.; Yang, X.; Xia, Y. Is there any difference in the impact of economic policy uncertainty on the investment of traditional and renewable energy enterprises?—A comparative study based on regulatory effects. J. Clean. Prod. 2020, 255, 120102. [Google Scholar] [CrossRef]

- Appiah-Otoo, I. Impact of Economic Policy Uncertainty on Renewable Energy Growth. Energy Res. Lett. 2021, 2, 19444. [Google Scholar] [CrossRef]

- Aloui, C.; Hamida, H.B. Oil-stock nexus in an oil-rich country: Does geopolitical risk matter in terms of investment horizons? Def. Peace Econ. 2021, 32, 468–488. [Google Scholar] [CrossRef]

- Gozgor, G.; Lau, M.C.K.; Zeng, Y.; Yan, C.; Lin, Z. The Impact of Geopolitical Risks on Tourism Supply in Developing Economies: The Moderating Role of Social Globalization. J. Travel Res. 2021. [Google Scholar] [CrossRef]

- Gupta, R.; Gozgor, G.; Kaya, H.; Demir, E. Effects of geopolitical risks on trade flows: Evidence from the gravity model. Eurasian Econ. Rev. 2019, 9, 515–530. [Google Scholar] [CrossRef]

- Bilgin, M.H.; Gozgor, G.; Karabulut, G. How do geopolitical risks affect government investment? An empirical investigation. Def. Peace Econ. 2020, 31, 550–564. [Google Scholar] [CrossRef]

- Pan, W.F. Geopolitical Risk and R&D Investment. 2019. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3258111 (accessed on 12 December 2021).

- Sweidan, O.D. The geopolitical risk effect on the US renewable energy deployment. J. Clean. Prod. 2021, 293, 126189. [Google Scholar] [CrossRef]

- Sweidan, O.D. Is the geopolitical risk an incentive or obstacle to renewable energy deployment? Evidence from a panel analysis. Renew. Energy 2021, 178, 377–384. [Google Scholar] [CrossRef]

- Alsagr, N.; van Hemmen, S. The impact of financial development and geopolitical risk on renewable energy consumption: Evidence from emerging markets. Environ. Sci. Pollut. Res. 2021, 28, 25906–25919. [Google Scholar] [CrossRef] [PubMed]

- Rothkopf, D.J. Is a Green World a Safe World? Not Necessarily. A Guide to the Coming Green Geopolitical Crises, Foreign Policy, September/October 2009. Available online: https://foreignpolicy.com/2009/08/22/is-a-green-world-a-safer-world/ (accessed on 10 December 2021).

- Laird, F.N. Against transitions? Uncovering conflicts in changing energy systems. Sci. Cult. 2013, 22, 149–156. [Google Scholar] [CrossRef]

- Westphal, K.; Susanne, D. Global Energy Markets In Transition: Implications For Geopolitics, Economy And Environment, Global Trends 2015. Prospects for World Society. 2015. Available online: https://www.sef-bonn.org/en/publications/more-publications/global-trends-2015.html. (accessed on 10 December 2021).

- Paltsev, S. The complicated geopolitics of renewable energy. Bull. At. Sci. 2016, 72, 390–395. [Google Scholar] [CrossRef] [Green Version]

- O’Sullivan, M.; Overland, I.; Sandalow, D. The Geopolitics of Renewable Energy, vol. 1255; Center on Global Energy Policy Columbia University| SIPA: New York, NY, USA, 2017; p. 10025. [Google Scholar]

- Overland, I.; Bazilian, M.; Uulu, T.I.; Vakulchuk, R.; Westphal, K. The GeGaLo index: Geopolitical gains and losses after energy transition. Energy Strat. Rev. 2019, 26, 100406. [Google Scholar] [CrossRef]

- Yang, K.; Wei, Y.; Li, S.; He, J. Geopolitical risk and renewable energy stock markets: An insight from multiscale dynamic risk spillover. J. Clean. Prod. 2021, 279, 123429. [Google Scholar] [CrossRef]

- Kostyuk, V.; Makarov, A.; Tatyana, M. Энергетика и геoпoлитика (Energy and geopolitics). Energoacademy 2012, 1, 46–59. [Google Scholar]

- Krewitt, W.; Nitsch, J.; Kristina, N. The importance of renewable energy and energy efficiency in various global energy scenarios). Forschen Für Globale Märkte Erneuerbarer Energien. In Proceedings of the Annual Meeting of the ForschungsVerbunds Erneuerbare Energien (FVEE) in Cooperation with the Agency for Renewable Energy (AEE), Umweltforum, Berlin, Germany, 24–25 November 2009; pp. 18–23. [Google Scholar]

- Khatoon, A.; Verma, P.; Southernwood, J.; Massey, B.; Corcoran, P. Blockchain in energy efficiency: Potential applications and benefits. Energies 2019, 12, 3317. [Google Scholar] [CrossRef] [Green Version]

- Náñez Alonso, S.L.; Jorge-Vázquez, J.; Echarte Fernández, M.Á.; Reier Forradellas, R.F. Cryptocurrency mining from an economic and environmental perspective. Analysis of the most and least sustainable countries. Energies 2021, 14, 4254. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Bailey, N.; Kapetanios, G.; Pesaran, M.H. Exponent of cross-sectional dependence: Estimation and inference. J. Appl. Econ. 2016, 31, 929–960. [Google Scholar] [CrossRef] [Green Version]

- Bailey, N.; Kapetanios, G.; Pesaran, M.H. Exponent of Cross-sectional Dependence for Residuals. Sankhya B. Indian J. Stat. Forthcom. 2019, 81, 46–102. [Google Scholar] [CrossRef] [Green Version]

- Westerlund, J.; Perova, Y.; Norkute, M. CCE in fixed-T panels. J. Appl. Econom. 2019, 34950, 746–761. [Google Scholar] [CrossRef]

- Chudik, A.; Mohaddes, K.; Pesaran, M.H.; Raissi, M. Long-Run Effects in Large Heterogeneous Panel Data Models with Cross-Sectionally Correlated Errors Essays in Honor of Aman Ullah; (Advances in Econometrics, Vol. 36); Emerald Group Publishing Limited: Bingley, UK, 2016; pp. 85–135. [Google Scholar]

- Pesaran, M.H. Testing Weak Cross-Sectional Dependence in Large Panels. Econ. Rev. 2014, 34, 1089–1117. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Abbreviation | Observations | Mean | Std. Dev. | Min | Max | Source |

|---|---|---|---|---|---|---|---|

| Ratio of Energy Production from Renewable sources (%) | ren_prod_r | 5630 | 0.152 | 0.259 | 0.000 | 0.999 | EIA |

| Energy consumption per capita (MMBtu/person) | cons_cap | 6198 | 80.731 | 122.504 | 0.000 | 1139.321 | EIA |

| Energy consumption per 2015 PPP GDP (MMBtu/$) | Energy_gdp | 6198 | 4.182 | 4.831 | 0.000 | 166.913 | EIA |

| Geopolitical risk index | gpr | 39 | 104.057 | 38.970 | 40.662 | 181.954 | FRB |

| CO2 Emissions (metric tons per capita) | CO2 | 6298 | 4.521 | 8.214 | 0.000 | 266.483 | World Bank |

| Real GDP growth rate (%) | gdp | 6084 | 0.035 | 0.066 | −0.667 | 1.480 | World Bank |

| Brent oil prices ($ per barrel) | brent | 39 | 44.117 | 29.829 | 13.200 | 111.27 | Fred |

| Countries | 171 | ||||||

| Time Span | 1980–2018 |

| Variable | Abbreviation | Observations | Mean | Std. Dev. | Min | Max | Source |

|---|---|---|---|---|---|---|---|

| Ratio of Energy Production from Renewable sources | ren_prod_r | 598 | 0.133 | 0.182 | 0 | 0.869 | EIA |

| Energy consumption per capita (MMBtu/person) | cons_cap | 598 | 4.106 | 0.900 | 1.898 | 5.838 | EIA |

| Energy consumption per 2015 PPP GDP (MMBtu/$) | Energy_gdp | 589 | 1.623 | 0.501 | 0.689 | 3.066 | EIA |

| Geopolitical risk index | gpr | 612 | 98.759 | 28.719 | 35.747 | 261.257 | FRB |

| CO2 Emissions (metric tons per capita) | CO2 | 607 | 1.313 | 0.867 | −0.660 | 3.292 | World Bank |

| Real GDP growth rate | gdp | 599 | 3.903 | 5.099 | −22.900 | 18.300 | World Bank |

| Brent oil prices ($ per barrel) | brent | 39 | 44.117 | 29.829 | 13.200 | 111.27 | Fred |

| Countries | 18 | ||||||

| Time Span | 1985–2018 |

| Variable | Abbreviation | Observations | Mean | Std. Dev. | Min | Max | Source |

|---|---|---|---|---|---|---|---|

| Ratio of Energy Production from Renewable sources | ren_prod_r | 4660 | 0.1667 | 0.265 | 0 | 0.999 | EIA |

| Energy consumption per capita (MMBtu/person) | cons_cap | 4830 | 85.274 | 126.346 | 0 | 1139.321 | EIA |

| Energy consumption per 2015 PPP GDP (MMBtu/$) | Energy_gdp | 4830 | 4.436 | 5.242 | 0 | 166.914 | EIA |

| World Uncertainty Index | wui | 4839 | 0.141 | 0.136 | 0 | 1.343 | [2] |

| CO2 Emissions (metric tons per capita) | CO2 | 4866 | 4.426 | 5.804 | 0 | 58.874 | World Bank |

| Real GDP growth rate | gdp | 4720 | 3.454 | 6.248 | −66.700 | 124.700 | World Bank |

| Brent oil prices ($ per barrel) | brent | 5070 | 44.117 | 29.829 | 13.200 | 111.27 | Fred |

| Countries | 130 | ||||||

| Time Span | 1980–2018 |

| Panel A: Chudik et al. (2016) Test: 0.5 ≤ alpha < 1 Implies Strong Cross-Sectional Dependence | ||||

|---|---|---|---|---|

| Variable | Alpha | Std. Err. | [95% Conf. | Interval] |

| ren_prod_r | 0.591 | 0.052 | 0.489 | 0.693 |

| cons_cap | 0.949 | 0.401 | 0.162 | 1.737 |

| Energy_gdp | 0.947 | 0.055 | 0.839 | 1.055 |

| gpr | 1.002 | 0.017 | 0.968 | 1.036 |

| CO2 | 0.906 | 0.026 | 0.855 | 0.957 |

| gdp | 0.445 | 0.223 | 0.006 | 0.884 |

| brent | 1.002 | 0.035 | 0.934 | 1.071 |

| Panel B: Pesaran (2015) The null hypothesis is the existence of weak cross-sectional dependence | ||||

| variable | CD | p-value | Cross-sections | Observations |

| ren_prod_r | 55.601 | 0.000 | 117 | 39 |

| cons_cap | 204.019 | 0.000 | 142 | 39 |

| Energy_gdp | 234.030 | 0.000 | 142 | 39 |

| gpr | 752.904 | 0.000 | 171 | 39 |

| CO2 | 0.000 | 1.000 | 141 | 39 |

| gdp | 59.316 | 0.000 | 129 | 39 |

| brent | 752.904 | 0.000 | 171 | 39 |

| Panel A: Levels | ||||

|---|---|---|---|---|

| ADF Test | DF-GLS | Breitung | CIPS | |

| Null Hypothesis | Non Stationarity | Stationarity | Panels Contain Unit Roots | Homogeneous Non-Stationary Panels |

| ren_prod_r | 11.735 | −0.689 | ||

| cons_cap | 4.196 | −2.498 * | ||

| Energy_gdp | −1.998 ** | −2.713 *** | ||

| gpr | −2.198 | −2.557 | ||

| CO2 | 4.285 | −2.122 | ||

| gdp | −27.982 *** | −4.468 *** | ||

| brent | −2.674 | −2.234 | ||

| Panel B: First differences | ||||

| ren_prod_r | −19.805 *** | −3.163 *** | ||

| cons_cap | −33.999 *** | −5.640 *** | ||

| Energy_gdp | −42.123 *** | −5.501 *** | ||

| gpr | −4.682 *** | −5.178 *** | ||

| CO2 | −35.357 *** | −5.618 *** | ||

| gdp | −46.334 *** | −6.250 *** | ||

| Brent | −5.897 *** | −5.316 *** | ||

| Dependent Variable | Mean Group ARDL Estimator (1) | Common Correlated Effects ARDL Estimator (2) | Dynamic Common Correlated Effects ARDL Estimator (3) |

|---|---|---|---|

| Panel A: Short-run coefficients | |||

| 0.250 | 0.139 | 0.203 | |

| (0.290) | (0.218) | (0.151) | |

| 0.010 | 0.023 * | 0.016 | |

| (0.016) | (0.014) | (0.018) | |

| −0.007 | −0.010 ** | −0.009 ** | |

| (0.005) | (0.004) | (0.005) | |

| −0.001 | −0.001 | −0.001 | |

| (0.000) | (0.000) | (0.000) | |

| −0.084 *** | −0.085 *** | −0.087 *** | |

| (0.013) | (0.014) | (0.014) | |

| 0.003 | 0.002 | 0.004 | |

| (0.005) | (0.004) | (0.005) | |

| −0.000488 | −0.001 | −0.001 | |

| (0.001) | (0.002) | (0.001) | |

| 0.663 *** | 0.544 *** | 0.577 *** | |

| (0.115) | (0.115) | (0.138) | |

| 0.001 *** | 0.001 *** | 0.001 *** | |

| (0.000) | (0.000) | (0.000) | |

| Panel B: Long-run coefficients | |||

| 0.011 | 0.023 * | 0.016 | |

| (0.016) | (0.013) | (0.018) | |

| −0.007 | −0.009 ** | −0.009 * | |

| (0.005) | (0.004) | (0.005) | |

| 0.003 | 0.000 | 0.004 | |

| (0.004) | (0.004) | (0.005) | |

| −0.001 * | −0.001 * | −0.001 *** | |

| (0.000) | (0.000) | (0.000) | |

| −0.084 *** | −0.0851 *** | −0.087 *** | |

| (0.014) | (0.014) | (0.010) | |

| −0.001 | −0.001 | −0.001 | |

| (0.001) | (0.002) | (0.001) | |

| 0.470 *** | 0.426 *** | 0.463 *** | |

| (0.046) | (0.070) | (0.047) | |

| 0.001 *** | 0.003 *** | 0.001 *** | |

| (0.000) | (0.000) | (0.000) | |

| Panel C: Adjustment Term (ECM) | |||

| −0.750 *** | −0.861 *** | −0.797 *** | |

| (0.290) | (0.218) | (0.151) | |

| Observations | 2805 | 2805 | 2668 |

| Number of groups | 100 | 100 | 97 |

| R-squared | 0.99 | 0.050 | 0.050 |

| Cross-sectional means lag | - | - | 2 |

| Cross-sectional Exponent on residuals | 0.606 | 0.588 | 0.607 |

| Weak cross-sectional dependence on residuals | 33.390 *** | 31.81 *** | 33.79 *** |

| Long-run common F-test | 7.430—I(1) | 9.10—I(1) | 10.73—I(1) |

| Long-run ECM t-test | 6.69 *** | 15.64 *** | 27.94 *** |

| Linear trend | Cross-section | No | No |

| Pooled Constant | Yes | Yes | Yes |

| Variable | Mean Group ARDL Estimator (1) | Common Correlated Effects ARDL Estimator (2) | Dynamic Common Correlated Effects ARDL Estimator (3) |

|---|---|---|---|

| Panel A: Short-run coefficients | |||

| 0.001 | 0.068 | 0.207 | |

| (0.006) | (0.076) | (0.206) | |

| −0.048 | −0.031 | −0.047 | |

| (0.040) | (0.036) | (0.045) | |

| 0.001 | −0.002 | −0.000 | |

| (0.008) | (0.007) | (0.008) | |

| 0.001 | 0.001 | 0.000 | |

| (0.001) | (0.001) | (0.000) | |

| −0.024 *** | −0.023 *** | −0.023 *** | |

| (0.007) | (0.007) | (0.007) | |

| 0.002 | 0.002 | 0.002 | |

| (0.006) | (0.005) | (0.007) | |

| 0.001 | 0.001 | 0.001 | |

| (0.001) | (0.001) | (0.001) | |

| 0.217 *** | 0.181 *** | 0.212 *** | |

| (0.003) | (0.037) | (0.007) | |

| 0.000 | −0.002 ** | −0.002 ** | |

| (0.000) | (0.001) | (0.001) | |

| Panel B: Long-run coefficients | |||

| −0.049 | −0.035 | −0.048 | |

| (0.040) | (0.035) | (0.046) | |

| 0.001 | −0.001 | −0.000 | |

| (0.008) | (0.001) | (0.008) | |

| 0.002 | 0.001 | 0.0018 | |

| (0.006) | (0.005) | (0.008) | |

| 0.001 | 0.001 | 0.000 | |

| (0.000) | (0.000) | (0.000) | |

| −0.023 *** | −0.023 *** | −0.023 *** | |

| (0.007) | (0.007) | (0.007) | |

| 0.001 | 0.001 | 0.001 | |

| (0.001) | (0.001) | (0.001) | |

| 0.218 *** | 0.289 *** | 0.203 *** | |

| (0.004) | (0.073) | (0.016) | |

| 0.000 | −0.001 *** | −0.001 *** | |

| (0.000) | (0.001) | (0.000) | |

| Panel C: Adjustment Term (ECM) | |||

| −1.000 *** | −0.932 *** | −0.793 *** | |

| (0.001) | (0.076) | (0.206) | |

| Observations | 478 | 495 | 478 |

| Number of groups | 17 | 17 | 17 |

| R-squared | 0.996 | 0.004 | 0.005 |

| Cross-sectional means lag | - | - | 1 |

| Cross-sectional Exponent on residuals | 0.619 | 0.609 | 0.587 |

| Weak cross-sectional dependence on residuals | −0.52 | 2.27 ** | 1.63 |

| Long-run common F-test | 569.34—I(1) | 77.45—I(1) | 4.89—I(1) |

| Long-run ECM t-test | 215.65 *** | 150.21 *** | 14.84 *** |

| Linear trend | No | No | No |

| Pooled Constant | Yes | Yes | Yes |

| Variable | Mean Group ARDL Estimator (1) | Common Correlated Effects ARDL Estimator (2) | Dynamic Common Correlated Effects ARDL Estimator (3) |

|---|---|---|---|

| Panel A: Short-run coefficients | |||

| 0.021 | 0.042 | −0.008 | |

| (0.035) | (0.056) | (0.039) | |

| −0.012 | −0.010 | −0.058 | |

| (0.069) | (0.069) | (0.066) | |

| 0.082 | 0.085 | 0.113 | |

| (0.066) | (0.062) | (0.069) | |

| 0.001 ** | 0.001 | 0.001 * | |

| (0.000) | (0.000) | (0.000) | |

| −0.465 *** | −0.473 *** | −0.458 *** | |

| (0.079) | (0.079) | (0.079) | |

| −0.082 *** | −0.085 *** | −0.079 ** | |

| (0.026) | (0.027) | (0.032) | |

| −0.002 | −0.004 | 0.003 | |

| (0.002) | (0.003) | (0.004) | |

| 2.050 *** | 2.027 *** | 2.023 *** | |

| (0.226) | (0.233) | (0.218) | |

| 0.000 | −0.000 | 0.033 | |

| (0.000) | (0.000) | (0.023) | |

| Panel B: Long-run coefficients | |||

| −0.011 | −0.011 | −0.079 | |

| (0.071) | (0.072) | (0.076) | |

| 0.079 | 0.077 | 0.169 | |

| (0.069) | (0.066) | (0.108) | |

| −0.086 *** | −0.084 *** | −0.121 * | |

| (0.028) | (0.029) | (0.067) | |

| 0.001 ** | 0.001 * | 0.001 * | |

| (0.000) | (0.000) | (0.000) | |

| −0.490 *** | −0.494 *** | −0.487 *** | |

| (0.087) | (0.085) | (0.086) | |

| −0.002 | −0.005 | 0.009 | |

| (0.002) | (0.003) | (0.009) | |

| 2.063 *** | 2.027 *** | 2.059 *** | |

| (0.269) | (0.233) | (0.284) | |

| 0.000 | −0.000 *** | 0.080 | |

| (0.000) | (0.000) | (0.063) | |

| Panel C: Adjustment Term (ECM) | |||

| −0.979 *** | −0.958 *** | −0.997 *** | |

| (0.0350) | (0.0560) | (0.039) | |

| Observations | 2934 | 3033 | 2934 |

| Number of groups | 98 | 98 | 98 |

| R-squared | 0.644 | 0.350 | 0.520 |

| Cross-sectional means lag | - | - | 2 |

| Cross-sectional Exponent on residuals | 0.500 | 0.508 | 0.519 |

| Weak cross-sectional dependence on residuals | 1.64 | 4.410 *** | 1.670* |

| Long-run common F-test | 169.47—I(1) | 66.100—I(1) | 154—I(1) |

| Long-run ECM t-test | 783.57 *** | 292.000 *** | 669.82 *** |

| Linear trend | No | No | No |

| Pooled Constant | Yes | Yes | No |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Flouros, F.; Pistikou, V.; Plakandaras, V. Geopolitical Risk as a Determinant of Renewable Energy Investments. Energies 2022, 15, 1498. https://doi.org/10.3390/en15041498

Flouros F, Pistikou V, Plakandaras V. Geopolitical Risk as a Determinant of Renewable Energy Investments. Energies. 2022; 15(4):1498. https://doi.org/10.3390/en15041498

Chicago/Turabian StyleFlouros, Floros, Victoria Pistikou, and Vasilios Plakandaras. 2022. "Geopolitical Risk as a Determinant of Renewable Energy Investments" Energies 15, no. 4: 1498. https://doi.org/10.3390/en15041498

APA StyleFlouros, F., Pistikou, V., & Plakandaras, V. (2022). Geopolitical Risk as a Determinant of Renewable Energy Investments. Energies, 15(4), 1498. https://doi.org/10.3390/en15041498