Abstract

To limit the global temperature change to no more than 2 °C by reducing global emissions, the European Union (EU) set up a goal of a 20% improvement on energy efficiency, a 20% cut of greenhouse gas emissions, and a 20% share of energy from renewable sources by 2020 (10% share of renewable energy (RE), specifically in the transport sector). By 2030, the goal is a 27% improvement in energy efficiency, a 40% cut of greenhouse gas emissions, and a 27% share of RE. However, the integration of RE in energy system faces multiple challenges. The geographical distribution of energy supply changes significantly the availability of the primary energy source (wind, solar, water) and is the determining factor, rather than where the consumers are. This leads to an increasing demand to match supply and demand for power. Especially intermittent RE like wind and solar power face the issue of energy production unrelated to demand (issue of excess energy production beyond demand and/or grid capacity) and forecast errors leading to an increasing demand for grid services like balancing power. Megawatt electrolyzer units (beyond 3 MW) can provide a technical solution to convert large amounts of excess electricity into hydrogen for industrial applications, substitute for natural gas, or the decarbonization of the mobility sector. The demonstration of successful MW electrolyzer operation providing grid services under dynamic conditions as request by the grid can broaden the opportunities of new business models that demonstrate the profitability of an electrolyzer in these market conditions. The aim of this work is the demonstration of a technical solution utilizing Pressurized Alkaline Electrolyzer (PAE) technology for providing grid balancing services and harvesting Renewable Energy Sources (RES) under realistic circumstances. In order to identify any differences between local market and grid requirements, the work focused on a demonstration site located in Austria, deemed as a viable business case for the operation of a large-scale electrolyzer. The site is adapted to specific local conditions commonly found throughout Europe. To achieve this, this study uses a market-based solution that aims at providing value-adding services and cash inflows, stemming from the grid balancing services it provides. Moreover, the work assesses the viability of various business cases by analyzing (qualitatively and quantitatively) additional business models (in terms of business opportunities/energy source, potential grid service provision, and hydrogen demand) and analyzing the value and size of the markets developing recommendations for relevant stakeholder to decrease market barriers.

1. Introduction

The replacement of fossil fuels with renewable energy sources at the EU level will demand a total transformation of its energy system [1,2,3]. The new EU energy system will be characterized by two basic modifications: (1) highly increasing power generation from Renewable Energy Sources and (2) increased electrification of energy end-use segments. The combination of the above parameters creates significant challenges for the electrical stability of the emerging power system, since on the one hand the power supply is intermittent (wind and solar power production varies significantly both in the short and long-term), and on the other hand the power demand is variable (daily and seasonal), resulting in the fact that they do not easily match over long periods of time. These characteristics of the new energy system result in problems related to the voltage and frequency of the electrical network and to frequent power curtailments, especially from wind parks [4].

These problems are even more severe in autonomous-isolated power systems, such as the ones serving non-interconnected islands. Therefore, measures related to energy storage to achieve grid balancing should be enforced in the electricity networks at an EU level. Such measures will significantly contribute in higher RES penetration and in the production of useful energy carriers (electricity and hydrogen) that could be used in a variety of applications. The variable power production of renewables, especially when exceeding specific thresholds, in combination with the daily and seasonal variable power demand, creates a need for short- and long-term grid balancing [4].

The concept of grid balancing is related to the introduction of additional load demand, especially in the periods of high renewable energy production and low power demand, absorbing excess renewable energy, which can be sent back to the grid at periods of low production from wind and solar parks and relatively high demand.

It is widely known [5,6,7] that in order to balance the variations of power production from renewables and power consumption and ensure that stability of the electricity grid, there are different methods and approaches.

The simplest balancing method, which has been used widely in the past is the enforcement of power curtailments in wind parks mainly at periods of high renewable energy production. According to this method, the operator of the electricity grid provides wind energy producers with low set-points of operation/production, or even shuts-off the entire wind energy production. This method is highly ineffective, since on the one hand it significantly increases the payback period of large investments in the field of renewable energy and on the other hand it significantly reduces renewable energy penetration in the overall energy system [8]. In case of high demand and low renewable energy production, the simplest method used in the past was to turn on additional generators driven by fossil fuels, which is not a viable option as well, since this strategy is not compatible with EU decarbonization targets [9].

Extensive research has already been done in order to explore the potential of integrating renewable energy sources with electrolyzers and fuel cells for the stabilizing of the power grid. This research concerns not only the pure technical part, but the economical part as well. Matute et al. [10] showed for the case of Spain that the use of multi-MW electrolysis for the provision of grid balancing services appears to be a promising option in order to obtain cost competitive hydrogen. Gutierrez-Martın et al. [11] also examined different scenarios for the adoption of hydrogen use for electric grid balancing in the Spanish power system, showcasing the feasibility of a 42% renewable energy penetration. Guinot et al. [12] investigated the economic viability of an electrolysis-based hydrogen power plant, which provides balancing services to the network and highlighted the threshold values within which it could become economically attractive. Mansilla et al. [13] examined possible cost reductions in hydrogen production by a discontinuous operation of alkaline electrolyzers, observing a 4% increase in profits compared to continuous operation. Grueger et al. [14] investigated the integration of electrolyzers with wind turbines as a means to balance any fluctuations in the grid, showcasing the profitability of the above under the suitable circumstances. Sorensen [15] showed the effect of power to power systems including hydrogen production on the renewable energy penetration for northern European grids. Paulus et al. [16] examined the effects of electrolyzer operation for the provision of grid services in an industrial context, while Jorgensen et al. [17] investigated the effect on hydrogen pricing resulting from the adoption of an electrolysis unit, powered by curtailed wind power with the subsequent participation in the power market. Kiaee et al. [18] demonstrated the feasibility of utilizing alkaline electrolyzers for regulating the grid’s frequency, based on the fast response to varying operation loads, which can be achieved by such devices.

The three leading technologies for electrolysis are the Proton Exchange Membrane (PEM) electrolyzers, the Solid Oxide Electrolysis Cell (SOEC) electrolyzers, and the alkaline electrolyzers, each of which comes with its benefits and its drawbacks. SOEC electrolyzers still are a relatively immature technology, but show great potential, due to certain characteristics such as their ability to operate reversibly. PEM electrolyzers provide high current densities and high hydrogen purity, while presenting the ability to respond to variable loads in a satisfying manner. Alkaline electrolyzers, while not as flexible as PEM electrolyzers, due to their ability to overload operation up to 150% seem ideal for power to gas applications, coupled with intermittent power supply. Besides, pressurized alkaline electrolyzers tend to contribute to an overall lower power consumption due to the fact that the energy needed for compression by an external compressor is lower [19].

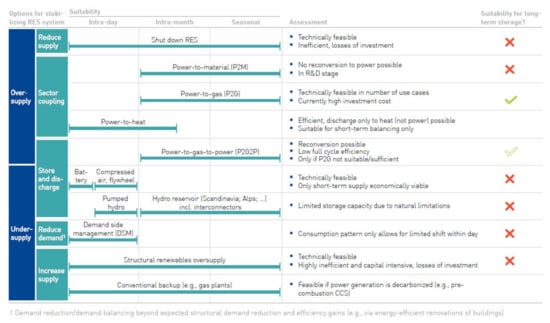

The new and emerging EU energy system uses modern and innovative techniques for grid balancing. The first approach for the new grid balancing method is a combination of coupling different sectors and an interconnection of the building heating and cooling demand, the transport and industrial sector as energy consumers with power generation. Such an approach provides a higher stability to the renewable energy system [20]. The second approach for grid stabilization and balancing is the application of long-term storage/discharge technologies. The third approach is the transportation of energy from centers of supply to centers of demand, using also smart grid techniques. The first approach enables balanced demand between different sectors, the second one provides grid balancing directly through the storage/discharge units of renewable power, while the third approach can be combined with the other two, in order to come up with a stabilized, efficient, and environmentally friendly EU energy system.

Hydrogen is an ideal solution for grid balancing, both as a mechanism for the coupling of sectors, and as a long-term plus large-scale energy storage option [21]. Hydrogen can also serve ideally the third grid balancing approach as well, since it can be transported from centers of supply to centers of demand. In other words, hydrogen is necessary to ensure the transition to the transformed EU energy system [21]. In more detail, the contribution of hydrogen to grid balancing of the emerging EU system (for each of the three approaches) is analyzed below.

1.1. Sector Coupling

The basic concept behind coupling of sectors lies in the direct connection of power generation with other energy demand sectors, such as the one of transport. This approach solves two problems related to grid balancing: (a) energy is not produced at the location where it is required and (b) it is not produced at the time it is required. The following technologies of the approach are used:

Power to heat: This is an interesting technology, using the excess of renewable energy production to supply heating/cooling for buildings or other infrastructure, driving electric boilers, heat pumps, etc., or feed it directly into the district heating infrastructure, wherever it is available. The power to heat technique is generally efficient, yet nevertheless has specific drawbacks: (a) it can only be used in specific applications (buildings and infrastructure), (b) it does not contribute significantly to grid stabilization, since the timing of excess renewable energy production and heating/cooling demand is usually different, and (c) long-term heating storage is not possible without degradation.

Power to gas: This is a more flexible sector coupling option in terms of achieving grid balancing and stabilization. Hydrogen can play an important role in this method, since in contradiction with other gases, the conversion of excess power to hydrogen through electrolysis can be a cost-efficient solution, especially when there is abundant renewable power. By using this method of hydrogen production through electrolysis driven by excess renewable energy, the emerging EU system can be stabilized on a yearly basis and high RES penetration accompanied with very low wind energy curtailments can be achieved. Hydrogen is as flexible as natural gas, and in addition this option produces zero greenhouse gas emissions (especially CO2). Moreover, hydrogen has the advantages of rapid scale-up, storage, and efficient power distribution to a variety of other energy consuming segments, without introducing a need for major infrastructure modifications as well.

1.2. Storage and Discharge

The option of storage/discharge is complementary to the approach of sector coupling, in order to achieve direct grid balancing and stabilization. Batteries can be considered as an obvious solution for this method of grid balancing, but they have specific disadvantages: (a) they can only store energy for short-term periods, (b) they are also expensive when taking into account the amount of energy stored, and (c) they have significantly lower energy density. Therefore, the main drawback of this technology is that they cannot store high energy amounts, especially for longer periods of time. With respect to storage and discharge method for grid balancing, there are specific technologies that can be used:

Pumped Hydro: This is a well appreciated long-term energy storage option, which unfortunately has a limited application in the EU energy system. Another drawback of this technology is the fact that it has specific natural, regulatory, permitting, and social-related barriers. Pumped hydro units have also another disadvantage: they can only be installed in selected geographical areas, having specific characteristics, therefore their application is limited

Hydrogen: It has the advantages of storing energy in the long-term, at higher quantities (large-scale energy storage), and at a competitive cost as well, when compared to other conventional large-scale energy storage technologies, such as pumped hydro. This storage/discharge option may have a lower conversion efficiency compared to other technologies, it is widely accepted that the re-electrification of hydrogen (and the associated low conversion factors) will not be required, since hydrogen can be used in a variety of applications, such as the transport and industrial sector and also provide heat for buildings and related infrastructure. Another advantage of hydrogen compared to other storage solutions, such as pumped hydro is the fact that the EU has significant H2 storage capacities. EU has a grid capacity of 36 billion m3 and if we assume a 10% blending, then the energy storage capacity in the form of hydrogen is in the order of 100 TWh [22]. Specific geological formations, such as salt caverns and depleted gas fields, will be used in the future for storing hydrogen. It has been calculated that almost 40 TWh of hydrogen can be stored only in salt caverns in the EU [23]. It is also important that the technical feasibility of this concept has already been proved, since six projects related to storing hydrogen in salt caverns are already in operation today.

1.3. Transportation of Energy

This is the third approach for grid balancing, dealing with the fact that except from the seasonality of supply, the location of supply is also critical. It is widely known that the renewable energy installations are often situated in areas that cannot absorb the entire production of wind and solar parks. The solution of building energy transmission lines infrastructure has a high cost. Hydrogen provides an advantageous solution for this grid balancing approach as well, since after the conversion of electricity to this energy carrier, it can be transported in liquid and compressed form, or transferred through pipelines.

In Figure 1, a comparison of sector coupling and storage technologies is depicted, clearly showing the advantages of hydrogen use in grid balancing applications.

Figure 1.

Comparison of sector coupling and storage technologies for grid balancing [21].

The following work aims at evaluating potential benefits, stemming from the use of hydrogen in grid balancing applications, while identifying different value streams resulting from the integration with industrial settings. One of the main findings of this study is the need for inter-sector co-operation for achieving profitable business cases based on hydrogen adoption.

2. EU Policies for the Promotion of Renewable Energy Sources and Energy Storage

In the context of this paragraph, the most significant EU policies for the promotion of renewable energy sources and energy storage will be presented. Specific targets for the targeted EU member states (Spain, Austria, and Greece) in these fields will also be demonstrated.

2.1. EU Policies for the Promotion of Renewable Energy Sources

The promotion of renewable energy sources in the European Union has been adopted through the Directive 2009/28/EC, which sets specific goals for the RE share in the European energy mix of at least 20% by 2020. The above mentioned directive was revised in 2018. The revised renewable energy directive resulted in a European policy adopting one of the most ambitious policies in the field worldwide. The revised renewable energy directive is part of the Clean Energy for all Europeans package. The main components of this policy are the following [2]:

- The revised renewable energy EU directive continues European leadership in the field, setting a binding target of renewables of at least 27% by 2030 in the energy system of Europe.

- The directive significantly contributes to Europe’s fight against climate change and the achievement of Paris Agreement climate goals.

- The new directive contributes in the protection of EU environment and will specifically help in reducing air pollution in European cities and regions.

- The revised renewable energy EU directive gives the chance (and allows) to households, communities, and companies to become producers of clean energy and contribute to the reduction of greenhouse gas emissions.

- It also reduces the dependency of the European Union on energy imports and increases the security of energy supply.

- The revised RE directive highly contributes in the creation of more job positions and in the attraction of new investments in the European economy related to energy.

- The new policy framework established for renewables, incorporated through the adoption of the revised EU directive results in specific benefits:

- o

- It provides a longer-term risk reduction for investors and speeds up the procedures to receive permits for renewable energy projects.

- o

- It introduces an innovation, where the energy consumer has an important role in the energy transition, having a clear right to produce their own renewable energy and distribute it to the European electricity grid.

- o

- It helps increasing the competition and the integration of renewable electricity to the market.

- o

- It will accelerate the uptake of renewable energy sources in other sectors such as heating/cooling and transport applications.

- o

- It has a main focus on increasing the sustainability of bio-energy and promoting innovative technologies (including hydrogen production as a grid-balancing method).

The policies and measures for the targeted countries (Austria, Greece, and Spain) for the promotion of renewable energy sources will be presented in detail in the following sections.

2.1.1. Austria

The 2010 National Renewable Energy Action Plan [24] of the country was developed in order to adopt Directive 2009/28/EC. According to this directive, Austria should have increased its renewable energy share in the final energy consumption to 34% by 2020. This figure in 2005, which is used as a base year, was 24.4%, while in 2008 this value had already reached 29%. The achievement of this target will be based on the following two conditions:

- In comparison to the reference scenario of base year 2005, a total reduction of final energy consumption in the order of 13% should be achieved.

- The installed capacity of renewable energy should be increased by 18% in comparison to the installed capacity of 2008.

The target of 34% renewables in the final energy consumption of Austria can be achieved by different combinations of each renewable energy technology. In addition to renewable energy technologies producing electricity such as wind, solar, and hydro, the exhaustion of available biomass potential is important to provide heating and cooling, while achieving the 10% biofuel target. To determine the final energy mix of different renewable energy technologies in order to achieve the above-mentioned target, the factors of cost-efficiency, resource availability, and environmental protection are taken into account.

With respect to the decrease of final energy consumption compared to the reference scenario, required in the context of the national renewable energy plan of Austria, the following reductions should be achieved in the three main areas of energy use:

- 22% reduction in the transport sector,

- 12% reduction in heating and cooling, and

- 5% reduction in the electricity sector.

The National Renewable Energy Action Plan identifies the existing or planned measures and policies that will be used in order to achieve its targets and promote the use of energy produced from renewable energy sources. The most significant measures and policies in the Austrian plan are presented in Table 1.

Table 1.

Overview of all policies and measures of the National Renewable Energy Action Plan of Austria [24].

2.1.2. Spain

The National Renewable Energy Action Plan of Spain [25] foresaw that the Share of Renewables in the Annual Average Electricity Demand Would be Close to 40% by 2020. The Breakdown between Different Renewable Energy Technologies Shows that Wind Energy Has the Lion Share of the whole re production (in the order of 52%), and is followed at a high distance from Hydro, Solar Thermoelectric and Solar Photovoltaic which Have a Share of Respectively 8.3%, 3.8% and 3.6% of Gross Total Electricity Generation. The National Electricity Balance of Spain is presented in Table 2.

Table 2.

National Electricity Balance of Spain [25].

According to the Spanish National Renewable Energy Action Plan, the share of energy from renewable energy sources in the gross final consumption of energy was 8.7% in 2005 (base year). The target for energy from renewables in gross final consumption of energy for the year 2020 was 20%, while the total expected adjusted energy consumption in year 2020 was 97,041 ktoe, from which 19,408 ktoe would come from renewable energy sources.

Spain’s target and estimated trajectory of energy from renewable energy sources in heating and cooling, electricity, and transport are presented in Table 3.

Table 3.

Spain’s target and estimated trajectories in heating/cooling, transport, and electricity [25].

Measures and policies to support the achievement of Spain’s targets in the renewable energy sector are presented in Table 4 and Table 5.

Table 4.

General measures [25].

Table 5.

Measures in the field of electricity generation using renewables [25].

2.1.3. Greece

The National Renewable Energy Action Plan of Greece [26] describes the procedures and goals of the country in order to promote the penetration of renewable energy sources and meets the obligations imposed by the 2009/28/EC Directive. According to the Greek National Renewable Energy Action Plan, the share of energy from renewable energy sources in the gross final consumption of energy in the country was 6.9% in 2005 (base year). The target for energy from renewables in gross final consumption of energy for the year 2020 was 18%, while the total expected adjusted energy consumption in the year 2020 was expected to be 24,114 ktoe, from which 4341 ktoe would come from renewable energy sources.

Greece’s target and estimated trajectory of energy from renewable energy sources in heating and cooling, electricity, and transport are presented in Table 6.

Table 6.

Greece’s target and estimated trajectories in heating/cooling, transport, and electricity [26].

Measures and policies to support the achievement of Greece’s targets in the renewable energy sector are presented in Table 7.

Table 7.

Selected measures and policies of the Greek National Renewable Energy Action Plan [26].

2.2. EU Policies for the Promotion of Energy Storage (Including Hydrogen)

Energy storage, both short- and longer-term has been recognized as a prerequisite for higher RES penetration and grid balancing in the EU. The objective of this paragraph is to present policies adopted by the European Commission and the Member States as well those that support the promotion of energy storage. Focus will also be given to the countries of Austria, Spain, and Greece.

Energy storage has a growing role in the energy transition of the European Commission. It contributes in the following:

- Greenhouse gases reduction

- Decarbonization of other economic sectors such as the transport and industrial sector

- More electricity in the energy consumption

- It is necessary to bring up changes in the electricity mix: in more detail it helps phasing out conventional generation and introducing more intermittent renewables.

The following steps related to energy storage and its promotion to the European energy system have been made so far:

- Definition of energy storage and set-up of basic policy principles

- Electricity market design

- Storage technologies initiatives have been developed

- Sector coupling (electricity, gas, heating, industry, transport, agriculture)

- Support of Energy Storage Projects,

- Discussion with stakeholders.

With respect to the latter step (discussion with stakeholders), the European Commission asked stakeholders to answer to the following questions:

- Why does the energy system need storage?

- What are the barriers (regulatory, fiscal, economic, technical) in the deployment of energy storage?

- Is the regulatory framework sufficient to ensure that markets can deploy energy storage?

- Should the EU make further efforts? What type of actions/policy options should be considered?

In the following paragraphs, the above-mentioned six (6) steps related to energy storage and its promotion as a means of grid balancing amongst other, will be analyzed in detail.

Definition and policy principles: According to the Proposal of Electricity Directive (recast), Article 2, “Energy Storage” means (in terms of an electricity system) deferring an amount of the electricity that was generated to the moment of use, either as final energy or converted into another energy carrier. The following principles support the market development of energy storage:

- Contribution in energy security and decarbonization targets of the electricity system

- Participation in electricity markets

- Participation with equal terms with providers of flexibility services

- The cost-efficient use of decentralized energy storage and its integration into the system should be enabled in a non-discriminatory way

Electricity market design: The Electricity Market is designed by taking into consideration certain rules that ensure the flexibility of energy storage:

- It ensures the neutrality of network operators vis-à-vis new business activities in storage: In more detail, when a network operator needs energy to manage its network, this energy is procured from market participants, and only in cases there are no market interests at all, a regulatory authority may grant a temporary derogation.

- Regulatory authorities should ensure that charges for access to network do not discriminate energy storage.

- Storage deployment will be facilitated by the fact that stricter rules on RES curtailment (in combination with higher targets on RES penetration) exist.

- In day-ahead and intra-day market, energy trading should be as close to real time as possible and a bid size should not exceed 1 MW.

- Strengthening of short-term price signals will ensure that electricity prices provide correct and meaningful production and investment signals.

- Risk preparedness: all measure, including storage that will help in avoiding crisis or containing a crisis are equally relevant.

Storage technologies initiatives: The following energy storage technologies initiatives already exist at EU level:

- Technological innovation in energy storage is strongly supported and financed by the EU under the HORIZON 2020 Programme.

- The collaboration within the Strategic Energy Technology Plan (SET Plan) enables EU players to define priorities on research and innovation and collaborate in the energy sector. This includes also the action on smart energy system and the action on batteries.

- The technologies related to the use of electricity to produce gas, mainly hydrogen, are managed through a specific program office, the Fuel Cells and Hydrogen Joint Undertaking (FCH JU).

- The EU Battery Alliance aims to create competitive and sustainable battery cell manufacturing in Europe, supported by a full EU-based value chain. The Action Plan supporting this alliance was published by the European Commission in May 2018.

Sector coupling: The objectives of coupling between different sectors (electricity, heating and cooling, transport, industry, and agriculture) are the following:

- The basic concept lies in both physical and market coupling of the electricity, gas, heating and cooling with other economic sectors (industry, transport, agriculture)

- It is a tool contributing to the decarbonization of the energy system, while in parallel provides the necessary flexibility to the electricity and has networks (e.g., excess of decarbonized electricity is transformed to other forms of energy for temporary storage, or direct use, or for the production of useful products)

- There are several studies available at the EU level, aiming to identify:

- o

- Existing regulatory barriers and potential gaps to the coupling, in particular of electricity, gas, and heating sectors.

- o

- Recommendations to overcome barriers/fill the gaps.

Support of Energy Storage Projects: The following support is given to energy storage projects by the EU:

- Energy Storage Projects in electricity can also become Projects of Common Interest (PCIs).

- In the context of the TEN-E infrastructure framework, large storage projects, above 225 MW, may be included in the selection process for the PCI. Smaller storage units may be part of smart grid PCIs.

- In November 2017, the European Commission published its third list of PCIs, which includes 15 storage projects in electricity (11 projects on pumped hydro storage and 4 projects on compressed air energy storage).

Discussion with stakeholders: The following interaction with different stakeholders and the EC has been done [9]:

- High level roundtable on energy storage and sectoral integration was organized on March 2018. Representatives from industry, research, and the European Commission participated in the discussions related to the role of energy storage and sectoral integration in the transition to a low-carbon economy.

- Discussions with member states at the Electricity Co-ordination Group took place on July 2018.

In more detail, the following policies aiming to regulate the contribution of energy storage in the EU electricity market have been designed by the commission:

- Balancing: The concept of financial responsibility is defined with an aim of balancing the energy system with the contribution of all participants of the energy market.

- Day ahead and intra-day: The electricity market is evaluated in time periods of 15 min and facilitates bids up to 1MW.

- Price caps: There exist no maximum or minimum price caps.

- Priority dispatching: Priority is given to small-scale renewable energy producers as to high efficiency CHP.

- Curtailment of re-dispatching: There is curtailment only in case it is cost efficient and while it is not exceeding 5%.

- Bidding zone: The bidding zones are shaped according to the observed long-term high-demand scenarios.

- Network congestion: Any issues of network congestion should be resolved by utilizing non-discriminatory solutions that are adapted to the market needs.

- Grid fees: The fee structure is being recommended partially by ACER. The structure should take into consideration issues such as customer’s profile, the presence of energy storage, etc.

- Regional TSO cooperation is assured by developing solutions at the regional level.

- The “EU DSO entity” has a twofold role: (a) The co-ordination of transmission and distribution networks, and (b) the integration of RES with distributed power generation, energy storage, etc.

In the next sections, the initiatives, measures, and policies related to energy storage and hydrogen in particular, at national level of the three targeted countries (Austria, Spain, and Greece), will be presented.

2.2.1. Austria

Austrian Climate and Energy Strategy (2030-objectives)

- Share of 44–50% renewable energy in gross final energy consumption by 2030 (currently 33.5%).

- A total of 100% of total national electricity consumption from renewable energy sources by 2030 (currently 72%).

- Transition to low and zero-emission vehicles via alternative propulsion systems and fuels based on renewable energies (battery vehicles, fuel cell vehicles, bio-gas, and liquid bio-fuels).

National Hydrogen Strategy

- This strategy is being developed by BMVIT and the Ministry for Sustainability and Tourism in close cooperation with science and industry until the end of 2019.

- The strategy is part of the contents of the European Hydrogen Initiative initiated by Austria during the EU-presidency. The elaborated targets and measures will be included in the National Climate and Energy Plan, which will be submitted to the EC by the end of this year, which will already be partially implemented in the Renewable Development Act (EAG) 2020.

- Four working groups:

- o

- Infrastructure, generation, and storage

- o

- Greening the gas

- o

- Hydrogen in industrial processes

- o

- Fuel cells and hydrogen end-use (mobility and buildings).

European Hydrogen Initiative

- Objective: Maximize the great potentials of sustainable hydrogen technology for the decarbonization of multiple sectors, the energy system, and for the long-term energy security of the EU.

- Signatories: 23 EU member states and more than 100 companies and research organizations.

- Conversion of hydrogen to renewable natural gas: Austria explores the most effective conversion of renewable hydrogen into synthetic methane and other renewable fuels.

- Sector integration and coupling: Austria emphasizes the role of hydrogen as a promising link between the electricity, industry, and mobility sectors. In this way, new opportunities arise, in activities such as energy flexibility, availability, and security, as well as improved efficiency and cost-effectiveness, which contribute to the overall decarbonization of the energy sector.

- Industry: Austria promotes the use of renewable hydrogen as well as derived products in industrial processes.

Austria as a potential hydrogen valley in the heart of Europe

- Bridging many neighboring countries including eastern Europe.

- Central player of the European natural gas grid with huge storage capacity.

- High share in renewable energy sources: second in Europe in transport, approaching 100% renewable electricity.

- Strong energy sector and vehicle industry as well as high R&D-competence.

- Complementarity with other European counties as provider of supply components and engineering services.

Challenges

- Dependency on energy imports: fossil fuels worth around €400 billion are imported annually, which accounts for more than 25% of all imports into the EU.

- Emission reduction: simultaneous reduction of greenhouse gases, pollutants, and noise to achieve EC climate goals, COP21 objectives, and clear air regulations.

- Storage of intermittent renewable energy sources, setup of nationwide grid of hydrogen refueling stations, development of cheap and reliable fuel cells.

Austrian automotive industry

- Automotive industry is a global key industry sector and one of the most successful industrial branches in Austria.

- 75,000 employees and 700 companies.

- Turnover of 21.5 billion €/year.

- Automotive export revenues three times higher than import expenditures.

- 26% of employees in R&D and 21,459€ for R&D per employee (industrial average of 8700 €).

2.2.2. Spain

Policies Enabling Demand Response in Spain

Currently, in Spain the only possibility to provide grid services using loads [2] is called interruptibility grid service and is meant for situations where there is not enough generation to supply the demand [2]. This could be due to a peak of extraordinary consumption, or a sudden loss of production, which are not usual events in Spain due to the sufficient capacity of the generation system. The service is regulated by Order IET/2013/2013 [27], which establishes the competitive mechanism of assignation of the interruptibility demand management grid service. The service awards large industrial consumers and has been used very few times in the past decade until 2018, when the transmission system operator (TSO) Red Eléctrica de España decided to use it with economic criteria to lower electricity prices instead of restricting it to shortcoming technical issues. Since the beginning of 2018, the service has been requested to the providers more times than in the last decade. The service requires decreasing consumption from loads through 5 or 90 MW packages and with three different response times: (a) instantaneous execution without pre-order (response within seconds), (b) fast execution (minimum pre-order of 15 min), and (c) hourly execution (minimum pre-order of 2 h) with tenders every year to select the providers and set the remuneration for the available capacity offered (EUR/MW) and for the energy reduction (EUR/MWh). This scenario is feasible for participation of multi MW electrolyzers, but a service availability of more than 95% is required by the TSO, which would mean an electrolyzer of minimum 5 MW in continued production being able to reduce power consumption in 5 MW when requested, with the consequent operational costs linked to such a mode of operation. This is feasible for a large electrolyzer providing a continuous stream of hydrogen, for example in a chemical plant, with a huge demand of this fuel. However, this use is already mature (stationary operation) and restricted to specific niche markets. These include industries with a need for hydrogen for their processes, unable to cover the large upcoming hydrogen markets planned to be deployed in the EU, with smaller demands. This is the case of mobility with FCEVs, which do not require such an amount of this fuel yet. Thus, the interruptibility grid service is not considered as the option to capture revenues in a case study meant to analyze the potential to serve mobility with FCEVs.

A more attractive option to implement demand response with flexible multi-MW loads to provide grid services in Spain would be the possibility to adjust grid frequency through the secondary regulation market (as it is possible in Austria for example with the aFRR). This is because the provision of the service includes a remuneration not only for power reductions (as it is the case of interruptibility), but also for increases through 10 MW packages with a time response of less than 5 min. Currently, only generators are allowed to participate in the secondary regulation service, so loads such as electrolyzers would be excluded from application, which limits the possibilities for demand response implementation in the country as a complementary tool to face the increasing penetration of renewable generation in the electricity system. However, having a look at the trends in other EU countries where there are already grid services in place providing remuneration to loads increasing or decreasing consumption by packages of more than 1 MW or 5 MW to regulate frequency, accommodate RES, and comply with the EU goals in this matter, it seems Spain should require soon a similar approach to avoid substantial updates in grid infrastructures.

Potential for Hydrogen Markets

Besides mature markets (e.g., hydrogen production required in chemical plants), in Spain the greatest potential in the last years has been towards hydrogen mobility. However, Spain is still lagging behind EU initiatives in terms of hydrogen refueling infrastructure, which concentrate mainly in the countries in the center and north of Europe. Table 8 shows the expected amount of HRS in the EU in 2020, 2025, and 2030 in the pioneering countries in the introduction of FCEVs [28,29,30,31,32].

Table 8.

Perspectives for the cumulated number of HRS deployed in EU countries.

Inside this framework, Spain is trying to join these initiatives so as not to remain isolated from the deployment of hydrogen corridors, which link these EU countries and specifically, to create links with France. Now, six HRS are available in Spain for refueling and four new ones are foreseen by 2020 to link the north of the country with the south of France through the H2PiyR project [33,34]. The aforementioned initiatives will try to meet the targets of the Spanish Government, aiming at the commissioning of 20 HRS by 2020 [35]. A drawback that hinders the adoption of hydrogen mobility in Spain is the high total costs of ownership (TCO) for the FCEVs. The FCEVs, which are currently available in the market, showcase similar performance to conventional ICE vehicles (e.g., Hyundai ix35, Toyota Mirai, Honda Clarity FCV, or Renault Kangoo ZE H2). The improved CAPEX and OPEX values result from the improved efficiency of hydrogen, since it is converted into electricity onboard, instead of being burnt in an ICE. There, it is still need to reduce the presence of platinum group metals to reduce CAPEX in the fuel cell as well as to work on durability to increase lifetime of fuel cell stacks and reduce maintenance costs (i.e., OPEX). In the case of the refueling infrastructure, if built to be fed with green hydrogen from renewable energy by means of electrolysis, it involves the CAPEX of the electrolyzer and the cost of hydrogen storage and the HRS (which includes a compression installation), which in case of supply at 700 bar (latest standard pressure for refueling in the EU) means more than 1000 kEUR for a supply of around 200 kg of hydrogen per day (an average car in the EU travels 12,000 km/year, which means 2.3 kg of hydrogen demand per week if 1 kg of this fuel allows to drive for 100 km). These costs are even increased if the HRS is small, as economies of scale strongly benefit FCH technologies.

2.2.3. Greece

The main policy adopted by Greece to facilitate the deployment of energy storage in its national energy system is related to provisions introduced in Greek Laws 3468/2006 and 3851/2010 with respect to the operation of hybrid power systems in the non-interconnected electricity networks of the country.

More specifically, Greece was one of the first EU member states to introduce specific policies and measures promoting energy storage as a medium of increasing renewable energy sources penetration, mainly in the weak electricity grids of islands. According to this legislative and regulatory framework, the operation of hybrid power stations comprising of at least one renewable energy source and at least one energy storage device is allowed in all autonomous (non-interconnected) electricity networks of the country.

According to the provisions of the above-mentioned legislation, a feed-in tariff model is introduced for the promotion of hybrid power stations in Greece; the tariff being calculated differently for each individual isolated (autonomous) electricity network, as a result of a detailed energy study and simulations taking mainly into account the marginal system price, the actual cost for energy production, and the existing renewable energy penetration. Using this legislative and policies measures, the following hybrid power stations operate/have been designed in Greece:

- Tilos island hybrid power station comprising wind, PV, and batteries (in operation).

- Ikaria hybrid power station comprising wind and pumped hydro (under construction).

- Crete hybrid power station comprising wind and pumped hydro (under permitting procedure).

- Ai Stratis hybrid power station comprising wind, PV, and batteries (design of the project completed).

- The Greek government has announced that three additional small Greek island will be transformed into green energy islands, through the introduction of energy storage technologies in combination with RES, namely Symi, Astypalaia, and Kastelorizo. There will be a tendering procedure for investors that will take over the implementation of these projects.

The feed-in tariffs for hybrid power stations have not been set for all non-interconnected electricity in Greece, since this is a time-consuming procedure, triggered by investor applications for power production permits in each system. For the time being, the tariffs that have already been set in Greece range from 165 to 234€/MWh.

The technical specifications regarding the terms of operation and pricing, and the provisions set in the above-described legislation have been designed mainly taking into account the energy storage technology of pumped-hydro. This fact creates significant problems in the economic viability of hybrid power stations using other energy storage technologies, including hydrogen.

In addition, according to Greek Law 4439/2016, the country adopts the EC Directive 94/2014 regarding alternative fuels infrastructure. All required technical specifications of vehicles and hydrogen refueling station infrastructure are set in this legislation. Unfortunately, the Greek state has not taken any other measures and policies to promote hydrogen, both as an energy storage medium and grid-balancing method.

3. Overview of European Electricity Markets and Prices

One of the most important parameters and input in the market potential assessment of hydrogen produced through electrolysis for grid balancing purposes is the identification of the methodology of operation of the European electricity markets and especially the prices related to renewable electricity, including its short- and long-term variations. This is a critical parameter for the economic viability of any project aiming at providing grid balancing services for the following reasons:

- The economic viability of hydrogen production through PAE for grid balancing applications is strongly related to the cost of electricity used to drive the electrolyzer. Therefore, the operation of the electrolyzer to provide grid balancing services becomes economically favorable when the cost of electricity is low.

- In the northern European countries and in general in countries with high RES (especially wind) penetration, there is an opportunity to buy electricity at very low (or even negative cost) at periods of high RES production and when the electricity demand is relatively low (e.g., during nighttime).

- On the other hand, hydrogen production to provide grid balancing services makes sense in financial terms, in countries that have low cost of electricity (with Greece being one among them) all year around.

- Daily variations on the cost of electricity in countries with smart metering operation and the ability to change between electrical energy providers gives the opportunity to the producers of hydrogen through electrolysis to decide the periods of time in which they will operate in order to reduce their costs of electricity and come up with a more profitable business case.

- In addition, another option for grid balancing is to sell electricity produced from hydrogen in fuel cells back to the grid. Electricity prices are important for this option as well, where hydrogen producers become electricity producers and they are able to select periods of low renewable energy production in order to sell electricity at higher prices.

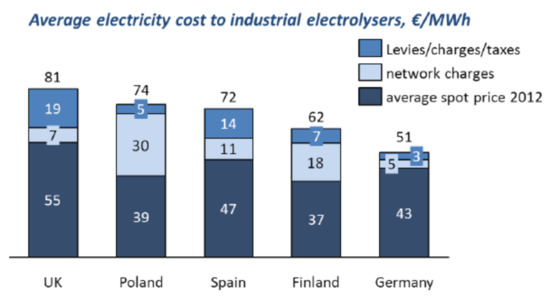

3.1. Overview of Electricity Prices for Industrial Electrolyzers at an EU Level

In the FCH JU study titled “Water Electrolysis in the European Union” [4], representative data sets values for different types of regulatory and pricing environment from five European member states were selected in order to analyze the available cost of electricity for industrial electrolyzers. The countries selected represented significant variations (by electricity price, penetration of renewables, and overall market size) in order to come up with an overview of different cases and business development environments. As can be seen in Figure 2, a large range of electricity prices for industrial consumers is available in different member states.

Figure 2.

Average electricity cost of industrial electrolyzers in 2012 [4].

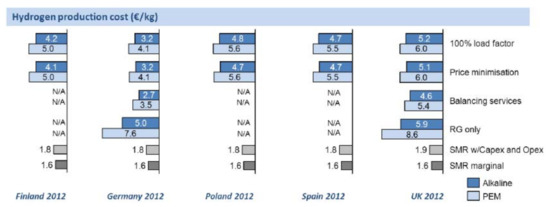

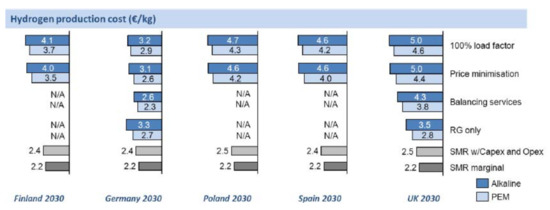

The large variation in electricity prices in different countries and in different periods of time and conditions results in a significant differentiation on the cost of hydrogen produced from electrolysis, depicted in Figure 3 and Figure 4, since as will be analyzed in the following paragraphs, electricity prices are a critical factor affecting highly both total hydrogen production cost and the economic viability of the investment as well. It should be noted that in Figure 3 and Figure 4,“RG only” refers to renewable generators.

Figure 3.

Hydrogen production costs in 2012 for best case KPIs for Alkaline and PEM electrolyzers in different electricity market scenarios [4].

Figure 4.

Hydrogen production costs estimated for 2030 for the best case KPIs for Alkaline and PEM electrolyzers in different electricity market scenarios [4].

3.2. Identification of Electricity Prices for Industrial Electrolyzers in the Targeted EU Countries

The electricity prices for industrial electrolyzers in the remaining targeted EU countries, namely Austria and Greece (these prices were presented for Spain in the previous paragraph), are presented in the following paragraphs.

3.2.1. Austria

Market conditions in Austria have changed significantly. The bidding zone integrity between German and Austrian electricity market has been suspended and replaced with a capacity market mechanism. This has led to significant price changes for wholesale electricity. Additionally, the market design for the Austrian regulatory energy market changed in 2018.

A simulation based on past market data was designed and implemented. This simulation incorporates the new balancing power market design (introduced in summer 2018) and changes originating from the bidding zone separation of Austrian and German wholesale electricity market. Due to the new market design, price levels and bidding strategies have changed considerably.

The new simulation data is based on market information from October 2018 until March 2019. Although a full calendar year set of market data is not available yet, relevant changes are incorporated in the available data and the results of the simulation incorporate actual market conditions.

Thus for the case of Austria, the relevant costs have been calculated as presented in Table 9.

Table 9.

Production cost of hydrogen.

3.2.2. Greece

The electricity prices for industrial customers in Greece vary according to: (1) grid connection status (low, medium, or high voltage), (2) the required maximum capacity, and (3) the usage factor (low or high). Currently, there are no provisions related to lower electricity prices for the operation of the electrolyzers in time periods and areas with excess renewable energy production and high curtailments in the regulatory framework of the country. The only exemption to that is the existence of specific provisions and high feed-in tariffs for selling electrical energy from hybrid power stations (combined RES and energy storage installations, which may include hydrogen as a storage medium) back to the grid. The feed-in tariff mentioned from the energy storage installations above, could reach up to 250€/MWh.

Therefore, Greece cannot be considered currently as a member state with a high market potential for power to hydrogen applications, with the potential exception of re-electrification systems in the autonomous, non-interconnected to the mainland grid, islands of the country.

To provide an idea of the electricity costs for industrial electrolyzers for the country of Greece, the so-called BY pricing invoice of the Public Power Corporation (PPC) is presented in Table 10. This electricity pricing invoice is directed to commercial and industrial end-users at medium voltage, having a high usage factor of electrical energy.

Table 10.

BY electricity pricing invoice of the Public Power Corporation (PPC) in Greece (www.dei.gr, last accessed at 5 January 2022).

On top of the electricity prices related to the production and procurement of electrical energy, PPC pricing invoices have also regulated charges, which are presented in Table 11.

Table 11.

BY regulated charges invoice of the Public Power Corporation (PPC) in Greece (www.dei.gr, last accessed at 5 January 2022).

4. Business Climate for Grid Balancing/Current Markets for Pressurized Alkaline Electrolyzers in Europe

In the following paragraphs, the overall business climate for pressurized alkaline electrolyzers and the potential end-users for hydrogen per each application sector will be presented. This analysis is a significant part of the overall market potential assessment, since it identifies the target market groups and specific potential applications. The business climate analysis for grid balancing and all the above-mentioned components will be described in detail and categorized per application in the following sectors.

The versatility of hydrogen applications is the strongest advantage, since it can be used as a fuel, can be injected to the natural gas grid, can be used as an industrial gas in many processes, provides an ideal solution for clean transport, and can be re-electrified in fuel cells to produce power again. Moreover, hydrogen produced from electrolysis is an excellent medium to provide grid services and balancing and produce additional revenues.

The business climate for hydrogen production through water electrolysis to contribute to grid balancing was analyzed in detail in the “Study on early business cases for H2 in energy storage and more broadly power to H2 applications” prepared by TRACTEBEL and Hinicio, which was funded by the Fuel Cells and Hydrogen Joint Undertaking (FCH JU) and supported by the European Commission [4].

The basic conclusion of the above-mentioned study was that power to hydrogen is bankable already today. It has been concluded that the estimated cumulative electrolyzer capacity to be installed in Europe by 2025 is in the order of 2.8 GW. This estimation is based on sound economics and represents a total market value of €4.2 bn. Even today, the total amount of profitable business cases in the field would be in the order of 1.4. GW, with a market value of €2.6 bn, if all these cases were realized.

As was already described in the previous paragraph, the critical factor for the economic viability of such an investment is the price of electricity. According to this study, a total (baseload) electricity price in the order of 40–50€/MWh is required to build a profitable business case. This price includes the total cost of electricity needed to drive the electrolyzer, grid fees, all taxes and levies.

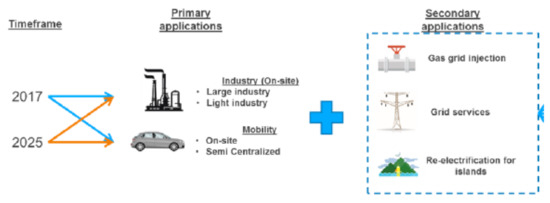

The most effective method to achieve profitability is to combine several revenue streams from different market applications that will be described in more detail in the next paragraphs. In European areas that have access to discounted electricity prices through valorization of local curtailed renewable electricity, the most bankable business cases identified for the short- and medium-term include mobility and industry as primary applications. These include regional hydrogen mobility, refineries and cooking oil production, complemented by hydrogen injection to the natural gas grid. The payback time of the identified business cases varies from 3 to 11 years, depending on the primary application. The primary success condition is a gas grid injection tariff of at least 90 €/MWh LHV.

The refinery business case is the only one that is not identified as profitable (as a stand-alone application) in the study. To bring this business case to breakeven today, a subsidy of at least 10% on capital investment costs would be required.

One of the basic conclusion of the study was that business cases that are based in single primary applications (selling hydrogen to industrial or mobility applications) will have good chances of profitability, but with higher payback periods compared to business cases that combine multiple revenue streams. The bankability of such an application will be improved when including revenues from the provision of services to balance and improve the quality of grid frequency to the power system (frequency containment and/or restoration reserves). Such an approach contributes in decreasing payback times as well. These services, even though representing a relatively small share of the total revenues of the investment (between 10% and 30%), also have a sizeable and positive effect on net margin (+40 to +80%), since the additional cost needed to provide grid services is relatively low. The impact of including grid frequency/balancing services to the investment payback time is a reduction, ranging between 30 and 50%, and more specifically from 4–11 years, down to 3–8 years.

In Table 12, the profitability results for the three best short-term business cases assessed in the context of this study are presented.

Table 12.

Profitability results of the three best short-term business cases of the study [4].

4.1. Power to Gas

This business case refers to the production of hydrogen through water electrolysis and its injection to the natural gas grid. This concept was first tested in small-scale in the last two decades. Currently, it is characterized as a secondary value stream, since it is considered insufficient to drive a solid business case on its own, but it can turn out to be very useful in creating opportunities to stack additional revenues on top of a primary value stream at very low marginal cost, resulting in a significant increase of the profitability of the investment.

Gas injection to the grid is an energy storage method and is being characterized as a large-scale application. In addition, this is a pathway for long-term storage of excess renewable electricity. The basic advantage of gas grid injection lies in the fact that no additional investments in infrastructure are required, since the already existing natural gas grid can be used for storage and as a transport medium for hydrogen as well. This method can therefore be applied in order to both store and transport very large quantities of excess renewable energy, which in several cases occur on a seasonal basis, over long distances, without introducing a need for building new connectors.

This energy storage method is being seriously examined in Germany, where large quantities of excess wind energy (produced in the north) that cannot be absorbed by the electricity grid of the country, cannot be easily transferred to the consumption centers of the south due to line congestion. The result of this situation is wind energy curtailment at a very high percentage. Of course, it can be easily understood that batteries are not an option for large-scale and long-term energy storage of the excess wind energy. Moreover, the construction of new electricity distribution lines is extremely challenging in terms of cost and public acceptance. Energy storage in hydrogen, followed by its injection to the natural gas grid is a potential solution to the above-mentioned problems.

As described above, the power to gas option has theoretically several advantages, but specific issues related to economic and regulatory matters should be solved in order to become a solid business case. In more detail, there is one barrier related to a regulatory limitation on the maximum hydrogen percentage that can be injected to the natural gas grid. There are also technical limits for specific natural gas end-users, the processes of which are not tolerant to high hydrogen content in the NG. The production of synthetic natural gas through methanation is a potential solution to overcome the limitations on maximum hydrogen content injected to the grid, but this option is associated with the introduction of additional costs and makes this business case economically unattractive.

The economic analysis of this study concluded that the power to gas option is not attractive, since without any kind of support or subsidies, the cost of hydrogen injected is comparable to the natural gas delivered by the pipeline. Therefore, in order to build solid power to gas business cases, specific instruments should be introduced. There are two options:

- A feed-in tariff (or injection tariff) scheme for green hydrogen, which can operate on principles, which are similar to the scheme that already exists in several countries for biomethane. Currently, such a scheme does not exist for green hydrogen or low carbon hydrogen in any European country.

- A carbon price that would apply (among others) as a tax on natural gas. Such a provision would help in reducing the cost between these two gases (natural gas and hydrogen).

The first option of introducing feed-in tariffs for green hydrogen, is considered to be the most probable action in the short- to medium-term.

As a conclusion, the power to gas market option will have to be handled as a secondary value stream to build a successful and profitable business case. Until, the above regulatory, technical, and economic barriers are removed through modifications in the existing support policies (and mainly by introducing a green hydrogen feed-in tariff), this will not be a solid and profitable stand-alone business case for hydrogen producers through water electrolysis.

4.2. Power to Mobility

This is the second option/business case for hydrogen produced from water electrolysis, providing grid services/balancing. Using hydrogen in the mobility sector to contribute to greenhouse gases emissions reductions is an emerging market, the development of which requires additional refueling infrastructure. It is considered as a primary application, having good chances of profitability, but with higher payback periods of time as a stand-alone value stream. When combined with other methods of commercial exploitation of hydrogen (including power to gas), the payback time of the investment will significantly reduce.

The critical factor for the economic viability of the value stream of this application is the end-users acceptable final price of hydrogen. One basic assumption of this study was that the end-user will accept to pay a final price that is at least equal to the current cost of fossil fuels/km.

The end-user acceptance price is very important in order to calculate the price at which hydrogen will be provided by hydrogen producers through electrolysis to the owners of hydrogen refueling stations (HRS), taking also into account the costs and profit margin of HRS operators. In this analysis, hydrogen is taken into account as tax-free in the short-term, as a policy to promote low and zero emission mobility.

In Table 13, the HRS operator acceptance prices per each mobility application are presented. This calculation has been based on specific reference boundary conditions, namely:

Table 13.

Acceptable hydrogen prices to end-users and HRS operators per mobile application [4].

- Typical fleet consumption of hydrogen (daily, weekly, monthly, and annually)

- Constraints that impact the operation of the electrolyzer and available storage tank

- Typical requirements of HRS

- Ranges for acceptable hydrogen prices

The results of these calculations demonstrated that the acceptable prices of hydrogen for HRS operators ranges between 4–7 €/kg, depending on each mobility application. The cost margin for HRS operators ranges from 40 to 100%.

As a conclusion, the power to mobility market option should be handled as a primary value stream to build a successful and profitable business case. In order to maximize revenues and reduce significantly payback times, this business case should be (at least in the short-term) combined with one or more other applications (primary or secondary), such as power to gas, power to power, or power to industry in order to come up with an attractive business case from the financial point of view.

4.3. Power to Industry

The third option/business case for hydrogen produced from water electrolysis, providing grid services/balancing is the one of selling hydrogen as a chemical in order to be used in industrial applications. The usage of hydrogen in industry can be divided into large and light applications depending on their hydrogen consumption volume. Large industry typically includes refineries, chemical plants, and steel manufacture characterized by a very large quantity of hydrogen consumption (over 10,000 Nm3/hr). In these applications, hydrogen is supplied either by steam methane reforming (SMR) or by pipelines available in specific countries. On the other hand, light industrial applications are supplied by hydrogen either through trucks or small-scale SMR units. In industrial applications, hydrogen is used as a chemical required in the processes of the various categories of plants.

The power to industry business case is characterized as a primary value stream that has good chances for creating profitability, but when used as a stand-alone end-user, results in higher payback periods of time. Therefore, a better economic viability for this application can be achieved by combining this application of hydrogen produced from water electrolyzers with additional value streams in order to reduce payback times and increase profitability.

In general, hydrogen required for large-scale industrial applications (especially in refineries) is produced through SMR at significantly lower costs compared to hydrogen produced from electrolysis. Unless, specific decarbonization policies are enforced in order to promote green hydrogen through subsidies, this business case will not be profitable for hydrogen producers using electrolyzers.

On the other hand, hydrogen required for light industrial applications could be a viable business case/value stream dependent on the specific conditions and the industrial sites locations. In more detail, in the context of the above-mentioned study, it has been concluded that in Denmark and France [36], there is a high potential for introducing hydrogen produced from electrolysis in light industry applications, due to high distances from any filling center and the low competitive environment and high price of trucked in hydrogen. Similar favorable conditions for this value stream can also be found in other European areas.

As a conclusion, the power to industry market option should be handled as a primary value stream to build a successful and profitable business case. It is evident that light industry applications come up with a higher profitability for hydrogen producers through water electrolysis. In order to maximize revenues and reduce significantly payback times, this business case should be (at least in the short-term) combined with one or more other applications (primary or secondary), such as power to gas, power to power, or power to gas in order to come up with an attractive business case from the financial point of view.

4.4. Power to Power (Re-Electrification of Hydrogen)

The fourth option/business case for hydrogen produced from water electrolysis is producing energy in fuel cells driven by the previously stored hydrogen and selling it back to the electricity grid. Non-interconnected islands, where electricity is currently produced by diesel or heavy oil are the best locations for hydrogen re-electrification, since the cost of energy produced in these systems is already high.

Power to power business case should be combined with provision of grid services (combined grid balancing and frequency control) to have an additional income and make this application more economically attractive and profitable. Nevertheless, it should be noted that in almost all European countries, there is not a regulatory provision for capacity payments for frequency containment.

From the financial point of view, the power to power option is stronger in small autonomous island systems that present an already high cost. It has been estimated that this business case becomes viable in island systems that present a power generation cost over 200–250 €/MWh, depending also on the availability of wind and solar potential. This option will highly contribute in the increase of renewable energy penetration in the weak electricity grids of islands and its decarbonization. The main competitor here, is batteries, but the power to power business case provides the advantage of seasonal energy storage.

As a conclusion, the power to power market option should be considered in the short-term for small-size, non-interconnected islands with already high power generation costs. Power to produce hydrogen through the electrolyzer should be provided by renewables (excess electricity that cannot be absorbed by the grid). To achieve profitability, this business case should be combined with the provision of grid services (grid balancing and frequency control) to maximize revenues and come up with an attractive investment.

4.5. Grid Services Provision

The fifth option/business case for hydrogen produced from water electrolysis is the provision of grid services by the owner of the electrolyzer (hydrogen producer). This is a secondary value stream, since it cannot provide a profitable business case as a stand-alone application and should be considered as an additional income source, combined with a primary application. A water electrolyzer could potentially provide the following grid services to transmission and distribution operators:

- Balancing and management of congestion (transmission grid at national level).

- Frequency containment services for increased stability of the electricity network (at transmission grid and also includes enhanced frequency reserve service type).

- Distribution grid services: these services are not as mature as services at the transmission level. The value of the distribution grid should be assessed by taking into account the respective CAPEX and OPEX, which can be avoided due to the operation of the electrolyzer (load shifting activation).

The revenues produced from the operation of an electrolyzer and its flexibility to provide grid services in each of the above-described categories are depicted in the following paragraphs:

- Balancing services: In cases where hydrogen production targets are clearly set for the electrolyzer over time periods, such as a week, while maintaining a spare capacity, it allows an electrolyzer to provide load shifting (meaning additional flexibility) for balancing services. Therefore, it could adopt its consumption to renewable energy variation. The analysis conducted in the context of this study, showed that the revenues of an electrolyzer providing balancing services vary according to the operation scenario. In Figure 5, the expected revenues for a 1 MW electrolyzer providing balancing services for a number of case studies in different EU member states and different activation costs are presented.

Figure 5. Balancing services expected annual revenues for a 1 MW electrolyzer with 3 activation costs [4].

Figure 5. Balancing services expected annual revenues for a 1 MW electrolyzer with 3 activation costs [4].

- Load frequency control: There is a great differentiation in the terms of regulation and remuneration related to ancillary services for load-frequency control across EU member states, therefore the revenue expected from this application/business case of hydrogen produced through electrolysis differ greatly.

- Distribution grid services: In the context of the above-mentioned study, specific simulations were realized, in order to calculate the profitability of this business case. The key results of this assessment indicated that the income linked to the flexibility provided by the electrolyzer are very low, since the electricity networks need to be reinforced to install the electrolyzer (which results in an additional capital cost), while this added value of its flexibility lies in postponing reinforcement investments. The calculations showed that the expected income from such an operation of the electrolyzer will be lower than 1 k€/MW/yr (annualized over the lifetime of the electrolyzer).

As a conclusion, the grid services provision market option should be handled as a secondary value stream to build successful and profitable business cases. It is evident that provision of grid services (balancing services, load frequency control, and distribution grid services) for hydrogen producers through water electrolysis should be combined with at least one other business case/application of hydrogen, such as power to mobility, power to industry, or power to gas. Such an approach would result in creating a more attractive and profitable business case for hydrogen producers.

4.6. Power to Heat

Power to Heat application of hydrogen is sometimes overlooked due to the low overall efficiency of the process of producing hydrogen through electrolyzers using renewable electricity and then using hydrogen in H2 burners in order to produce heat. This application has the disadvantage of needing additional infrastructure, mainly for the hydrogen burner, therefore it is usually less profitable compared to natural gas grid injection. Nevertheless, in specific cases, power to heat applications could turn into solid and profitable business cases. The main end-user of this application would be light industrial applications with high heating demand. The most important critical factors for the economic viability of this business case are: (1) cost of electricity, (2) distance from the end-user, and (3) current cost of natural gas of the industrial users.

In cases of proximity of the industry to the hydrogen producer, low cost of electricity to produce hydrogen and high natural gas prices, the business case of power to heat gas has a good chance to become a viable and profitable investment. To increase income and profitability, it should be combined.

As a conclusion, the power to heat market option could become viable as a light industry application when the following conditions exist: (1) proximity of the industry to the hydrogen producer, (2) low cost of electricity to produce hydrogen, (3) high heating demand, and (4) high natural gas prices. It is evident that for power to heat applications to become profitable for hydrogen producers through water electrolysis, it should be combined with at least one other business case/application of hydrogen, such as power to mobility, or provision of grid services. Such an approach would result in creating a more attractive and profitable business case for hydrogen producers.

4.7. List of at Least Ten Market Opportunities at the EU Level

Following the analysis of business climate and current potential markets for the application of pressurized alkaline electrolyzers in providing grid balancing services, the following market opportunities have been identified:

- Power to gas application in northern Germany: Although power to gas applications are considered as a secondary value stream (due to the existing regulatory and legislative frameworks all over Europe), a solid application/business case of a pressurized alkaline electrolyzer for this scope can be set up in northern Germany due to the high percentage of wind energy curtailments in the area. A significant market opportunity can be created in this area of Europe, which will be facilitated by the fact that several demonstration projects in this field have been already realized in the last two decades, resulting in the acquisition of high-level experience for scaling it up.

- Power to mobility application MPREIS (Austria): This project has already taken a strategic decision to replace a good part of its fossil-fuel-driven vehicles with hydrogen ones. In addition, the company has already decided to install a pressurized alkaline electrolyzer to produce hydrogen that will be fed in a Hydrogen Refueling Station (HRS) to support its new hydrogen vehicle fleet. As analyzed above, the power to mobility business case is considered as a primary value stream and will most probably be a profitable business case as well. Moreover, such a large-scale introduction of hydrogen technologies in the transport sector will facilitate a wider use of hydrogen vehicles in commercial applications (heavy duty trucks) in Austria.

- Power to mobility applications in Innsbruck region (Austria): The region of Innsbruck is one of the ones showing a high penetration of hydrogen vehicles. Hydrogen refueling stations (HRS) are also located in this area. Therefore, it is sensible to identify a market opportunity for pressurized alkaline electrolyzers in this location and this application, which will be higher in the next years, when the penetration of hydrogen vehicles will be higher.

- Power to mobility application in AB Vasilopoulos logistic center in Greece: Logistic centers are considered one of the best markets for the commercial introduction of hydrogen technologies, including hydrogen production through pressurized alkaline electrolyzers. One of the largest supermarket chains in Greece, namely AB Vasilopoulos, are interested in creating the hydrogen production infrastructure required in order to substitute part of their battery electric forklift vehicles with hydrogen ones in their main logistics center.