2.1. Definition and Identification of Dual Attributes of Oil

The financial attribute of oil is highly related to the financialization of the international crude oil market. The development of oil financial derivatives such as crude oil futures has become the main force to promote the financialization of the international crude oil market. The international crude oil market and financial market have been closely combined. Oil can no longer be simply regarded as a commodity, but a composite commodity with the characteristics of financial products [

38]. Specifically, the shortening of the period of price fluctuation and the increase of fluctuation range in the international crude oil market are the manifestations of oil financial attributes [

39]. Secondly, the development of the oil derivatives financial market, such as markets of international crude oil futures, oil options, forward and swap, makes oil price indexation gradually. The pricing power of crude oil has not only become the strategic goal of national and regional competition, but also the key indicator of investors’ judgment of market information [

40,

41,

42]. In addition, the inflow of financial assets into the international crude oil market increases the volatility and risk of oil prices. At the same time, considering the negative relationship between the international crude oil market and the financial market, the price fluctuation and risk not only reflect changes in investors’ expectations, but also be infected by the risk of the financial market. Based on this, this paper defines the financial attribute of oil as: the formation and fluctuation of international crude oil market prices have the basic characteristics of financial products and can play a role in the financial market. In essence, the financial attribute of oil refers to the use of various oil financial derivatives by oil investment groups, driven by the dollar exchange rate, crude oil speculation and other financial factors, so that international crude oil prices reflect more the will of financial institutions such as speculative groups.

The financial attribute of oil determines that the price of the international crude oil market is positively affected by monetary policy. On the one hand, monetary policy is a key factor for the dollar exchange rate to influence or even manipulate international oil prices [

40,

41]. On the other hand, monetary policy creates opportunities for hedgers and speculators to profit from the international crude oil market. The impact of monetary policy on international crude oil market prices is mainly due to changes in speculative demand [

39,

43]. As a demand regulation policy, expansionary monetary policy will increase the demand for oil, reduce the uncertainty of the international crude oil market, and release good news for investors. Investors’ mastery of the news enhances their optimistic expectations, and then changes the allocation of investors’ funds in real investment and financial investment, and the speculative demand increases accordingly [

44]. Therefore, good news leads to the rise in the price of oil financial derivatives, and ultimately affects the spot price of the international crude oil market. On the contrary, tightening monetary policy increases the uncertainty of investment in the international crude oil market, which leads to the change of investors’ expectations and the decline of speculative demand, resulting in the decline of oil financial derivatives prices [

45]. Due to the important role of oil financial derivatives in price discovery, hedging and risk aversion, the spot price of the international crude oil market has also changed accordingly.

Based on the above analysis, this paper puts forward the basic hypothesis of oil financial attribute identification

Hypothesis 1 (H1). The financial attribute of oil is related to the positive impact of monetary policy on international crude oil prices.

The particularity of oil commodity determines its commodity attribute. As a key input commodity in production activities, oil has three remarkable characteristics besides the characteristics of general commodities. The first characteristic is scarcity. Oil is a kind of non-renewable energy, which has certain restrictions on exploitation and storage. Due to the fact that oil is not enough to meet the long-term dependence of human development on oil, so the primary characteristic of oil is scarcity. At the same time, the increasing dependence of economic development on oil increases the demand for oil and further affects the oil supply. Second, oil has a strategic characteristic. As the most important input factor, oil has penetrated into different fields of economic development, so the dependence of economic development on oil is formed, and this dependence varies in different stages of the economic cycle. Therefore, different countries and regions regard the control of different links of oil as an important strategy. Third, oil has a political feature. The uneven distribution of oil supply and the difference in oil demand among countries and regions determine that oil has political characteristics. In particular, the reserves and production of oil resources are concentrated in the Middle East, Africa, South America and Canada. On the contrary, countries with high oil demand have no regional aggregation characteristics, including developed countries such as the United States, Europe and Japan, and developing countries such as China and India. This uneven global distribution of oil supply and demand has made oil political. Based on this, this paper defines the commodity attribute of oil as: the change of oil price is affected by the change of the market’s supply and demand relationship to a certain extent. In essence, the commodity attribute of oil refers to that the international crude oil price gradually reflects the characteristics of production cost and supply–demand balance conversion, which are affected by the oil use cost of enterprises, oil production capacity, national oil demand and energy strategic reserves.

The identification of oil’s commodity attribute is related to the positive impact of crude oil demand on international crude oil market price. The supply structure of the international crude oil market has evolved from the original OPEC countries as the main body to the present OPEC rich countries group, OPEC poor countries group and non-OPEC countries three main bodies [

15,

46]. Based on this supply structure, OPEC combined with market demand to further put forward the oil price range pricing mechanism. Yet because of differences in oil production reserves, idle capacity, and extraction costs within OPEC countries, OPEC not being a cartel, they can only act as recipients rather than setters of international oil prices [

47]. In reality, the scarcity of oil determines the high uncertainty of oil reserves in the future. Supply is inelastic in the short term, and OPEC has a lag effect on the regulation of oil supply, so the international crude oil market price is affected by demand in the short term [

46,

48]. The demand for crude oil is usually correlated with the total demand of the national economy. When the economy is in a boom, crude oil demand increases with the increase of total social demand. At this time, the price of the international crude oil market will inevitably rise, under the condition of constant supply in the short term. Conversely, when the economy is in a depression, the total social demand is weak and the demand for oil decreases, which will reduce the price of the international crude oil market [

49,

50]. In the long run, the supply of crude oil is more elastic. However, as oil is a non-renewable resource, the storage capacity, resource endowment, production cost, production capacity and OPEC’s decision will limit the supply of crude oil [

48]. To sum up, in the long term, the price change of the international crude oil market is also mainly affected by the positive impact of oil demand.

Based on the above analysis, this paper puts forward the basic hypothesis of oil commodity attribute identification:

Hypothesis 2 (H2). The commodity attribute of oil is related to the positive impact of oil demand on international crude oil price.

2.2. Model Selection of the Oil Dual Attributes Identification

There is an endogenous relationship between international crude oil market price and monetary policy as well as oil demand. First, the above analysis made it clear that monetary policy and oil demand have positive impacts on the international crude oil price. Second, the change of international oil price will change the production cost of enterprises, and then make the oil demand change. Changes in international oil prices will also affect a country’s inflation level. As one of the objectives of monetary policy, in order to maintain price stability, the country will formulate corresponding monetary policy to adjust the inflation level, so the price of the international crude oil market will also affect monetary policy [

9]. Therefore, there is an endogenous relationship between international crude oil market price and monetary policy as well as oil demand, which cannot be fully described by traditional linear models. Hence, this paper considers building a series of VAR models. Moreover, taking into account the immediate impact of international crude oil price, oil demand and monetary policy, as well as the description of structural shocks on the correlation, this paper attempts to construct the SVAR model to identify the dual attributes of oil by imitating the practice of Kilian [

51].

A basic form of the SVAR (p) model is constructed as Equation (1):

where

is a 3 × 3 vector;

is the international crude oil market price at time t;

refers to the oil demand at time t;

represents the monetary policy at time t; p is the lag order, identified by the SC criterion;

describes the immediate impact between international crude oil market price, oil demand as well as monetary policy, and

describes the marginal impact of lagging order i in the same way.

Since

is reversible, Equation (1) can be simplified to Equation (2):

where

is the structural vector of shocks on international oil price, including the specific oil price shock, the demand shock and the monetary policy shock.

Combined with the purpose of this paper and the existing literature, this paper imposes short-term zero constraints on the immediate impact matrix

and constructs the SVAR model. Specific constraint matrix is shown in (3):

The corresponding position in the matrix represents the immediate impact between variables. Specifically, international crude oil price responds to oil demand and monetary policy shocks, so except that the first element in the first row of the constraint matrix is 1, the other elements are not 0. Although oil is the main raw material and fuel in global economic activities, yet when oil prices change, the impulse of oil demand to international crude oil price lags behind due to enterprise investment planning and oil reserves, that is, oil price shocks do not affect current oil demand, . In addition, changes in international oil prices and oil demand will not cause changes in monetary policy, i.e., , while the change of monetary policy will cause the change of oil demand in the current period.

The variables in this paper include three variables of international crude oil market price, oil demand and monetary policy. This paper uses Brent oil spot price as a proxy variable of international crude oil market price. The change of spot price of Brent and WTI crude oil can reflect the evolution characteristics of international crude oil market price. Since 2011, with the change of crude oil market mining costs, idle capacity and other factors, the international crude oil industry has gradually shifted to Western Europe, and Brent also gradually surpassed the WTI market to become the benchmark of the international crude oil market. Thus, this paper selects the spot price of Brent to measure the international crude oil price.

Oil demand is measured by the growth rate of the Baltic dry bulk freight index (BDI). The change of oil demand is highly related to economic demand, and the demand for oil increases during the economic boom, and then the price of the international crude oil market shows an upward trend, whereas the demand for oil decreases during the economic depression. Therefore, two problems should be considered in the selection of the oil demand measurement index. First, the difference in the industrial structure of different countries makes the dependence of economic development on oil different from each other. Second, the contribution of emerging countries such as BRICS in global economic development makes oil demand a key factor affecting the price change of the international crude oil market. By imitating Kilian [

51] and considering the close relationship between the shipping index and oil demand, this paper selects the BDI as the proxy variable of oil demand.

This paper selects the global money supply to measure monetary policy. Based on the availability of data, this paper uses the sum of money supply in three countries or regions, i.e., the United States, Japan and the European Union, to quantify the global money supply. All the above data are from the Wind database. After acquiring the money supply of each country, we use the historical bilateral exchange rate data to convert them into US dollars and then aggregate them, and finally get the value of the monetary policy proxy variable. Monthly data from April 2003 to October 2020 are adopted in this empirical analysis. Central Bank of Japan first announced money supply M2 in April 2003. Although the time duration is short, yet the result can reflect the dynamic characteristics of the dominant oil attribute. In addition, considering the seasonal effects of variables, this paper employs X12 to adjust international crude oil price, BDI and money supply (GM2) seasonally. To eliminate heteroscedasticity, this paper further implements logarithmic processing for data.

2.3. Dynamic Characteristics Analysis of Dual Attributes of Oil

Based on the model test results (see

Appendix A), this paper uses first-order differential variables of Brent, BDI and GM2 to fit the SVAR model (1) to identify the dynamic characteristics of different attributes of oil. According to the basic hypotheses, the dynamic identification of oil dual attributes mainly includes two aspects: one is to identify the existence of oil commodity and financial attributes; two is to identify the dynamic characteristics of oil dual attributes. Based on this, this part first analyzes the existence of oil commodity and financial attributes with the impulse test, and finally analyzes their dynamic characteristics according to the correlation between structural shocks.

As can be seen from

Figure 2, crude oil demand and money supply have a significant positive impact on international crude oil market price.

Figure 2 displays the impulse response of international crude oil market price to crude oil demand (BDI) and monetary policy (M2) respectively.

Figure 2a is the impulse response of the change of crude oil demand to the international crude oil market price, and

Figure 2b is the impulse response of the change of money supply to the international crude oil market price, indicating that the positive impact of crude oil demand and monetary policy on international crude oil price shows the existence of oil commodity attribute and financial attribute. Specifically, the impact of crude oil demand and monetary policy on the international crude oil price is positive, and this positive impact reaches the maximum when the lag period is 2, and the impact is basically zero when the lag period is 5. On the one hand, these results show that oil has dual attributes of commodity and finance. According to Hypothesis 1, the financial attribute of oil is related to the positive impact of monetary policy. This is mainly because the change of monetary policy will affect the driving role of financial factors such as US dollar exchange rate and crude oil asset speculation in the change of international crude oil price, thus forming the financial attribute of oil [

38,

40].

The commodity attribute of oil is related to the positive impact of crude oil demand. The evolution of the supply structure of the oil market, from the original OPEC countries as the main body to the present three main bodies of OPEC rich countries, OPEC poor countries and non-OPEC countries, has affected the supply of crude oil and weakened the pricing power of OPEC on the international crude oil market [

47]. Affected by factors such as alternative energy, if oil prices are expected to rise, or future technological progress is expected to improve production efficiency and reduce production costs, oil-producing countries may delay oil production or reduce the existing production scale. The difference of long-term and short-term effects of supply and demand elasticity on international crude oil price also makes crude oil demand a key factor in international oil price fluctuation. Oil reserves always change with oil exploration activities around the world, which leads to uncertainty in future oil reserves. As a result, the supply is inelastic in the short term, and the adjustment of OPEC oil supply has a lag effect, so the international crude oil market price is affected by the demand in the short term. In the long run, crude oil supply elasticity is relatively large, but since oil is a non-renewable resource, its storage capacity, resource endowment, exploitation cost, extraction capacity and OPEC resolution will limit the supply of crude oil [

9,

10]. Therefore, in the long run, the price change of the international crude oil market is mainly affected by the demand for oil. In conclusion, Hypotheses 1 and 2 hold.

On the other hand, the responses of the international crude oil market to changes in oil demand and monetary policy are similar, and the similarity is related to the source of the shock. The impact of crude oil demand on the international crude oil market price is mainly affected by the external environmental changes such as technological progress, economic development and alternative energy; while the impact of monetary policy on the international crude oil market is mainly highly related to the external environment such as exchange rate fluctuations, capital flows, investor expectations and speculation [

45,

52]. This similarity not only illustrates the dynamic characteristics of oil dual attributes, but also indicates the importance of using the correlation between structural shocks to judge the dynamic characteristics. Under the influence of uncertain factors such as technological progress and financial market investment, entity enterprises and oil investment groups will adjust their investment strategies according to the changes of external environment to ensure their expected profits, leading to the alternation of the dominant periods of oil commercial attribute and financial attribute in the formation of international crude oil price. However, since they are all positive shocks with different impact scales, structural shocks can better describe the main roles of different variables in the market, and the correlation direction of structural shocks indicates the contribution of crude oil demand or monetary policy to the price changes in the international crude oil market. Therefore, this part further analyzes the dynamic alternation characteristics of oil commodity attributes and financial attributes.

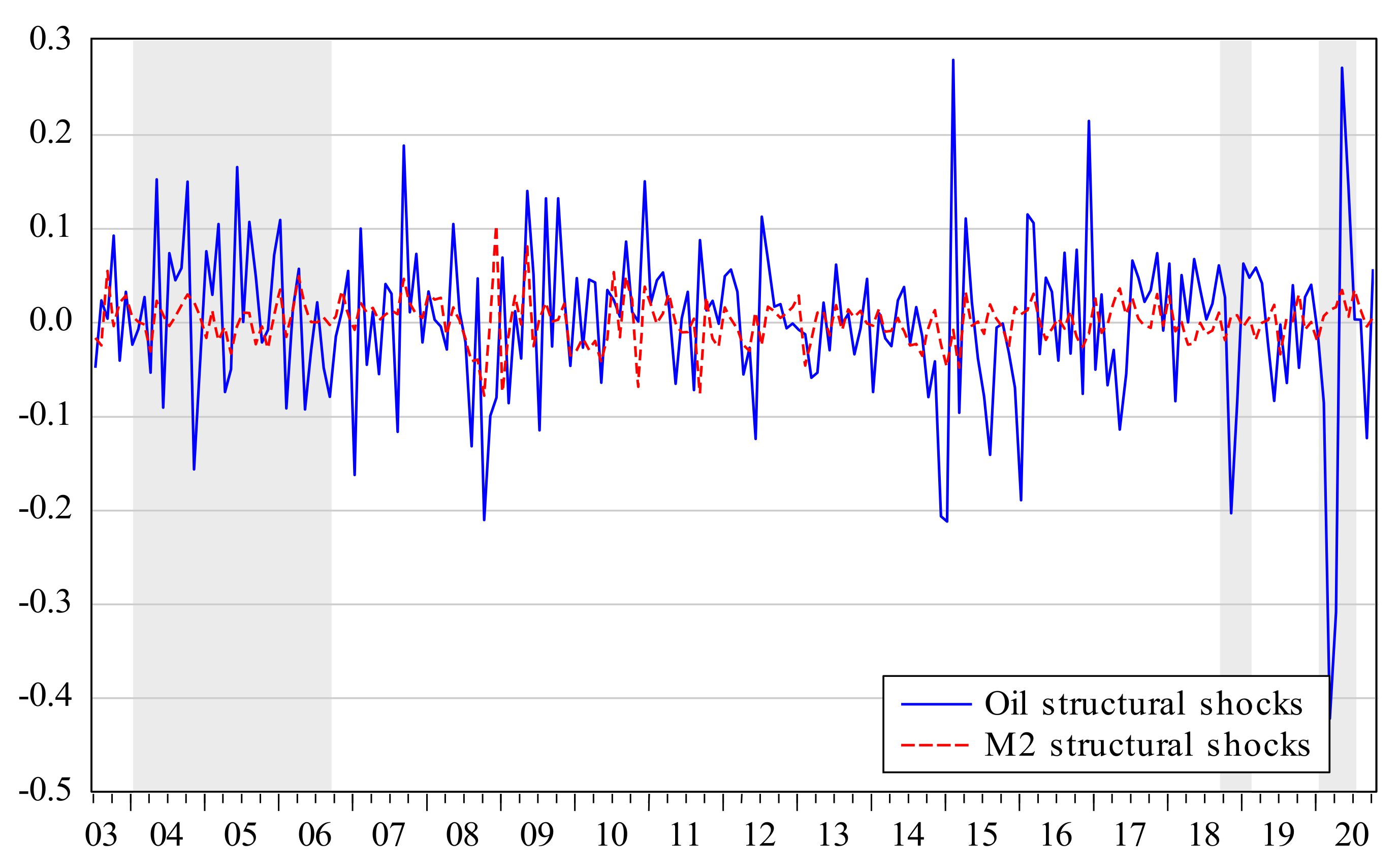

The dominant position of oil commodity attribute and financial attribute has dynamic characteristics.

Figure 3 and

Figure 4 show the dynamic feature identification of oil commodity and financial attributes, respectively. In this paper, the identification is from two aspects. On the one hand, it can be seen that crude oil demand and the structural shock of crude oil price basically change in the same direction, except for the periods of 2006M07–2007M03, 2011M12–2013M04, 2015M05–2015M12, 2019M02–2019M09, and 2020M01–2020M06. Monetary policy and the structural shock of crude oil price also change in the same direction, except for the periods of 2004M01–2006M09, 2018M09–2019M02, 2020M01–2020M07. On the other hand, in order to further compare and analyze the dynamic characteristics of the dual attributes of oil in the sample period except for the above-mentioned periods, this paper identifies whether the changing direction is positive or negative. For example, in the second half of 2003, there is a positive relationship between the shock of crude oil price and the shock of crude oil demand, so is the relationship between the shock of monetary policy and the shock of crude oil price, but the shock of monetary policy on the international crude oil price is lagging behind. This shows that the change of international crude oil price is mainly affected by the spot demand of oil, while the influence of monetary policy is lagging behind, that is, the fluctuation of international crude oil price is mainly regulated by the relationship between market supply and demand. Therefore, at this time, the oil commodity attribute dominates. From the second half of 2007 to the beginning of 2008, although the oil demand shock is positively related to the international crude oil market price shock, the shock direction is negative, while the monetary policy shock is positively related to the international crude oil market price shock, and the shock direction is positive. This indicates that the financialization of commodity markets has gradually formed, and a large amount of oil has entered the reserve field as investment or even speculation instead of entering the production field. Therefore, the oil financial attribute occupies the dominant position at this time. The same happened since July 2020. To sum up, this paper obtains the stage characteristics dominated by the dual attributes of oil as shown in

Table 1.

The dominant stages of oil financial attribute and commodity attribute are different, and there are joint domination periods.

Table 1 shows that the dominant periods of oil financial attributes are mostly before and after special events. Specifically, the oil financial attribute dominates six stages of 2006.9–2007.3, 2007.7–2007.12, 2011.12–2013.4, 2015.5–2015.12, 2019.2–2019.9 and 2020.7-later. The period that oil commodity attribute dominates is the stable period of the international crude oil market, including 2003.7–2006.9, 2007.3–2007.6, 2013.4–2015.5 and 2016.1–2019.2. At the same time, the time period in which the dual attributes of oil jointly dominate the international crude oil market price is related to special events: 2008.1–2011.12 and 2020.1–2020.7.

Since the second half of 2006, countries around the world have gradually established commodity markets and improved their market systems. Because of the negative relationship between commodities like crude oil and financial assets such as stocks, a growing number of investors use crude oil as a hedge to secure their own expectations or excess profits [

53,

54]. Investors can further obtain relevant information of the international crude oil market through monetary policy changes. At this time, the price changes of the international crude oil market are mainly dominated by the financial attribute of oil. However, Since the uncertainty of profits in the financial market is higher than the expected profits from investment in the real economy, and the international crude oil market gradually adjusts the price fluctuations caused by the financialization of the commodity market, the international oil price gradually stabilizes and is regulated by the market supply and demand relationship. Therefore, the commodity attribute of oil dominated from March to June 2007. In addition, since July 2020, affected by the global epidemic and the residual effect of the implementation of sanctions against Iran by developed countries such as the United States, the price of the international crude oil market is under pressure to recover. From the perspective of market stability and investor sentiment, policymakers use relevant policy tools to adjust the price of the international crude oil market, gradually improve the confidence of market participants, and then achieve the effect of stabilizing the market.

The dynamic characteristics of the dominant stages of the two attributes of oil are mainly related to the external environment. As the financialization of commodity markets deepens, more and more investors trade crude oil as a financial asset. A large amount of capital flows into the international crude oil market to further expand its degree of financialization, thus promoting the development of the oil industry in the direction of financialization [

38]. Affected by capital flows, investor expectations and speculative activities, international crude oil market prices mainly reflect the speculative will of oil investment groups. At this time, because the profit of the financial market is greater than that of the real investment, in order to pursue the expected profit or excess profit, the enterprise will change its capital allocation between finance and entity, and then the commodity attribute of oil becomes weak, and the financial attribute of oil will dominate. However, the uncertainty of profits in the financial market will make the commodity attribute of oil dominate. The international crude oil market has a regulating effect on the speculative manipulation of oil investment groups, and the investment of enterprises in the financial market will bear higher risks, which increases the uncertainty of enterprises to obtain expected profits. The change of external environment, such as economic development, technological progress and industrial structure adjustment, makes enterprises change their investment strategy. The macroeconomic improvement expands the profit space of the enterprise to invest in the real economy, and the consumption demand of oil is bound to rise; otherwise, the consumption demand of oil will be reduced. The financial attribute of oil plays a major role in price discovery in the international crude oil market. On the contrary, hedging and speculative arbitrage are obviously inadequate. The influence of monetary policy on the price of the international crude oil market is mainly reflected in changing the demand for oil consumption [

50]. At this time, the commodity attribute of oil dominates.

The joint action of two attributes of oil is highly related to special events. From 2008 to 2011, the global financial crisis caused by the subprime mortgage crisis in the United States and the European debt crisis first impacted the stability of the financial market. Due to the development of economic and financial integration, the impact gradually spilled into the commodity market and affected the smooth operation of the economy. Countries use policy tools such as monetary policies to maintain the confidence of investors in the market and the smooth operation of the economy to stimulate consumers demand and minimize the impact of the crisis on the market [

55]. Early in 2020, the outbreak of the COVID-19 epidemic posed new challenges to the effectiveness of the global health system. Affected by the epidemic, countries have taken different attitudes and measures to reduce the impact [

56]. As a result of the development of global integration, the epidemic began to spread around the world, further affecting international links such as shipping and air transportation, and ultimately affecting the development of the global economy. This effect undoubtedly creates pressure for global economic recovery. Because of the high dependence of economic development on oil and other energy sources, the international crude oil market price is impacted by oil demand. Meanwhile, the epidemic also affects the exchange of information and expectations of market participants, so the price of the international crude oil market can also be influenced by monetary policy. Therefore, the change of international crude oil price is dominated by both oil financial attributes and commodity attributes. To sum up, Hypothesis 1 and 2 holds.

There are differences in the duration characteristics of the two oil attributes.

Table 1 also reports the statistical characteristics of the duration of two oil attributes. According to

Table 1, both the maximum duration and minimum duration of international oil price jointly dominated by the two attributes of oil are the largest, which are 48 months and 7 months, respectively. The maximum duration of oil commodity attribute dominating international crude oil price is 38 months, being greater than that of oil financial attribute, which is 16 months; however, the minimum duration of oil financial attribute is greater than that of oil commodity attribute, which are 5 months and 4 months respectively. By comparing the proportion of dominant time of different attributes in the sample period, it is found that the international crude oil market price is mainly influenced by oil commodity attribute, accounting for 51%. The second is the jointly dominant time of the two attributes of oil on the international oil price, accounting for 26%. The least is the dominant time of oil’s financial attribute, accounting for 23%. Combined with the above analysis, it can be seen that the impact of special events on the international crude oil market lasts the longest, and the ability of the market to deal with special events is still a key indicator to test the stability of the market [

10]. As oil is the most important input factor, the price change of the international crude oil market is still affected by the market supply and demand relationship, especially the change of demand to a large extent. However, the impact of the financial attribute of oil on the international oil price has gradually developed into a factor that cannot be ignored in the market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}