The Evolution of Job Lock in the U.S.: Evidence from the Affordable Care Act

Abstract

:1. Introduction

2. Background

3. Methods

4. Data

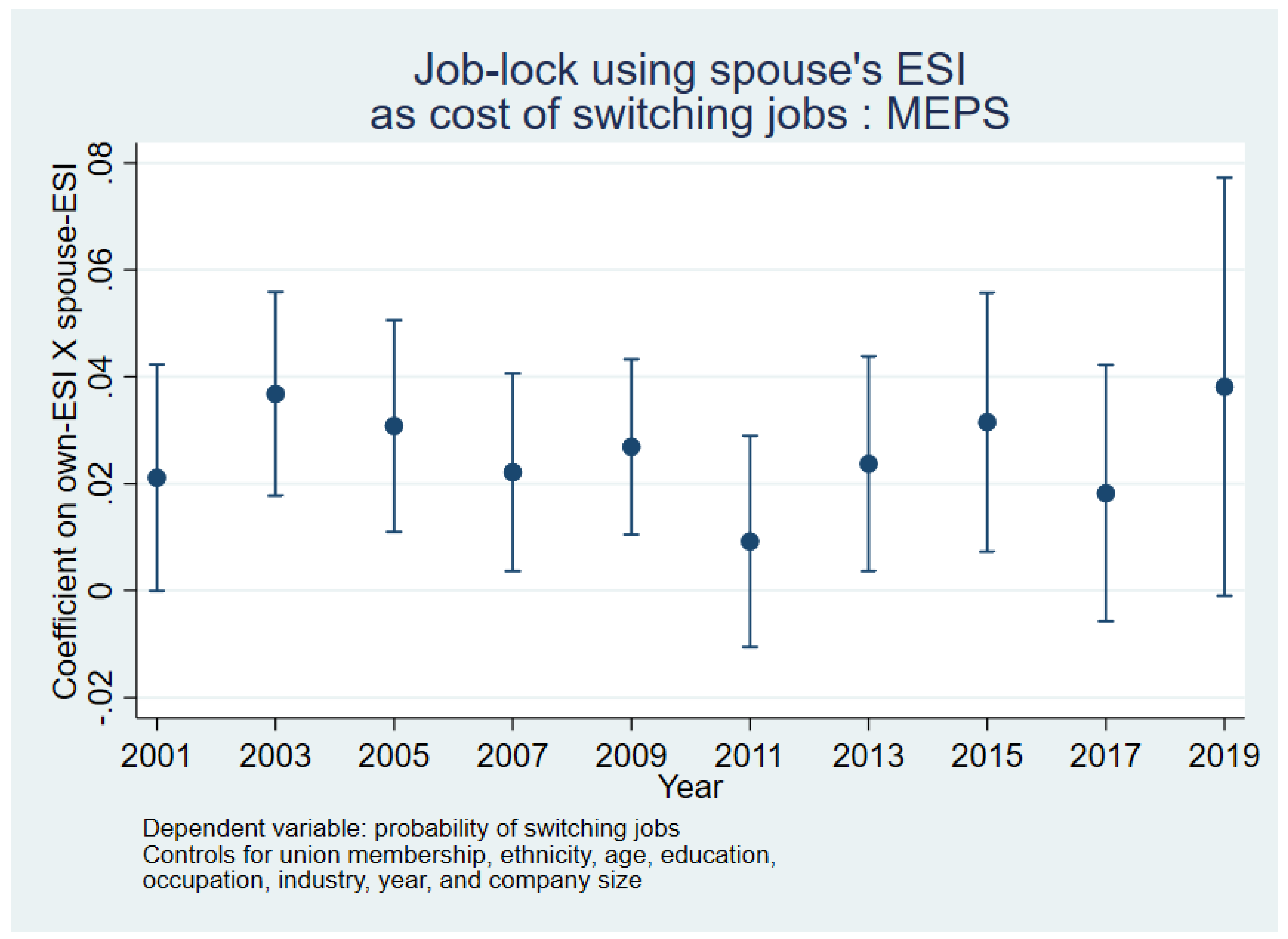

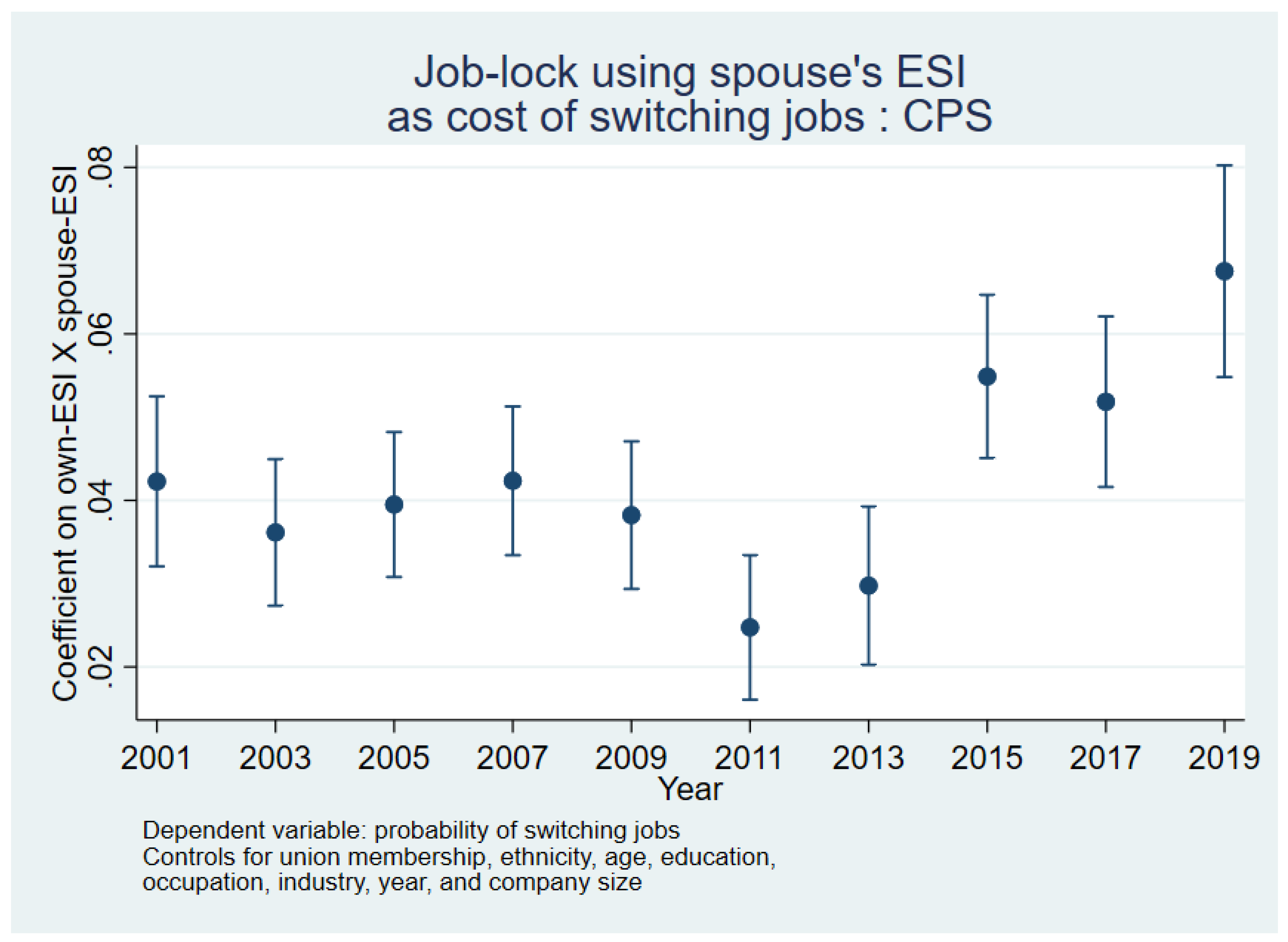

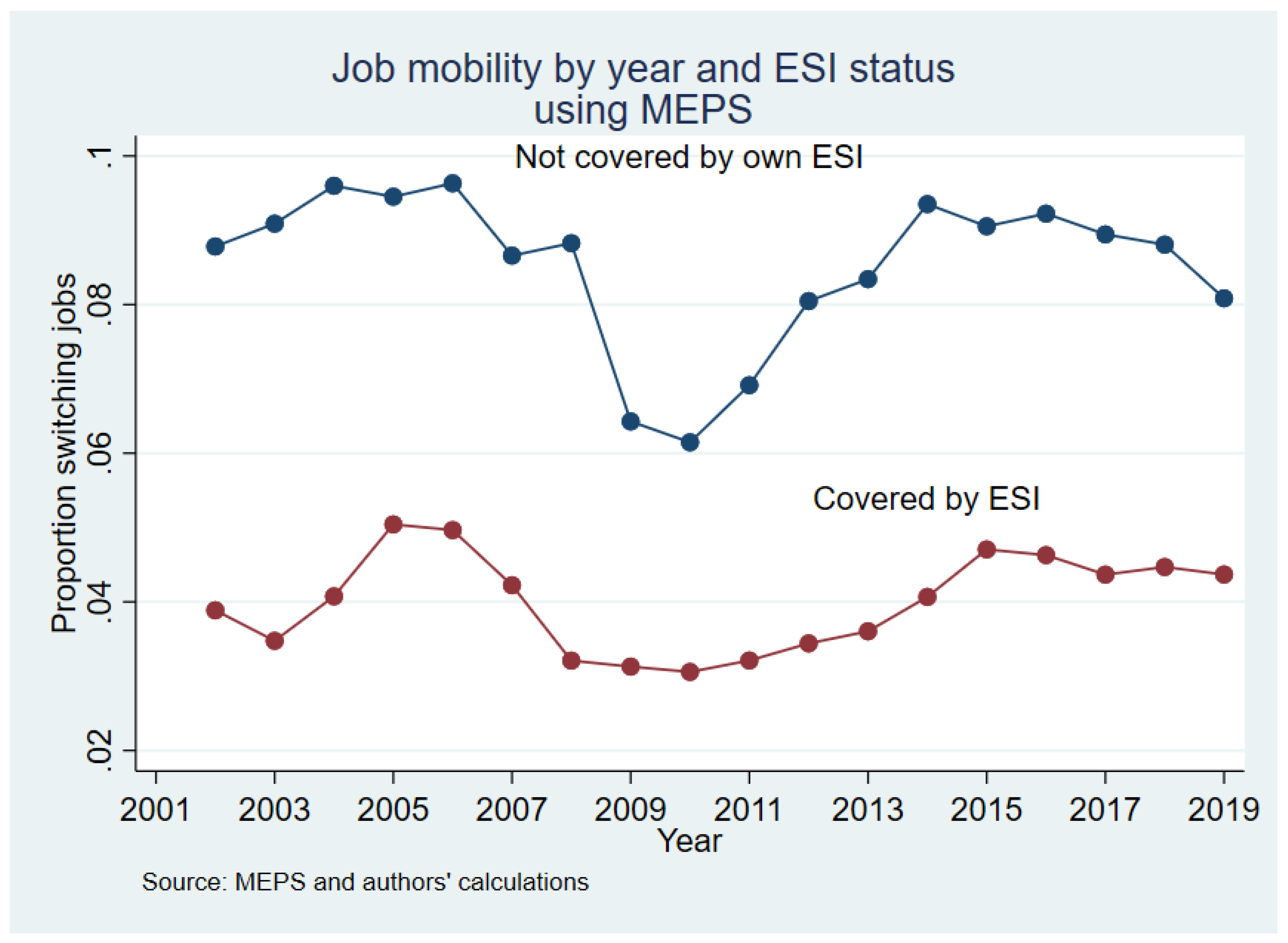

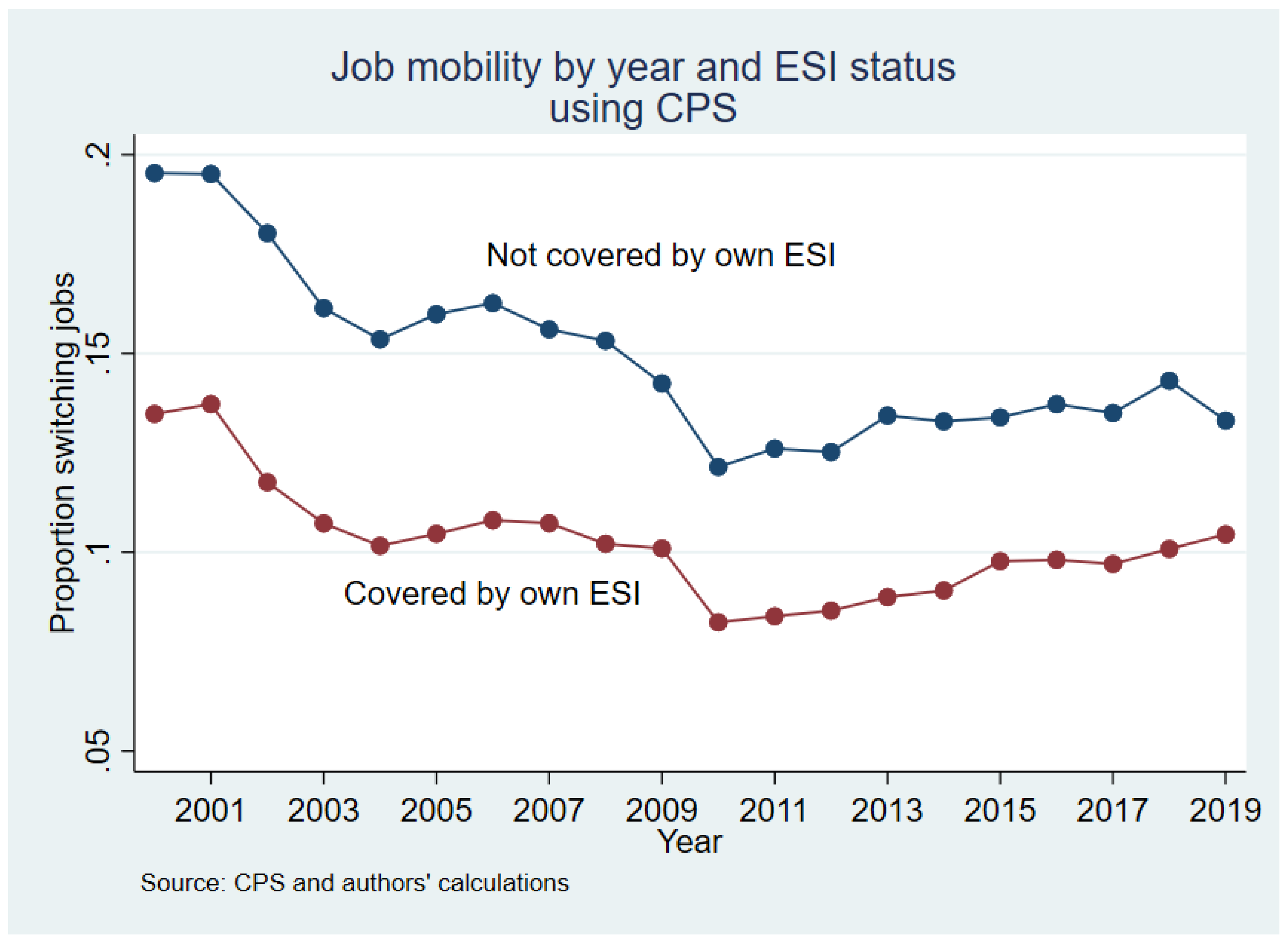

5. Results

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | See Colman et al. (2019) for an overview of the relationships between health insurance (both employer-sponsored health insurance and public coverage such as Medicaid) and labor supply, a review of the post-ACA literature. |

| 2 |

References

- Akosa Antwi, Yaa, Asako S. Moriya, and Kosali Simon. 2013. Effects of federal policy to insure young adults: Evidence from the 2010 Affordable Care Act’s dependent-coverage mandate. American Economic Journal: Economic Policy 5: 1–28. [Google Scholar]

- Aslim, Erkmen Giray. 2019. The relationship between health insurance and early retirement: Evidence from the Affordable Care Act. Eastern Economic Journal 45: 112–40. [Google Scholar] [CrossRef]

- Bailey, James. 2017. Health insurance and the supply of entrepreneurs: Evidence from the Affordable Care Act. Small Business Economics 49: 627–646. [Google Scholar] [CrossRef]

- Bailey, James, and Anna Chorniy. 2016. Employer-provided health insurance and job mobility: Did the affordable care act reduce job lock? Contemporary Economic Policy 34: 173–83. [Google Scholar] [CrossRef]

- Bailey, James, and Dhaval Dave. 2019. The Effect of the Affordable Care Act on Entrepreneurship among Older Adults. Eastern Economic Journal 45: 141–59. [Google Scholar] [CrossRef]

- Bureau of Labor Statistics. 2021. National Compensation survey. Available online: https://www.bls.gov/ncs/ (accessed on 23 June 2022).

- CBO (United States Congressional Budget Office). 1994. The Tax Treatment Of Employment-Based Health Insurance; Washington, DC: U.S. Government Printing Office.

- Claxton, Gary, Cynthia Cox, Anthony Damico, Larry Levitt, and Karen Pollitz. 2016. Pre-existing Conditions and Medical Underwriting in the Individual Insurance Market Prior to the ACA. Issue Brief, Kaiser Family Foundation. Available online: https://www.kff.org/health-reform/issue-brief/pre-existing-conditions-and-medical-underwriting-in-the-individual-insurance-market-prior-to-the-aca/ (accessed on 23 June 2022).

- Colman, Gregory, and Dhaval Dave. 2018. It’s about time: Effects of the affordable care act dependent coverage mandate on time use. Contemporary Economic Policy 36: 44–58. [Google Scholar] [CrossRef] [Green Version]

- Colman, Gregory, Dhaval Dave, and Otto Lenhart. 2019. Health Insurance and Labor Supply. Oxford Research Encyclopedia of Economics and Finance. Available online: https://oxfordre.com/economics/view/10.1093/acrefore/9780190625979.001.0001/acrefore-9780190625979-e-438 (accessed on 17 March 2021).

- Cooper, Philip F., and Alan C. Monheit. 1993. Does employment-related health insurance inhibit job mobility? Inquiry 30: 400–16. [Google Scholar]

- DeNavas-Walt, Carmen, Bernadette D. Proctor, and Jessica C. Smith. 2011. Income, Poverty, and Health Insurance Coverage in the United States: 2010; Census Bureau, Current Population Reports, P60-239; Washington, DC: U.S. Government Printing Office.

- Dey, Matthew S., and Christopher J. Flinn. 2005. An equilibrium model of health insurance provision and wage determination. Econometrica 73: 571–627. [Google Scholar] [CrossRef]

- Economic Report of the President. 2011. Council of Economic Advisors. Available online: https://obamawhitehouse.archives.gov/administration/eop/cea/economic-report-of-the-President/2011 (accessed on 23 June 2022).

- Flood, Sarah, Miriam King, Renae Rodgers, Steven Ruggles, and J. Robert Warren. 2020. Integrated Public Use Microdata Series, Current Population Survey: Version 8.0 [Dataset]. Minneapolis: IPUMS. [Google Scholar] [CrossRef]

- Gallagher, Emily, Nathan Blascak, Stephen Roll, and Michal Grinstein-Weiss. 2020. Health Insurance as an Income Stabilizer; FRB of Philadelphia Working Paper No. 20-05; Philadelphia: Federal Reserve Bank. [CrossRef]

- GAO (United States Government Accountability Office). 2011. Job Lock and the PPACA; (GAO Publication No. 12-166R); Washington, DC: U.S. Government Printing Office.

- Gilleskie, Donna B., and Byron F. Lutz. 2002. The Impact of Employer-Provided Health Insurance on Dynamic Employment Transitions. The Journal of Human Resources 37: 129–62. [Google Scholar] [CrossRef]

- Heim, Bradley T., and Ithai Z. Lurie. 2015. The Impact of Health Reform on Job Mobility: Evidence from Massachusetts. American Journal of Health Economics 1: 374–98. [Google Scholar] [CrossRef]

- Heim, Bradley, Ithai Lurie, and Kosali Simon. 2018. Did the Affordable Care Act young adult provision affect labor market outcomes? Analysis using tax data. ILR Review 71: 1154–78. [Google Scholar] [CrossRef] [Green Version]

- Jun, Dajung. 2018. The Effects of the Dependent Coverage Mandates on Fathers’ Job Mobility and Compensation. In Proceedings of the Annual Conference on Taxation and Minutes of the Annual Meeting of the National Tax Association. Washington, DC: National Tax Association, vol. 111, pp. 1–42. [Google Scholar] [CrossRef]

- Kofoed, Michael S., and Wyatt J. Frasier. 2019. [Job] Locked and [Un]loaded: The effect of the Affordable Care Act dependency mandate on reenlistment in the U.S. Army. Journal of Health Economics 65: 103–16. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Levy, Helen, Thomas C. Buchmueller, and Sayeh Nikpay. 2018. Health reform and retirement. The Journals of Gerontology: Series B 73: 713–22. [Google Scholar] [CrossRef] [PubMed]

- Madrian, Brigitte C. 1994. Employment-based health insurance and job mobility: Is there evidence of job-lock? The Quarterly Journal of Economics 109: 27–54. [Google Scholar] [CrossRef]

- Mitchell, Olivia S. 1982. Fringe benefits and labor mobility. The Journal of Human Resources 17: 286–98. [Google Scholar]

- Obama, Barack. 2012. Securing the future of American health care. New England Journal of Medicine 367: 1377–81. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- U.S. Census Bureau. 2021. 2017 SUSB Annual Data Tables by Establishment Industry. Available online: https://www.census.gov/data/tables/2017/econ/susb/2017-susb-annual.html (accessed on 23 June 2022).

- U.S. Department of Health and Human Services. 2017. The Future of the SHOP: CMS Intends to Allow Small Businesses in SHOPs Using HealthCare.gov More Flexibility when Enrolling in Healthcare Coverage. Available online: https://www.cms.gov/CCIIO/Resources/Regulations-and-Guidance/Downloads/The-Future-of-the-SHOP-CMS-Intends-to-Allow-Small-Businesses-in-SHOPs-Using-HealthCaregov-More-Flexibility-when-Enrolling-in-Healthcare-Coverage.pdf (accessed on 23 June 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Weighted Mean Pre-ACA | Standard Deviation Pre-ACA | Weighted Mean Post-ACA | Standard Deviation Post-ACA |

|---|---|---|---|---|

| Changed jobs (percent) | 6.2 | 24.1 | 6.9 | 25.4 |

| Respondent has ESI (percent) | 54.9 | 49.8 | 52.9 | 49.9 |

| Partner has ESI (percent) | 41.7 | 49.3 | 42.4 | 49.4 |

| Deniable condition (0/1) (percent) | 9.4 | 29.2 | 10.8 | 31.0 |

| Union member (percent) | 11.3 | 31.6 | 10.3 | 30.4 |

| Hispanic (percent) | 15.6 | 36.3 | 18.9 | 39.2 |

| Non-Hispanic White (percent) | 66.9 | 47.0 | 60.5 | 48.9 |

| Non-Hispanic Black (percent) | 10.2 | 30.3 | 10.9 | 31.2 |

| Non-Hispanic Asian (percent) | 6.1 | 23.8 | 6.8 | 25.1 |

| Non-Hispanic Other (percent) | 1.2 | 10.9 | 2.9 | 16.8 |

| Age in years | 37.9 | 9.9 | 37.5 | 10.0 |

| Married (percent) | 68.0 | 46.7 | 61.1 | 48.7 |

| Divorced (percent) | 7.0 | 25.4 | 6.7 | 25.0 |

| Separated (percent) | 1.7 | 12.7 | 1.6 | 12.5 |

| Widowed (percent) | 0.5 | 6.8 | 0.4 | 6.6 |

| Never married (percent) | 23.0 | 42.1 | 30.1 | 45.9 |

| Less than High School (percent) | 11.1 | 31.4 | 8.1 | 27.3 |

| High School (percent) | 29.3 | 45.5 | 25.5 | 43.6 |

| Some college (percent) | 26.5 | 44.1 | 27.8 | 44.8 |

| College (percent) | 20.9 | 40.7 | 24.4 | 43.0 |

| Graduate (percent) | 12.1 | 32.7 | 14.2 | 34.9 |

| Management, Business, and Financial (percent) | 15.1 | 35.8 | 17.4 | 37.9 |

| Professional and Related (percent) | 23.6 | 42.5 | 25.7 | 43.7 |

| Service (percent) | 15.4 | 36.1 | 15.9 | 36.6 |

| Sales and Related (percent) | 9.3 | 29.0 | 8.5 | 27.9 |

| Office and Administrative Support (percent) | 12.7 | 33.3 | 11.1 | 31.4 |

| Farming, Fishing, and Forestry (percent) | 0.8 | 8.6 | 0.7 | 8.2 |

| Construction, Extraction, and Maintenance (percent) | 9.8 | 29.8 | 8.4 | 27.8 |

| Production, Transportation (percent) | 13.2 | 33.9 | 12.3 | 32.8 |

| Military Specific (percent) | 0.1 | 2.5 | 0.0 | 2.0 |

| Natural Resources (percent) | 1.2 | 10.8 | 1.2 | 10.7 |

| Mining (percent) | 0.5 | 6.8 | 0.5 | 7.3 |

| Construction (percent) | 7.5 | 26.3 | 6.8 | 25.1 |

| Manufacturing (percent) | 12.4 | 32.9 | 11.2 | 31.6 |

| Wholesale and Retail Trade (percent) | 13.4 | 34.1 | 12.4 | 33.0 |

| Transportation and Utilities (percent) | 5.1 | 22.0 | 4.7 | 21.3 |

| Information (percent) | 2.4 | 15.2 | 2.2 | 14.7 |

| Financial Activities (percent) | 6.7 | 25.0 | 6.6 | 24.8 |

| Professional And Business Services (percent) | 10.7 | 30.9 | 12.2 | 32.7 |

| Education, Health, and Social Services (percent) | 22.3 | 41.7 | 23.7 | 42.5 |

| Leisure and Hospitality (percent) | 8.0 | 27.2 | 8.6 | 28.1 |

| Other Services (percent) | 4.6 | 21.0 | 4.4 | 20.5 |

| Public Administration (percent) | 5.2 | 22.1 | 5.4 | 22.6 |

| Military (percent) | 0.1 | 2.5 | 0.0 | 2.0 |

| Employment in firm | 141.7 | 181.0 | 131.1 | 174.2 |

| Pension available (percent) | 56.3 | 49.6 | 59.0 | 49.2 |

| Variable | Weighted Mean Pre-ACA | Standard Deviation Pre-ACA | Weighted Mean Post-ACA | Standard Deviation Post-ACA |

|---|---|---|---|---|

| Switches jobs (1/0) (percent) | 12.6 | 33.2 | 11.9 | 32.3 |

| Respondent has ESI (percent) | 52.5 | 49.9 | 50.1 | 50.0 |

| Family has ESI (percent) | 21.9 | 41.4 | 20.5 | 40.4 |

| Female (percent) | 47.3 | 49.9 | 47.4 | 49.9 |

| Age | 37.5 | 10.9 | 37.5 | 10.9 |

| Hispanic (percent) | 14.8 | 35.5 | 18.3 | 38.6 |

| non-Hispanic White (percent) | 67.4 | 46.9 | 61.3 | 48.7 |

| non-Hispanic Black (percent) | 11.2 | 31.5 | 11.8 | 32.3 |

| non-Hispanic Asian (percent) | 5.6 | 23.0 | 7.1 | 25.7 |

| non-Hispanic other (percent) | 1.0 | 10.1 | 1.5 | 12.2 |

| Less than High School (percent) | 10.4 | 30.5 | 8.2 | 27.4 |

| High School (percent) | 29.3 | 45.5 | 26.3 | 44.0 |

| Some college (percent) | 30.4 | 46.0 | 30.0 | 45.8 |

| College (percent) | 20.4 | 40.3 | 23.3 | 42.3 |

| Graduate (percent) | 9.5 | 29.4 | 12.2 | 32.7 |

| Married (percent) | 54.8 | 49.8 | 51.2 | 50.0 |

| Divorced (percent) | 10.2 | 30.2 | 9.1 | 28.8 |

| Separated (percent) | 2.5 | 15.6 | 2.3 | 15.0 |

| Widowed (percent) | 0.9 | 9.4 | 0.9 | 9.2 |

| Never married (percent) | 31.6 | 46.5 | 36.5 | 48.2 |

| Union Member (percent) | 15.7 | 36.4 | 14.6 | 35.3 |

| Agriculture, forestry and fisheries (percent) | 2.3 | 15.1 | 2.5 | 15.6 |

| Mining (percent) | 0.5 | 7.1 | 0.6 | 7.9 |

| Construction (percent) | 7.7 | 26.7 | 7.1 | 25.6 |

| Manufacturing (percent) | 11.9 | 32.4 | 10.1 | 30.1 |

| Transportation (percent) | 4.4 | 20.5 | 4.5 | 20.6 |

| Communications and public utilities (percent) | 2.5 | 15.7 | 2.3 | 14.9 |

| Trade (percent) | 21.0 | 40.7 | 21.0 | 40.8 |

| Finance, insurance, and real estate (percent) | 6.5 | 24.6 | 6.3 | 24.3 |

| Services (percent) | 43.1 | 49.5 | 45.6 | 49.8 |

| Executive, administrative, and managerial (percent) | 13.5 | 34.1 | 14.4 | 35.1 |

| Professional specialty (percent) | 17.0 | 37.6 | 19.6 | 39.7 |

| Technicians and related support (percent) | 3.1 | 17.4 | 2.9 | 16.9 |

| Sales (percent) | 11.3 | 31.7 | 10.6 | 30.8 |

| Administrative support, including clerical (percent) | 13.8 | 34.5 | 12.1 | 32.6 |

| Private household (percent) | 1.0 | 9.9 | 1.0 | 10.0 |

| Protective service (percent) | 2.1 | 14.4 | 2.2 | 14.5 |

| Service, except protective and household (percent) | 12.7 | 33.3 | 13.8 | 34.4 |

| Precision production, craft, and repair (percent) | 10.5 | 30.7 | 9.1 | 28.8 |

| Machine operators, assemblers, and inspectors (percent) | 4.7 | 21.2 | 4.0 | 19.7 |

| Transportation and material moving equipment (percent) | 4.1 | 19.7 | 3.9 | 19.4 |

| Handlers, equipment cleaners, helpers, and laborers (percent) | 3.7 | 19.0 | 3.8 | 19.2 |

| Farming, forestry, and fishing (percent) | 2.4 | 15.3 | 2.5 | 15.5 |

| Armed Forces | 0.0 | 0.0 | 0.0 | 0.0 |

| Number of employees | 6.0 | 3.2 | 6.2 | 3.1 |

| (A) | ||||||

| Dependent Variable: Job Switch | Pre-ACA | Post-ACA | Pre-ACA | Post-ACA | ||

| Changed jobs | Changed jobs | Changed jobs | Changed jobs | |||

| Respondent has ESI | −0.028 *** | −0.033 *** | −0.040 *** | −0.031 *** | ||

| (0.0035) | (0.0065) | (0.0027) | (0.0041) | |||

| Partner has ESI | −0.015 *** | −0.016 ** | ||||

| (0.0039) | (0.0071) | |||||

| Respondent has ESI X Partner has ESI | 0.017 *** | 0.018 ** | ||||

| (0.0043) | (0.0080) | |||||

| Deniable condition (0/1) | 0.021 ** | 0.036 *** | ||||

| (0.0089) | (0.012) | |||||

| Respondent has ESI X Deniable condition (0/1) | −0.020 ** | −0.028 ** | ||||

| (0.0100) | (0.014) | |||||

| Observations | 98,288 | 36,594 | 99,348 | 50,241 | ||

| (B) | ||||||

| Proportion of workers changing jobs per MEPS wave | ||||||

| Pre-ACA | Post-ACA | |||||

| R has ESI | Difference | R has ESI | Difference | |||

| Partner has ESI | No | Yes | No | Yes | ||

| No | 0.069 | 0.042 | −0.027 | 0.076 | 0.045 | −0.031 |

| Yes | 0.054 | 0.043 | −0.011 | 0.059 | 0.046 | −0.013 |

| Difference | 0.015 | −0.001 | 0.016 | 0.017 | −0.001 | 0.018 |

| (C) | ||||||

| Proportion of workers changing jobs per MEPS wave | ||||||

| Pre-ACA | Post-ACA | |||||

| R ESI | Difference | R ESI | Difference | |||

| Deniable Condition | No | Yes | No | Yes | ||

| No | 0.092 | 0.053 | −0.039 | 0.094 | 0.063 | −0.031 |

| Yes | 0.113 | 0.053 | −0.06 | 0.13 | 0.07 | −0.06 |

| Difference | −0.021 | 0 | −0.021 | −0.036 | −0.007 | −0.029 |

| (A) | ||||||

| Pre-ACA | Post-ACA | |||||

| Switches jobs | Switches jobs | |||||

| Respondent has ESI | −0.0436 *** | −0.0387 *** | ||||

| (0.00134) | (0.00170) | |||||

| Family has ESI | −0.0226 *** | −0.0209 *** | ||||

| (0.00185) | (0.00188) | |||||

| Respondent has ESI X Family has ESI | 0.0348 *** | 0.0557 *** | ||||

| (0.00203) | (0.00375) | |||||

| Observations | 1,229,859 | 448,419 | ||||

| (B) | ||||||

| Proportion of workers changing jobs each year (CPS) | ||||||

| Pre-ACA | Post-ACA | |||||

| R ESI | Difference | R ESI | Difference | |||

| Partner ESI | No | Yes | No | Yes | ||

| No | 0.155 | 0.111 | −0.044 | 0.141 | 0.102 | −0.039 |

| Yes | 0.132 | 0.124 | −0.008 | 0.12 | 0.137 | 0.017 |

| Difference | 0.023 | −0.013 | 0.036 | 0.021 | −0.035 | 0.056 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bailey, J.; Colman, G.; Dave, D. The Evolution of Job Lock in the U.S.: Evidence from the Affordable Care Act. J. Risk Financial Manag. 2022, 15, 296. https://doi.org/10.3390/jrfm15070296

Bailey J, Colman G, Dave D. The Evolution of Job Lock in the U.S.: Evidence from the Affordable Care Act. Journal of Risk and Financial Management. 2022; 15(7):296. https://doi.org/10.3390/jrfm15070296

Chicago/Turabian StyleBailey, James, Gregory Colman, and Dhaval Dave. 2022. "The Evolution of Job Lock in the U.S.: Evidence from the Affordable Care Act" Journal of Risk and Financial Management 15, no. 7: 296. https://doi.org/10.3390/jrfm15070296

APA StyleBailey, J., Colman, G., & Dave, D. (2022). The Evolution of Job Lock in the U.S.: Evidence from the Affordable Care Act. Journal of Risk and Financial Management, 15(7), 296. https://doi.org/10.3390/jrfm15070296