_Zheng.png)

Bank Crisis Boosts Bitcoin Price

Abstract

1. Introduction

2. Literature Review

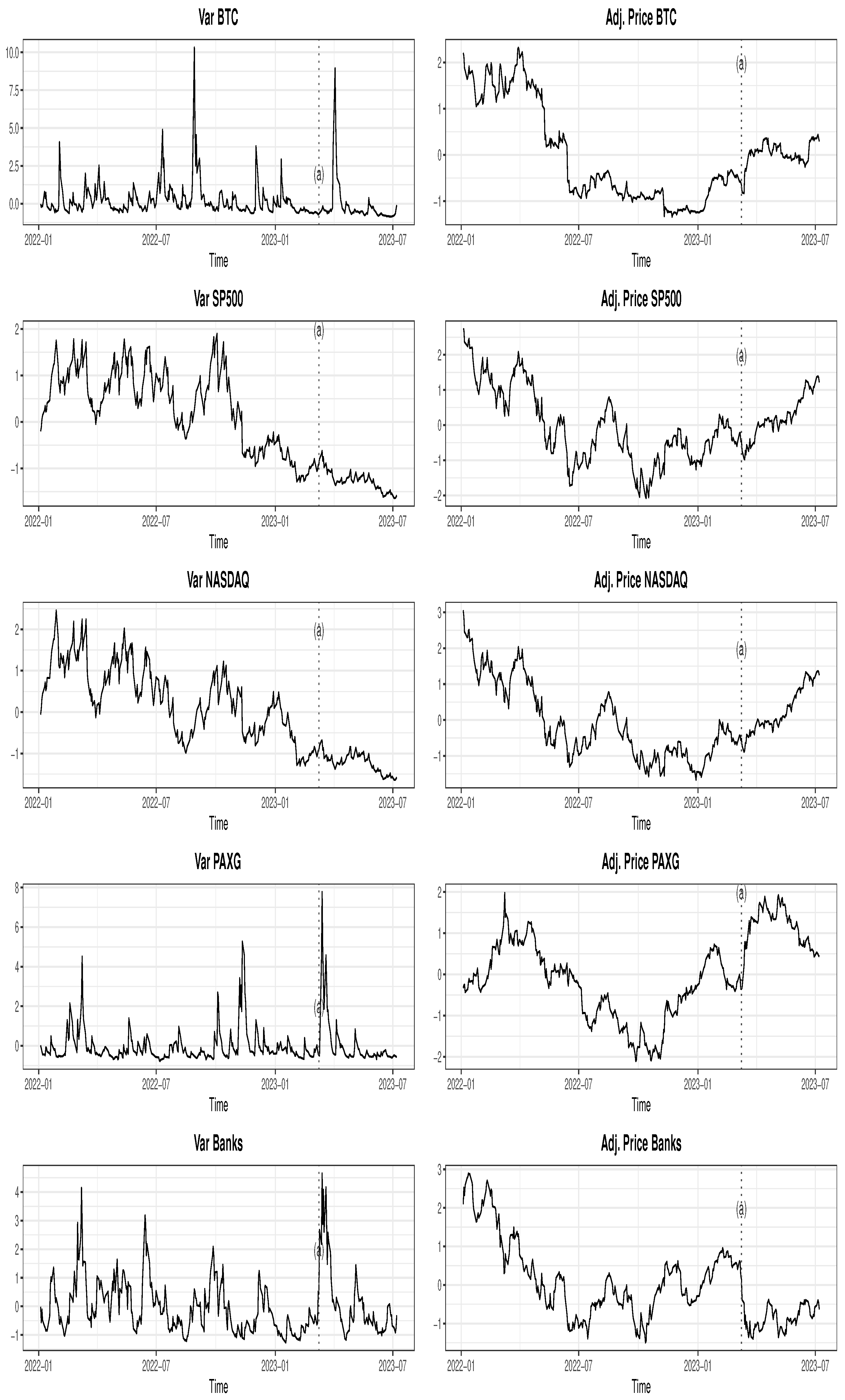

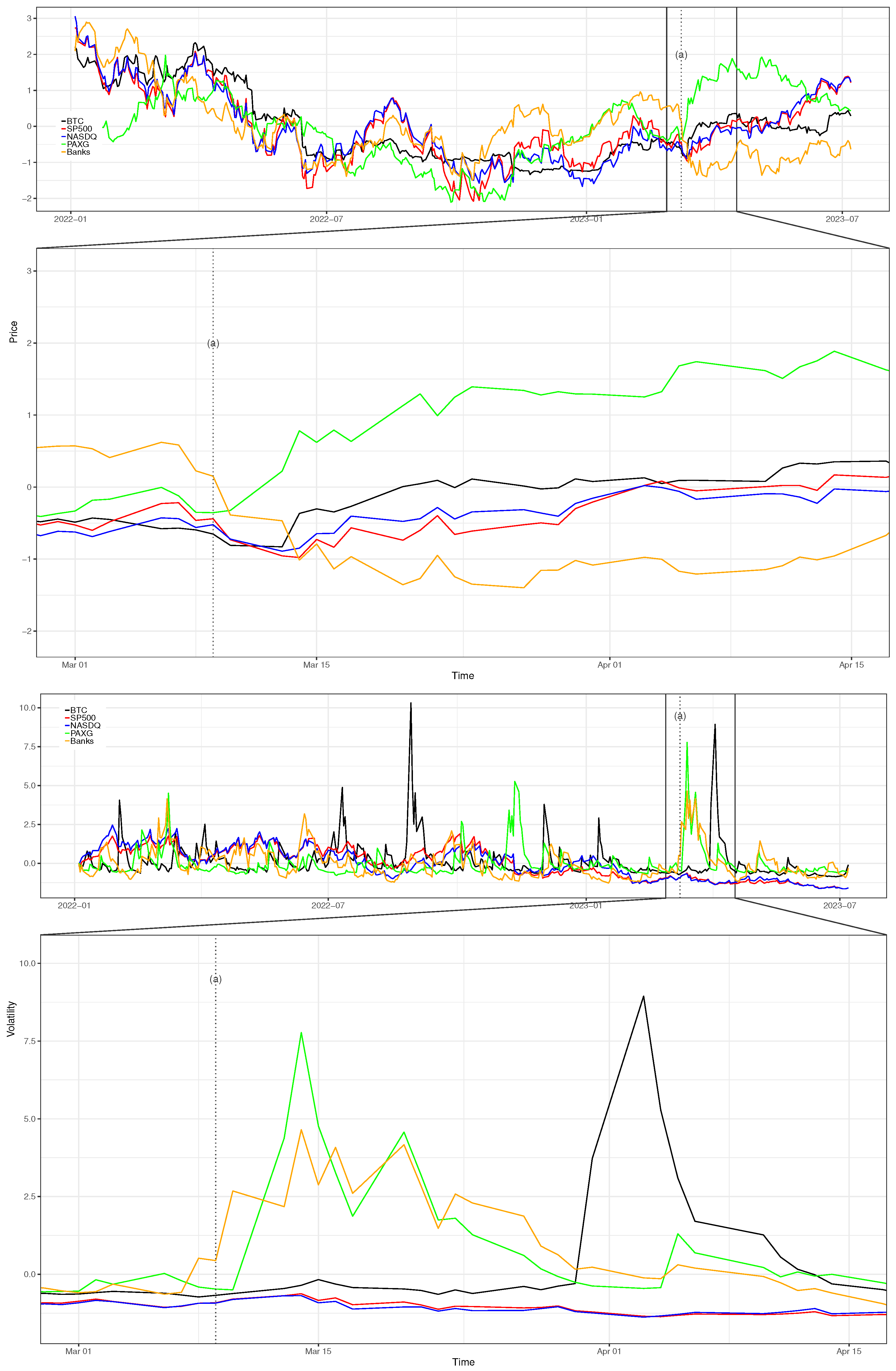

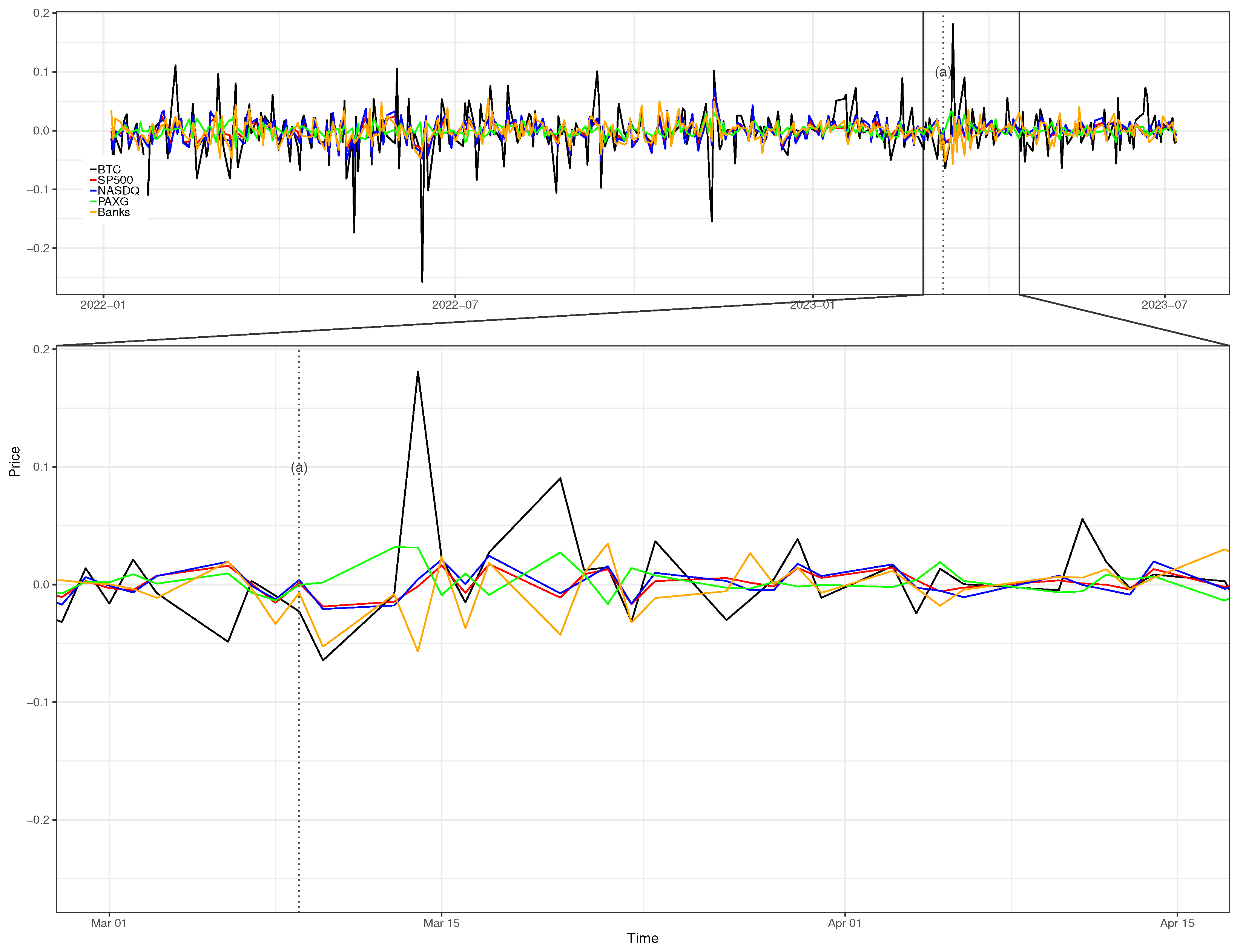

3. Macroeconomics Scenario

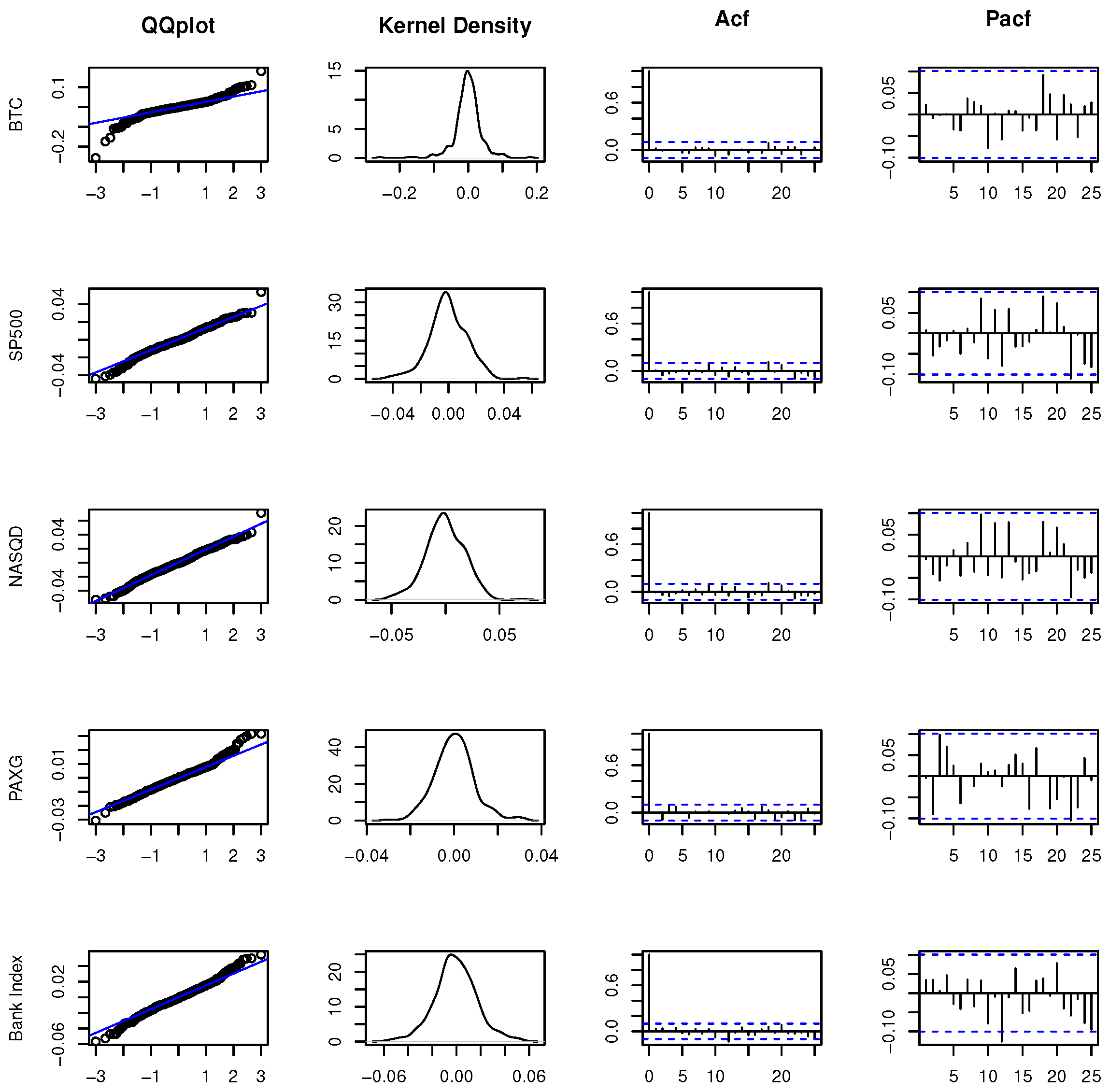

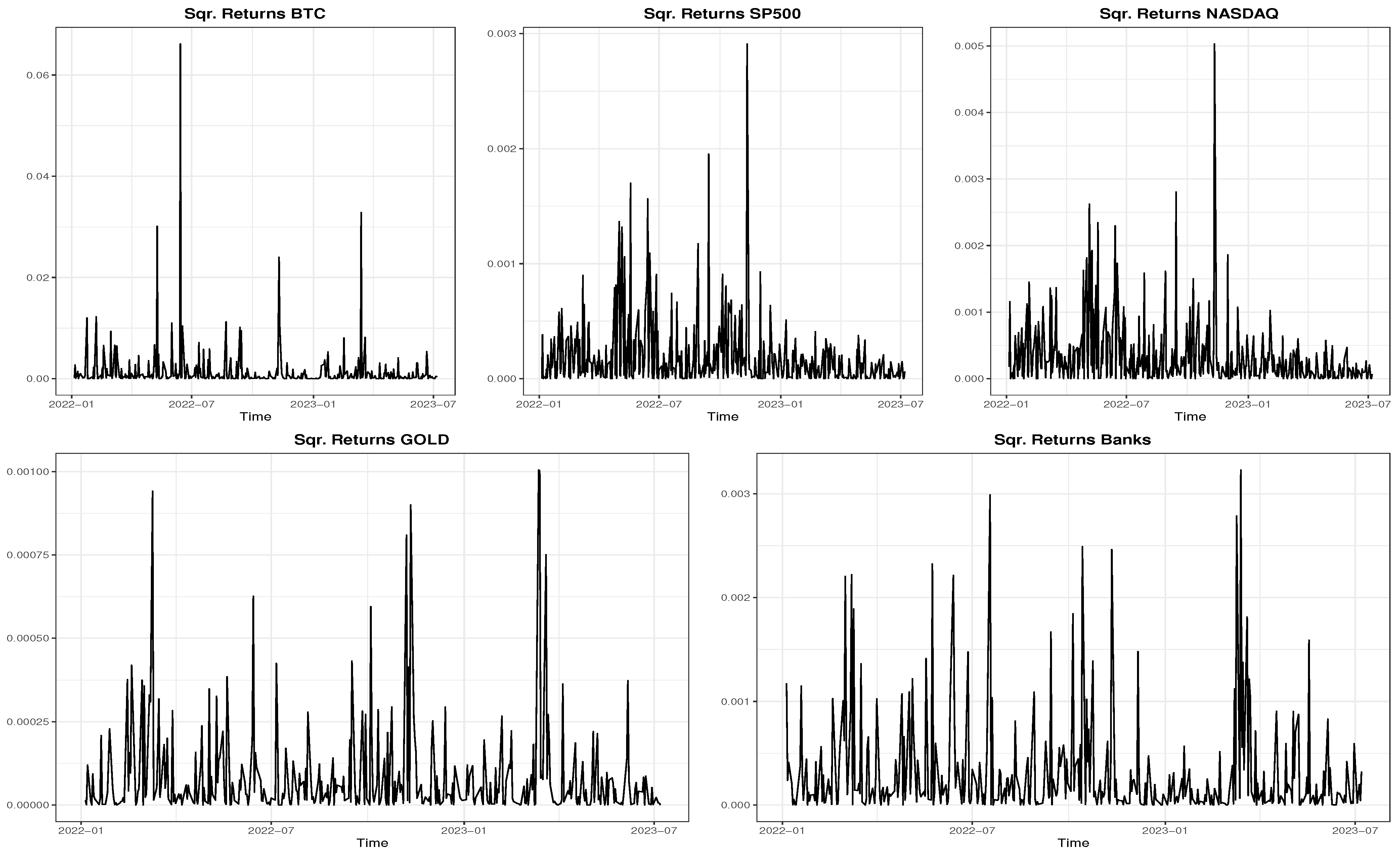

4. Data and Methodology

5. Analysis

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | Bitcoin is a cryptocurrency, or digital currency, that operates on a peer-to-peer network. |

| 2 | However, it should be noted that Bitcoin was emerging from the so-called crypto winter, and this may have contributed to the impressive growth. |

| 3 | The last access of web references was on 13 January 2024. |

References

- Ahn, Yongkil, and Dongyeon Kim. 2021. Emotional trading in the cryptocurrency market. Finance Research Letters 42: 101912. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and John W. Goodell. 2023. Did the collapse of silicon valley bank catalyze financial contagion? Finance Research Letters 56: 104082. [Google Scholar] [CrossRef]

- Almeida, José, and Tiago Cruz Gonçalves. 2023. A systematic literature review of investor behavior in the cryptocurrency markets. Journal of Behavioral and Experimental Finance 37: 100785. [Google Scholar] [CrossRef]

- Bhowmik, Roni, and Shouyang Wang. 2020. Stock market volatility and return analysis: A systematic literature review. Entropy 22: 522. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef]

- Bouri, Elie, Peter Molnár, Georges Azzi, David Roubaud, and Lars Ivar Hagfors. 2017. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192–98. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Jawad Hussain Shahzad, David Roubaud, Ladislav Kristoufek, and Brian Lucey. 2020. Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance 77: 156–64. [Google Scholar] [CrossRef]

- Butterfill, James. 2022. Digital Asset Fund Flows Weekly Report. Available online: https://blog.coinshares.com/volume-72-digital-asset-fund-flows-weekly-report-a4ac4ebf0fff (accessed on 13 March 2024).

- Böhme, Rainer, Nicolas Christin, Benjamin Edelman, and Tyler Moore. 2015. Bitcoin: Economics, technology, and governance. Journal of Economic Perspectives 29: 213–38. [Google Scholar] [CrossRef]

- Cheah, Eng-Tuck, and John Fry. 2015. Speculative bubbles in bitcoin markets? an empirical investigation into the fundamental value of bitcoin. Economics Letters 130: 32–36. [Google Scholar] [CrossRef]

- Ciaian, Pavel, Miroslava Rajcaniova, and d’Artis Kancs. 2016. The economics of Bitcoin price formation. Applied Economics 48: 1799–815. [Google Scholar] [CrossRef]

- Conlon, Thomas, and Richard McGee. 2020. Safe haven or risky hazard? bitcoin during the covid-19 bear market. Finance Research Letters 35: 101607. [Google Scholar] [CrossRef]

- Corbet, Shaen, Charles Larkin, and Brian Lucey. 2020. The contagion effects of the covid-19 pandemic: Evidence from gold and cryptocurrencies. Finance Research Letters 35: 101554. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016a. Bitcoin, gold and the dollar—A GARCH volatility analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016b. Hedging capabilities of bitcoin. Is it the virtual gold? Finance Research Letters 16: 139–44. [Google Scholar] [CrossRef]

- Frino, Alex, Steven Lecce, and Reuben Segara. 2011. The impact of trading halts on liquidity and price volatility: Evidence from the australian stock exchange. Pacific-Basin Finance Journal 19: 298–307. [Google Scholar] [CrossRef]

- Galati, Luca, and Francesco Capalbo. 2023. Silicon valley bank bankruptcy and stablecoins stability. International Review of Financial Analysis 91: 103001. [Google Scholar] [CrossRef]

- Ghalanos, Alexios. 2022. rugarch: Univariate GARCH Models. R Package Version 1.4-9. Available online: https://cran.r-project.org/web/packages/rugarch/index.html (accessed on 13 March 2024).

- Gowda, Nandan, and Chandrani Chakravorty. 2021. Comparative study on cryptocurrency transaction and banking transaction. Global Transitions Proceedings 2: 530–34. [Google Scholar] [CrossRef]

- Hamilton, James D. 2020. Time Series Analysis. Princeton: Princeton University Press. [Google Scholar]

- Hatemi-J, Abdulnasser, Mohamed A. Hajji, Elie Bouri, and Rangan Gupta. 2022. The benefits of diversification between bitcoin, bonds, equities and the us dollar: A matter of portfolio construction. Asia-Pacific Journal of Operational Research 39: 2040024. [Google Scholar] [CrossRef]

- Jareño, Francisco, María de la O González, Marta Tolentino, and Karen Sierra. 2020. Bitcoin and gold price returns: A quantile regression and nardl analysis. Resources Policy 67: 101666. [Google Scholar] [CrossRef]

- Klein, Tony, Hien Pham Thu, and Thomas Walther. 2018. Bitcoin is not the new gold – a comparison of volatility, correlation, and portfolio performance. International Review of Financial Analysis 59: 105–16. [Google Scholar] [CrossRef]

- Luther, William J., and Alexander W. Salter. 2017. Bitcoin and the bailout. The Quarterly Review of Economics and Finance 66: 50–56. [Google Scholar] [CrossRef]

- Lynch, David J. 2023. Silicon Valley Bank Failure Raises Fear of Broader Financial Contagion. The Washington Post. Available online: https://www.washingtonpost.com/us-policy/2023/03/10/silicon-valley-bank-failure-financial-industry/ (accessed on 13 March 2024).

- Mokni, Khaled, Elie Bouri, Ahdi Noomen Ajmi, and Xuan Vinh Vo. 2021. Does bitcoin hedge categorical economic uncertainty? A quantile analysis. SAGE Open 11: 21582440211016377. [Google Scholar] [CrossRef]

- Morrow, Allison, and Matt Egan. 2023. Silicon Valley Bank Collapses after Failing to Raise Capital. Available online: https://edition.cnn.com/2023/03/10/investing/svb-bank/index.html (accessed on 13 March 2024).

- Murty, Sarika, Vijay Victor, and Maria Fekete-Farkas. 2022. Is bitcoin a safe haven for indian investors? A garch volatility analysis. Journal of Risk and Financial Management 15: 317. [Google Scholar] [CrossRef]

- Nakamoto, Satoshi. 2009. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 13 March 2024).

- Nathan, Allison, Gabriel Lipton Galbraith, and Jenny Grimberg. 2021. Crypto: A new asset class? In Global Macro Research. New York City: The Goldman Sachs Group Inc. [Google Scholar]

- Ndinga, Eliézer. 2023. State of Crypto. 21Share. Available online: https://connect.21shares.com/web3-magazine (accessed on 13 March 2024).

- Neureuter, Jack, and Chris Kuiper. 2023. Bitcoin First Revisited. Available online: https://www.fidelitydigitalassets.com/research-and-insights/bitcoin-first-revisited (accessed on 13 March 2024).

- Nguyen, Khanh Quoc. 2022. The correlation between the stock market and Bitcoin during COVID-19 and other uncertainty periods. Finance Research Letters 46: 102284. [Google Scholar] [CrossRef]

- Pandey, Dharen Kumar, M. Kabir Hassan, Vineeta Kumari, and Rashedul Hasan. 2023. Repercussions of the silicon valley bank collapse on global stock markets. Finance Research Letters 55: 104013. [Google Scholar] [CrossRef]

- Phillips, Gavin. 2022. What Will Happen after All 21 Million Bitcoins Are Mined? December. Available online: https://www.makeuseof.com/what-happens-to-Bitcoin-after-all-21-million-coins-are-mined/ (accessed on 13 March 2023).

- Pichl, Lukáš, and Taisei Kaizoji. 2017. Volatility analysis of bitcoin price time series. December. Quantitative Finance and Economics 1: 474–85. [Google Scholar] [CrossRef]

- Raydan, Rodayna. 2022. Lebanese Turn to Cryptocurrency as Economy Tanks. March. Available online: https://www.al-monitor.com/originals/2022/02/lebanese-turn-cryptocurrency-economy-tanks (accessed on 13 March 2023).

- Rudolf, Karl Oton, Samer Ajour El Zein, and Nicola Jackman Lansdowne. 2021. Bitcoin as an investment and hedge alternative. a dcc mgarch model analysis. Risks 9: 154. [Google Scholar] [CrossRef]

- Sapuric, Svetlana, Angelika Kokkinaki, and Ifigenia Georgiou. 2022. The relationship between Bitcoin returns, volatility and volume: Asymmetric GARCH modeling. Journal of Enterprise Information Management 35: 1506–521. [Google Scholar] [CrossRef]

- Scott, Brett, John Loonam, and Vikas Kumar. 2017. Exploring the rise of blockchain technology: Towards distributed collaborative organizations. Strategic Change 26: 423–28. [Google Scholar] [CrossRef]

- Suberg, William. 2023. BTC Price Hits 2-Week Highs after Grayscale and SEC Bitcoin ETF Win. August. Available online: https://cointelegraph.com/news/btc-price-2-week-highs-grayscale-sec-Bitcoin-etf-win (accessed on 13 March 2023).

- Taylor, Stephen J. 2008. Modelling Financial Time Series. Singapore: World Scientific. [Google Scholar]

- Tsay, Ruey S. 2005. Analysis of Financial Time Series. New York: John Wiley & Sons. [Google Scholar]

- Vo, Lai Van, and Huong T. T. Le. 2023. From hero to zero—The case of silicon valley bank. Journal of Economics and Business 127: 106138. [Google Scholar] [CrossRef]

- Wang, Gangjin, Yanping Tang, Chi Xie, and Shou Chen. 2019. Is bitcoin a safe haven or a hedging asset? evidence from china. Journal of Management Science and Engineering 4: 173–88. [Google Scholar] [CrossRef]

- WGC. 2019. Annual Review. Available online: https://www.gold.org/goldhub/research/2019-annual-review (accessed on 13 March 2023).

- World Bank. 2022. COVID-19 Boosted the Adoption of Digital Financial Services. Washington, DC: World Bank. [Google Scholar]

- Yermack, David. 2015. Chapter 2—Is bitcoin a real currency? An economic appraisal. In Handbook of Digital Currency. Edited by David Lee Kuo Chuen. San Diego: Academic Press, pp. 31–43. [Google Scholar] [CrossRef]

- Young, Martin. 2023. Bitcoin in Nigeria is 60 Percent More Expensive, but There’s a Catch. Available online: https://cointelegraph.com/news/bitcoin-premium-hits-60-in-nigeria-as-it-limits-atm-cash-withdrawals (accessed on 13 March 2023).

- Yousaf, Imran, and John W. Goodell. 2023. Responses of us equity market sectors to the silicon valley bank implosion. Finance Research Letters 55: 103934. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| BTC | SP500 | NASDAQ | PAXG | Bank Index | |

|---|---|---|---|---|---|

| Summary Statistics | |||||

| Mean | −0.00 | −0.00 | −0.00 | −0.00 | 0.00 |

| Sd | 0.04 | 0.01 | 0.02 | 0.02 | 0.01 |

| Min | −0.26 | −0.04 | −0.05 | −0.06 | −0.03 |

| Max | 0.18 | 0.05 | 0.07 | 0.05 | 0.03 |

| Median | −0.00 | −0.00 | −0.00 | −0.00 | 0.00 |

| MAD | 0.03 | 0.01 | 0.02 | 0.02 | 0.01 |

| Skew | −0.83 | −0.08 | −0.04 | 0.05 | 0.32 |

| Kurt | 4.57 | −2.23 | −2.57 | −2.34 | −1.96 |

| JB-test (p-val.) | <2.2 × 10−16 | 0.006187 | 0.1964 | 0.02321 | <2.2 × 10−16 |

| Stationarity and Heteroschedasticity Tests | |||||

| ADF— no trend | −7.63 | −5.90 | −5.98 | −6.94 | −5.90 |

| ADF—trend | −15.81 | −13.40 | −13.60 | −18.47 | −12.53 |

| PP—no trend | −570.52 | −304.42 | −301.49 | −561.23 | −301.40 |

| PP—trend | −567.99 | −303.29 | −299.41 | −561.28 | −300.85 |

| LB lag 5 (p-val.) | 0.001201 | 0.06895 | 0.07226 | 0.03193 | 1.124 × 10−6 |

| LB lag 10 (p-val.) | 0.01375 | 0.002174 | 0.001153 | 1.346 × 10−5 | 5.942 × 10−6 |

| LB lag 15 (p-val.) | 0.03168 | 0.001183 | 7.079 × 10−5 | 7.202 × 10−5 | 7.597 × 10−5 |

| LB lag 20 (p-val.) | 0.03438 | 0.000987 | 2.234 × 10−5 | 0.0002009 | 0.0002584 |

| LM test (p-val.) | <2.2 × 10−16 | <2.2 × 10−16 | <2.2 × 10−16 | <2.2 × 10−16 | <2.2 × 10−16 |

| Volatility Model | Expression |

|---|---|

| GARCH(1,1) | |

| EGARCH(1,1) | |

| GJR(1,1) | |

| APARCH(1,1) |

| Criterion | Formula |

|---|---|

| AIC | |

| BIC | |

| HQIC | |

| SIC |

| Company Name | Symbol | Average Price ($) | Shares Outstanding | Weight |

|---|---|---|---|---|

| JPMorgan Chase & Co. | JPM | 127.84 | 2,920,000,000 | 24.35% |

| Bank of America Corporation | BAC | 34.24 | 7,970,000,000 | 17.80% |

| Wells Fargo & Co. | WFC | 43.84 | 3,750,000,000 | 10.72% |

| Morgan Stanley | MS | 85.64 | 1,670,000,000 | 9.33% |

| Goldman Sachs Group | GS | 328.09 | 332,450,000 | 7.11% |

| Citigroup Inc. | C | 48.84 | 1,950,000,000 | 6.21% |

| U.S. Bancorp | USB | 43.38 | 1,530,000,000 | 4.33% |

| PNC Financial Services Group | PNC | 155.46 | 399,680,000 | 4.05% |

| Truist Financial Corporation | TFC | 44.24 | 1,330,000,000 | 3.84% |

| Capital One Financial Corporation | COF | 110.81 | 381,810,000 | 2.76% |

| Discover Financial Services | DFS | 104.50 | 253,950,000 | 1.73% |

| M&T Bank Corporation | MTB | 154.15 | 164,900,000 | 1.66% |

| Fifth Third Bancorp | FITB | 33.81 | 680,720,000 | 1.50% |

| Regions Financial Corporation | RF | 20.38 | 938,310,000 | 1.25% |

| Huntington Bancshares Inc. | HBAN | 12.95 | 1,440,000,000 | 1.22% |

| KeyCorp | KEY | 16.94 | 935,260,000 | 1.03% |

| Ally Financial Inc. | ALLY | 32.57 | 300,820,000 | 0.64% |

| Zions Bancorporation | ZION | 48.65 | 148,100,000 | 0.47% |

| Model | BTC | SP500 | ||||||

|---|---|---|---|---|---|---|---|---|

| AIC | BIC | SIC | HQIC | AIC | BIC | SIC | HQIC | |

| AR(1)−GARCH(1,1) | −2276.18 | −2254.60 | −2276.27 | −2267.75 | −2210.02 | −2190.34 | −2210.15 | −2202.21 |

| AR(1)−EGARCH(1,1) | −2329.73 | −2303.84 | −2329.86 | −2319.61 | −2231.14 | −2207.53 | −2231.32 | −2221.77 |

| AR(1)−GJR(1,1) | −2321.24 | −2295.35 | −2321.37 | −2311.13 | −2219.11 | −2195.50 | −2219.29 | −2209.74 |

| AR(1)−APARCH(1,1) | −2331.35 | −2301.14 | −2331.53 | −2319.55 | −2218.60 | −2191.05 | −2218.85 | −2207.67 |

| AR(1)−GARCH(1,1) | −2426.72 | −2400.83 | −2426.85 | −2416.60 | −2208.70 | −2185.09 | −2208.88 | −2199.33 |

| AR(1)−EGARCH(1,1) | −2431.67 | −2401.46 | −2431.84 | −2419.87 | −2228.72 | −2201.18 | −2228.97 | −2217.79 |

| AR(1)−GJR(1,1) | −2428.63 | −2398.42 | −2428.80 | −2416.83 | −2217.29 | −2189.75 | −2217.55 | −2206.36 |

| AR(1)−APARCH(1,1) | −2430.06 | −2395.54 | −2430.29 | −2416.57 | NA | NA | NA | NA |

| AR(1)−GARCH(1,1) | −2423.22 | −2388.70 | −2423.45 | −2409.73 | −2208.70 | −2185.09 | −2208.88 | −2199.33 |

| AR(1)−EGARCH(1,1) | −2427.50 | −2388.66 | −2427.79 | −2412.33 | −2228.72 | −2201.18 | −2228.97 | −2217.79 |

| AR(1)−GJR(1,1) | −2424.72 | −2385.88 | −2425.00 | −2409.54 | −2217.29 | −2189.75 | −2217.55 | −2206.36 |

| AR(1)−APARCH(1,1) | −2425.77 | −2382.62 | −2426.12 | −2408.91 | NA | NA | NA | NA |

| AR(1)−GARCH(1,1) | −2420.91 | −2395.02 | −2421.04 | −2410.80 | −2208.39 | −2184.78 | −2208.58 | −2199.02 |

| AR(1)−EGARCH(1,1) | −2422.98 | −2392.78 | −2423.16 | −2411.18 | −2228.16 | −2200.61 | −2228.41 | −2217.22 |

| AR(1)−GJR(1,1) | −2421.20 | −2391.00 | −2421.38 | −2409.40 | −2216.27 | −2184.79 | −2216.60 | −2203.78 |

| AR(1)−APARCH(1,1) | −2420.97 | −2386.45 | −2421.20 | −2407.48 | −2216.27 | −2184.79 | −2216.60 | −2203.78 |

| NASDAQ | PAXG | |||||||

| AIC | BIC | SIC | HQIC | AIC | BIC | SIC | HQIC | |

| AR(1)−GARCH(1,1) | −2276.18 | −2254.60 | −2276.27 | −2267.75 | −2482.81 | −2463.14 | −2482.94 | −2475.00 |

| AR(1)−EGARCH(1,1) | −2329.73 | −2303.84 | −2329.86 | −2319.61 | −2482.29 | −2458.68 | −2482.47 | −2472.92 |

| AR(1)−GJR(1,1) | −2321.24 | −2295.35 | −2321.37 | −2311.13 | −2486.15 | −2462.54 | −2486.34 | −2476.78 |

| AR(1)−APARCH(1,1) | −2331.35 | −2301.14 | −2331.53 | −2319.55 | −2479.42 | −2451.88 | −2479.68 | −2468.49 |

| AR(1)−GARCH(1,1) | −2420.91 | −2395.02 | −2421.04 | −2410.80 | −2488.71 | −2465.10 | −2488.89 | −2479.34 |

| AR(1)−EGARCH(1,1) | −2422.98 | −2392.78 | −2423.16 | −2411.18 | −2488.18 | −2460.63 | −2488.43 | −2477.25 |

| AR(1)−GJR(1,1) | −2421.20 | −2391.00 | −2421.38 | −2409.40 | −2490.98 | −2463.44 | −2491.24 | −2480.05 |

| AR(1)−APARCH(1,1) | −2420.97 | −2386.45 | −2421.20 | −2407.48 | −2484.50 | −2453.02 | −2484.83 | −2472.01 |

| AR(1)−GARCH(1,1) | −2426.72 | −2400.83 | −2426.85 | −2416.60 | −2485.78 | −2454.31 | −2486.11 | −2473.29 |

| AR(1)−EGARCH(1,1) | −2431.67 | −2401.46 | −2431.84 | −2419.87 | −2485.18 | −2449.77 | −2485.60 | −2471.13 |

| AR(1)−GJR(1,1) | −2428.63 | −2398.42 | −2428.80 | −2416.83 | −2487.65 | −2452.24 | −2488.07 | −2473.60 |

| AR(1)−APARCH(1,1) | −2430.06 | −2395.54 | −2430.29 | −2416.57 | −2483.45 | −2444.10 | −2483.96 | −2467.83 |

| AR(1)−GARCH(1,1) | −2423.22 | −2388.70 | −2423.45 | −2409.73 | −2488.31 | −2464.70 | −2488.49 | −2478.94 |

| AR(1)−EGARCH(1,1) | −2427.50 | −2388.66 | −2427.79 | −2412.33 | −2487.62 | −2460.07 | −2487.87 | −2476.68 |

| AR(1)−GJR(1,1) | −2424.72 | −2385.88 | −2425.00 | −2409.54 | −2490.31 | −2462.76 | −2490.56 | −2479.38 |

| AR(1)−APARCH(1,1) | −2425.77 | −2382.62 | −2426.12 | −2408.91 | −2484.63 | −2453.15 | −2484.96 | −2472.13 |

| Bank Index | ||||||||

| AIC | BIC | SIC | HQIC | |||||

| AR(1)−GARCH(1,1) | −1994.84 | −1975.16 | −1994.97 | −1987.03 | ||||

| AR(1)−EGARCH(1,1) | −2017.60 | −1993.99 | −2017.79 | −2008.23 | ||||

| AR(1)−GJR(1,1) | −2009.09 | −1985.48 | −2009.28 | −1999.72 | ||||

| AR(1)−APARCH(1,1) | −2012.77 | −1985.22 | −2013.02 | −2001.84 | ||||

| AR(1)−GARCH(1,1) | −1996.93 | −1973.32 | −1997.12 | −1987.56 | ||||

| AR(1)−EGARCH(1,1) | −2016.73 | −1989.19 | −2016.99 | −2005.80 | ||||

| AR(1)−GJR(1,1) | −2008.83 | −1981.28 | −2009.08 | −1997.90 | ||||

| AR(1)−APARCH(1,1) | −2011.94 | −1980.46 | −2012.27 | −1999.45 | ||||

| AR(1)−GARCH(1,1) | −1994.02 | −1962.54 | −1994.35 | −1981.53 | ||||

| AR(1)−EGARCH(1,1) | −2012.52 | −1977.11 | −2012.94 | −1998.47 | ||||

| AR(1)−GJR(1,1) | −2005.34 | −1969.93 | −2005.76 | −1991.29 | ||||

| AR(1)−APARCH(1,1) | −2007.71 | −1968.36 | −2008.22 | −1992.09 | ||||

| AR(1)−GARCH(1,1) | −1996.26 | −1972.65 | −1996.44 | −1986.89 | ||||

| AR(1)−EGARCH(1,1) | −2016.49 | −1988.94 | −2016.74 | −2005.55 | ||||

| AR(1)−GJR(1,1) | −2008.21 | −1980.67 | −2008.47 | −1997.28 | ||||

| AR(1)−APARCH(1,1) | NA | NA | NA | NA | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Petti, D.; Sergio, I. Bank Crisis Boosts Bitcoin Price. J. Risk Financial Manag. 2024, 17, 134. https://doi.org/10.3390/jrfm17040134

Petti D, Sergio I. Bank Crisis Boosts Bitcoin Price. Journal of Risk and Financial Management. 2024; 17(4):134. https://doi.org/10.3390/jrfm17040134

Chicago/Turabian StylePetti, Danilo, and Ivan Sergio. 2024. "Bank Crisis Boosts Bitcoin Price" Journal of Risk and Financial Management 17, no. 4: 134. https://doi.org/10.3390/jrfm17040134

APA StylePetti, D., & Sergio, I. (2024). Bank Crisis Boosts Bitcoin Price. Journal of Risk and Financial Management, 17(4), 134. https://doi.org/10.3390/jrfm17040134