An Overview of Islamic Accounting: The Murabaha Contract

Abstract

1. Introduction

2. Historical Development of Islamic Accounting

3. Modern Developments in Islamic Accounting

4. Common Contracts Used by Islamic Banks to Conduct Business

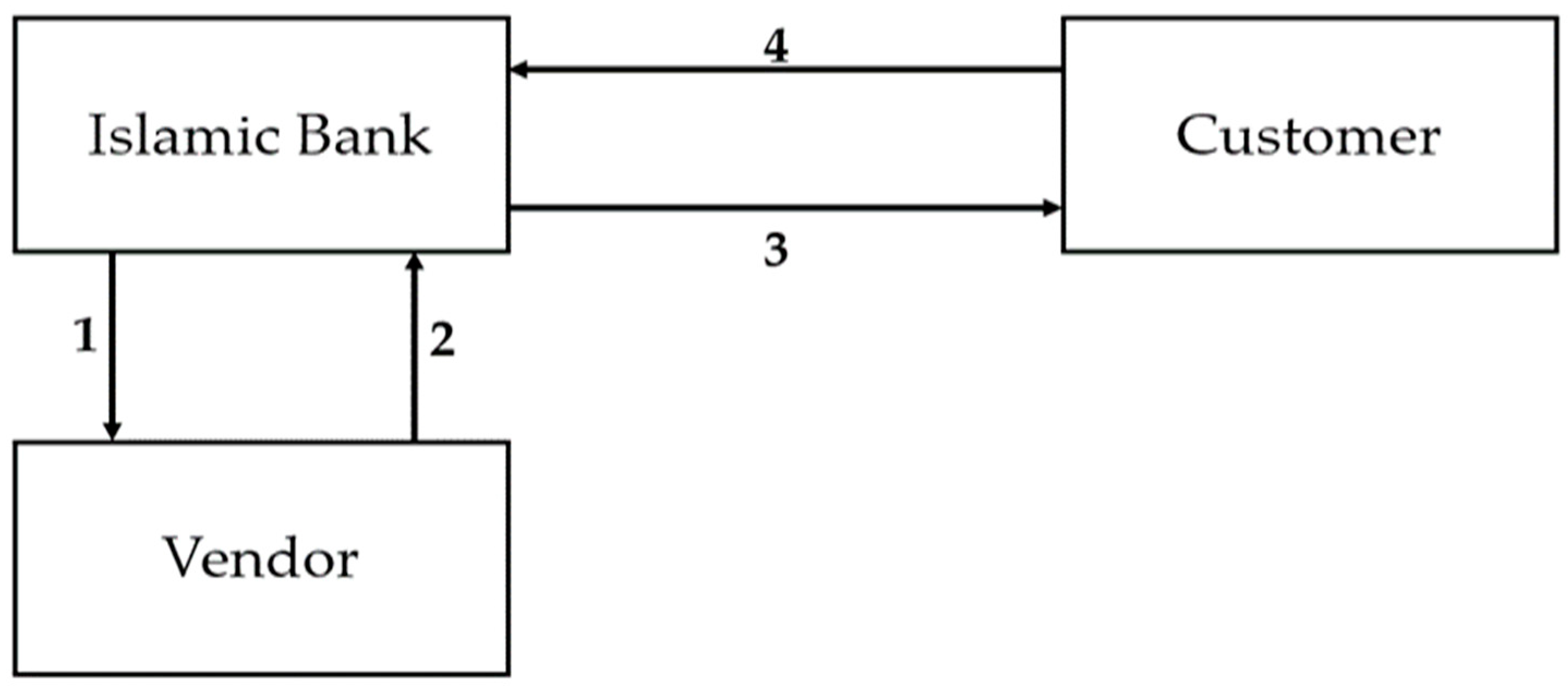

5. The Murabaha Contract

6. Criticisms of the Murabaha Contract

7. Accounting for the Murabaha Contract

8. Related Studies on Accounting for the Murabaha Contract

9. The Simulation of a Murabaha Contract

10. Discussion

11. Conclusions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- AAOIFI. 2023. Accounting and Auditing Organization for Islamic Financial Institutions. Available online: https://aaoifi.com/?lang=en (accessed on 10 June 2023).

- Abdel Karim, Rifaat A. 1995. The nature and rationale of a conceptual framework for financial reporting by Islamic banks. Accounting and Business Research 25: 285–300. [Google Scholar] [CrossRef]

- Abdel Karim, Rifaat A. 2001. International accounting harmonization, banking regulation, and Islamic banks. The International Journal of Accounting 36: 169–93. [Google Scholar] [CrossRef]

- Abdel-Magid, Mostafa F. 1981. The theory of Islamic banking: Accounting implications. International Journal of Accounting 17: 79–102. [Google Scholar]

- Aburime, Toni, and Felix Alio. 2009. Islamic banking: Theories, practices and insight for Nigeria. International Review of Business Research Papers 5: 321–39. Available online: https://ssrn.com/abstract=1262291 (accessed on 12 June 2023).

- Ahmed, Mezbah U., Ruslan Sabirzyanov, and Romzie Rosman. 2016. A critique on accounting for Murabaha contract: A comparative analysis of IFRS and AAOIFI accounting standards. Journal of Islamic Accounting and Business Research 7: 190–201. [Google Scholar] [CrossRef]

- Akacem, Mohammed, and Lynde Gilliam. 2002. Principles of Islamic banking: Debt versus equity finance. Middle East Policy IX: 124–38. [Google Scholar] [CrossRef]

- Alam, Nafis, Lokesh Gupta, and Bala Shanmugam. 2017. Islamic Finance: A Practical Perspective. London: Palgrave Macmillan. [Google Scholar]

- Aldohni, Abdul Karim. 2015. The quest for a better legal and regulatory framework for Islamic banking. Ecclesiastical Law Society 17: 15–35. [Google Scholar] [CrossRef]

- Al-Sulaiti, Jabir, Abulrahman Anam Ousama, and Helmi Hamammi. 2018. The compliance of disclosure with AAOIFI financial accounting standards: A comparison between Bahrain and Qatar Islamic banks. Journal of Islamic Accounting and Business Research 9: 549–66. [Google Scholar] [CrossRef]

- Ambashe, Mohamud, and Hikmat A. Alrawi. 2013. The development of accounting through the history. International Journal of Advances in Management and Economics 2: 95–100. Available online: https://www.managementjournal.info/index.php/IJAME/article/view/261 (accessed on 12 June 2023).

- Ariff, Mohamed. 1988. Islamic banking. Asian-Pacific Economic Literature 2: 48–64. [Google Scholar] [CrossRef]

- Ariff, Mohamed. 2014. Whiter Islamic banking. The World Economy 37: 733–46. [Google Scholar] [CrossRef]

- Arslan-Ayaydin, Ozgur, Kris Boudt, and Muhammad Wajid Raza. 2018. Avoiding interest-based revenues while constructing Shariah-compliant portfolios: False negatives and false positives. The Journal of Portfolio Management 44: 136–43. [Google Scholar] [CrossRef]

- Askari, Hossein, Zamir Iqbal, and Abbas Mirakhor. 2009. New Issues in Islamic Finance & Economics: Progress & Challenges. Hoboken: John Wiley & Sons. [Google Scholar]

- Askary, Saeed, and Frank L. Clarke. 1997. Accounting in the Koranic verses. In Islamic Accounting. Edited by Christopher Napier and Roszaini Haniffa. Cheltenham: Edward Elgar Publishing, pp. 144–58. [Google Scholar]

- Asutay, Mehmet. 2007. A political economy approach to Islamic economics: Systemic understanding for an alternative economic system. Kyoto Bulletin of Islamic Area Studies 1: 1–15. Available online: https://dro.dur.ac.uk/4530/1/4530.pdf (accessed on 12 June 2023).

- Asutay, Mehmet. 2008. Islamic banking and finance: Social failure. New Horizon—Global Perspectives on Islamic Banking and Insurance 169: 1–3. [Google Scholar] [CrossRef]

- Asutay, Mehmet. 2012. Conceptualising and locating the social failure of Islamic finance: Aspirations of Islamic moral economy vs. the realities of Islamic finance. Asian and African Area Studies 11: 93–113. Available online: https://www.jstage.jst.go.jp/article/asafas/11/2/11_93/_pdf (accessed on 8 June 2023).

- Benamraoui, Abdelhafid. 2008. Islamic banking: The case of Algeria. International Journal of Islamic and Middle Eastern Finance and Management 1: 113–31. [Google Scholar] [CrossRef]

- Billah, Mohd Ma’sum. 2007. Islamic banking and the growth of takaful. In Handbook of Islamic Banking. Edited by Mohammad K. Hassan and Mervin K. Lewis. Cheltenham: Edward Elgar Publishing, pp. 401–18. [Google Scholar]

- Bjorvatn, Kjetil. 1998. Islamic Economics and Economic Development. Forum for Development Studies 2: 229–43. [Google Scholar] [CrossRef]

- Boutayeba, Faical, Mohammed Benhamida, and Souad Guesmi. 2014. Ethics in Islamic economics. Annales. Ethics in Economic Life 17: 111–21. [Google Scholar] [CrossRef]

- Cebeci, Ismail. 2012. Integrating the social maslaha into Islamic finance. Accounting Research Journal 25: 166–84. [Google Scholar] [CrossRef]

- Chapra, Muhamed Umer. 2008. The Global Financial Crisis: Can Islamic Finance Help Minimize the Severity and Frequency of Such a Crisis in the Future. A paper presentation at the forum on the Global Financial Crisis. Jeddah: Islamic Development Bank. [Google Scholar]

- Daly, Saida, and Mohamed Frikha. 2016. Islamic finance: Basic principles and contributions in financing economic. Journal of the Knowledge Economy 7: 496–512. [Google Scholar] [CrossRef]

- Dar, Humayon A. 2007. Incentive compatibility of Islamic financing. In Handbook of Islamic Banking. Edited by Mohammad K. Hassan and Mervin K. Lewis. Cheltenham: Edward Elgar Publishing, pp. 85–95. [Google Scholar]

- Dean, Graeme, and Frank Clarke. 2003. An Evolving conceptual framework. Abacus 39: 279–97. [Google Scholar] [CrossRef]

- Dusuki, Asyraf Wajdi, and Abdulazeem Abozaid. 2007. A critical appraisal on the challenges of realising maqasid al-Shariah in Islamic banking and finance. Journal of Economics and Management 15: 143–65. Available online: https://journals.iium.edu.my/enmjournal/index.php/enmj/article/view/133 (accessed on 12 June 2023).

- Echchabi, Abdelghani, and Hassanuddeen Abd Aziz. 2014. Shari’ah issues in Islamic banking: A qualitative survey in Malaysia. Qualitative Research in Financial Markets 6: 198–210. [Google Scholar] [CrossRef]

- Elfakhani, Said M., Imad J. Zbib, and Zafar U. Ahmed. 2007. Marketing of Islamic financial products. In Handbook of Islamic Banking. Edited by Mohammad K. Hassan and Mervin K. Lewis. Cheltenham: Edward Elgar Publishing, pp. 116–27. [Google Scholar]

- El-Gamal, Mahmoud A. 2006. Islamic Finance: Law, Economics, and Practice. Cambridge: Cambridge University Press. [Google Scholar]

- El-Halaby, Sherif, Sameh Aboul-Dahab, and Nuha Bin Qoud. 2021. A systematic literature review on AAOIFI standards. Journal of Financial Reporting and Accounting 19: 133–83. [Google Scholar] [CrossRef]

- Financial Accounting Standard 28. 2017. Murabaha and Other Deferred Payment Sales. Available online: https://aaoifi.com/e-standards/?lang=en (accessed on 8 June 2023).

- Gattoo, Mujeeb Hussain, and Muneeb Hussain Gattoo. 2017. Modern economics and the Islamic alternative: Disciplinary evolution and current crisis. International Journal of Economics, Management and Accounting 25: 173–203. Available online: https://journals.iium.edu.my/enmjournal/index.php/enmj/article/view/494 (accessed on 12 June 2023).

- Ghauri, Shahid Muhammad Khan, and Amal Sabah Obaid Qambar. 2012. Rewards in faith-based vs conventional banking. Qualitative Research in Financial Markets 4: 176–96. [Google Scholar] [CrossRef]

- Ginena, Karim. 2013. Shari’ah risk and corporate governance of Islamic banks. Corporate Governance 14: 86–103. Available online: https://ssrn.com/abstract=2355872 (accessed on 8 June 2023).

- Gray, Sidney. 1988. Towards a theory of cultural influence on the development of accounting systems internationally. Abacus 24: 1–15. [Google Scholar] [CrossRef]

- Habib, Syeda Fahmida. 2018. Fundamentals of Islamic Finance and Banking. Hoboken: John Wiley & Sons. [Google Scholar]

- Hamid, Shaari, Russell Craig, and Frank Clarke. 1995. Bookkeeping and accounting control systems in a tenth-century Muslim administrative office. Accounting, Business and Financial History 5: 321–33. [Google Scholar] [CrossRef]

- Hanif, Muhammad. 2011. Differences and similarities in Islamic and conventional banking. International Journal of Business and Social Science 2: 166–75. Available online: http://www.ijbssnet.com/journals/Vol._2_No._2%3B_February_2011/20.pdf (accessed on 8 June 2023).

- Haniffa, Roszaini, and Mohammad Hudaib. 2002. A theoretical framework for the development of the Islamic perspective of accounting. Accounting, Commerce and Finance: The Islamic Perspective Journal 6: 1–71. [Google Scholar]

- Haniffa, Roszaini, and Mohammad Hudaib. 2007. Exploring the ethical identity of Islamic banks via communication in annual reports. Journal of Business Ethics 76: 97–116. [Google Scholar] [CrossRef]

- Haniffa, Roszaini, Mohammad Hudaib, and Abul Malik Mirza. 2002. Accounting Policy Choice within the Shari’ah Islami’iah Framework. Discussion Papers in Accountancy and Finance, Working Paper 02/04. Exeter: School of Business and Economics, University of Exeter, pp. 1–27. [Google Scholar]

- Heidhues, Eva, and Chris Patel. 2011. A critique of Gray’s framework on accounting values using Germany as a case study. Critical Perspectives on Accounting 22: 273–87. [Google Scholar] [CrossRef]

- Hofstede, Geert. 1984. Cultural dimensions in management and planning. Asia Pacific Journal of Management 1: 81–99. [Google Scholar] [CrossRef]

- Ismail, Abdul Ghafar B., and Achmad Tohirin. 2010. Islamic law and finance. Humanomics 26: 178–99. [Google Scholar] [CrossRef]

- Jamaldeen, Faleel. 2012. Islamic Finance for Dummies. Hoboken: John Wiley. [Google Scholar]

- Jawadi, Fredj, Abdoulkarim Idi Cheffou, and Nabila Jawadi. 2016. Do Islamic and conventional banks really differ? A panel data statistical analysis. Open Economies Review 27: 293–302. [Google Scholar] [CrossRef]

- Jha, Yusuf. 2013. Examining the meta-principles of modern economics and the implications for Islamic banking and finance. Islamic Sciences 11: 169–84. Available online: https://cis-ca.org/_media/pdf/2013/2/TEM_temetmomeatifibaf.pdf (accessed on 12 June 2023).

- Kahf, Monzer. 1999. Islamic banks at the threshold of the third millennium. Thunderbird International Business Review 41: 445–60. [Google Scholar] [CrossRef]

- Kahf, Monzer. 2007. Islamic banks and economic development. In Handbook of Islamic Banking. Edited by Mohammad K. Hassan and Mervin K. Lewis. Cheltenham: Edward Elgar Publishing, pp. 277–84. [Google Scholar]

- Kazi, Ashraf U., and Abdel K. Halabi. 2006. The influence of Quran and Islamic financial transactions and banking. Arab Law Quarterly 20: 321–31. Available online: https://www.jstor.org/stable/27650555 (accessed on 12 June 2023).

- Kettell, Brian. 2010. Frequently Asked Questions in Islamic Finance. Hoboken: John Wiley & Sons. [Google Scholar]

- Kettell, Brian. 2011. Introduction to Islamic Banking and Finance. Hoboken: John Wiley & Sons. [Google Scholar]

- Khan, Madiha. 2011. Islamic banking practices: Islamic law and prohibition of riba. Islamic Studies 50: 413–22. Available online: https://www.jstor.org/stable/41932604 (accessed on 8 June 2023).

- Khan, Mansoor M., and Ishaq M. Bhatti. 2008. Islamic banking and finance: On its way to globalization. Managerial Finance 34: 708–28. [Google Scholar] [CrossRef]

- Khan, Muhammad Akram. 2013. What Is Wrong with Islamic Economics? Analysing the Present State and Future Agenda. Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Kholvadia, Faatima. 2017. Islamic banking in South Africa—Form over substance. Meditari Accountancy Research 25: 65–81. [Google Scholar] [CrossRef]

- Kuran, Timur. 1995. Islamic economics and the Islamic subeconomy. The Journal of Economic Perspectives 9: 155–73. [Google Scholar] [CrossRef]

- Lahsasna, Ahcene. 2014. Sharia Non-Compliance Risk Management and Legal Documentation in Islamic Finance. Hoboken: John Wiley & Sons. [Google Scholar]

- Lewis, Mervin K. 2001. Islam and accounting. Accounting Forum 25: 103–27. Available online: https://www.tandfonline.com/doi/abs/10.1111/1467-6303.00058?journalCode=racc20 (accessed on 8 June 2023).

- Lica, Madalina. 2015. The origins and development of Islamic economics. Cogito VII: 80–91. Available online: https://cogito.ucdc.ro/cogito7.nr2.june.pdf#page=80 (accessed on 12 June 2023).

- Mansour, Walid, Khoutem Ben Jedidia, and Jihed Majdoub. 2015. How ethical is Islamic banking in the light of the objectives of Islamic law. Journal of Religious Ethics 43: 51–77. [Google Scholar] [CrossRef]

- Mirakhor, Abbas, and Iqbal Zaidi. 2007. Profit-and-loss sharing contracts in Islamic finance. In Handbook of Islamic Banking. Edited by Mohammad K. Hassan and Mervin K. Lewis. Cheltenham: Edward Elgar Publishing, pp. 49–63. [Google Scholar]

- Mohammed, Nor Farizal, Fadzlina Mohd Fahmi, and Asyaari Elmiza Ahmad. 2015. The influence of AAOIFI accounting standards in reporting Islamic financial institutions in Malaysia. Procedia Economics and Finance 31: 418–24. [Google Scholar] [CrossRef]

- Moosa, Riyad. 2022. The role of customer selection criteria, banking objective, CSR, and service quality in enhancing positive customer perception: An Islamic banking perspective. International Journal of Economics and Finance Studies 14: 388–408. [Google Scholar]

- Moosa, Riyad, and Smita Kashiramka. 2022. Objectives of Islamic banking, customer satisfaction and customer loyalty: Empirical evidence from South Africa. Journal of Islamic Marketing. [Google Scholar] [CrossRef]

- Muhamat, Amirul Afif, Mohamad Nizam Jaafar, and Norfaridah Binti Ali Azizan. 2011. An empirical study on banks’ clients’ sensitivity towards the adoption of Arabic terminology among Islamic banks. International Journal of Islamic and Middle Eastern Finance and Management 4: 343–54. [Google Scholar] [CrossRef]

- Murtuza, Athar. 2002. Islamic antecedents for financial accountability. In Islamic Accounting. Edited by Christopher Napier and Roszaini Haniffa. Cheltenham: Edward Elgar Publishing, pp. 203–21. [Google Scholar]

- Nathan, Samy, and Chris Pierce. 2009. CSR in Islamic financial institutions in the Middle East. In Corporate Social Responsibility: A Case Study Approach. Edited by Christine A. Mallin. Cheltenham: Edward Elgar Publishing, pp. 258–73. [Google Scholar]

- Nethercott, Craig R., and David M. Eisenberg. 2012. Islamic Finance Law and Practice. Oxford: Oxford University Press. [Google Scholar]

- Nouman, Muhammad, Karim Ullah, and Saleem Gul. 2018. Why Islamic banks tend to avoid participatory financing? A demand, regulation, and uncertainty framework. Business & Economic Review 10: 1–32. Available online: https://ssrn.com/abstract=3214064 (accessed on 8 June 2023).

- Oshodi, Basheer A. 2014. An Integral Approach to Development Economics: Islamic Finance in an African Context. Aldershot: Gower. [Google Scholar]

- Pollard, Jane, and Michael Samers. 2007. Islamic banking and finance: Postcolonial political economy and the decentring of economic geography. Royal Geographical Society 32: 313–30. [Google Scholar] [CrossRef]

- Ramabulana, Khuthadzo, and Riyad Moosa. 2022. Disclosure of Risks and Opportunities in the Integrated Reports of South African Banks. Journal of Risk and Financial Management 15: 551. [Google Scholar] [CrossRef]

- Roy, Delwin A. 1991. Islamic banking. Middle Eastern Studies 27: 427–56. [Google Scholar] [CrossRef]

- Saidani, Raoudha, Neila Boulila Taktak, and Khaled Hussainey. 2021. The determinants of investment account holders’ disclosure in Islamic banks: International Evidence. Journal of Risk and Financial Management 14: 564. [Google Scholar] [CrossRef]

- Sairally, Salma. 2007. Community development financial institutions: Lessons in social banking for the Islamic financial industry. Kyoto Bulletin of Islamic Area Study 1: 19–37. [Google Scholar]

- Salman, Kautsar Riza. 2022. Exploring the history of Islamic accounting and the concept of accountability in an Islamic perspective. Journal of Islamic Economic and Business Research 2: 114–30. [Google Scholar] [CrossRef]

- Schoon, Natalie. 2016. Modern Islamic Banking: Products and Processes in Practice. Hoboken: John Wiley & Sons. [Google Scholar]

- Sharair, Mohammad, Jesmin Islam, and Harun Harun. 2013. A history of the development of Islamic accounting standards: An investigation of the influence of key players. Conference presentation. Paper presented at 9th Asian Business Research Conference, BIAM Foundation, Dhaka, Bangladesh, December 20–21. [Google Scholar]

- Shaukat, Mughees, Mohammad Saeed Rahman, and Saji Luka. 2017. The nexus between business ethics and economics justice: An Islamic framework. Journal of Economic Development, Management, IT, Finance and Marketing 9: 1–11. Available online: https://www.proquest.com/docview/1861052108 (accessed on 12 June 2023).

- Solas, Cigdem, and Ismail Otar. 1994. The accounting system practiced in the Near East during the period 1220–350 based on the book Risale-I Felekiyye. Accounting Historians Journal 21: 117–35. Available online: https://www.jstor.org/stable/40698133 (accessed on 12 June 2023).

- Sulaiman, Maliah, and Roger Willett. 2001. Islam, Economic rationalism and accounting. American Journal of Islamic Social Sciences 18: 61–93. [Google Scholar] [CrossRef]

- Tlemsani, Issam. 2010. Co-evolution and reconcilability of Islam and the west: The context of global banking. Education, Business and Society: Contemporary Middle Eastern Issues 3: 262–76. [Google Scholar] [CrossRef]

- Tripp, Charles. 2006. Islam and the Moral Economy. Cambridge: Cambridge University Press. [Google Scholar]

- Trokic, Amela. 2015. Islamic accounting; history, development and prospects. European Journal of Islamic Finance 3: 1–6. [Google Scholar] [CrossRef]

- Usmani, Muhammad Taqi. 2002. An Introduction to Islamic Finance. Alphen aan den Rijn: Kluwer Law International. [Google Scholar]

- Velayutham, Sivakumar. 2014. Conventional accounting vs Islamic accounting: The debate revisited. Journal of Islamic Accounting and Business Research 5: 126–41. [Google Scholar] [CrossRef]

- Venardos, Angelo M. 2006. Islamic Banking & Finance in South-East Asia: Its Development & Future. Singapore: World Scientific Publishing. [Google Scholar]

- Vinnicombe, Thea. 2012. A study of compliance with AAOIFI accounting standards by Islamic banks in Bahrain. Journal of Islamic Accounting and Business Research 3: 78–98. [Google Scholar] [CrossRef]

- Visser, Hans. 2009. Islamic Finance Principles and Practice. Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Wahyudi, Muhammad, Sri Herianingrum, and Ririn Ratnasari. 2022. Examining the trend, themes, and social structure of the Islamic Accounting using a bibliometric approach. Jurnal Ekonomi dan Bisnis Islam 8: 153–78. Available online: https://e-journal.unair.ac.id/JEBIS/article/view/34073/23286 (accessed on 12 June 2023).

- Warde, Ibrahim. 2012. Status of the Global Islamic Finance Industry. In Islamic Finance: Law and Practice. Edited by Craig R. Nethercott and David M. Eisenberg. Oxford: Oxford University Press, pp. 1–14. [Google Scholar]

- Yanikkaya, Halit, and Yasar Ugur Pabuccu. 2017. Causes and solutions for the stagnation of Islamic banking in Turkey. ISRA International Journal of Islamic Finance 9: 43–61. [Google Scholar] [CrossRef]

- Zaid, Omar Abdullah. 2000. Were Islamic records precursors to accounting books based on the Italian method. Accounting Historians Journal 27: 73–90. Available online: https://core.ac.uk/download/pdf/288025182.pdf (accessed on 12 June 2023).

- Zakariyah, Luqman. 2015. Harmonising legality with morality in Islamic banking and finance: A quest for Maqasid al-shari’ah paradigm. Intellectual Discourse 23: 355–76. Available online: https://journals.iium.edu.my/intdiscourse/index.php/id/article/view/700 (accessed on 8 June 2023).

- Zia, Mehwish Darakhshan, and Nida Nasir-Ud-Din. 2016. Islamic economic rationalism and distribution of wealth: A comparative view. Journal of Business and Management 18: 43–52. [Google Scholar]

- Zineb, Shayeh, and Mondher Bellalah. 2013. Introduction to Islamic finance and Islamic banking: From theory to innovations. In Islamic Banking and Finance. Edited by Mondher Bellalah and Omar Masood. Cambridge: Cambridge Scholars Publishing, pp. 1–70. [Google Scholar]

{kind=link}

| Time Period | Characterisation |

|---|---|

| 1950 to 1974 | the period of theory development |

| 1974 to 1991 | the early or experimentation years |

| 1991 to date | the period of globalisation globalization |

| Contact type | Mode | Definition | Application |

|---|---|---|---|

| Partnership (Equity-based profit and loss sharing contracts) | Mudarabah (Silent partnership) | A partnership where one party provides capital while the other provides labour in a business venture. Profit is shared according to an agreed ratio, while losses are borne solely by the capital provider (Lahsasna 2014; Visser 2009). | Project, trade, and property finance. |

| Musharakah (Joint partnership) | A partnership where both parties provide capital and labour. Profits are shared according to an agreed ratio, while losses are limited to the capital invested (Lahsasna 2014; Visser 2009). | House, project, trade, and property finance. | |

| Sales or Trading (Debt-based) | Murabaha (Cost plus profit) | A credit sale transaction in which the seller discloses to the buyer the cost price and profit margin of the item sold (Daly and Frikha 2016; Khan 2011). | Home, asset, property, and trade finance. |

| Istisna (Build to order) | Used for manufacturing contracts where cash is paid in advance for future delivery of manufactured assets (Usmani 2002). | Project, property, and asset finance. | |

| Salam (Deferred delivery) | Used for agricultural contracts where cash is paid when the contract is concluded for future delivery of agricultural produce (Venardos 2006). | Agricultural trade finance. | |

| Leasing (Debt-based) | Ijarah (Operating or finance lease) | A lease agreement where the Islamic bank purchases an asset and thereafter transfers a usufruct to the lessee for an agreed time and rental (Visser 2009; Usmani 2002). | Asset and property finance. |

| Fee-based (Debt-based) | Qard-hassan (Beneficent loan) | A beneficent loan given to help the poor, the repayment of which only entails the capital amount as no interest is charged (Zia and Nasir-Ud-Din 2016). | Personal loan or safekeeping account without profit. |

| Financial Accounting Standard 28: Murabaha and Other Deferred Payment Sales | |

|---|---|

| Inventory | Receivables |

| Initial Recognition | |

|

|

|

|

|

|

| Subsequent Measurement | |

|

|

|

|

|

|

| |

| Derecognition (When no future economic benefits are expected to flow to the Islamic bank) | |

The Islamic bank losing control (physical loss or theft); or Inventory losing the capacity to provide future economic benefits. |

The carrying amount cannot be settled due to customer insolvency; or The Islamic bank decides to waive its right by writing off the outstanding amount or it is treated as a hibah (gift) to the customer. |

| Revenue |

|---|

|

| Cost of Sales |

|

| Deferred Profit |

|

|

|

|

|

|

| Year | Opening Balance | Annual Payment | Principal | Profit | Closing Balance |

|---|---|---|---|---|---|

| $ | $ | $ | $ | $ | |

| 1 | 25,000 | 6000 | 4399.44 | 1600.56 | 20,601 |

| 2 | 20,601 | 6000 | 4681.10 | 1318.90 | 15,919 |

| 3 | 15,919 | 6000 | 4980.80 | 1019.20 | 10,939 |

| 4 | 10,939 | 6000 | 5299.68 | 700.32 | 5639 |

| 5 | 5639 | 6000 | 5638.98 | 361.02 | 0 |

| Description | Debit | Credit |

|---|---|---|

| $ | $ | |

| Murabaha inventory | 25,000 | |

| Bank | 25,000 |

| Description | Debit | Credit |

|---|---|---|

| $ | $ | |

| Murabaha receivable | 30,000 | |

| Revenue | 25,000 | |

| Deferred profit | 5000 | |

| Cost of sales | 25,000 | |

| Murabaha inventory | 25,000 |

| Year | Debit | Credit | Debit | Credit | Murabaha Receivable Balance at Year-End |

|---|---|---|---|---|---|

| Bank | Murabaha Receivable | Deferred Profit | Profit from Sale of Vehicle | ||

| $ | $ | $ | $ | $ | |

| 1 | 6000 | 4399.44 | 1600.56 | 1600.56 | 20,601 |

| 2 | 6000 | 4681.10 | 1318.90 | 1318.90 | 15,919 |

| 3 | 6000 | 4980.80 | 1019.20 | 1019.20 | 10,939 |

| 4 | 6000 | 5299.68 | 700.32 | 700.32 | 5639 |

| 5 | 6000 | 5638.98 | 361.02 | 361.02 | 0 |

| Description | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total |

|---|---|---|---|---|---|---|

| $ | $ | $ | $ | $ | $ | |

| Revenue | 25,000 | 25,000 | ||||

| Cost of sales | 25,000 | 25,000 | ||||

| Profit from sale of vehicle | 1600.56 | 1318.90 | 1019.20 | 700.32 | 361.02 | 5000 |

| Description | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|

| $ | $ | $ | $ | $ | |

| Murabaha receivable | 20,601 | 15,919 | 10,939 | 5639 | 0 |

| Deferred profit | 3399.44 | 2080.52 | 1061.34 | 361.02 | 0 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Moosa, R. An Overview of Islamic Accounting: The Murabaha Contract. J. Risk Financial Manag. 2023, 16, 335. https://doi.org/10.3390/jrfm16070335

Moosa R. An Overview of Islamic Accounting: The Murabaha Contract. Journal of Risk and Financial Management. 2023; 16(7):335. https://doi.org/10.3390/jrfm16070335

Chicago/Turabian StyleMoosa, Riyad. 2023. "An Overview of Islamic Accounting: The Murabaha Contract" Journal of Risk and Financial Management 16, no. 7: 335. https://doi.org/10.3390/jrfm16070335

APA StyleMoosa, R. (2023). An Overview of Islamic Accounting: The Murabaha Contract. Journal of Risk and Financial Management, 16(7), 335. https://doi.org/10.3390/jrfm16070335