Consumer Stock Ownership Plans (CSOPs)—The Prototype Business Model for Renewable Energy Communities

Abstract

1. Introduction

1.1. Prosumership in the 2018/19 EU Clean Energy Package

- Consumers, as prosumers, will have the right to consume, store or sell RE generated on their premises, (1) individually (Art. 21 RED II), that is, households and non-energy small and medium sized enterprises (SMEs); and collectively, for example, in tenant electricity projects, or (2) as part of RECs (Art. 22 RED II) organised as independent legal entities.

- Transposing the RED II into national law, Member States—amongst others—have until June 2021 to adopt an “enabling framework” for prosumership and, in particular, for RECs. The Directive defines citizen’s rights and duties and links prosumership to such different topics as increasing acceptance, fostering local development, fighting energy poverty, and incentivising demand-flexibility.

- “which, according to applicable national law, is based on open and voluntary participation, is autonomous, and is effectively controlled by shareholders or members that are located in the proximity of the renewable energy projects owned and developed by that community;

- whose shareholders or members are natural persons, local authorities, including municipalities, or SMEs;

- whose primary purpose is to provide environmental, economic or social community benefits for its members/the local areas where it operates rather than financial profits.”

1.2. Research Questions and Approach

- To what extent does the governance model for energy communities stipulated by the Clean Energy Package actually meet the needs of practice?

- Can the RE-CSOP and similar business models provide attractive conditions respecting both the RED II prerequisites for RECs as well as the individual needs of different types of co-investors?

2. Theory

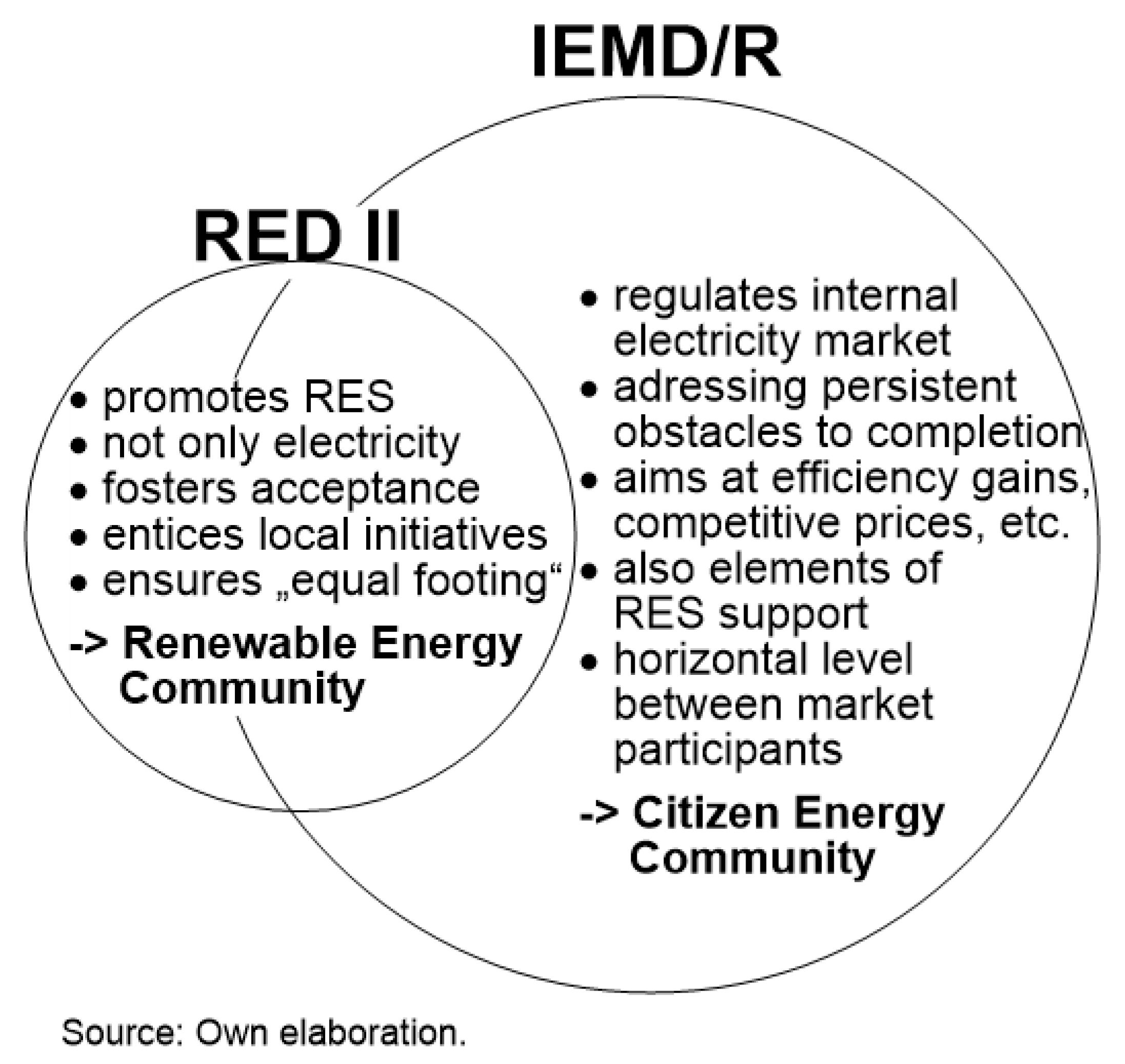

2.1. Relation of Electricity Market Directive/Regulation and Renewable Energy Directive

2.2. The New Governance Model and its Importance for RE Clusters

- Must be autonomous and independent of other RES project partners. “Autonomy” in this context should be understood as a 33% ceiling for ownership stakes of individual shareholders or members; recital 71 RED II stipulates that “REC should be capable of remaining autonomous from individual members and other traditional market actors that participate in the community as members or shareholders, or who cooperate through other means such as investment”.

- In addition, “is effectively controlled by shareholders or members that are located in the proximity of the renewable energy projects owned and developed by that community” result in a ceiling for the strategic investor’s participation of 49% (see the requirements of the definition of Art. 2 of the RED II in Section 1.1 above) or at least binding contractual arrangements that confer decisive influence on the composition, voting or decisions. Art. 2 pt. (56) IEMD defines “control” as “rights, contracts or other means which, either separately or in combination and having regard to the considerations of fact or law involved, confer the possibility of exercising decisive influence on an undertaking, in particular by: (a) ownership or the right to use all or part of the assets of an undertaking; (b) rights or contracts which confer decisive influence on the composition, voting or decisions of the organs of an undertaking”.

3. Empirical Evidence: Material, Methods and Results

- They show that in the evaluation of the 67 cases, 37 had co-investors as envisioned by the RED II for the future RECs. Although these numbers seem low they are nevertheless unsurprising as energy communities operating exclusively in RE are a recent phenomenon not yet widely implemented.

- What is more surprising is, that only 9 projects already meet RE cluster requirements while merely 22 have RE cluster potential. Many projects are of small size and do not or only to a limited extend involve flexibility, bi-directionality, interconnectivity and complementarity; but this is a condition to become fully fledged RECs that will also be able to benefit from energy sharing [15].

- Only in 20 of the 37 cases this involved genuinely heterogeneous co-investors although not all of them comply with the governance structure required by the RED II. Some projects are solely owned by one shareholder; other projects, although showing heterogeneous co-investors are dominated by commercial actors not based in the proximity of the RE installations; in yet other projects a large energy firm has a majority ownership stake violating the autonomy criterion.

- Of the remaining 17 cases that only formally comply with the heterogeneity criterion of the RED II some cases were either cooperatives exclusively with citizens as members or municipal projects without other co-investors.

- Furthermore, geographic and cultural diversity of RE projects even within a given country lead to complexities that do not permit “one size fits all” solutions. While identities and interests are often deeply rooted in geographies and cultures, organizational and contractual arrangements are a more flexible factor that can be adapted to the former two [24].

4. Presentation of the Renewable Energy Consumer Stock Ownership Plan

4.1. The Modular CSOP Approach

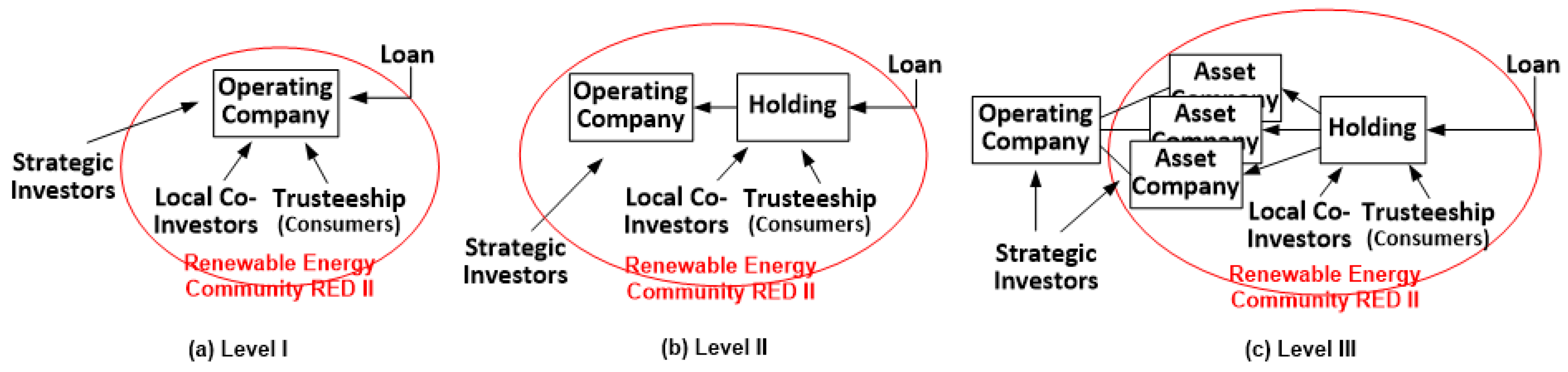

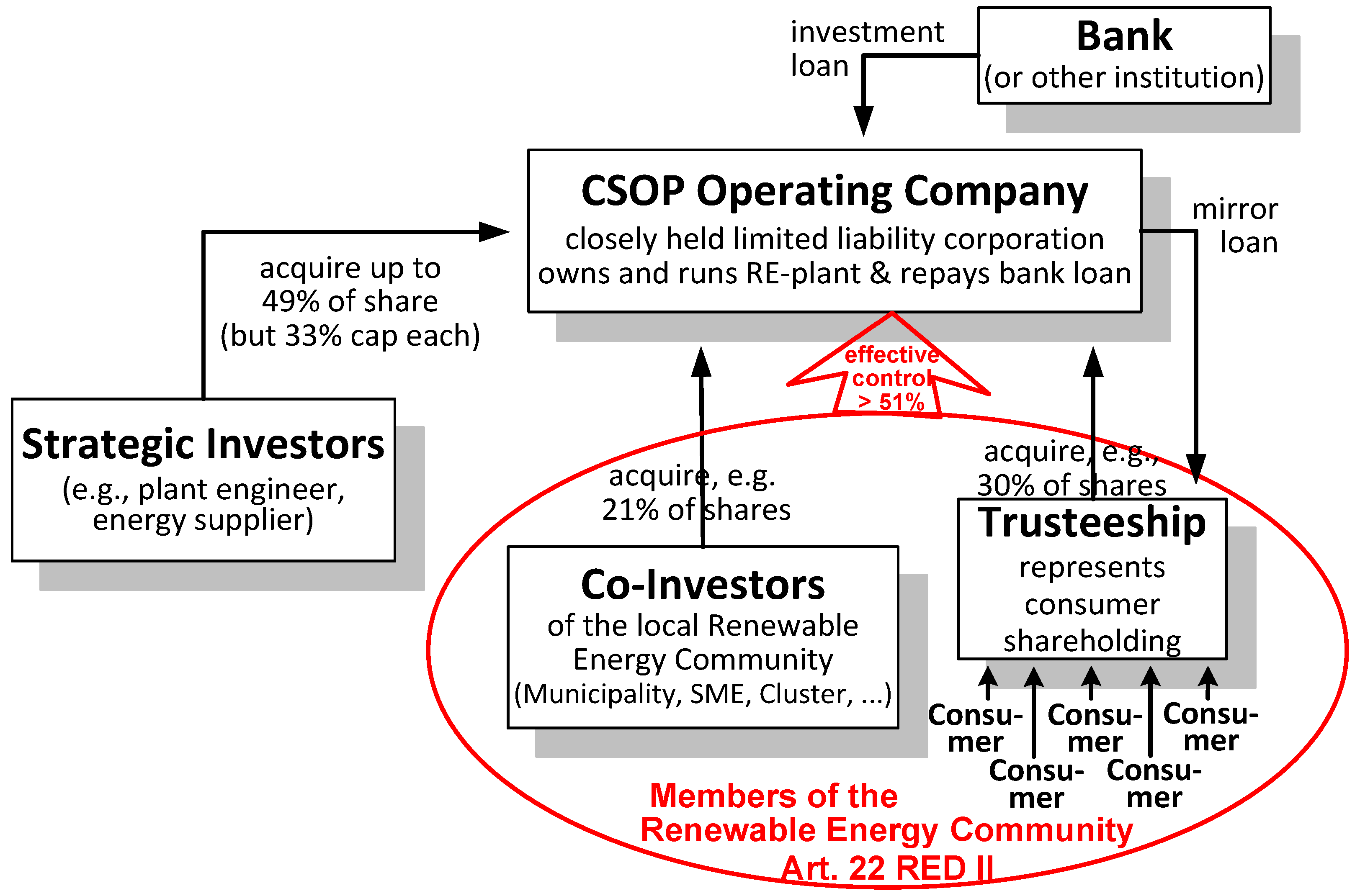

4.2. Level I—Key Elements of the Base Model (Leveraged or not)

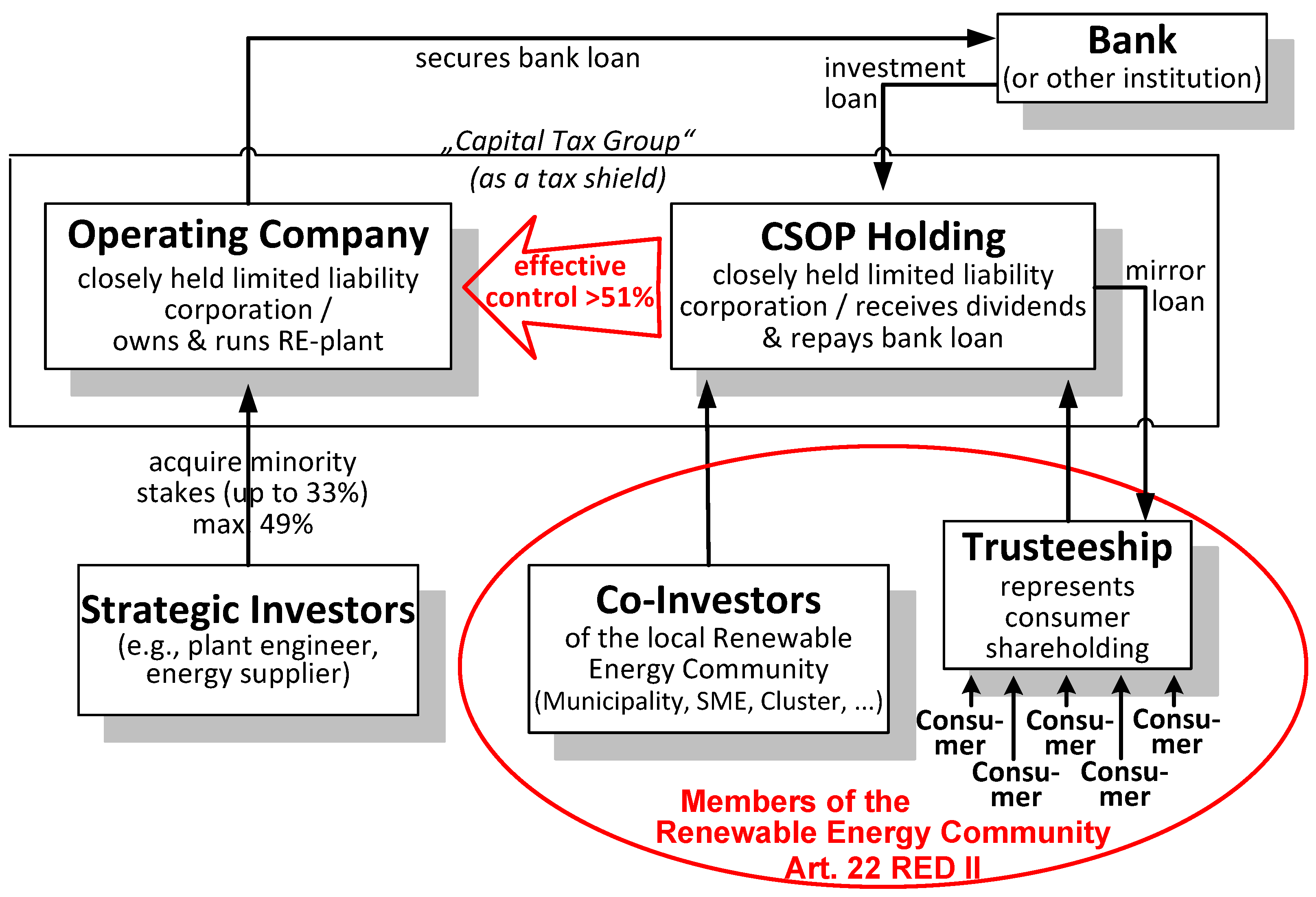

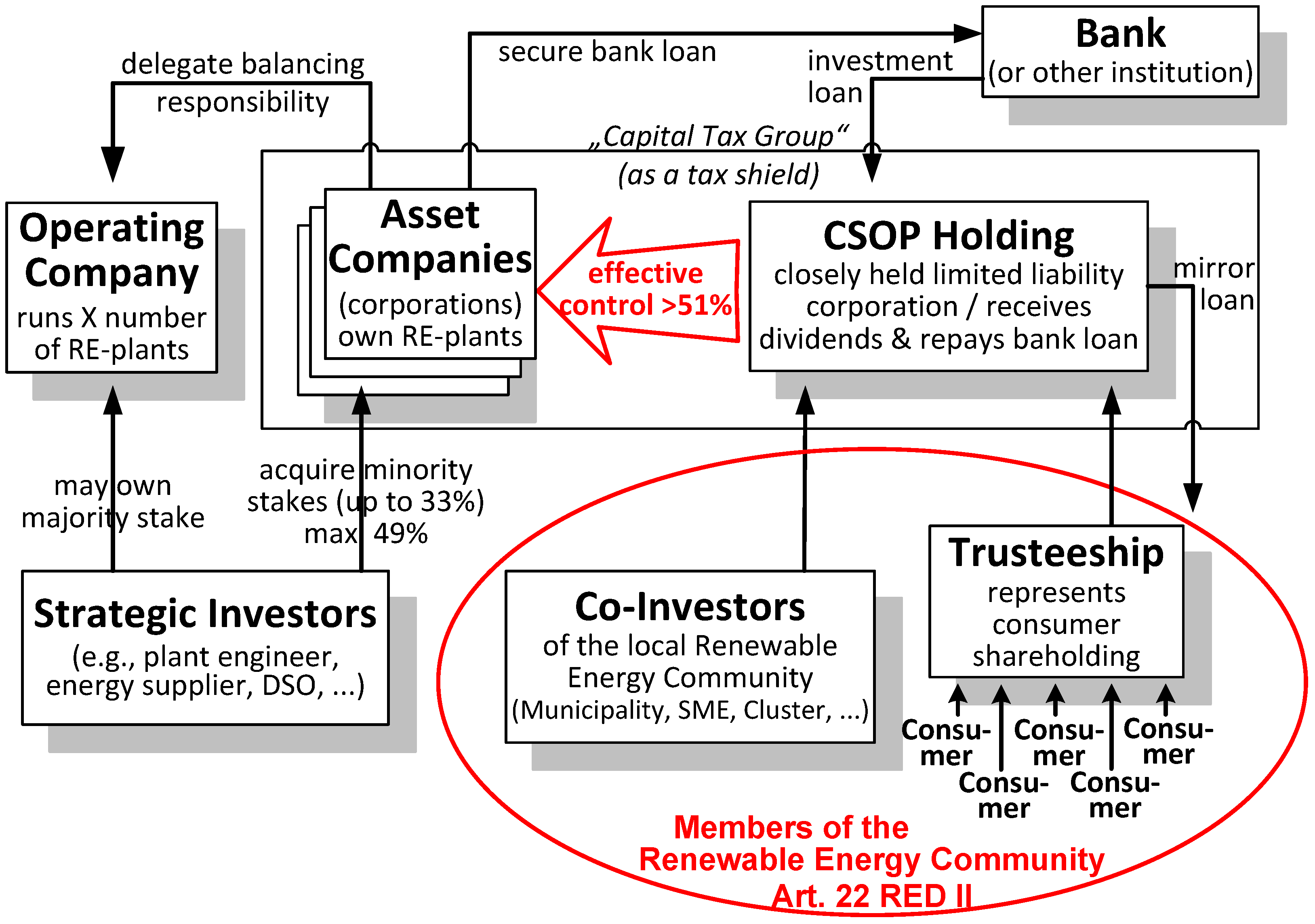

4.3. Level II—Leveraged RE-CSOP with External Strategic Investor

- Consumers are still not direct shareholders in the dominating Holding Company (in the case of a Holding Company whose direct shareholders would be supplied by the dependent Operating Company, problems relating company law institutions could arise, such as actions to exclude a shareholder, the increase and decrease of share capital, organization of shareholders’ meetings, change of statutes, etc.).

- The division of the shareholding between the members of the REC (i.e., municipality, SMEs, and other local co-investors on the one hand, and the consumers represented by the fiduciary entity (Trusteeship) on the other hand) is flexible and reflects the respective contributions and roles, as long as they together have effective control of the operating company by keeping at least 51% of its shares.

- External strategic investors can buy into the project without being burdened by the leveraged transaction that enables consumers without significant savings to participate.

4.4. Level III—Upscaling and Pooling RE-CSOP Investments

- The variety of renewable sources (wind, PV, biomass, etc. and their complementarity) or other energy sources (fossils as back-up but also those not easily to divest from);

- The specific combination of different energy sources where energy production is not the primary aim of economic activity (e.g., cogeneration, waste, biomass, etc.).

- Management and governance requirements [29]:

- More than one RE-CSOP project organised in various asset companies with majority ownership stakes of the members of the REC but managed by one operating company in which a professional energy company may have a majority interest;

- The operating company is run by a third party with expertise in installation and operation, including metering and maintenance, but such third party remains subject to the RECs instructions.

5. Discussion of the Key Elements of the RE-CSOP as Applied at Levels I–III

5.1. Indirect Consumer-Shareholding in the Capital of the Operating Company (or Holding)

5.1.1. Conveying Individual Share Ownership through a Trusteeship

5.1.2. Core Issues to be Considered for all RE-CSOP Models (Levels I–III)

- Exit of a consumer-shareholder with simultaneous transfer of the capital participation to a new CSOP participant only requiring a change of the party of the fiduciary contract (Investment Agreement).

- Exit of a consumer-shareholder with sale of the capital participation to the Operating Company which holds the share(s) until a new CSOP participant buys into the RE-CSOP. The Operating Company “warehouses” the shares, while at the same time creating a market place of these shares between the CSOP participants; this requires a definition of the legitimate motives to exit and of the period to announce this leave, as well as that of the instalment period for the cashing-out to avoid haemorrhaging of liquidity for CSOP.

- Exclusion of “bad leavers” (e.g., where consumer-shareholders obstruct decision-making within the fiduciary entity (Trusteeship), violate the supply contract substantially, etc). Here a cancellation of shares may occur with a subsequent transfer of monies from the Trusteeship.

- Exit following the death of a consumer-shareholder, which requires rules concerning the transfer by inheritance.

- Decisions concerning the day-to-day business of the Operating Company (or respectively of the CSOP Holding) that the Trusteeship represented by its managing director is authorized to take on behalf of the consumer-shareholders as trustors.

- Decisions of strategic importance (e.g., change of range of activity or business purpose, change of management, and those decisions involving financial commitments above a specific threshold; for example, EUR 50,000 requiring a vote of all trustors).

- They have the possibility for an internal consultation advised by an expert (the managing director of the Trusteeship should have appropriate qualifications or access to expertise).

- They vote their shares together (in a block proportional to the Trusteeship’s share in the Operating Company’s or CSOP Holding’s capital).

5.2. Financing the Consumer-Investment in the Operating Company

- Fixed capital and interest instalments—in certain periods additional financial resources will be generated that can be allocated to reserves to ensure timely repayment in the event of an economic downturn or the payment of funds to consumers due to resignation from the plan;

- Or variable capital and interest instalments—allocation of a fixed percentage of the net profit for this purpose in each period.

- Deferment of the repayment to the public partner until the loan is repaid in relation to the bank: The public partner agrees to subordinate its loan repayment to the investment loan, and agrees to postpone of its repayment period until other creditors, in particular those of the co-financing bank, have been repaid.

- Parallel repayment of the bank and the public partner.

5.3. Taxation of the RE-CSOP and its Consumer-Shareholders

- When leveraged, the transaction is financed, if possible, by loans from state development banks with low interest rates under programs specifically promoting RE.

- As a rule, the Operating Company—due to the financing cost of the leveraged transaction—will make losses or, in the best case, very small profits during the first years.

- In the case that the CSOP invests in a new RE plant pro rata profits/losses are allocated directly to the Operating Company; when it invests in an existing incorporated utility, they are allocated indirectly through dividend payments/depreciation of shares. In both cases taxation of profits occurs only once at the level of the Operating Company.

6. Conclusions and Policy Recommendations

- The attractiveness and coherence of the RED II “enabling framework”;

- The flexibility of the underlying business model allowing for an adequate division of responsibilities and benefits between the different co-investors according to their expertise and contributions.

6.1. Recognising the Challenges of RE Clusters in the Energy Systems of Tomorrow

- With decreasing cost of energy storage and increasing demand for local flexibility, community energy storage systems will become increasingly important for the energy transition as such and, consequently, for RECs. The challenge of integrating community storage in the energy system that presently is still largely centralized demands for socio-technical innovation [38].

- Apart from concerns that the new European regulatory framework does not sufficiently encourage, or in places even inadvertently discourages, complementarity between RES [15], the RED II does not adequately answer the question how energy sharing between local partners within RECs and with the possible involvement of professional energy companies can be facilitated.

- The question of operating and managing electricity networks and especially grid ownership of energy communities both RECs and CECs remains a thorny issue since regulators and the incumbent DSOs are inclined to opposition [29]. Although optional for Member States, it should be supported for RE clusters depending on their complexity and incentivised in a targeted way, in particular during the pioneering period to foster RE deployment.

- Inclusion of low-income households and vulnerable consumers is an important cornerstone in the fight against energy poverty and a postulate of energy justice [39] taken up both in RED II and IEMD. However, although prosumership reduces households’ overall expenditure for energy and provides a second source of income through the sale of excess production [40], we observed a lack of concrete proposals in view to facilitate their participation.

6.2. Spelling Out the “Enabling Framework” for RECs

- Elasticity with regard to the eligibility requirements of proximity of shareholders is important in order not to unintentionally hinder the realisation of more complex RECs, namely fully fledged RE clusters. This is particularly important in view of their impact on complementarity of RES in urban settings [15].

- Where it is expected to delegate the balancing responsibility to professional partners or to pool it for more than one REC, the incentive system of the “enabling framework” should take into account the increased costs of pioneering RE clusters in the still largely centralized present energy systems.

- Energy sharing in RECs is highly sensitive to national regulation, especially when using the public grid, as value creation depends on the ability of its members to sell electricity to each other or make use of offsetting mechanisms of the electricity meters [28]. Network fees should be reduced in proportion to the actual distances in order to maintain the benefits of prosumership in RECs.

- To this end, a real-world testing environment, operated for a limited period of time, also dubbed “regulatory sandboxes” [43], should allow for the testing of incentives for RECs. This would allow to better tailor the “enabling framework” to the most suited business models, proving to meet, in particular, the challenges of RE clusters. Identified best practise could then be supported in a more targeted manner.

Funding

Acknowledgments

Conflicts of Interest

Glossary

| Autonomy of a REC | Recital 71 RED II stipulates the capability “of remaining autonomous from individual members and other traditional market actors that participate in the community as members or shareholders, or who cooperate through other means such as investment”. |

| Capital Tax Group | Corporate structure that permits to calculate profits, losses and, what is most important here, costs, for tax purposes jointly for the combined tax group. |

| Clean Energy for All Europeans Package of the European Union | A package of measures that the European Commission presented on 30 November 2016 to keep the EU competitive as the energy transition changes global energy markets; this legislative initiative has four main goals, that is, energy efficiency, global leadership in RE, a fair deal for consumers and a redesign of the internal electricity market. |

| Citizen Energy Communities (CECs) | Defined in Art. 2 (11) of the IEMD as a legal entity that “(a) is based on voluntary and open participation and is effectively controlled by members or shareholders that are natural persons, local authorities, including municipalities, or small enterprises; (b) has for its primary purpose to provide environmental, economic or social community benefits to its members or shareholders or to the local areas where it operates rather than to generate financial profits; and (c) may engage in generation, including from renewable sources, distribution, supply, consumption, aggregation, energy storage, energy efficiency services or charging services for electric vehicles or provide other energy services to its members or shareholders“. |

| Consumer Stock Ownership Plan (CSOP) | A financing technique that employs an intermediary corporate vehicle, facilitates the involvement of individual investors through a trusteeship and may use external financing, thereby achieving the benefit of financial leverage. |

| Demonstration Projects for Innovative Technologies | Defined in Art. 2 para. 2 (x) of the IEMR as “a project demonstrating a technology as a first of its kind in the Union and representing a significant innovation that goes well beyond the state of the art”. |

| Effective control of RECs and CECs | Defined in Art. 2 pt. (56) IEMD as “rights, contracts or other means which, either separately or in combination and having regard to the considerations of fact or law involved, confer the possibility of exercising decisive influence on an undertaking, in particular by (a) ownership or the right to use all or part of the assets of an undertaking; (b) rights or contracts which confer decisive influence on the composition, voting or decisions of the organs of an undertaking”. |

| Electricity/Energy Sharing (incl. (virtual) net-metering) | Recital (46) IEMD stipulates: “Electricity sharing enables members or shareholders to be supplied with electricity from the generation installations within the community without being in direct physical proximity to the generating installation and without being behind a single metering point”. In the context of RECs, this is extended in Recital (71) and Art. 21 para. 6 to energy sharing. |

| Employee Stock Ownership Plan (ESOP) | An ESOP can use leverage and enables workers to acquire shares of their employer corporations, repaying the acquisition loan not from their wages but from the future earnings of their shares in the company. |

| Enabling Framework | Art. 22 para. 4 RED II foresees an enabling framework “to promote and facilitate the development of RECs”; furthermore, Art. 21 para. 6. foresees an enabling framework “to promote and facilitate the development of renewables self-consumption“. |

| Fiduciary Trusteeship | A fiduciary, fully fledged Trusteeship of a shareholding occurs when a shareholder (here the fiduciary entity = trustee) owns the shareholding for the account of one or more other entities (here individual consumer-shareholders = trustors) in the sense that she is entitled to the rights arising from the shareholding only in accordance with a fiduciary contract concluded with the trustors. |

| Internal Electricity Market Directive (IEMD) | Defines amongst others “citizen energy communities” (CECs), introducing in Art. 16 a new governance model and the possibility of energy sharing for them. |

| Internal Electricity Market Regulation (IEMR) | Mainly focussing on the completion of the internal market in electricity that has progressively been implemented since 1999. |

| Investment Agreements | In the RE-CSOP these are concluded between CSOP participants and the Trusteeship and stipulate the fiduciary relationship including rights and obligations of both parties. |

| Leveraged investment | Financing transaction that uses external financing (debt), thereby achieving the benefit of financial leverage. |

| Mirror Loan | Structure of capital acquisition loan in a CSOP directly to the Operating Company and then in a second “mirror loan” to the Trusteeship resulting in favourable taxation and a stronger position of the lender. |

| Renewable Energy Cluster | (Renewable) energy systems of the future, entailing flexibility, bi-directionality and interconnectivity options between prosumers and producers of energy and the market. |

| Renewable Energy Community (REC) | Defined in Art. 2 (16) the RED II as a legal entity: “(a) which, according to applicable national law, is based on open and voluntary participation, is autonomous, and is effectively controlled by shareholders or members that are located in the proximity of the renewable energy projects owned and developed by that community; (b) whose shareholders or members are natural persons, local authorities, including municipalities, or SMEs; (c) whose primary purpose is to provide environmental, economic or social community benefits for its members/the local areas where it operates rather than financial profits”. |

| Renewable Energy Directive (RED II) | Defines amongst others “renewable energy communities” (RECs) introducing a new governance model and in Art. 22 the possibility of energy sharing for them, while providing them with an enabling framework. |

| Trusteeship | Contractual arrangement with a fiduciary (as a rule a legal entity but also a physical person) to facilitate individual shareholding of the participating consumers in a CSOP. |

References

- NCEO. NCEO Statistics. Available online: http://www.nceo.org/articles/esops-by-the-numbers (accessed on 31 May 2019).

- Lowitzsch, J. The CSOP financing technique—Origins, legal concept and implementation. In Energy Transition—Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave/McMillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- McLuhan, M.; Nevitt, B. Take Today; Harcourt College: San Diego, CA, USA, 1972. [Google Scholar]

- Toffler, A. The Third Wave; Bantam: New York City, NY, USA, 1980. [Google Scholar]

- Official Journal of the European Union L 328/82. Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the promotion of the use of energy from renewable sources (recast). 2018.

- Official Journal of the European Union L 158/125. Directive (EU) 2019/944 of the European Parliament and of the Council of 5 June 2019 on common rules for the internal market for electricity and amending Directive 2012/27/EU (recast). 2019; to be transposed into national Law until June 2021.

- Official Journal of the European Union L 158/54. Regulation (EU) 2019/943 of the European Parliament and of the Council 5 June 2019 on the internal market for electricity (recast). 2019; as a Regulation to enter into force on 1 January 2020 without the need for transposition.

- Gauthier, C.; Lowitzsch, J. Outlook: Energy Transition and Regulatory Framework 2.0: Insights from the European Union. In Energy Transition-Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- Holstenkamp, L. Financing Consumer Co-Ownership of Renewable Energy Sources. In Energy Transition-Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- Ramirez Camargo, L.; Gruber, K.; Nitsch, F.; Dorner, W. Hybrid renewable energy systems to supply electricity self-sufficient residential buildings in Central Europe. Energy Procedia 2019, 158, 321–326. [Google Scholar] [CrossRef]

- Mancarella, P. MES (multi-energy systems): An overview of concepts and evaluation models. Energy 2014, 65, 1–17. [Google Scholar] [CrossRef]

- Lowitzsch, J.; Hanke, F. Renewable Energy Cooperatives. In Energy Transition-Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- REScoop. Mobilising European Citizens to Invest in Sustainable Energy—Final Results Oriented Report of the REScoop MECISE Horizon 2020 Project. 2019. Available online: https://www.rescoop-mecise.eu/ (accessed on 5 December 2019).

- Fici, A. An Introduction to Cooperative Law. In International Handbook of Cooperative Law; Cracogna, D., Fici, A., Henrÿ, H., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; pp. 3–62. [Google Scholar] [CrossRef]

- Lowitzsch, J.; Hoicka, C.; van Tulder, F. Renewable Energy Communities under the 2019 European Clean Energy Package—Governance Model for the Energy Clusters of the Future? Renew. Sustain. Energy Rev. 2019. forthcoming. [Google Scholar]

- Lowitzsch, J.; van Tulder, F. Overview of the Examples of Consumer (Co-)Ownership from the Country Chapters. In Energy Transition-Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- Jasiak, M. Energy Communities in the Clean Energy Package. Eur. Energy J. 2018, 8, 29–39. [Google Scholar]

- Martinot, E. Grid Integration of Renewable Energy: Flexibility, Innovation, and Experience. Annu. Rev. Environ. Resour. 2016, 41, 223–251. [Google Scholar] [CrossRef]

- Rezaie, B.; Rosen, M.A. District heating and cooling: Review of technology and potential enhancements. Appl. Energy 2012, 93, 2–10. [Google Scholar] [CrossRef]

- Risso, A.; Beluco, A.; De Cássia Marques Alves, R. Complementarity roses evaluating spatial complementarity in time between energy resources. Energies 2018, 11, 1918. [Google Scholar] [CrossRef]

- Lowitzsch, J. Investing in a Renewable Future—Renewable Energy Communities, Consumer (Co-) Ownership and Energy Sharing in the Clean Energy Package. Renew. Energy Law Policy Rev. 2019, 9, 14–36. [Google Scholar]

- Musall, F.; Kuik, O. Local acceptance of renewable energy—A case study from southeast Germany. Energy Policy 2011, 39, 3252–3260. [Google Scholar] [CrossRef]

- Lowitzsch, J. Introduction: The Challenge of Achieving the Energy Transition. In Energy Transition-Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- Baigorrotegui, G.; Lowitzsch, J. Institutional Aspects of Consumer (Co-)Ownership in RE Energy Communities. In Energy Transition-Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- Lowitzsch, J.; Kudert, S.; Neusel, T. Legal Opinion on the German Trust Model; Viadrina working paper; European University Viadrina: Frankfurt, Germany, 2012. [Google Scholar]

- Ackermann, D. How to Cash Out Tax-Free, Yet Keep Your Business … ESOPs—A Practical Guide for Business Owners and their Advisors; Conference Paper; National Center for Employee Ownership: San Francisco, CA, USA, 2002. [Google Scholar]

- Kahla, F. Die Kapitalstruktur von Bürgerenergiegesellschaften unter dem rechtlichen Rahmenwerk der deutschen Energiewende; Zeitschrift für Umweltpolitik & Umweltrecht (ZfU): Frankfurt, Germany, 2019; pp. 94–123. [Google Scholar]

- Tounquet, F.; De Vos, L.; Abada, I.; Kielichowska, I.; Klessmann, C. Energy Communities in the European Union. In Revised Final Report of the ASSET Project (Advanced System Studies for Energy Transition); Energy Communities in the European Union: Brussels, Belgium, 2019. [Google Scholar]

- Council of European Energy Regulators. Regulatory Aspects of Self-Consumption and Energy Communities—CEER Report; Ref: C18-CRM9_DS7-05-03; Council of European Energy Regulators: Brussels, Belgium, 2019. [Google Scholar]

- Jenkins, K. Energy Justice, Energy Democracy, and Sustainability: Normative Approaches to the Consumer Ownership of Renewables. In Energy Transition-Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: London, UK, 2019; Available online: https://link.springer.com/book/10.1007/978-3-319-93518-8 (accessed on 5 December 2019).

- Kelso, L.O.; Hetter-Kelso, P. Democracy and Economic Power: Extending the ESOP Revolution through Binary Economics; University Press of America: Lanham, MA, USA, 1991. [Google Scholar]

- Criddle, E.; Miller, P.; Sitkoff, R. The Oxford Handbook of Fiduciary Law; Oxford University Press: Oxford, UK, 2019. [Google Scholar]

- Schmidt, K. Handelsgesetzbuch (HGB). In Münchener Kommentar HGB; C.H. Beck: München, Germany, 2012; 230p. [Google Scholar]

- Oestreicher, A.; Koch, R. The Determinants of Opting for the German Group Taxation Regime with Regard to Taxes on Corporate Profits; Springer: Berlin, Germany, 2009. [Google Scholar]

- Hunkin, S.; Krell, K. Renewable Energy Communities—A Policy Brief from the Policy Learning Platform on Low-carbon economy. Interreg Europe, August 2018. Available online: https://interregeurope.eu (accessed on 5 December 2019).

- Thuronyi, V.; Brooks, K. Comparative Tax Law; Kluwer Law International B.V.: Alphen aan den Rijn, The Netherlands, 2016. [Google Scholar]

- Heeter, J.; McLaren, J. Innovations in Voluntary Renewable Energy Procurement: Methods for Expanding Access and Lowering Cost for Communities, Governments, and Businesses; Technical Report; National Renewable Energy Lab.(NREL): Golden, CO, USA, 2012. [Google Scholar]

- Koirala, B.; van Oost, E.; van der Windt, H. Community energy storage: A responsible innovation towards a sustainable energy system? Appl. Energy 2018, 231, 570–585. [Google Scholar] [CrossRef]

- Sovacool, B.K.; Burke, M.; Baker, L.; Kotikalapudi, C.K.; Wlokas, H. New frontiers and conceptual frameworks for energy justice. Energy Policy 2017, 105, 677–691. [Google Scholar] [CrossRef]

- Lowitzsch, J.; Hanke, F. Consumer (Co-)ownership in RE, EE & the fight against energy poverty—A dilemma of energy transitions. Renew. Energy Law Policy 2019, 9, 5–22. [Google Scholar]

- SCORE. Horizon 2020 SCORE (Grant Agreement N° 784960) n.d. Available online: https://www.score-h2020.eu (accessed on 5 December 2019).

- SCORE. CSOP-Financing. 2018. Available online: https://www.score-h2020.eu/?id=16883 (accessed on 5 December 2019).

- Heldeweg, M.A. Legal regimes for experimenting with cleaner production—Especially in sustainable energy. J. Clean. Prod. 2017, 169, 48–60. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Criteria | Renewable Energy Communities (RECs) Pursuant to Arts. 2 (16), 22 RED II | Citizen Energy Communities (CECs) as Defined in Arts. 2 (11), 16 IEMD |

|---|---|---|

| Eligibility |

| In principle open to all types of entities; |

| Primary Purpose | “environmental, economic or social community benefits for its shareholders / members or for local areas where it operates, rather than financial profits”; | |

| Membership | Voluntary participation open to all potential local members based on non-discriminatory criteria; | Voluntary participation open to all potential members based on non-discriminatory criteria; |

| Ownership and control |

|

|

| Advantages to qualify as REC or CEC |

|

|

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lowitzsch, J. Consumer Stock Ownership Plans (CSOPs)—The Prototype Business Model for Renewable Energy Communities. Energies 2020, 13, 118. https://doi.org/10.3390/en13010118

Lowitzsch J. Consumer Stock Ownership Plans (CSOPs)—The Prototype Business Model for Renewable Energy Communities. Energies. 2020; 13(1):118. https://doi.org/10.3390/en13010118

Chicago/Turabian StyleLowitzsch, Jens. 2020. "Consumer Stock Ownership Plans (CSOPs)—The Prototype Business Model for Renewable Energy Communities" Energies 13, no. 1: 118. https://doi.org/10.3390/en13010118

APA StyleLowitzsch, J. (2020). Consumer Stock Ownership Plans (CSOPs)—The Prototype Business Model for Renewable Energy Communities. Energies, 13(1), 118. https://doi.org/10.3390/en13010118