Stability and Growth Pact: Too Young to Die, Too Old to Rock ‘n’ Roll

Abstract

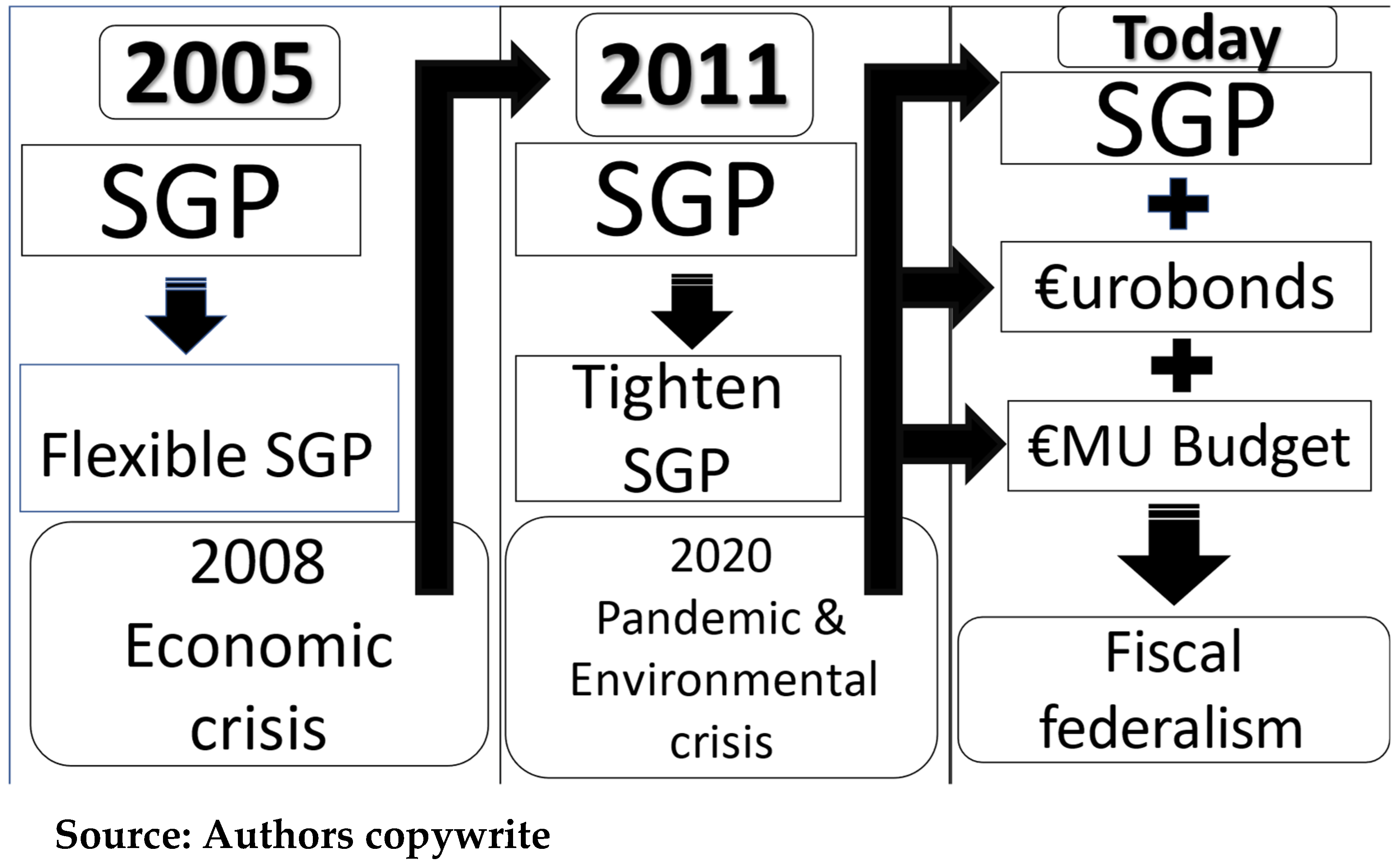

1. Introduction

2. Literature Review

3. Data and Methodology

- (i)

- We begin by ordering the N countries, starting first with the country that had the highest-ranking last period as first, and proceed with the country that had the next-highest ranking, and so forth until no country remains.

- (ii)

- We proceed with forming core clubs from the first k highest-ordered (as described in step (i)) where , and compute t-statistics () using (4). Club size k* is predefined by the t-statistic of the logt regressions for .

- (iii)

- Third, for a t-statistic greater than zero, we augment the core clubs of (ii) by one country at a time from the countries.

- (iv)

- We repeat steps (i)–(iii) until no further country-merging is possible.

4. Results

5. Discussion

6. Policy Implications

7. Limitations

8. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | Resolution of the European Council on the Stability and Growth Pact, OJ 1997, C 236/1, Council Regulation No. 1466/97 of 7 July 1997 on the strengthening of the surveillance of budgetary positions and the surveillance and co-ordination of economic policies, OJ 1997, L 209/1, and Council Regulation No. 1467/97 on speeding up and clarifying the implementation of the excessive deficit procedure, OJ L 209/6. |

| 2 | |

| 3 | A club is defined as a group of countries, converging to a single steady state, hence displaying similar characteristics regarding their level of deficits. |

| 4 | As the unification process of EMU members progresses, one would expect more similarity regarding SGP mandates and macroeconomic fundamentals. Diverging to a greater number of clubs, and not to a single club containing all members, indicates a need to reconsider the current form of the SGP. |

| 5 | For further information visit https://ec.europa.eu/commission/presscorner/detail/en/qanda_22_6563 (accessed on 9 December 2022). |

References

- Alesina, Alberto, Roberto Perotti, and Jose Tavares. 1998. The political economy of fiscal adjustments. In Brookings Papers on Economic Activity. Berlin and Heidelberg: Spring, pp. 197–266. [Google Scholar]

- Alesina, Alberto, Silvia Ardagna, Roberto Perotti, and Fabio Schiantarelli. 2002. Fiscal policy, profits, and investment. American Economic Review 92: 571–89. [Google Scholar] [CrossRef]

- Allsopp, Christopher, and David Vines. 1996. Fiscal Policy and EMU. National Institute Economic Review 158: 91–107. [Google Scholar] [CrossRef]

- Amato, Massimo, Luca Fantacci, Dimitri B. Papadimitriou, and Gennaro Zezza. 2016. Going Forward from B to A? Proposals for the Eurozone Crisis. Economies 3: 18. [Google Scholar] [CrossRef]

- Annett, Antony M., Jorg Decressin, and Michael Deppler. 2005. Reforming the Stability and Growth Pact. IMF Policy Discussion Papers, February 1. [Google Scholar]

- Argy, Victor E., and Joanne Salop. 1979. Price and Output Effects of Monetary and Fiscal Policy under Flexible Exchange Rates. IMF Staff Papers 26: 224–56. [Google Scholar] [CrossRef]

- Aslett, Kevin, and James Caporaso. 2016. Breaking up Is Hard to Do: Why the Eurozone Will Survive. Economies 4: 21. [Google Scholar] [CrossRef]

- Bacchiocchi, Emanuele, Elisa Borghi, and Alessandro Missale. 2011. Public Investment under Fiscal Constraints. Fiscal Studies 32: 11–42. [Google Scholar] [CrossRef]

- Baerg, Nicole Rae, and Mark Hallerberg. 2016. Explaining Instability in the Stability and Growth Pact: The Contribution of Member State Power and Euroskepticism to the Euro Crisis. Comparative Political Studies 49: 98–1009. [Google Scholar] [CrossRef]

- Balassa, Bela. 1962. The Theory of Economic Integration, 1st ed. London: Routledge. [Google Scholar]

- Barro, Robert J. 1974. Are Government Bonds Net Wealth? Journal of Political Economy 82: 1095–117. [Google Scholar] [CrossRef]

- Beetsma, Roel M. W., and Xavier Debrun. 2004. Reconciling Stability and Growth: Smart Pacts and Structural Reforms. IMF Staff Papers 51: 431–56. [Google Scholar] [CrossRef][Green Version]

- Bénétrix, Agustin S., and Philip R. Lane. 2013. Fiscal cyclicality and EMU. Journal of International Money and Finance 34: 164–76. [Google Scholar] [CrossRef]

- Bofinger, Peter. 2003. Should the European Stability and Growth Pact be Changed? Intereconomics 38: 4–18. [Google Scholar] [CrossRef]

- Buchanan, James M. 1976. Barro on the Ricardian Equivalence Theorem. Journal of Political Economy 84: 337–42. [Google Scholar] [CrossRef]

- Buiter, Willem H. 1977. ‘Crowding out’ and the effectiveness of fiscal policy. Journal of Public Economics 7: 309–28. [Google Scholar] [CrossRef]

- Buti, Marco, Sylvester Eijffinger, and Daniele Franco. 2003. Revisiting EMU’s Stability Pact: A Pragmatic Way Forward. Oxford Review of Economic Policy 19: 100–11. [Google Scholar] [CrossRef][Green Version]

- Cooper, Russell, and Hubert Kempf. 2004. Overturning Mundell: Fiscal Policy in a Monetary Union. The Review of Economic Studies 71: 371–96. [Google Scholar] [CrossRef]

- de Grauwe, Paul. 2020. The Need for Monetary Financing of Corona Budget Deficits. Intereconomics 55: 133–34. [Google Scholar] [CrossRef]

- de Haan, Jakob, and Patrick Kosterink. 2017. Institutional reforms of EMU since the crisis: An assessment in view of recent DNB research. Journal for Comparative Government and European Policy 15: 70–83. [Google Scholar]

- Eichengreen, Barry. 1998. European monetary unification: A tour d’horizon. Oxford Review of Economic Policy 14: 24–40. [Google Scholar] [CrossRef]

- Eichengreen, Barry, and Jurgen von Hagen. 1996. Fiscal Policy and Monetary Union: Is There a Tradeoff between Federalism and Budgetary Restrictions? National Bureau of Economic Research. Working Paper 5517. Available online: https://www.nber.org/papers/w5517 (accessed on 9 December 2022).

- Enoch, Charles, Gilian Garcia, and V. Sundararajan. 2001. Recapitalizing Banks with Public Funds. IMF Staff Papers 48: 58–110. [Google Scholar]

- Enowbi Batuo, Michael, and Mlambo Kupukile. 2010. How can economic and political liberalisation improve financial development in African countries? Journal of Financial Economic Policy 2: 35–59. [Google Scholar] [CrossRef]

- Estella, Antonio. 2021. The ‘Muting’ of the Stability and Growth Pact. In Cambridge Yearbook of European Legal Studies. Cambridge: Cambridge University Press, pp. 1–18. [Google Scholar]

- Eurostat. 2022. Government Finance Statistics—General Government Deficit/Surplus. Available online: https://ec.europa.eu/eurostat/web/main/data/database (accessed on 8 December 2022).

- Fatás, Antonio. 1998. Does EMU need a fiscal federation? Economic Policy 13: 164–203. [Google Scholar] [CrossRef]

- Fischer, Stanley. 1988. Recent Developments in Macroeconomics. The Economic Journal 98: 294–339. [Google Scholar] [CrossRef][Green Version]

- Flammer, Caroline. 2019. Green Bonds: Effectiveness and Implications for Public Policy. Environmental and Energy Policy and the Economy 1: 95–128. [Google Scholar] [CrossRef]

- Friedman, Milton. 1948. A Monetary and Fiscal Framework for Economic Stability. The American Economic Review 38: 245–64. [Google Scholar]

- Furceri, Davide. 2007. Is Government Expenditure Volatility Harmful for Growth? A Cross-Country Analysis. Fiscal Studies 28: 103–20. [Google Scholar] [CrossRef]

- Goldbach, Roman, and Christian Fahrholz. 2011. The euro area’s common default risk: Evidence on the Commission’s impact on European fiscal affairs. European Union Politics 12: 507–28. [Google Scholar] [CrossRef]

- Hallerberg, Mark. 2011. Fiscal federalism reforms in the European Union and the Greek crisis. European Union Politics 12: 127–42. [Google Scholar] [CrossRef]

- Hauptmeier, Sebastian, and Nadine Leiner-Killinger. 2020. Reflections on the Stability and Growth Pact’s Preventive Arm in Light of the COVID-19 Crisis. Intereconomics 55: 296–300. [Google Scholar] [CrossRef]

- Herzog, Bodo. 2016. Modelling Monetary and Fiscal Governance in the Wake of the Sovereign Debt Crisis in Europe. Economies 4: 9. [Google Scholar] [CrossRef]

- Hauptmeier, Sebastian, A. Jesus Sanchez-Fuentes, and Ludger Schuknecht. 2011. Towards expenditure rules and fiscal sanity in the euro area. Journal of Policy Modeling 33: 597–617. [Google Scholar] [CrossRef]

- Hicks, John Richard. 1939. The Foundations of Welfare Economics. The Economic Journal 49: 696–712. [Google Scholar] [CrossRef]

- Howarth, David, and Lucia Quaglia. 2016. The Political Economy of European Banking Union. Oxford: Oxford University Press. [Google Scholar]

- Kammer, Alfred, and Nathaniel Arnold. 2021. Europe’s COVID-19 Crisis Response: A Race Well Run, But Not Yet Won. Intereconomics 56: 194–96. [Google Scholar] [CrossRef] [PubMed]

- Karagounis, Konstantinos, Dimitrios Syrrakos, and John Simister. 2015. The Stability and Growth Pact, and Balanced Budget Fiscal Stimulus: Evidence from Germany and Italy. Intereconomics 50: 32–39. [Google Scholar] [CrossRef][Green Version]

- Kenen, Peter B. 1981. The Theory of Optimum Currency Areas: An Eclectic View. In Essays in International Economics. Princeton: Princeton University Press. [Google Scholar]

- Keynes, John Maynard. 1939. Official Papers. The Economic Journal 49: 558–77. [Google Scholar] [CrossRef]

- Lane, Philip R. 2012. The European Sovereign Debt Crisis. Journal of Economic Perspectives 26: 49–68. [Google Scholar] [CrossRef]

- Lastauskas, Povilas. 2019. Heterogeneity and Convergence in EU28: 25 Years After Maastricht. The Decade of Catching-Up: The Case of the EU and Asia. Conference Logbook on the Sixth Conference of the Magyar Nemzeti Bank’s Lamfalussy Lectures Conference Series, Magyar Nemzeti Bank, Hungary, 4 February 2019. Featured in Ferenc Tóth, Report on the 2019 Lámfalussy Lectures Conference. Financial and Economic Review 18: 155–62. [Google Scholar]

- Liargovas, Panagiotis, Marios Psychalis, and Nikolaos Apostolopoulos. 2022. Fiscal policy, growth and entrepreneurship in the EMU. European Politics and Society 23: 468–89. [Google Scholar] [CrossRef]

- Mackiewicz, Michal. 2007. Making the Stability Pact More Flexible: Does It Lead to Pro-Cyclical Fiscal Policies? Fiscal Studies 28: 251–68. [Google Scholar] [CrossRef]

- Maris, Georgios, Pantelis Sklias, and Napoleon Maravegias. 2022. The political economy of the Greek economic crisis in 2020. European Politics and Society 23: 447–67. [Google Scholar] [CrossRef]

- Matthijs, Matthias, and Mark Blyth. 2017. When Is It Rational to Learn the Wrong Lessons? Technocratic Authority, Social Learning, and Euro Fragility. Perspectives on Politics 16: 110–26. [Google Scholar] [CrossRef]

- Mendelson, Morris. 1972. The Eurobond and Capital Market Integration. The Journal of Finance 27: 110–26. [Google Scholar]

- Menguy, Severine. 2010. How to Limit the Moral Hazard Related to a European Stabilization Mechanism. Journal of Economic Integration 25: 252–75. [Google Scholar] [CrossRef][Green Version]

- Mian, Atif, Ludwig Straub, and Amir Sufi. 2021. A goldilocks theory of fiscal policy. National Bureau of Economic Research. Working Paper 29351. Available online: https://www.tcd.ie/Economics/assets/pdf/Seminars/20212022/goldilocks-theory-of-fiscal-policyLudwigStraub17Nov21.pdf (accessed on 9 December 2022).

- Minea, Alexandru, and Patrick Villieu. 2009. Borrowing to Finance Public Investment? The ‘Golden Rule of Public Finance’ Reconsidered in an Endogenous Growth Setting. Fiscal Studies 30: 103–33. [Google Scholar] [CrossRef]

- Mosley, Layna. 2004. Government–financial market relations after EMU: New currency, new constraints? European Union Politics 5: 181–209. [Google Scholar] [CrossRef]

- Mundell, Robert A. 1961. A Theory of Optimum Currency Areas. The American Economic Review 51: 657–65. [Google Scholar]

- Okun, Arthur M. 1972. Fiscal-Monetary Activism: Some Analytical Issues. Brookings Papers on Economic Activity 3: 123–72. [Google Scholar] [CrossRef][Green Version]

- Pagoulatos, George. 2020. EMU and the Greek crisis: Testing the extreme limits of an asymmetric union. Journal of European Integration 42: 363–79. [Google Scholar] [CrossRef]

- Persson, Torsten, and Guido Tabellini. 1996. Federal Fiscal Constitutions: Risk Sharing and Moral Hazard. Econometrica 64: 623–46. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., and Donggyu Sul. 2007. Transition modeling and econometric convergence tests. Econometrica 75: 1771–855. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., and Donggyu Sul. 2009. Economic transition and growth. Journal of Applied Econometrics 24: 1153–85. [Google Scholar] [CrossRef]

- Posen, Adam S. 2021. Fiscal Success During COVID-19 Says Believe the Good News. Intereconomics 56: 190–3. [Google Scholar] [CrossRef] [PubMed]

- Prinz, Aloys, and Hanno Beck. 2012. Fighting Debt Explosion in the European Sovereign Debt Crisis. Intereconomics 47: 185–9. [Google Scholar] [CrossRef][Green Version]

- Savage, James D. 2001. Budgetary Collective Action Problems: Convergence and Compliance under the Maastricht Treaty on European Union. Public Administration Review 61: 43–53. [Google Scholar] [CrossRef]

- Savage, James D., and Amy Verdun. 2007. Reforming Europe’s stability and growth pact: Lessons from the American experience in macrobudgeting. Review of International Political Economy 14: 842–67. [Google Scholar] [CrossRef]

- Schuknecht, Ludger, Philippe Moutot, Philipp Rother, and Jurgen Stark. 2011. The Stability and Growth Pact-Crisis and Reform. Frankfurt: European Central Bank. [Google Scholar]

- Scitovsky, Tibor. 1951. The State of Welfare Economics. The American Economic Review 41: 303–15. [Google Scholar]

- Sigl-Glöckner, Philippa, Max Krahé, Florian Kern, and Florian Schuster. 2022. A proposal for reforming the Stability and Growth Pact. Available online: https://www.dezernatzukunft.org/wp-content/uploads/2022/06/Sigl-Gloeckner-et-al.-2022-A-proposal-for-reforming-the-Stability-and-Growth-pact.pdf (accessed on 8 December 2022).

- Thygesen, Niels, Roel Beetsma, Massimo Bordigton, Xavier Debrun, and Mateusz Szczurek. 2020. Annual Report 2020. Bruseless: European Fiscal Board. [Google Scholar]

- Tsiddon, Daniel. 1992. A Moral Hazard Trap to Growth. International Economic Review 33: 299–31. [Google Scholar] [CrossRef]

- von Hagen, Jurgen, Andrew Hughes Hallett, and Rolf Strauch. 2001. Budgetary Consolidation in EMU. London: CEPR. [Google Scholar]

- Wang, Guizhou, and Kjell Hausken. 2021. Conventionalists, Pioneers and Criminals Choosing between a National Currency and a Global Currency. Journal of Banking and Financial Economics 2: 104–33. [Google Scholar] [CrossRef]

- Williamson, Stephen. 2022. Central bank digital currency: Welfare and policy implications. Journal of Political Economy 130: 2829–61. [Google Scholar] [CrossRef]

- Wyplosz, Charles. 2013. Fiscal Rules: Theoretical Issues and Historical Experiences. In Fiscal Policy after the Financial Crisis. Chicago: University of Chicago Press. [Google Scholar]

{kind=link}

| Years | Obs. | Mean | Std. Dev. | Min | Max | |

|---|---|---|---|---|---|---|

| Full Sample | 1995–2021 | 702 | −2.75 | 3.52 | −32.1 | 6.9 |

| Pre-Financial Crisis | 1995–2008 | 364 | −2.30 | 3.24 | −12.6 | 6.9 |

| Post-Financial Crisis | 2009–2021 | 338 | −3.22 | 3.76 | −32.1 | 4.1 |

| Obs. | Mean | Std. Dev. | Min | Max | |

|---|---|---|---|---|---|

| Austria | 27 | −2.71 | 2.01 | −8 | 0.6 |

| Belgium | 27 | −2.41 | 2.22 | −9 | 0.2 |

| Croatia | 27 | −2.91 | 2.70 | −7.9 | 2 |

| Cyprus | 27 | −2.89 | 2.85 | −8.8 | 3.2 |

| Czechia | 27 | −3.23 | 2.94 | −12.4 | 1.5 |

| Denmark | 27 | 0.48 | 2.57 | −3.6 | 5 |

| Estonia | 27 | −0.08 | 1.91 | −5.6 | 2.9 |

| Finland | 27 | 0.04 | 3.40 | −5.9 | 6.9 |

| France | 27 | −3.90 | 1.82 | −8.9 | −1.3 |

| Germany | 27 | −1.83 | 2.53 | −9.4 | 1.9 |

| Greece | 27 | −6.70 | 4.11 | −15.1 | 1.1 |

| Hungary | 27 | −4.96 | 2.37 | −9.3 | −1.8 |

| Ireland | 27 | −2.90 | 7.47 | −32.1 | 4.9 |

| Italy | 27 | −3.63 | 1.94 | −9.6 | −1.3 |

| Latvia | 27 | −2.29 | 2.65 | −9.5 | 1.4 |

| Lithuania | 27 | −2.83 | 3.25 | −11.8 | 0.5 |

| Luxembourg | 27 | 1.67 | 1.97 | −3.4 | 5.6 |

| Malta | 27 | −3.78 | 3.42 | −9.5 | 3.3 |

| Netherlands | 27 | −1.77 | 2.43 | −8.7 | 1.7 |

| Poland | 27 | −3.88 | 1.83 | −7.4 | −0.2 |

| Portugal | 27 | −4.70 | 2.53 | −11.4 | 0.1 |

| Romania | 27 | −3.66 | 2.34 | −9.3 | −0.6 |

| Slovakia | 27 | −4.71 | 2.89 | −12.6 | −1 |

| Slovenia | 27 | −3.50 | 3.27 | −14.6 | 0.7 |

| Spain | 27 | −4.21 | 4.04 | −11.6 | 2.1 |

| Sweden | 27 | −0.13 | 2.12 | −7 | 3.3 |

| Countries | Panel A: Phillips and Sul (2007) | Panel B: Phillips and Sul (2009) | ||||

|---|---|---|---|---|---|---|

| Coefficient | t-Stat | New Club | Final Club | Coefficient | t-Stat | |

| Full sample | −3.1477 | −16.3322 | ||||

| Club 1 (Austria, Belgium, Cyprus, Denmark, Finland, Netherlands, Slovenia, Spain, Sweden) | −3.091 | −0.595 | 1 + 2 | Club 1 (Austria, Belgium, Cyprus, Denmark, Finland, Netherlands, Slovenia, Spain, Sweden, Estonia, Lithuania, Luxembourg) | −1.08 | −0.557 |

| Club 2 (Estonia, Lithuania, Luxembourg) | 7.636 | 13.171 | 3 + 4 + 5 | Club 2 (Czechia, Germany, Ireland, Latvia, France, Italy, Romania, Slovakia, Croatia, Malta, Poland, Portugal) | 0.029 | 0.341 |

| Club 3 (Czechia, Germany, Ireland, Latvia]) | 1.419 | 4.605 | Nonconverging (Greece, Hungary) | −2.683 | −8.717 | |

| Club 4 (France, Italy, Romania, Slovakia] | 2.872 | 4.747 | ||||

| Club 5 (Croatia, Malta, Poland, Portugal) | 3.047 | 4.698 | ||||

| Nonconverging (Greece, Hungary) | −2.683 | −8.717 | ||||

| Countries | Phillips and Sul (2007) | |

|---|---|---|

| Coefficient | t-Stat | |

| Full sample | −1.8475 | −7.168 |

| Club 1 (Denmark, Ireland, Luxembourg) | 1.037 | 0.523 |

| Club 2 (Germany, Lithuania, Sweden) | 0.103 | 0.179 |

| Club 3 (Austria, Belgium, Croatia, Cyprus, Czechia, Estonia, Finland, Greece, Latvia, Malta, Poland, Portugal, Slovakia, Slovenia) | 0.404 | 0.941 |

| Club 4 (France, Hungary, Italy, Romania, Spain) | 3.648 | 5.67 |

| Nonconverging (Netherlands) | - | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Patsoulis, P.; Psychalis, M.; Deirmentzoglou, G.A. Stability and Growth Pact: Too Young to Die, Too Old to Rock ‘n’ Roll. J. Risk Financial Manag. 2022, 15, 608. https://doi.org/10.3390/jrfm15120608

Patsoulis P, Psychalis M, Deirmentzoglou GA. Stability and Growth Pact: Too Young to Die, Too Old to Rock ‘n’ Roll. Journal of Risk and Financial Management. 2022; 15(12):608. https://doi.org/10.3390/jrfm15120608

Chicago/Turabian StylePatsoulis, Patroklos, Marios Psychalis, and Georgios A. Deirmentzoglou. 2022. "Stability and Growth Pact: Too Young to Die, Too Old to Rock ‘n’ Roll" Journal of Risk and Financial Management 15, no. 12: 608. https://doi.org/10.3390/jrfm15120608

APA StylePatsoulis, P., Psychalis, M., & Deirmentzoglou, G. A. (2022). Stability and Growth Pact: Too Young to Die, Too Old to Rock ‘n’ Roll. Journal of Risk and Financial Management, 15(12), 608. https://doi.org/10.3390/jrfm15120608