Determinants and Characteristics of Korean Companies’ Carbon Management under the Carbon Pricing Scheme

Abstract

1. Introduction

2. Corporate Carbon Management

2.1. Environmental Management and Carbon Management

2.2. Strategic Approaches to Carbon Management

3. Research Method and Materials

3.1. Theories for Analysis

3.1.1. Analytical Framework

3.1.2. Strategic STAGEs of Carbon Management

3.2. Econometric Approach

3.2.1. Valuation of the Variables

Dependent Variables

Independent Variables

Control Variables

3.2.2. Empirical Models for Econometric Analysis

Quantitative Assessment of Internal Carbon Pricing

Model for Regression Analysis

3.3. Outline of Questionnaire Survey and Samples

4. Results and Discussion

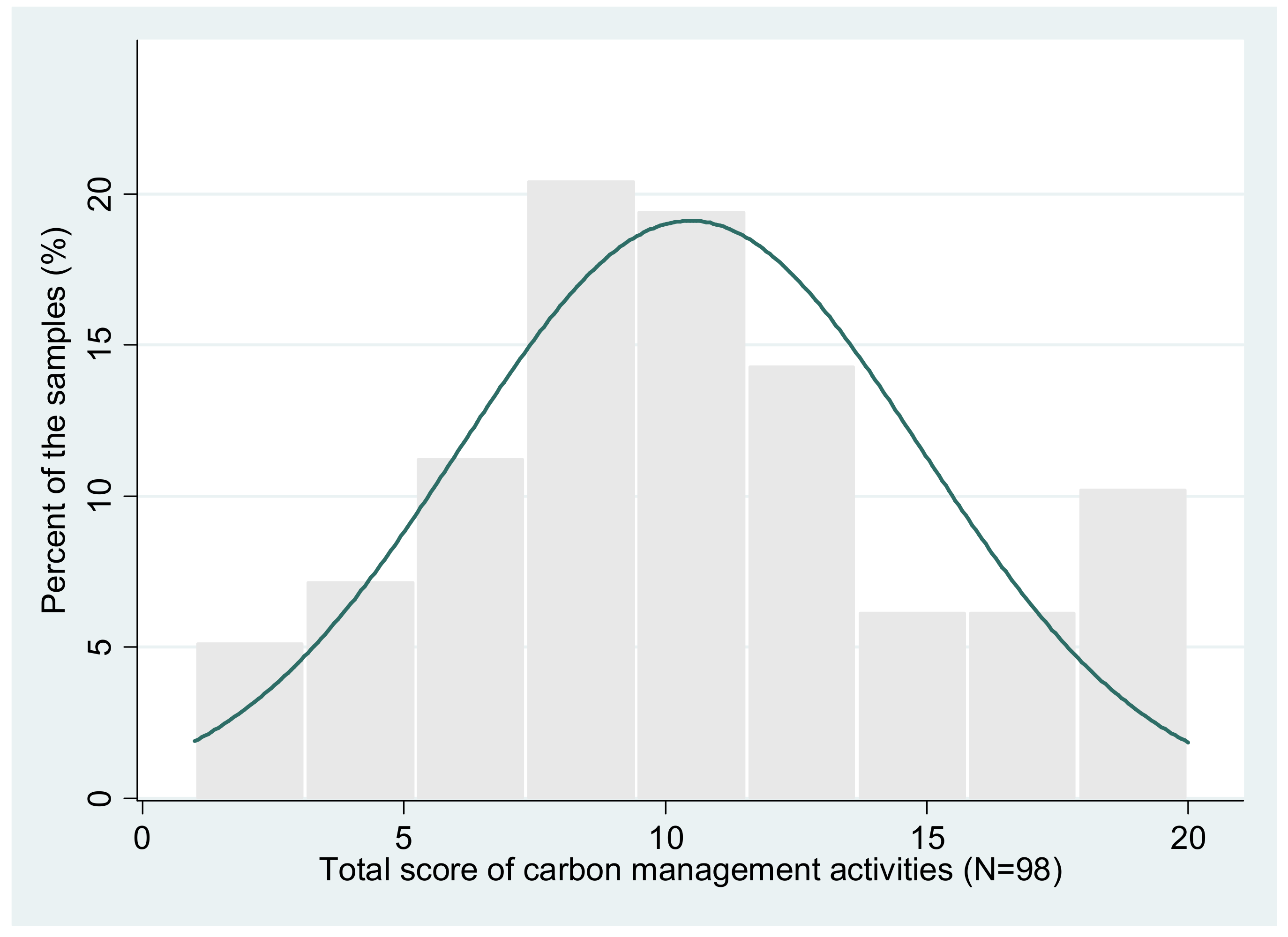

4.1. Korean Companies’ Carbon Management Status

4.2. Statistics of the Independent Variables and Companies’ Internal Carbon Price

4.3. Correlation Matrix and Bi-Variable Results

4.4. Determinant Factors for Carbon Management in Korean Companies

4.5. Statistics of the Supplementary Survey Questions

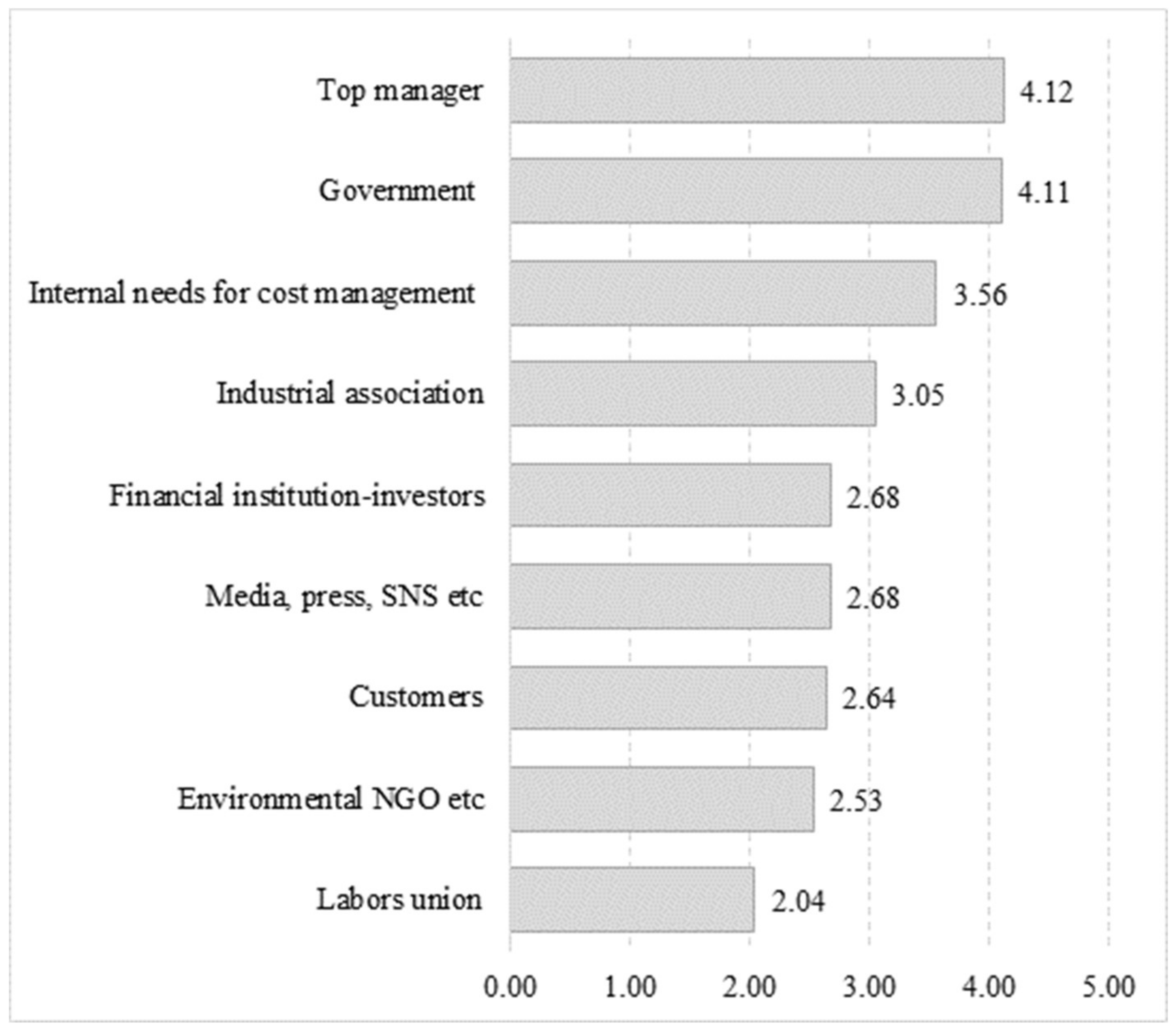

4.5.1. Important Stakeholders for Carbon Management

4.5.2. Company Evaluation of Impact of Carbon Management on Business Factors

4.5.3. Supportive Policy for Carbon Management

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Hoffmann, V.H.; Busch, T. Corporate Carbon Performance Indicators: Carbon intensity, dependency, exposure, and risk. J. Ind. Ecol. 2008, 12. [Google Scholar] [CrossRef]

- Lee, S.Y. Corporate Carbon Strategies in Responding to Climate Change. Bus. Strategy Environ. 2012, 21, 33–48. [Google Scholar] [CrossRef]

- Galbreath, J. Corporate governance practices that address climate change: An exploratory study. Bus. Strategy Environ. 2009, 19, 335–350. [Google Scholar] [CrossRef]

- Sullivan, R. An assessment of the climate change policies and performance of large European companies. Clim. Policy 2010, 10, 38–50. [Google Scholar] [CrossRef]

- Weinhofer, G.; Hoffmann, V.H. Mitigating Climate Change—How Do Corporate Strategies Differ? Bus. Strategy Environ. 2008, 19, 77–89. [Google Scholar] [CrossRef]

- Hendrics, H.; Busch, T. Carbon management as a strategic challenge for SMEs. Greenh. Gas Meas. Manag. 2012, 2, 61–72. [Google Scholar] [CrossRef]

- Bebbington, J.; Larrinaga-González, C. Carbon trading: Accounting and reporting issues. Eur. Account. Rev. 2008, 17, 697–717. [Google Scholar] [CrossRef]

- Stechemesser, K.; Guenther, E. Carbon accounting: A systematic literature review. J. Clean. Prod. 2012, 36, 17–38. [Google Scholar] [CrossRef]

- Evangelinos, K.; Nikolaou, I.; Filho, W.H. The effects of climate change policy on the business community: A corporate environmental accounting perspective. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 257–270. [Google Scholar] [CrossRef]

- Böttcher, C.F.; Müller, M. Drivers, Practices and Outcomes of Low-carbon Operations: Approaches of German Automotive Suppliers to Cutting Carbon Emissions. Bus. Strategy Environ. 2013, 24, 477–498. [Google Scholar] [CrossRef]

- Jeswani, H.K.; Wehrmeyer, W.; Mulugetta, Y. How warm is the corporate response to climate change? Evidence from Pakistan and the UK. Bus. Strategy Environ. 2008, 17, 46–60. [Google Scholar] [CrossRef]

- Gouldson, A.; Sullivan, R. Long-term corporate climate change targets: What could they deliver? Environ. Sci. Policy 2013, 27, 1–10. [Google Scholar] [CrossRef]

- Sprengel, D.C.; Busch, T. Stakeholder engagement and environmental strategy-the case of climate change. Bus. Strategy Environ. 2010, 20, 351–364. [Google Scholar] [CrossRef]

- Pinkse, J.; Kolk, A. Challenges and trade-offs in corporate innovation for climate change. Bus. Strategy Environ. 2010, 19, 261–272. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K.E. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Doda, B.; Gennaioli, C.; Grover, D. Are corporate carbon management practices reducing corporate carbon emissions. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 257–270. [Google Scholar] [CrossRef]

- Sullivan, R.; Gouldson, A. Ten years of corporate action on climate change: What do we have to show for it? Energy Policy 2013, 60, 733–740. [Google Scholar] [CrossRef]

- Suk, S.H.; Liu, X.B.; Sudo, K. A survey study of energy saving activities of industrial companies in the Republic of Korea. J. Clean. Prod. 2013, 41, 301–311. [Google Scholar] [CrossRef]

- Suk, S.H.; Lee, S.; Jeong, Y. The Korean Emissions Trading Scheme: Business perspectives on the first year of operations. Clim. Policy 2017. [Google Scholar] [CrossRef]

- Gill, P.; Dolan, G. Originality and the PhD: What is it and how can it be demonstrated? Nurse Res. 2015, 22, 11–15. [Google Scholar] [CrossRef] [PubMed]

- Porter, M. America’s Green Strategy. Sci. Am. 1992, 264, 168. [Google Scholar] [CrossRef]

- Maier, S.; Vanstone, K. Do Good Environmental Management Systems Lead to Good Environmental Performance? Research Briefing; Ethical Investment Research Services: London, UK, 2005. [Google Scholar]

- Shrivastava, P.; Scott, H.I. Corporate Self-Greenewal: Strategic Responses to Environmentalism. Bus. Strategy Environ. 1992, 1, 9–20. [Google Scholar] [CrossRef]

- Sunderland, T.J. Environmental management standards and certification—Do they add value? In ISO 14001 and Beyond: Environmental Management System in the Real World; Sheldon, C., Ed.; Greenleaf Publishing: Yorkshire, UK, 1997. [Google Scholar]

- Epstein, M.J. Measuring Corporate Environmental Performance: Best Practices for Costing and Managing and Effective Environmental Strategy, 1st ed.; McGraw-Hill Education: Chicago, IL, USA, 1996. [Google Scholar]

- Boiral, O.; Henri, J.F.; Talbot, D. Modeling the impacts of corporate commitment on climate change. Bus. Strategy Environ. 2011, 21, 495–516. [Google Scholar] [CrossRef]

- Suk, S.H.; Liu, X.B. A Survey Analysis of Company Perspective to the GHG Emissions Trading Scheme in the Republic of Korea. In Environmental Taxation and Green Fiscal Reform: Theory and Impact; Kreiser, L., Lee, S., Ueta, K., Milne, J.E., Ashiabor, H., Eds.; Edward Elgar Publishing, Inc.: Northampton, MA, USA, 2014; pp. 289–306. [Google Scholar]

- Luo, L.; Tang, Q. Determinants of the quality of corporate carbon management systems: An international study. Int. J. Account. 2016, 51, 275–305. [Google Scholar] [CrossRef]

- Microsoft. The Microsoft Carbon Fee: THEORY & Practice: The What, Why and How of Microsoft’s Efforts to Drive Culture Change; Microsoft: Redmond, WA, USA, December 2013. [Google Scholar]

- Abreu, M.C.S.; Freitas, A.R.P.; Rebouças, S.M.D.R. Conceptual model for corporate climate change strategy development: Empirical evidence from the energy sector. J. Clean. Prod. 2017, 165, 382–392. [Google Scholar] [CrossRef]

- Cades, S.; Czerny, A. Climate change mitigation strategies in carbon-intensive firms. J. Clean. Prod. 2016, 112, 4132–4143. [Google Scholar] [CrossRef]

- Giacomo, N.D.; Guthrie, J.; Farneti, F. Environmental management control systems for carbon emissions. PSU Res. Rev. 2017, 1, 39–50. [Google Scholar] [CrossRef]

- Tang, S.; Demeritt, D. Climate change and mandatory carbon reporting: Impacts on business process and performance. Bus. Strategy Environ. 2017. [Google Scholar] [CrossRef]

- Schaltegger, S.; Csutora, M. Carbon accounting for sustainability and management. Status quo and challenges. J. Clean. Prod. 2012, 36, 1–16. [Google Scholar] [CrossRef]

- Teng, M.-J.; Wu, S.-Y.; Chou, S.J.-H. Environmental Commitment and Economic Performance- Short-Term Pain for Long-Term Gain. Environ. Policy Gov. 2014, 24, 16–27. [Google Scholar] [CrossRef]

- Luo, L.; Tang, Q. Corporate ecological transparency: Theories and empirical evidence. Asian Rev. Account. 2016, 24, 498–524. [Google Scholar] [CrossRef]

- Sullivan, R.; Gouldson, A. The Governance of Corporate Responses to Climate Change: An International Comparison. Bus. Strategy Environ. 2016, 26. [Google Scholar] [CrossRef]

- Katsikeas, C.S.; Leonidou, C.N.; Zeriti, A. Eco-friendly product development strategy: Antecedents, outcomes, and contingent effects. J. Acad. Mark. Sci. 2016, 44, 660–684. [Google Scholar] [CrossRef]

- OECD. An Overview of Corporate Environmental Management Practices: Joint Study by the OECD Secretariat and EIRIS; OECD: Paris, France, 2003. [Google Scholar]

- Schot, J.; Fischer, K. Introduction: The greening of the industrial firm. In Environmental Strategies for Industry; Fischer, K., Schot, J., Eds.; Island Press: Washington, DC, USA, 1993; pp. 3–33. [Google Scholar]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar]

- Bhargave, S.; Welford, R. Chapter 2 Corporate Strategy and the Environment: The theory. In Corporate Environmental Management: System and Strategies; Welford, R., Ed.; Eathscan Publications Ltd.: London, UK, 1996; ISBN 1853833088. [Google Scholar]

- Murillo-Luna, J.L.; Garcés-Ayerbe, C.; Rivera-Torres, P. Why do patterns of environmental response differ? A stakeholders’ pressure approach. Strateg. Manag. J. 2008, 29, 1225–1240. [Google Scholar] [CrossRef]

- Buysse, K.; Verbeke, A. Proactive environmental strategies: A stakeholder management perspective. Strateg. Manag. J. 2003, 24, 453–470. Available online: http://dx.doi.org/10.1002/smj.299 (accessed on 1 November 2017). [CrossRef]

- Gasbarro, F.; Pinkse, J. Corporate adaptation behavior to deal with climate change: The influence of firm-specific interpretations of physical climate impacts. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 179–192. [Google Scholar] [CrossRef]

- I4CE (Institute for Climate Economics). Internal Carbon Pricing: A Growing Corporate Practice, November 2016. Available online: https://www.i4ce.org/download/internal-carbon-pricing-an-increasingly-widespread-corporate-practice/ (accessed on 1 January 2018).

- Cuff, M. Web Article. Carbon Pricing is Becoming the Norm for Big Companies, October 16, 2017. Available online: https://www.greenbiz.com/article/carbon-pricing-becoming-norm-big-companies (accessed on 1 January 2018).

- Goldstandard. Supply Report Q3 2016: Better Information for Better Decision-Making. Available online: https://www.goldstandard.org/sites/default/files/documents/gs_supply_report_q12016.pdf (accessed on 1 January 2018).

- Matisoff, D.C.; Noonan, D.S.; O’Brien, J.J. Convergence in environmental reporting: Assessing the Carbon Disclosure Project. Bus. Strategy Environ. 2013, 22, 285–305. [Google Scholar] [CrossRef]

- Liu, X.B.; Wang, C.; Zhang, W.S.; Suk, S.H.; Sudo, K. Company’s affordability of increased energy costs due to climate policies: A survey by sector in China. Energy Econ. 2013, 36, 419–430. [Google Scholar] [CrossRef]

- Nunnally, J.C.; Bernstein, I.H. Psychometric Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994. [Google Scholar]

- Korea Exchange. A Report of the Operating Result of the Korea Emissions Trading Market in 2015; KRX: Busan, Korea, 2016. (In Korean) [Google Scholar]

- Kline, R.B. Principles and Practice of Structural Equation Modeling; Guilford Press: New York, NY, USA, 1998. [Google Scholar]

- Suk, S.H. An Estimate of Internal Carbon Pricing of Korean Companies under the Emission Trading scheme. J. Clean. Prod. 2018. Under Review. [Google Scholar]

- Farrar, D.; Glauber, R. Multi-collinearity in regression analysis: The problem revisited. Rev. Econ. Stat. 1967, 49, 92–107. [Google Scholar] [CrossRef]

- Chrun, E.; Dolšak, N.; Prakash, A. Corporate environmentalism: Motivations and mechanisms. Annu. Rev. Environ. Resour. 2016, 41, 341–362. [Google Scholar] [CrossRef]

- Mazurikiewicz, P. Corporate Environmental Responsibility: Is a Common CSR Framework Possible? World Bank: Washington, DC, USA. Available online: http://documents.worldbank.org/curated/en/577051468339093024/pdf/421830csrframework01PUBLIC1.pdf (accessed on 1 November 2017).

- Damert, M.; Baumgartner, R.J. External pressures or internal governance- what determines the extent of corporate responses to climate change? Corp. Soc. Responsib. Environ. Manag. 2017. [Google Scholar] [CrossRef]

- Economic Circles Requests Lowered Greenhouse Gas Reduction Target; The Federation of Korean Industries (FKI): Seoul, Korea, 16 June 2015. (In Korean)

- Brewer, T.L. Business perspectives on the EU emissions trading scheme. Clim. Policy 2005, 5, 137–144. [Google Scholar] [CrossRef]

- Oestreich, A.M.; Tsiakas, I. Carbon emissions and stock returns: Evidence from the EU Emissions Trading Scheme. J. Bank. Financ. 2015, 58, 294–308. [Google Scholar] [CrossRef]

- Bushnell, J.B.; Chong, H.; Mansur, E.T. Profiting from Regulation: Evidence from the European Carbon Market. Am. Econ. J. Econ. Policy 2013, 5, 78–106. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Techniques/Strategies/Step/Type | |

|---|---|---|

| Stepwise classification | Schot and Fischer (1993) [40] | Compliance-driven, merely attend to legal requirements, proactive environmental strategies |

| Buysse and Verbke (2003) [44] | Reactive strategy, defensive strategy, accommodative strategy, proactive strategy | |

| OECD (2003) [39] | First step: issuance of a policy statement Second step: formal management systems Third step: environmental performance reporting | |

| Murillo-Luna et al. (2008) [43] | Passive, attention to legislation, attention to stakeholders, total environmental quality (highest level of proactivity) | |

| Firm performance-based classification | Levy and Kolk (2002, in [2]) * | Avoidant, resistant, compliant, proactive |

| Kolk and Pinkse (2005, in [2]) * | Cautious planner, emerging planner, internal explorer, vertical explorer, horizontal explorer, emissions trader | |

| Jeswani et al. (2008) [11] | Indifferent, beginner, emerging, active | |

| Sprengel and Busch (2010) [13] | Minimalists, regulation shapers, pressure managers, emission avoiders | |

| Weinhofer and Hoffmann (2008) [5] | All-rounder, compensator, substituting compensator, reducer, substituting reducer, preserver | |

| Lee (2012) [2] | Wait-and see observer, cautious reducer, product enhancer, all-round enhancer, emergent explorer, all-round explorer | |

| Gasbarro and Pinkse (2016) [45] | Pre-emptive, reactive, continuous, and deferred adaptation | |

| Abreu et al. (2017) [30] | Minimalist approach, regulation shaper, pressure manager or greenhouse gas emission avoiders | |

| Variable | Description | Reference | |

|---|---|---|---|

| External | GOVERNMENT | Strictness of the government’s policy | Sullivan and Gouldson (2016) [37] |

| COMPETITOR | Degree of market competition of the same sector | Böttcher and Müller (2013) [10] | |

| ENERGY PRICE | Degree of pressure due to energy price | Gouldson and Sullivan (2013) [12] | |

| Stakeholder | Degree of importance of relevant stakeholder | Sprengel and Busch (2010) [13] | |

| Internal | TOPSUPPORT | Management support for carbon management | Katsikeas et al. (2016) [38] |

| TOPUNDERSTANDING | Management understanding on carbon management | ||

| INCARBONPRICE | Emission allowance price determining trading | - | |

| TECHNOLOGY LEVEL | Level of technology that companies currently have | - | |

| Control | SIZE | SMALL, MEDIUM, L-MEDIUM, LARGE | Weinhofer, and Hoffmann (2008) [5] Böttcher, and Müller (2013) [10] |

| SECTOR | CEMENT, IRON&STEEL, PETROCHEMICAL, PAPER&PULP, NON_FERROUS, and MACHINERY, REFINING, ELECTRONIC and OTHER. | Jeswani, et al. (2008) [11] | |

| PRODUCT TYPE | RAW, INTER and FINAL | - | |

| Item | Carbon Management Activities | Valuation | ||

|---|---|---|---|---|

| 0 | 1 | |||

| STAGE 1 | CMA01 | Collecting information on policy related to energy savings and GHG emission reduction | ||

| CMA02 | Regular in-house training program for energy saving and GHG emission reduction | |||

| CMA03 | Encouraging daily energy saving activities in office (ex. turning off lights) | |||

| CMA04 | Participating in training programs for energy saving and GHG emission reduction held by the government/local government | |||

| STAGE 2 | CMA05 | Short & long-term targets for energy savings and GHG emission reduction in place | ||

| CMA06 | Conducting analysis on energy use and GHG emissions to identify potential areas for energy savings and emission reduction | |||

| CMA07 | Installing monitoring equipment on energy consuming facilities | |||

| CMA08 | Enhancing daily facility maintenance for energy saving and GHG emission reduction | |||

| STAGE 3 | CMA09 | Setting up an internal standard for energy savings and GHG emission reduction management | ||

| CMA10 | Establishing a unit or department for emission trading | |||

| CMA11 | Purchase new production facilities to save energy and reduce GHG emissions | |||

| CMA12 | Investing in R&D to improve production processes for energy savings and emission reduction | |||

| STAGE 4 | CMA13 | Enhancing optimization in transporting materials and goods | ||

| CMA14 | Making adjustments in energy mix to use more clean energy sources | |||

| CMA15 | Releasing sustainability reports regularly that contain data for energy consumption and GHG emissions | |||

| CMA16 | Set up a strategic carbon management (plan-do-check-act) | |||

| STAGE 5 | CMA17 | Setting up a plan and allocating budget for purchasing permits and trading | ||

| CMA18 | Establishing decision making process in relation to carbon trading (e.g., purchase, sell, price projection, etc.) | |||

| CMA19 | Establishing carbon management strategy based on regular analysis of carbon market | |||

| CMA20 | Adopting a green or carbon management accounting system | |||

| Price of Emission Allowance (KRW/tCO2) | Possibility for Purchasing Permits | ||||

|---|---|---|---|---|---|

| Very High | High | Modest | Low | Very Low | |

| 3000 | √ | ④ | ③ | ② | ① |

| 5000 | √ | ④ | ③ | ② | ① |

| 8000 | √ | ④ | ③ | ② | ① |

| 10,000 | ⑤ | √ | ③ | ② | ① |

| 12,000 | ⑤ | √ | ③ | ② | ① |

| 15,000 | ⑤ | √ | ③ | ② | ① |

| 18,000 | ⑤ | ④ | √ | ② | ① |

| 20,000 | ⑤ | ④ | √ | ② | ① |

| 23,000 | ⑤ | ④ | ③ | √ | ① |

| 26,000 | ⑤ | ④ | ③ | √ | ① |

| 30,000 | ⑤ | ④ | ③ | ② | √ |

| 33,000 | ⑤ | ④ | ③ | ② | √ |

| 37,000 | ⑤ | ④ | ③ | ② | √ |

| Classification Criteria | Number of Respondents | Percentage (%) | |

|---|---|---|---|

| Sector | Petrochemical | 16 | 16 |

| Cement | 6 | 6 | |

| Steel & iron | 14 | 14 | |

| Paper | 11 | 11 | |

| Non-ferrous | 10 | 10 | |

| Machinery | 5 | 5 | |

| Refining | 2 | 2 | |

| Electronics | 7 | 7 | |

| Others | 29 | 29 | |

| In total | 100 | 100.0 | |

| ETS | Targeted | 83 | 83 |

| Non-targeted | 17 | 17 | |

| Size | Large | 6 | 6 |

| L-medium | 36 | 36 | |

| Medium | 35 | 35 | |

| Small | 23 | 23 | |

| Product type | Raw materials | 32 | 32 |

| Intermediate goods | 44 | 44 | |

| Finished goods. | 22 | 22 | |

| Variable | Obs. | Mean | Std. Dev. | Min. | Max | Skewness Coefficient | Kurtosis Coefficient | |

|---|---|---|---|---|---|---|---|---|

| Independent | GOVERNMENT | 100 | 3.77 | 0.709 | 2 | 5 | −0.97 | 2.51 |

| COMPETITION | 100 | 3.86 | 0.853 | 2 | 5 | −0.49 | 2.23 | |

| ENERGY_PRICE | 99 | 3.71 | 0.693 | 2 | 5 | −1.26 | 2.79 | |

| STAKEHOLDER | 99 | 3.62 | 0.681 | 1 | 9 | 2.32 | 4.41 | |

| TOP_SUPPORT | 100 | 3.44 | 0.891 | 1 | 5 | −1.89 | 2.90 | |

| UNDERSTANDING | 100 | 3.52 | 0.915 | 2 | 5 | −1.57 | 2.15 | |

| TECHNOLOGY_LEVEL | 100 | 3.16 | 0.718 | 1 | 4 | −2.09 | 2.68 | |

| IN_CARBON_PRICE | 73 | 16,906 | 5908 | 3000 | 33,185 | −2.76 | 6.94 | |

| TCMA | GOVE. | COMP. | ENPR | STAK. | TOPS. | UNDE. | INCA. | |

|---|---|---|---|---|---|---|---|---|

| TCMA | 1.000 | |||||||

| GOVERNMENT | 0.115 | 1.000a | ||||||

| COMPETITION | 0.018 | 0.297 | 1.000 | |||||

| ENERGY_PRICE | −0.036 | 0.119 | 0.230 b | 1.000 | ||||

| STAKEHOLDER | 0.281 a | −0.026 | −0.118 | −0.165 | 1.000 | |||

| TOP_SUPPORT | 0.565 a | 0.098 | 0.055 | 0.072 | 0.269 a | 1.000 | ||

| UNDERSTANDING | 0.432 a | −0.001 | −0.113 | 0.051 | 0.066 | 0.299 a | 1.000 | |

| IN_CARBON_PRICE | 0.173 | 0.001 | −0.072 | −0.132 | −0.072 | 0.168 | 0.199 c | 1.000 |

| Variables | STAGE1 | STAGE 2 | STAGE 3 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Model1 | Model2 | Model3 | Model1 | Model2 | Model3 | Model1 | Model2 | Model3 | |||

| External pressure | GOVERNMENT | −0.351 | −0.438 | −0.646 | −0.675 b | −0.713 b | −0.632 | −0.510 | −0.491 | −0.803 | |

| COMPETITION | 0.277 | 0.244 | 0.618 | 0.012 | −0.004 | −0.039 | 0.137 | 0.187 | −0.243 | ||

| ENERGY_PRICE | −0.094 | −0.091 | 0.177 | −0.442 | −0.451 | −0.422 | −1.012 a | −1.056 a | −1.160 | ||

| STAKEHOLDER | −0.050 | 0.013 | 0.166 | 0.202 | 0.148 | 0.165 | 0.135 | 0.098 | −0.828 | ||

| Internal factor | TOP_SUPPORT | 0.604 b | 0.667 b | 0.645 | 0.953 a | 0.959 a | 0.898 | 1.552 a | 1.623 a | 2.217 | |

| UNDERSTANDING | 0.433 | 0.387 | 0.588 | −0.051 | −0.027 | 0.146 | 0.123 | 0.166 | −0.214 | ||

| IN_CARBON_PRICE | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| TECH_LEVEL | 0.713 c | 0.723 c | 0.816 | 0.507 | 0.302 | 0.148 | 0.323 | 0.258 | 0.435 | ||

| Control | Production type | RAW | −0.458 | 0.699 | −0.281 | ||||||

| INTERMEDIARY | −0.380 | −0.226 | 0.706 | −0.572 | −0.424 | −0.316 | |||||

| FINAL | 0.168 | −1.245 | 0.543 | ||||||||

| Size | SMALL | −0.645 | −19.830 | 1.116 | 0.783 | 1.075 | 1.298 | ||||

| MEDIUM | −1.305 | −20.924 | 0.396 | 0.135 | 0.933 | 0.054 | |||||

| L_MEDIUM | −1.114 | −20.288 | 0.587 | 0.496 | 1.413 | −0.025 | |||||

| Sector | CHEMICAL | 20.439 | −20.163 | −25.505 | |||||||

| CEMENT | −1.197 | −21.524 | −25.306 | ||||||||

| STEEL | 20.179 | −20.911 | −21.889 | ||||||||

| PAPER | 21.424 | −19.752 | −20.705 | ||||||||

| NON-FERROUS | 20.906 | −20.826 | −22.505 | ||||||||

| MACHINERY | 21.150 | −18.518 | −23.179 | ||||||||

| ELECTRICS | 22.496 | −20.993 | −23.473 | ||||||||

| OTHERS | 20.798 | −19.666 | −23.235 | ||||||||

| Number of obs. | 71 | 71 | 71 | 71 | 71 | 71 | 71 | 71 | 71 | ||

| LR chi2(8) | 19.7 b | 22.66 c | 40.55 b | 23.17 a | 25.64 b | 32.56 | 38.73 a | 41.09 a | 65.14 a | ||

| Pseudo R2 | 0.108 | 0.124 | 0.223 | 0.128 | 0.142 | 0.180 | 0.178 | 0.189 | 0.299 | ||

| Variables | STAGE 4 | STAGE 5 | TCMA | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Model1 | Model2 | Model3 | Model1 | Model2 | Model3 | Model1 | Model2 | Model3 | |||

| External pressure | GOVERNMENT | 0.199 | 0.308 | −0.127 | 0.761 b | 0.777 c | 0.070 | −0.261 | −0.291 | −0.677 c | |

| COMPETITION | 0.058 | −0.001 | 0.385 | −0.236 | −0.350 | 0.205 | 0.187 | 0.152 | 0.454 | ||

| ENERGY_PRICE | −0.100 | −0.036 | −0.045 | −0.068 | −0.006 | −0.025 | −0.447 | −0.449 | −0.391 | ||

| STAKEHOLDER | 0.237 | 0.030 | 0.537 | 0.784 c | 0.710 | 1.768 b | 0.518 | 0.430 | 0.658 | ||

| Internal factor | TOP_SUPPORT | 0.738 b | 0.780 b | 0.539 c | 0.648 b | 0.651 b | 0.386 | 1.281 a | 1.310 a | 1.220 a | |

| UNDERSTANDING | 0.465 c | 0.562 c | 0.532 | 1.040 a | 1.519 a | 1.414 a | 0.636 b | 0.707 b | 0.800 a | ||

| IN_CARBON_PRICE | 0.000 | 0.000 | 0.000 | 0.000 b | 0.000 b | 0.000 a | 0.000 | 0.000 | 0.000 | ||

| TECH_LEVEL | 0.123 | −0.067 | 0.007 | 0.114 | −0.314 | −0.532 | 0.556 c | 0.261 | 0.222 | ||

| Control | Production type | RAW | 0.231 | 0.881 | 0.463 | ||||||

| INTERMEDIARY | 0.756 | −0.012 | 1.165 | −0.157 | 0.759 | −0.411 | |||||

| FINAL | −0.879 | 2.238 | −1.876 b | −1.104 c | |||||||

| Size | SMALL | 2.611 c | 2.265 | 0.573 | 1.132 | 1.810 | 0.495 | ||||

| MEDIUM | 2.408 c | 1.813 | 0.906 | −1.709 | 0.565 | −1.279 | |||||

| L_MEDIUM | 2.478 c | 1.882 | −1.179 | 0.904 | −0.808 | ||||||

| Sector | CHEMICAL | −0.567 | −1.002 | −2.212 | |||||||

| CEMENT | −35.257 | −37.644 | −6.787 a | ||||||||

| STEEL | −3.321 | −4.813 b | −3.308 c | ||||||||

| PAPER | −0.143 | −1.508 | −0.569 | ||||||||

| NON-FERROUS | −2.467 | −1.517 | −2.331 | ||||||||

| MACHINERY | −3.755 c | −40.268 | −2.184 | ||||||||

| ELECTRICS | −2.833 | −2.715 | −2.446 | ||||||||

| OTHERS | −2.169 | −2.937 | −2.053 | ||||||||

| Number of obs. | 71 | 71 | 71 | 71 | 71 | 71 | 71 | 71 | 71 | ||

| LR chi2(8) | 17.55 b | 24.63 b | 43.71 a | 37.8 a | 45.56 a | 75.53 a | 46.66 a | 52.35 a | 69.00 a | ||

| Pseudo R2 | 0.085 | 0.119 | 0.211 | 0.187 | 0.226 | 0.374 | 0.122 | 0.137 | 0.180 | ||

| Factors to be Affected by Carbon Management | Mean | Min | Max |

|---|---|---|---|

| Domestic and international competitiveness | 3.12 | 1 | 5 |

| Production cost savings | 3.44 | 1 | 5 |

| Profit increase | 3.00 | 1 | 5 |

| Corporate image improvement | 3.62 | 1 | 5 |

| Emission reduction cost savings | 3.41 | 1 | 5 |

| Overall | 3.29 | 1 | 5 |

| Supportive Policies | Mean | Min | Max |

|---|---|---|---|

| Consistency and transparency of policy | 3.89 | 2 | 5 |

| Financial support (tax incentives, lending with low interest, etc.) | 2.44 | 1 | 5 |

| Support mechanisms to expand low-carbon technology market | 2.62 | 1 | 5 |

| Training on tools for carbon management | 2.47 | 1 | 5 |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Suk, S. Determinants and Characteristics of Korean Companies’ Carbon Management under the Carbon Pricing Scheme. Energies 2018, 11, 966. https://doi.org/10.3390/en11040966

Suk S. Determinants and Characteristics of Korean Companies’ Carbon Management under the Carbon Pricing Scheme. Energies. 2018; 11(4):966. https://doi.org/10.3390/en11040966

Chicago/Turabian StyleSuk, Sunhee. 2018. "Determinants and Characteristics of Korean Companies’ Carbon Management under the Carbon Pricing Scheme" Energies 11, no. 4: 966. https://doi.org/10.3390/en11040966

APA StyleSuk, S. (2018). Determinants and Characteristics of Korean Companies’ Carbon Management under the Carbon Pricing Scheme. Energies, 11(4), 966. https://doi.org/10.3390/en11040966