1. Introduction

Although modern renewable generators do have improved controllability properties compared to earlier solutions, they still exhibit a higher level of supply uncertainty compared to non-renewable generators. In addition, uncertainty is present in several forms in the power grid. First of all, in addition to renewable sources with fundamental characteristics of production uncertainty (of some level), conventional power plants are also naturally subject to failures and technological issues, which may limit their output from time to time. Furthermore, significant part of the demand corresponds to domestic consumers, the schedule of whom may be predicted only with limited accuracy [

1,

2].

As supply-demand imbalance causes frequency shift in the power network, certain forms of ancillary services (or ‘reserves’ to put it shorter) are needed for frequency stability. Activating these reserves in the appropriate time restores power balance and thus network frequency. Ancillary markets [

3] are specialized energy-economical platforms, in which commodities connected to ancillary services are traded. Although there is a broad spectrum of ancillary service and reserve types, in this paper we consider reserves used for frequency control. In a typical ancillary market, reserve providers are paid for allocating the required reserves and an additional fee is paid if the reserve is activated as well. According to this, in the current paper (regarding reserves) we consider capacity-allocation payment (and we are not interested if later the reserve is activated or not and do not consider these activation payments).

Reserves may be classified furthermore into non-event and event driven resources. While non-event driven resources are used to compensate production-consumption imbalances, event driven resources are used in reaction to contingencies and power plant or line outages. In the current article we focus on non-event driven resources and their allocation.

As maintaining the frequency stability of the power grid is the responsibility of the system operator (The terminology may differ as the expressions TSO (transmission system operator) and ISO (independent system operator) are also used for this player. In our case, as reserves will be allocated in the integrated power-reserve auction, we will assume that the operator is in charge not only of the transmission system but also of the auction, so we will use ISO.), it is its task to ensure the allocation of the required amount of reserve via long-term contracts or from the ancillary markets. Ensuring the necessary reserves via long term contracts is by nature more inflexible, as the actual power mix resulting from day ahead power exchanges and its uncertainty properties can not be taken into account. Either the system operator takes a conservative (and costly) approach and allocates a high amount of reserves in long term contracts or uses a mix of long term and short term solutions to account for the actual reserve requirements.

Regarding the general issues of reserve allocation, Reference [

4] formulates two general questions: How much reserve should be allocated and who should pay for it? The first problem, in addition to the simple approach presented in the same paper [

4], has been a subject to several articles. Following the lead idea of Reference [

4], namely that reserve should be purchased up to the point where the marginal cost of providing reserve is equal to the marginal value of this reserve, the article [

5] considers the customer outage cost to determine the marginal value of reserve. Regarding more recent approaches, motivated by the increasing market share of renewable sources, stochastic unit commitment based reserve procurement procedure for power systems including wind farms is described in Reference [

6], while more or less the same problem is approached by a different solution in Reference [

7]. Reference [

8] contributes to the same topic by applying a chance-constrained optimization to determine the required amounts of reserve capacity. A robust optimization based method of joint determination of day-ahead energy and reserve dispatch is described in Reference [

9]. Allocation of reserve-related costs is however not discussed in detail in these articles.

Regarding the allocation of these costs, which is discussed less in the literature, the original paper [

4] gives two approaches: In addition to the most simple solution, namely ‘

all consumers should pay a share of the cost of reserve on the basis of their consumption’, it also adds that on the other hand ‘

the cost of reserve should be shared among the generators on the basis of their contribution to the need for reserve’. It also discusses the possible scenario when generators forward these cost to their consumers. Regarding the allocation of reserve-related balancing and ramping costs, Reference [

10] proposes a unit commitment-based approach, applying the principle of pareto-optimality for the problem. Reference [

11] aims to distribute the reserve cost among the most appropriate consumers, applying agent-based modelling and simulation approach. A somewhat similar agent-based approach combined with stochastic unit commitment for the reserve cost allocation problem is presented in Reference [

12]. The two latter papers both use the concept of

demand factors (first defined in Reference [

13]) to characterize the reliability level of customers.

In the current article we follow the second principle formulated in Reference [

4] and aim to put the burden of reserve allocation costs to market participants whose activity significantly contributes to the need of reserve allocation. In the context of portfolio-bidding markets, the ‘

who pays for’ question is typically answered by the principle that the accepted demand bids cover the costs of products, thus we need to introduce any cost-allocation policy in the form of demand bids. This principle can be considered promising as it fits into the official market development plans of the European Union. It is stated in the Clean Energy Package that ‘

all market participants shall be responsible for the imbalances they cause in the system’ and this imposition includes variable renewable energy producers [

14]. However, the explicit regulation concerns only balancing markets while the more liquid day-ahead trading platform may remain free of uncertainties. This gap could be filled using a model developed in the current article.

In order to facilitate European market development, the created clearing formulation has to be adjusted to the usual European approach. Thus, in contrast to previous results, which analyzed the problem in a unit commitment framework [

15], we consider self-scheduling generators and a purely portfolio-bidding market based framework, consisting energy and reserve markets. We define the concept of supplementary reserve demand bids, which ensure that the owner of any uncertain energy bid, in the case of acceptance, will also automatically contribute to the costs of reserve allocation as well. While uncertainty characterization in the majority of previous literature was focussing to either power plants or customers, in the proposed approach we consider the potential uncertainty of both side of the energy market—both uncertain supply and demand energy bids are considered. Furthermore while previous methods use computationally demanding agent based modelling (as References [

11,

12]) or include quadratic constraints [

10] (or their semidefinite relaxation), we formulate the suggested method as a simple mixed integer linear problem (MILP), which can be efficiently solved, for example, via Benders-decomposition [

16] and/or the branch-and-bound algorithm [

17]. (Both techniques are widely used to solve problems in the power sector [

18,

19,

20].) In addition, the method suggested in the current paper uses a single scalar parameter according to which the set of uncertain/not uncertain energy bids are defined. Decreasing this parameter from a sufficiently large value, the market implementation of the method presented may be introduced to the market incrementally.

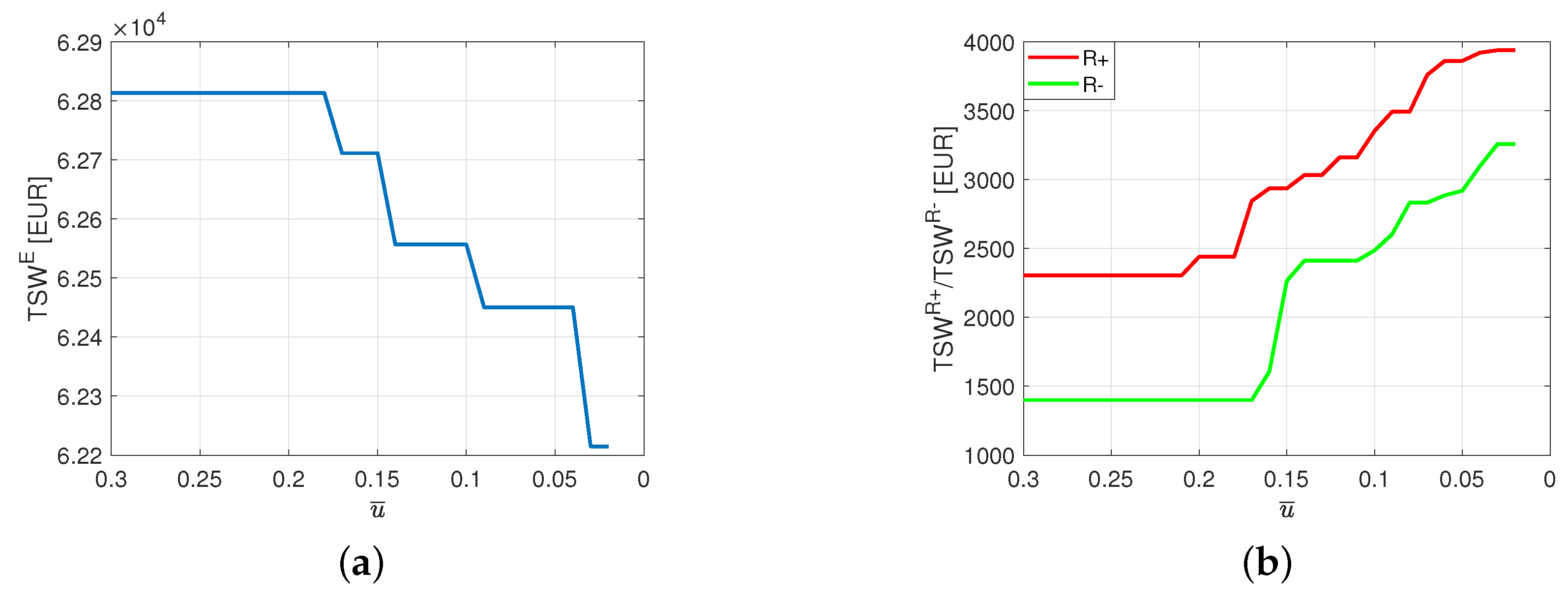

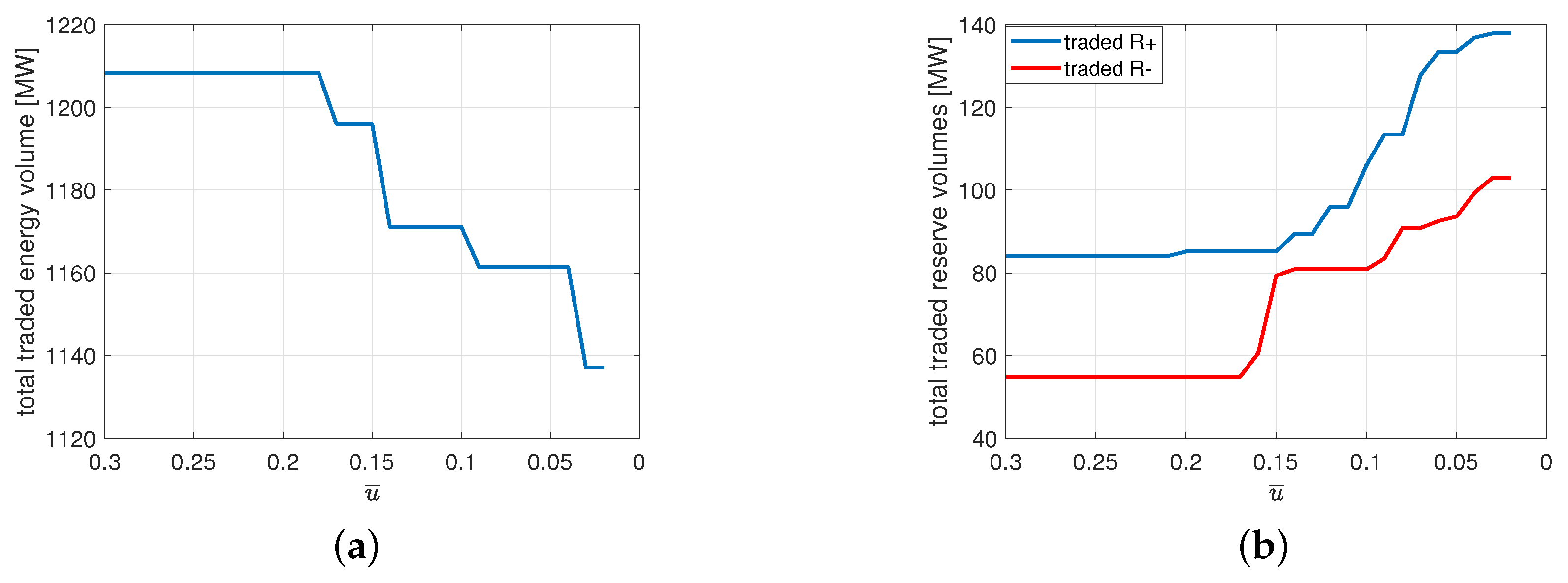

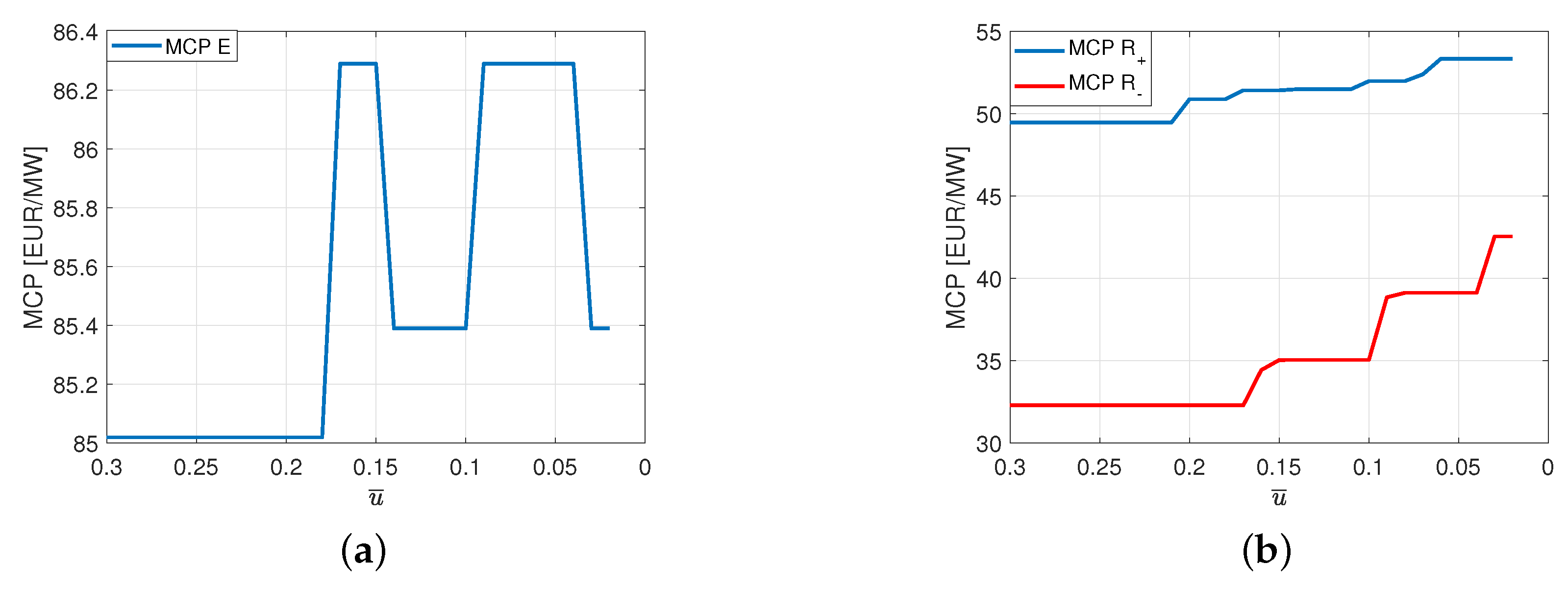

For the aim of simplicity and clarity, we introduce the proposed concept assuming a period decoupled market, in which no multiperiod block orders or minimum income condition (MIC) orders are present, thus every period may be dispatched independently of the others. This means that it is enough for us to define the framework for a single period and introduce the concepts in this context. Later, in

Section 4, we discuss the principles according to which the proposed concepts may be implemented in markets using multi-period block orders or MIC orders.

2. Materials and Methods

2.1. Uncertainty Quantification

We assume that every bid of the market can be connected to a bidder. We assume that there are

K bidders in the energy market. Similar to the approach of demand factors [

12,

13], we use simple scalar quantities to characterize the uncertainty of market participants. While in the case of the demand factor the characterizing scalar is formulated as the quotient of the expected energy not supplied (EENS) and the current load, we also account for deviations in the positive direction and define two uncertainty measures corresponding respectively to the positive and negative part of the deviation in question. Based on previous bidding and market behavior of the bidder (or if no data present, then based on the applied technology), we assign the uncertainty quantifiers (

and

) for each energy-bidder. The previous market behaviour in this case means that we may analyze how many times and how much the bidder deviated from its previously fixed schedule in relative terms (%) in the positive or in the negative direction, weighted by the quantity of the bid in question. Let us denote the expected relative value in the positive direction of bidder

k by

, while the expected relative value in the negative direction of bidder

k by

. By nature, both

and

are non-negative quantities.

For example, let us suppose a bidder corresponding to a renewable source with significant uncertainty. If we have for example, a bid/schedule realization history (

H) for bidder

k (For the indexing of bidders we use the variable

k, while

j and

i are used for the indexing of bids.) as

Each column of

H corresponds to a previous auction, where the bid of the bidder has been accepted. The top element of each column holds the nominal bid quantity, while the bottom row corresponds to the realized schedule. In this particular case we have the following signed relative deviation vector

D (in %).

Taking the positive and the negative part of this vector and weighing with the first row of (

1), we get the expected values

for bidder

k. Let us define the positive and negative uncertainty upper bounds

and

. Bids belonging to bidders with

and

will be called positively uncertain (U+) bids, while bids belonging to bidders with

and

will be called negatively uncertain (U-) bids. Bids belonging to bidders with both

and

will be called bi-uncertain (Ub) bids.

To consider a simple example, if we assume the above bid with , and , the bid will be considered as a negatively uncertain bid. In contrast, if , the bid will be taken into account as a bi-uncertain bid.

While the above example was demonstrating the case of a supply bid, we apply the same approach for demand bids as well in the proposed framework (domestic consumers may be for example, considered as uncertain demand bidders).

Let us note that uncertainty upper bounds in general may be different in the case of supply and demand bids, however in this paper we will not distinguish between uncertainty bounds of supply and demand bids. As we will see later, we will use these values to account for reserve allocation needed for the coverage of this uncertainty.

2.2. Market Model of the Single Period Case

We consider a basic portfolio bidding scenario, where participants capable of delivering a certain product (energy or reserve in this case) are represented by supply bids, while entities who are ready to pay for it are submitting demand bids. The market clearing aims to balance the supply with the demand in the terms of the traded quantity and the price.

As in the first step we do not consider multi-period block bids, which define interdependencies over time periods, the calculations for each period may be carried out independently. For this reason, to make the notation more simple, in the first step we describe the calculations regarding only a single time period. Later we discuss how the proposed approach may be generalized for multi-period cases including block orders. Regarding the bid format, the two generally used bid types in portfolio-bidding electricity markets are the step bid and the linear bid. In the case of the step bid the price per unit (PPU) of the bid is independent of the acceptance rate, while in the case of linear bid the price depends on the acceptance rate linearly. In other words, while step bids are parametrized by two values (the quantity (q) and the bid PPU), linear bids are parametrized by the quantity, a starting price and a final price. If a linear bid is partially accepted the resulting PPU may be derived as a linear interpolation of the two prices: If for example, the acceptance rate is 0.5, the resulting PPU is the average of the starting price and the final price. In the proposed framework, for the aim of simplicity and computational efficiency, we do not allow linear bids, only step bids.

In the proposed model, there are 3 sub-markets: the energy sub-market and the reserve sub-markets corresponding to positive and negative reserve. The term ‘sub-market’ is used to emphasize that interdependencies between these markets will be defined and thus they have to be cleared together—in this case the ‘market’ is composed of the sub-markets and the sub-markets are not independent entities anymore.

We do not consider fill-or-kill type bids in the market model, in other words partial acceptance is allowed for all energy bids. Regarding energy bids with uncertainty levels below the thresholds and , the variable denotes the acceptance variable of j-th energy supply bid, while denotes the acceptance variable of j-th energy demand bid. In the case of uncertain bids, , and denote the acceptance variables of energy supply bids with (respectively positive, negative or both) uncertainty, while , and denote the acceptance variables of energy demand bids with uncertainty.

As we will see later, these acceptance indicators will be included in variable vector of the problem. In addition to the acceptance indicators, the variable vector will also hold the income variables, logical integer variables used in the formulation of logical constraints and the market clearing prices (MCP) for energy and reserves. Under market clearing prices we mean prices which are compatible with the bid acceptance and balance constraints (see their formulation later). In other words, if the prices are equal to the market clearing prices, such an acceptance configuration of bids is possible (according to the bid acceptance rules), which ensures the balance of supply and reserve in every sub-market.

2.2.1. Supplementary Reserve Demand Bids

We assume that if uncertainty is present in the dispatch, in the spirit of the uncertain bidder pays principle, reserves must be allocated according to the measure of the uncertainty in question. We assume furthermore that these uncertain sources (being typically non-controllable units) are physically unable to provide reserves which could be used to handle the uncertainty implied by them. As we would like to make uncertain sources and consumers (bidders) pay for the implicated allocation of reserves, we assign obligatory reserve bids in the corresponding (positive, negative or both) reserve markets to each bid submitted in the energy sub-market. We call these compulsorily submitted reserve demand bids supplementary reserve demand bids (SRDBs). Both the bid price and bid quantity of these SRDBs are centrally regulated, they are not determined by the bidder. Uncertain energy bids together with the one or two connected SRDB(s) are called orders. As we will see later, the acceptance of the bids composing the order is dependent on the total income of the order, thus SRDBs and the related orders define interdependencies between the sub-markets.

Let us assume that is acceptance indicator of the energy supply bid of the bi-uncertain bidder k, the quantity of which is denoted by , while stands for price per unit (PPU) of the bid. In the proposed setup, implied by the bid corresponding to , bidder k also compulsorily submits a positive and a negative reserve demand bid, whose acceptance indicators are denoted by and respectively. The upper index in the notation refers to the set of positive/negative reserve demand bids implied by bi-uncertain energy supply bids.

As it is detailed in the following, the proposed concept of supplementary reserve demand bids may be introduced in the market gradually. In the beginning, it is the task of the ISO to allocate reserves and cover the connected costs. Furthermore, it is plausible that the ISO aims to ensure some of the required reserves in the day-ahead reserve markets. According to this consideration, we consider also reserve bids, which are not connected to uncertain energy bids. In the case when SRDBs cover all reserve needs, the model is completely functional without any non-SRDB reserve demand bid. The acceptance indicators of these (non-SRDB) bids are denoted by , , and in the case of positive reserve supply, positive reserve demand, negative reserve supply and negative reserve demand respectively.

Returning however to SRDBs, we need to consider the following. As positive deviations must be balanced by negative reserve and vice versa, positively uncertain ES bids (

) imply negative reserve demand bids denoted by

and negatively uncertain ES bids (

) imply positive reserve demand bids denoted by

. In principle, the reserve amounts allocated for these demand bids cover the corresponding expected uncertainty, thus we may write

We can see in Equation (

4) that following the general convention, throughout the paper we use negative sign for the quantities of demand bids.

We also account for uncertainty in the case of energy demand bids—domestic retail electricity suppliers (who submit demand bids in the wholesale market, which is the subject of our study) may have for example, higher uncertainty compared to bidders corresponding to industrial demand. The notation is similar: the bi-uncertain energy demand bid implies the a positive and a negative reserve demand bids and .

In our formalism, we consider demand with negative sign, so the row vectors in Equation (

1) will be negative. Positive deviations in this case will mean less consumption, which must be balanced by negative reserves and mutatis mutandis. The SRDBs corresponding to demand bids are described by Equation (

5).

We will suppose that the PPUs of these SRDBs are slightly higher compared to the highest PPU of the submitted reserve supply bids for the corresponding period. The difference is denoted by

and corresponds to the unit of the market (e.g., 1 EUR/MW). The constant

is introduced to avoid the possible overlap of supply and demand price curves in the case of the reserve sub-markets, which would potentially undermine the uniqueness of the optimal solution. The SRDB prices are formally defined as

where

in the case of positive reserve and

in the case of negative reserve.

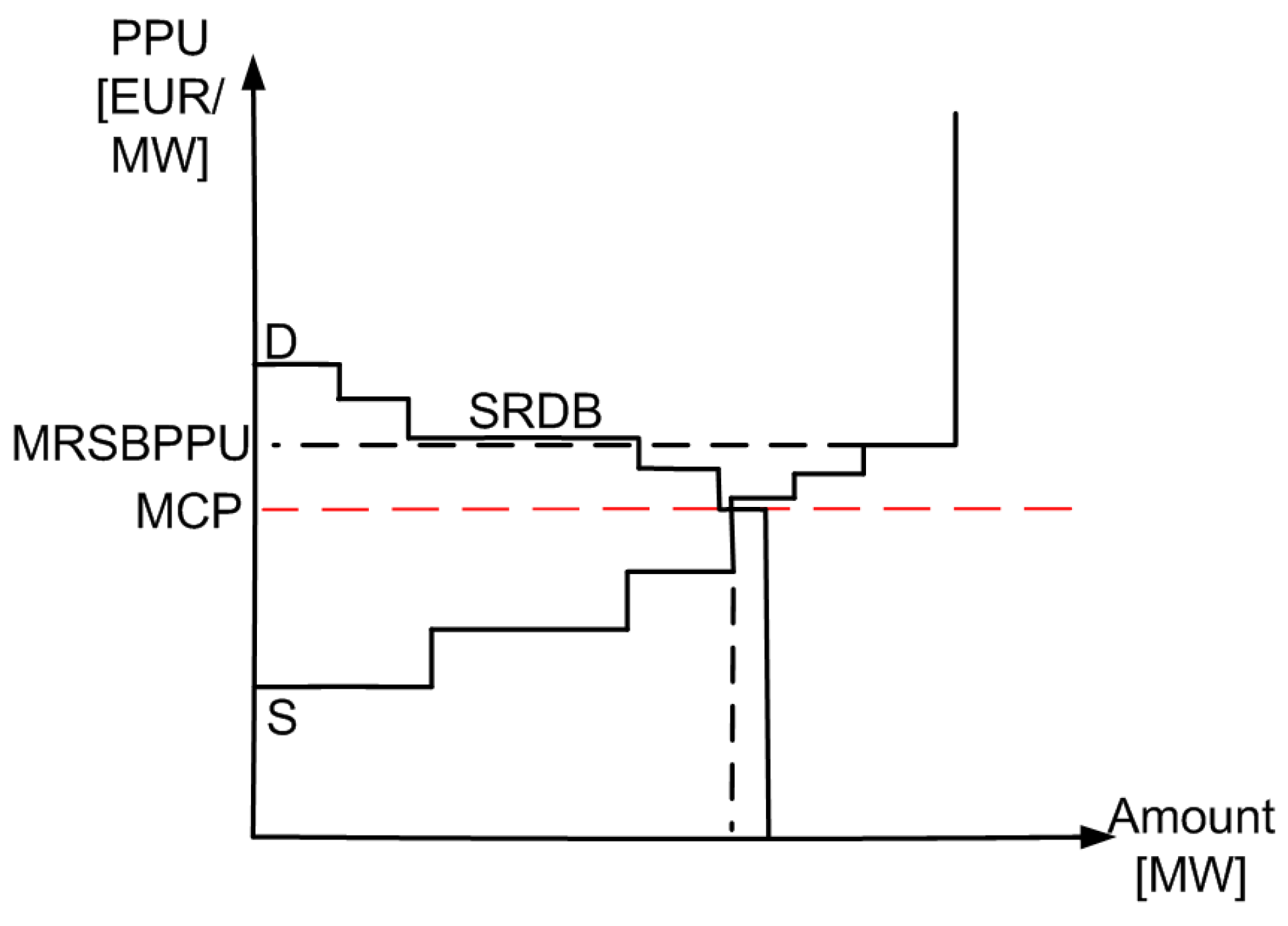

We assume that the amount of reserve supply is always enough to cover the total reserve demand. This assumption is usually valid in practice because regulators enforce power plants to offer reserve services. In this case the bid curves of the reserve spot markets (either positive or negative) will follow the qualitative scheme depicted in

Figure 1.

As all SRDBs are accounted for on the price of the supply bid with the highest PPU

, the central line segment in the demand curve (labeled by SRDB in

Figure 1) collects all the SRDBs. The line segments before and after it represent other reserve demand bids submitted to the reserve sub-market.

2.2.2. Minimum Surplus Conditions

Minimum Surplus Conditions for Uncertain Energy Supply Bids

In the proposed setup, without any additional considerations, it is possible that a submitted energy bid is rejected, while the connected SRDB(s) is/are accepted—this would naturally imply loss for the respective order, for the bidder is obliged to pay for the SRDB(s). Furthermore, even if the primary energy bid and the implied SRDB(s) is/are accepted, depending on the resulting MCPs, the surplus from the energy bid (originating from the energy sub-market) may not cover the cost of the SRDB(s) (originating from the reserve sub-markets) or the remaining surplus of the order (after extracting the costs of the SRDBs) may be very small. As the first step in the solution of this problem, we must calculate the incomes of the individual energy/reserve bids.

In order to formulate a linear computational framework, we take advantage of the dependence between MCPs and bid acceptance indicators (

y) and use the description of income introduced in References [

21,

22], as follows. Let us denote the income of the bid corresponding to

by

. Intuitively

may be calculated as

where

stands for the market clearing price of energy.

Equation (

7) holds however a quadratic expression of variables, namely the product of

and

, which would result in a computationally demanding quadratically constrained problem (MIQCP). To overcome this issue we formulate the expressions for income as

We implement the logical relations in the optimization framework based on the so called big-M method [

23], using integer logical variables (denoted by

z) as described in

Appendix A.

To elucidate the Formulas (

8) and (

9), let us enumerate the following three possibilities:

If the bid is entirely accepted (

),

equals the product of

and

according to (

8).

If the bid is partially accepted (

),

equals to

. Both (

8) and (

9) are active in this case and they result in the same inequality.

If the bid is entirely rejected (

), according to (

9)

.

The above considerations may be naturally formulated also for income of bids corresponding to and —and also for bids corresponding to but their income wont be important in the proposed framework.

The incomes of uncertain energy demand bids , , and incomes of positive and negative SRDBs connected to energy bids, denoted by, and () respectively, may be formulated similarly, taking into consideration in the latter two case that in the case of demand bids and , thus the income will mean practically expense because of the resulting negative sign.

According to these income calculations, now we may formulate constraints which exclude the scenario when the surplus of the primary energy bid does not meet the expense of the SRDB(s). In addition, we assume that for every uncertain order a surplus constant (

) is defined, which describes how much the surplus of the primary bid must exceed the expenses (in other words it gives a lower bound for the total resulting surplus). In the proposed approach we assume that this constant may be determined by the bidder, thus it is diverse. However, under certain market conditions, it may be also plausible to assume that

S is a parameter regulated by the central authority (system/market operator). Regarding the bid corresponding to

, we denote this constant by

(the notation is similar in the case of

and

). The constant

, will represent the minimum surplus value, which is required in the case of the acceptance of the order. According to this we may formulate the minimum surplus condition (MSC) for bi-uncertain energy supply bids as

where the right side is the surplus of the bid and the left side is the sum of the costs of the connected SRDBs (the incomes are negative because of demand) and the parameter

. In the case of positively uncertain

bids, we may write

while in the case of negatively uncertain

bids, the formula becomes

Minimum Surplus Conditions for Uncertain Energy Demand Bids

In the case of bi-uncertain energy demand bids, the minimum surplus condition will state that total cost of the bid must be no more than the maximal potential cost of the bid, which would have been realized in the energy sub-market in the particular case if

, minus a similar surplus constant (

) as in the case of supply bids.

In the case of positively uncertain

bids, we may write

while in the case of negatively uncertain

bids, we may write

2.2.3. Bid Acceptance Constraints

For energy supply bids with no uncertainty

For bi-uncertain energy supply bids

For positively uncertain energy supply bids

For negatively uncertain energy supply bids

For energy demand bids with no uncertainty

For bi-uncertain energy demand bids

For positively uncertain energy demand bids

For negatively uncertain energy demand bids

For positive reserve supply bids

For negative reserve supply bids

For not SRDB positive reserve demand bids

For not SRDB negative reserve demand bids

For positive SRDBs

For negative SRDBs

The structure of the variable vector and the formulation of logical implications based thereon may be found in

Appendix A.

2.2.4. Energy and Reserve Balances

The energy and reserve balances may be formulated as

2.2.5. The Objective Function

The objective function to maximize is the total social welfare (TSW). By definition the TSW is the total utility of consumption minus the total costs of production [

24]. The TSW equals in this case the sum of the social welfare in the three sub-markets.

where

denotes set of possible types of uncertain energy bids. Negative signs are needed because of the quantity convention of bids: the amount of demand bids is negative (while supply is positive).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}