Long-Run Trade Relationship between the U.S. and Canada: The Case of the Canadian Dollar with the U.S. Dollar

Abstract

1. Background to Study

2. Literature Review

2.1. Exchange Rate Determination

2.2. Real and Nominal Shocks

2.3. Structural Vector Autoregressions

3. Methodology

3.1. Nominal and Real Shocks

3.2. Nominal and Real Exchange Rate

3.3. Structural VAR Model

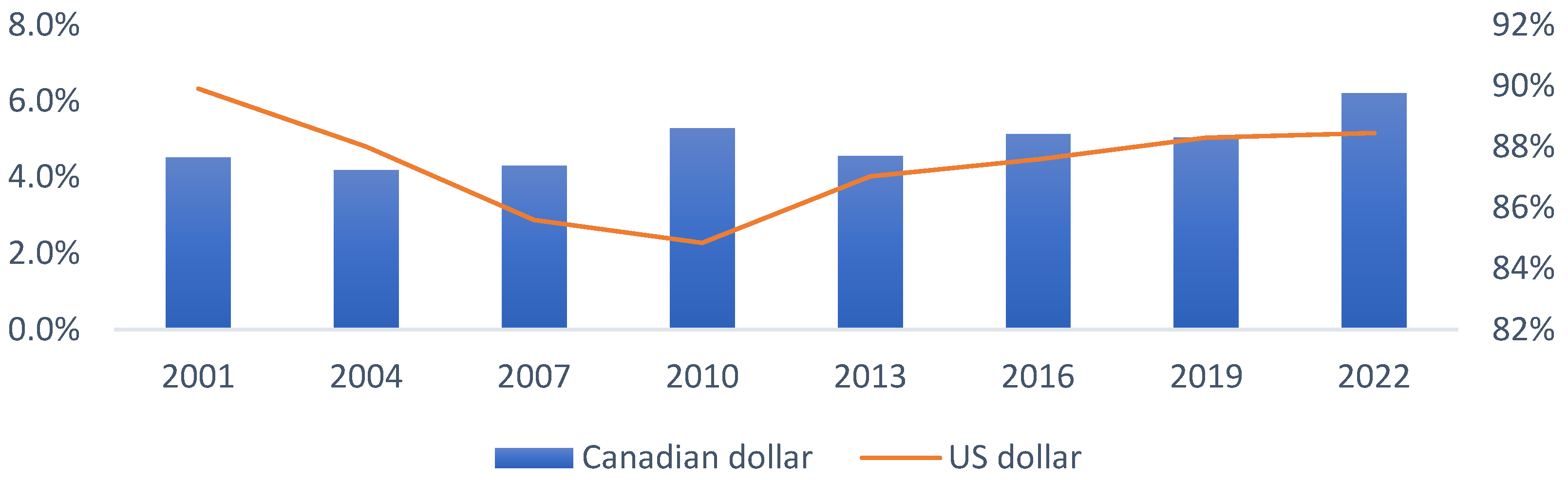

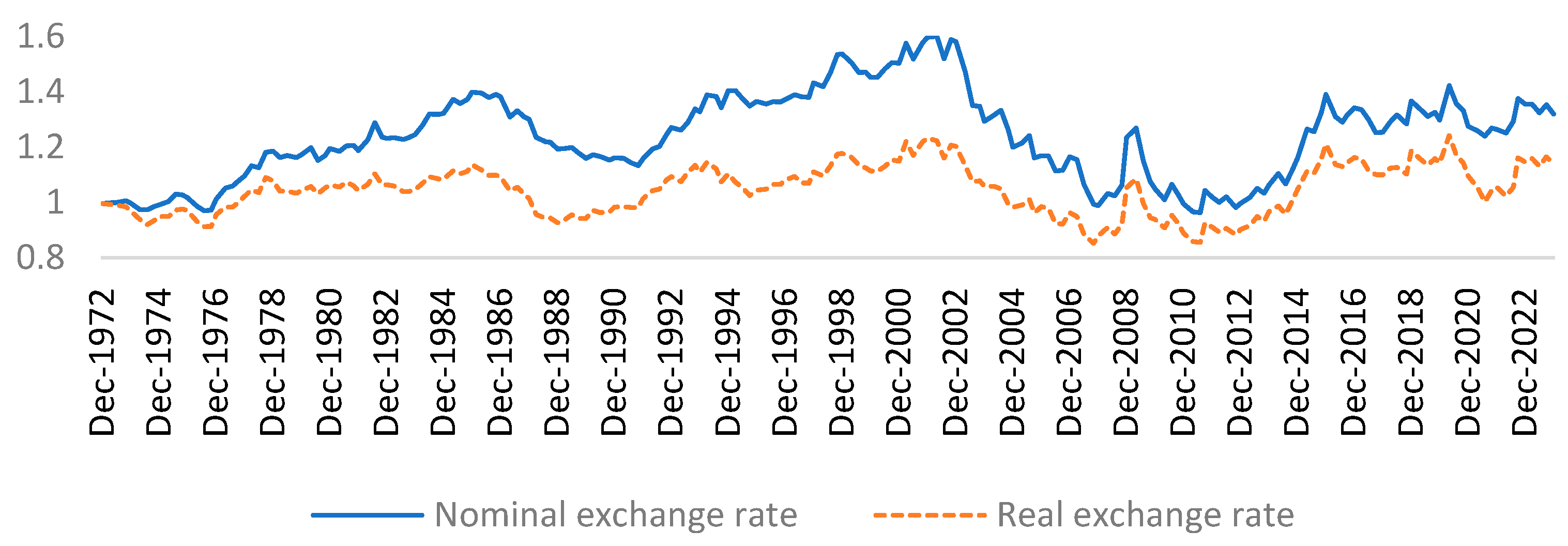

4. Data

Preliminary Analysis

5. Research Findings

5.1. Lag Optimization

5.2. Structural VAR

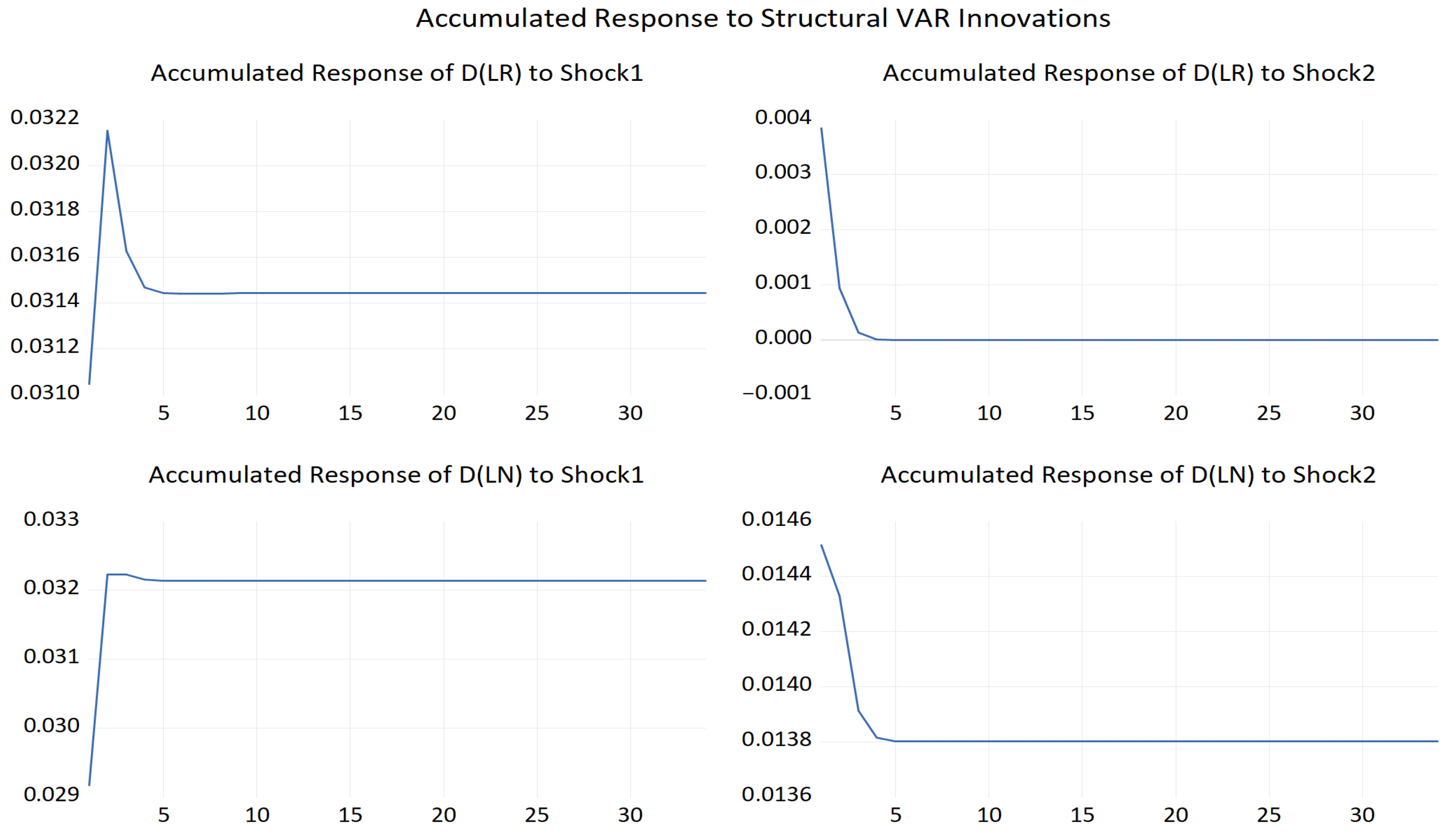

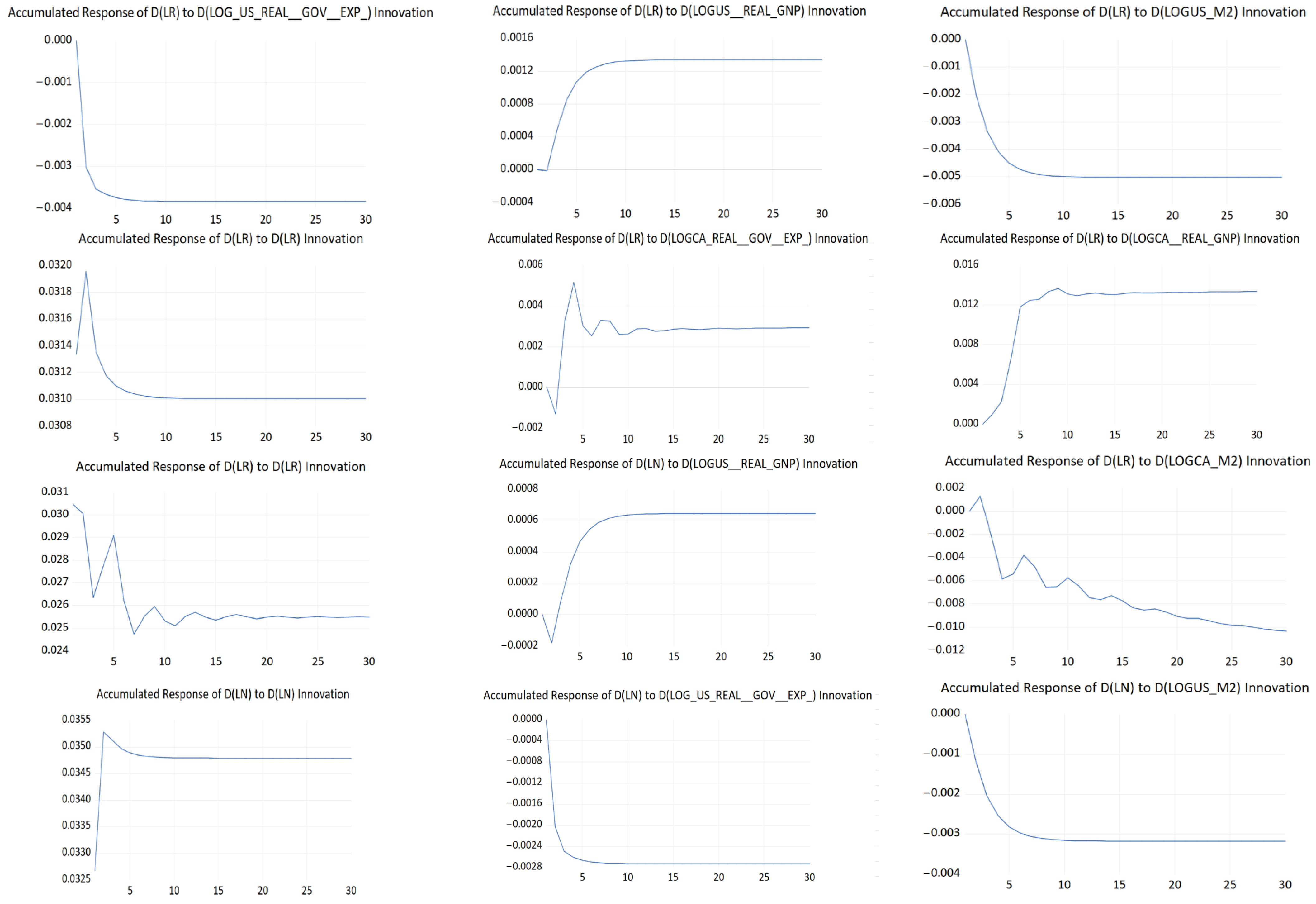

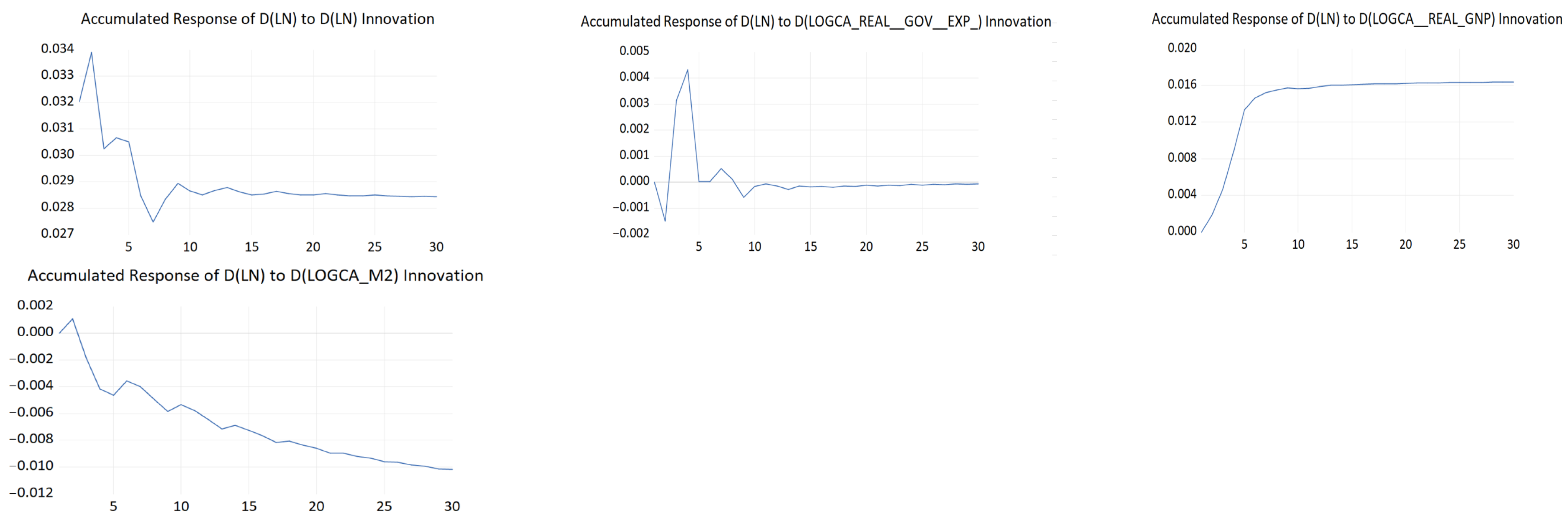

5.3. Impulse Responses

5.4. Real and Nominal Shocks

6. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Adaramola, Anthony Olugbenga, and Oluwabunmi Dada. 2020. Impact of inflation on economic growth: Evidence from Nigeria. Investment Management & Financial Innovations 17: 1–13. [Google Scholar] [CrossRef]

- Ahmad, Ahmad Hassan, Eric J. Pentecost, and Marie M. Stack. 2023. Foreign aid, debt interest repayments and Dutch disease effects in a real exchange rate model for African countries. Economic Modelling 126: 106434. [Google Scholar] [CrossRef]

- Arias, Jonas E., Juan F. Rubio-Ramírez, and Daniel F. Waggoner. 2018. Inference based on structural vector autoregressions identified with sign and zero restrictions: Theory and applications. Econometrica 86: 685–720. [Google Scholar] [CrossRef]

- Avdjiev, Stefan, Wenxin Du, Catherine Koch, and Hyun Song Shin. 2019. The dollar, bank leverage, and deviations from covered interest parity. American Economic Review: Insights 1: 193–208. [Google Scholar] [CrossRef]

- Baillie, Richard T., and Patrick C. McMahon. 1989. The Foreign Exchange Market: Theory and Econometric Evidence. Cambridge: Cambridge University Press. [Google Scholar]

- Balke, Nathan S. 2000. Credit and Economic Activity: Credit Regimes and Nonlinear Propagation of Shocks. Review of Economics and Statistics 82: 344–49. [Google Scholar] [CrossRef]

- Banbura, Marta, Domenico Giannone, and Lucrezia Reichlin. 2010. Large Bayesian Vector Autoregressions. Journal of Applied Econometrics 25: 71–92. [Google Scholar] [CrossRef]

- Bank for International Settlements. 2022. Triennial Central Bank Survey. Bank of International Settlements. Available online: https://www.bis.org/statistics/rpfx22.htm (accessed on 12 December 2023).

- Baumeister, Christiane, and James D. Hamilton. 2019. Structural interpretation of vector autoregressions with incomplete identification: Revisiting the role of oil supply and demand shocks. American Economic Review 109: 1873–910. [Google Scholar] [CrossRef]

- Bénétrix, Agustín S., and Philip R. Lane. 2013. Fiscal shocks and the real exchange rate. International Journal of Central Banking 32: 1–32. Available online: https://www.ijcb.org/journal/ijcb13q3a1.htm (accessed on 12 December 2023).

- Blanchard, Olivier Jean, and Danny Quah. 1988. The Dynamic Effects of Aggregate Demand and Supply Disturbances (Working Paper No. 2737). National Bureau of Economic Research. Available online: https://www.nber.org/system/files/working_papers/w2737/w2737.pdf (accessed on 12 December 2023).

- Bouakez, Hafedh, and Aurélien Eyquem. 2015. Government spending, monetary policy, and the real exchange rate. Journal of International Money and Finance 56: 178–201. [Google Scholar] [CrossRef]

- Bruno, Valentina, and Hyun Song Shin. 2023. Dollar and exports. The Review of Financial Studies 36: 2963–96. [Google Scholar] [CrossRef]

- Bussière, Matthieu, Guillaume Gaulier, and Walter Steingress. 2020. Global trade flows: Revisiting the exchange rate elasticities. Open Economies Review 31: 25–78. [Google Scholar] [CrossRef]

- Butt, Shamaila, Muhammad Ramzan, Wing-Keung Wong, Muhammad Ali Chohan, and Suresh Ramakrishnan. 2023. Unlocking the secrets of exchange rate determination in Malaysia: A Game-Changing hybrid model. Heliyon 9: e19140. [Google Scholar] [CrossRef] [PubMed]

- Canada Action. 2024. Environmental Leadership in Natural Resources. Available online: https://www.canada.ca/en/natural-resources-canada/news/2021/06/canada-in-a-changing-climate-national-issues-report.html (accessed on 10 February 2024).

- Canada Nuclear Safety Commission. 2023. Regulatory Action. Available online: https://www.cnsc-ccsn.gc.ca/eng/acts-and-regulations/regulatory-action/impala-canada-ltd/ (accessed on 15 March 2024).

- Canadian Association of Petroleum Producers. n.d. Oil and Natural Gas in Canada. Available online: https://www.capp.ca/energy/canadas-energy-mix/ (accessed on 12 January 2024).

- Carriero, Andrea, Todd E. Clark, and Massimiliano Marcellino. 2019. Large Bayesian vector autoregressions with stochastic volatility and non-conjugate priors. Journal of Econometrics 212: 137–54. [Google Scholar] [CrossRef]

- Carrière-Swallow, Yan, Nicolás E. Magud, and Juan F. Yépez. 2021. Exchange rate flexibility, the real exchange rate, and adjustment to terms-of-trade shocks. Review of International Economics 29: 439–83. [Google Scholar] [CrossRef]

- Charfeddine, Lanouar, and Karim Barkat. 2020. Short-and long-run asymmetric effect of oil prices and oil and gas revenues on the real GDP and economic diversification in oil-dependent economy. Energy Economics 86: 104680. [Google Scholar] [CrossRef]

- Chicago Mercantile Exchange Group. 2024. Crude Oil Futures and Options. CME Group. Available online: https://www.cmegroup.com/markets/energy/crude-oil/light-sweet-crude.html (accessed on 21 March 2024).

- Demir, Firat, and Arslan Razmi. 2022. The real exchange rate and development theory, evidence, issues and challenges. Journal of Economic Surveys 36: 386–428. [Google Scholar] [CrossRef]

- Dibooglu, Selahattin, and Walter Enders. 1995. Multiple cointegrating vectors and structural economic models: An application to the French Franc/US Dollar exchange rate. Southern Economic Journal 61: 1098–116. [Google Scholar] [CrossRef]

- Dogru, Tarik, Cem Isik, and Ercan Sirakaya-Turk. 2019. The balance of trade and exchange rates: Theory and contemporary evidence from tourism. Tourism Management 74: 12–23. [Google Scholar] [CrossRef]

- Dornbusch, Rudiger. 1976. Expectations and exchange rate dynamics. Journal of political Economy 84: 1161–76. [Google Scholar] [CrossRef]

- Eichenbaum, Martin, Benjamin K. Johannsen, and Sergio Rebelo. 2021. Monetary policy and the predictability of nominal exchange rates. The Review of Economic Studies 88: 192–228. [Google Scholar] [CrossRef]

- Enders, Walter. 2014. Applied Econometric Time Series. New York: Wiley. [Google Scholar]

- Enders, Walter, and Bong-Soo Lee. 1997. Accounting for real and nominal exchange rate movements in the post-Bretton Woods period. Journal of International Money and Finance 16: 233–54. [Google Scholar] [CrossRef]

- Evans, George W. 1987. Output and Unemployment Dynamics in the United States: 1950–1985. London: London School of Economics. [Google Scholar]

- Factset. 2024. Investment Research. Available online: https://www.factset.com/solutions/investment-research (accessed on 16 January 2024).

- Fisher, Lance A., and Hyeon-Seung Huh. 2002. Real exchange rates, trade balances and nominal shocks: Evidence for the G-7. Journal of International Money and Finance 21: 497–518. [Google Scholar] [CrossRef]

- Frankel, Jeffrey A., and Andrew K. Rose. 1995. Empirical research on nominal exchange rates. Handbook of International Economics 3: 1689–729. [Google Scholar] [CrossRef]

- Frenkel, Jacob A. 1976. Inflation and the Formation of Expectations. Journal of Monetary Economics 1: 403–21. [Google Scholar] [CrossRef]

- Global Affairs Canada. 2020. The Canada-United States-Mexico Agreement: Economic Impact Assessment. Available online: https://www.international.gc.ca/trade-commerce/assets/pdfs/agreements-accords/cusma-aceum/cusma-impact-repercussion-eng.pdf (accessed on 19 July 2024).

- Government of Canada. 2024. Coal Facts. Available online: https://natural-resources.canada.ca/our-natural-resources/minerals-mining/mining-data-statistics-and-analysis/minerals-metals-facts/coal-facts/20071 (accessed on 14 April 2024).

- Granger, Clive W. J., and Timo Teräsvirta. 1993. Modeling Nonlinear Economic Relationships. Oxford: Oxford University Press. [Google Scholar]

- Greenwood, Robin, Samuel Hanson, Jeremy C. Stein, and Adi Sunderam. 2023. A quantity-driven theory of term premia and exchange rates. The Quarterly Journal of Economics 138: 2327–89. [Google Scholar] [CrossRef]

- Gründler, Daniel, Eric Mayer, and Johann Scharler. 2023. Monetary policy announcements, information shocks, and exchange rate dynamics. Open Economies Review 34: 341–69. [Google Scholar] [CrossRef]

- Gurrib, Ikhlaas, and Firuz Kamalov. 2019. The implementation of an adjusted relative strength index model in foreign currency and energy markets of emerging and developed economies. Macroeconomics and Finance in Emerging Market Economies 12: 105–23. [Google Scholar] [CrossRef]

- Gurrib, Ikhlaas, and Firuz Kamalov. 2022. Predicting bitcoin price movements using sentiment analysis: A machine learning approach. Studies in Economics and Finance 39: 347–64. [Google Scholar] [CrossRef]

- Gurrib, Ikhlaas, Firuz Kamalov, Olga Starkova, Adham Makki, Anita Mirchandani, and Namrata Gupta. 2023. Performance of Equity Investments in Sustainable Environmental Markets. Sustainability 15: 7453. [Google Scholar] [CrossRef]

- Gürkaynak, Refet S., A. Hakan Kara, Burçin Kısacıkoğlu, and Sang Seok Lee. 2021. Monetary policy surprises and exchange rate behavior. Journal of International Economics 130: 103443. [Google Scholar] [CrossRef]

- Hanif, Waqas, Walid Mensi, Mohammad Alomari, and Jorge Miguel Andraz. 2023. Downside and upside risk spillovers between precious metals and currency markets: Evidence from before and during the COVID-19 crisis. Resources Policy 81: 103350. [Google Scholar] [CrossRef]

- Huang, Chunhua. 2020. Research on the linkage relationship between different levels of money supply and economic growth based on VAR model. Paper presented at 2020 2nd International Conference on Economic Management and Model Engineering (ICEMME), Chongqing, China, 20–22 November. [Google Scholar]

- International Energy Agency. 2022. Canada 2022: Energy Policy Review. February 26. Available online: https://www.iea.org/reports/canada-2022 (accessed on 2 January 2024).

- Ji, Qiang, Syed Jawad Hussain Shahzad, Elie Bouri, and Muhammad Tahir Suleman. 2020. Dynamic structural impacts of oil shocks on exchange rates: Lessons to learn. Journal of Economic Structures 9: 1–19. [Google Scholar] [CrossRef]

- Jia, Yanjing, Zhiliang Dong, and Haigang An. 2023. Study of the modal evolution of the causal relationship between crude oil, gold, and dollar price series. International Journal of Energy Research 2023: 7947434. [Google Scholar] [CrossRef]

- Kamalov, Firuz, and Ikhlaas Gurrib. 2022. Machine learning-based forecasting of significant daily returns in foreign exchange markets. International Journal of Business Intelligence and Data Mining 21: 465–83. [Google Scholar] [CrossRef]

- Kamalov, Firuz, Ikhlaas Gurrib, and Khairan Rajab. 2021. Financial forecasting with machine learning: Price vs. return. Journal of Computer Science 17: 251–64. [Google Scholar] [CrossRef]

- Kelesbayev, Dinmukhamed, Kundyz Myrzabekkyzy, Artur Bolganbayev, and Sabit Baimaganbetov. 2022. The impact of oil prices on the stock market and real exchange rate: The case of Kazakhstan. International Journal of Energy Economics and Policy 12: 163–68. [Google Scholar] [CrossRef]

- Kilian, Lutz. 2013. Structural vector autoregressions. In Handbook of Research Methods and Applications in Empirical Macroeconomics. Cheltenham: Edward Elgar Publishing, pp. 515–54. [Google Scholar]

- Kilian, Lutz, and Helmut Lütkepohl. 2017. Structural Vector Autoregressive Analysis. Cambridge: Cambridge University Press. [Google Scholar]

- Kim, Jin-Ock, and Walter Enders. 1991. Real and monetary causes of real exchange rate movements in the Pacific Rim. Southern Economic Journal 57: 1061–70. [Google Scholar] [CrossRef]

- King, Robert G., and Mark W. Watson. 1992. Testing Long Run Neutrality (September 1992). NBER Working Paper No. w4156. Available online: https://ssrn.com/abstract=226809 (accessed on 15 December 2023).

- Krolzig, Hans-Martin. 2013. Markov-Switching Vector Autoregressions: Modelling, Statistical Inference, and Application to Business Cycle Analysis. Berlin/Heidelberg: Springer Science & Business Media, vol. 454. [Google Scholar]

- Kuan, Chung-Ming, and Tung Liu. 1995. Forecasting exchange rates using feedforward and recurrent neural networks. Journal of Applied Econometrics 10: 347–64. [Google Scholar] [CrossRef]

- Lane, Philip R., and Gian Maria Milesi-Ferretti. 2007. The external wealth of nations mark II: Revised and extended estimates of foreign assets and liabilities, 1970–2004. Journal of international Economics 73: 223–50. [Google Scholar] [CrossRef]

- Lavoie, Marc, and Mario Seccareccia. 2006. The Bank of Canada and the modern view of central banking. International Journal of Political Economy 35: 44–61. [Google Scholar] [CrossRef]

- Lee, Chien-Chiang, and Jafar Hussain. 2023. An assessment of socioeconomic indicators and energy consumption by considering green financing. Resources Policy 81: 103374. [Google Scholar] [CrossRef]

- Ling, Shiqing, and Michael McAleer. 2003. Asymptotic theory for a vector ARMA-GARCH model. Econometric Theory 19: 280–310. [Google Scholar] [CrossRef]

- Liu, Donghui, Lingjie Meng, and Yudong Wang. 2020. Oil price shocks and Chinese economy revisited: New evidence from SVAR model with sign restrictions. International Review of Economics & Finance 69: 20–32. [Google Scholar]

- Malik, Farooq, and Zaghum Umar. 2019. Dynamic connectedness of oil price shocks and exchange rates. Energy Economics 84: 104501. [Google Scholar] [CrossRef]

- Mao, Yuntao, Ziwei Chen, Siyuan Liu, and Yanfeng Li. 2024. Unveiling the potential: Exploring the predictability of complex exchange rate trends. Engineering Applications of Artificial Intelligence 133: 108112. [Google Scholar] [CrossRef]

- Meese, Richard A., and Kenneth Rogoff. 1983. Empirical exchange rate models of the seventies: Do they fit out of sample? Journal of International Economics 14: 3–24. [Google Scholar] [CrossRef]

- Moulle-Berteaux, Cyril. 2023. Global Multi-Asset Viewpoint: The Five Forces of Secular Inflation. Morgan Stanley Investment Management. Available online: https://www.morganstanley.com/im/publication/insights/articles/article_thefiveforcesofsecularinflation.pdf (accessed on 15 December 2023).

- Mussa, Michael. 1976. Adaptive and regressive expectations in a rational model of the inflationary process. Journal of Monetary Economics 1: 423–42. [Google Scholar] [CrossRef]

- Nakatani, Ryota. 2017. The effects of productivity shocks, financial shocks, and monetary policy on exchange rates: An application of the currency crisis model and implications for emerging market crises. Emerging Markets Finance and Trade 53: 2545–61. [Google Scholar] [CrossRef]

- Natural Resources Canada. 2023. Energy Factbook 2023–24. Available online: https://energy-information.canada.ca/sites/default/files/2023-10/energy-factbook-2023-2024.pdf (accessed on 16 February 2024).

- Plotnick, Alan R. 1963. Oil Imports: Protectionism vs. National Security. Challenge 11: 28–32. [Google Scholar] [CrossRef]

- Sarangi, Pradeepta Kumar, Muskaan Chawla, Pinaki Ghosh, Sunny Singh, and P. K. Singh. 2022. FOREX trend analysis using machine learning techniques: INR vs. USD currency exchange rate using ANN-GA hybrid approach. Materials Today: Proceedings 49: 3170–76. [Google Scholar] [CrossRef]

- Sarno, Lucio, and Mark P. Taylor. 2001. Official intervention in the foreign exchange market: Is it effective and, if so, how does it work? Journal of Economic Literature 39: 839–68. [Google Scholar] [CrossRef]

- Sánchez, Juan José García. 2023. American Protectionism: Can It Work? Epicenter At the Heart of Research and Ideas, Harvard University. August 16. Available online: https://epicenter.wcfia.harvard.edu/blog/american-protectionism-can-it-work (accessed on 23 May 2024).

- Sims, Christopher A. 1980. Macroeconomics and reality. Econometrica: Journal of the Econometric Society 48: 1–48. [Google Scholar] [CrossRef]

- Sokhanvar, Amin, and Chien-Chiang Lee. 2023. How do energy price hikes affect exchange rates during the war in Ukraine? Empirical Economics 64: 2151–64. [Google Scholar] [CrossRef]

- Sokhanvar, Amin, Serhan Çiftçioğlu, and Chien-Chiang Lee. 2023. The effect of energy price shocks on commodity currencies during the war in Ukraine. Resources Policy 82: 103571. [Google Scholar] [CrossRef]

- Suhendra, Indra, and Cep Jandi Anwar. 2022. The response of asset prices to monetary policy shock in Indonesia: A structural VAR approach. Banks and Bank Systems 17: 104–14. [Google Scholar] [CrossRef]

- Tan, Eu Chye, Chor Foon Tang, and Rupah Devi Palaniandi. 2022. What could cause a country’s GNP to be greater than its GDP? The Singapore Economic Review 67: 557–66. [Google Scholar] [CrossRef]

- Yilmazkuday, Hakan. 2023. COVID-19 effects on the S&P 500 index. Applied Economics Letters 30: 7–13. [Google Scholar]

- Yıldız, Bünyamin Fuat, Siamand Hesami, Husam Rjoub, and Wing-Keung Wong. 2021. Interpretation of oil price shocks on macroeconomic aggregates of South Africa: Evidence from SVAR. The Journal of Contemporary Issues in Business and Government 27: 279–87. [Google Scholar]

- Youssef, Manel, and Khaled Mokni. 2020. Modeling the relationship between oil and USD exchange rates: Evidence from a regime-switching-quantile regression approach. Journal of Multinational Financial Management 55: 100625. [Google Scholar] [CrossRef]

- Zhou, Su. 1995. The response of real exchange rates to various economic shocks. Southern Economic Journal 61: 936–54. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| WPI_CA | WPI_U.S. | Nominal USD/CAD | Real USD/CAD | WPI-U.S./ WPI-CA | ||

| Mean | 391.678 | 330.030 | 1.237 | 1.043 | 0.849 | |

| Median | 401.115 | 310.709 | 1.244 | 1.052 | 0.856 | |

| Standard deviation | 142.439 | 121.213 | 0.158 | 0.088 | 0.057 | |

| Kurtosis | −0.331 | −0.602 | −0.650 | −0.783 | −0.549 | |

| Skewness | −0.049 | 0.190 | 0.083 | −0.075 | 0.250 | |

| Jarque-Bera | 1.019 | 4.319 | 3.843 | 5.427 | 4.713 | |

| p-value | 0.601 | 0.115 | 0.146 | 0.066 | 0.095 | |

| ADF | −0.358 | 0.244 | −0.1250 | −2.5970 | −2.6080 | |

| p-value | 0.9124 | 0.9747 | 0.2350 | 0.0953 | 0.0930 | |

| Observations | 205 | 205 | 205 | 205 | 205 | |

| U.S. Real Gov. Exp. | CA Real Gov. Exp. | U.S. Real GNP | CA Real GNP | U.S. Money Supply | CA Money Supply | |

| Mean | 2752 | 336 | 13.230 | 1.120 | 6483.614 | 706.313 |

| Median | 2709 | 313 | 12 | 0.905 | 4184.100 | 449.658 |

| Standard deviation | 669 | 84 | 5 | 0.750 | 5543.982 | 639.924 |

| Kurtosis | −1.267 | −0.864 | −1.265 | −0.766 | 0.765 | 0.639 |

| Skewness | −0.199 | 0.353 | 0.186 | 0.546 | 1.258 | 1.229 |

| Jarque-Bera | 15.068 | 10.634 | 14.853 | 15.187 | 59.052 | 55.070 |

| p-value | 0.001 | 0.005 | 0.001 | 0.001 | 0.000 | 0.000 |

| ADF | −0.4620 | 1.5730 | 1.4430 | 2.9980 | 2.7830 | 3.7530 |

| p-value | 0.8946 | 0.9995 | 0.9991 | 1.0000 | 1.0000 | 1.0000 |

| Observations | 205 | 205 | 205 | 205 | 205 | 205 |

| WPI_CA | WPI_U.S. | Nominal USD/CAD | Real USD/CAD | WPI-U.S. /WPI-CA | U.S. Real Gov. Exp. | CA Real Gov. Exp. | U.S. Real GNP | CA Real GNP | U.S. Money Supply | |

|---|---|---|---|---|---|---|---|---|---|---|

| WPI_U.S. | 0.988 | 1.000 | ||||||||

| p-value | 0.000 | 0.000 | ||||||||

| Nominal USD/CAD | 0.301 | 0.183 | 1.000 | |||||||

| p-value | 0.000 | 0.000 | 0.000 | |||||||

| Real USD/CAD | 0.238 | 0.174 | 0.881 | 1.000 | ||||||

| p-value | 0.000 | 0.012 | 0.000 | 0.000 | ||||||

| WPI-U.S./WPI-CA | (0.328) | (0.187) | (0.795) | (0.421) | 1.000 | |||||

| p-value | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| U.S. Real Gov. Exp. | 0.957 | 0.955 | 0.196 | 0.130 | (0.256) | 1.000 | ||||

| p-value | 0.000 | 0.000 | 0.000 | 0.063 | 0.000 | 0.000 | ||||

| CA Real Gov. Exp. | 0.968 | 0.988 | 0.135 | 0.155 | (0.118) | 0.961 | 1.000 | |||

| p-value | 0.000 | 0.000 | 0.054 | 0.026 | 0.092 | 0.000 | 0.000 | |||

| U.S. Real GNP | 0.965 | 0.975 | 0.184 | 0.187 | (0.159) | 0.973 | 0.982 | 1.000 | ||

| p-value | 0.000 | 0.000 | 0.000 | 0.000 | 0.022 | 0.000 | 0.000 | 0.000 | ||

| CA Real GNP | 0.962 | 0.982 | 0.133 | 0.169 | (0.089) | 0.945 | 0.991 | 0.988 | 1.000 | |

| p-value | 0.000 | 0.000 | 0.058 | 0.016 | 0.206 | 0.000 | 0.000 | 0.000 | 0.000 | |

| U.S. Money supply | 0.905 | 0.930 | 0.123 | 0.216 | (0.013) | 0.857 | 0.952 | 0.928 | 0.966 | 1.000 |

| p-value | 0.000 | 0.000 | 0.078 | 0.000 | 0.855 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| CA Money supply | 0.906 | 0.934 | 0.117 | 0.215 | (0.002) | 0.858 | 0.955 | 0.927 | 0.967 | 0.998 |

| p-value | 0.000 | 0.000 | 0.096 | 0.000 | 0.978 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| ρ(k) | k = 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Without first order differencing | |||||

| NER | 0.961 | 0.916 | 0.879 | 0.838 | 0.796 |

| RER | 0.93 | 0.856 | 0.801 | 0.737 | 0.663 |

| With first order differencing | |||||

| NER | 0.081 | −0.101 | 0.036 | 0.016 | −0.057 |

| RER | 0.025 | −0.137 | 0.06 | 0.075 | −0.056 |

| Lag | LogL | LR | FPE | AIC | SC | HQ |

|---|---|---|---|---|---|---|

| 0 | 999.609 | NA | 1.3 × 107 | −10.180 | −10.146 | −10.166 |

| 1 | 1010.102 | 20.663 | 1.22 × 107 | −10.246 | −10.145 | −10.205 |

| 2 | 1012.760 | 5.181 | 1.23 × 107 | −10.232 | −10.064 | −10.164 |

| 3 | 1015.074 | 4.462 | 1.26 × 107 | −10.215 | −9.981 | −10.120 |

| 4 | 1019.371 | 8.201 | 1.25 × 107 | −10.218 | −9.917 | −10.096 |

| 5 | 1021.178 | 3.411 | 1.28 × 107 | −10.195 | −9.983 | −10.046 |

| Variable | ∆RER | ∆RER | ∆NER | ∆NER |

|---|---|---|---|---|

| Shock | ||||

| 1-quarter | 98.489 | 1.511 | 80.153 | 19.847 |

| 3-quarters | 97.589 | 2.411 | 80.311 | 19.689 |

| 5-quarters | 97.588 | 2.412 | 80.311 | 19.689 |

| 7-quarters | 97.588 | 2.412 | 80.311 | 19.689 |

| 9-quarters | 97.588 | 2.412 | 80.311 | 19.689 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gurrib, I.; Kamalov, F.; Atayah, O.; Hemdan, D.; Starkova, O. Long-Run Trade Relationship between the U.S. and Canada: The Case of the Canadian Dollar with the U.S. Dollar. J. Risk Financial Manag. 2024, 17, 411. https://doi.org/10.3390/jrfm17090411

Gurrib I, Kamalov F, Atayah O, Hemdan D, Starkova O. Long-Run Trade Relationship between the U.S. and Canada: The Case of the Canadian Dollar with the U.S. Dollar. Journal of Risk and Financial Management. 2024; 17(9):411. https://doi.org/10.3390/jrfm17090411

Chicago/Turabian StyleGurrib, Ikhlaas, Firuz Kamalov, Osama Atayah, Dalia Hemdan, and Olga Starkova. 2024. "Long-Run Trade Relationship between the U.S. and Canada: The Case of the Canadian Dollar with the U.S. Dollar" Journal of Risk and Financial Management 17, no. 9: 411. https://doi.org/10.3390/jrfm17090411

APA StyleGurrib, I., Kamalov, F., Atayah, O., Hemdan, D., & Starkova, O. (2024). Long-Run Trade Relationship between the U.S. and Canada: The Case of the Canadian Dollar with the U.S. Dollar. Journal of Risk and Financial Management, 17(9), 411. https://doi.org/10.3390/jrfm17090411