Abstract

The issue of co-movements is still crucial and arguable in international finance. An optimum and significant level of co-movement is highly desirable to investors, and it mostly depends on investors’ decisions (behavior and psychology). We use frequency–time bands and multi-scale-based wavelet analysis to investigate the co-movement between developed and emerging countries’ stock markets for better asset allocation and portfolio diversification strategies. The results show that a significant level of co-movement is observed between conventional and Islamic stock markets in developed and emerging countries, and it varies in terms of its time–frequency domain properties. Particularly, the dependency among conventional and Islamic stock markets is strong at 4–512-band scales. However, the USA Islamic stock market illustrates a higher level of coherency with the UK, Japan and China’s Islamic stock markets, while a relatively lower level of co-movement is detected with the Chinese composite, Malaysian and Indonesian Islamic stock markets. The findings further confirm that the developed countries’ stock markets are substantially influenced by the GFC in 2007–2008 and the European debt crisis in 2012, while this trend is surprisingly not observed in the emerging markets on a similar scale. Therefore, these crises have opened the door for the grabbing of portfolio diversification benefits from the emerging countries’ stock markets. These findings give some interesting insights to policymakers, investors and fund managers for portfolio diversification and risk management strategies.

1. Introduction

Globalization describes an integrated process that surges the capital flow from cross-border countries. It has developed financial linkages worldwide (Obstfeld 2021). Hence, globalization and financial market co-movements are integrated parts of the modern economy that have been used in increasing trade ties and economic and business phenomena from the domestic to regional and regional to international levels and for a broader market around the world (Boako and Alagidede 2017; Dewandaru et al. 2014). From a historical perspective, global financial markets increased with the globalization process from the mid-1980s and reinforced the linkages between developed and emerging countries (OECD 2018). This trend has matured due to advancing information technology, trade openness and financial liberalization (Balli et al. 2015; Goldstein 2012).

Moreover, the recent trend in financial markets has become more integrated and maintained complex interconnections between returns and microeconomic variables. Thus, the trend in capital markets is challenging to predict due to complex linkages. Stock market investors face more challenges; they are particularly worried and concerned about their investment decisions due to a scarcity of information (Zhang et al. 2018). Stock market co-movements not only depend on how these markets are transformed and show relationships in the long run and short-run holding periods but also how they maintain the focus on dynamic frequency–time domain properties and investors’ psychology by responding to global information flow (Alam et al. 2019; Buriev et al. 2018). These technological developments have made individuals closer at the institutional, national, and international levels. The movement of stocks can influence these events, as well as other asset prices disposed to open an investment horizon in cross-country boundaries (Khan 2011). Therefore, recent research interests have shifted from predicting single market trends to multiple markets’ co-movements.

In contrast, increasingly globalized markets have caused tiny pricing gaps among several equities markets, making nations more susceptible to global financial blows. Thus, the benefits of globalization were brought to task during the worldwide financial crisis, due to the trust placed in the inter-connected markets that propagated the financial situation throughout international markets (Lehkonen 2014). Financial market co-movements have created adequate room and promoted the opening of new windows for investors to earn and defend their nest eggs from different economic notions and horizons (Sahabuddin et al. 2020). In this regard, Islamic stock markets have not only emerged as a viable alternative but were also more secure and resilient during the crisis compared to the mainstream markets due to their rapid growth rate and significant features of Shariah law (Ahmed 2018; Bhuiyan et al. 2018; Ng et al. 2017; Saiti 2015). Nevertheless, financial markets’ dependency and co-movements are still arguable issues in international finance avenues that have received considerable attention in recent years (Ahmed and Huo 2019; Li et al. 2021). Hence, investor behavior and psychology are important for risk–return balancing and asset allocation strategies. Otherwise, they will fail to receive the benefits from their portfolio horizons (Aamir and Shah 2018; Chuluun 2017; Panda and Nanda 2017). These issues motivate us to investigate the dependency and co-movements between developed and emerging countries’ stock markets within frequency–time bands and multi-scale-based wavelet approaches. Wavelets are a multi-solution-based powerful and dynamic approach that enable efforts to overcome the barriers of time-series parametric-based estimation under the Capital Asset Price Model’s (CAPM) guidelines. Moreover, it explains the decoupling hypothesis and heterogeneity of asset returns by observing different risk patterns between conventional and Islamic stock markets (Anas et al. 2020; Sharif et al. 2020).

Thus, the present study seeks to investigate the dynamic levels of co-movements for portfolio optimization. The fresh insights contribute to this study in many ways. First, this study not only extends the current literature on time-varying properties but also explores them from frequency–time domain perspectives to quantify the magnitude of dynamic co-movements. Second, determining the optimum level of co-movement is still crucial and desirable to the investors with different and alternative investment environment horizons. Third, an optimum level of co-movement leads to making gains and shrinking risk patterns in different asset classes. Finally, these phenomena provide essential consequences and practical implications for investors’ behavior and psychology, portfolio diversification and risk–return strategies (Mensi et al. 2017b, 2018; Ying et al. 2020).

2. Literature Review

Theoretical implications are highly motivated in international finance for portfolio diversification. The optimum co-movement level is always desirable for expected returns from investors’ perspectives. Hence, co-movement and portfolio diversification benefits have maintained interesting chemistry in different investment horizons. For instance, co-movement and portfolio diversification benefits stand in opposition (Loh 2013; Aloui et al. 2015). In particular, for stock markets, when showing a relatively high level of co-movement, there is a high chance of losing portfolio diversification benefits. In contrast, a relatively weak or a lower level of co-movement signifies better benefits for portfolio diversification (Rua and Nunes 2009).

Moreover, Markowitz (1958) and Grubel (1968) developed the seminal works for international portfolio diversification. They suggested that investment diversification might play a pivotal role in mitigating the risk of investments or portfolios. From an international perspective, market movements in different investment horizons are essential for investment strategies and portfolio diversification decisions. When two or more markets move in a similar direction, co-movement among the asset classes is substantially increased. This movement might moderate the returns or portfolio diversification benefits (Song et al. 2021). It is noteworthy that this fusion might change the degree of co-movement in response to the portfolio adjustment (Xiao and Dhesi 2010). However, the potential outcomes from overseas channels can be realized when return patterns in domestic markets are not precisely associated with those in international markets. This evidence demonstrates that a comparatively low level of co-movement is associated with superior portfolio advantages worldwide, regardless of country. Investors are enthusiastic to mitigate risk and grab opportunities by assigning their funds and assets to different prospects. Thus, investors like to distribute their investment strategies across different product lines. They might permit the purchase of equities from foreign firms or markets (Panda and Nanda 2017). The studies on stock market co-movement have been empirically reviewed based on the latest relevant literature on international financial markets (Antar and Alahouel 2019). Nevertheless, portfolio diversification implications are not sufficiently established in terms of time–frequency domain properties (Rahim and Masih 2016).

Nevertheless, Majdoub and Mansour (2014) investigated volatility spillover effects between five developed and emerging Islamic countries’ stock markets using multi-variate GARCH approaches. They found that the developed and emerging Islamic countries do not demonstrate a strong correlation over time. Moreover, Saiti et al. (2014) stated that Islamic equity markets exhibit better portfolio opportunities for developed countries. Abbes and Trichilli (2015) investigated the dynamic inter-dependency between advanced and emerging countries’ Islamic stock markets in both tranquil and tumultuous periods using a co-integration technique. They observed that countries in similar economic groupings do not provide any diversification opportunities; however, countries in diverse economic groupings among developed and emerging Islamic countries create enough room for better portfolio diversification benefits. Similarly, Yilmaz et al. (2015) examined the effect of excess global financialization on major Islamic sectors’ equity indices using DCC-GARCH and DECO models. They demonstrated that not only financialization but also firm fundamentals and real economic factors play a significant role in growing the value of Islamic equity. These findings suggested that Islamic equity indices are also willing to be exposed to global shocks, as it helps the investors to know the structure of Islamic equity indices (Nagayev et al. 2016). However, Mensi et al. (2017b) investigated the conditional correlation structure for an effective hedging strategy between conventional and Islamic equity indices using MGARCH models. The empirical evidence reported that the conditional correlation is significant, and it shows a time-varying dependency among all pairwise indices, except the utility and telecommunication sectors. Moreover, Kabir et al. (2017) and Majdoub et al. (2018) suggested that Islamic equities offer better portfolio opportunities due to distinct features of Shariah law. Therefore, Muslim investors not only desire to earn maximum returns but also want to see a reflection of their moral and religious values in their investments.

Saiti and Noordin (2018) reported that Malaysian-based investors diversified their investments in the world’s ten largest South Asian countries and developed countries, such as China, Japan, Hong Kong, India, UK, USA, Canada, France, Germany, and Switzerland, based conventional and Islamic stock markets and they obtained better returns from their combined portfolios between the Islamic and conventional stock indices. Moreover, this study identifies the risk averters and chasers’ frontiers. Hence, Islamic stock indices deal with risk averters and conventional stock indices favor tail risk frontiers. In their recent study, Ying et al. (2020) supported the findings that are in line with the previous study of Baker et al. (2012). They stated that investors show a low demand for the safe-haven products during a high sentiment period, while investors look forward to quality during a low sentiment-holding period. Khalfaoui et al. (2015) analyzed hedging and volatility spillovers between the oil and stock markets of G7 countries. They used the mean and volatility spillovers of oil and stock market prices over various time horizons by using the wavelet-based MGARCH approach. Their results show strong evidence of significant volatility spillovers between oil and stock markets, as well as time-varying correlations for various market pairs. Mensi et al. (2017a) examined risk spillover between developed and emerging countries’ stock markets. They found significant and time-varying volatility spillovers between oil and stock markets. Moreover, Bouri et al. (2018) investigated the volatility spillover between developed and commodity markets. They used the Bayesian graphical vector autoregressive model. They found that predictability depends on global and regional VIXs. Furthermore, Bouri et al. (2020) explored the role of business cycle proxies, measured by the output gap at the global, regional, and local levels as a potential predictor of stock market volatility in BRICS countries. They found that the emerging BRICS countries exhibit a rather heterogeneous pattern when it comes to the relative role of idiosyncratic factors. In 2022, Sifat et al. (2022) studied the interbank liquidity risk transmission to BRICS in crisis periods. Their results show weak associations between the interbank credit market and US monetary policy and market conditions.

In sum, a few limited empirical studies, to the best of our knowledge, have investigated the frequency–time domain properties among traditional and Islamic stock markets in emerging and developed countries along with the establishment of a link to investors’ sentiment and psychology. The current study fills these gaps by employing a multi-scale-based wavelet approach.

3. Methodology

3.1. Data

The data of this study were obtained from three developed countries (the USA, UK and Japan) and three developing countries (Malaysia, Indonesia and China). The daily closing price was taken from the selected indices, and the period considered was from 26 October 2007 until 7 June 2018. Due to dual availability and market capitalization, these variables were selected in both Shariah and non-Shariah compliant stock markets in order to examine co-movement for better portfolio diversification benefits. All data were obtained from DataStream. The researchers conducted a matched-pair comparison between the two groups since conventional and Islamic measurements were evaluated for the same length of time.

Along with the mainstream indices, several Muslim and non-Muslim countries have launched Shariah-based indices to meet the demand of Islamic finance products and services. Table 1 represents the selected list of variables. Dow Jones is one of the largest index provider companies in the world. They launched the DJIMI in 1999. FTSE is the second-largest indices provider in the world. They launched their indices in 1999 for the London stock exchange. Standard and Poor (S&P) is another of the largest indices providers, and they established their Shariah indices in 2006. Consequently, many developed and developing countries like Japan, China and Indonesia have followed suit in order to cater to the demand for benchmark Shariah products.

Table 1.

Lists of variables.

3.2. Model Specification

The present study specified its model using the stock prices return form. The return form of data is expressed in natural logarithm criteria as a percentage multiplied by 100. Hence, the popular return transformation process is applied, such as the current stock index prices (Pt), and divided by the previous days’ prices (Pt−1). Here we demonstrate the return form formula:

Here, Rt denotes the stock return index and Pt and Pt−1 indicate the present days and previous days’ stock prices, respectively. Missing data and time differences due to bank and public holidays or other reasons in different markets are adjusted using the previous day’s prices. According to Chiang et al. (2007), it was once assumed that the most recent day’s prices remained unchanged and they should stay the same as the previous day’s prices.

However, the wavelet approach has been widely used as a dynamic econometric approach in recent years (Tien and Hung 2022; Vukovic et al. 2021). It is not only popular for signal and image processing activities in the Engineering and Physics disciplines but also has wide-range applications in the Finance and Social Science literature. Along with the signal processing properties, it critically investigates the time–frequency domain characteristics in finance applications. Notably, the prime focus of this approach is to measure a significant level of dependency and co-movement in multi-stage properties. This method can decompose data into different scales. Therefore, it can provide robust outcomes, unlike the standard time-series techniques (Ferrer et al. 2016). In addition, frequency and time band properties provide a better way to understand the higher (and lower) levels of co-movement for future investment decisions (Aguiar-Conraria et al. 2008). Notably, this nascent technique discusses the economic synergy that can overcome the shortcomings of structural breaking and error terms procedures (Antonakakis et al. 2018; Yang et al. 2017). The function of the wavelet is as follows:

where s and denotes the length and localization of the parameter, respectively. In other words, s presents normalization and 1 exhibits frequency–time scale dynamics. Furthermore, the Morlet-based wavelet is used in this study, which explains the father (smoothest) and mother (details) functions of the wavelet family (Reboredo et al. 2017). This function is as follows:

4π1/4 depicts the energy of wavelet that is here known as the band and central frequency. ϖο denotes the location of frequency and time domain properties. Moreover, indicates the Gaussian envelope, and eiϖοt shows complex wavelet analytics. Two set of techniques are broadly used from the wavelet family, such as CWT (continuous wavelet transformation) and DWT (discrete wavelet transformation). However, CWT is more a popular and wide-range acceptable technique that provides a very simple colorful orientation and it is also known as a multi-solution-based approach for contraction and dilatation, while DWT is known as a multi-resolution-based approach for data decomposition and re-composition (Aguiar-Conraria and Soares 2011).

where Ψ represents the function of details (mother) wavelet and * describes the complex link among the functions. Moreover, τ signifies the transformation of the parameter and S denotes for the scales of the parameter. The wavelet coherence function is as follows:

Here, R2 presents the wavelets coherence and S indicates the smoothing operator.

4. Results and Discussion

4.1. Primary Results

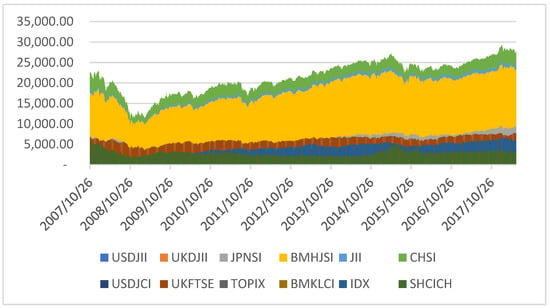

Figure 1 displays the stock indices price movement and this movement is expressed in local currencies. Preliminary, daily closing prices are abstracted from the selected stock indices. However, the stock prices movement show a positive momentum during the study period.

Figure 1.

Stock price performance.

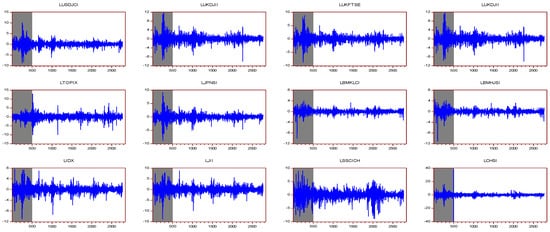

This study plots the return movement in Figure 2. Time series data are used in this study in a log form. The results demonstrate that stock prices return movement is volatile, while volatility movement dominated during the GFC period 2007–2008. However, the return indices’ trajectory indicates that they moved in lockstep and a comparable manner.

Figure 2.

Stock prices return movement.

4.2. Summary of Descriptive Statistics

Table 2 presents descriptive statistics summary for the return series. In line with the Islamic stock markets, the highest was shown for the USA, whereas the lowest average value was shown for the UK, respectively. Interestingly, the UK leads over China by its average value of the Islamic stock index perspectives. Preliminarily, the average value of JII was reported as better than the BMHJSI compliant stock index. However, the highest standard deviation was shown for both conventional and Islamic stock markets in China. In contrast, BMHJSI and BMKLCI were shown to be the least volatility among all the variables during the study period. Notably, skewness was also considered as an important moment of every distribution. It indicates symmetry and the asymmetric movements of the distribution. The symmetry of distribution is demonstrated by zero skewness. Negative skewness suggests an asymmetric distribution with an enormous tail inclined to the left, whereas positive skewness denotes an asymmetric distribution with a larger tail tilted to the right. Table 2 shows that the distributions of all indices are negatively skewed, meaning that stock price distributions are not symmetric, resulting in increased volatility and risk. Kurtosis, on the other hand, measured how fat the distribution is. This can be used to uncover the normal distribution of a series. It also shows how densely dispersed the data are and how they fit into the mean distribution. Data that are more peaked or flatly spread have a lower degree of regularity and vice-a-versa. The value of 3.00 represents the normal distribution. It is not clear from the normal distribution whether it peaked or was flat. Furthermore, a leptokurtic (peaked) distribution has a kurtosis value larger than 3.00, and a platykurtic (flat) distribution has a value less than 3.00. According to the preceding statistics, the conventional and Islamic stock markets have a leptokurtic (peaked) price distribution.

Table 2.

Summary of the descriptive statistics.

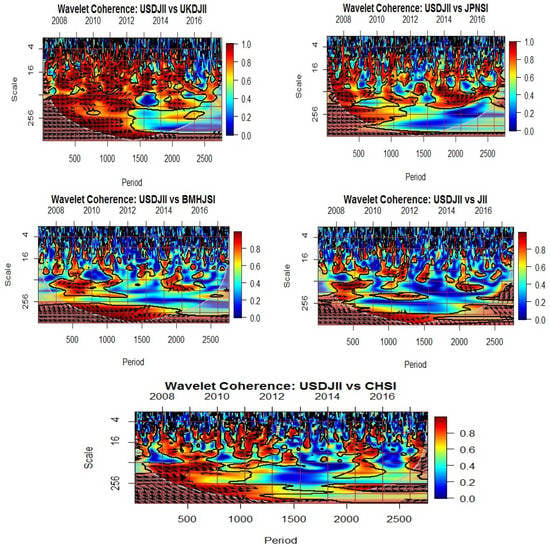

4.3. Wavelet Coherence Transformation (WCT)

This study investigates the co-movement and portfolio diversification opportunity nexus in developed and emerging stock markets using wavelet coherence techniques. Hence, color codes play a vital role in interpreting the results. The red color island measures the higher-level coherence (co-movement) and the blue island measures the comparatively lower level coherency (co-movement). Figure 3 shows the vivid red (blue) zones at the bottom (top) of the wavelet squared coherence plot. This indicates a strong (weak) coherency or co-movement at low (high) frequencies, respectively. In contrast, the presence of the red zone on the left implies that there is a significant level of co-movement among the variables. Hence, the study span can be decomposed into different scales and frequencies. The lower scales indicate the higher frequency and the higher scales followed by the lower frequency. The horizontal axis presents the study period from 26 October 2007 to 7 June 2018. There were 500, 1000, 1500, 2000 and 2500 working days starting on 26 October 2007 (2008/500, 2010/1000, 2012/1500, 2014/2000 and 2016/2500), indicating 500 and 2500 days, respectively. Another feature of this graph is the frequency with which events occur. The frequency element is represented by the vertical line, which comprises daily units and can range from 4 to 256 days in length. Moreover, the holding can be decomposed into different holding periods, such as short term (2–64), mid-range (64–128) and long term (128–256). A color component in the middle inspects how near the two indices move together. The warmer parts with red color indicate that the two series are strongly linked, whereas the colder regions with blue color indicate that they are not as closely linked as one might believe. However, the thick black line indicates the region which confirms the 5% statistical significance level. When the arrows are stand to the right, it indicates that the variables are in a phase and show a positive correlation, while the arrows that stand to the left demonstrate that the variables are out of phase and show a negative correlation, when the first variable shows its leading position. When the vector arrows are stand to the right and point down, this indicates that the second variable is in a leading position and vice versa (Madaleno and Pinho 2010; Sakti et al. 2018).

Figure 3.

WCT: USDJII vs. UKDJII; USDJII vs. JPNSI; USDJII vs. BMHJSI; USDJII vs. JII; USDJII vs. CHSI.

As exhibited in Figure 3, the interdependence among the Islamic stock markets is varies over frequency–time domain properties. However, the dependency among conventional and Islamic stock markets is strong at 4–512 band scales. The co-movement of conventional and Islamic stock markets can be significantly observed in developed and emerging countries. However, the USA Islamic stock market depicts higher coherency with the UK, Japan and China’s Islamic stock markets, while relatively lower coherency can be observed with the Malaysian and Indonesian Islamic stock markets (Bhuiyan et al. 2019). Findings further show that the GFC in 2007–2008 and the European debt crisis in 2012 substantially influenced developed countries’ stock markets, and, unsurprisingly, following the global and European debt crises, opened the door to grab portfolio diversification benefits from emerging countries’ Islamic stock markets in all holding periods.

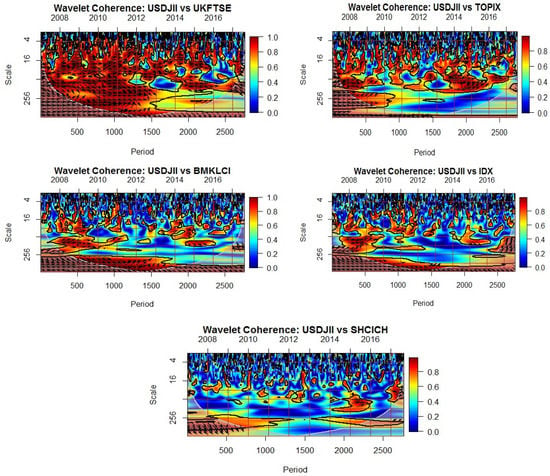

Figure 4 shows the conventional and Islamic stock markets’ dependency from developed and emerging countries’ perspectives. The UKFTSE and USDJII were strongly correlated at all levels (short-, medium- and long-term) from 2007 to 2013. This evidence indicates that the UKFTSE composite stock market was highly integrated with the US Islamic stock market during the GFC and Eurozone crisis periods. Therefore, a contagion effect is also observed in all frequency–time bands during both crises periods, which is consistent with the prior studies of Bodart and Candelon (2009) and Saiti et al. (2016). However, stock markets have a dynamic nature, which is crucial for analyzing financial gains from international stock market diversification. Furthermore, any potential return is dependent on international portfolio diversification, which is inversely proportional to stock market integration. A low correlation between two markets decreases portfolio risk while increasing the benefits of international diversification. In this setting, interdependent international stock prices symbolize economic integration via trade links and foreign direct investment. Across countries, stock prices may move in lockstep with underlying macroeconomic variables, market size and capitalization. However, due to the similar market trend, size, capitalization, macroeconomics and political influence, the US Islamic stock market is highly integrated with UK composite and Islamic stock markets. These findings are consistent with previous empirical evidence from Chittedi (2010) and Majid and Shabri (2018).

Figure 4.

WCT: USDJII vs. UKFTSE; USDJII vs. TOPIX; USDJII vs. BMKLCI; USDJII vs. IDX; USDJII vs. SHCICH.

Moreover, findings exhibit the wavelet coherence plots for the UK, Japan, Malaysia, Indonesia and Chinese composite (UKFTSE, TOPIX, BMKLCI, IDX and SHCICH) stock indices with the USA Islamic stock index (USDJII) return pairs. Overall, it can be seen on the diagram that there are more blue and light blue regions than red regions, except on UKFTSE, which indicates that the lower level of co-movement is observed among TOPIX, BMKLCI, IDA SHCICH and USDJII returns. In particular, the Chinese composite (SHCICH) market offers better portfolio opportunities for USDJII investors in all frequency and time domain properties. It is not surprising that the Chinese market still strongly appeals to foreign investors as a top choice. The business environment, economic strength and technological development mainly attracts foreign investors and offers the best business opportunities in China. As released in the World Investment Report in 2018, China, by itself, attracted 136 billion US dollar investment worth in 2017. These findings are supported and in line with the prior studies of (Gourène and Mendy 2018; Panda and Nanda 2017; Zhang and Li 2014). Moreover, market integration, financial contagion and trade linkages play an important role in making investment decisions. Financial contagion is closely and positively related to market integration, where an immediate shock in one market leads to a crisis in other highly integrated markets. For instance, if financial contagion arises in one developed country, it spreads to other developed countries more quickly. Due to increasing market integration, it is considered riskier to diversify all investments in the same regions only. Therefore, investors have a keen interest in diversifying their investments in emerging countries, although it is more desirable to create a portfolio in a combination of emerging and developed countries (Bouri et al. 2020; Joyo and Lefen 2019).

4.4. Robustness Check

Interestingly, the robust results are similar to the earlier wavelet coherence results, which is a pleasant surprise. When only the selected markets are considered, the China composite equity market offers the greatest opportunity for portfolio diversification across all investment horizons and scales, whereas the China Islamic index offers portfolio benefits primarily when only the short-term holding period is considered, as shown in the chart below (D1 and D2 scales). Comparatively, the US Islamic index shows portfolio benefits on a lower scale (higher frequency) at level 1 (D1). On the contrary, the higher correlation between the US composite and US Islamic index does not offer any benefits on any scale (d1–d8). However, from developed and emerging countries’ perspectives, emerging countries provide better portfolio opportunities for US Shariah-based investors in short-run investment horizons.

Table 3 indicates the wavelet-based correlation analysis results. These findings from the wavelet-based MODWT analysis decompose time series data into multi-scales, such as d1–d8. These scales indicate different investment horizons. For example, d1–d5 indicates a short-term holding period, d5–d6 indicates a medium-term holding period and d7–d8 indicates the long-term holding period (Dahir et al. 2018). The results of the wavelet-based decomposition correlation are consistent with wavelet coherence analysis, which justifies the research objective robustly. The evidence confirms that the degree of stock market co-movement depends not only on time–domain properties but also on different frequency band scales. For example, some markets offer portfolio benefits in lower correlation level properties in short and medium-term holding periods. On the other hand, some markets open windows for portfolio benefits for long-term holding periods.

Table 3.

Wavelet-based decomposed correlation analysis.

5. Conclusions

This study investigated the dynamic relationship between conventional and Islamic stock markets in developed and emerging countries by considering the investors’ behavior and psychology. The robust findings show a significant level of co-movement between conventional and Islamic stock markets in developed and emerging countries, which vary in terms of time–frequency domain properties. Particularly, the dependency among conventional and Islamic stock markets is strong at 4–512 band scales. However, the USA Islamic stock market illustrates a higher level of coherency with the UK, Japan and China’s Islamic stock markets but a relatively low level of co-movement is detected with the Chinese composite, Malaysian and Indonesian Islamic stock markets. The findings further confirm that the developed countries’ stock markets were substantially influenced by the GFC in 2007–2008 and the European debt crisis in 2012, while this trend is unsurprisingly observed in the emerging markets on a similar scale.

This study provided several insights based on empirical findings. First, the degree of co-movement varies among the developed and emerging countries’ stock markets. For instance, some investors are ready to grab benefits from short-term investment avenues, some are happy to invest in the long-term and others may choose a mid-term holding period for better-expected returns. In this context, investor behavior and psychology, information, trade-ties, real sector contributions and long-term convergence play a prime role in making investment decisions. Second, a lower dependency or coherency is observed in both developed and emerging stock markets except the UK. Third, China composite stock markets offer better diversification benefits in all band scales with USDJII. Finally, there was a strong convergence observed during the GFC and European debt crises among developed countries’ Islamic and traditional stock market indices.

All the evidence conveyed several insights regarding the policy implications of this study. First, investors can choose the alternative investment horizons in different characterized products, which offer portfolio gains. Furthermore, the findings of this study have confirmed that the conventional and Islamic stock markets are not separate, whether in developed or emerging countries. Interdependency and level of co-movement differ from country to country, however, following different time and scale properties. These implications may have practical uses for investors regarding assets price performance evaluation, risk management strategies and portfolio decisions (Ahmed 2018). Second, fund managers can take the appropriate steps to assess market movement in international avenues. Because of portfolio strategy, success depends on a better understanding of market co-movement by innovative measures (Sharma and Seth 2012). Wavelet is an innovative econophysical technique that helps to gauge the stock market co-movement by time-frequency domain properties. Lower scales indicate the higher frequency and confirm short-term co-movement. On the other hand, higher scales exhibit a lower frequency and offer a long-term co-movement. Therefore, this study provides a clear understanding to investors and portfolio managers to identify the perception and concerns of different investors according to their investment horizons.

Third, financial institutions, policymakers and monetary authorities should take proper steps to revise the provisions and movements of funds for economic development and growth. Financial policymakers can take defensive or offensive actions to protect excessive fund inflow or outflow. For example, the USA imposed a 25% tariff on Chinese goods in 2018. On the other hand, some countries may plan to liberalize their policies to attract foreign investment through market channels. Malaysia, Indonesia and China are the best examples of endeavoring to attract foreign funds. Regarding these perspectives, policymakers may introduce alternative products and services, creating new avenues for investment horizons (Hassan and Choudhury 2019).

Finally, as a theoretical implication, this study discussed the issue of stock markets’ co-movement and performance conceptually, theoretically and methodologically. One of the theoretical implications for researchers and academicians is that, as a specific concept, stock market co-movement contains distinguished features from other ideas, such as stock market integration. However, as a novel technique, the multi-solution-based wavelet approach provides more insights than Fourier analysis and resolves the drawback of the standard time-series techniques. Furthermore, while the wavelet was first introduced in econophysics, it has recently gained popularity and is discussed in the literature as a wavelet-based financial econometric synergy, which covers the shortcoming of the error term and structural changes (Yang et al. 2017; Ferrer et al. 2016).

In sum, the findings of this current study provide fresh insights for investors and fund managers as well as policymakers regarding the optimum level of co-movement and market integration. This study is limited to conventional and Islamic stock indices and the period of study did not extend past 2018. However, subject to the availability of data, future research should be carried out on sectorial and uncertainty indices and the study period should be expanded to take into account how COVID-19 has influenced the stock markets and how it affected the price movement of stock indices in developed and emerging countries.

Author Contributions

All authors contributed equally to this study. All authors have read and agreed to the published version of the manuscript.

Funding

We have received no funding or any other financial support for the conduct of this research.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data that support the findings of this study is available on request.

Conflicts of Interest

All the authors declare that we have no potential conflicts regarding the conduct of research that may interrupt the publication process.

References

- Aamir, Muhammad, and Syed Zulfiqar Ali Shah. 2018. Determinants of stock market co-movements between Pakistan and Asian emerging economies. Journal of Risk and Financial Management 11: 32. [Google Scholar] [CrossRef] [Green Version]

- Abbes, Mouna Boujelbene, and Yousra Trichilli. 2015. Islamic stock markets and potential diversification benefits. Borsa Istanbul Review 15: 93–105. [Google Scholar] [CrossRef] [Green Version]

- Aguiar-Conraria, Luís, and Maria Joana Soares. 2011. The Continuous Wavelet Transform: A Primer (No. 16/2011). Braga: NIPE-Universidade do Minho. [Google Scholar]

- Aguiar-Conraria, Luís, Nuno Azevedo, and Maria Joana Soares. 2008. Using wavelets to decompose the time—Frequency effects of monetary policy. Physica A: Statistical Mechanics and Its Applications 387: 2863–78. [Google Scholar] [CrossRef] [Green Version]

- Ahmed, Walid M. 2018. How do Islamic versus conventional equity markets react to political risk? Dynamic panel evidence. International Economics 156: 284–304. [Google Scholar] [CrossRef]

- Ahmed, Abdullahi D., and Rui Huo. 2019. Impacts of China’s crash on Asia-Pacific financial integration: Volatility interdependence, information transmission and market co-movement. Economic Modelling 79: 28–46. [Google Scholar] [CrossRef]

- Alam, Md Samsul, Syed Jawad Hussain Shahzad, and Román Ferrer. 2019. Causal flows between oil and forex markets using high-frequency data: Asymmetries from good and bad volatility. Energy Economics 84: 104513. [Google Scholar] [CrossRef]

- Aloui, Chaker, Shawkat Hammoudeh, and Hela Ben Hamida. 2015. Co-movement between sharia stocks and sukuk in the GCC markets: A time-frequency analysis. Journal of International Financial Markets, Institutions and Money 34: 69–79. [Google Scholar] [CrossRef]

- Anas, Muhammad, Ghulam Mujtaba, Sadaf Nayyar, and Saira Ashfaq. 2020. Time-frequency based dynamics of decoupling or integration between Islamic and conventional equity markets. Journal of Risk and Financial Management 13: 156. [Google Scholar] [CrossRef]

- Antar, Monia, and Fatma Alahouel. 2019. Co-movements and diversification opportunities among Dow Jones Islamic indexes. International Journal of Islamic and Middle Eastern Finance and Management 13: 94–115. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, Tsangyao Chang, Juncal Cunado, and Rangan Gupta. 2018. The relationship between commodity markets and commodity mutual funds: A wavelet-based analysis. Finance Research Letters 24: 1–9. [Google Scholar] [CrossRef] [Green Version]

- Baker, Malcolm, Jeffrey Wurgler, and Yu Yuan. 2012. Global, local, and contagious investor sentiment. Journal of Financial Economics 104: 272–87. [Google Scholar] [CrossRef] [Green Version]

- Balli, Faruk, Hatice O. Balli, Rosmy Jean Louis, and Tuan Kiet Vo. 2015. The transmission of market shocks and bilateral linkages: Evidence from emerging economies. International Review of Financial Analysis 42: 349–57. [Google Scholar] [CrossRef]

- Bhuiyan, Rubaiyat Ahsan, Maya Puspa Rahman, Buerhan Saiti, and Gairuzazmi Bin Mat Ghani. 2018. Financial integration between sukuk and bond indices of emerging markets: Insights from wavelet coherence and multivariate-GARCH analysis. Borsa Istanbul Review 18: 218–30. [Google Scholar] [CrossRef]

- Bhuiyan, Rubaiyat Ahsan, Maya Puspa Rahman, Buerhan Saiti, and Gairuzazmi Bin Mat Ghani. 2019. Does the Malaysian sovereign sukuk market offer portfolio diversification opportunities for global fixed-income investors? Evidence from wavelet coherence and multivariate-GARCH analyses. The North American Journal of Economics and Finance 47: 675–87. [Google Scholar] [CrossRef]

- Boako, Gideon, and Paul Alagidede. 2017. Co-movement of Africa’s equity markets: Regional and global analysis in the frequency–time domains. Physica A: Statistical Mechanics and Its Applications 468: 359–80. [Google Scholar] [CrossRef]

- Bodart, Vincent, and Bertrand Candelon. 2009. Evidence of interdependence and contagion using a frequency domain framework. Emerging Markets Review 10: 140–50. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, Seyedmehdi Hosseini, and Chi Keung Marco Lau. 2018. Does global fear predict fear in BRICS stock markets? Evidence from a Bayesian Graphical Structural VAR model. Emerging Markets Review 34: 124–42. [Google Scholar]

- Bouri, Elie, Riza Demirer, Rangan Gupta, and Xiaojin Sun. 2020. The predictability of stock market volatility in emerging economies: Relative roles of local, regional, and global business cycles. Journal of Forecasting 39: 957–65. [Google Scholar] [CrossRef]

- Buriev, Abdul Aziz, Ginanjar Dewandaru, Mohd-Pisal Zainal, and Mansur Masih. 2018. Portfolio diversification benefits at different investment horizons during the Arab uprisings: Turkish perspectives based on MGARCH–DCC and wavelet approaches. Emerging Markets Finance and Trade 54: 3272–93. [Google Scholar] [CrossRef]

- Chiang, Thomas C., Bang Nam Jeon, and Huimin Li. 2007. Dynamic correlation analysis of financial contagion: Evidence from Asian markets. Journal of International Money and Finance 26: 1206–28. [Google Scholar] [CrossRef]

- Chittedi, Krishna Reddy. 2010. Global stock markets development and integration: With special reference to BRIC countries. International Review of Applied Financial Issues and Economics 2: 18–36. [Google Scholar]

- Chuluun, Tuugi. 2017. Global portfolio investment network and stock market co-movement. Global Finance Journal 33: 51–68. [Google Scholar] [CrossRef]

- Dahir, Ahmed Mohamed, Fauziah Mahat, Nazrul Hisyam Ab Razak, and A. N. Bany-Ariffin. 2018. Revisiting the dynamic relationship between exchange rates and stock prices in BRICS countries: A wavelet analysis. Borsa Istanbul Review 18: 101–13. [Google Scholar] [CrossRef]

- Dewandaru, Ginanjar, Syed Aun R. Rizvi, Rumi Masih, Mansur Masih, and Syed Othman Alhabshi. 2014. Stock market co-movements: Islamic versus conventional equity indices with multi-timescales analysis. Economic Systems 38: 553–71. [Google Scholar] [CrossRef]

- El Amri, Henda, and Taher Hamza. 2017. Are there causal relationships between Islamic versus conventional equity indices? International Evidence. Studies in Business and Economics 12: 40–60. [Google Scholar] [CrossRef]

- Ferrer, Román, Vicente J. Bolós, and Rafael Benítez. 2016. Interest rate changes and stock returns: A European multi-country study with wavelets. International Review of Economics & Finance 44: 112. [Google Scholar]

- Goldstein, Itay. 2012. Empirical literature on financial crises: Fundamentals vs. panic. The Evidence and Impact of Financial Globalization, 523–34. [Google Scholar]

- Gourène, Grakolet Arnold Zamereith, and Pierre Mendy. 2018. Oil prices and African stock markets co-movement: A time and frequency analysis. Journal of African Trade 5: 55–67. [Google Scholar] [CrossRef]

- Grubel, Herbert G. 1968. Internationally diversified portfolios: Welfare gains and capital flows. The American Economic Review 58: 1299–314. [Google Scholar]

- Hassan, Abul, and Masudul Alam Choudhury. 2019. Islamic Economics: Theory and Practice. London: Routledge. [Google Scholar]

- Joyo, Ahmed Shafique, and Lin Lefen. 2019. Stock market integration of Pakistan with its trading partners: A multivariate DCC-GARCH model approach. Sustainability 11: 303. [Google Scholar] [CrossRef] [Green Version]

- Kabir, Sarkar Humayun, A. Mansur M. Masih, and Obiyathulla Ismath Bacha. 2017. Risk–profiles of Islamic equities and commodity portfolios in different market conditions. Emerging Markets Finance and Trade 53: 1477–500. [Google Scholar] [CrossRef]

- Khalfaoui, Rabeh, Mohamed Boutahar, and Heni Boubaker. 2015. Analyzing volatility pillovers and hedging between oil and stock markets: Evidence from wavelet analysis. Energy Economics 49: 540–49. [Google Scholar] [CrossRef]

- Khan, Taimur A. 2011. Co-integration of international stock markets: An investigation of diversification opportunities. Economic Review 8: 7. [Google Scholar]

- Lehkonen, Heikki. 2014. Stock market integration and the global financial crisis. Review of Finance 19: 2039–94. [Google Scholar] [CrossRef] [Green Version]

- Li, Xiyang, Xiaoyue Chen, Bin Li, Tarlok Singh, and Kan Shi. 2021. Predictability of stock market returns: New evidence from developed and developing countries. Global Finance Journal, 100624. [Google Scholar] [CrossRef]

- Loh, Lixia. 2013. Co-movement of Asia-Pacific with European and US stock market returns: A cross-time-frequency analysis. Research in International Business and Finance 29: 1–13. [Google Scholar] [CrossRef]

- Madaleno, Mara, and Carlos Pinho. 2010. Relationship of the multi-scale variability on world indices. Revista De Economia Financiera 20: 69–92. [Google Scholar]

- Majdoub, Jihed, and Walid Mansour. 2014. Islamic equity market integration and volatility spillover between emerging and US stock markets. The North American Journal of Economics and Finance 29: 452–70. [Google Scholar] [CrossRef]

- Majdoub, Jihed, Walid Mansour, and Arrak Islem. 2018. Volatility Spillover among Equity Indices and Crude Oil Prices: Evidence from Islamic Markets. Journal of King Abdulaziz University: Islamic Economics 31: 27–45. [Google Scholar] [CrossRef]

- Majid, M. Shabri Abd, and M. Shabri. 2018. Who Co-moves the Islamic Stock Market of Indonesia-the US, UK or Japan? Journal of Islamic Economics 10: 267–84. [Google Scholar]

- Markowitz, Harry. 1958. Portfolio Selection. Efficient Diversification of Investments. New Haven and London: Yale University Press. [Google Scholar]

- Mensi, Walid, Shawkat Hammoudeh, and Sang Hoon Kang. 2017a. Risk spillovers and portfolio management between developed and BRICS stock markets. The North American Journal of Economics and Finance 41: 133–55. [Google Scholar] [CrossRef]

- Mensi, Walid, Syed Jawad Hussain Shahzad, Shawkat Hammoudeh, Rami Zeitun, and Mobeen Ur Rehman. 2017b. Diversification potential of Asian frontier, BRIC emerging and major developed stock markets: A wavelet-based value at risk approach. Emerging Markets Review 32: 130–47. [Google Scholar] [CrossRef]

- Mensi, Walid, Besma Hkiri, Khamis H. Al-Yahyaee, and Sang Hoon Kang. 2018. Analyzing time–frequency comovements across gold and oil prices with BRICS stock markets: A VaR based on wavelet approach. International Review of Economics& Finance 54: 74–102. [Google Scholar]

- Nagayev, Ruslan, Mustafa Disli, Koen Inghelbrecht, and Adam Ng. 2016. On the dynamic links between commodities and Islamic equity. Energy Economics 58: 125–40. [Google Scholar] [CrossRef]

- Najeeb, Syed Faiq, Obiyathulla Bacha, and Mansur Masih. 2015. Does heterogeneity in investment horizo affect portfolio diversification? some insights using M-GARCH-DCC and wavelet correlation analysis. Emerging Markets Finance and Trade 51: 188–208. [Google Scholar] [CrossRef]

- Ng, Sew Lai, Wen Cheong Chin, and Lee Lee Chong. 2017. Multivariate market risk evaluation between Malaysian Islamic stock index and sectoral indices. Borsa Istanbul Review 17: 49–61. [Google Scholar] [CrossRef] [Green Version]

- Obstfeld, Maurice. 2021. Trilemmas and tradeoffs: Living with financial globalization. In The Asian Monetary Policy Forum: Insights for Central Banking. Singapore: World Scientific, pp. 16–84. [Google Scholar] [CrossRef]

- OECD. 2018. Available online: https://www.oecd.org/iaos2018/programme/IAOS-OECD2018_Elkjaer-Damgaard.pdf (accessed on 19 September 2018).

- Panda, Ajaya Kumar, and Swagatika Nanda. 2017. Short-term and long-term Interconnectedness of stock returns in Western Europe and the global market. Financial Innovation 3: 1–24. [Google Scholar] [CrossRef] [Green Version]

- Rahim, Adam Mohamed, and Mansur Masih. 2016. Portfolio diversification benefits of Islamic investors with their major trading partners: Evidence from Malaysia based on MGARCH-DCC and wavelet approaches. Economic Modelling 54: 425–38. [Google Scholar] [CrossRef]

- Reboredo, Juan C., Miguel A. Rivera-Castro, and Andrea Ugolini. 2017. Wavelet-based test of co-movement and causality between oil and renewable energy stock prices. Energy Economics 61: 241252. [Google Scholar] [CrossRef]

- Rua, António, and Luís C. Nunes. 2009. International co-movement of stock market returns: A wavelet analysis. Journal of Empirical Finance 16: 632–39. [Google Scholar] [CrossRef] [Green Version]

- Sahabuddin, Mohammad, Junaina Muhammad, Mohamed Hisham Yahya, and Sabarina Mohammed Shah. 2020. Co-movements between Islamic and Conventional Stock Markets: An Empirical Evidence. Jurnal Ekonomi Malaysia 54: 27–40. [Google Scholar]

- Saiti, Buerhan, and Nazrul Hazizi Noordin. 2018. Does Islamic equity investment provide diversification benefits to conventional investors? evidence from the multivariate GARCH analysis. International Journal of Emerging Markets 13: 267–89. [Google Scholar] [CrossRef]

- Saiti, Buerhan. 2015. Cointegration of Islamic stock indices: Evidence from five ASEAN countries. International Journal of Scientific & Engineering Research 6: 1392–405. [Google Scholar]

- Saiti, Buerhan, Obiyathulla I. Bacha, and Mansur Masih. 2014. The diversification benefits from Islamic investment during the financial turmoil: The case for the US-based equity investors. Borsa Istanbul Review 14: 196–211. [Google Scholar] [CrossRef] [Green Version]

- Saiti, Buerhan, Obiyathulla Ismath Bacha, and Mansur Masih. 2016. Testing the conventional and Islamic financial market contagion: Evidence from wavelet analysis. Emerging Markets Finance and Trade 52: 1832–49. [Google Scholar] [CrossRef] [Green Version]

- Sakti, Muhammad Rizky Prima, Mansur Masih, Buerhan Saiti, and Mohammad Ali Tareq. 2018. Unveiling the diversification benefits of Islamic equities and commodities: Evidence from multivariate-GARCH and continuous wavelet analysis. Managerial Finance 44: 830–50. [Google Scholar] [CrossRef]

- Sharif, Arshian, Chaker Aloui, and Larisa Yarovaya. 2020. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis 70: 101496. [Google Scholar] [CrossRef]

- Sharma, Anil, and Neha Seth. 2012. Literature review of stock market integration: A global perspective. Qualitative Research in Financial Markets 4: 84–122. [Google Scholar] [CrossRef]

- Sifat, Imtiaz, Alireza Zarei, Seyedmehdi Hosseini, and Elie Bouri. 2022. Interbank liquidity risk transmission to large emerging markets in crisis periods. International Review of Financial Analysis 82: 102200. [Google Scholar] [CrossRef]

- Song, Ge, Zhiqing Xia, Muhammad Farhan Basheer, and Syed Mehmood Ali Shah. 2021. Co-movement dynamics of US and Chinese stock market: Evidence from COVID-19 crisis. Economic Research-Ekonomska Istraživanja, 1–17. [Google Scholar] [CrossRef]

- Tien, Ho Thuy, and Ngo Thai Hung. 2022. Volatility spillover effects between oil and GCC stock markets: A wavelet-based asymmetric dynamic conditional correlation approach. International Journal of Islamic and Middle Eastern Finance and Management. [Google Scholar] [CrossRef]

- Vukovic, Darko B., Kseniya A. Lapshina, and Moinak Maiti. 2021. Wavelet coherence analysis of returns, volatility and interdependence of the US and the EU money markets: Pre & post crisis. The North American Journal of Economics and Finance 58: 101457. [Google Scholar]

- Xiao, Ling, and Gurjeet Dhesi. 2010. Volatility Spillover and Time-Varying Conditional Correlation between the European and US stock markets. Global Economy and Finance Journal 3: 148–64. [Google Scholar]

- Yang, Lu, Xiao Jing Cai, and Shigeyuki Hamori. 2017. Does the crude oil price influence the exchange rates of oil-importing and oil-exporting countries differently? A wavelet coherence analysis. International Review of Economics & Finance 49: 536–47. [Google Scholar]

- Yilmaz, Mustafa K., Ahmet Sensoy, Kevser Ozturk, and Erk Hacihasanoglu. 2015. Cross-sectoral interactions in Islamic equity markets. Pacific-Basin Finance Journal 32: 1–20. [Google Scholar] [CrossRef]

- Ying, Qianwei, Tahir Yousaf, Qurat Ul Ain, and Yasmeen Akhtar. 2020. Investor psychology, mood variations, and sustainable cross-sectional returns: A Chinese case study on investing in illiquid stocks on a specific day of the week. Frontiers in Psychology 11: 173. [Google Scholar] [CrossRef]

- Zhang, Bing, and Xiao-Ming Li. 2014. Has there been any change in the co-movement between the Chinese and US stock markets? International Review of Economics & Finance 29: 525536. [Google Scholar]

- Zhang, Xi, Yunjia Zhang, Senzhang Wang, Yuntao Yao, Binxing Fang, and S. Yu Philip. 2018. Improving stock market prediction via heterogeneous information fusion. Knowledge-Based Systems 143: 236–47. [Google Scholar] [CrossRef] [Green Version]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).